1. Introduction

The scope of China’s participation in global trade has expanded rapidly in recent years. A competitive environment has gradually generated in the agricultural product market due to the close link between domestic and international markets. As crude oil is a primary source of energy for agricultural production, its price changes will inevitably cause variations in agricultural commodities on international markets. In terms of the futures market, a large number of investors and speculators have been attracted to participate in crude oil futures trading ever since such derivatives were launched by the futures exchange. These active transactions may bring about great uncertainties and dramatic price swings not only to the crude oil market but also to other commodity markets. In addition, with the spread of the global food crisis, the agricultural market will, in turn, affect other commodity markets. As the world’s largest importer of crude oil and agricultural products, it is essential to figure out the causal relationship and dynamic interaction characteristics between the crude oil futures market and China’s agricultural product futures market. The outcomes of the study are expected to provide reference information for avoiding a global systemic food crisis.

Theoretically, international crude oil prices can affect China’s agricultural product prices in three major ways: (1) agricultural trade. Associated with international agricultural product prices, China’s agricultural products usually respond consistently to international standards. It is well-known that the rise of international crude oil can cause international agricultural product prices to change in the same direction. Such a shift drives up the domestic price levels due to higher import costs. (2) The production cost of agricultural products. As a net importer of crude oil, China’s oil price will rise when the international crude oil price goes up. Higher oil price brings extra costs to production, processing, and transportation. Correspondingly, suppliers will increase the price of agricultural products in order to keep their own profits. (3) Biofuel development. The Chinese government attaches primary importance to the growing climate problem and has encouraged the development of a green economy over the years. Biofuels produced from agricultural raw materials are gradually replacing oil and being supplied in various fields with their own advantages, such as recyclability and environmental protection. Once the crude oil price rises substantially, China will reduce the demand for oil and turn to biofuels instead. As a result, the increased consumption of raw materials such as soybean meal and corn will promote agricultural prices to rise, especially in cases when demand exceeds supply.

It is therefore critical to find out the impact of the crude oil price changes on agricultural product markets. The objective of this paper is to explore the internal mechanism of volatility in the agricultural futures market and crude oil futures market so that the latter can be monitored to improve the early warning mechanism for oil prices. The major contributions are as follows: First, our research takes both the Granger causality of returns and the spillover effect of volatilities into consideration, while most previous studies focus only on the relationship of different return series. Second, the sample size covers almost 20 years and reveals the dynamics of causality and spillover during stable and volatile periods, so that risk managers and investors can predict returns and volatilities of one market based on the other market. Third, we find that the current decrease in the net spillover of crude oil futures to agricultural futures is mainly attributed to the promotion of biofuel energy. These findings will play a supportive role in enabling the macro-department of the Chinese government to formulate relevant policies that contribute to controlling risks and stabilizing the agricultural product market.

The remainder of this paper is organized as follows.

Section 2 presents the relevant previous literature.

Section 3 introduces the methodology. Data and empirical results are analyzed in

Section 4 and

Section 5, respectively.

Section 6 concludes the paper.

2. Literature Review

Previous works use different models for various financial assets and time scales to investigate the futures price relationship between crude oil and agricultural products. With the continuous improvement in econometrical methods, research on the aspects of the Granger causality test and risk-spillover effects has become increasingly in-depth.

It has been reported in many empirical studies that the international crude oil price has a significant impact on the prices of agricultural products. Further research even found mutual influence between the two. Specifically, by using the panel VAR and the Granger causality test to examine the relationship between crude oil prices and agricultural prices, a study documented a bidirectional causal relationship between the two [

1]. Meanwhile, such a relationship was also pointed out by some scholars, where the long-term correlation and causal relationship were tested by Granger causality analysis [

2]. By applying the ARDL method combined with Granger causality to examine the dynamic relationship among crude oil, biofuels, and agricultural prices, the results showed that there is a strong dependence in both long and short terms [

3]. By adopting the panel method and cointegration test to analyze the dynamic relationship between crude oil and agricultural products during 2006–2015, the study showed that the rise of oil prices could correspondingly push agricultural prices higher [

4]. Linear and Non-linear Autoregressive Distributed Lag (ARDL) Models are often used by scholars to investigate the impact of oil price shocks on agricultural prices, and a large number of research results suggest that agricultural products and crude oil are co-moving in the long run [

5,

6,

7]. By applying the Panel-VAR model to energy prices and food prices during the years 2000–2016, the results of the impulse response function demonstrated a positive response to any shock to oil prices [

8]. Some references considered using the time-varying rolling window technique to explore the causal relationship in prices between oil and agricultural products. The research showed the existence of a time-varying positive bidirectional causal relationship in a certain period of time [

9].

