The Equity of Health Care Spending in South Korea: Testing the Impact of Publicness

Abstract

1. Introduction

2. Literature Review

2.1. Expanded Theories on Publicness and Organizational Form

2.2. Organizational Publicness and Market Competition: What Makes Better Performance?

2.3. Comparing the Equity of Public and Private Healthcare Organizations

3. Research Frame and Method

3.1. Comparing Organizational Form and Equity in Health Care Services

3.2. Variables and Data

3.3. Analytical Methods

4. Empirical Findings and Discussions

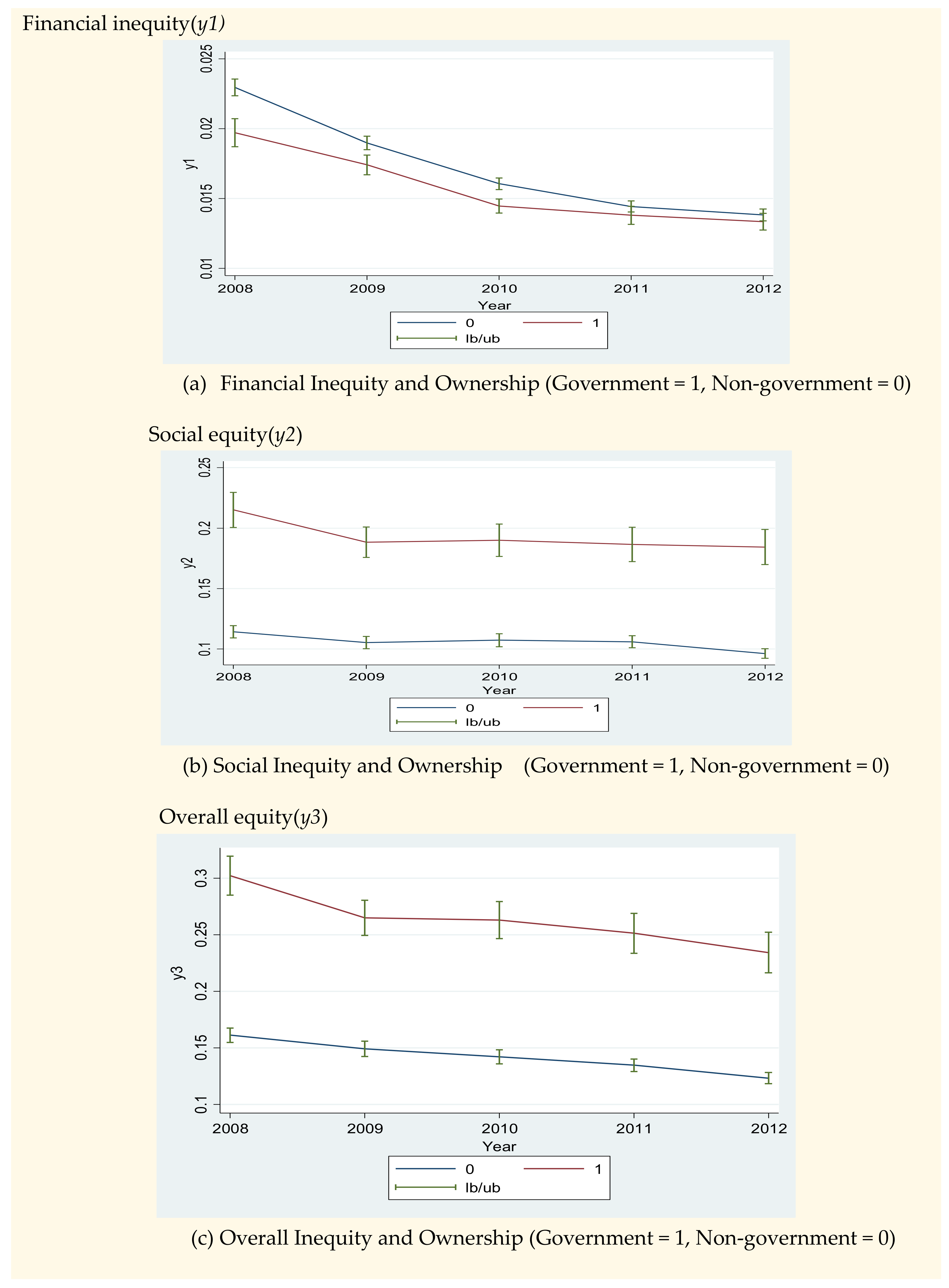

4.1. Trends of Equitable Performance in Hospitals

4.2. The Impact of Publicness on Social Performance in Hospitals

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variables | Definitions | Sources |

|---|---|---|

| Proportion of out-of-pocket money for the poor (y1 = Financial inequity) | The ratio of out-of-pocket payments over medical care expenses for the poor in the Medical Aid program for each hospital | The Health Insurance Review and Assessment Service |

