Research on the Tail Risk Spillover Effect of Cryptocurrencies and Energy Market Based on Complex Network

Abstract

1. Introduction

2. Literature Review

2.1. Research on Risk Contagion Between Cryptocurrency and Energy Market

2.2. Research on Tail Risk Spillover Model

2.3. Complex Network Method and Network Topology Index Construction

2.4. Research on the Spatial Spillover Effect of the Energy Market

3. Theoretical Model

3.1. Leptokurtic Stochastic Volatility Model

3.2. Quantile Time–Frequency Spillover Network

3.3. Network Influencing Factors of Tail Risk Spillover

4. Empirical Analysis

4.1. Data

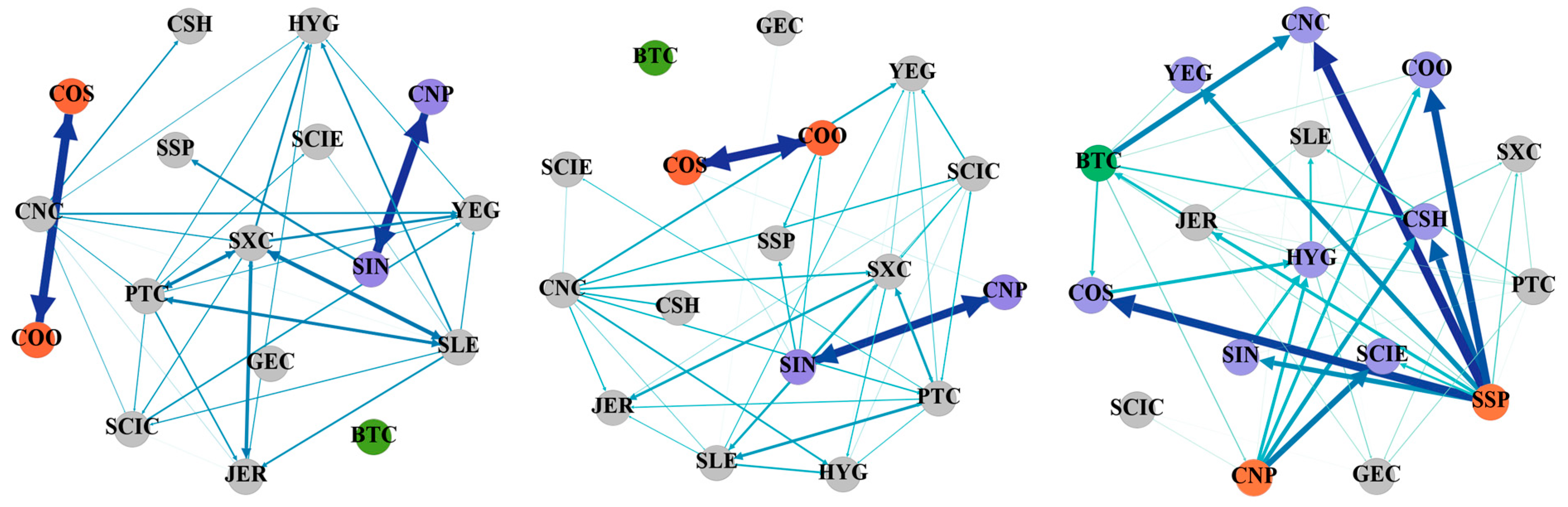

4.2. The Static Spillover Effect of Tail Risk in Cryptocurrency and Energy Market

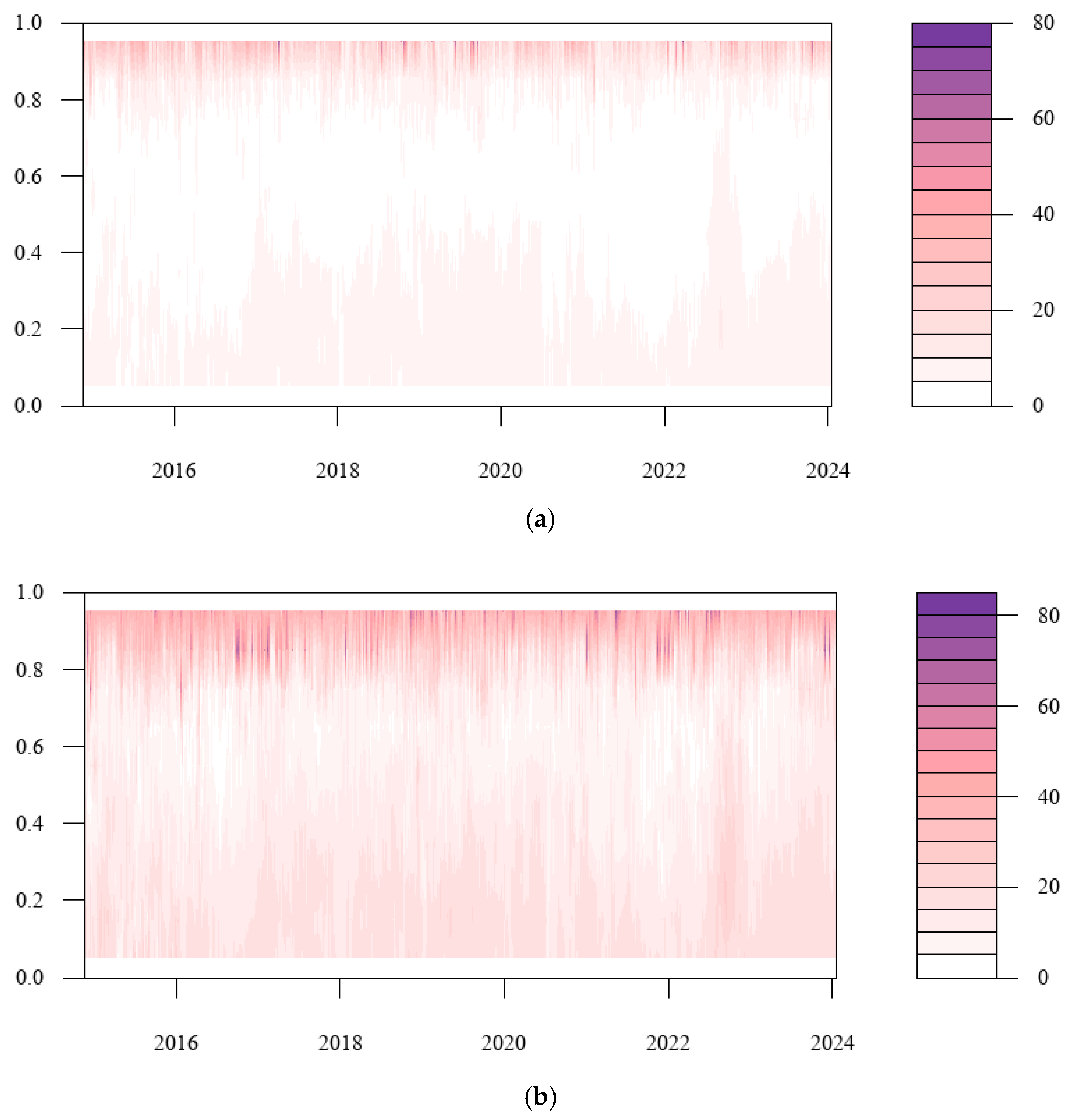

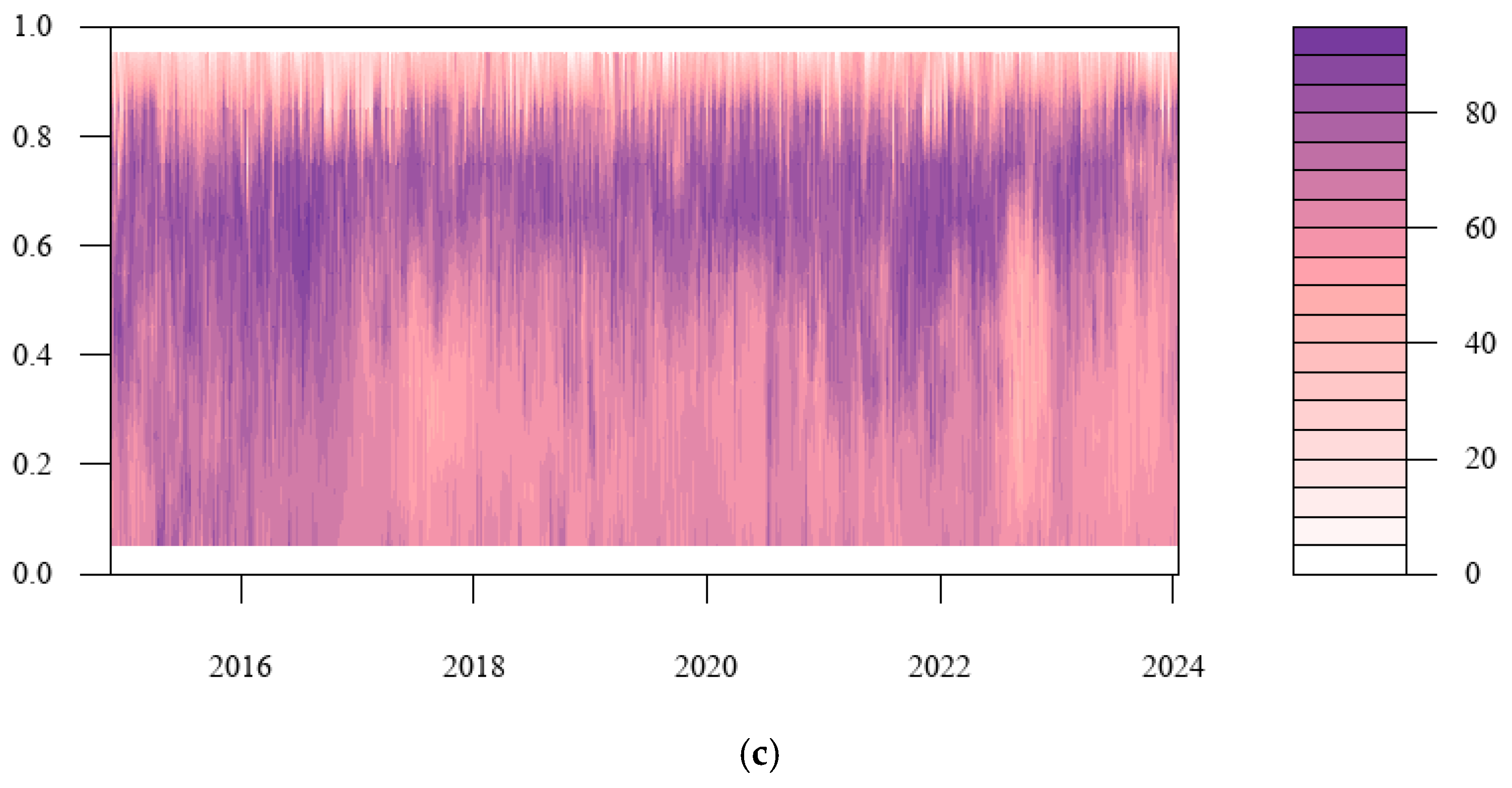

4.3. Dynamic Spillover Effect of Tail Risk Between Cryptocurrency and Energy Market

4.3.1. Total Spillover Effect of Tail Risk Between Cryptocurrency and Energy Market

4.3.2. The Net Spillover Effect of Tail Risks Between Cryptocurrency and China’s Energy Market

4.4. Spatial Spillover Effects and Network Influencing Factors of Tail Risks in Energy Market

5. Conclusions and Suggestions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Descriptive Statistics

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | Minimum | Maximum | Variance | Skewness | Kurtosis | Jarque-Bera |

