Assessment of the Mandatory Non-Financial Reporting of Romanian Companies in the Circular Economy Context

Abstract

:1. Introduction

2. Literature Review

2.1. Circular Economy and Corporate Social Responsibility

2.2. CSR and Non-Financial Reporting

2.3. Non-Financial Reporting in Romania

3. Materials and Methods

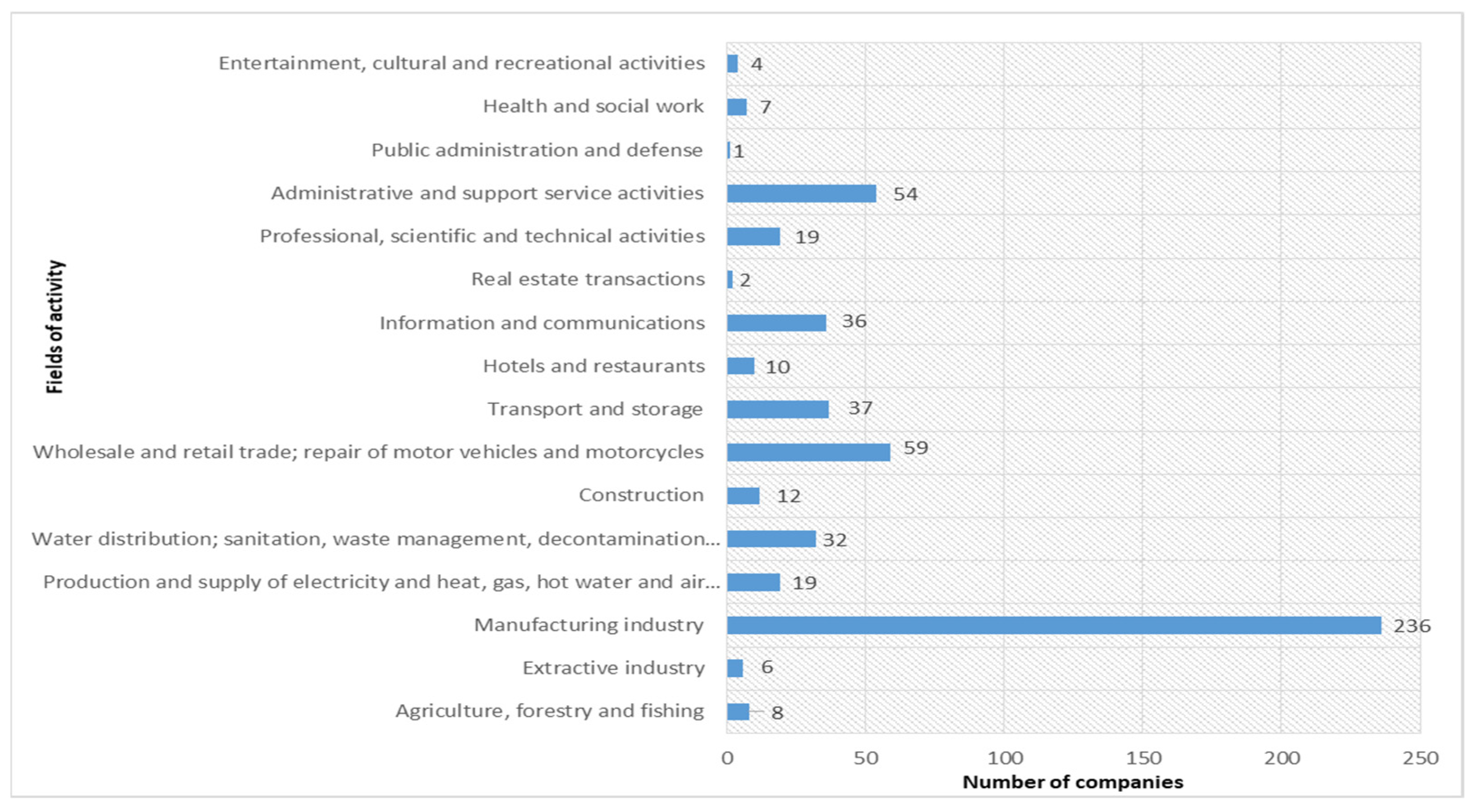

3.1. Sample

3.2. Methodology

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bautista-Lazo, S.; Short, T. Introducing the all seeing eye of business: A model for understanding the nature, impact and potential uses of waste. J. Clean. Prod. 2013, 40, 141–150. [Google Scholar] [CrossRef]

- Núñez-Cacho, P.; Molina-Moreno, V.; Corpas-Iglesias, F.A.; Cortés-García, F.J. Family businesses transitioning to a circular economy model: The case of “Mercadona”. Sustainability 2018, 10, 538. [Google Scholar] [CrossRef] [Green Version]

- Fortunati, S.; Morea, D.; Mosconi, E.M. Circular economy and corporate social responsibility in the agricultural system: Cases study of the Italian agri-food industry. Agric. Econ. 2020, 66, 489–498. [Google Scholar] [CrossRef]

- European Union. Directive 2014/95/UE of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/UE as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32014L0095 (accessed on 25 July 2021).