| Proportion of treatment for the disadvantaged (y2 = Social equity) | The ratio of payment statement of medical aid and veteran relief to total payment statements for each hospital | The Health Insurance Review and Assessment Service |

| The proportion of payment coverage for the disadvantaged (y3 = Overall equity) | The ratio of payment of medical aid and veteran relief to total amount of medical payments for each hospital | The Health Insurance Review and Assessment Service |

| Govt (Dummy variables) | The value of the Govt dummy variable is 1 if the hospital is national, provincial, and city hospitals owned by central and local governments. Otherwise, the value is 0. | The Health Insurance Review and Assessment Service |

| Govt_EV (Dummy) | The value is 1 if the hospital has legal obligation for government evaluation. Otherwise, the value is 0. | Coding based on related legislation and regulations |

| Audit (Dummy) | The value is 1 if the hospital has legal obligation for accounting audit. Otherwise, the value is 0. | Coding based on related legislation and regulations |

| Credit (Dummy) | The value is 1 if the hospital receives accreditation by Korea Institute for Healthcare Accreditation. Otherwise, the value is 0. | Webpage of Korea Institute for Healthcare Accreditation |

| Ln_Pay_Count | All the medical care statements from health insurance expenses, medical aid expenses, and veterans expenses transformed by natural logarithm | The Health Insurance Review and Assessment Service |

| Age | Foundation year representing organizational age | Korean Hospital Association (List of Hospitals in Korea) |

| Bed | The number of hospital beds representing organizational size | The Health Insurance Review and Assessment Service |