|---|---|---|---|---|---|---|---|

| CNP | −0.000027 | −0.105244 | 0.095636 | 0.000300 | 0.046049 | 7.296687 | 5415.206 |

| CSH | 0.000353 | −0.142997 | 0.095487 | 0.000474 | −0.371965 | 6.188202 | 3950.9369 |

| SIN | 0.000060 | −0.105807 | 0.095630 | 0.000277 | −0.353348 | 6.942405 | 4952.237 |

| SCIC | 0.000660 | −0.124568 | 0.095993 | 0.000742 | −0.224247 | 2.873445 | 860.9597 |

| YEG | 0.000432 | −0.591336 | 0.095864 | 0.001120 | −2.327731 | 41.168308 | 174,459.6079 |

| CNC | 0.000371 | −0.107631 | 0.095891 | 0.000649 | −0.201124 | 4.274696 | 1875.5766 |

| COS | −0.000157 | −0.105631 | 0.095737 | 0.000663 | −0.108174 | 3.375334 | 1164.249 |

| GEC | 0.000017 | −0.113759 | 0.096159 | 0.000641 | −0.142312 | 3.749895 | 1439.1314 |

| SLE | 0.000362 | −0.245087 | 0.096026 | 0.000873 | −0.349495 | 4.012301 | 1687.6606 |

| SXC | 0.000215 | −0.291028 | 0.096100 | 0.000887 | −0.431423 | 6.021678 | 3763.6358 |

| HYG | 0.000178 | −0.476967 | 0.096100 | 0.000898 | −1.71198 | 28.053193 | 81,182.1093 |

| SSP | −0.000036 | −0.105956 | 0.096522 | 0.000556 | −0.051379 | 5.868337 | 3503.7159 |

| SCIE | 0.000565 | −0.181092 | 0.096627 | 0.001117 | −0.155580 | 2.106496 | 461.8347 |

| COO | −0.000146 | −0.105770 | 0.096074 | 0.000550 | −0.294255 | 4.622766 | 2209.225 |

| PTC | 0.000384 | −0.124313 | 0.096163 | 0.000827 | −0.200230 | 2.875170 | 857.8261 |

| JER | 0.000042 | −0.291108 | 0.095952 | 0.000780 | −0.639923 | 8.073070 | 6793.8023 |

| BTC | 0.001550 | −0.848829 | 1.474180 | 0.003496 | 4.700465 | 180.342682 | 3,314,272.4956 |

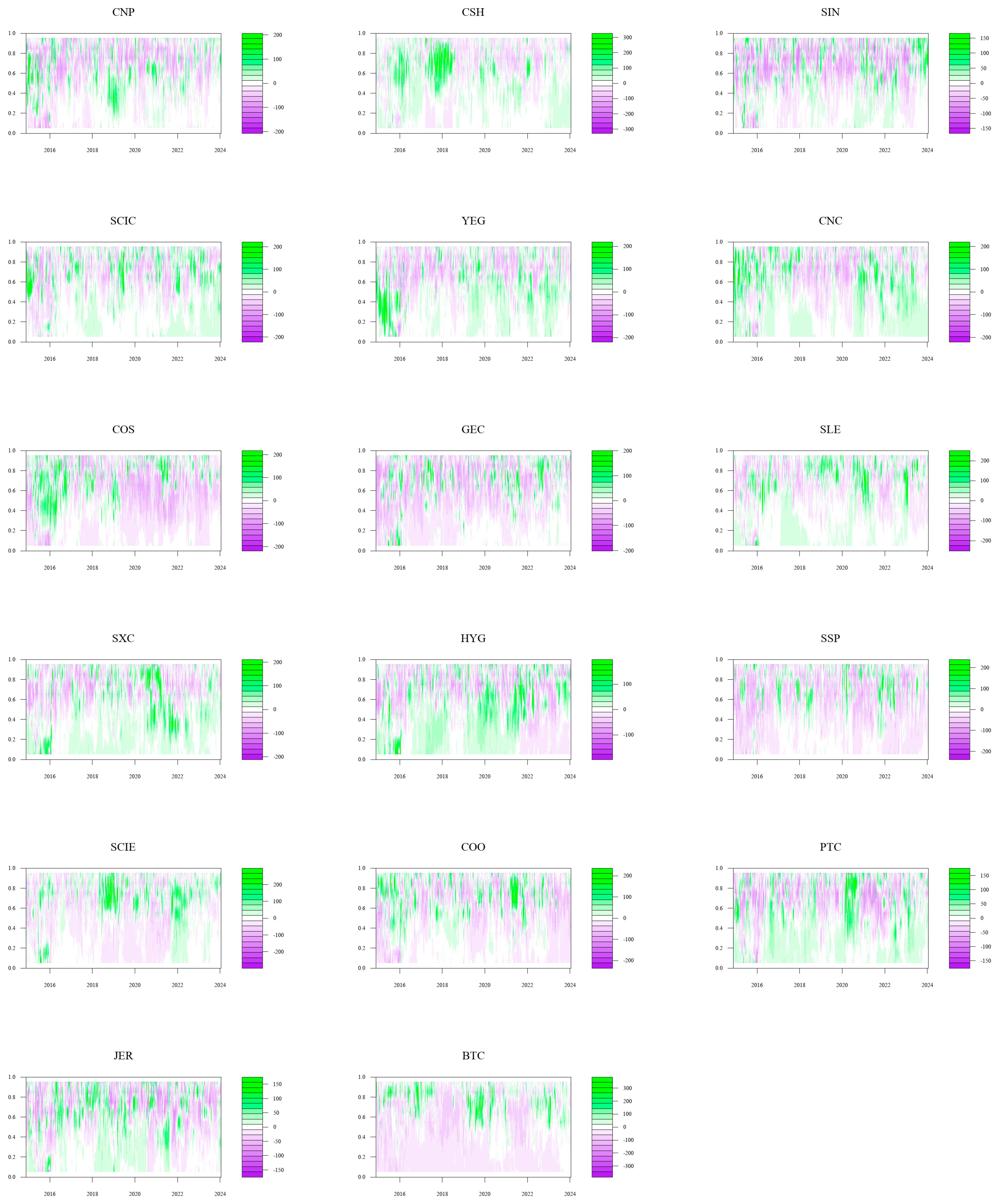

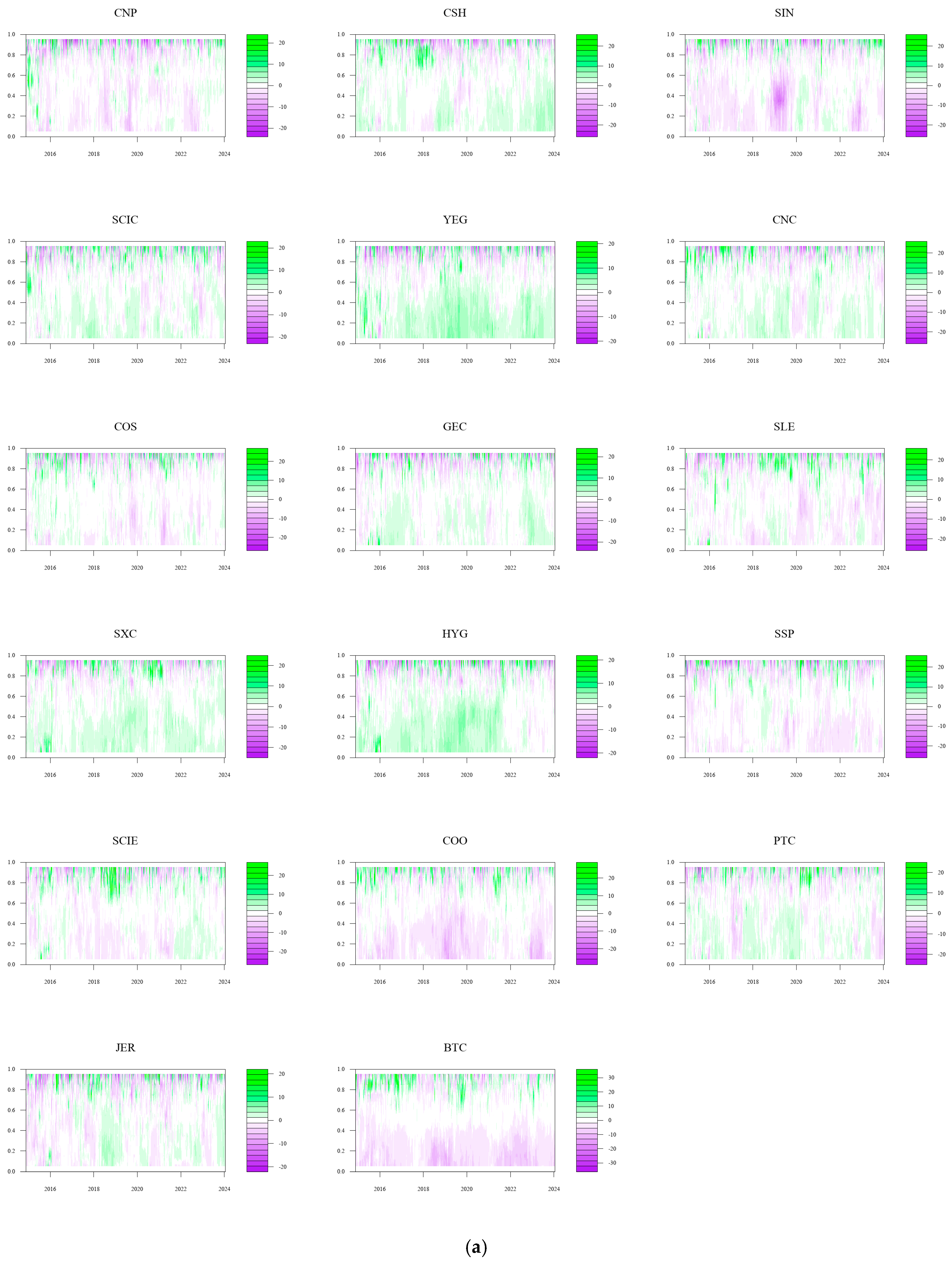

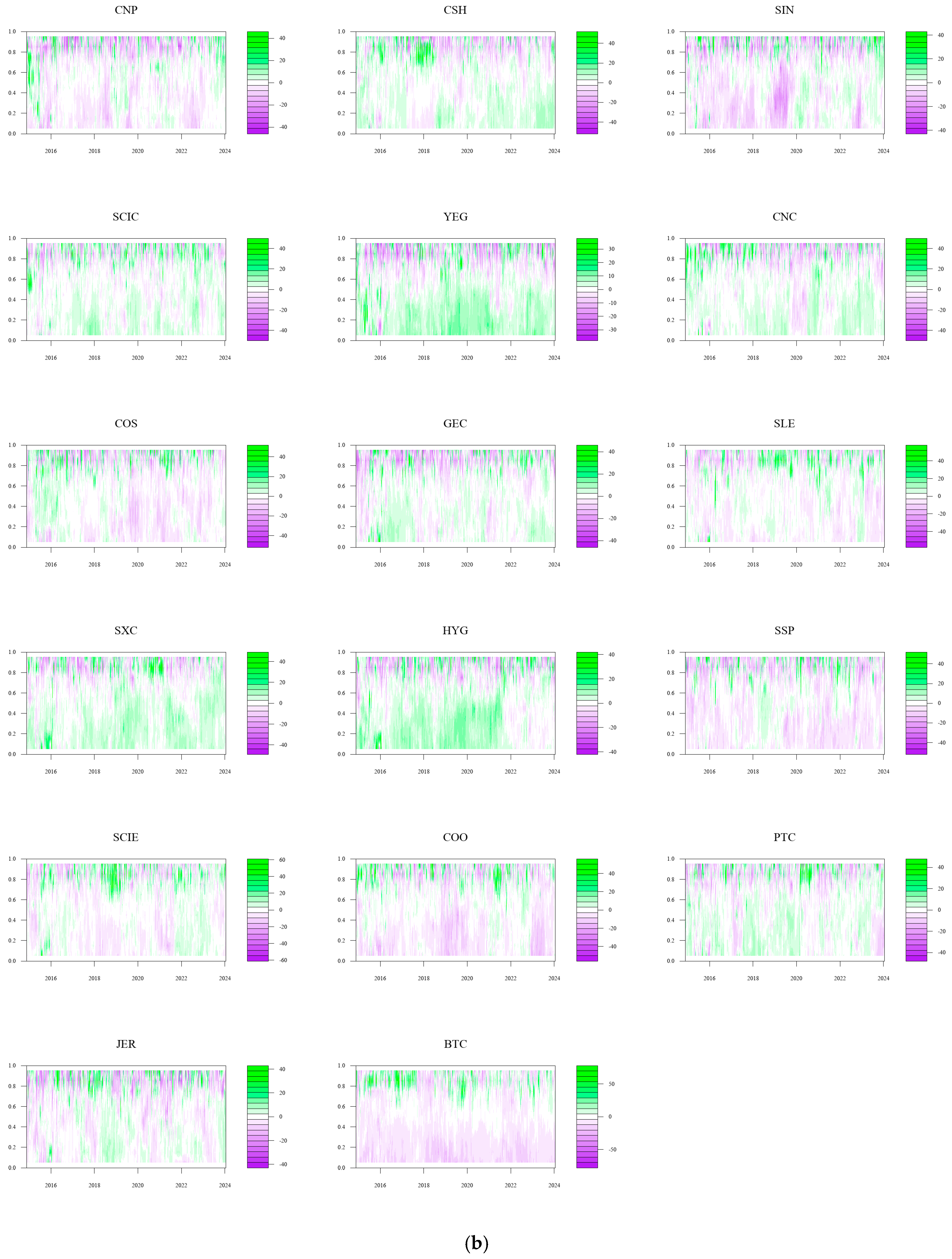

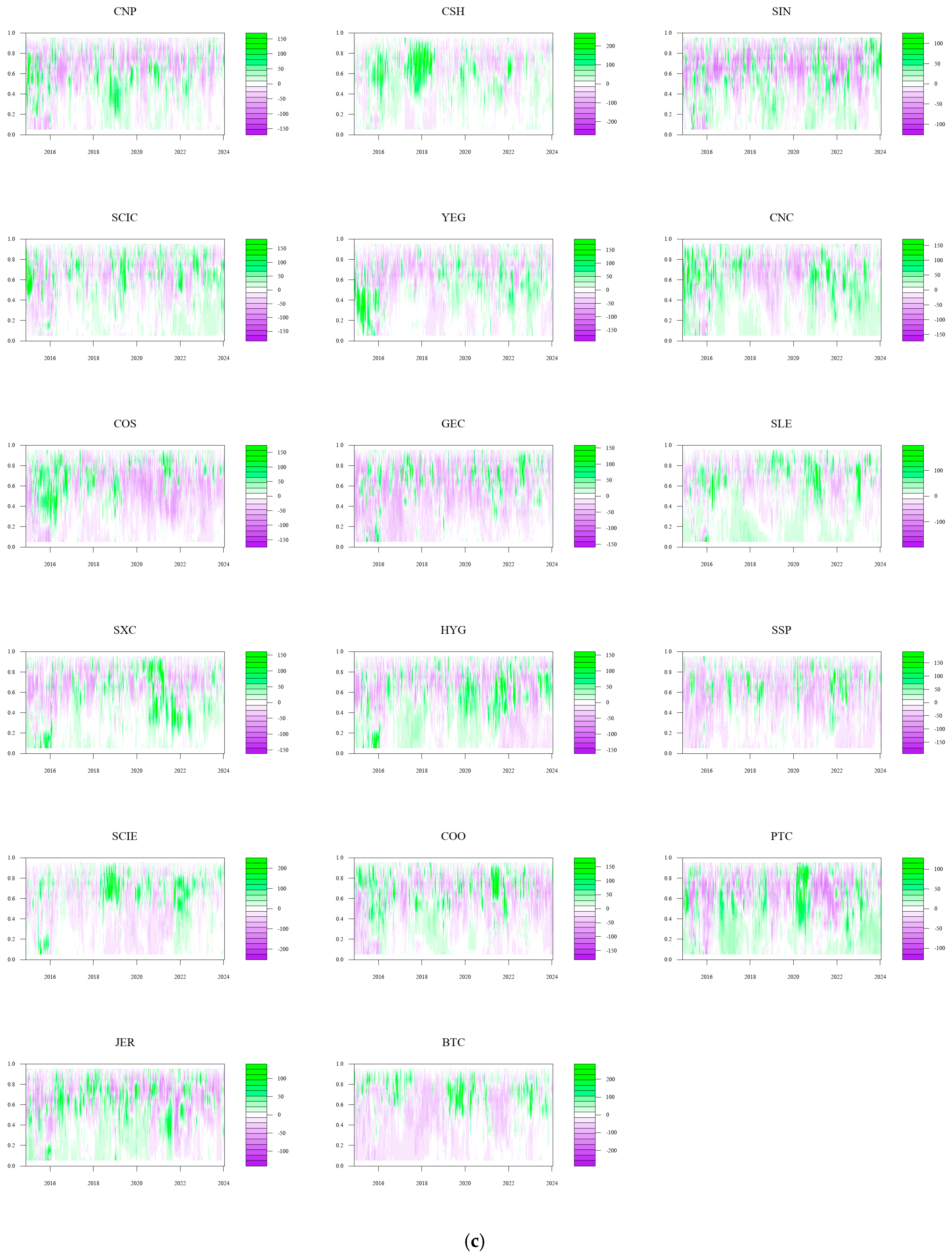