- Beleneși, M.; Bogdan, V.; Popa, D.N. Disclosure Dynamics and Non-Financial Reporting Analysis. The Case of Romanian Listed Companies. Sustainability 2021, 13, 4732. [Google Scholar] [CrossRef]

- Ştefănescu, C.A.; Tiron-Tudor, A.; Moise, E.M. Eu non-financial reporting research–insights, gaps, patterns and future agenda. J. Bus. Econ. Manag. 2021, 22, 257–276. [Google Scholar] [CrossRef]

- Oprean-Stan, C.; Oncioiu, I.; Iuga, I.C.; Stan, S. Impact of Sustainability Reporting and Inadequate Management of ESG Factors on Corporate Performance and Sustainable Growth. Sustainability 2020, 12, 8536. [Google Scholar] [CrossRef]

- Băndoi, A.; Bocean, C.G.; Del Baldo, M.; Mandache, L.; Mănescu, L.G.; Sitnikov, C.S. Including Sustainable Reporting Practices in Corporate Management Reports: Assessing the Impact of Transparency on Economic Performance. Sustainability 2021, 13, 940. [Google Scholar] [CrossRef]

- Meseguer-Sánchez, V.; Gálvez-Sánchez, F.J.; López-Martínez, G.; Molina-Moreno, V. Corporate Social Responsibility and Sustainability. A Bibliometric Analysis of Their Interrelations. Sustainability 2021, 13, 1636. [Google Scholar] [CrossRef]

- Stoyanova, T. CSR Strategies Applied in Terms of Circular Economy. Econ. Altern. 2019, 2, 263–274. [Google Scholar]

- Scarpellini, S. Social indicators for businesses’ circular economy: Multi-faceted analysis of employment as an indicator for sustainability reporting. Eur. J. Soc. Impact Circ. Econ. 2021, 17–44. [Google Scholar] [CrossRef]

- Urmanaviciene, A. Wises’ Social Impact Measurement in the Baltic States. Eur. J. Soc. Impact Circ. Econ. 2020, 48–75. [Google Scholar] [CrossRef]

- Massaro, M.; Secinaro, S.; Dal Mas, F.; Brescia, V.; Calandra, D. Industry 4.0 and circular economy: An exploratory analysis of academic and practitioners’ perspectives. Bus. Strategy Environ. 2021, 30, 1213–1231. [Google Scholar] [CrossRef]

- Urmanaviciene, A.; Arachchi, U.S. The Effective Methods and Practices for Accelerating Social Entrepreneurship Through Corporate Social Responsibility. Eur. J. Soc. Impact Circ. Econ. 2020, 27–47. [Google Scholar] [CrossRef]

- Fortunati, S.; Martiniello, L.; Morea, D. The Strategic Role of the Corporate Social Responsibility and Circular Economy in the Cosmetic Industry. Sustainability 2020, 12, 5120. [Google Scholar] [CrossRef]

- Campra, M.; Brescia, V.; Jafari-Sadeghi, V.; Calandra, D. Islamic countries and Maqasid al-Shariah towards the circular economy. The Dubai case study. Eur. J. Islamic Financ. 2021, 17, 1–9. [Google Scholar]

- Scarpellini, S.; Marín-Vinuesa, L.M.; Aranda-Uson, A.; Portillo-Tarragona, P. Dynamic capabilities and environmental accounting for the circular economy in businesses. Sustain. Account. Manag. Policy J. 2020, 11, 1129–1158. [Google Scholar] [CrossRef] [Green Version]

- Skare, M.; Golja, T. Corporate Social Responsibility and Corporate Financial Performance—Is there a link? Econ. Res.-Ekon. Istraz. 2012, 25, 215–242. [Google Scholar] [CrossRef] [Green Version]

- Janik, A.; Ryszko, A.; Szafraniec, M. Greenhouse gases and circular economy issues in sustainability reports from the energy sector in the European Union. Energies 2020, 13, 5993. [Google Scholar] [CrossRef]

- Oncioiu, I.; Petrescu, A.G.; Bilcan, F.R.; Petrescu, M.; Popescu, D.M.; Anghel, E. Corporate Sustainability Reporting and Financial Performance. Sustainability 2020, 12, 4297. [Google Scholar] [CrossRef]

- Hategan, P.V. Philosophical practice and ethics applied in organizations. An. Univ. București-Ser. Filos. 2019, 68, 53–65. [Google Scholar]

- Rodrigo-González, A.; Grau-Grau, A.; Bel-Oms, I. Circular Economy and Value Creation: Sustainable Finance with a Real Options Approach. Sustainability 2021, 13, 7973. [Google Scholar] [CrossRef]

- Ionescu, G.H.; Firoiu, D.; Pirvu, R.; Vilag, R.D. The impact of ESG factors on market value of companies from travel and tourism industry. Technol. Econ. Dev. Econ. 2019, 25, 820–849. [Google Scholar] [CrossRef]

- European Reporting LAB. Proposals for a Relevant and Dynamic EU Sustainability Reporting Standard Setting. 2021. Available online: https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/210308-report-efrag-sustainability-reporting-standard-setting_en.pdf (accessed on 2 May 2021).

- European Commission. FAQ: What Is the EU Taxonomy Article 8 Delegated Act and how will It Work in Practice? 2021. Available online: https://ec.europa.eu/info/sites/default/files/business_economy_euro/banking_and_finance/documents/sustainable-finance-taxonomy-article-8-faq_en.pdf (accessed on 22 October 2021).

- Accountancy Europe. SME Risk Management: Sustainability. 2020. Available online: https://www.accountancyeurope.eu/publications/sme-risk-management-sustainability/https://www.accountancyeurope.eu/wp-content/uploads/SME-sustainability_Accountancy-Europe-2020.pdf (accessed on 23 August 2021).