Appendix B

| Variable | Obs | Mean | SD | Min | Max |

|---|---|---|---|---|---|

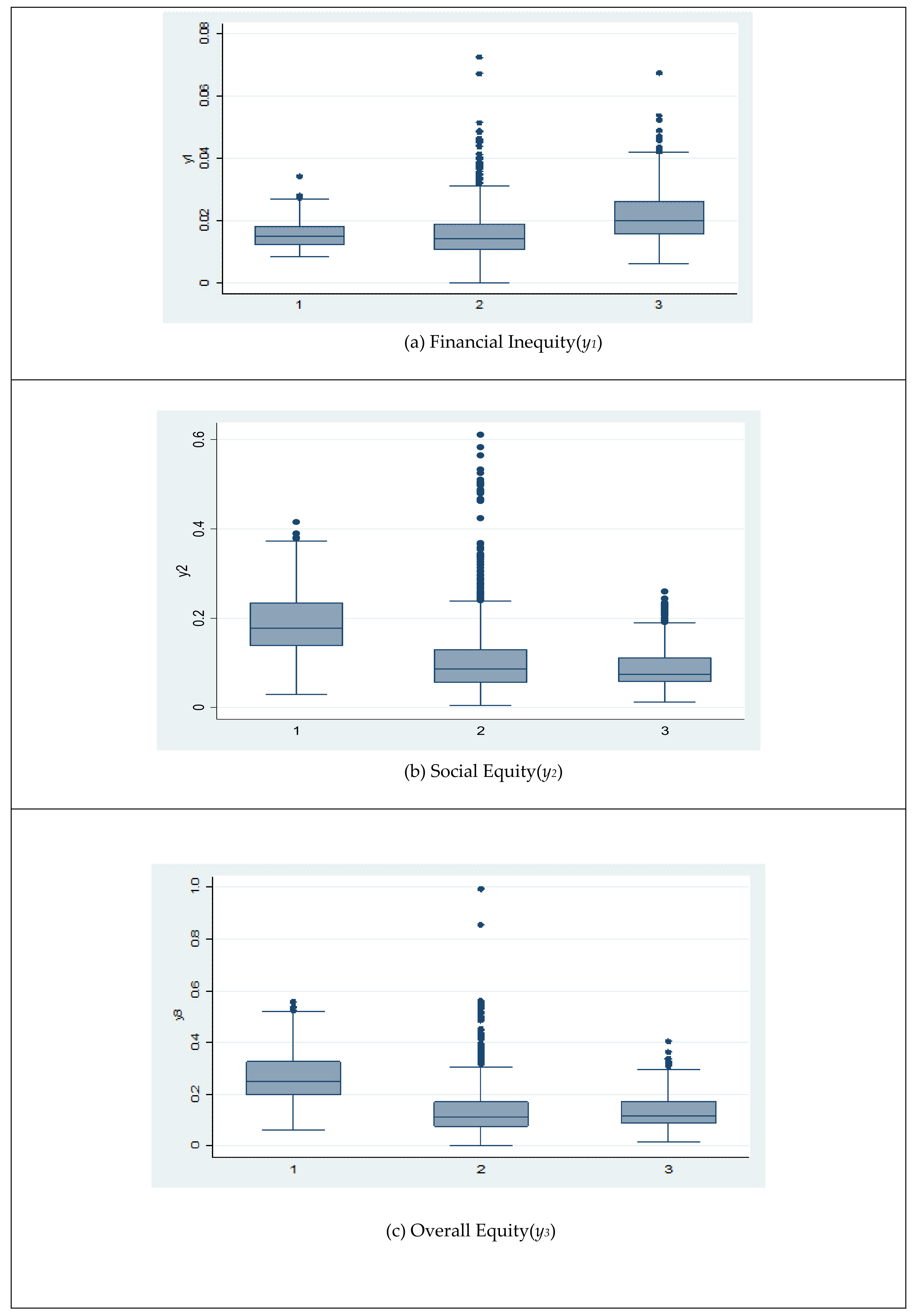

| y1 (Financial inequity) | 1578 | 0.0171 | 0.0082 | 0.00005 | 0.0725 |

| y2 (Social equity) | 1578 | 0.1146 | 0.0864 | 0.0047 | 0.6106 |

| y3 (Overall equity) | 1578 | 0.1542 | 0.1071 | 0.0043 | 0.9942 |

| Govt | 1584 | 0.10 | 0.30 | 0 | 1 |

| Govt_EV | 1584 | 0.30 | 0.46 | 0 | 1 |

| Credit | 1584 | 0.11 | 0.32 | 0 | 1 |

| Audit | 1584 | 0.18 | 0.38 | 0 | 1 |

| Private | 1584 | 0.21 | 0.41 | 0 | 1 |

| Ln_Pay_Count | 1578 | 9.05 | 1.03 | 4.14 | 11.95 |

| Int_govt | 1578 | 0.84 | 2.53 | 0 | 10.44 |

| Int_private | 1578 | 1.81 | 3.51 | 0 | 9.65 |

| Age | 1584 | 1992.24 | 15.16 | 1909 | 2012 |

| Bed | 1584 | 422.30 | 311.00 | 100 | 2680 |

| Year | 1584 | 2010.02 | 1.41 | 2008 | 2012 |

Appendix C

| Frequency | Percent | Cumulative | 2008 | 2009 | 2010 | 2011 | 2012 |

|---|---|---|---|---|---|---|---|

| 295 | 87.02 | 87.02 | Yes | Yes | Yes | Yes | Yes |

| 10 | 2.95 | 89.97 | No | No | Yes | Yes | Yes |

| 7 | 2.06 | 92.04 | No | No | No | Yes | Yes |

| 6 | 1.77 | 93.81 | No | Yes | Yes | Yes | Yes |

| 6 | 1.77 | 95.58 | Yes | Yes | Yes | No | No |

| 5 | 1.47 | 97.05 | Yes | No | No | No | No |

| 5 | 1.47 | 98.53 | Yes | Yes | No | No | No |

| 4 | 1.18 | 99.71 | No | No | No | No | Yes |

| 1 | 0.29 | 100 | Yes | Yes | Yes | Yes | No |

| 339 | 100 |

Appendix D

| National Health Insurance | |||||

| Inpatients | Outpatients | ||||

| Year | N | Mean | SD | Mean | SD |

| 2008 | 311 | 12,603.8 | 15,094.8 | 152,844.3 | 180,090.0 |

| 2009 | 312 | 13,379.1 | 16,459.6 | 178,672.8 | 209,294.7 |

| 2010 | 316 | 14,180.1 | 17,273.0 | 188,745.7 | 235,695.9 |

| 2011 | 319 | 14,623.1 | 17,471.2 | 201,214.3 | 246,827.7 |

| 2012 | 320 | 15,048.2 | 17,837.0 | 276,836.8 | 336,685.8 |

| Medical Care Assistance | |||||

| Inpatients | Outpatients | ||||

| Year | N | Mean | SD | Mean | SD |

| 2008 | 311 | 1774.8 | 1983.9 | 14,668.5 | 13,176.5 |

| 2009 | 312 | 1670.9 | 1886.2 | 16,063.1 | 15,244.9 |

| 2010 | 316 | 1719.5 | 2401.4 | 17,064.6 | 17,459.3 |

| 2011 | 319 | 1806.8 | 2565.1 | 18,021.9 | 18,233.7 |

| 2012 | 320 | 1463.6 | 1440.1 | 21,363.6 | 17,009.1 |

Appendix E

| Coefficient | SE | t-Value | p > |t| | ||

|---|---|---|---|---|---|

| Govt | −0.024 | 0.011 | −2.070 | 0.038 | |

| Govt_EV | −0.002 | 0.0008 | −2.550 | 0.011 | |

| Credit | 0.000 | 0.00036 | −0.730 | 0.463 | |

| Audit | 0.000005 | 0.0011 | 0.000 | 0.997 | |

| Private | −0.005 | 0.006 | −0.760 | 0.447 | |

| Ln_pay_count | −0.001 | 0.00036 | −3.920 | 0.000 | |

| Int_govt | 0.003 | 0.0013 | 2.090 | 0.036 | |

| Int_private | 0.0009 | 0.0007 | 1.350 | 0.178 | |

| Age | 0.000039 | 0.000021 | 1.810 | 0.070 | |

| Bed | −0.0000016 | 0.0000015 | −1.080 | 0.282 | |

| Year | 2009 | −0.004 | 0.00026 | −13.670 | 0.000 |

