Natural Capital Accounting Informing Water Management Policies in Europe

Abstract

:1. Introduction

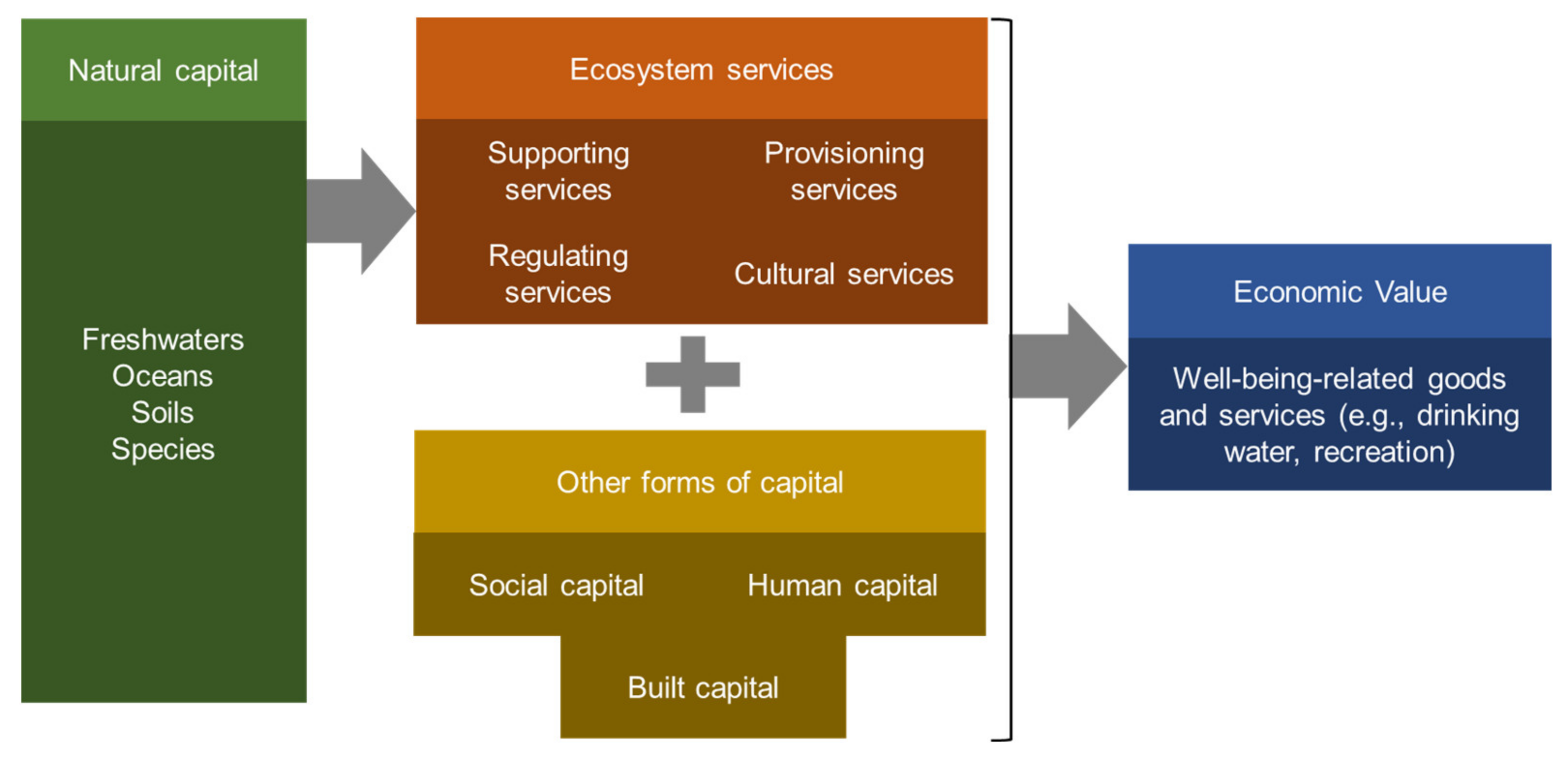

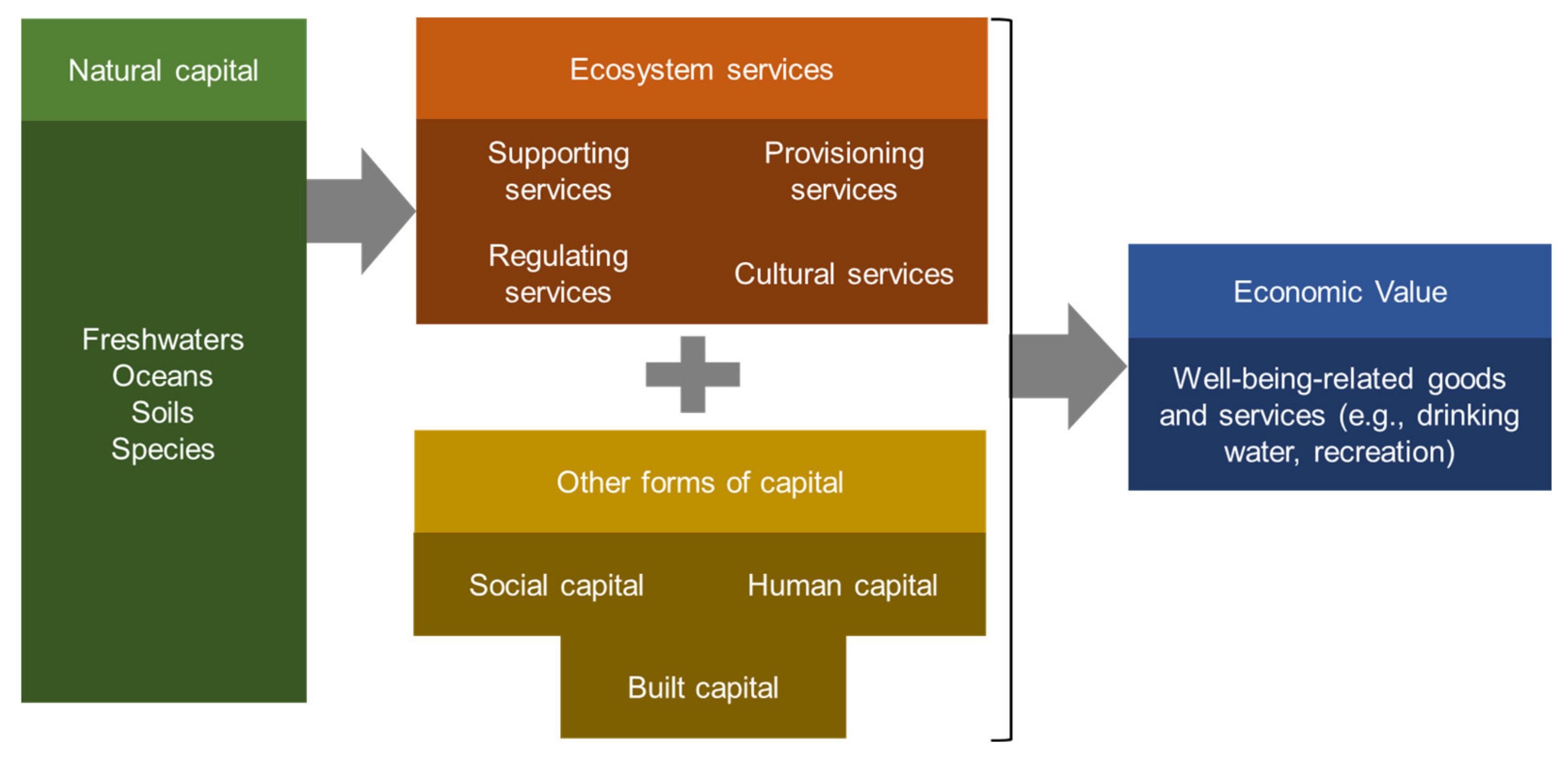

2. Natural Capital and the WFD

- By identifying the users and uses of water resources within each catchment area that will be impacted the most by the policy intervention;

- By assessing the trade-offs between different ecosystem uses;

- By establishing a common currency to allow for a comparison of changes within and between each asset of each ecosystem;

- By incorporating information from a natural capital assessment into a CBA or other appraisal techniques.

