Control of a New Financial Risk Contagion Dynamic Model Based on Finite-Time Disturbance

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. A Single Equilibrium New Chaotic System

2.1. Equilibria

2.2. Dissipativity

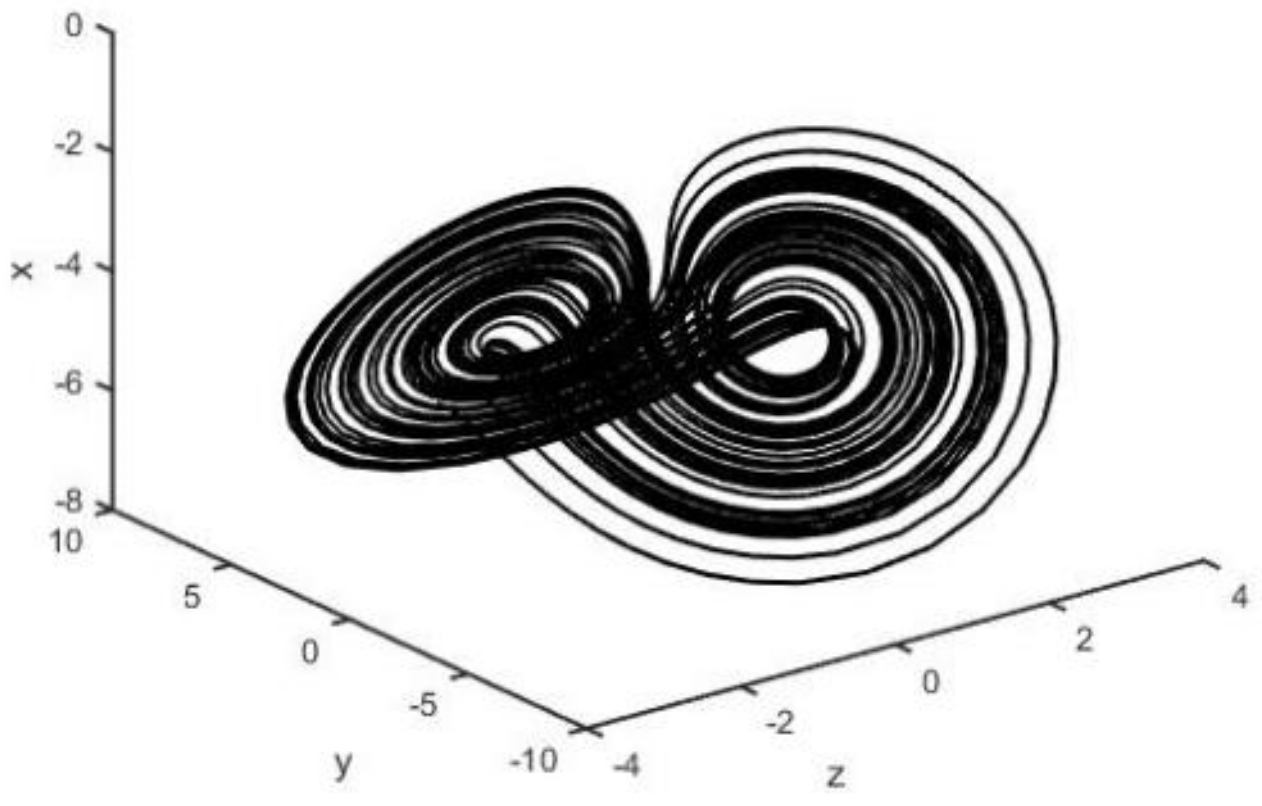

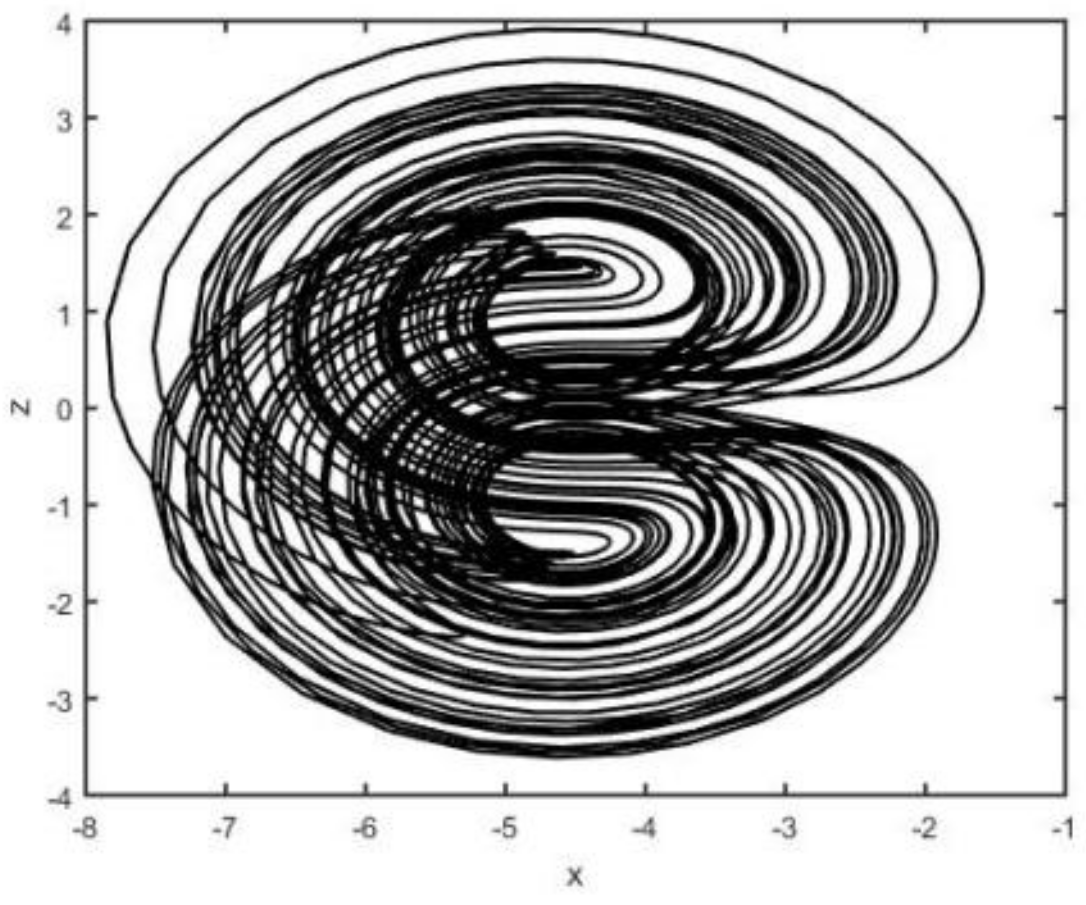

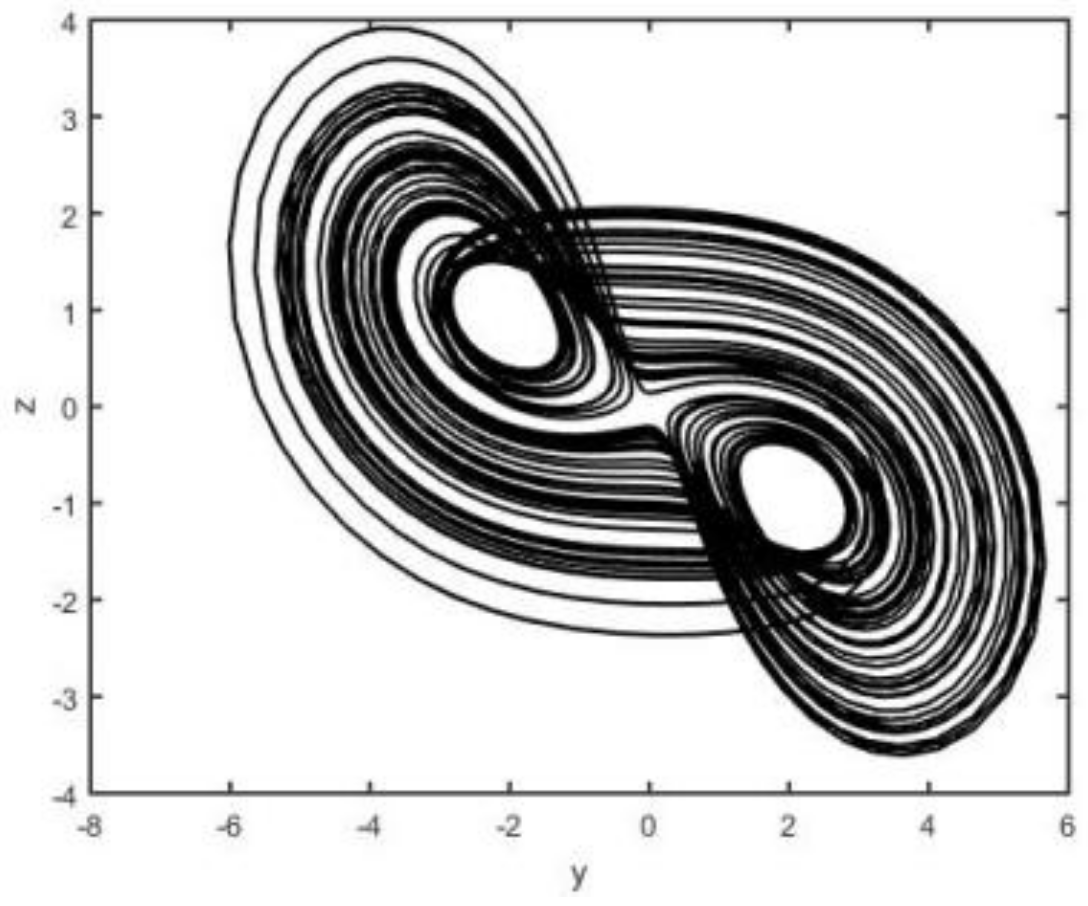

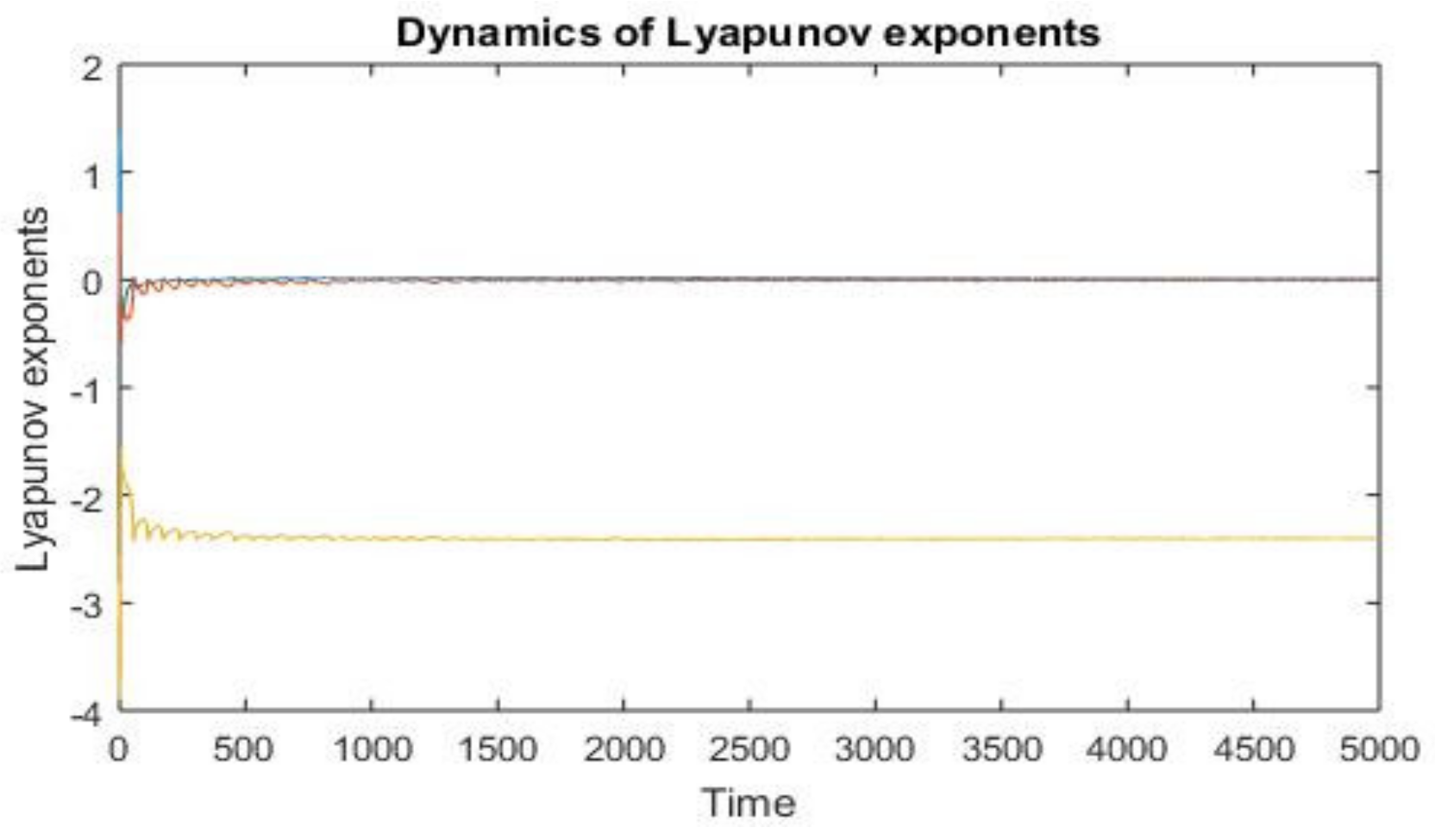

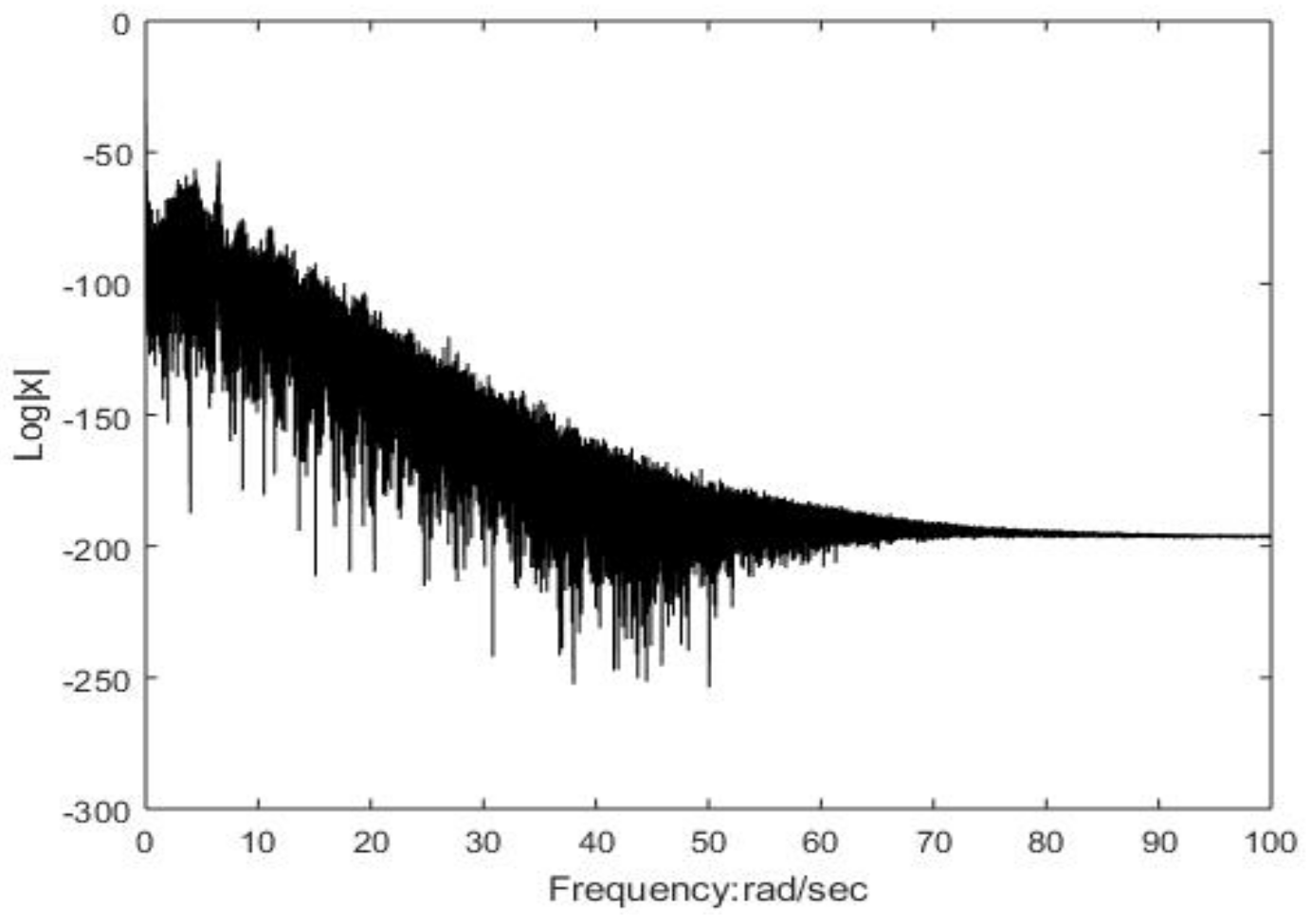

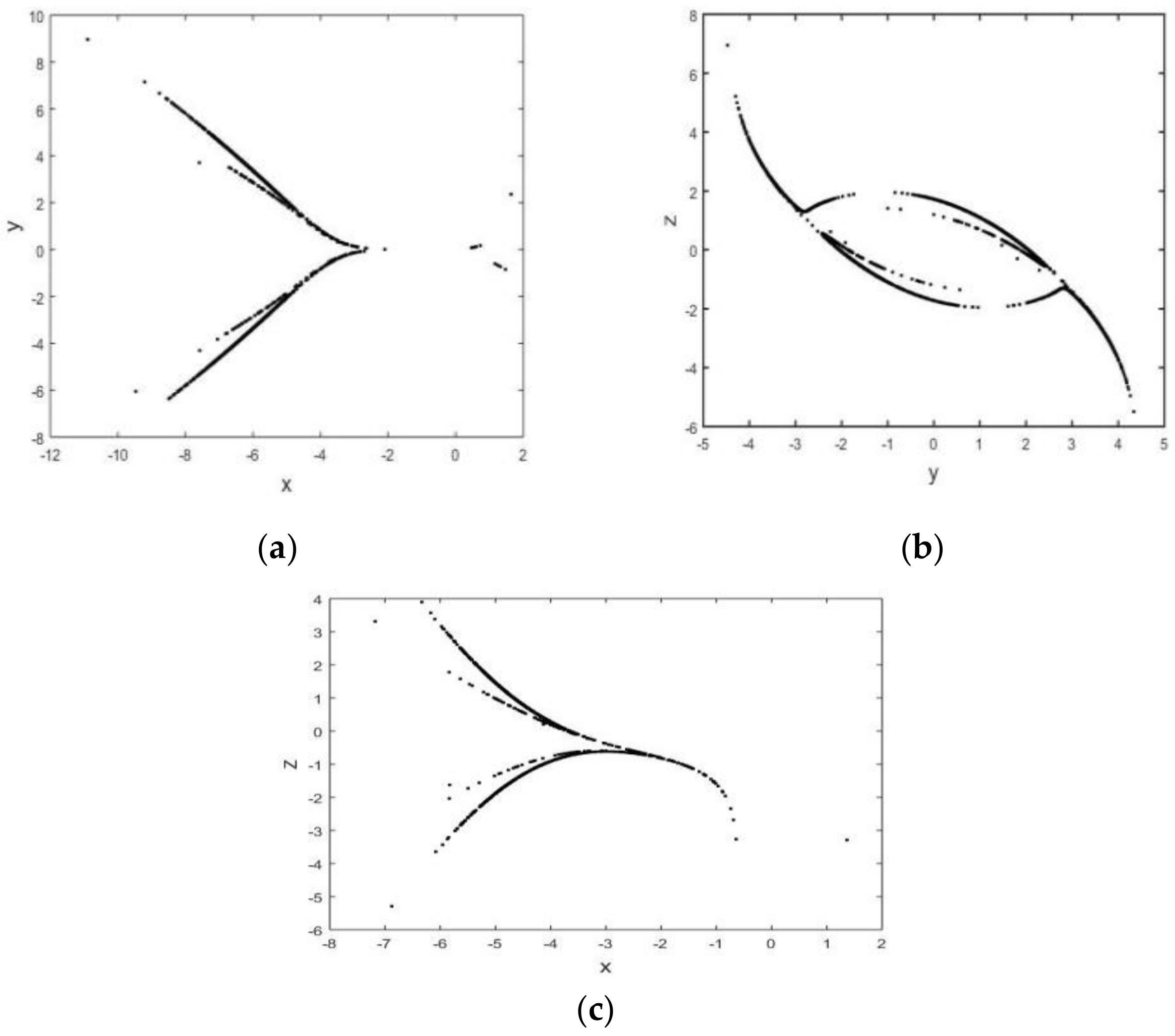

2.3. Chaotic Behavior of System (2)

3. FnT Control of Financial Risk Contagion Dynamic with Finite-Time Perturbation