| 2010 | −0.006 | 0.00026 | −24.880 | 0.000 | |

| 2011 | −0.008 | 0.00028 | −28.140 | 0.000 | |

| 2012 | −0.008 | 0.00029 | −28.520 | 0.000 | |

| Intercept | −0.041 | 0.043 | −0.960 | 0.337 | |

Appendix F

| Coefficient | SE | t-Value | p > |t| | ||

|---|---|---|---|---|---|

| Govt | 0.2547 | 0.1179 | 2.16 | 0.031 | |

| Govt_EV | 0.1147 | 0.0086 | 13.41 | 0.000 | |

| Credit | −0.0036 | 0.0036 | −0.99 | 0.324 | |

| Audit | −0.0297 | 0.0110 | −2.70 | 0.007 | |

| Private | −0.1220 | 0.0622 | −1.96 | 0.050 | |

| Ln_pay_count | −0.0128 | 0.0037 | −3.41 | 0.001 | |

| Int_govt | −0.0298 | 0.0136 | −2.19 | 0.029 | |

| Int_private | 0.0132 | 0.0072 | 1.84 | 0.065 | |

| Age | −0.0006 | 0.0002 | −2.51 | 0.012 | |

| Bed | −0.000058 | 0.000015 | −3.81 | 0.000 | |

| Year | 2009 | −0.0090 | 0.0026 | −3.46 | 0.001 |

| 2010 | −0.0048 | 0.0026 | −1.81 | 0.070 | |

| 2011 | −0.0037 | 0.0028 | −1.31 | 0.190 | |

| 2012 | −0.0097 | 0.0030 | −3.27 | 0.001 | |

| Intercept | 1.3501 | 0.4517 | 2.99 | 0.003 | |

Appendix G

| Coefficient | SE | t-Value | p > |t| | ||

|---|---|---|---|---|---|

| Govt | 0.5537 | 0.1384 | 4.00 | 0.000 | |

| Govt_EV | 0.0435 | 0.0100 | 4.33 | 0.000 | |

| Credit | −0.0021 | 0.0043 | −0.50 | 0.617 | |

| Audit | 0.0221 | 0.0129 | 1.71 | 0.088 | |

| Private | −0.1604 | 0.0730 | −2.20 | 0.028 | |

| Ln_pay_count | −0.0222 | 0.0044 | −5.06 | 0.000 | |

| Int_govt | −0.0611 | 0.0160 | −3.82 | 0.000 | |

| Int_private | 0.0175 | 0.0084 | 2.09 | 0.037 | |

| Age | −0.0008 | 0.0003 | −2.95 | 0.003 | |

| Bed | −0.000029 | 0.000018 | −1.64 | 0.101 | |

| Year | 2009 | −0.0119 | 0.0031 | −3.87 | 0.000 |

| 2010 | −0.0155 | 0.0031 | −5.01 | 0.000 | |

| 2011 | −0.0207 | 0.0033 | −6.27 | 0.000 | |

| 2012 | −0.0292 | 0.0035 | −8.37 | 0.000 | |

| Intercept | 1.9081 | 0.5295 | 3.60 | 0.000 | |

References

- Rosenau, P.V.; Linder, S.H. Two Decades of Research Comparing For-Profit and Nonprofit Health Provider Performance in the United States. Soc. Sci. Q. 2003, 84, 219–241. [Google Scholar] [CrossRef]

- Trivedi, A.N.; Grebla, R.C. Quality and equity of care in the veterans affairs health-care system and in Medicare advantage health plans. Med. Care 2011, 49, 560–568. [Google Scholar] [CrossRef] [PubMed]

- Anderson, S. Public, private, neither, both? Publicness theory and the analysis of healthcare organization. Soc. Sci. Med. 2012, 74, 313–322. [Google Scholar] [CrossRef]

- Anderson, S. The end of publicness? public and private healthcare organizations are alike in all important respects. Int. J. Public Priv. Healthc. Manag. Econ. 2013, 3, 44–61. [Google Scholar]

- Barbetta, G.P.; Turati, G.; Zago, A.M. Behavioral differences between public and private not-for-profit hospitals in the Italian national health service. Health Econ. 2007, 16, 75–96. [Google Scholar] [CrossRef] [PubMed]

