Iterative Forecasting of Financial Time Series: The Greek Stock Market from 2019 to 2024

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

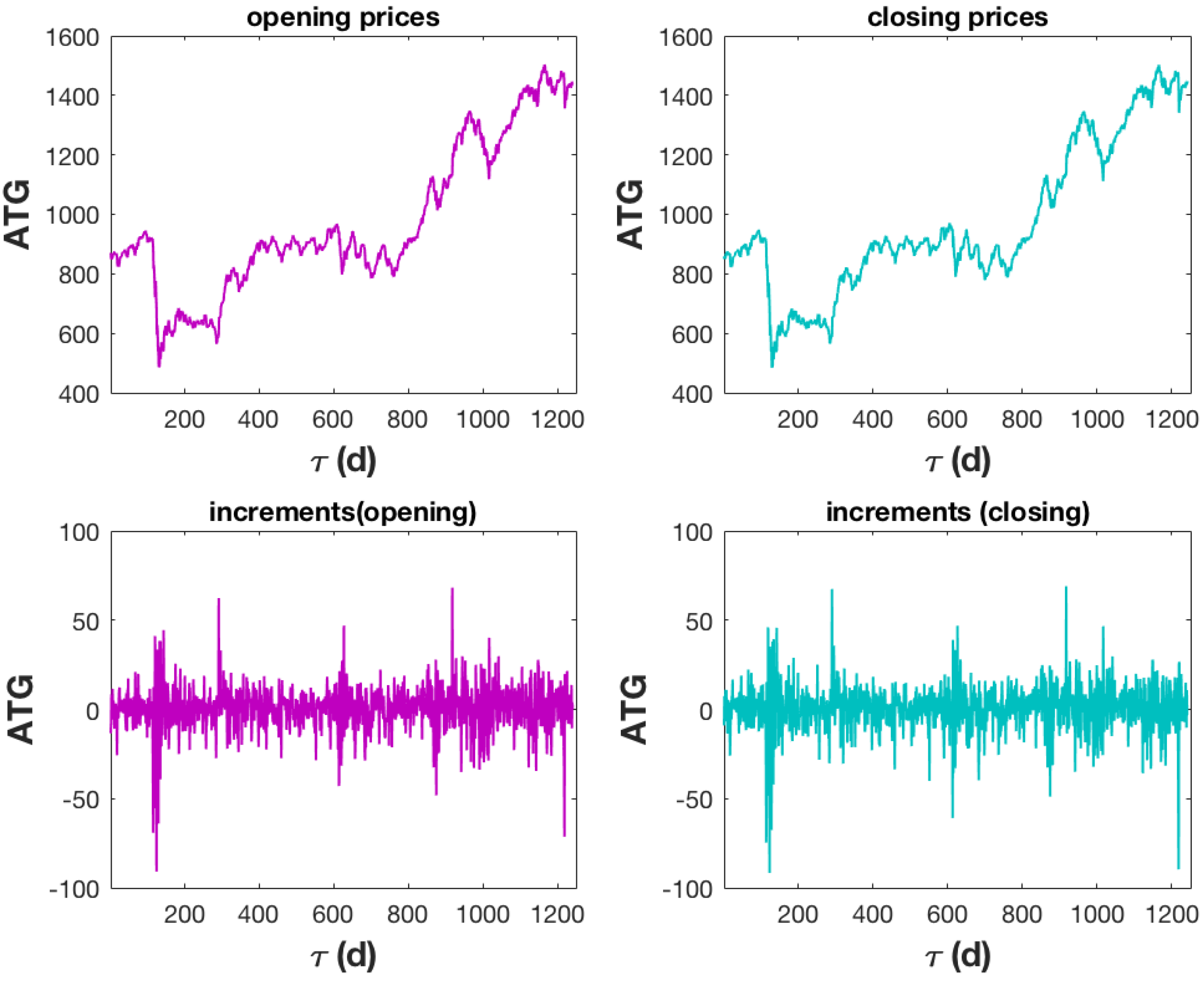

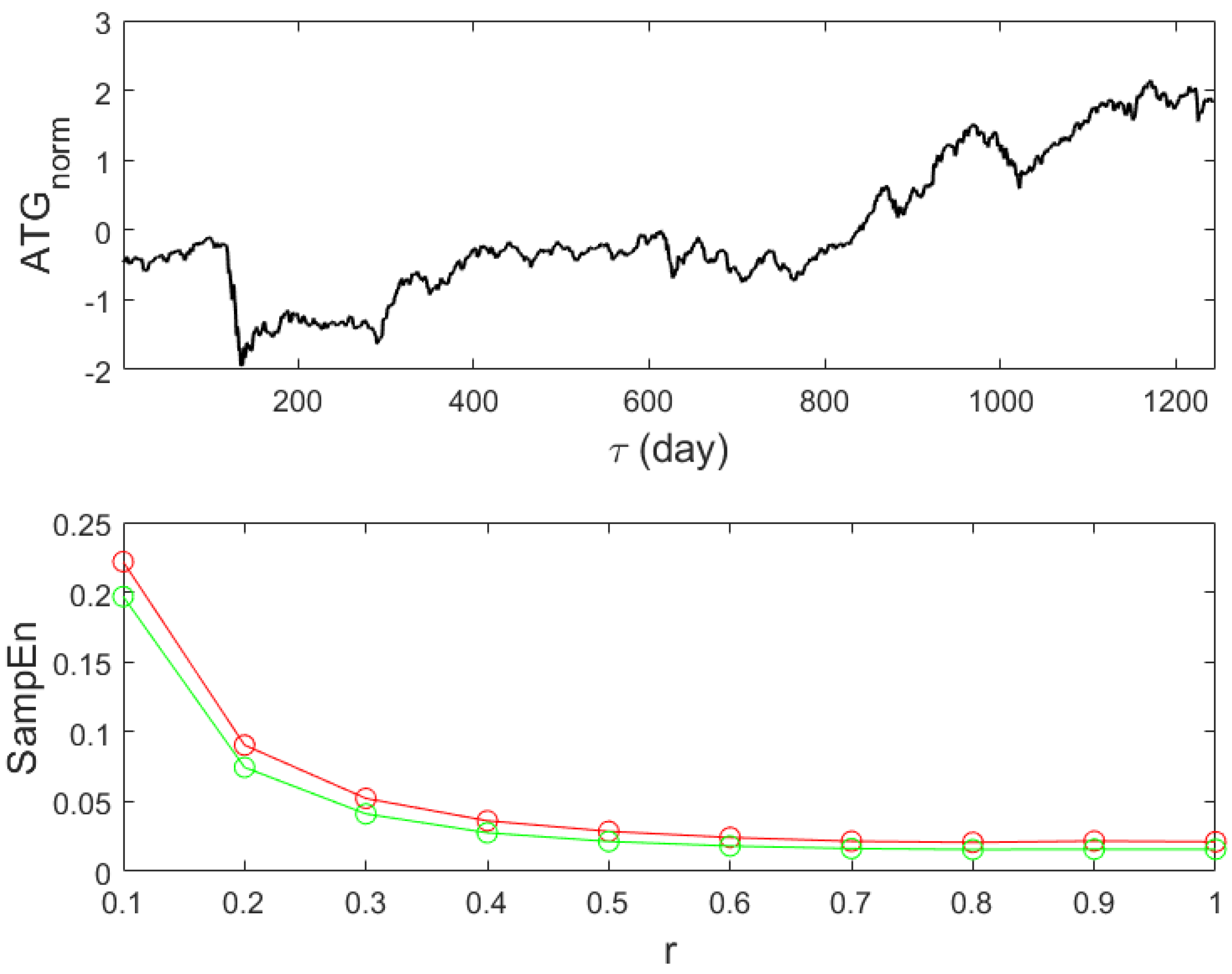

2. Materials and Methods

2.1. Time Series and Generalised Moments Method

- (i)

- The construction of time series characterized by different lag times, , which contain the absolute change of the values between two points of the initial time series for and for , where is the maximum lag time.