On the other hand, some scholars hold the opposite view that there is no correlation with respect to prices between international crude oil and agricultural products. The Copula model was employed to study the co-movement of prices in crude oil and several typical agricultural products (corn, soybeans, and wheat), where no extreme market dependence was found between crude oil and agricultural product prices, indicating that the impact of agricultural product markets on crude oil was neutral [

10]. A SVAR, along with a direct cyclic graph, was employed to decompose how supply/demand structural shocks affect food and fuel markets. Empirical results supported the hypothesis that fundamental market forces of demand and supply are the main drivers of food price volatility, while the shocks from oil, gasoline, and ethanol markets did not spill over into grain prices in the long run [

11]. The study argued that the price of agricultural products in South Africa is neutral to the fluctuation of oil price based on the results of the structural mutation cointegration test and nonlinear causality test [

12].

The existence of spillover effects will help investors, risk managers, manufacturers, and policymakers to capture the demand for commodity futures prices dynamically [

13,

14]. Since the outbreak of the 2008 global financial crisis, various sorts of data and econometric models have been selected to investigate the spillover effects between crude oil and agricultural products. For instance, by using the causal variance test and impulse response function to examine the volatility transmission between oil and agricultural prices from 1986 to 2011, research found that despite there being no volatility spillover before the financial crisis, oil volatility transmitted to agricultural products was detected after the financial crisis [

15]. Three different GARCH models were employed to catch the correlation between crude oil and energy crops by some scholars. Results from such dynamic models exhibit a strong correlation of about 20 percent in regard to daily returns. Furthermore, they further used the frequency-dependent spillovers measure to explore return spillovers from crude oil to ethanol, corn, soybean, and wheat and showed return spillover is stronger only during periods of energy and food crisis [

16,

17]. A multifractal detrended cross-correlation analysis approach was utilized to analyze the cross-correlations between the Brent crude oil and agricultural futures. The experimental results indicated that the multifractal cross-correlation was stronger under the influence of the COVID-19 pandemic [

18]. A relational measurement based on Markov-switching GRG copula was constructed to analyze the dependence structure between futures prices of WTI crude oil and 12 kinds of Chinese agricultural commodities. The degree of correlation with crude oil futures prices varies under different agricultural commodity futures prices [

19]. Some scholars examined the nature and dynamics of volatility spillovers during the period of the 2008–2009 financial crisis via the bivariate heterogeneous autoregressive model, from which bidirectional spillovers were observed between crude oil and agricultural commodity markets [

20].

Along with the improvement in related models and methods, Diebold and Yilmaz proposed a DY spillover index in 2009 to measure the spillover effect of return and volatility spillovers. Such an index was based on the forecast-error variance decompositions and was improved later by them with a generalized variance decompositions framework to avoid the sequence-dependence problem in 2012. By using this approach in the US stock, bond, foreign exchange, and commodity markets, they concluded that with the deepening of the financial crisis, volatility spillover effects also increased subsequently. Moreover, they proposed several connectedness measures and focused on the average and daily time-varying connectedness of major US financial institutions’ stock return volatilities in recent years, including during the financial crisis of 2007–2008 [

21,

22,

23]. Some scholars used the spillover index method to describe the relationship between the volatility of corn and energy prices in 2018 [

24]. By combining a multivariate heteroscedastic autoregressive (HAR) model with the DCC-GARCH model to analyze the connectedness characteristics between US crude oil futures and China’s agricultural commodity futures, the results verified the existence of leverage volatility transmission across markets [

25].

Spillover effects include the mean spillover effect and the volatility spillover effect. The former refers to the impact of a specific commodity price change on the price level of other commodities, while the latter represents the impact of volatility for one certain commodity on other commodities [

26]. A number of studies on the spillover effect between crude oil and agricultural commodities started with these two perspectives. Against this background, a fractionally integrated VAR model was employed to capture the long-memory behavior of the implied volatilities alongside the Markov Switching Autoregressive model to extract the regimes of crude oil. Evidence showed that the net volatility spillover effect from crude oil to all agricultural commodities tends to decrease when crude oil remains in its low-volatility regime. Conversely, this effect experienced an increasing trend when crude oil remained in its relatively high-volatility regime [

27]. An analysis of the spillover effect and time-frequency connectedness between crude oil prices and agricultural commodity markets was conducted by some scholars. Via the DY spillover index and the wavelet coherence model, a more apparent mean spillover was revealed during the COVID-19 pandemic [

28]. Some references examined spillover effects by employing the DY spillover index to returns and volatilities. The findings indicated an asymmetric and bidirectional flow of information among crude oil and agricultural commodities that intensifies during periods of financial and economic turmoil [

29].

It is important to research the relationship between energy and agricultural commodity markets, especially for investors’ portfolio optimization, risk management, and asset allocation. Despite the fact that many existing studies have explored such an issue, their conclusions are not consistent with each other. Methodologically, VAR, MGARCH, and Copula are frequently used in the current literature to analyze volatility spillover. These models, however, failed to provide information with respect to the direction of volatility spillover, which therefore may lead to opaque dynamic spillover effects. To cope with these problems, this paper applies the time-varying Granger model and the DY spillover index model to examine the dynamic Granger causality that exists in crude oil and agricultural futures and identify the direction of volatility spillover of the investigated markets.