- Herr, A.; Schmitz, H.; Augurzky, B. Profit efficiency and ownership of German hospitals. Health Econ. 2011, 20, 660–674. [Google Scholar] [CrossRef] [PubMed]

- Moulton, S. Putting together the publicness puzzle: A framework for realized publicness. Public Adm. Rev. 2009, 69, 889–900. [Google Scholar] [CrossRef]

- Brinkerhoff, D.W.; Brinkerhoff, J.M. Public–private partnerships: Perspectives on purposes, publicness, and good governance. Public Adm. Dev. 2011, 31, 2–14. [Google Scholar] [CrossRef]

- Cram, P.; Bayman, L.; Popescu, I.; Vaughan-Sarrazin, M.S.; Cai, X.; Rosenthal, G.E. Uncompensated care provided by for-profit, not-for-profit, and government owned hospitals. BMC Health Serv. Res. 2010, 10, 90. [Google Scholar] [CrossRef]

- Dalton, C.M.; Warren, P.L. Cost versus control: Understanding ownership through outsourcing in hospitals. J. Health Econ. 2016, 48, 1–15. [Google Scholar] [CrossRef]

- Hernández-Martínez, A.; Martínez-Galiano, J.M.; Rodríguez-Almagro, J.; Delgado-Rodríguez, M.; Gómez-Salgado, J. Evidence-based Birth Attendance in Spain: Private versus Public Centers. Int. J. Environ. Res. Public Health 2019, 16, 894. [Google Scholar] [CrossRef] [PubMed]

- Rocha de Almeida, R.; de Souza, C.; Ferreira, M.; Gama de Matos, D.; Monteiro Costa Pereira, L.; Batista Oliveira, V.; de Freitas Zanona, A. A Retrospective Study about the Differences in Cardiometabolic Risk Indicators and Level of Physical Activity in Bariatric Surgery Patients from Private vs. Public Units. Int. J. Environ. Res. Public Health 2019, 16, 4751. [Google Scholar] [CrossRef] [PubMed]

- Edwards, M.; Miller, J.D.; Schumacher, R. Classification of community hospitals by scope of service: Four indexes. Health Serv. Res. 1972, 7, 301. [Google Scholar] [PubMed]

- Scott, P.G.; Falcone, S. Comparing public and private organizations: An exploratory analysis of three frameworks. Am. Rev. Public Adm. 1998, 28, 126–145. [Google Scholar] [CrossRef]

- Murray, M.A. Comparing public and private management: An exploratory essay. Public Adm. Rev. 1975, 35, 364–371. [Google Scholar] [CrossRef]

- Rainey, H.G. Public agencies and private firms: Incentive structures, goals, and individual roles. Adm. Soc. 1983, 15, 207–242. [Google Scholar] [CrossRef]

- Perry, J.L.; Rainey, H.G. The public-private distinction in organization theory: A critique and research strategy. Acad. Manag. Rev. 1988, 13, 182–201. [Google Scholar] [CrossRef]

- Bozeman, B. What organization theorists and public policy researchers can learn from one another: Publicness theory as a case-in-point. Organ. Stud. 2013, 34, 169–188. [Google Scholar] [CrossRef]

- Heinrich, C.J.; Fournier, E. Dimensions of publicness and performance in substance abuse treatment organizations. J. Policy Anal. Manag. 2004, 23, 49–70. [Google Scholar] [CrossRef]

- Bozeman, B.; Bretschneider, S. The “publicness puzzle” in organization theory: A test of alternative explanations of differences between public and private organizations. J. Public Adm. Res. Theory 1994, 4, 197–224. [Google Scholar]

- Frank, R.G.; Salkever, D.S. Nonprofit organizations in the health sector. J. Econ. Perspect. 1994, 8, 129–144. [Google Scholar] [CrossRef] [PubMed]

- Tuckman, H.P. Competition, commercialization, and the evolution of nonprofit organizational structures. J. Policy Anal. Manag. J. Assoc. Public Policy Anal. Manag. 1998, 17, 175–194. [Google Scholar] [CrossRef]

- Brickley, J.A.; Van Horn, R.L. Managerial incentives in nonprofit organizations: Evidence from hospitals. J. Law Econ. 2002, 45, 227–249. [Google Scholar] [CrossRef]

- Wang, J.Y.; Probst, J.C.; Stoskopf, C.H.; Sanders, J.M.; Mc Tigue, J.F. Information asymmetry and performance tilting in hospitals: A national empirical study. Health Econ. 2011, 20, 1487–1506. [Google Scholar] [CrossRef] [PubMed]

- Govender, V.; Mooney, G. People’s policies for the health of the poor globally. Int. J. Health Plan. Manag. 2012, 27, e92–e103. [Google Scholar] [CrossRef] [PubMed]