- (ii)

- Calculation of the moments of various orders q for , including also fractional orders . Notice that the small order moments, , are responsible for the core of the probability density function (pdf), and higher moments contribute to tails of a pdf [48].

- (iii)

- Finding the scaling exponent for each moment. Assuming that , then the slope of the linear regression in log–log scale returns the value of for each q.

- (iv)

- Construction of the structure function. Having the values of the term for the various moments, fit the data with Equation (1) and find the parameters .

2.2. Self-Similar Stochastic Models and Fractional Lévy Stable Motion

2.3. Stochastic Differential Equation

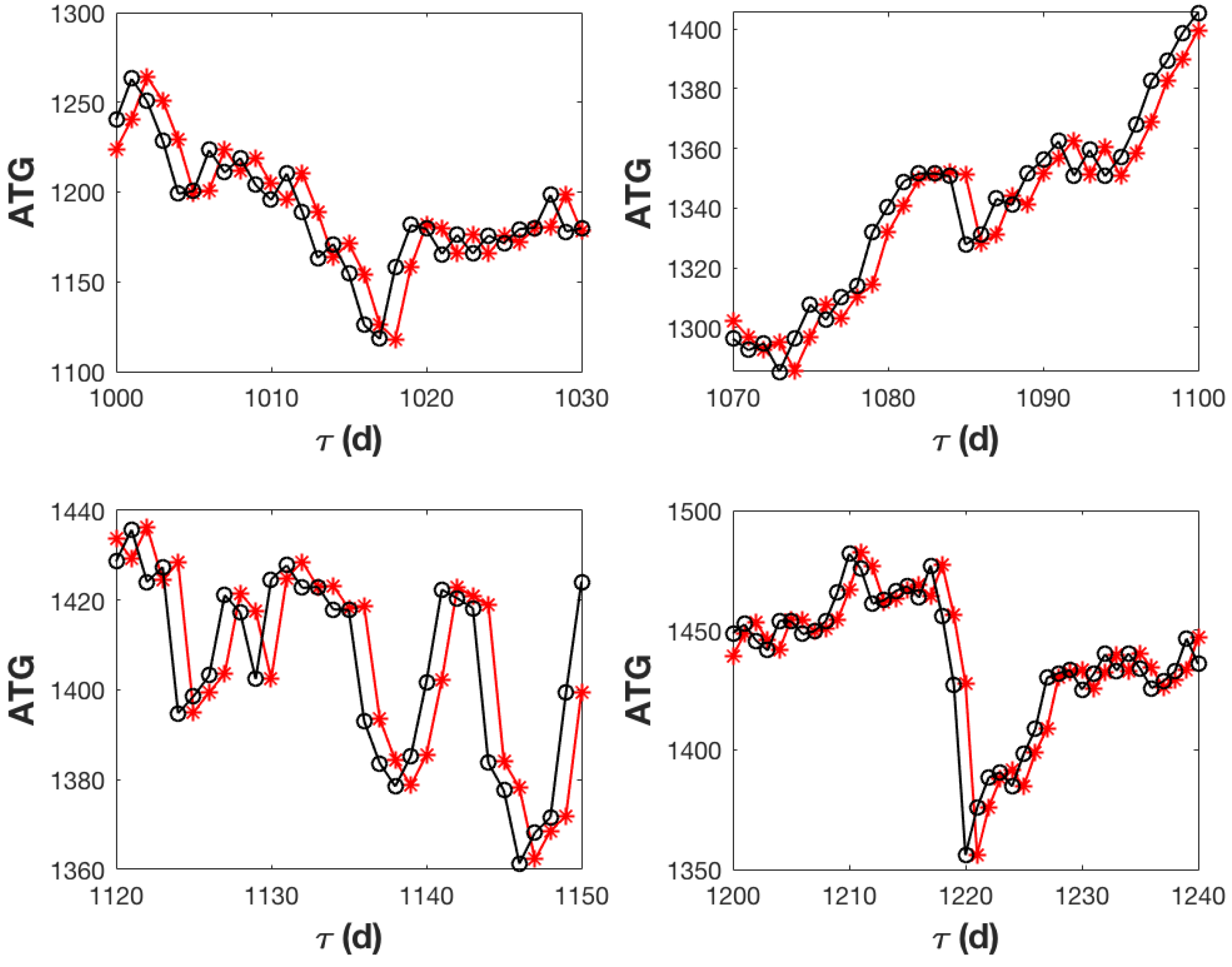

3. Results and Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| fBm | fractional Brownian motion |

| fGn | fractional Gaussian noise |

| mfBm | multifractional fractional Brownian motion |

| fLsm | fractional Lévy stable motion |

| fLsn | fractional Lévy stable noise |

References

- Beran, J. Statistics for Long-Memory Processes; Chapman & Hall: London, UK, 2017; pp. 32–58. [Google Scholar]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Polit. Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Di Matteo, T. Multi-scaling in finance. Quant. Financ. 2007, 7, 21–36. [Google Scholar] [CrossRef]

- Bentes, S.R.; Menezes, R.; Mendes, D.A. Long memory and volatility clustering: Is the empirical evidence consistent across stock markets? Physica A 2008, 387, 3826–3830. [Google Scholar] [CrossRef]