3. Methodology

3.1. Time-Varying Granger Causality Tests

The fundamental idea of the Granger causality test is to determine whether one sequence is useful in terms of forecasting another sequence. That is, if the prior values have an explanatory ability to predict the future values of another time series, there should be a causal link between the two variables. The Granger causality test is directly related by sample period so that data in different time spans may result in different conclusions; we therefore alternatively use the time-varying Granger causality test to test the causal relationship between crude oil and agricultural futures markets.

A brief introduction to the Granger causality framework is as follows. We can consider a VAR(

m) model including two variables:

where

and

stand for two different time series. Variable

is referred to as the Granger cause of a variable

if the current value of

can be predicted by the historical values of

. The Wald test is used for testing the joint significance of parameters

, whose null hypothesis is no Granger causality between

and

. The matrix structure for

can be expressed as

where

,

,

, and

,

,

. The null hypothesis of the Granger causality test for variables

and

is

, where

is the coefficient restriction matrix, and

is the row-vectorized

.

The Wald statistic modified for heteroscedasticity

is defined as

where

,

,

, and

,

.

3.2. Spillover Index Frameworks

Diebold and Yilmaz (2009) proposed the DY spillover index, which is based on the decomposition of the forecast-error variance of the VAR model, to measure the spillover effect for different variables. Such an approach was improved later in Diebold and Yilmaz (2012) using a generalized variance decompositions framework in which forecast-error variance decompositions are invariant to the variable ordering. This paper implements the advanced index for measuring the spillover effect over crude oil and agricultural futures.

The

model, including

variables, takes the form of

Random variables are assumed to be independent and identically distributed, i.e.,

. Through a moving average, Equation (5) can be rewritten as given below.

where

denotes the

identity matrix and satisfies the following expression.