3.1. General Method for Control of Chaotic Systems Based on Finite-Time Disturbance

3.2. FnT Control of Financial Risk Contagion Dynamic with Finite-Time Disturbance

3.3. A Simulation Example

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

References

- Xu, Y.F. Economic model and economic chaos. J. Xi’an Jiaotong Univ. 1994, 28, 83–86. [Google Scholar]

- Yang, Z.H.; Chen, L.X.; Chen, Y.T. Cross-market contagion of economic policy uncertainty and systemic financial risk: A nonlinear network connectedness analysis. Econ. Res. J. 2020, 1, 65–81. [Google Scholar]

- Chen, T.Q.; He, J.M.; Wang, J.N. Bifurcation and chaotic behavior of credit risk contagion based on Fitzhugh-Nagumo system. Int. J. Bifurc. Chaos 2013, 23, 1350117. [Google Scholar] [CrossRef]

- Yuan, Y.; Adrián, L.D. Limits to extreme event forecasting in chaotic systems. Phys. D 2024, 467, 134246. [Google Scholar] [CrossRef]

- Wu, J.; Xia, L. Double well stochastic resonance for a class of three-dimensional financial systems. Chaos Solitons Fractals 2024, 181, 114632. [Google Scholar] [CrossRef]

- Wen, C.; Yang, J. Complexity evolution of chaotic financial systems based on fractional calculus. Chaos Solitons Fractals 2019, 128, 242–251. [Google Scholar] [CrossRef]

- Ma, Y.; Li, W. Application and research of fractional differential equations in dynamic analysis of supply chain financial chaotic system. Chaos Solitons Fractals 2020, 130, 109417. [Google Scholar] [CrossRef]

- Shi, J.; He, K.; Fang, H. Chaos, Hopf bifurcation and control of a fractional-order delay financial system. Math. Comput. Simul. 2022, 194, 348–364. [Google Scholar] [CrossRef]