- IFRS Foundation. Consultation Paper on Sustainability Reporting. 2020. Available online: https://www.ifrs.org/content/dam/ifrs/project/sustainability-reporting/consultation-paper-on-sustainability-reporting.pdf (accessed on 23 August 2021).

- Fiandrino, S.; Tonelli, A. A Text-Mining Analysis on the Review of the Non-Financial Reporting Directive: Bringing Value Creation for Stakeholders into Accounting. Sustainability 2021, 13, 763. [Google Scholar] [CrossRef]

- La Torre, M.; Sabelfeld, S.; Blomkvist, M.; Dumay, J. Rebuilding trust: Sustainability and non-financial reporting and the European Union regulation. Meditari Account. Res. 2020, 28, 701–725. [Google Scholar] [CrossRef]

- Raucci, D.; Tarquinio, L. Sustainability performance indicators and non-financial information reporting. Evidence from the Italian case. Adm. Sci. 2020, 10, 13. [Google Scholar] [CrossRef] [Green Version]

- Gazzola, P.; Pezzetti, R.; Amelio, S.; Grechi, D. Non-Financial information disclosure in Italian Public interest companies: A sustainability reporting perspective. Sustainability 2020, 12, 6063. [Google Scholar] [CrossRef]

- Venturelli, A.; Pizzi, S.; Caputo, F.; Principale, S. The revision of nonfinancial reporting directive: A critical lens on the comparability principle. Bus. Strategy Environ. 2020, 29, 3584–3597. [Google Scholar] [CrossRef]

- Caputo, F.; Pizzi, S.; Ligorio, L.; Leopizzi, R. Enhancing environmental information transparency through corporate social responsibility reporting regulation. Bus. Strategy Environ. 2021, 1–15. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory Nonfinancial Disclosure and Its Consequences on the Sustainability Reporting Quality of Italian and German Companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef] [Green Version]

- Aureli, S.; Salvatori, S.; Magnaghi, E. A Country-Comparative Analysis of the Transposition of the EU Non-Financial Directive: An Institutional Approach. Account. Econ. Law. 2020. [Google Scholar] [CrossRef]

- Piesiewicz, M.; Ciechan-Kujawa, M.; Kufel, P. Differences in Disclosure of Integrated Reports at Energy and Non-Energy Companies. Energies 2021, 14, 1253. [Google Scholar] [CrossRef]

- Krasodomska, J.; Godawska, J. CSR in Non-Large Public Interest Entities: Corporate Talk vs. Actions. Sustainability 2020, 12, 9075. [Google Scholar] [CrossRef]

- Arraiano, I.G.; Hategan, C.D. The stage of corporate social responsibility in EU-CEE countries. Eur. J. Sustain. Dev. 2019, 8, 340. [Google Scholar] [CrossRef] [Green Version]

- Popescu, C.R.G.; Popescu, G.N. An Exploratory Study Based on a Questionnaire Concerning Green and Sustainable Finance, Corporate Social Responsibility, and Performance: Evidence from the Romanian Business Environment. J. Risk Financ. Manag. 2019, 12, 162. [Google Scholar] [CrossRef] [Green Version]

- Ienciu, I.A.; Muller, V.; Popa, I.; Bonaci, C. Study on Non-Financial Reporting in Accordance with European Directives in the Case of Romanian Companies. Audit. Financ. 2014, 117, 43–49. [Google Scholar]

- Stolowy, H.; Paugam, L. The expansion of non-financial reporting: An exploratory study. Account. Bus. Res. 2018, 48, 525–548. [Google Scholar] [CrossRef] [Green Version]

- Testarmata, S.; Ciaburri, M.; Fortuna, F.; Sergiacomi, S. Harmonization of non-financial reporting regulation in Europe: A study of the transposition of the directive 2014/95/EU. In Accountability, Ethics and Sustainability of Organizations; Springer: Cham, Switzerland, 2020; pp. 67–88. [Google Scholar]

- Veltri, S. The mandatory non-financial disclosure in the European Union. In Mandatory Nonfinancial Risk-Related Disclosure; Springer: Cham, Switzerland, 2020; pp. 31–55. [Google Scholar]

- Marinescu, A.-O. Analysis on the Compliance of Sustainability Reports of Romanian Companies with GRI Conceptual Framework. Audit Financ. 2020, 18, 361–375. [Google Scholar] [CrossRef]

- Fărcaş, T.V. Study about the Implementation of the Directive 95/2014 in Romania—Legislative Perspective and the Actual Application. Audit Financ. 2020, 18, 339–351. [Google Scholar] [CrossRef]

- Cosofret, B.D.; Mart, R.A.; Manea, M. An overview of the non-financial reporting practices of the Romanian public-interest entities listed on Bucharest Stock Exchange. Rev. Econ. 2020, 72, 57–64. [Google Scholar]

- Hategan, C.-D.; Curea-Pitorac, R.-I.; Hategan, V.-P. The Romanian Family Businesses Philosophy for Performance and Sustainability. Sustainability 2019, 11, 1715. [Google Scholar] [CrossRef] [Green Version]

- Secinaro, S.; Brescia, V.; Calandra, D.; Saiti, B. Impact of climate change mitigation policies on corporate financial performance: Evidence-based on European publicly listed firms. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2491–2501. [Google Scholar] [CrossRef]