- Drzazga-Szczesniak, E.A.; Szczepanik, P.; Kaczmarek, A.Z.; Szczesniak, D. Entropy of Financial Time Series Due to the Shock of War. Entropy 2023, 25, 823. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Stanley, H.E. Econophysics: Financial time series from a statistical physics point of view. Physica A 2000, 279, 443–456. [Google Scholar] [CrossRef]

- Mandelbrot, B. The Variation of Certain Speculative Prices. J. Bus. 1963, 36, 394–419. Available online: https://www.jstor.org/stable/2350970 (accessed on 26 March 2025). [CrossRef]

- Mantegna, R.; Stanley, H.E. Scaling behaviour in the dynamics of an economic index. Nature 1995, 376, 46–49. [Google Scholar] [CrossRef]

- Bouchaud, J.P.; Potters, M.; Meyer, M. Apparent multifractality in financial time series. Eur. Phys. J. B 2000, 13, 595–599. [Google Scholar] [CrossRef]

- Scalas, E. Scaling in the market of futures. Physica A 1998, 253, 394–402. [Google Scholar] [CrossRef]

- Calvet, L.; Fisher, A. Multifractality in Asset Returns: Theory and Evidence. Rev. Econ. Stat. 2002, 84, 381–406. Available online: https://www.jstor.org/stable/3211559 (accessed on 26 March 2025). [CrossRef]

- Ruipeng, L.; Di Matteo, T.; Lux, T. Multifractality and long-range dependence of asset returns: The scaling behaviour of the Markov-switching multifractal model with lognormal volatility components. Adv. Complex Syst. 2008, 11, 669–684. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Wallis, J.R. Robustness of the rescaled range R/S in the measurement of noncyclic long run Statistical dependence. J. Wat. Res. 1969, 5, 967–988. [Google Scholar] [CrossRef]

- Hurst, H.E. Long term storage capacity of reservoirs. Trans. Am. Soc. Eng. 1951, 116, 770–799. [Google Scholar] [CrossRef]

- Yin, Y.; Shang, P. Modified multidimensional scaling approach to analyze financial markets. Chaos 2014, 24, 022102. [Google Scholar] [CrossRef]