- Barsanti, S.; Nuti, S. The equity lens in the health care performance evaluation system. Int. J. Health Plan. Manag. 2014, 29, e233–e246. [Google Scholar] [CrossRef] [PubMed]

- Norton, E.C.; Staiger, D.O. How Hospital Ownership Affects Access to Care for the Uninsured. RAND J. Econ. 1994, 25, 171–185. [Google Scholar] [CrossRef] [PubMed]

- Lewin, L.S.; Eckels, T.J.; Miller, L.B. Setting the record straight. New Engl. J. Med. 1988, 318, 1212–1215. [Google Scholar] [CrossRef]

- Nerlove, M. Essays in Panel Data Econometrics; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Mummolo, J.; Peterson, E. Improving the interpretation of fixed effects regression results. Political Sci. Res. Methods 2018, 6, 829–835. [Google Scholar] [CrossRef]

- Welch, E.W.; Wong, W. Effects of global pressures on public bureaucracy: Modeling a new theoretical framework. Adm. Soc. 2001, 33, 371–402. [Google Scholar] [CrossRef]

- Hvidman, U.; Andersen, S.C. Impact of performance management in public and private organizations. J. Public Adm. Res. Theory 2014, 24, 35–58. [Google Scholar] [CrossRef]

- Roh, C.Y.; Moon, M.J.; Jung, K.H. Decomposing Organizational Productivity Changes in Acute Care Hospitals in Tennessee, 2002–2006: A Malmquist Approach. Korean J. Policy Stud. 2013, 28, 29–49. [Google Scholar]

- Roh, C.Y.; Moon, M.J. Does Governance Affect Organizational Performance? Governance Structure and Hospital Performance in Tennessee. Korean J. Policy Stud. 2016, 31, 23–40. [Google Scholar]

- Hall, K.; Miller, R.; Millar, R. Public, private or neither? Analysing the publicness of health care social enterprises. Public Manag. Rev. 2016, 18, 539–557. [Google Scholar] [CrossRef]

- Jung, K.H. A Review of Contracting Out in the US Medicare HMOs: Theories and Hypotheses. Korean J. Policy Stud. 2005, 19, 73–97. [Google Scholar]

- Biancone, P.; Secinaro, S.; Brescia, V.; Calandra, D. Management of Open Innovation in Healthcare for Cost Accounting Using EHR. J. Open Innov. Technol. Mark. Complex. 2019, 5, 99. [Google Scholar] [CrossRef]

- Shin, C.; Park, J. Classifying Social Enterprises with Organizational Culture, Network and Socioeconomic Performance: Latent Profile Analysis Approach. J. Open Innov. Technol. Mark. Complex. 2019, 5, 17. [Google Scholar] [CrossRef]

- Roh, C.Y.; Kim, S. Medical innovation and social externality. J. Open Innov. Technol. Mark. Complex. 2017, 3, 3. [Google Scholar] [CrossRef]

| Dependent Variables | Independent Variables | ||

|---|---|---|---|

| Equity | Financial Equity | Publicness | Ownership (Government, nonprofit, private) Government evaluation Hospital accreditation Accounting audit |

| Social Equity | |||

| Overall Equity | Control variables | Number of medical payments Hospital age Number of hospital beds | |

| Financial Inequity (y1) | Social Equity (y2) | Overall Equity (y3) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Year | N | Mean | Median | SD | Mean | Median | SD | Mean | Median | SD |

| 2008 | 311 | 0.023 | 0.021 | 0.010 | 0.125 | 0.095 | 0.090 | 0.176 | 0.141 | 0.113 |

| 2009 | 312 | 0.019 | 0.018 | 0.008 | 0.114 | 0.087 | 0.087 | 0.161 | 0.127 | 0.116 |

| 2010 | 316 | 0.016 | 0.015 | 0.007 | 0.116 | 0.087 | 0.092 | 0.154 | 0.122 | 0.111 |

| 2011 | 319 | 0.014 | 0.013 | 0.006 | 0.114 | 0.088 | 0.086 | 0.146 | 0.117 | 0.100 |

| 2012 | 320 | 0.014 | 0.012 | 0.007 | 0.105 | 0.085 | 0.074 | 0.134 | 0.107 | 0.090 |

| Total | 1578 | 0.017 | 0.016 | 0.008 | 0.115 | 0.088 | 0.086 | 0.154 | 0.122 | 0.107 |

| Financial Inequity (y1) | Social Equity (y2) | Overall Equity (y3) | |||||

|---|---|---|---|---|---|---|---|

| N | Mean | Median | Mean | Median | Mean | Median | |

| Government Nonprofit | 159 | 0.01579 | 0.01507 | 0.1929 | 0.1773 | 0.2634 | 0.2486 |