- Lu, J.; Javeed, S.A.; Latief, R.; Jiang, T.; Ong, T.S. The Moderating Role of Corporate Social Responsibility in the Association of Internal Corporate Governance and Profitability; Evidence from Pakistan. Int. J. Environ. Res. Public Health 2021, 18, 5830. [Google Scholar] [CrossRef] [PubMed]

- Cosma, S.; Venturelli, A.; Schwizer, P.; Boscia, V. Sustainable Development and European Banks: A Non-Financial Disclosure Analysis. Sustainability 2020, 12, 6146. [Google Scholar] [CrossRef]

- Fonseca, L.; Carvalho, F. The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations. Sustainability 2019, 11, 5797. [Google Scholar] [CrossRef] [Green Version]

- Nechita, E.; Manea, C.L.; Nichita, E.M.; Irimescu, A.M.; Manea, D. Is Financial Information Influencing the Reporting on SDGs? Empirical Evidence from Central and Eastern European Chemical Companies. Sustainability 2020, 12, 9251. [Google Scholar] [CrossRef]

- Hąbek, P. CSR Reporting Practices in Visegrad Group Countries and the Quality of Disclosure. Sustainability 2017, 9, 2322. [Google Scholar] [CrossRef] [Green Version]

- Matuszak, Ł.; Różańska, E. CSR disclosure in Polish-listed companies in the light of Directive 2014/95/EU requirements: Empirical evidence. Sustainability 2017, 9, 2304. [Google Scholar] [CrossRef] [Green Version]

- Hategan, C.D.; Sirghi, N.; Curea-Pitorac, R.-I. The Financial Indicators Influencing the Market Value of the Romanian Listed Companies at the Regional Level. In Economic and Social Development: Book of Proceedings, Proceedings of the 22nd International Scientific Conference on Economic and Social Development, Split, Croatia 29–30 June 2017; Varazdin Development and Entrepreneurship Agency: Varazdin, Croatia, 2017; pp. 160–171. [Google Scholar]

- Chelariu, G. The link between Corporate Social Responsibility and Financial Performance: A quantitative analysis for companies in Romania. North Econ. Rev. 2017, 1, 179–185. [Google Scholar]

- Batae, O.M.; Dragomit, V.; Feleaga, L. Environmental, social, governance (ESG), and financial performance of European banks. J. Account. Manag. Inf. Syst. 2020, 19, 480–501. [Google Scholar] [CrossRef]

- Hategan, V.-P. Promoting the Eco-Dialogue through Eco-Philosophy for Community. Sustainability 2021, 13, 4291. [Google Scholar] [CrossRef]

- Nechita, E.; Manea, C.L.; Irimescu, A.M.; Nichita, E.M. The Content Analysis of Reporting on Sustainable Development Goals. Audit. Financ. 2020, 4, 704–728. [Google Scholar] [CrossRef]

- Paunescu (Petre), C.F.; Man, M. Analysis of Corporate Social Responsibility Aspects Included in The Integrated Reports at OMV Petrom Group. J. East. Eur. Res. Bus. Econ. 2021. [Google Scholar] [CrossRef]

- Equileap. Gender Equality in Poland, Romania & The Czech Republic Assessing Leading Companies on Workplace Equality. 2020. Available online: https://equileap.com/wp-content/uploads/2020/06/Equileap_EuropeanReport_Poland-Romania-CzechRepublic.pdf (accessed on 22 October 2021).

- Sava, A.; Bogdan, M.; Kocsi, K. Online disclosure of non-financial information in Romanian large companies. Acta Tech. Napoc.-Ser. Appl. Math. Mech. Eng. 2018, 61, 203–208. [Google Scholar]

- Doni, F.; Martini, S.B.; Corvino, A.; Mazzoni, M. Voluntary versus mandatory non-financial disclosure: EU Directive 95/2014 and sustainability reporting practices based on empirical evidence from Italy. Meditari Account. Res. 2019, 28, 781–802. [Google Scholar] [CrossRef]

- Albu, N.; Albu, C.N.; Apostol, O.; Cho, C.H. The past is never dead: The role of imprints in shaping social and environmental reporting in a post-communist context. Account. Audit. Account. J. 2020, 34, 1109–1136. [Google Scholar] [CrossRef]

- Dumitru, M.; Dyduch, J.; Gușe, R.G.; Krasodomska, J. Corporate reporting practices in Poland and Romania–an ex-ante study to the new non-financial reporting European directive. Account. Eur. 2017, 14, 279–304. [Google Scholar] [CrossRef]

- Morea, D.; Fortunati, S.; Martiniello, L. Circular economy and corporate social responsibility: Towards an integrated strategic approach in the multinational cosmetics industry. J. Clean. Prod. 2021, 315, 128232. [Google Scholar] [CrossRef]

- Crișan-Mitra, C.S.; Stanca, L.; Dabija, D.-C. Corporate Social Performance: An Assessment Model on an Emerging Market. Sustainability 2020, 12, 4077. [Google Scholar] [CrossRef]

- Stewart, R.; Niero, M. Circular economy in corporate sustainability strategies: A review of corporate sustainability reports in the fast-moving consumer goods sector. Bus. Strategy Environ. 2018, 27, 1005–1022. [Google Scholar] [CrossRef] [Green Version]