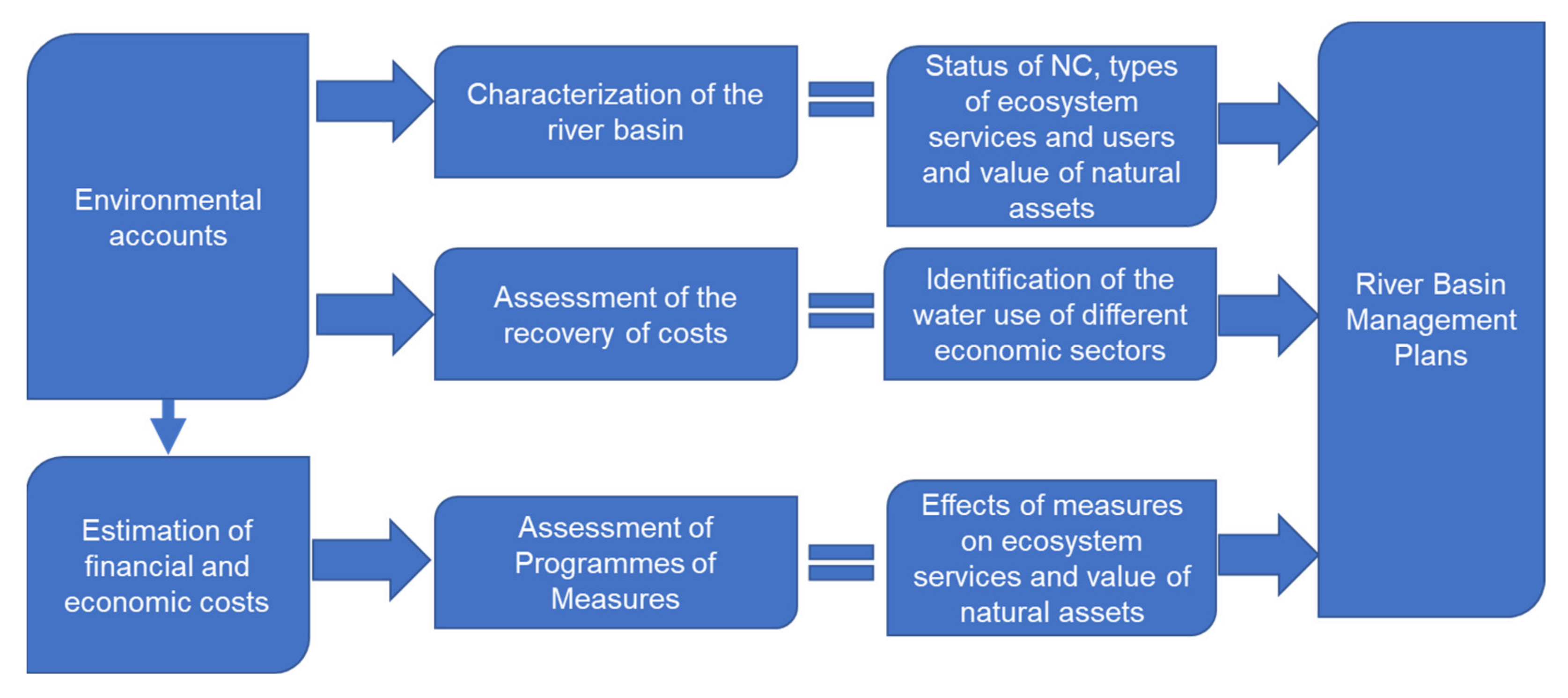

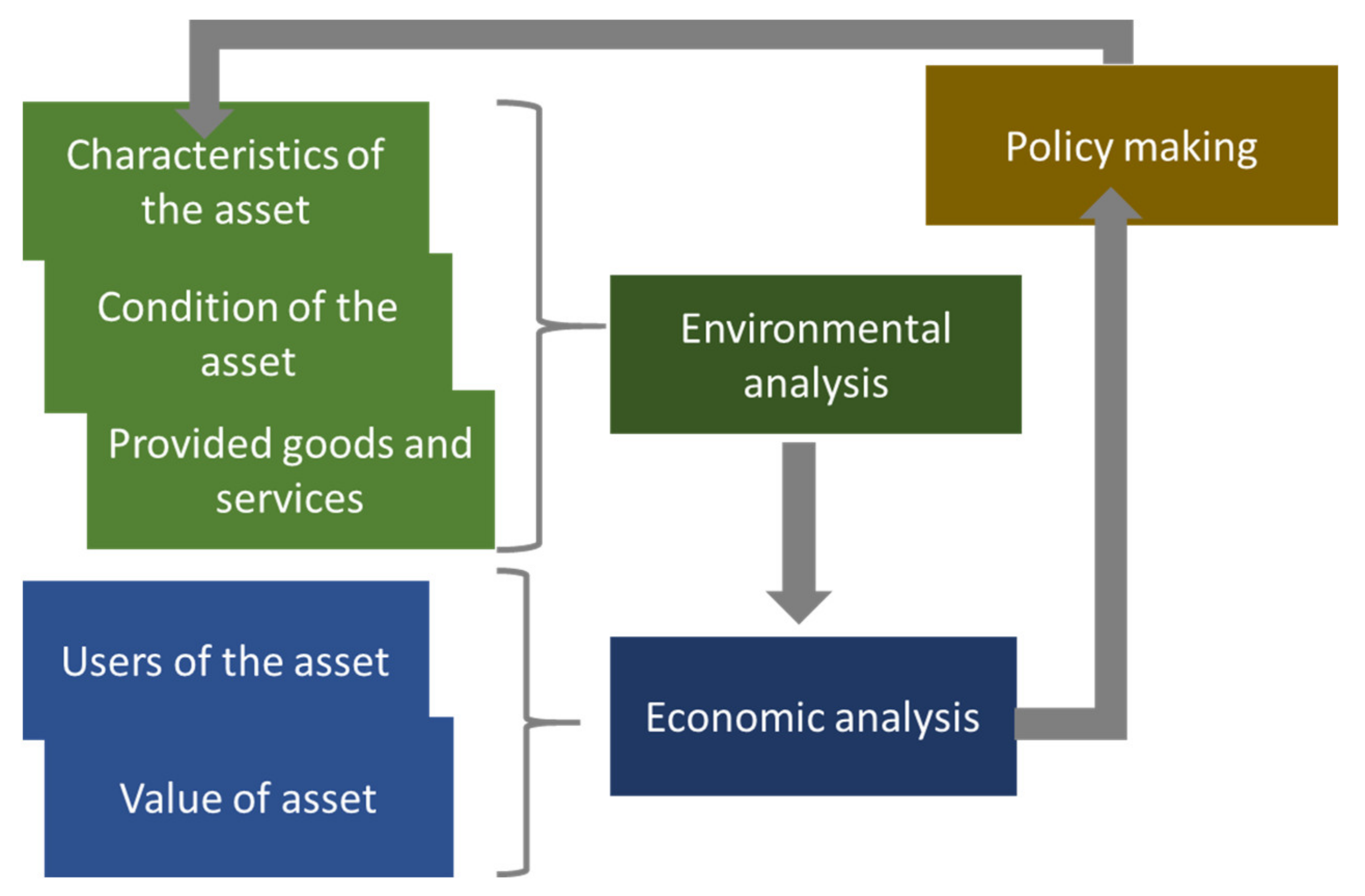

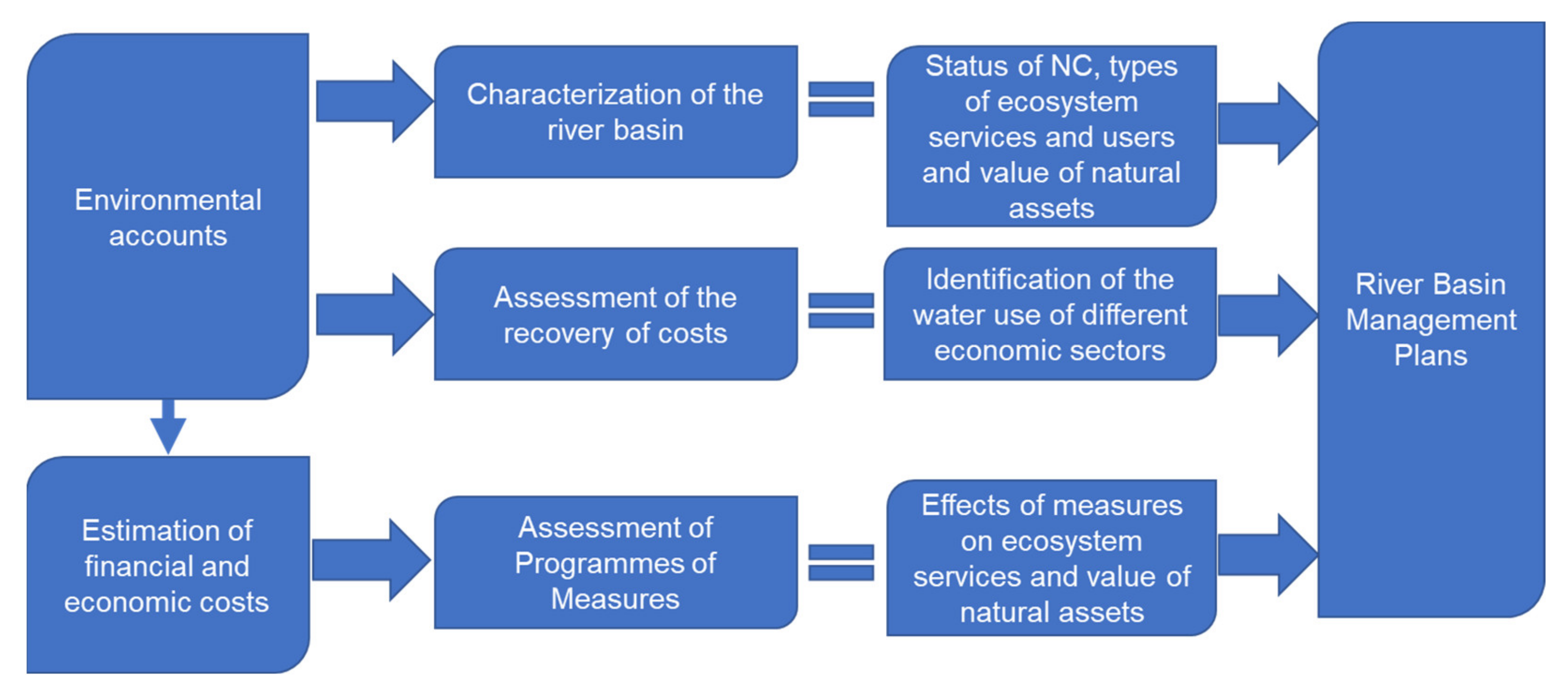

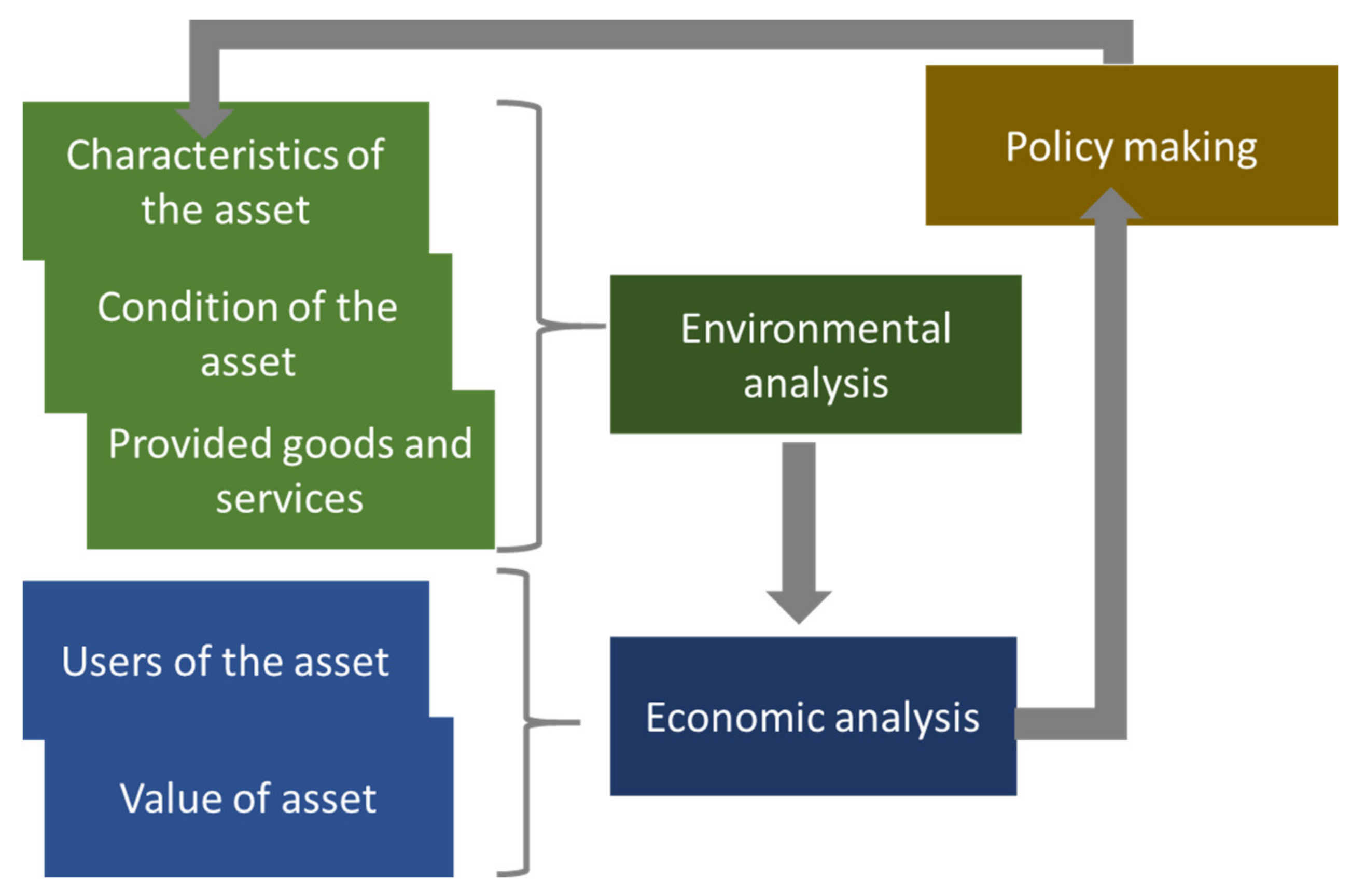

3. Assessing the Value of Natural Assets in Line with the WFD

- Step 1: Characteristics of the water body.