Appendix B. Time–Frequency Domain Tail Risk Net Spillover Effect Between Cryptocurrency and Energy Markets

References

- Yarovaya, L.; Matkovskyy, R.; Jalan, A. The effects of a “black swan” event (COVID-19) on herding behavior in cryptocurrency markets. J. Int. Financ. Mark. Inst. Money 2021, 75, 101321. [Google Scholar] [CrossRef]

- Yao, S.; Kong, X.; Sensoy, A.; Akyildirim, E.; Cheng, F. Investor attention and idiosyncratic risk in cryptocurrency markets. Eur. J. Financ. 2021, 27, 1932–1950. [Google Scholar] [CrossRef]

- Glenn, N.; Reed, R. Cryptocurrency, security, and financial intermediation. J. Money Credit Bank. 2024, 56, 185–223. [Google Scholar] [CrossRef]

- Makarov, I.; Schoar, A. Trading and arbitrage in cryptocurrency markets. J. Financ. Econ. 2020, 135, 293–319. [Google Scholar] [CrossRef]

- Liu, T.; Gong, X.; Lin, B. Analyzing the frequency dynamics of volatility spillovers across precious and industrial metal markets. J. Futures Mark. 2021, 41, 1375–1396. [Google Scholar] [CrossRef]

- Lee, S.S.; Wang, M. Variance Decomposition and Cryptocurrency Return Prediction. J. Financ. Quant. Anal. 2024, 59, 1–60. [Google Scholar] [CrossRef]

- Borri, N. Conditional tail-risk in cryptocurrency markets. J. Empir. Financ. 2019, 50, 1–19. [Google Scholar] [CrossRef]

- Guesmi, K.; Saadi, S.; Abid, I.; Ftiti, Z. Portfolio diversification with virtual currency: Evidence from bitcoin. Int. Rev. Financ. Anal. 2019, 63, 431–437. [Google Scholar] [CrossRef]

- Shahbaz, M.; Khan, S.; Tahir, M.I. The dynamic links between energy consumption, economic growth, financial development and trade in China: Fresh evidence from multivariate framework analysis. Energy Econ. 2013, 40, 8–21. [Google Scholar] [CrossRef]