| 1090 | 0.01575 | 0.01428 | 0.1101 | 0.0864 | 0.1442 | 0.1149 | |

| Private | 335 | 0.02197 | 0.02009 | 0.0916 | 0.0746 | 0.1348 | 0.1158 |

| Financial Inequity (y1) | Social Equity (y2) | Overall Equity (y3) | ||||||

|---|---|---|---|---|---|---|---|---|

| N | Mean | Median | Mean | Median | Mean | Median | ||

| Government Ownership | No | 1425 | 0.0172 | 0.0157 | 0.1058 | 0.0824 | 0.1420 | 0.1152 |

| Yes | 159 | 0.0158 | 0.0151 | 0.1929 | 0.1773 | 0.2634 | 0.2486 | |

| Govt_Ev | No | 1105 | 0.0187 | 0.0169 | 0.0975 | 0.0820 | 0.1422 | 0.1201 |

| Yes | 479 | 0.0134 | 0.0130 | 0.1539 | 0.1229 | 0.1818 | 0.1326 | |

| Government Ownership | Financial Inequity (y1) | Social Equity (y2) | Overall Equity (y3) | |||||

|---|---|---|---|---|---|---|---|---|

| Year | N | Mean | Median | Mean | Median | Mean | Median | |

| No | 2008 | 279 | 0.023 | 0.021 | 0.114 | 0.089 | 0.161 | 0.133 |

| 2009 | 279 | 0.019 | 0.018 | 0.105 | 0.081 | 0.149 | 0.120 | |

| 2010 | 284 | 0.016 | 0.015 | 0.107 | 0.082 | 0.142 | 0.115 | |

| 2011 | 288 | 0.014 | 0.013 | 0.106 | 0.084 | 0.135 | 0.112 | |

| 2012 | 289 | 0.014 | 0.012 | 0.096 | 0.078 | 0.123 | 0.102 | |

| Total | 1419 | 0.017 | 0.016 | 0.106 | 0.082 | 0.142 | 0.115 | |

| Yes | 2008 | 32 | 0.020 | 0.019 | 0.215 | 0.195 | 0.302 | 0.285 |

| 2009 | 33 | 0.017 | 0.017 | 0.188 | 0.174 | 0.265 | 0.242 | |

| 2010 | 32 | 0.014 | 0.014 | 0.190 | 0.176 | 0.263 | 0.245 | |

| 2011 | 31 | 0.014 | 0.014 | 0.187 | 0.171 | 0.251 | 0.226 | |

| 2012 | 31 | 0.013 | 0.013 | 0.184 | 0.174 | 0.234 | 0.204 | |

| Total | 159 | 0.016 | 0.015 | 0.193 | 0.177 | 0.263 | 0.249 | |

| Government Evaluation | Financial Inequity (y1) | Social Equity (y2) | Overall Equity (y3) | |||||

|---|---|---|---|---|---|---|---|---|

| Year | N | Mean | Median | Mean | Median | Mean | Median | |

| No | 2008 | 217 | 0.025 | 0.023 | 0.107 | 0.088 | 0.163 | 0.137 |

| 2009 | 216 | 0.020 | 0.019 | 0.096 | 0.080 | 0.147 | 0.124 | |

| 2010 | 219 | 0.017 | 0.016 | 0.096 | 0.079 | 0.141 | 0.119 | |

| 2011 | 222 | 0.016 | 0.014 | 0.094 | 0.081 | 0.135 | 0.117 | |

| 2012 | 226 | 0.015 | 0.013 | 0.094 | 0.080 | 0.126 | 0.106 | |

| Total | 1100 | 0.019 | 0.017 | 0.097 | 0.082 | 0.142 | 0.120 | |

| Yes | 2008 | 94 | 0.018 | 0.018 | 0.166 | 0.136 | 0.204 | 0.155 |

| 2009 | 96 | 0.015 | 0.015 | 0.156 | 0.128 | 0.194 | 0.141 | |

| 2010 | 97 | 0.013 | 0.013 | 0.160 | 0.126 | 0.185 | 0.131 | |

| 2011 | 97 | 0.011 | 0.011 | 0.158 | 0.125 | 0.171 | 0.119 | |

| 2012 | 94 | 0.011 | 0.010 | 0.130 | 0.098 | 0.155 | 0.113 | |

| Total | 478 | 0.013 | 0.013 | 0.154 | 0.123 | 0.182 | 0.133 | |

| Dependent Variable = y1 (Financial Inequity) | Coefficient | SE | t-Value | p > |t| | |