- Step 2: Condition of the asset.

- Step 3: Types of goods and services the asset provides to water users.

- Step 4: Value of the provided goods and services.

4. Materials and Methods

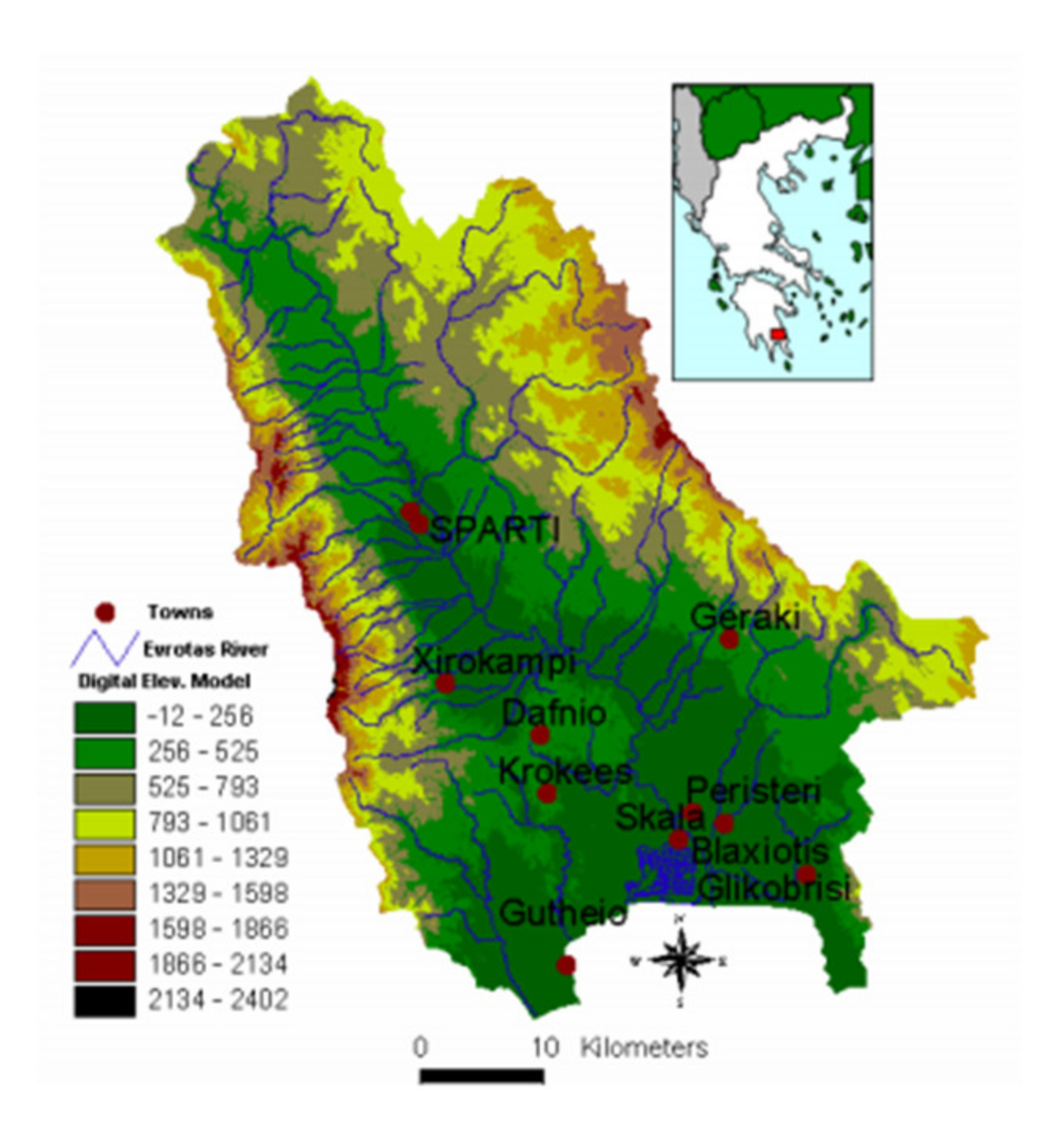

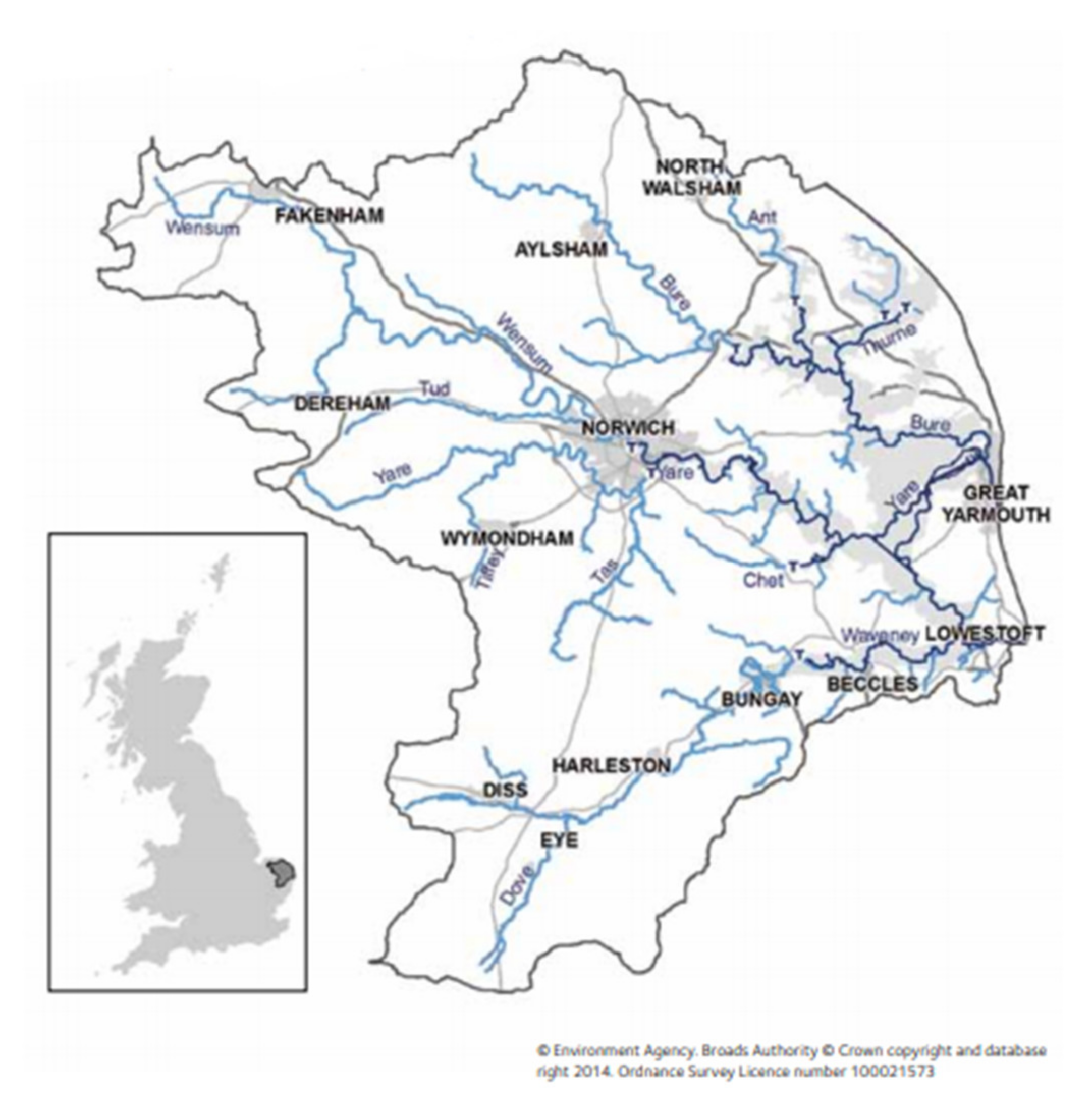

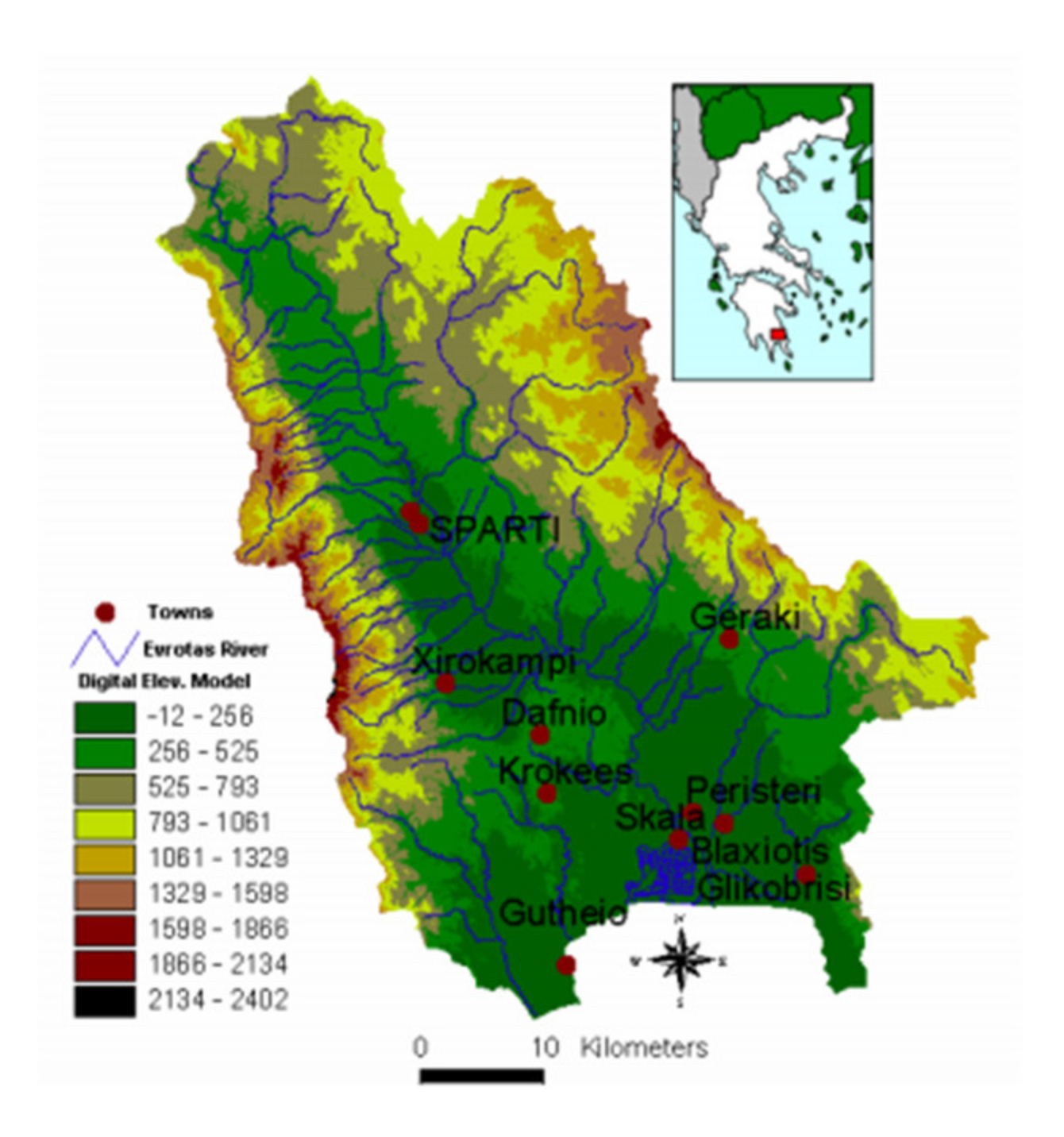

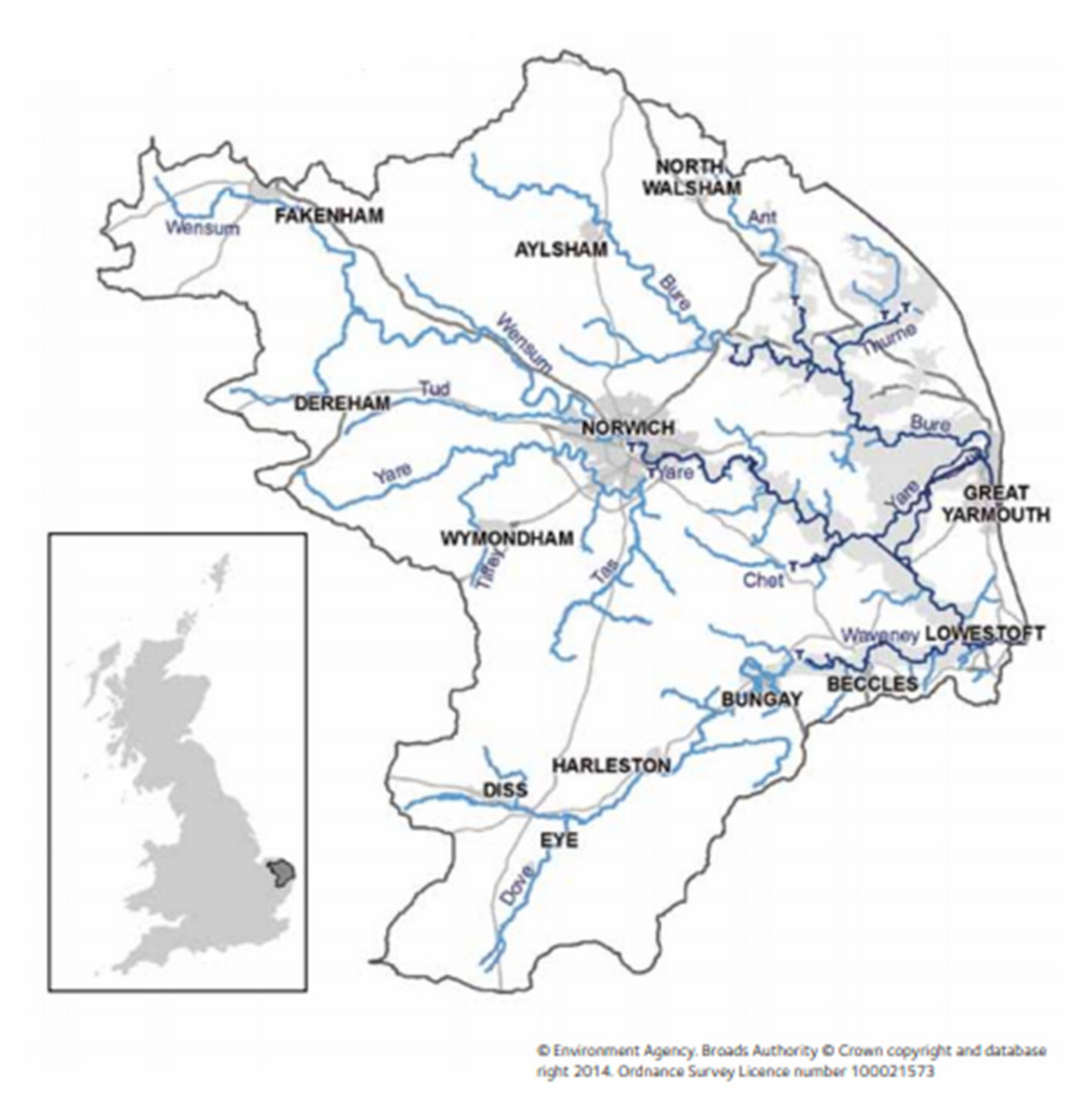

4.1. Description of Case Studies

4.2. Collection of Data

4.3. Estimation of the Value of Natural Capital