- Antonakakis, N.; Cunado, J.; Filis, G.; Gabauer, D.; De Gracia, F.P. Oil volatility, oil and gas firms and portfolio diversification. Energy Econ. 2018, 70, 499–515. [Google Scholar] [CrossRef]

- Khalfaoui, R.; Mefteh-Wali, S.; Dogan, B.; Ghosh, S. Extreme spillover effect of COVID-19 pandemic-related news and cryptocurrencies on green bond markets: A quantile connectedness analysis. Int. Rev. Financ. Anal. 2023, 86, 102496. [Google Scholar] [CrossRef] [PubMed]

- Pham, S.D.; Nguyen, T.T.T.; Do, H.X. Dynamic volatility connectedness between thermal coal futures and major cryptocurrencies: Evidence from China. Energy Econ. 2022, 112, 106114. [Google Scholar] [CrossRef]

- Bissoondoyal-Bheenick, E.; Do, H.; Hu, X.; Zhong, A. Sentiment and stock market connectedness: Evidence from the US–China trade war. Int. Rev. Financ. Anal. 2022, 80, 102031. [Google Scholar] [CrossRef]

- Carlomagno, G.; Albagli, E. Trade wars and asset prices. J. Int. Money Financ. 2022, 124, 102631. [Google Scholar] [CrossRef]

- Hou, Y.; Li, Y.; Hu, Y.; Oxley, L. Time-varying spillovers of higher moments between Bitcoin and crude oil markets and the impact of the US–China trade war: A regime-switching perspective. Eur. J. Financ. 2022, 28, 1876–1906. [Google Scholar] [CrossRef]

- Ghabri, Y.; Rhouma, O.B.; Gana, M.; Guesmi, K.; Benkraiem, R. Information transmission among energy markets, cryptocurrencies, and stablecoins under pandemic conditions. Int. Rev. Financ. Anal. 2022, 82, 102197. [Google Scholar] [CrossRef]

- Wu, X.; Jiang, Z. Time-varying asymmetric volatility spillovers among China’s carbon markets, new energy market and stock market under the shocks of major events. Energy Econ. 2023, 126, 107004. [Google Scholar] [CrossRef]