|---|---|---|---|---|---|

| Govt | −0.0393 | 0.0159 | −2.48 | 0.013 | |

| Govt_EV | −0.0022 | 0.0010 | −2.16 | 0.031 | |

| Credit | −0.0004 | 0.0004 | −1.10 | 0.270 | |

| Audit | 0.0044 | 0.0020 | 2.13 | 0.033 | |

| Private | −0.0236 | 0.0073 | −3.25 | 0.001 | |

| Ln_pay_count | −0.0027 | 0.0005 | −5.89 | <0.001 | |

| Int_govt | 0.0047 | 0.0018 | 2.68 | 0.007 | |

| Int_private | 0.0028 | 0.0008 | 3.43 | 0.001 | |

| Age | 0.0000604 | 0.0000386 | 1.56 | 0.118 | |

| Bed | 0.00000249 | 0.00000244 | 1.02 | 0.308 | |

| Year | 2009 | −0.0035 | 0.0003 | −13.61 | <0.001 |

| 2010 | −0.0065 | 0.0003 | −24.81 | <0.001 | |

| 2011 | −0.0077 | 0.0003 | −27.54 | <0.001 | |

| 2012 | −0.0083 | 0.0003 | −27.68 | <0.001 | |

| Intercept | −0.0750 | 0.0775 | −0.97 | 0.334 | |

| Dependent Variable = y2 (Social Equity) | Coefficient | SE | t-Value | p > |t| | |

|---|---|---|---|---|---|

| Govt | 0.5707 | 0.1579 | 3.62 | <0.001 | |

| Govt_Ev | 0.1508 | 0.0099 | 15.17 | <0.001 | |

| Credit | −0.0026 | 0.0036 | −0.73 | 0.463 | |

| Audit | −0.0560 | 0.0203 | −2.76 | 0.006 | |

| Private | 0.0104 | 0.0723 | 0.14 | 0.886 | |

| Ln_pay_count | 0.0066 | 0.0045 | 1.47 | 0.141 | |

| Int_govt | −0.0607 | 0.0175 | −3.48 | 0.001 | |

| Int_private | −0.0021 | 0.0080 | −0.27 | 0.791 | |

| Age | −0.00004 | 0.00038 | −0.10 | 0.919 | |

| Bed | −0.000042 | 0.000024 | −1.73 | 0.085 | |

| Year | 2009 | −0.0102 | 0.0025 | −4.02 | <0.001 |

| 2010 | −0.0066 | 0.0026 | −2.56 | 0.011 | |

| 2011 | −0.0065 | 0.0028 | −2.33 | 0.020 | |

| 2012 | −0.0130 | 0.0030 | −4.36 | <0.001 | |

| Intercept | 0.1174 | 0.7711 | 0.15 | 0.879 | |

| Dependent Variable = y3 (Overall Equity) | Coefficient | SE | t-Value | p > |t| | |

|---|---|---|---|---|---|

| Govt | 0.8453 | 0.1855 | 4.56 | <0.001 | |

| Govt_Ev | 0.0709 | 0.0117 | 6.07 | <0.001 | |

| Credit | −0.0004 | 0.0042 | −0.10 | 0.920 | |

| Audit | −0.0151 | 0.0239 | −0.63 | 0.526 | |

| Private | 0.0206 | 0.0849 | 0.24 | 0.808 | |

| Ln_pay_count | 0.0056 | 0.0053 | 1.06 | 0.290 | |

| Int_govt | −0.0943 | 0.0205 | −4.60 | <0.001 | |

| Int_private | −0.0027 | 0.0094 | −0.29 | 0.771 | |

| Age | −0.0006 | 0.0005 | −1.34 | 0.182 | |

| Bed | 0.000028 | 0.000029 | −0.97 | 0.330 | |

| Year | 2009 | −0.0133 | 0.0030 | −4.47 | <0.001 |

| 2010 | −0.0178 | 0.0031 | −5.83 | <0.001 | |

| 2011 | −0.0243 | 0.0033 | −7.40 | <0.001 | |

| 2012 | −0.0335 | 0.0035 | −9.57 | <0.001 | |

| Intercept | 1.3112 | 0.9063 | 1.45 | 0.148 | |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kang, Y.; Kim, M.; Jung, K. The Equity of Health Care Spending in South Korea: Testing the Impact of Publicness. Int. J. Environ. Res. Public Health 2020, 17, 1775. https://doi.org/10.3390/ijerph17051775

Kang Y, Kim M, Jung K. The Equity of Health Care Spending in South Korea: Testing the Impact of Publicness. International Journal of Environmental Research and Public Health. 2020; 17(5):1775. https://doi.org/10.3390/ijerph17051775

Chicago/Turabian StyleKang, Youngju, Minyoung Kim, and Kwangho Jung. 2020. "The Equity of Health Care Spending in South Korea: Testing the Impact of Publicness" International Journal of Environmental Research and Public Health 17, no. 5: 1775. https://doi.org/10.3390/ijerph17051775

APA StyleKang, Y., Kim, M., & Jung, K. (2020). The Equity of Health Care Spending in South Korea: Testing the Impact of Publicness. International Journal of Environmental Research and Public Health, 17(5), 1775. https://doi.org/10.3390/ijerph17051775