4.3.1. Water for Residential Use—Evrotas

4.3.2. Water for Residential Use—Broadland Rivers

4.3.3. Recreation—Evrotas

4.3.4. Recreation—Broadland Rivers

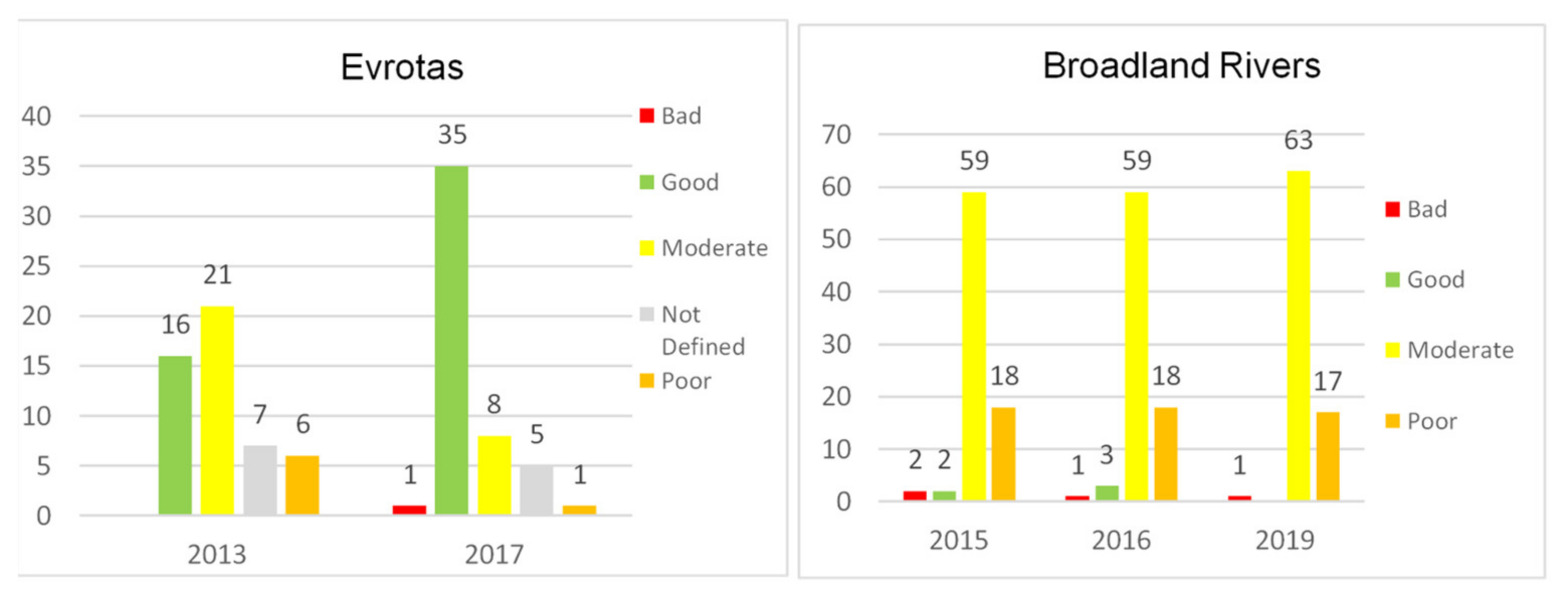

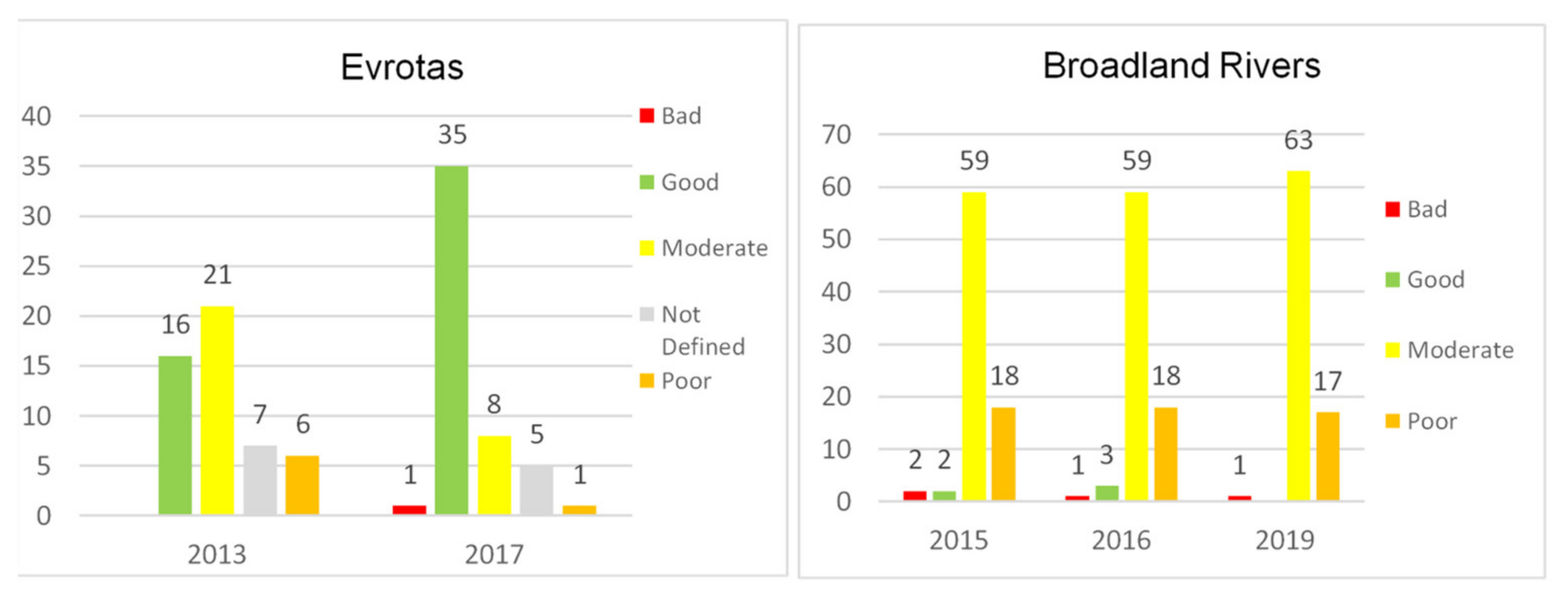

5. Results

6. Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ruijs, A.; Vardon, M.; Bass, S.; Ahlroth, S. Natural capital accounting for better policy. Ambio 2019, 48, 714–725. [Google Scholar] [CrossRef] [PubMed]