- Karkowska, R.; Urjasz, S. How does the Russian-Ukrainian war change connectedness and hedging opportunities? Comparison between dirty and clean energy markets versus global stock indices. J. Int. Financ. Mark. Inst. Money 2023, 85, 101768. [Google Scholar] [CrossRef]

- Wang, Y.; Liu, S.; Abedin, M.Z.; Lucey, B. Volatility spillover and hedging strategies among Chinese carbon, energy, and electricity markets. J. Int. Financ. Mark. Inst. Money 2024, 91, 101938. [Google Scholar] [CrossRef]

- Kelly, B.; Jiang, H. Tail risk and asset prices. Rev. Financ. Stud. 2014, 27, 2841–2871. [Google Scholar] [CrossRef]

- Weller, B.M. Measuring tail risks at high frequency. Rev. Financ. Stud. 2019, 32, 3571–3616. [Google Scholar] [CrossRef]

- Van Oordt, M.R.; Zhou, C. Systematic tail risk. J. Financ. Quant. Anal. 2016, 51, 685–705. [Google Scholar] [CrossRef]

- Cabrales, A.; Gottardi, P.; Vega-Redondo, F. Risk sharing and contagion in networks. Rev. Financ. Stud. 2017, 30, 3086–3127. [Google Scholar] [CrossRef]

- Yang, J.; Zhou, Y. Return and volatility transmission between China’s and international crude oil futures markets: A first look. J. Futures Mark. 2020, 40, 860–884. [Google Scholar] [CrossRef]

- Huszár, Z.R.; Kotró, B.B.; Tan, R.S. European equity markets volatility spillover: Destabilizing energy risk is the new normal. J. Financ. Res. 2023, 46, S205–S271. [Google Scholar] [CrossRef]

- Uddin, G.S.; Luo, T.; Yahya, M.; Jayasekera, R.; Rahman, M.L.; Okhrin, Y. Risk network of global energy markets. Energy Econ. 2023, 125, 106882. [Google Scholar] [CrossRef]

- Wu, F.; Zhang, D.; Ji, Q. Systemic risk and financial contagion across top global energy companies. Energy Econ. 2021, 97, 105221. [Google Scholar] [CrossRef]

- Corbet, S.; Meegan, A.; Larkin, C.; Lucey, B.; Yarovaya, L. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Econ. Lett. 2018, 165, 28–34. [Google Scholar] [CrossRef]

- Zhao, M.; Park, H. Quantile time-frequency spillovers among green bonds, cryptocurrencies, and conventional financial markets. Int. Rev. Financ. Anal. 2024, 93, 103198. [Google Scholar] [CrossRef]

- Sapra, N.; Shaikh, I.; Roubaud, D.; Asadi, M.; Grebinevych, O. Uncovering Bitcoin’s electricity consumption relationships with volatility and price: Environmental Repercussions. J. Environ. Manag. 2024, 356, 120528. [Google Scholar] [CrossRef]

- Corbet, S.; Lucey, B.; Yarovaya, L. Bitcoin-energy markets interrelationships-New evidence. Resour. Policy 2021, 70, 101916. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Roubaud, D.; Kristoufek, L. Information interdependence among energy, cryptocurrency and major commodity markets. Energy Econ. 2019, 81, 1042–1055. [Google Scholar] [CrossRef]

- Okorie, D.I.; Lin, B. Crude oil price and cryptocurrencies: Evidence of volatility connectedness and hedging strategy. Energy Econ. 2020, 87, 104703. [Google Scholar] [CrossRef]

- Symitsi, E.; Chalvatzis, K.J. Return, volatility and shock spillovers of Bitcoin with energy and technology companies. Econ. Lett. 2018, 170, 127–130. [Google Scholar] [CrossRef]

- Oh, D.H.; Patton, A.J. Time-varying systemic risk: Evidence from a dynamic copula model of CDS spreads. J. Bus. Econ. Stat. 2018, 36, 181–195. [Google Scholar] [CrossRef]

- Gong, X.L.; Liu, X.H.; Xiong, X. Measuring tail risk with GAS time varying copula, fat tailed GARCH model and hedging for crude oil futures. Pac.-Basin Financ. J. 2019, 55, 95–109. [Google Scholar] [CrossRef]

- Wu, X.; Xia, M.; Zhang, H. Forecasting VaR using realized EGARCH model with skewness and kurtosis. Financ. Res. Lett. 2020, 32, 101090. [Google Scholar] [CrossRef]

- Klein, T.; Walther, T. Oil price volatility forecast with mixture memory GARCH. Energy Econ. 2016, 58, 46–58. [Google Scholar] [CrossRef]

- Nelson, D.B. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Ni, X.; Wang, Z.; Akbar, A.; Ali, S. Measuring natural resources rents volatility: Evidence from EGARCH and TGARCH for global data. Resour. Policy 2022, 76, 102553. [Google Scholar] [CrossRef]

- Johnson, N.L. Systems of frequency curves generated by methods of translation. Biometrika 1949, 36, 149–176. [Google Scholar] [CrossRef]

- Choi, P.; Nam, K. Asymmetric and leptokurtic distribution for heteroscedastic asset returns: The SU-normal distribution. J. Empir. Financ. 2008, 15, 41–63. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Measuring financial asset return and volatility spillovers, with application to global equity markets. Econ. J. 2009, 119, 158–171. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yılmaz, K. On the network topology of variance decompositions: Measuring the connectedness of financial firms. J. Econ. 2014, 182, 119–134. [Google Scholar] [CrossRef]

- Liu, Y.; Tsyvinski, A. Risks and returns of cryptocurrency. Rev. Financ. Stud. 2021, 34, 2689–2727. [Google Scholar] [CrossRef]

- Jiang, W.; Zhang, Y. Carbon assets and Bitcoin: Hedging roles in global stock markets during the tranquil and turbulent periods? J. Futures Mark. 2023, 43, 1183–1203. [Google Scholar] [CrossRef]

- Strohsal, T.; Proaño, C.R.; Wolters, J. Characterizing the financial cycle: Evidence from a frequency domain analysis. J. Bank. Financ. 2019, 106, 568–591. [Google Scholar] [CrossRef]

- Zhao, L.T.; Liu, H.Y.; Chen, X.H. How does carbon market interact with energy and sectoral stocks? Evidence from risk spillover and wavelet coherence. J. Commod. Mark. 2024, 33, 100386. [Google Scholar] [CrossRef]

- Baruník, J.; Křehlík, T. Measuring the frequency dynamics of financial connectedness and systemic risk. J. Financ. Econ. 2018, 16, 271–296. [Google Scholar] [CrossRef]

- Asadi, M.; Roubaud, D.; Tiwari, A.K. Volatility spillovers amid crude oil, natural gas, coal, stock, and currency markets in the US and China based on time and frequency domain connectedness. Energy Econ. 2022, 109, 105961. [Google Scholar] [CrossRef]

- Mensi, W.; Hammoudeh, S.; Vo, X.V.; Kang, S.H. Volatility spillovers between oil and equity markets and portfolio risk implications in the US and vulnerable EU countries. J. Int. Financ. Mark. Inst. Money 2021, 75, 101457. [Google Scholar] [CrossRef]

- Bouri, E.; Saeed, T.; Vo, X.V.; Roubaud, D. Quantile connectedness in the cryptocurrency market. J. Int. Financ. Mark. Inst. Money 2021, 71, 101302. [Google Scholar] [CrossRef]

- Ando, T.; Greenwood-Nimmo, M.; Shin, Y. Quantile connectedness: Modeling tail behavior in the topology of financial networks. Manage. Sci. 2022, 68, 2401–2431. [Google Scholar] [CrossRef]

- Chatziantoniou, I.; Abakah, E.J.A.; Gabauer, D.; Tiwari, A.K. Quantile time–frequency price connectedness between green bond, green equity, sustainable investments and clean energy markets. J. Clean. Prod. 2022, 361, 132088. [Google Scholar] [CrossRef]

- Jena, S.K.; Tiwari, A.K.; Abakah, E.J.A.; Hammoudeh, S. The connectedness in the world petroleum futures markets using a Quantile VAR approach. J. Commod. Mark. 2022, 27, 100222. [Google Scholar] [CrossRef]

- Gong, X.L.; Zhao, M.; Wu, Z.C.; Jia, K.W.; Xiong, X. Research on tail risk contagion in international energy markets—The quantile time-frequency volatility spillover perspective. Energy Econ. 2023, 121, 106678. [Google Scholar] [CrossRef]