- Peng, C.-K.; Buldyrev, S.V.; Havlin, S.; Simons, M.; Stanley, H.E.; Goldberger, A.L. Mosaic organization of DNA nucleotides. Phys. Rev. E 1994, 49, 685–1689. [Google Scholar] [CrossRef] [PubMed]

- Kantelhardt, J.W.; Zschiegner, S.A.; Koscielny-Bunde, E.; Havlin, S.; Bunde, A.; Stanley, H.E. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A 2002, 316, 87–114. [Google Scholar] [CrossRef]

- Barunik, J.; Kristoufek, L. On Hurst exponent estimation under heavy-tailed distributions. Physica A 2010, 389, 3844–3855. [Google Scholar] [CrossRef]

- Bakalis, E.; Höfinger, S.; Venturini, A.; Zerbetto, F. Crossover of two power laws in the anomalous diffusion of a two lipid membrane. J. Chem. Phys. 2015, 142, 215102. [Google Scholar] [CrossRef] [PubMed]

- Schertzer, D.; Lovejoy, S. Physical modeling and Analysis of Rain and Clouds by Anisotropic Scaling of Multiplicative Processes. J. Geophys. Res. 1987, 92, 9693–9714. [Google Scholar] [CrossRef]

- Mantegna, R.N. Lévy walks and enhanced diffusion in Milan stock exchange. Physica A 1991, 179, 232–242. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional brownian motions, fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Samorodnitsky, G.; Taqqu, M. Stable Non-Gaussian Random Processes: Stochastic Models with Infinte Variance, 1st ed.; Chapman and Hall: New York, NY, USA, 1994. [Google Scholar]

- Fama, E.F.; Roll, R. Some properties of symmetric stable distributions. J. Am. Stat. Assoc. 1968, 63, 817–836. [Google Scholar] [CrossRef]

- Kogon, S.M.; Manolakis, G. Signal modeling with self- similar α/-stable processes: The fractional Levy stable motion model. IEEE Trans. Signal Process. 1996, 44, 1006–1010. [Google Scholar] [CrossRef]

- Samorodnitsky, G.; Taqqu, M. Linear models with long-range dependence and with finite and infinite variance. In The IMA Volumes in Mathematics and Its Applications, 1st ed.; New Directions in Time Series Analysis; Brillinger, D., Caines, P., Geweke, J., Parzen, E., Rosenblatt, M., Taqqu, M.S., Eds.; Springer: New York, NY, USA, 1993; pp. 325–340. [Google Scholar]

- Song, W.; Cattani, C.; Chi, C.-H. Multifractional Brownian motion and quantum-behaved particle swarm optimization for short term power load forecasting: An integrated approach. Energy 2020, 194, 116847. [Google Scholar] [CrossRef]

- Liu, H.; Song, W.; Li, M.; Kudreyko, A.; Zio, E. Fractional Lévy stable motion: Finite difference iterative forecasting model. Chaos 2020, 133, 109632. [Google Scholar] [CrossRef]

- Eke, A.; Herman, P.; Kocsis, L.; Kozak, L.R. Fractal characterization of complexity in temporal physiological signals. Physiol. Meas. 2002, 23, R1–R38. [Google Scholar] [CrossRef]

- Caccia, D.C.; Percival, D.; Cannon, M.J.; Raymond, G.; Bassingthwaighte, J.B. Analyzing exact fractal time series: Evaluating dispersional analysis and rescaled range methods. Physica A 1997, 246, 609–632. [Google Scholar] [CrossRef]

- Bakalis, E.; Ferraro, A.; Gavriil, V.; Pepe, F.; Kollia, Z.; Cefalas, A.-C.; Malapelle, U.; Sarantopoulou, E.; Troncone, G.; Zerbetto, F. Universal Markers Unveil Metastatic Cancerous Cross-Sections at Nanoscale. Cancers 2022, 14, 3728. [Google Scholar] [CrossRef]