- Hasan, S.S.; Zhen, L.; Miah, M.G.; Ahamed, T.; Samie, A. Impact of land use change on ecosystem services: A review. Environ. Dev. 2020, 34, 100527. [Google Scholar] [CrossRef]

- Lu, Z.N.; Chen, H.; Hao, Y.; Wang, J.; Song, X.; Mok, T.M. The dynamic relationship between environmental pollution, economic development and public health: Evidence from China. J. Clean. Prod. 2017, 166, 134–147. [Google Scholar] [CrossRef]

- Jouanjean, M.-A.; Tucker, J.; Willem, D. Understanding the Effects of Resource Degradation on Socio-Economic Outcomes in Developing Countries; Overseas Development Institute: London, UK, 2014. [Google Scholar]

- Costanza, R.; Daly, H.E. Natural Capital and Sustainable Development. Conserv. Biol. 1992, 6, 37–46. [Google Scholar] [CrossRef]

- European Environment Agency. The European Environment—State and Outlook 2020. Knowledge for Transition to a Sustainable Europe; Publications Office of the European Union: Luxembourg, 2019. [Google Scholar] [CrossRef]

- Balvanera, P.; Quijas, S.; Karp, D.S.; Ash, N.; Bennett, E.M.; Boumans, R.; Brown, C.; Chan, K.M.A.; Chaplin-Kramer, R.; Halpern, B.S.; et al. Ecosystem Services. In The GEO Handbook on Biodiversity Observation Networks; Springer International Publishing: Cham, Switzerland, 2017; pp. 39–78. [Google Scholar]

- MEA. Ecosystems and Human Well-Being: Synthesi; Island Press: Washington, DC, USA, 2005; ISBN 1597260401. [Google Scholar]

- Barbier, E.B. Valuing ecosystem services as productive inputs. Econ. Policy 2007, 22, 177–229. [Google Scholar] [CrossRef]

- Fisher, B.; Turner, R. Ecosystem services: Classification for valuation. Biol. Conserv. 2008, 141, 1167–1169. [Google Scholar] [CrossRef]

- Koundouri, P.; Ker Rault, P.; Pergamalis, V.; Skianis, V.; Souliotis, I. Development of an integrated methodology for the sustainable environmental and socio-economic management of river ecosystems. Sci. Total Environ. 2015, 540, 90–100. [Google Scholar] [CrossRef] [Green Version]

- Liu, S.; Costanza, R.; Farber, S.; Troy, A. Valuing ecosystem services: Theory, practice, and the need for a transdisciplinary synthesis. Ann. N. Y. Acad. Sci. 2010, 1185, 54–78. [Google Scholar] [CrossRef]

- National Research Council. Valuing Ecosystem Services: Toward Better Environmental Decision-Making; National Academies Press: Washington, DC, USA, 2005. [Google Scholar] [CrossRef] [Green Version]

- Wallace, K. Classification of ecosystem services: Problems and solutions. Biol. Conserv. 2007, 139, 235–246. [Google Scholar] [CrossRef] [Green Version]

- Turner, R.K.; Morse-Jones, S.; Fisher, B. Ecosystem valuation: A sequential decision support system and quality assessment issues. Ann. N. Y. Acad. Sci. 2010, 1185, 79–101. [Google Scholar] [CrossRef]

- Robinson, D.A.; Hockley, N.; Reynolds, B. What are Ecosystem Services and Natural Capital, and how does this apply to Soil Science? In Proceedings of the 1st International Conference and Exploratory Workshop on Soil Architecture and Physico-Chemical Functions “CESAR”, Research Centre Foulum, Tjele, Denmark, 30 November–2 December 2010; National Environment Research Council: Swindon, UK, 2010. [Google Scholar]

- Pearce, D.; Markandya, A.; Barbier, E. Blueprint 1: For a Green Economy; Routledge: London, UK, 2013; ISBN 9781853830662. [Google Scholar]

- Petersen, J.E.; Desaulty, D.; Gelabert, E.R.; Zal, N. Natural Capital Accounting in Support of Policymaking in Europe: A Review Based on EEA Ecosystem Accounting Work; EEA Report 26/2018; Publications Office of the European Union: Luxembourg, 2019. [Google Scholar]

- Costanza, R.; D’Arge, R.; de Groot, R.; Farber, S.; Grasso, M.; Hannon, B.; Limburg, K.; Naeem, S.; O’neill, R.V.; Paruelo, J.; et al. The value of the world’s ecosystem services and natural capital. Nat. Wkly. J. Sci. 1997, 387, 253–260. [Google Scholar] [CrossRef]

- Costanza, R. Valuing natural capital and ecosystem services toward the goals of efficiency, fairness, and sustainability. Ecosyst. Serv. 2020, 43, 101096. [Google Scholar] [CrossRef]

- Smith, A.C.; Harrison, P.A.; Pérez Soba, M.; Archaux, F.; Blicharska, M.; Egoh, B.N.; Erős, T.; Fabrega Domenech, N.; György, I.; Haines-Young, R.; et al. How natural capital delivers ecosystem services: A typology derived from a systematic review. Ecosyst. Serv. 2017, 26, 111–126. [Google Scholar] [CrossRef] [Green Version]

- Badura, T.; Ferrini, S.; Agarwala, M.; Turner, R.K. Valuation for Natural Capital and Ecosystem Accounting—Synthesis Paper. Synthesis Report for the European Commission. Centre for Social and Economic Research on the Global Environment, University of East Anglia. Norwich 2017. Available online: https://ec.europa.eu/environment/nature/capital_accounting/pdf/Valuation_for_natural_capital_and_ecosystem_acounting.pdf (accessed on 9 October 2021).

- Bateman, I.J.; Mace, G.M. The natural capital framework for sustainably efficient and equitable decision making. Nat. Sustain. 2020, 3, 776–783. [Google Scholar] [CrossRef]

- Mace, G.M.; Hails, R.S.; Cryle, P.; Harlow, J.; Clarke, S.J. Towards a risk register for natural capital. J. Appl. Ecol. 2015, 52, 641–653. [Google Scholar] [CrossRef] [Green Version]

- Capitals Coalition. Integrating Biodiversity into Natural Capital Assessments. 2020. Available online: https://naturalcapitalcoalition.org/wp-content/uploads/2020/10/Biodiversity-Guidance_COMBINED_single-page.pdf (accessed on 9 October 2021).

- The World Economic Forum. The Global Risks Report 2021, 16th ed.; World Economic Forum: Geneva, Switzerland, 2021. [Google Scholar]

- UN—Statistics Division. SEEA Experimental Ecosystem Accounting. 2013. Available online: http://unstats.un.org/unsd/statcom/doc13/BG-SEEA-Ecosystem.pdf (accessed on 9 October 2021).

- Hein, L.; Bagstad, K.J.; Obst, C.; Edens, B.; Schenau, S.; Castillo, G.; Soulard, F.; Brown, C.; Driver, A.; Bordt, M.; et al. Progress in natural capital accounting for ecosystems. Science 2020, 367, 514–515. [Google Scholar] [CrossRef] [PubMed]

- DeWitt, T.H.; Berry, W.J.; Canfield, T.J.; Fulford, R.S.; Harwell, M.C.; Hoffman, J.C.; Johnston, J.M.; Newcomer-Johnson, T.A.; Ringold, P.L.; Russell, M.J.; et al. The Final Ecosystem Goods & Services (FEGS) Approach: A Beneficiary-Centric Method to Support Ecosystem-Based Management. Ecosyst. Manag. Ecosyst. Serv. Aquat. Biodivers. 2020, 127–145. [Google Scholar] [CrossRef]

- Russell, M.; Rhodes, C.; Van Houtven, G.; Sinha, P.; Warnell, K.; Harwell, M.C. Ecosystem-Based Management and Natural Capital Accounting. In Ecosystem-Based Management, Ecosystem Services and Aquatic Biodiversity; Springer: Cham, Switzerland, 2020; pp. 149–163. [Google Scholar] [CrossRef]

- EC Our life insurance, our natural capital: An EU biodiversity strategy to 2020. Commun. Comm. Eur. Parliam. Counc. Econ. Soc. Comm. Comm. Reg. 2011, 244, 16.

- European Union. Decision No 1386/2013/EU of the European Parliament and of the Council of 20 November 2013 on a General Union Environment Action Programme to 2020 “Living well, within the Limits of Our Planet”. 2013. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013D1386&rid=1 (accessed on 9 October 2021).

- European Commission. Proposal for a Decision of the European Parliament and of the Council on a General Union Environment Action Programme to 2030, COM (2020) 652 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1602781627860&uri=COM:2020:652avail:FIN (accessed on 9 October 2021).

- La Notte, A.; Vallecillo, S.; Polce, C.; Zulian, G.; Maes, J. Implementing an EU System of Accounting for Ecosystems and Their Services. 2017. Available online: https://publications.jrc.ec.europa.eu/repository/bitstream/JRC107150/jrc107150_jrc107150_jrc_report_ecosystem_services_accounts_final_pubsy.pdf (accessed on 9 October 2021).

- European Commission. Fitness Check of the Water Framework Directive and the Floods Directive; Publications Office of the European Union: Luxembourg, 2019; pp. 1–184. Available online: https://ec.europa.eu/ (accessed on 9 October 2021).