- Kyriazis, N.; Papadamou, S.; Tzeremes, P.; Corbet, S. Quantifying spillovers and connectedness among commodities and cryptocurrencies: Evidence from a Quantile-VAR analysis. J. Commod. Mark. 2024, 33, 100385. [Google Scholar] [CrossRef]

- Yousaf, I.; Pham, L.; Goodell, J.W. Dynamic spillovers between leading cryptocurrencies and derivatives tokens: Insights from a quantile VAR approach. Int. Rev. Financ. Anal. 2024, 94, 103156. [Google Scholar] [CrossRef]

- Abduraimova, K. Contagion and tail risk in complex financial networks. J. Bank. Financ. 2022, 143, 106560. [Google Scholar] [CrossRef]

- Yang, L. Idiosyncratic information spillover and connectedness network between the electricity and carbon markets in Europe. J. Commod. Mark. 2022, 25, 100185. [Google Scholar] [CrossRef]

- Zhang, Z.-K.; Liu, C.; Zhan, X.-X.; Lu, X.; Zhang, C.-X.; Zhang, Y.-C. Dynamics of information diffusion and its applications on complex networks. Phys. Rep. 2016, 651, 1–34. [Google Scholar] [CrossRef]

- Yu, M.; Hu, X.; Zhong, A. Network centrality, information diffusion and asset pricing. Int. Rev. Financ. Anal. 2024, 93, 103223. [Google Scholar] [CrossRef]

- Jiang, S.; Jin, X. Effects of investor sentiment on stock return volatility: A spatio-temporal dynamic panel model. Econ. Model. 2021, 97, 298–306. [Google Scholar] [CrossRef]

- Zhu, B.; Lin, R.; Liu, J. Magnitude and persistence of extreme risk spillovers in the global energy market: A high-dimensional left-tail interdependence perspective. Energy Econ. 2020, 89, 104761. [Google Scholar] [CrossRef]

- Wang, Z.; Gao, X.; An, H.; Tang, R.; Sun, Q. Identifying influential energy stocks based on spillover network. Int. Rev. Financ. Anal. 2020, 68, 101277. [Google Scholar] [CrossRef]

| Code | Name | Variable | Code | Name | Variable |

|---|---|---|---|---|---|

| 601857 | China National Petroleum Corporation(Beijing, China) | CNP | 601699 | Shanxi Lu’an Environmental Energy Development Co., Ltd. (Changzhi, Shanxi, China) | SLE |

| 601088 | China Shenhua Energy Co., Ltd. (Beijing, China) | CSH | 000983 | Shanxi Coking Coal Group Co., Ltd. (Taiyuan, Shanxi, China) | SXC |

| 600028 | China Petroleum & Chemical Corporation (Beijing, China) | SIN | 600348 | Shan Xi Hua Yang Group New Energy Co., Ltd. (Yangquan, Shanxi, China) | HYG |

| 601225 | Shaanxi Coal Industry Co., Ltd. (Xi’an, Shaanxi, China) | SCIC | 600688 | Sinopec Shanghai Petrochemical Co., Ltd. (Shanghai, China) | SSP |

| 600188 | Yankuang Energy Group Co., Ltd.(Jining, Shandong, China) | YEG | 600546 | Shanxi Coal International Energy Group Co., Ltd. (Taiyuan, Shanxi, China) | SCIE |

| 601898 | China Coal Energy Co., Ltd. (Beijing, China) | CNC | 600583 | Offshore Oil Engineering Co., Ltd. (Tianjin, China) | COO |

| 601808 | China Oilfield Services Limited (Tianjin, China) | COS | 601666 | Pingdingshan Tianan Coal Mining Co., Ltd. (Pingdingshan, Henan, China) | PTC |

| 600256 | Guanghui Energy Co., Ltd. (Urumqi, Xinjiang, China) | GEC | 000937 | Jizhong Energy Resources Co., Ltd. (Xingtai, Hebei, China) | JER |

| 0.05 Conditional Quantile | 0.50 Conditional Quantile | 0.95 Conditional Quantile | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SELF | FROM | TO | NET | SELF | FROM | TO | NET | SELF | FROM | TO | NET | |

| TCI | 82.66 | 73.89 | 94.83 | |||||||||

| CNP | 16.86 | 83.14 | 78.58 | −4.56 | 25.9 | 74.1 | 77.61 | 3.52 | 9.39 | 90.61 | 131.31 | 40.7 |

| CSH | 17.81 | 82.19 | 73.68 | −8.51 | 25.83 | 74.17 | 73.24 | −0.93 | 1.17 | 98.83 | 52.88 | −45.95 |

| SIN | 16.1 | 83.9 | 85.94 | 2.04 | 27.15 | 72.85 | 84.97 | 12.12 | 0.56 | 99.44 | 53.65 | −45.79 |

| SCIC | 13.81 | 86.19 | 98.82 | 12.63 | 17.59 | 82.41 | 85.26 | 2.86 | 6.47 | 93.53 | 64.16 | −29.36 |

| YEG | 14.69 | 85.31 | 89.18 | 3.86 | 15.64 | 84.36 | 71.88 | −12.49 | 3.28 | 96.72 | 64.16 | −32.56 |

| CNC | 13.35 | 86.65 | 100.19 | 13.54 | 17.69 | 82.31 | 113.11 | 30.8 | 0.71 | 99.29 | 60.21 | −39.07 |

| COS | 16.82 | 83.18 | 78.57 | −4.61 | 26.17 | 73.83 | 65.17 | −8.65 | 0.54 | 99.46 | 48.73 | −50.72 |

| GEC | 17.67 | 82.33 | 77.08 | −5.24 | 25.51 | 74.49 | 69.33 | −5.16 | 8.38 | 91.62 | 92.86 | 1.24 |

| SLE | 13.15 | 86.85 | 102.88 | 16.03 | 18.19 | 81.81 | 94.4 | 12.59 | 3.15 | 96.85 | 68.96 | −27.89 |

| SXC | 13.23 | 86.77 | 101 | 14.23 | 17.05 | 82.95 | 91.91 | 8.95 | 7.47 | 92.53 | 76.26 | −16.27 |

| HYG | 15.51 | 84.49 | 84.18 | −0.32 | 17.67 | 82.33 | 68.11 | −14.22 | 0.14 | 99.86 | 137.88 | 38.02 |

| SSP | 19.04 | 80.96 | 67.07 | −13.89 | 27.52 | 72.48 | 58.54 | −13.93 | 20.28 | 79.72 | 306.76 | 227.04 |

| SCIE | 16.95 | 83.05 | 78.47 | −4.58 | 27.56 | 72.44 | 50.12 | −22.31 | 0.1 | 99.9 | 73.33 | −26.57 |

| COO | 17.38 | 82.62 | 76.83 | −5.78 | 33.15 | 66.85 | 75.05 | 8.2 | 0.56 | 99.44 | 47.76 | −51.68 |

| PTC | 13.22 | 86.78 | 103.28 | 16.51 | 17.77 | 82.23 | 96.96 | 14.73 | 9.94 | 90.06 | 107.22 | 17.17 |

| JER | 14.54 | 85.46 | 90.43 | 4.97 | 18.67 | 81.33 | 76.31 | −5.03 | 7.84 | 92.16 | 89.6 | −2.56 |

| BTC | 44.66 | 55.34 | 19.03 | −36.31 | 84.77 | 15.23 | 4.19 | −11.04 | 7.84 | 92.16 | 136.42 | 44.26 |

| Short-Term | Medium-Term | Long-Term | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SELF | FROM | TO | NET | SELF | FROM | TO | NET | SELF | FROM | TO | NET | |