- Pasko, O.; Chen, F.; Oriekhova, A.; Brychko, A.; Shalyhina, I. Mapping the Literature on Sustainability Reporting: A Bibliometric Analysis Grounded in Scopus and Web of Science Core Collection. Eur. J. Sustain. Dev. 2021, 10, 303. [Google Scholar] [CrossRef]

- Monciardini, D.; Mähönen, J.T.; Tsagas, G. Rethinking non-financial reporting: A blueprint for structural regulatory changes. Account. Econ. Law Conviv. 2020, 10. [Google Scholar] [CrossRef]

- García-Sánchez, I.M. Corporate social reporting and assurance: The state of the art: Información social corporativa y aseguramiento: El estado de la cuestión. Rev. Contab.-Span. Account. Rev. 2021, 24, 241–269. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Social Responsibility: Perspectives on the CSR Construct’s Development and Future. Bus. Soc. 2021, 00076503211001765. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

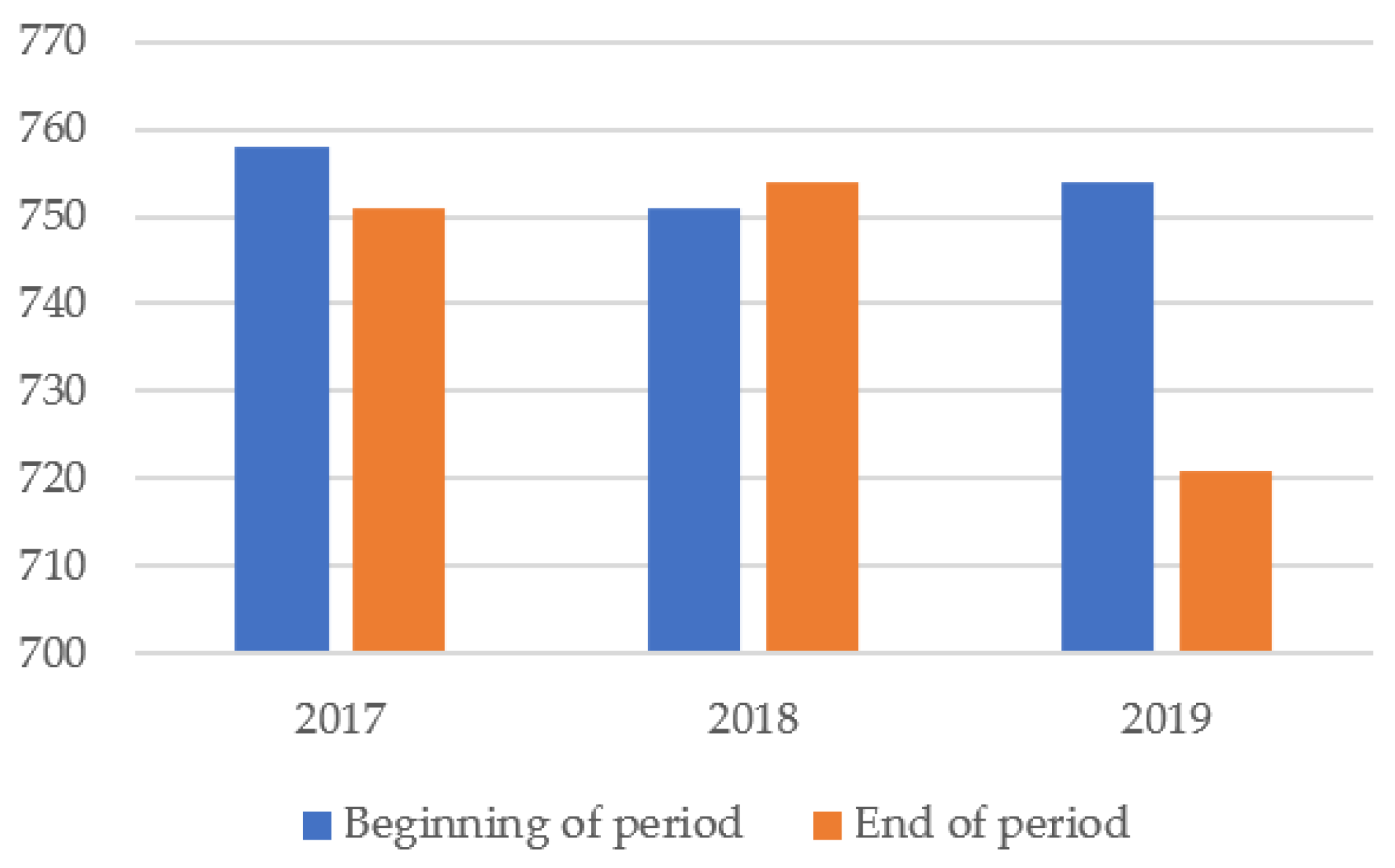

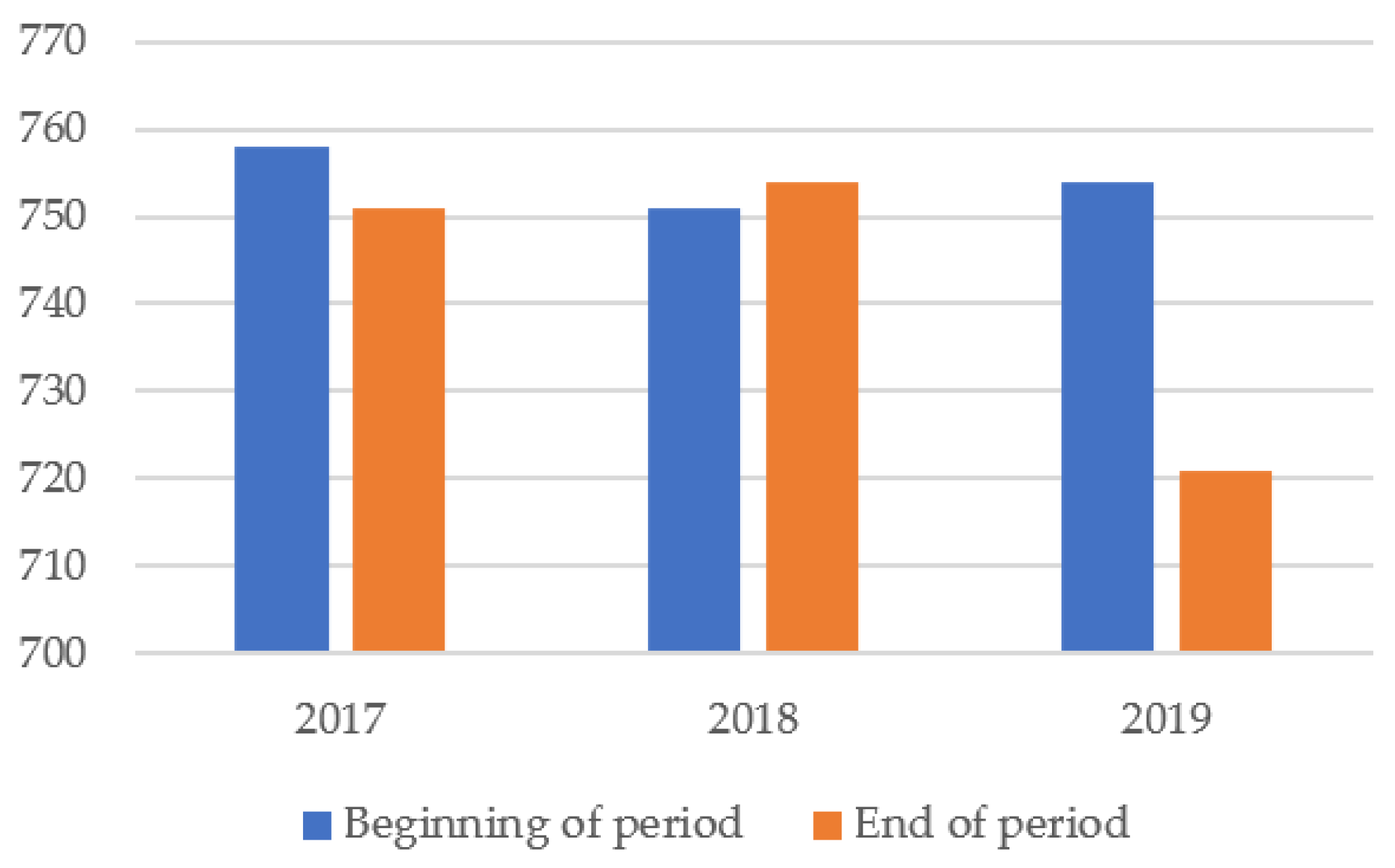

| Year | Beginning of Period | Inputs | Outputs | End of Period |

|---|---|---|---|---|

| 2017 | 758 | 74 | 81 | 751 |

| 2018 | 751 | 64 | 61 | 754 |

| 2019 | 754 | 53 | 86 | 721 |

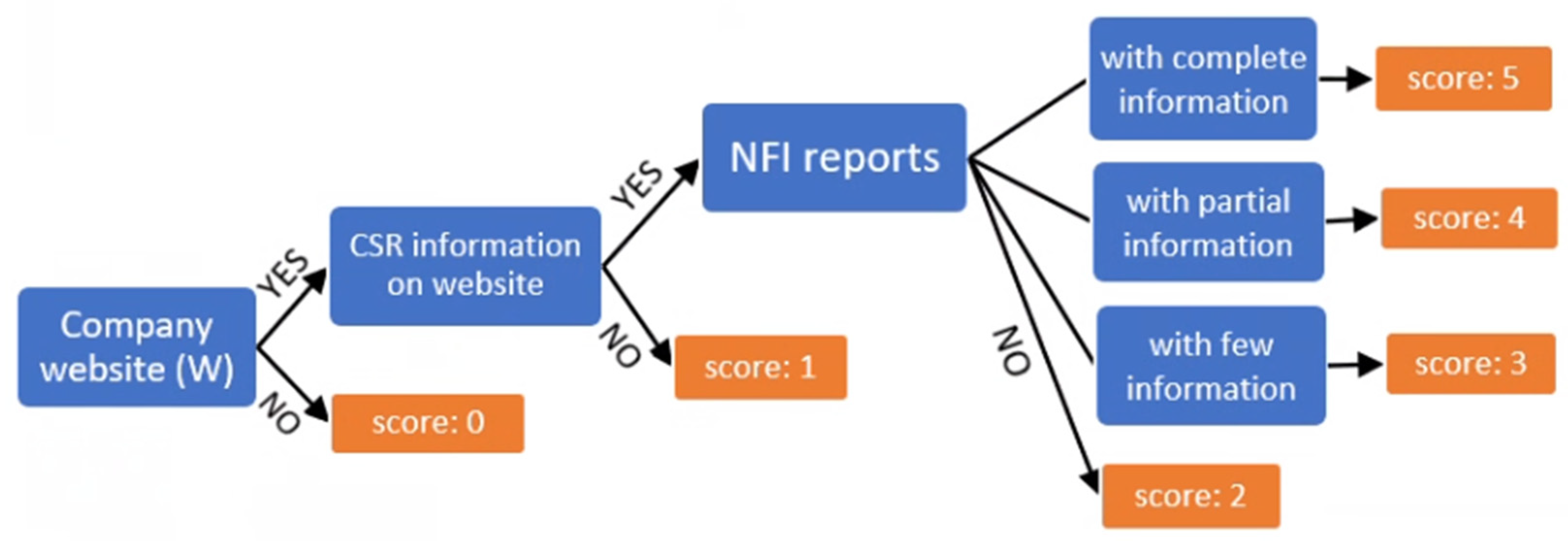

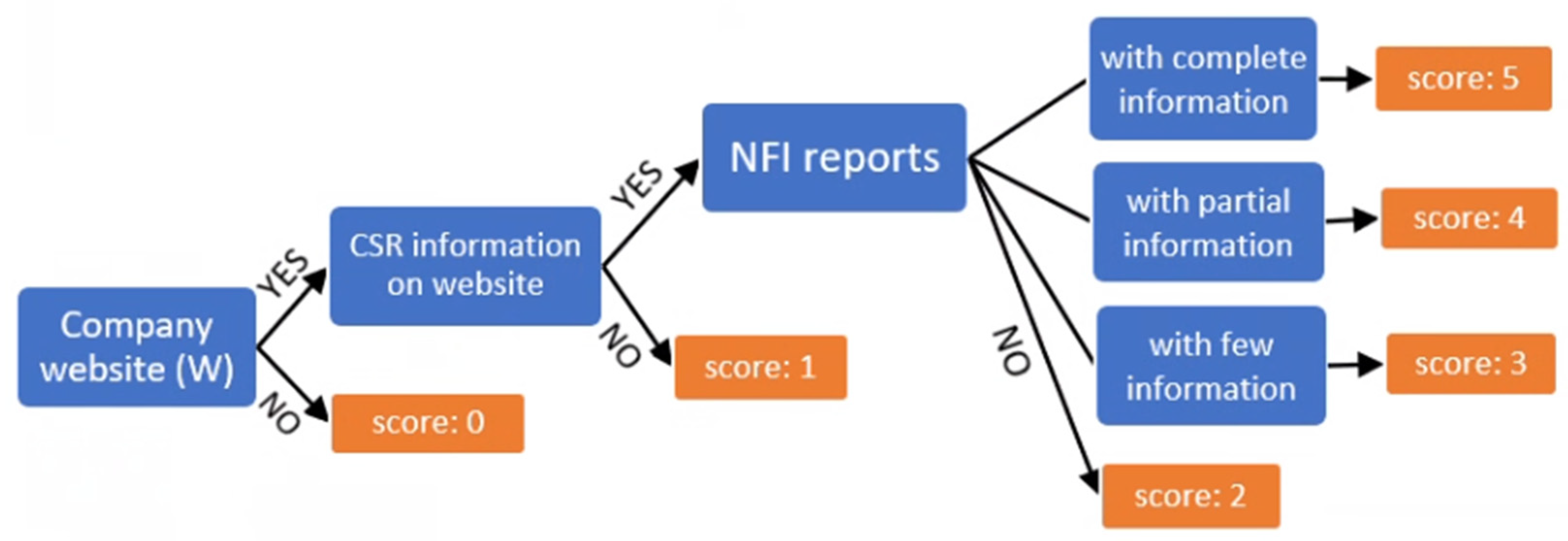

| Score | Description |

|---|---|

| 1 | lack of non-financial information in separate corporate social responsibility reports/statements or sections in the annual reports; |

| 2 | limited information, the information is mentioned on the website, but is not described in a section of a report or in a separate report; |

| 3 | some information is presented in the annual reports, but with deficiencies, the information is described in insufficient coverage; |

| 4 | almost comprehensive information, a good description of the information, but there is no connection with other sections of the report, this information can be found in separate reports or sections of the annual reports; |

| 5 | complete information, the information presented is comprehensive, with a clear link to other sections of the report. |

| Indicator | Code | Description |

|---|---|---|

| Score | S | 1 to 5 |

| Information on a website | I | 1—Yes; 0—No |

| Foreign ownership | F | 1—Yes; 0—No |

| Private ownership | P | 1—Yes; 0—No |

| Listed company | L | 1—Yes; 0—No |

| Return on assets | ROA | Own computation based on financial statements |

| Return on equity | ROE | Own computation based on financial statements |

| Employees | E | Number of employees |

| Website | W | 1—Yes; 0—No |

| Variables | Obs. | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| S | 1626 | 2.3862 | 1.5399 | 1 | 5 |