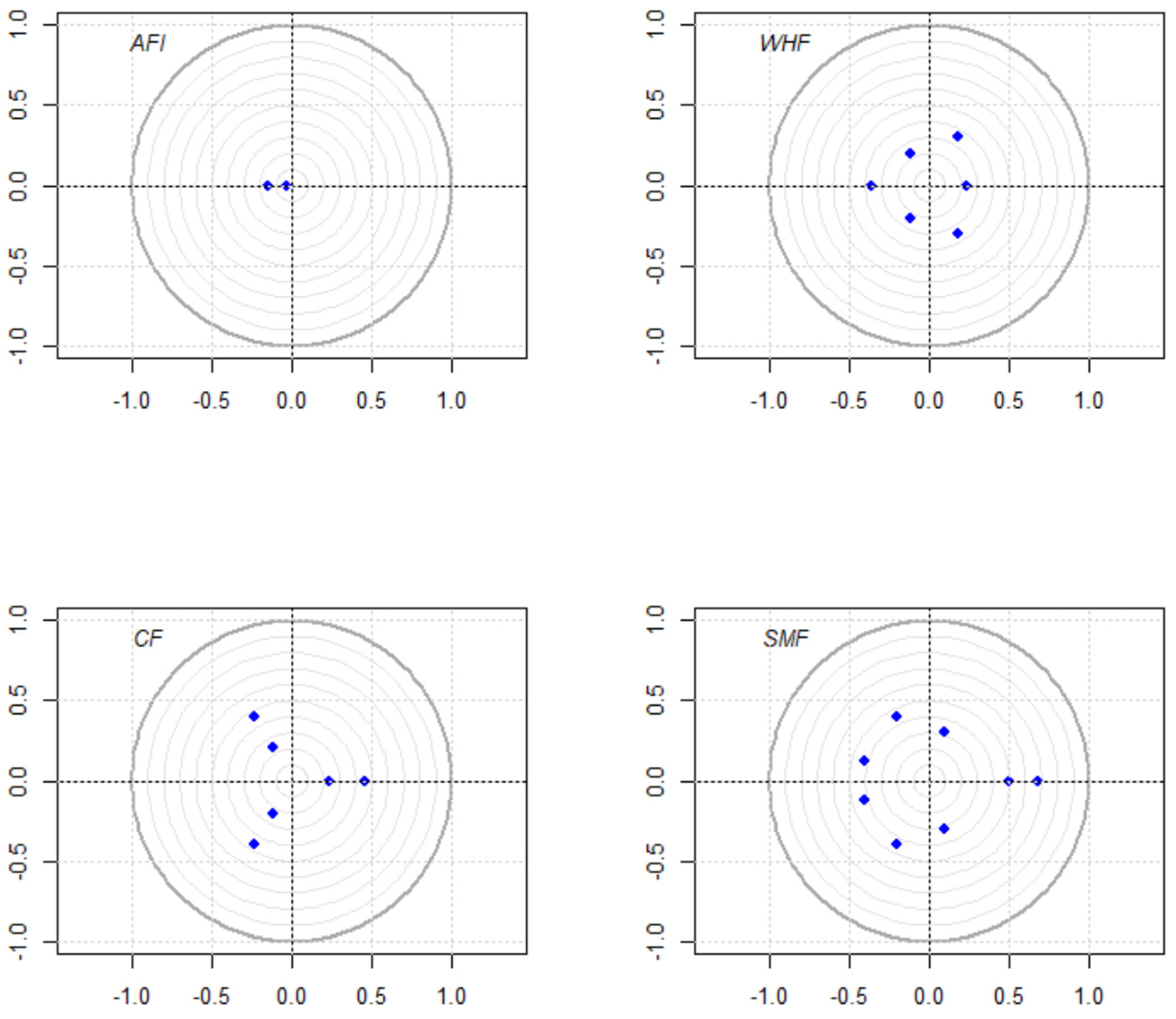

Particularly, if . This moving average coefficient is the key to the VAR model. Variance decomposition attributes the forecast-error variance decomposition of the respective variables to the shocks of other variables within a specific system. Variance decomposition requires orthogonalized information. The information in the VAR model, however, is contemporaneously correlated. Although Cholesky decomposition can realize orthogonalization, the result of variance decomposition depends on variable ordering. For this purpose, a generalized VAR model is constructed to cope with the ordering problem. The DY dynamic spillover index is based on the generalized variance decomposition. By calculating the variance component, it is possible to obtain the total spillover, the directional spillover, the net spillover, and the net pairwise spillover, respectively.

The variance component is defined as the score of the -period forecast-error variance with respect to the shock of variable to itself, while the covariance component or spillover represents the score of the -period forecast-error variance with respect to the shock of variable to variable , where and .

Let

be the

-period forecast-error variance decomposition obtained from the KPPS method under the generalized VAR framework. For

,

is calculated by

where

is the variance–covariance matrix of the error vector

,

is the standard deviation of the error term

, and

is a vector whose

-th element is 1 and the remaining elements are 0. Then, normalizing the variance decomposition matrix by row so that they sum to unity:

Accordingly, and .

Therefore, the total volatility spillover index used to measure the contribution of spillovers from all market shocks to the total forecast-error variance in a generalized VAR can be constructed as follows, given the variance contribution rate computed by KPPS variance decomposition.

In view that the generalized impulse response and variance decomposition are invariant to variable ordering, we use the elements of the normalized generalized variance decomposition matrix to calculate the directional spillover effect. In a measurement system, Equation (11) describes the directional spillover received by variable

from all other variables

.

Similarly, the directional spillover transmitted from variable

to all other variables

can be expressed as

Thus, a set of directional spillovers can be recognized as spillovers with specific sources decomposed from the total spillover.

In addition, the net volatility spillover effect from variable

to the other

variables identifies whether

is a source or recipient of spillovers.

The net volatility spillover provides aggregated information with respect to the net contribution of a specific variable to the other variables. The net pairwise volatility spillover effect between variables

and

measures the difference between the total volatility shock transmitted from variables

to

and variables

to

.