- Capriolo, A.; Boschetto, R.G.; Mascolo, R.A.; Balbi, S.; Villa, F. Biophysical and economic assessment of four ecosystem services for natural capital accounting in Italy. Ecosyst. Serv. 2020, 46, 101207. [Google Scholar] [CrossRef]

- Carvalho, L.; Mackay, E.B.; Cardoso, A.C.; Baattrup-Pedersen, A.; Birk, S.; Blackstock, K.L.; Borics, G.; Borja, A.; Feld, C.K.; Ferreira, M.T.; et al. Protecting and restoring Europe’s waters: An analysis of the future development needs of the Water Framework Directive. Sci. Total Environ. 2019, 658, 1228–1238. [Google Scholar] [CrossRef]

- Santos, J.I.; Vidal, T.; Gonçalves, F.J.M.; Castro, B.B.; Pereira, J.L. Challenges to water quality assessment in Europe—Is there scope for improvement of the current Water Framework Directive bioassessment scheme in rivers? Ecol. Indic. 2021, 121, 107030. [Google Scholar] [CrossRef]

- Josefsson, H.; Baaner, L. The Water Framework Directive—A Directive for the Twenty-First Century? J. Environ. Law 2011, 23, 463–486. [Google Scholar] [CrossRef]

- Moss, B. The Water Framework Directive: Total Envrionment or Political Compromise. Sci. Total Environ. 2008, 400, 32–41. [Google Scholar] [CrossRef]

- Berbel, J.; Expósito, A. Economic challenges for the EU Water Framework Directive reform and implementation. Eur. Plan. Stud. 2018, 26, 20–34. [Google Scholar] [CrossRef]

- Zingraff-Hamed, A.; Schröter, B.; Schaub, S.; Lepenies, R.; Stein, U.; Hüesker, F.; Meyer, C.; Schleyer, C.; Schmeier, S.; Pusch, M.T. Perception of bottlenecks in the implementation of the european water framework directive. Water Altern. 2020, 13, 458–483. [Google Scholar]

- Moss, T.; Bouleau, G.; Albiac, J.; Slavíkova, L. The EU water framework directive twenty years on: Introducing the special issue. Water Altern. 2020, 13, 446–457. [Google Scholar]

- Souliotis, I.; Voulvoulis, N. Incorporating Ecosystem Services in the Assessment of Water Framework Directive Programmes of Measures. Environ. Manag. 2021, 68, 38–52. [Google Scholar] [CrossRef] [PubMed]

- Bone, J.; Head, M.; Jones, D.T.; Barraclough, D.; Archer, M.; Scheib, C.; Flight, D.; Eggleton, P.; Voulvoulis, N. From chemical risk assessment to environmental quality management: The challenge for soil protection. Environ. Sci. Technol. 2011, 45, 104–110. [Google Scholar] [CrossRef] [PubMed]

- Giakoumis, T.; Voulvoulis, N. Progress with monitoring and assessment in the WFD implementation in five European river basins: Significant differences but similar problems. Eur. J. Environ. Sci. 2018, 8, 44–50. [Google Scholar] [CrossRef]

- Giakoumis, T.; Voulvoulis, N. The Transition of EU Water Policy Towards the Water Framework Directive’s Integrated River Basin Management Paradigm. Environ. Manag. 2018, 62, 819–831. [Google Scholar] [CrossRef] [Green Version]

- Giakoumis, T.; Voulvoulis, N. Water Framework Directive programmes of measures: Lessons from the 1st planning cycle of a catchment in England. Sci. Total Environ. 2019, 668, 903–916. [Google Scholar] [CrossRef]

- Kochskämper, E.; Newig, J. Water Policy and Governance in Transition: The EU Water Framework Directive. In Water Resilience; Springer: Cham, Switzerland, 2021; pp. 23–40. [Google Scholar] [CrossRef]

- Boeuf, B.; Fritsch, O. Studying the implementation of the Water Framework Directive in Europe: A meta-analysis of 89 journal articles. Ecol. Soc. 2016, 21. [Google Scholar] [CrossRef] [Green Version]

- Voulvoulis, N.; Arpon, K.D.; Giakoumis, T. The EU Water Framework Directive: From great expectations to problems with implementation. Sci. Total Environ. 2017, 575, 358–366. [Google Scholar] [CrossRef] [Green Version]

- Everard, M.; Colvin, J.D.; Mander, M.; Dickens, C.; Chimbuya, S. Integrated Catchment Value Systems. J. Water Resour. Prot. 2009, 1, 174–187. [Google Scholar] [CrossRef]

- Guerry, A.D.; Polasky, S.; Lubchenco, J.; Chaplin-Kramer, R.; Daily, G.C.; Griffin, R.; Ruckelshaus, M.; Bateman, I.J.; Duraiappah, A.; Elmqvist, T.; et al. Natural capital and ecosystem services informing decisions: From promise to practice. Proc. Natl. Acad. Sci. USA 2015, 112, 7348–7355. [Google Scholar] [CrossRef] [Green Version]

- Maes, J.; Fabrega, N.; Zulian, G.; Barbosa, A.; Vizcaino, P.; Ivits, E.; Polce, C.; Vandecasteele, I.; Rivero, I.M.; Guerra, C.; et al. Mapping and Assessment of Ecosystems and Their Services: Trends in Ecosystems and Ecosystem Services in the European Union between 2000 and 2010 Luxembourg; Publications Office of the European Union: Luxembourg, 2015. [Google Scholar] [CrossRef]

- Grizzetti, B.; Liquete, C.; Antunes, P.; Carvalho, L.; Geamănă, N.; Giucă, R.; Leone, M.; McConnell, S.; Preda, E.; Santos, R.; et al. Ecosystem services for water policy: Insights across Europe. Environ. Sci. Policy 2016, 66, 179–190. [Google Scholar] [CrossRef] [Green Version]

- Pistocchi, A.; Udias, A.; Grizzetti, B.; Gelati, E.; Koundouri, P.; Ludwig, R.; Papandreou, A.; Souliotis, I. An integrated assessment framework for the analysis of multiple pressures in aquatic ecosystems and the appraisal of management options. Sci. Total Environ. 2017, 575, 1477–1488. [Google Scholar] [CrossRef] [Green Version]

- Giakoumis, T.; Voulvoulis, N. A participatory ecosystems services approach for pressure prioritisation in support of the Water Framework Directive. Ecosyst. Serv. 2018, 34, 126–135. [Google Scholar] [CrossRef]

- Grizzetti, B.; Lanzanova, D.; Liquete, C.; Reynaud, A.; Cardoso, A.C. Assessing water ecosystem services for water resource management. Environ. Sci. Policy 2016, 61, 194–203. [Google Scholar] [CrossRef]

- Vlachopoulou, M.; Coughlin, D.; Forrow, D.; Kirk, S. The potential of using the ecosystem approach in the implementation of the EU Water Framework Directive. Sci. Total Environ. 2014, 470–471, 684–694. [Google Scholar] [CrossRef]

- Pacetti, T.; Castelli, G.; Bresci, E.; Caporali, E. Water Values: Participatory Water Ecosystem Services Assessment in the Arno River Basin, Italy. Water Resour. Manag. 2020, 34, 4527–4544. [Google Scholar] [CrossRef]

- Borrego-Marín, M.M.; Gutiérrez-Martín, C.; Berbel, J. Estimation of cost recovery ratio for water services based on the system of environmental-economic accounting for water. Water Resour. Manag. 2015, 30, 767–783. [Google Scholar] [CrossRef]

- Macháč, J.; Brabec, J.; Vojáček, O. Development and implementation of the concept of disproportionate costs in water management in central europe in the light of the EU WFD. Water Altern. 2020, 13, 618–633. [Google Scholar]

- Martin-Ortega, J.; Skuras, D.; Perni, A.; Holen, S.; Psaltopoulos, D. The disproportionality principle in the WFD: How to actually apply it? Econ. Water Manag. Agric. 2014, 214–256. [Google Scholar] [CrossRef]

- Martin-Ortega, J. Economic prescriptions and policy applications in the implementation of the European Water Framework Directive. Environ. Sci. Policy 2012, 24, 83–91. [Google Scholar] [CrossRef]

- Brouwer, R. The potential role of stated preference methods in the Water Framework Directive to assess disproportionate costs. J. Environ. Plan. Manag. 2008, 51, 597–614. [Google Scholar] [CrossRef]

- European Commission Economics and the Environment. The Implementation Challenge of the Water Framework Directive. A Guidance Document. WATECO Working Group Report; Office for Official Publications of the European Communities: Luxembourg, 2003. [Google Scholar]

- Obst, C.; Hein, L.; Edens, B. National Accounting and the Valuation of Ecosystem Assets and Their Services. Environ. Resour. Econ. 2016, 64, 1–23. [Google Scholar] [CrossRef]

- European Commission. Report on the implementation of the Water Framework Directive (2000/60/EC) and the Floods Directive (2007/60/EC) Second River Basin Management Plans First Flood Risk Management Plans. 2019. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:bee2c9d9-39d2-11e9-8d04-01aa75ed71a1.0005.02/DOC_1&format=PDF (accessed on 9 October 2021).

- Natural Capital Committee towards a Framework for Defining and Measuring Change in Natural Capital. 2014. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/516946/ncc-working-paper-measuring-framework.pdf (accessed on 9 October 2021).

- European Commission. Directive 2000/60/EC of the European Parliament and of the Council of 23 October 2000 Establishing a Framework for Community Action in the Field of Water Policy. Available online: https://eur-lex.europa.eu/eli/dir/2000/60/oj (accessed on 9 October 2021).

- Everard, M. Why does “good ecological status” matter? Water Environ. J. 2012, 26, 165–174. [Google Scholar] [CrossRef]

- Daily, G.C. Nature’s services: Societal dependence on natural ecosystems. Futur. Nat. Doc. Glob. Chang. 2013, 454–461. [Google Scholar] [CrossRef] [Green Version]

- De Groot, R.S.; Wilson, M.A.; Boumans, R.M. A typology for the classification, description and valuation of ecosystem functions, goods and services. Ecol. Econ. 2002, 41, 393–408. [Google Scholar] [CrossRef] [Green Version]

- Millennium Ecosystem Assessment. Ecosystems and Human Well-Being: A Framework for Assessment; Island Press: Washington, DC, USA, 2003; Volume 41. [Google Scholar]

- Pearce, D.; Atkinson, G.; Mourato, S. Cost-Benefit Analysis and the Environment: Recent Developments; Organisation for Economic Co-operation and Development: Paris, France, 2006. [Google Scholar]

- United Nations Statistics Division. System of Environmental-Economic Accounting for Water (SEEA-Water); United Nations Publications: New York, NY, USA, 2012. [Google Scholar]

- Freeman, A. The Measurement of Environmental and Resource Values: Theory and Methods; Routledge: London, UK, 2003. [Google Scholar] [CrossRef]

- Wilson, M.A.; Howarth, R.B. Discourse-based valuation of ecosystem services: Establishing fair outcomes through group deliberation. Ecol. Econ. 2002, 41, 431–443. [Google Scholar] [CrossRef]

- Fontaine, C.M.; De Vreese, R.; Jacquemin, I.; Marek, A.; Mortelmans, D.; Dendoncker, N.; Devillet, G.; Francois, L.; Van Herzele, A. Valuation of Terrestrial Ecosystem Services in a Multifunctional Peri-Urban Space: The VOTES Project; Final Report; Belgian Science Policy: Brussels, Belgium, 2013. [Google Scholar]

- Fontaine, C.M.; Dendoncker, N.; De Vreese, R.; Jacquemin, I.; Marek, A.; Van Herzele, A.; Devillet, G.; Mortelmans, D.; François, L. Towards participatory integrated valuation and modelling of ecosystem services under land-use change. J. Land Use Sci. 2014, 9, 278–303. [Google Scholar] [CrossRef]

- Dickie, I.; Neupauer, S. Natural capital accounts: Nations and organizations. J. Environ. Econ. Policy 2019, 8, 379–393. [Google Scholar] [CrossRef]

- Vardon, M.; Burnett, P.; Dovers, S. The accounting push and the policy pull: Balancing environment and economic decisions. Ecol. Econ. 2016, 124, 145–152. [Google Scholar] [CrossRef]

- Navarro-Ortega, A.; Acuña, V.; Bellin, A.; Burek, P.; Cassiani, G.; Choukr-Allah, R.; Dolédec, S.; Elosegi, A.; Ferrari, F.; Ginebreda, A.; et al. Managing the effects of multiple stressors on aquatic ecosystems under water scarcity. The GLOBAQUA project. Sci. Total Environ. 2015, 503–504, 3–9. [Google Scholar] [CrossRef] [Green Version]

- UK NEA. The UK National Ecosystem Assessment; United Nations Environment Programme World Conservation Monitoring Centre: Cambridge, UK, 2011. [Google Scholar]

- Maes, M.J.A.; Jones, K.E.; Toledano, M.B.; Milligan, B. Accounting for natural capital has cross-cutting relevance for UK public sector decision-making. Ecosyst. Serv. 2020, 44, 101127. [Google Scholar] [CrossRef]

- European Commission. The Environmental Implementation Review 2019. Country Report Greece; 2019. Available online: https://ec.europa.eu/environment/eir/pdf/report_el_en.pdf (accessed on 9 October 2021).