| TCI | 2.06 | 5.77 | 66.06 | |||||||||

| CNP | 1.33 | 3.06 | 2.31 | −0.75 | 3.61 | 8.41 | 6.36 | −2.05 | 20.96 | 62.63 | 68.95 | 6.32 |

| CSH | 0.71 | 1.78 | 1.89 | 0.1 | 2 | 5 | 5.3 | 0.3 | 23.11 | 67.39 | 66.06 | −1.33 |

| SIN | 1.42 | 3.62 | 2.62 | −1 | 3.86 | 9.94 | 7.17 | −2.77 | 21.87 | 59.29 | 75.19 | 15.9 |

| SCIC | 0.5 | 1.4 | 2.42 | 1.02 | 1.4 | 4.01 | 6.84 | 2.82 | 15.69 | 77 | 76 | −1 |

| YEG | 0.47 | 1.45 | 2.71 | 1.26 | 1.34 | 4.15 | 7.54 | 3.39 | 13.82 | 78.77 | 61.61 | −17.15 |

| CNC | 0.58 | 2.07 | 2.7 | 0.62 | 1.64 | 5.96 | 7.65 | 1.7 | 15.47 | 74.28 | 102.76 | 28.49 |

| COS | 0.92 | 1.45 | 1.88 | 0.43 | 2.6 | 4.33 | 5.25 | 0.92 | 22.65 | 68.04 | 58.05 | −9.99 |

| GEC | 0.52 | 0.8 | 1.29 | 0.48 | 1.49 | 2.42 | 3.67 | 1.25 | 23.49 | 71.27 | 64.38 | −6.89 |

| SLE | 0.91 | 3.24 | 2.52 | −0.72 | 2.49 | 9 | 7.04 | −1.96 | 14.79 | 69.57 | 84.83 | 15.26 |

| SXC | 0.5 | 1.84 | 3 | 1.16 | 1.38 | 5.13 | 8.35 | 3.22 | 15.17 | 75.98 | 80.54 | 4.57 |

| HYG | 0.6 | 1.6 | 2.3 | 0.7 | 1.68 | 4.48 | 6.39 | 1.91 | 15.39 | 76.26 | 59.4 | −16.85 |

| SSP | 1.21 | 1.63 | 1.44 | −0.2 | 3.32 | 4.85 | 4 | −0.85 | 22.99 | 66 | 53.12 | −12.88 |

| SCIE | 1.04 | 2.08 | 1.47 | −0.61 | 2.86 | 5.75 | 4.09 | −1.66 | 23.66 | 64.61 | 44.57 | −20.05 |

| COO | 1.71 | 2.86 | 1.4 | −1.46 | 4.64 | 7.99 | 4.1 | −3.89 | 26.8 | 56 | 69.57 | 13.57 |

| PTC | 0.64 | 2.09 | 2.62 | 0.53 | 2.61 | 5.82 | 7.45 | 1.63 | 15.37 | 74.31 | 86.88 | 12.57 |

| JER | 0.96 | 3.01 | 2.35 | −0.66 | 21.82 | 8.24 | 6.55 | −1.69 | 15.1 | 70.08 | 67.4 | −2.68 |

| BTC | 8.76 | 1.05 | 0.14 | −0.91 | 84.77 | 2.66 | 0.39 | −2.27 | 54.19 | 11.52 | 3.67 | −7.86 |

| Short-Term | Medium-Term | Long-Term | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SELF | FROM | TO | NET | SELF | FROM | TO | NET | SELF | FROM | TO | NET | |

| TCI | 6.56 | 16.84 | 59.26 | |||||||||

| CNP | 1.52 | 7.44 | 6.51 | −0.93 | 3.9 | 19.07 | 16.57 | −2.5 | 11.44 | 56.64 | 55.5 | −1.13 |

| CSH | 0.96 | 4.6 | 5.79 | 1.19 | 2.63 | 12.51 | 14.93 | 2.43 | 14.21 | 65.08 | 52.95 | −12.13 |

| SIN | 1.55 | 8.11 | 7.22 | −0.89 | 3.92 | 20.47 | 18.26 | −2.21 | 10.63 | 55.32 | 60.46 | 5.14 |

| SCIC | 0.92 | 5.77 | 7.69 | 1.92 | 2.47 | 15.47 | 19.81 | 4.34 | 10.42 | 64.95 | 71.32 | 6.37 |

| YEG | 0.64 | 3.75 | 6.99 | 3.23 | 1.79 | 10.43 | 18.08 | 7.65 | 12.25 | 71.13 | 64.11 | −7.02 |

| CNC | 0.87 | 5.56 | 7.78 | 2.21 | 2.36 | 15.14 | 20.06 | 4.91 | 10.12 | 65.95 | 72.35 | 6.41 |

| COS | 1.35 | 6.49 | 6.75 | 0.27 | 3.52 | 17.09 | 17.07 | −0.02 | 11.95 | 59.61 | 54.75 | −4.86 |

| GEC | 1.03 | 4.99 | 6.22 | 1.23 | 2.77 | 13.36 | 15.92 | 2.56 | 13.87 | 63.98 | 54.95 | −9.03 |

| SLE | 1.24 | 8.17 | 7.81 | −0.36 | 3.17 | 20.94 | 20.21 | −0.73 | 8.74 | 57.74 | 74.86 | 17.12 |

| SXC | 0.83 | 5.42 | 7.85 | 2.43 | 2.25 | 14.68 | 20.27 | 5.59 | 10.16 | 66.66 | 72.88 | 6.21 |

| HYG | 0.8 | 4.35 | 6.59 | 2.24 | 2.19 | 11.95 | 17 | 5.05 | 12.51 | 68.2 | 60.59 | −7.61 |

| SSP | 1.73 | 7.3 | 5.67 | −1.63 | 4.43 | 18.69 | 14.32 | −4.37 | 12.87 | 54.97 | 47.08 | −7.89 |

| SCIE | 1.32 | 6.65 | 6.19 | −0.47 | 3.47 | 17.39 | 15.89 | −1.5 | 12.16 | 59 | 56.39 | −2.61 |

| COO | 1.98 | 9.39 | 6.18 | −3.21 | 4.8 | 22.78 | 15.85 | −6.93 | 10.61 | 50.45 | 54.8 | 4.36 |

| PTC | 1.11 | 7.3 | 7.92 | 0.63 | 2.87 | 18.91 | 20.48 | 1.58 | 9.24 | 60.57 | 74.87 | 14.3 |

| JER | 1.29 | 7.55 | 6.82 | −0.73 | 3.31 | 19.39 | 17.69 | −1.71 | 9.93 | 58.52 | 65.92 | 7.41 |

| BTC | 7.2 | 8.66 | 1.51 | −7.15 | 15.17 | 18.07 | 3.93 | −14.14 | 22.29 | 28.61 | 13.59 | −15.02 |

| Short-Term | Medium-Term | Long-Term | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SELF | FROM | TO | NET | SELF | FROM | TO | NET | SELF | FROM | TO | NET | |

| TCI | 14.04 | 31.53 | 49.27 | |||||||||

| CNP | 0.86 | 9.67 | 16.06 | 6.39 | 2.32 | 24.89 | 38.99 | 14.1 | 6.07 | 56.19 | 70.03 | 13.84 |

| CSH | 0.01 | 15.53 | 7.46 | −8.06 | 0.14 | 33.72 | 17.38 | −16.33 | 0.73 | 49.88 | 27.84 | −22.04 |

| SIN | 0.17 | 17.96 | 6.84 | −11.12 | 0.32 | 37.33 | 16.77 | −20.56 | 0.16 | 44.05 | 28.28 | −15.77 |

| SCIC | 0.94 | 12.91 | 8.87 | −4.04 | 2.23 | 31.07 | 20.49 | −10.59 | 3.37 | 49.47 | 34.98 | −14.49 |

| YEG | 0.65 | 16.7 | 8.7 | −8.01 | 1.36 | 35.74 | 20.38 | −15.35 | 1.39 | 44.16 | 34.9 | −9.26 |

| CNC | 0.07 | 16.99 | 7.41 | −9.59 | 0.17 | 35.58 | 18.18 | −17.4 | 0.39 | 46.8 | 33.16 | −13.64 |

| COS | 0.06 | 15.66 | 6.55 | −9.11 | 0.14 | 33.44 | 15.6 | −17.84 | 0.3 | 50.4 | 25.4 | −24.99 |

| GEC | 0.89 | 10.24 | 14.63 | 4.39 | 2.29 | 25.67 | 32.09 | 6.41 | 5.14 | 55.76 | 47.16 | −8.6 |

| SLE | 0.71 | 14.61 | 9.16 | −5.45 | 1.36 | 31.94 | 21.67 | −10.27 | 1.43 | 49.94 | 37.68 | −12.26 |

| SXC | 1.2 | 14.12 | 10.42 | −3.7 | 2.61 | 31.35 | 24.19 | −7.16 | 3.75 | 46.97 | 41.72 | −5.25 |

| HYG | 0 | 14.29 | 20.95 | 6.66 | 0 | 34.65 | 46.34 | 11.69 | 0.1 | 50.94 | 72.03 | 21.09 |

| SSP | 2.84 | 12.31 | 50.44 | 38.12 | 6.43 | 27.15 | 107.58 | 80.43 | 10.64 | 40.62 | 152.69 | 112.08 |

| SCIE | 0.03 | 15.22 | 11.93 | −3.3 | 0.04 | 34.49 | 25.96 | −8.53 | 0.05 | 50.16 | 36.34 | −13.82 |

| COO | 0.09 | 17.14 | 6.74 | −10.4 | 0.2 | 35.84 | 15.81 | −20.03 | 0.23 | 46.5 | 24.66 | −21.84 |

| PTC | 1.37 | 12.53 | 16.27 | 3.74 | 3.19 | 29.24 | 36.05 | 6.81 | 5.37 | 48.3 | 55.82 | 7.52 |

| JER | 1.3 | 14.61 | 12.91 | −1.7 | 2.78 | 31.76 | 29.24 | −2.52 | 3.84 | 45.71 | 48.06 | 2.34 |

| BTC | 0.73 | 8.15 | 23.32 | 15.17 | 1.97 | 22.23 | 49.37 | 27.14 | 5.2 | 61.71 | 66.82 | 5.11 |

| Year | Moran’s I (W1) | z | p-Value | Moran’s I (W2) | z | p-Value | Moran’s I (W3) | z | p-Value |