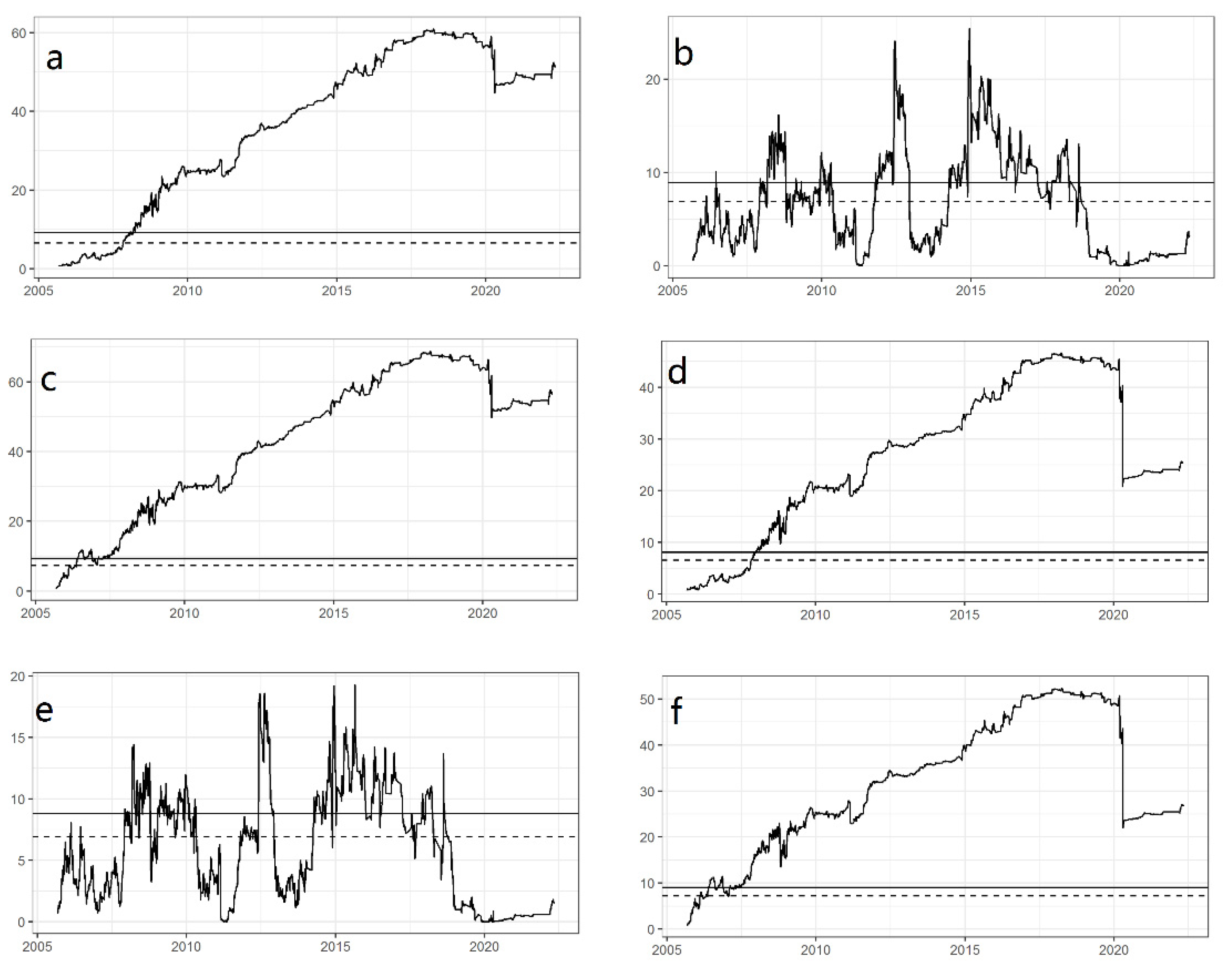

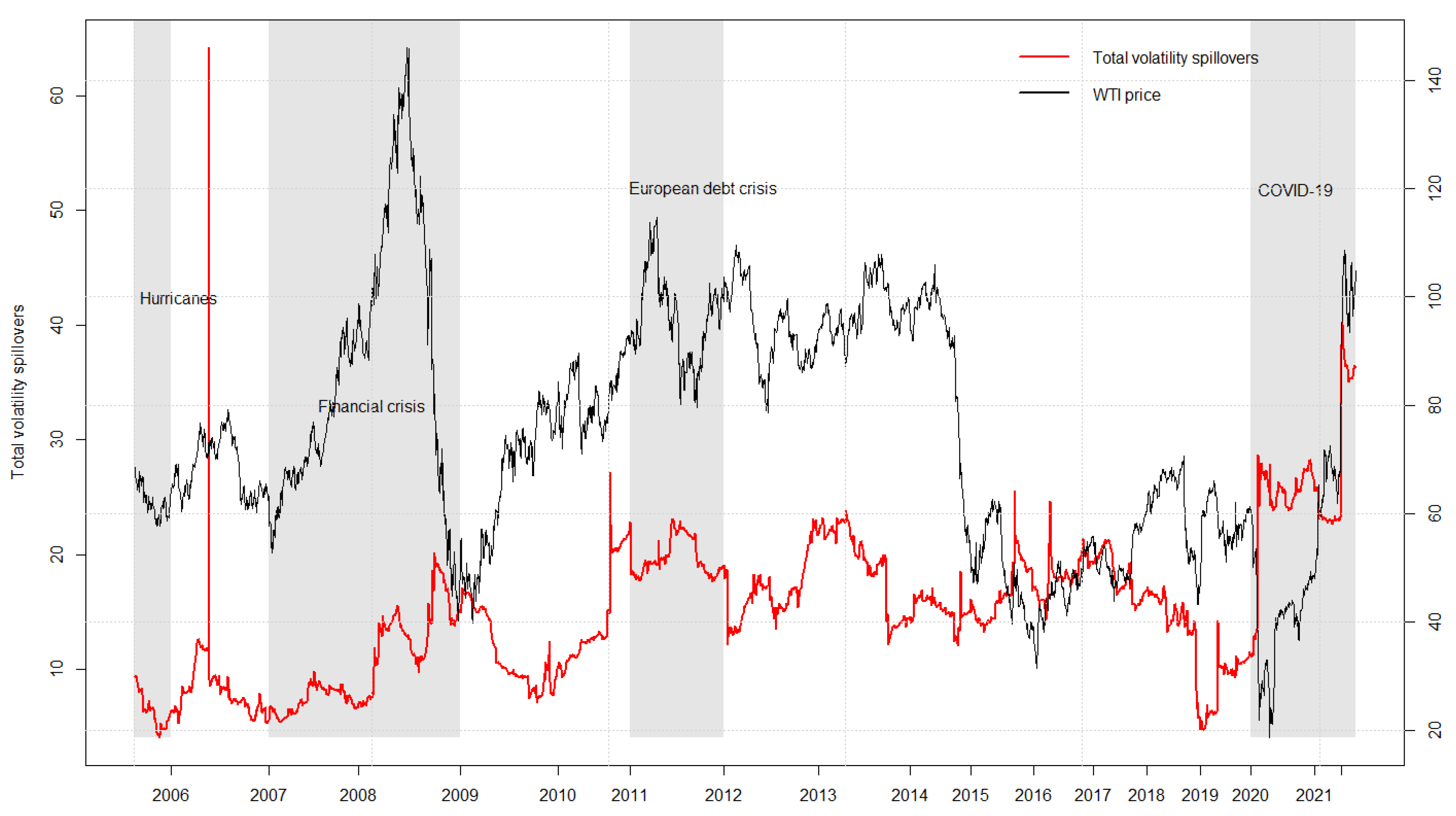

6. Conclusions

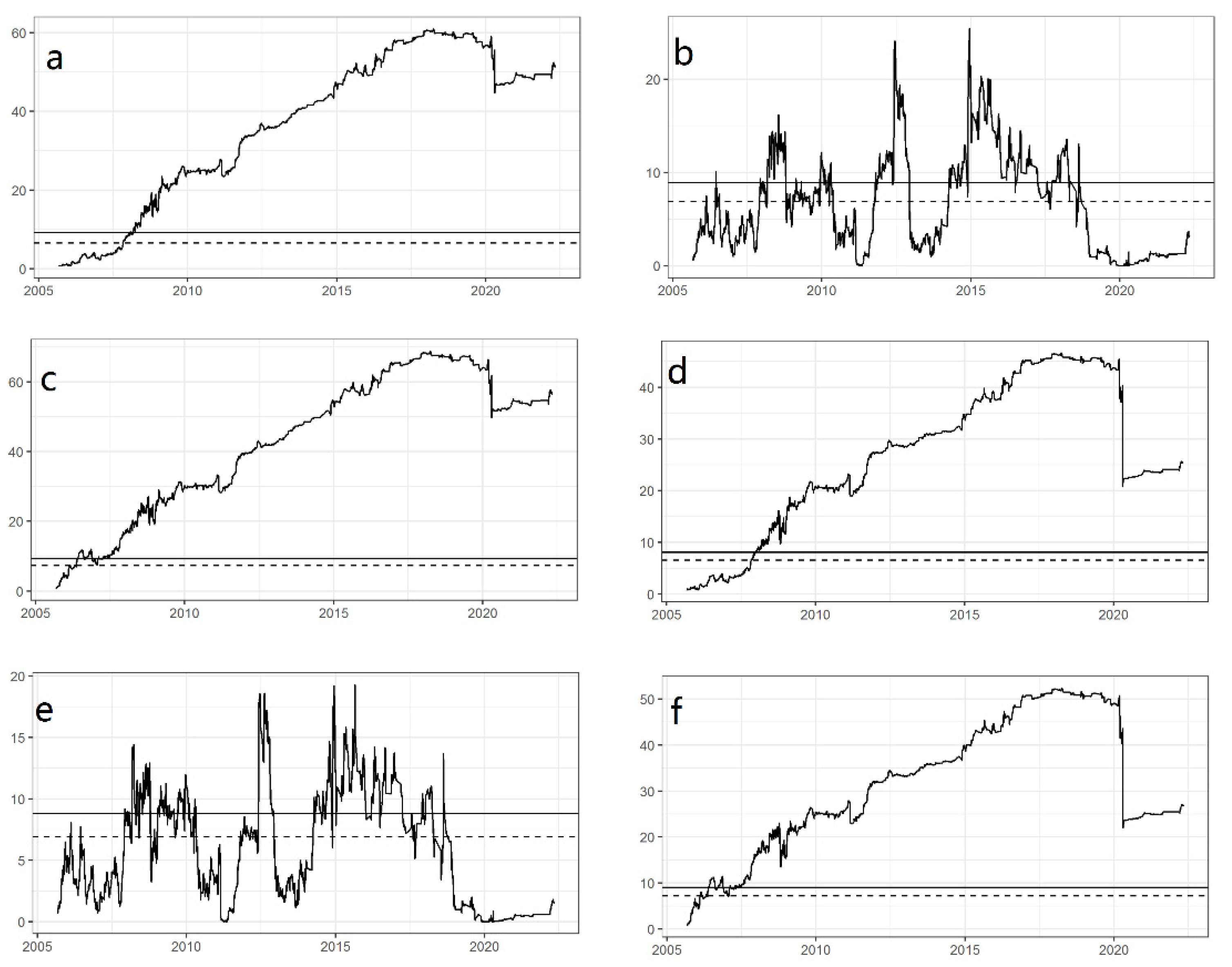

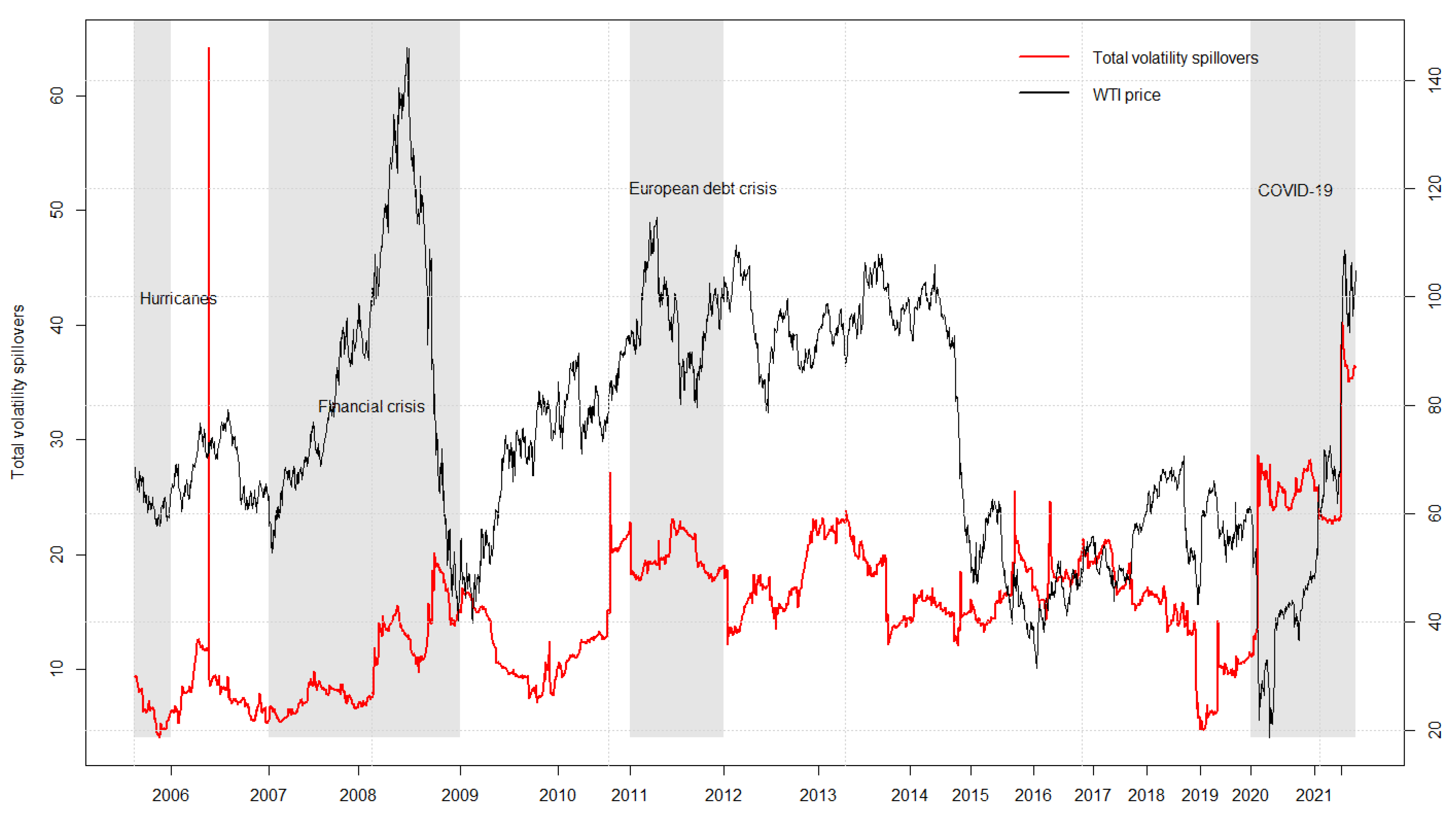

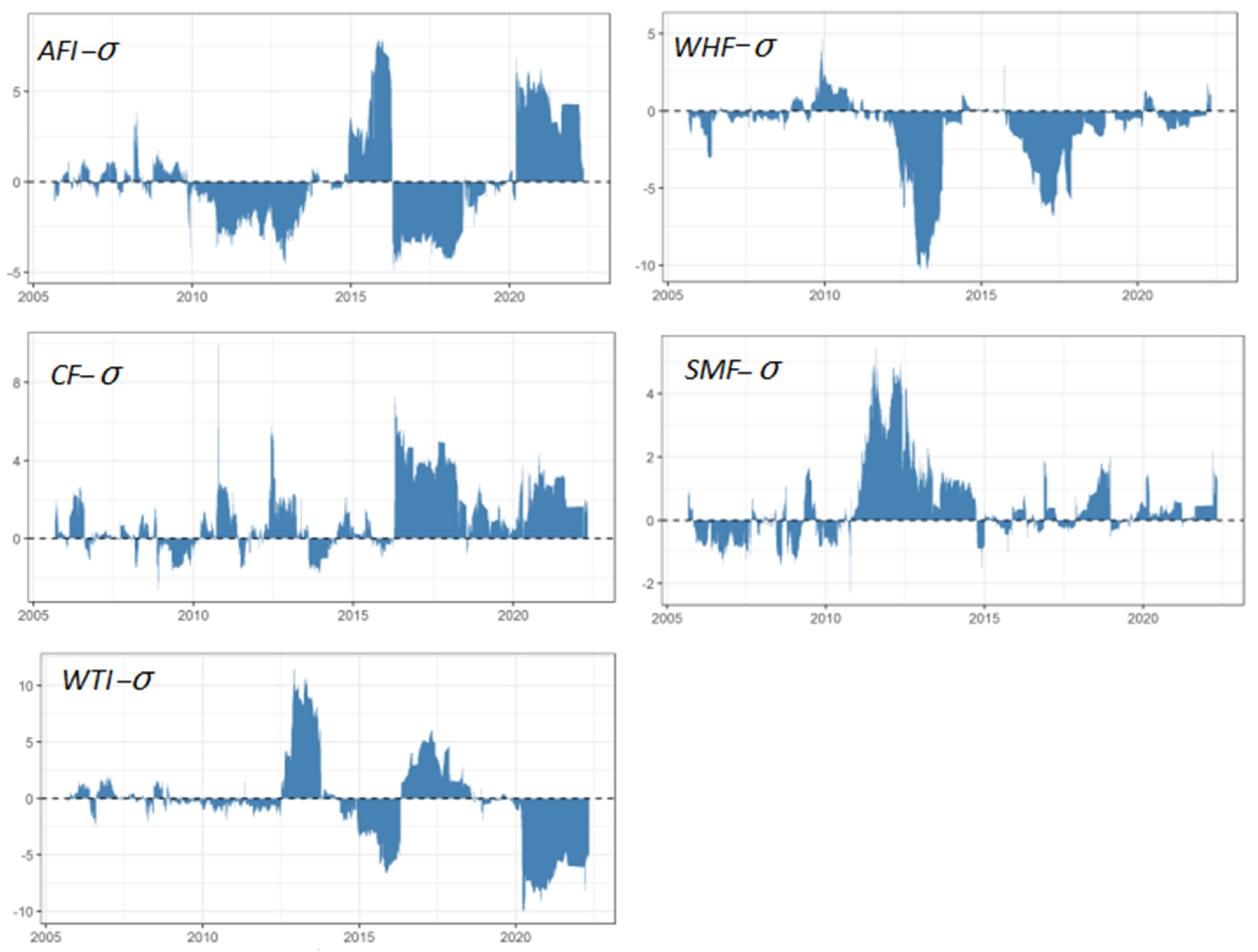

This paper examines the time-varying Granger causality and the spillover effects between crude oil futures and four sequences related to China’s agricultural futures, including the agricultural futures index, wheat hard futures, cotton futures, and soybean meal futures. Empirical evidence shows that crude oil futures are the time-varying Granger-cause of China’s agricultural futures during turbulent times such as financial crises, wars, and natural disasters. Moreover, the dynamics of volatility spillovers reveal the direction and degree of transmission during financial crises and economic turbulence over time.

Our empirical results are as follows. First, the linear Granger causality test results indicate that the Granger causality between international crude oil and soybean meal futures is bidirectional, whilst the others are unidirectional. In comparison, the time-varying Granger causality test shows significant results only when encountering special situations, such as major economic events and extreme natural disasters, and is also supported by a robust test under heteroskedasticity conditions. Second, the existence of bidirectional volatility spillovers in crude oil and agricultural futures is verified by the results of the DY spillover index. Such spillovers were exacerbated when the market or the international economic environment was undergoing a dramatic change.

The results of this research are expected to provide useful suggestions for many economic agents, such as international investors, speculators, and policymakers. With a comprehensive understanding of dynamic spillovers, investors can establish more effective risk-hedging models for the commodity futures markets, while policymakers can formulate appropriate policies to deal with financial risks and improve early warning capabilities. As mentioned above, the time-varying Granger causality test and dynamic spillover effects are highly dependent on the selected sample interval. An examination of the connectedness network and risk spillovers between crude oil and Chinese agricultural futures under short and long terms awaits future research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}