- Barabási, A.-L.; Viscek, T. Multifractality of self-affine fractals. Phys. Rev. A 1991, 44, 2730. [Google Scholar] [CrossRef]

- Sändig, N.; Bakalis, E.; Zerbetto, F. Stochastic analysis of movements on surfaces: The case of C60 on Au(1 1 1). Chem. Phys. Lett. 2015, 633, 163–168. [Google Scholar] [CrossRef]

- Bakalis, E.; Mertzimekis, T.J.; Nomikou, P.; Zerbetto, F. Breathing modes of Kolumbo submarine volcano (Santorini, Greece). Sci. Rep. 2017, 7, 46515. [Google Scholar] [CrossRef]

- Taqqu, M.S.; Teverovsky, V.; Willinger, W. Estimators for long-range dependence: An empirical study. Fractals 1995, 3, 785–798. [Google Scholar] [CrossRef]

- Laskin, N.; Lambadaris, I.; Harmantzis, F.C.; Devetsikiotis, M. Fractional Lévy motion and its application to network traffic modeling. Comput. Netw. 2002, 40, 363–375. [Google Scholar] [CrossRef]

- Gómez-Águila, A.; Trinidad-Segovia, J.E.; Sánchez-Granero, M.A. Improvement in Hurst exponent estimation and its application to financial markets. Financ. Innov. 2022, 8, 86. [Google Scholar] [CrossRef]

- Richman, J.S.; Moorman, J.R. Physiological time- series analysis using approximate entropy and sample entropy. Am. J. Physiol. Heart Circ. Physiol. 2000, 278, H2039–H2049. [Google Scholar] [CrossRef]

- Olbrys, J.; Ostrowski, K. An entropy-based approach to measurement of stock market depth. Entropy 2021, 23, 568. [Google Scholar] [CrossRef] [PubMed]

- Sokunbi, M.O.; Gradin, V.B.; Waiter, G.D.; Cameron, G.G.; Ahearn, T.F.; Murray, A.D.; Steele, D.J.; Staff, R.T. Nonlinear Complexity Analysis of Brain fMRI Signals in Schizophrenia. PLoS ONE 2014, 9, e105741. [Google Scholar] [CrossRef] [PubMed]

- Mandelbrot, B.B. The Fractal Geometry of Nature, 1st ed.; W. H. Freeman & Company: New York, NY, USA, 2008; 480p. [Google Scholar]

- Grassberger, P. Generalized dimensions of strange attractors. Phys. Lett. A 1983, 97, 227–230. [Google Scholar] [CrossRef]

- Hentschel, H.G.E.; Procaccia, I. The infinite number of generalized dimensions of fractals and strange attractors. Physica D 1983, 8, 435–444. [Google Scholar] [CrossRef]

- Kolmogorov, A.N. A refinement of previous hypotheses concerning the local structure of turbulence in a viscous incompressible fluid at high Reynolds number. J. Fluid. Mech. 1962, 13, 82–85. [Google Scholar] [CrossRef]

- Bakalis, E.; Gavriil, V.; Cefalas, A.-C.; Kollia, Z.; Zerbetto, F.; Sarantopoulou, E. Viscoelasticity and Noise Properties Reveal the Formation of Biomemory in Cells. J. Phys. Chem. B 2021, 125, 10883–10892. [Google Scholar] [CrossRef] [PubMed]

- Bakalis, E.; Fujie, H.; Zerbetto, F.; Tanaka, Y. Multifractal structure of microscopic eye–head coordination. Physica A 2018, 512, 945–953. [Google Scholar] [CrossRef]

- Bakalis, E.; Mertzimekis, T.J.; Nomikou, P.; Zerbetto, F. Temperature and Conductivity as Indicators of the Morphology and Activity of a Submarine Volcano: Avyssos (Nisyros) in the South Aegean Sea, Greece. Geosciences 2018, 8, 193. [Google Scholar] [CrossRef]