- Marinou, P.G.; Feloni, E.G.; Tzoraki, O.; Baltas, E.A. An implementation of a water balance model in the Evrotas basin. Eur. Water 2017, 57, 147–154. [Google Scholar]

- Querner, E.P.; Froebrich, J.; Gallart, F.; Cazemier, M.M.; Tzoraki, O. Simulating streamflow variability and aquatic states in temporary streams using a coupled groundwater-surface water model. Hydrol. Sci. J. 2016, 61, 146–161. [Google Scholar] [CrossRef]

- Karaouzas, I.; Theodoropoulos, C.; Vardakas, L.; Kalogianni, E.; Skoulikidis, N.T. A review of the effects of pollution and water scarcity on the stream biota of an intermittent Mediterranean basin. River Res. Appl. 2018, 34, 291–299. [Google Scholar] [CrossRef] [Green Version]

- Skoulikidis, N.T.; Vardakas, L.; Karaouzas, I.; Economou, A.N.; Dimitriou, E.; Zogaris, S. Assessing water stress in Mediterranean lotic systems: Insights from an artificially intermittent river in Greece. Aquat. Sci. 2011, 73, 581–597. [Google Scholar] [CrossRef]

- Environment Agency. The Broadland Rivers Management Catchment. A summary of Information about the Water Environment in the Broadland Rivers Management Catchment; Environment Agency: Bristol, UK, 2014. [Google Scholar]

- Environment Agency. The Broadland Rivers Management Catchment; Environment Agency: Bristol, UK, 2014. [Google Scholar]

- Ministry of Environment and Energy of Greece. 1st Update of River Basin Management Plan of the Eastern Peloponnese (EL03) 2016. Available online: http://wfdver.ypeka.gr/wp-content/uploads/2021/02/EL03_1REV_P22b_Perilipsi_E%CE%9D.pdf (accessed on 9 October 2021).

- EA Environment Agency—Catchment Data Explorer. Available online: https://environment.data.gov.uk/catchment-planning/OperationalCatchment/3336 (accessed on 5 August 2021).

- GLOBAQUA. GLOBAQUA Delverable 016. Final Integrated Models at the Basin Scale. 2018. Available online: http://www.globaqua-project.eu/files/repository/20190215120813_GLOBAQUAdeliverableD016(D9.16)FINAL.rar (accessed on 10 January 2021).

- Díaz-Cruz, M.S.; Molins-Delgado, D.; Serra-Roig, M.P.; Kalogianni, E.; Skoulikidis, N.T.; Barceló, D. Personal care products reconnaissance in EVROTAS river (Greece): Water-sediment partition and bioaccumulation in fish. Sci. Total Environ. 2019, 651, 3079–3089. [Google Scholar] [CrossRef] [PubMed]

- Lampou, A.; Skoulikidis, N.; Papadoulakis, V.; Vardakas, L. Evaluation of the Waters’ Condition in the Final Receiver of the Wastewater Treatment Plant in Municipality of Sparta. In Proceeding of the 11th Panhellenic Symposium on Oceanography and Fisheries, Lesvos, Greece, 13–17 May 2015. [Google Scholar]

- Huber García, V.; Meyer, S.; Kok, K.; Verweij, P.; Ludwig, R. Deriving spatially explicit water uses from land use change modelling results in four river basins across Europe. Sci. Total Environ. 2018, 628–629, 1079–1097. [Google Scholar] [CrossRef]

- Ministry of Environment and Energy of Greece Analysis of Human Pressures and Their Impacts on Surface Water and Groundwater Systems. Eastern Peloponesse River Basin (EL03). 2013. Available online: http://wfdver.ypeka.gr/wp-content/uploads/2017/04/files/GR03/GR03_P08_Pieseis.pdf (accessed on 9 October 2021).

- Environment Agency. Water Abstraction Licences Map. Available online: https://www.arcgis.com/home/item.html?id=fc92e5a3c298491aae8e566280f48d77 (accessed on 28 April 2021).

- Hotelling, H. An Economic Study of the Monetary Evaluation of Recreation in the National Parks; Department of the Interior, National Park Service and Recreational Planning Division: Washington, DC, USA, 1949; pp. 744–755. [Google Scholar]

- INSETE. Analysis of Inbound Tourism per Market and per Region; INSETE: Athens, Greece, 2019. [Google Scholar]

- Boutwell, J.; Westra, J. Benefit Transfer: A Review of Methodologies and Challenges. Resources 2013, 2, 517–527. [Google Scholar] [CrossRef] [Green Version]

- Latinopoulos, D. The impact of economic recession on outdoor recreation demand: An application of the travel cost method in Greece. J. Environ. Plan. Manag. 2014, 57, 254–272. [Google Scholar] [CrossRef]

- Clawson, M. Methods of Measuring the Demand for and Value of Outdoor Recreation; Resources for the Future: Washington, DC, USA, 1959. [Google Scholar]

- Whitehead, J.C.; Haab, T.C.; Huang, J.C. Measuring recreation benefits of quality improvements with revealed and stated behavior data. Resour. Energy Econ. 2000, 22, 339–354. [Google Scholar] [CrossRef] [Green Version]

- Navrud, S.; Ready, R. Valuing Cultural Heritage: Applying Environmental Valuation Techniques to Historic Buildings, Monuments and Artifacts; Edward Elgar Pub: Surrey, UK, 2002. [Google Scholar]

- Natural England. Monitor of Engagement with the Natural Environment. The National Survey on People and the Natural Environment. Technical Report to the 2009—2019 Surveys; 2019. Available online: http://publications.naturalengland.org.uk/file/5611620048044032 (accessed on 8 January 2021).

- EFTEC. Applying Values in Ecosystem Accounting; Department for Environment, Food and Rural Affairs: London, UK, 2015. Available online: http://sciencesearch.defra.gov.uk/Document.aspx?Document=13671_EcosystemAccountingDiscussionPaper_eftec_October2015.pdf (accessed on 9 October 2021).

- RAC. RAC cost of Motoring Index 2011; RAC: London, UK, 2011. [Google Scholar]

- RAC. RAC Cost of Motoring Index 2012; RAC: London, UK, 2012. [Google Scholar]

- RAC. RAC Cost of Motoring Index 2013; RAC: London, UK, 2013. [Google Scholar]

- Transport for London. Finance and Policy Committee- CHEI Report. 2014. Available online: https://www.london.gov.uk/about-us/londonassembly/meetings/documents/s37740/Annexe%20D%20-%20TfL%20Monitoring%20Report.pdf (accessed on 10 January 2021).

- Transport for London. Taxi Fares and Tariffs, and Taximeter Specification Review 2017. 2017. Available online: https://consultations.tfl.gov.uk/tph/taxi-fare-and-tariff-review-2017/user_uploads/taxi-fares-tariffs-taximeter-specification-consultation-report.pdf (accessed on 10 January 2021).

- Transport for London. Taxi Fares and Tariffs Review 2015. 2015. Available online: http://content.tfl.gov.uk/fpc-20150122-part-1-item08-taxi-fares-tariffs-2015.pdf (accessed on 10 January 2021).

- DfT Traffic Statistics. Table CGN0205b Average Vehicle Speeds during the Weekday Morning Peak on Locally Managed “A” Roads by Local Authority in England: Annual Averages from 2006/07. 2016. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/226963/cgn0205.xls (accessed on 9 October 2021).

- Railway Performance Society Fastest Times Listings. 2021. Available online: http://www.railperf.org.uk/fastmembers/6-MIDLANDS-EANG-2014.xls (accessed on 9 October 2021).

- Fezzi, C.; Bateman, I.J.; Ferrini, S. Using revealed preferences to estimate the value of travel time to recreation sites. J. Environ. Econ. Manag. 2014, 67, 58–70. [Google Scholar] [CrossRef]

- Parsons, G.R. The Travel Cost Model. Primer Nonmarket Valuat. 2003, 269–329. [Google Scholar] [CrossRef]

- Great Britain Day Visitor Survey. The Great Britain Day Visitor 2019 Annual Report. 2020. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/england_all_trips_2019.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2011. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/gb_tourist_2011_-_fv.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2012. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/gb_tourist_2012_-_30-08-2013_-_fv_tcm30-38527.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2013. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/gb_tourist_2013_v2.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2014. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/260121199_gb_tourist_report_2014_-_17th_sept_2015v2.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2015. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/gb_tourist_report_2015.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2016. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/260133160_gbts_2016_annual_report_hyperlinked_fv_v3.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2017. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/Documents-Library/documents/England-documents/40413193-260c_gb_tourist_2017_annual_report_v18.pdf (accessed on 10 January 2021).

- Visit Britain. The GB Tourist. 2018. Available online: https://www.visitbritain.org/sites/default/files/vb-corporate/40413193-260c_gb_tourist_annual_report_2018_fv-v3.pdf (accessed on 10 January 2021).

- Day, B.; Smith, G. Outdoor Recreation Valuation (ORVal) User Guide, Version 2.0; Land, Environment, Economics and Policy (LEEP) Insitutute, Business School, University of Exeter: Exeter, UK, 2016; pp. 1–24. [Google Scholar]

- SEEA EEA. SEEA Experimental Ecosystem Accounting: Technical Recommendations. 2017. Available online: https://seea.un.org/sites/seea.un.org/files/Presentations/Training_China_2017/seea_eea_tech_rec_final_v3.2_16oct2017.pdf (accessed on 10 January 2021).

- Turner, K.; Badura, T.; Ferrini, S. Valuation, Natural Capital Accounting and Decision-Support Systems: Process, Tools and Methods. 2019. Available online: https://ec.europa.eu/environment/nature/capital_accounting/pdf/EUNCA_SynthReport_4_2_CSERGE_Year2_190115_sent.pdf (accessed on 10 January 2021).

- ONS Natural Capital Accounts, UK—Office for National Statistics. Available online: https://www.ons.gov.uk/economy/environmentalaccounts/bulletins/uknaturalcapitalaccounts/2020#cultural-services (accessed on 10 May 2021).

- Dutton, A. UK Natural Capital Accounts Methodology Guide: 2020; Office for National Statistics: Newport, UK, 2020; pp. 1–18. Available online: https://www.ons.gov.uk/economy/environmentalaccounts/methodologies/uknaturalcapitalaccountsmethodologyguideoctober2019#asset-valuation (accessed on 5 September 2021).