|---|---|---|---|---|---|---|---|---|---|

| 2014 | 0.234 | 4.139 | 0.000 | 0.206 | 4.393 | 0.000 | 0.094 | 6.745 | 0.000 |

| 2015 | 0.267 | 3.976 | 0.000 | 0.255 | 4.429 | 0.000 | 0.112 | 6.598 | 0.000 |

| 2016 | 0.421 | 5.575 | 0.000 | 0.344 | 5.598 | 0.000 | 0.114 | 6.603 | 0.000 |

| 2017 | 0.321 | 4.465 | 0.000 | 0.281 | 4.687 | 0.000 | 0.122 | 9.138 | 0.000 |

| 2018 | 0.244 | 4.069 | 0.000 | 0.195 | 3.747 | 0.000 | 0.141 | 9.767 | 0.000 |

| 2019 | 0.332 | 4.761 | 0.000 | 0.300 | 5.100 | 0.000 | 0.158 | 8.248 | 0.000 |

| 2020 | 0.260 | 3.878 | 0.000 | 0.238 | 4.216 | 0.000 | 0.129 | 7.097 | 0.000 |

| 2021 | 0.310 | 4.348 | 0.000 | 0.216 | 3.834 | 0.000 | 0.099 | 6.294 | 0.000 |

| 2022 | 0.434 | 5.861 | 0.000 | 0.373 | 5.975 | 0.000 | 0.099 | 7.088 | 0.000 |

| 2023 | 0.393 | 5.327 | 0.000 | 0.304 | 5.103 | 0.000 | 0.114 | 6.751 | 0.000 |

| Variable | W1 | W2 | W3 |

|---|---|---|---|

| Outdegree | 0.229 *** | 0.617 *** | 3.465 *** |

| (0.005) | (0.014) | (0.090) | |

| ALR | 0.020 * | 0.059 * | −0.189 |

| (0.011) | (0.033) | (0.220) | |

| SHR | 0.025 * | 0.037 | 0.132 |

| (0.014) | (0.043) | (0.319) | |

| ATR | 0.007 ** | 0.012 | 0.200 *** |

| (0.003) | (0.009) | (0.065) | |

| ROE | −0.002 | 0.016 | 0.217 |

| (0.007) | (0.021) | (0.141) | |

| GRnx | −0.011 *** | −0.027 ** | 0.061 |

| (0.004) | (0.011) | (0.079) | |

| GRgdp | 0.002 | 0.043 | −0.168 |

| (0.010) | (0.030) | (0.241) | |

| W × Outdegree | −0.218 *** | −0.611 *** | −3.603 *** |

| (0.008) | (0.025) | (0.189) | |

| W × ALR | −0.071 ** | −0.279 *** | 2.081 ** |

| (0.030) | (0.104) | (0.993) | |

| W × SHR | −0.106 ** | −0.166 | 6.939 *** |

| (0.045) | (0.152) | (2.164) | |

| W × ATR | −0.015 * | −0.015 | 1.402 *** |

| (0.008) | (0.025) | (0.353) | |

| W × ROE | 0.001 | −0.095 | −2.344 *** |

| (0.017) | (0.058) | (0.737) | |

| W × GRnx | 0.011 | 0.068 ** | 0.553 ** |

| (0.008) | (0.026) | (0.269) | |

| W × GRgdp | −0.003 | −0.105 | −1.360 ** |

| (0.200) | (0.065) | (0.660) | |

| ρ | 0.865 *** | 0.802 *** | 0.449 *** |

| (0.029) | (0.044) | (0.129) | |

| 9.17 × 10−6 *** | 0.0001 *** | 0.007 *** | |

| (1.10 × 10−6) | (0.00001) | (0.001) | |

| Individual fixed effects | Yes | Yes | Yes |

| N | 160 | 160 | 160 |

| 0.915 | 0.894 | 0.826 |

| Variable | Direct | Indirect | Total | ||||||

|---|---|---|---|---|---|---|---|---|---|

| W1 | W2 | W3 | W1 | W2 | W3 | W1 | W2 | W3 | |

| Outdegree | 0.215 *** | 0.554 *** | 3.048 *** | −0.129 *** | −0.524 *** | −3.309 *** | −0.085 * | 0.031 | −0.262 |

| (0.005) | (0.011) | (0.062) | (0.041) | (0.088) | (0.270) | (0.043) | (0.093) | (0.273) | |

| ALR | −0.020 * | −0.065 ** | 0.223 | −0.345 ** | −1.014 *** | 3.313 ** | −0.364 ** | −1.079 *** | 3.537 ** |

| (0.012) | (0.030) | (0.169) | (0.141) | (0.337) | (1.344) | (0.150) | (0.358) | (1.398) | |

| SHR | −0.038 * | −0.035 | 1.600 *** | −0.570 ** | −0.615 | 11.558 *** | −0.608 ** | −0.650 | 13.159 *** |

| (0.019) | (0.049) | (0.348) | (0.240) | (0.584) | (4.036) | (0.257) | (0.624) | (4.308) | |

| ATR | 0.001 | 0.009 | 0.069 | −0.060 | −0.024 | 2.128 *** | −0.060 | −0.015 | 2.197 *** |

| (0.003) | (0.007) | (0.052) | (0.041) | (0.095) | (0.467) | (0.043) | (0.100) | (0.492) | |

| ROE | −0.002 | −0.027 | −0.243 ** | 0.003 | −0.352 | −3.632 *** | −0.001 | −0.379 | −3.875 *** |

| (0.007) | 0.018 | (0.120) | (0.091) | (0.221) | (1.336) | (0.097) | (0.233) | (1.404) | |

| GRnx | −0.011 ** | −0.002 | 0.183 ** | 0.005 | 0.204 ** | 0.938 * | −0.005 | 0.202 * | 1.120 ** |

| (0.004) | (0.011) | (0.075) | (0.040) | (0.097) | (0.509) | (0.043) | (0.103) | (0.539) | |

| GRgdp | 0.001 | 0.005 | −0.461 ** | −0.005 | −0.312 | −2.322 ** | 0.005 | −0.307 | −2.783 ** |

| (0.012) | (0.032) | (0.227) | (0.105) | (0.251) | (1.137) | (0.113) | (0.268) | (1.198) | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gong, X.-L.; Wang, X.-T. Research on the Tail Risk Spillover Effect of Cryptocurrencies and Energy Market Based on Complex Network. Entropy 2025, 27, 704. https://doi.org/10.3390/e27070704

Gong X-L, Wang X-T. Research on the Tail Risk Spillover Effect of Cryptocurrencies and Energy Market Based on Complex Network. Entropy. 2025; 27(7):704. https://doi.org/10.3390/e27070704

Chicago/Turabian StyleGong, Xiao-Li, and Xue-Ting Wang. 2025. "Research on the Tail Risk Spillover Effect of Cryptocurrencies and Energy Market Based on Complex Network" Entropy 27, no. 7: 704. https://doi.org/10.3390/e27070704

APA StyleGong, X.-L., & Wang, X.-T. (2025). Research on the Tail Risk Spillover Effect of Cryptocurrencies and Energy Market Based on Complex Network. Entropy, 27(7), 704. https://doi.org/10.3390/e27070704