- Andersen, K.; Castiglione, P.; Mazzino, A.; Vulpiani, A. Simple stochastic models showing strong anomalous diffusion. Eur. Phys. J. B 2000, 18, 447–452. [Google Scholar] [CrossRef]

- Fuliński, A. Fractional Brownian motions: Memory, diffusion velocity, and correlation functions. J. Phys. A Math. Theor. 2017, 50, 054002. [Google Scholar] [CrossRef]

- Bénichou, O.; Oshanin, G. A unifying representation of path integrals for fractional Brownian motions. J. Phys. A Math. Theor. 2024, 57, 2250012. [Google Scholar] [CrossRef]

- Bakalis, E.; Lugli, F.; Zerbetto, F. Daughter Coloured Noises: The Legacy of Their Mother White Noises Drawn from Different Probability Distributions. Fractal Fract. 2023, 7, 600. [Google Scholar] [CrossRef]

- Mercik, S.; Weron, K.; Burnecki, K.; Weron, A. Enigma of Self-Similarity of Fractional Lévy Stable Motions. Acta Polonica B 2003, 34, 3773–3791. [Google Scholar]

- Nakao, H. Multi-scaling properties of truncated Lévy flights. Phys. Lett. A 2000, 266, 282–289. [Google Scholar] [CrossRef]

- Janicki, A.; Weron, A. Can One See α-Stable Variables and Processes? Stat. Sci. 1994, 9, 109–126. [Google Scholar] [CrossRef]

- Yan, L.; Shen, G.; He, K. Itô’s formula for a sub-fractional Brownian motion. Commun. Stoc. Anal. 2011, 5, 135–159. [Google Scholar] [CrossRef]

- Jumarie, G. On the representation of fractional Brownian motion as an integral with respect to (dt)α. Appl. Math. Lett. 2005, 18, 739–748. [Google Scholar] [CrossRef]

- Grassberger, P.; Procaccia, I. Estimation of the Kolmogorov entropy from a chaotic signal. Phys. Rev. A 1983, 28, 2591(R). [Google Scholar] [CrossRef]

- Grassberger, P.; Procaccia, I. Characterization of Strange Attractors. Phys. Rev. Lett. 1983, 50, 346. [Google Scholar] [CrossRef]

- Delgado-Bonal, A.; Marshak, A. Approximate Entropy and Sample Entropy: A Comprehensive Tutorial. Entropy 2019, 21, 541. [Google Scholar] [CrossRef]

- Martínez-Cagigal, V. Sample Entropy. Mathworks, 2018. Available online: https://mathworks.com/matlabcentral/fileexchange/69381-sample-entropy (accessed on 26 March 2025).

- Omidvarnia, A.; Mesbah, M.; Pedersen, M.; Jackson, G. Range Entropy: A Bridge between Signal Complexity and Self-Similarity. Entropy 2018, 20, 962. [Google Scholar] [CrossRef]

- The MathWorks Inc. MATLAB, Version: 9.13.0 (R2022b); The MathWorks Inc.: Natick, MA, USA, 2022. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bakalis, E.; Zerbetto, F. Iterative Forecasting of Financial Time Series: The Greek Stock Market from 2019 to 2024. Entropy 2025, 27, 497. https://doi.org/10.3390/e27050497

Bakalis E, Zerbetto F. Iterative Forecasting of Financial Time Series: The Greek Stock Market from 2019 to 2024. Entropy. 2025; 27(5):497. https://doi.org/10.3390/e27050497

Chicago/Turabian StyleBakalis, Evangelos, and Francesco Zerbetto. 2025. "Iterative Forecasting of Financial Time Series: The Greek Stock Market from 2019 to 2024" Entropy 27, no. 5: 497. https://doi.org/10.3390/e27050497

APA StyleBakalis, E., & Zerbetto, F. (2025). Iterative Forecasting of Financial Time Series: The Greek Stock Market from 2019 to 2024. Entropy, 27(5), 497. https://doi.org/10.3390/e27050497