- Allen, W.L., III. Environmental Reviews and Case Studies Advancing Green Infrastructure at All Scales: From Landscape to Site. Environ. Pract. 2021, 14, 17–25. [Google Scholar] [CrossRef]

- Mell, I. Global Green Infrastructure: Lessons for Successful Policy-Making, Investment and Management; Routledge: London, UK, 2016. [Google Scholar]

- Lovell, S.T.; Taylor, J.R. Supplying urban ecosystem services through multifunctional green infrastructure in the United States. Landsc. Ecol. 2013, 28, 1447–1463. [Google Scholar] [CrossRef]

- Ouyang, Z.; Zheng, H.; Xiao, Y.; Polasky, S.; Liu, J.; Xu, W.; Wang, Q.; Zhang, L.; Xiao, Y.; Rao, E.; et al. Improvements in ecosystem services from investments in natural capital. Science 2016, 352, 1455–1459. [Google Scholar] [CrossRef]

- Eurostat Water Exploitation Index, Plus (WEI+). Available online: https://ec.europa.eu/eurostat/databrowser/view/sdg_06_60/default/table?lang=en (accessed on 25 August 2021).

- Grizzetti, B.; Liquete, C.; Pistocchi, A.; Vigiak, O.; Zulian, G.; Bouraoui, F.; De Roo, A.; Cardoso, A.C. Relationship between ecological condition and ecosystem services in European rivers, lakes and coastal waters. Sci. Total Environ. 2019, 671, 452–465. [Google Scholar] [CrossRef]

- Bright, G.; Connors, E.; Grice, J. Measuring natural capital: Towards accounts for the UK and a basis for improved decision-making. Oxford Rev. Econ. Policy 2019, 35, 88–108. [Google Scholar] [CrossRef]

- Bass, S.; Ahlroth, S.; Ruijs, A.; Vardon, M. Natural Capital Accounting for Policy-a Global View of Achievements, Challenges and Prospects. In Forum on Natural Capital Accounting for Better Policy Decsions: Taking Stock and Moving Forward; World Bank WAVES: Washington, DC, USA, 2017. [Google Scholar]

- Plummer, R.; de Loë, R.; Armitage, D. A Systematic Review of Water Vulnerability Assessment Tools. Water Resour. Manag. 2012, 26, 4327–4346. [Google Scholar] [CrossRef] [Green Version]

- Gunda, T.; Benneyworth, L.; Burchfield, E. Exploring water indices and associated parameters: A case study approach. Water Policy 2015, 17, 98–111. [Google Scholar] [CrossRef] [Green Version]

- McKenna, T.; Blaney, R.; Brooker, R.W.; Ewing, D.A.; Pakeman, R.J.; Watkinson, P.; O’Brien, D. Scotland’s natural capital asset index: Tracking nature’s contribution to national wellbeing. Ecol. Indic. 2019, 107, 105645. [Google Scholar] [CrossRef]

- Hattam, C.; Atkins, J.P.; Beaumont, N.; Börger, T.; Böhnke-Henrichs, A.; Burdon, D.; De Groot, R.; Hoefnagel, E.; Nunes, P.A.L.D.; Piwowarczyk, J.; et al. Marine ecosystem services: Linking indicators to their classification. Ecol. Indic. 2015, 49, 61–75. [Google Scholar] [CrossRef]

- Hein, L.; Bagstad, K.; Edens, B.; Obst, C.; De Jong, R.; Lesschen, J.P. Defining ecosystem assets for natural capital accounting. PLoS ONE 2016, 11, e0164460. [Google Scholar] [CrossRef] [Green Version]

- Barbier, E.B. The concept of natural capital. Oxford Rev. Econ. Policy 2019, 35, 14–36. [Google Scholar] [CrossRef]

- Vardon, M.; Castaneda, J.P.; Nagy, M.; Schanau, S. How the System of Environmental-Economic Accounting can improve environmental information systems and data quality for decision making. Environ. Sci. Policy 2018, 89, 83–92. [Google Scholar] [CrossRef]

- Maechler, S.; Graz, J.-C. The Standardisation of Natural Capital Accounting Methodologies. In Shaping the Future through Standardization; IGI Global: Hershey, PA, USA, 2020; pp. 27–53. [Google Scholar]

- Maechler, S.; Furrer, E.; Lunghi, E.S.; Monthoux, M.; Yousefzai, C.; Graz, J.-C. Substituting risk for uncertainty. Where are the limits and how to face them? Les Cah. l’IEP/IEP Work. Pap. 2019, 73, 1–26. [Google Scholar]

- European Commission. The Added Value of Natural Capital Accounting for EU Policies. 2015. Available online: https://ec.europa.eu/environment/nature/capital_accounting/pdf/The%20Added%20Value%20of%20Natural%20Capital%20Accounting%20for%20EU%20policies.pdf (accessed on 10 January 2021).

- Dworak, T.; Gonzalez, C.; Laaser, C.; Interwies, E. The need for new monitoring tools to implement the WFD. Environ. Sci. Policy 2005, 8, 301–306. [Google Scholar] [CrossRef]

- Bennett, E.M.; Peterson, G.D.; Gordon, L.J. Understanding relationships among multiple ecosystem services. Ecol. Lett. 2009, 12, 1394–1404. [Google Scholar] [CrossRef] [PubMed]

- Oosterhuis, F. The Use of Water Accounts for Water Policy in the Netherlands. In Better Policy through Natural Capital Accounting; The World Bank: Washington, DC, USA, 2017; pp. 139–146. [Google Scholar]

- Nagy, M.; Peevor, S.; Vardon, M. Applying Natural Capital Accounting to Water Policy. In Better Policy through Natural Capital Accounting: Stocktake and Ways Forward; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Schenau, S. Measuring Green Growth for Environmental Economic Policies in the Netherlands. In Better Policy through Natural Capital Accounting: Stocktake and Ways Forward; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Mullin, K.; Mitchell, G.; Nawaz, N.R.; Waters, R.D. Natural capital and the poor in England: Towards an environmental justice analysis of ecosystem services in a high income country. Landsc. Urban Plan. 2018, 176, 10–21. [Google Scholar] [CrossRef]

- Fenichel, E.P.; Hashida, Y. Choices and the value of natural capital. Oxford Rev. Econ. Policy 2019, 35, 120–137. [Google Scholar] [CrossRef]

- Russi, D.; ten Brick, P. Natural Capital Accounting and Water Quality: Commitments, Benefits, Needs and Progress. A Briefing Note. The Economics of Ecosystems and Biodiversity (TEEB); United Nations Environment Programme: Geneva, Switzerland, 2013. [Google Scholar]

- European Commission. Report from the Commission to the European Parliament and the Council implementation of the Water Framework Directive (2000/60/EC) and the Floods Directive (2007/60/EC) Second River Basin Management Plans First Flood Risk Management Plans. 2019. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52019DC0095&from=GA (accessed on 10 January 2021).

- European Commission. Green Infrastructure (GI)—Enhancing Europe’s Natural Capital. 2013. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:52013DC0249&from=EN (accessed on 10 January 2021).

- Eggermont, H.; Balian, E.; Azevedo, J.M.N.; Beumer, V.; Brodin, T.; Claudet, J.; Fady, B.; Grube, M.; Keune, H.; Lamarque, P.; et al. Nature-based solutions: New influence for environmental management and research in Europe. GAIA 2015, 24, 243–248. [Google Scholar] [CrossRef]

- Maes, J.; Jacobs, S. Nature-Based Solutions for Europe’s Sustainable Development. Conserv. Lett. 2017, 10, 121–124. [Google Scholar] [CrossRef] [Green Version]

- EEA. Green Infrastructure and Flood Management: Promoting Cost-Efficient Flood Risk Reduction via Green Infrastructure Solutions; Publications Office of the European Union: Luxembourg, 2017. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|

| Flow (Mm3) | 6.3 | 6.3 | 6.4 | 6.5 | 6.5 | 6.6 | 6.7 |

| Value | 2.6 | 2.8 | 2.7 | 2.6 | 2.5 | 2.5 | 2.6 |

| Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|

| Annual flow (Mm3) | 71.10 | 71.41 | 72.30 | 76.27 | 74.97 | 77.83 | 148.67 |

| Annual value | 26.13 | 30.84 | 30.19 | 25.46 | 18.92 | 41.73 | 57.39 |

| Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

|---|---|---|---|---|---|---|---|

| Overnight stays | 184,100 | 188,850 | 193,723 | 198,721 | 203,100 | 203,367 | 203,634 |

| Estimated number of trips | 25,048 | 25,694 | 26,357 | 27,037 | 27,633 | 27,669 | 27,705 |

| Annual value | 4.79 | 4.91 | 5.04 | 5.17 | 5.29 | 5.29 | 5.3 |

| Negative Binomial Model | Poisson Model | |

|---|---|---|

| Variables | ||

| Constant | 1.347 *** | 1.371 *** |

| (0.0666) | (0.0411) | |

| Cost per visit | −0.014 *** | −0.017 *** |

| (0.0035) | (0.0028) | |

| AIC: 989.27 | AIC: 1158.3 | |

| ‘log Lik.’ −491.636 | ‘log Lik.’ −577.1431 |

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|

| Number of visitors (thousands) | 954 | 725 | 900 | 700 | 583 | 1053 | 690 | 594 | 940 |

| Annual value (Poisson model) | 55.3 | 42 | 52.2 | 40.6 | 33.8 | 61.1 | 40 | 34.4 | 54.5 |

| Annual value (Negative Binomial model) | 66.1 | 50.2 | 62.4 | 48.5 | 40.3 | 73 | 47.8 | 41.1 | 65.1 |

| Catchment | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Water for residential use | Evrotas | 73 | 68 | 71 | 67 | 60 | 68 | 73 | ||

| Broadland Rivers | 763 | 817 | 829 | 807 | 765 | 840 | 937 | |||

| Recreation | Evrotas | 136 | 128 | 135 | 130 | 118 | 134 | 144 | ||

| Broadland Rivers (Poisson model) | 1491 | 1347 | 1379 | 1322 | 1263 | 1341 | 1300 | 1267 | 1306 | |

| Broadland Rivers (Negative Binomial model) | 1866 | 1609 | 1647 | 1580 | 1510 | 1602 | 1554 | 1514 | 1561 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Souliotis, I.; Voulvoulis, N. Natural Capital Accounting Informing Water Management Policies in Europe. Sustainability 2021, 13, 11205. https://doi.org/10.3390/su132011205

Souliotis I, Voulvoulis N. Natural Capital Accounting Informing Water Management Policies in Europe. Sustainability. 2021; 13(20):11205. https://doi.org/10.3390/su132011205

Chicago/Turabian StyleSouliotis, Ioannis, and Nikolaos Voulvoulis. 2021. "Natural Capital Accounting Informing Water Management Policies in Europe" Sustainability 13, no. 20: 11205. https://doi.org/10.3390/su132011205

APA StyleSouliotis, I., & Voulvoulis, N. (2021). Natural Capital Accounting Informing Water Management Policies in Europe. Sustainability, 13(20), 11205. https://doi.org/10.3390/su132011205