| I | 1626 | 0.5043 | 0.5001 | 0 | 1 |

| F | 1626 | 0.5092 | 0.5000 | 0 | 1 |

| P | 1626 | 0.8597 | 0.3473 | 0 | 1 |

| L | 1626 | 0.0405 | 0.1974 | 0 | 1 |

| ROE | 1626 | −0.1815 | 9.1171 | −280.06 | 4.03 |

| ROA | 1626 | 0.0716 | 0.1111 | −0.72 | 0.77 |

| E | 1626 | 1722.83 | 2392.755 | 500 | 23404 |

| W | 1626 | 0.9151 | 0.2787 | 0 | 1 |

| Obs. | S | I | F | P | L | ROE | ROA | E | W |

|---|---|---|---|---|---|---|---|---|---|

| S | 1 | ||||||||

| I | 0.6411 *** | 1 | |||||||

| F | 0.3294 *** | 0.3849 *** | 1 | ||||||

| P | −0.0540 ** | 0.1310 *** | 0.4114 *** | 1 | |||||

| L | 0.2116 *** | 0.0356 | −0.1347 *** | −0.1054 *** | 1 | ||||

| ROE | 0.0091 | −0.0332 | 0.0037 | 0.0443 * | 0.0058 | 1 | |||

| ROA | −0.0207 | 0.0143 | 0.0998 *** | 0.1656 *** | −0.0367 | 0.0882 *** | 1 | ||

| E | 0.2206 *** | 0.1524 *** | 0.0927 *** | −0.1248 *** | 0.0405 | 0.0054 | −0.0644 *** | 1 | |

| W | 0.2570 *** | 0.3072 *** | 0.0718 *** | −0.1039 *** | 0.0626 ** | −0.0128 | −0.1123 *** | 0.0570 ** | 1 |

| Obs. | R2 | F | I | F | P | L | ROE | ROA | E | W |

|---|---|---|---|---|---|---|---|---|---|---|

| All companies | ||||||||||

| 1626 | 0.8402 | 1045 *** | 1.6273 | 0.5606 | −0.1259 | 1.6055 | 0.0041 | 0.3613 | 0.0008 | 1.1782 |

| (26.74) *** | (9.69) *** | (−1.64) * | (13.99) *** | (4.56) *** | (1.40) | (5.48) *** | (15.12) *** | |||

| 1626 | 0.7979 | 1246 *** | 2.1367 | 0.5380 | 0.8036 | 2.041 | 0.0027 | 0.3873 | - | - |

| (38.93) *** | (9.74) *** | (19.97) *** | (14.80) *** | (1.41) | (1.38) | |||||

| Manufacturing industry | ||||||||||

| 708 | 0.8668 | 1530.5 *** | 1.9851 | 0.4810 | 0.5340 | 1.6687 | 0.0056 | 0.8792 | 0.0001 | 0.2386 |

| (23.11) *** | (5.80) *** | (4.44) *** | (10.39) *** | (11.52) *** | (2.05) ** | (3.17) *** | (2.08) *** | |||

| 708 | 0.8617 | 1926 *** | 2.098 | 0.569 | 0.831 | 1.718 | 0.0059 | 0.784 | - | - |

| (24.07) *** | (7.36) *** | (13.86) *** | (10.26) *** | (12.14) *** | (1.80) * | |||||

| Wald CHI2 (10) | I | F | P | L | ROE | ROA | E | W |

|---|---|---|---|---|---|---|---|---|

| All companies | ||||||||

| 1643.5 *** | 1.7116 | 0.6293 | −0.7830 | 1.517 | 0.0057 | −0.0855 | 0.0005 | 0.1987 |

| (27.64) *** | (9.76) *** | (−8.89) *** | (10.94) *** | (1.93) * | (−0.34) | (4.68) *** | (1.92) * | |

| 1593.5 *** | 1.7799 | 0.6648 | −0.8731 | 1.5491 | 0.0061 | −0.1912 | - | - |

| (30.10) *** | (10.30) *** | (−10.07) *** | (11.10) *** | (11.10) *** | (−0.77) | |||

| Manufacturing Industry | ||||||||

| 3433.7 *** | 1.9958 | 0.4814 | 0.5123 | 1.663 | 0.011 | 1.167 | 0.001 | 0.225 |

| (18.93) *** | (4.44) *** | (3.31) *** | (7.83) *** | (1.81) * | (2.07) ** | (4.19) *** | (1.47) | |

| 3250.7 *** | 2.110 | 0.569 | 0.792 | 1.711 | 0.011 | 1.093 | - | - |

| (20.92) *** | (5.24) *** | (8.46) *** | (7.97) *** | (1.79) * | (1.91) ** | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hategan, C.-D.; Pitorac, R.-I.; Milu, N.-D. Assessment of the Mandatory Non-Financial Reporting of Romanian Companies in the Circular Economy Context. Int. J. Environ. Res. Public Health 2021, 18, 12899. https://doi.org/10.3390/ijerph182412899

Hategan C-D, Pitorac R-I, Milu N-D. Assessment of the Mandatory Non-Financial Reporting of Romanian Companies in the Circular Economy Context. International Journal of Environmental Research and Public Health. 2021; 18(24):12899. https://doi.org/10.3390/ijerph182412899

Chicago/Turabian StyleHategan, Camelia-Daniela, Ruxandra-Ioana Pitorac, and Nicoleta-Daniela Milu. 2021. "Assessment of the Mandatory Non-Financial Reporting of Romanian Companies in the Circular Economy Context" International Journal of Environmental Research and Public Health 18, no. 24: 12899. https://doi.org/10.3390/ijerph182412899

APA StyleHategan, C.-D., Pitorac, R.-I., & Milu, N.-D. (2021). Assessment of the Mandatory Non-Financial Reporting of Romanian Companies in the Circular Economy Context. International Journal of Environmental Research and Public Health, 18(24), 12899. https://doi.org/10.3390/ijerph182412899