- Luo, C.Q.; Liu, L.; Wang, D. Multiscale financial risk contagion between international stock markets: Evidence from EMD-Copula-CoVaR analysis. N. Am. J. Econ. Financ. 2021, 58, 101512. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Boubaker, S.; Sensoy, A. Financial contagion during COVID–19 crisis. Financ. Res. Lett. 2021, 38, 101604. [Google Scholar] [CrossRef]

- Koliai, L. Extreme risk modeling: An EVT–pair-copulas approach for financial stress tests. J. Bank. Financ. 2016, 70, 1–22. [Google Scholar] [CrossRef]

- Zhang, S.; Zhu, X.; Liu, C. Stabilization of a 4D financial system with disturbance and uncertainty by UDE-based control method. J. Frankl. Inst. 2024, 361, 106897. [Google Scholar] [CrossRef]

- Huang, C.; Cai, L.; Cao, J. Linear control for synchronization of a fractional-order time-delayed chaotic financial system. Chaos Solitons Fractals 2018, 113, 326–332. [Google Scholar] [CrossRef]

- Huang, C.; Cao, J. Active control strategy for synchronization and anti-synchronization of a fractional chaotic financial system. Phys. A 2017, 473, 262–275. [Google Scholar] [CrossRef]

- Gong, X.L.; Liu, X.H.; Xiong, X. Chaotic analysis and adaptive synchronization for a class of fractional order financial system. Phys. A 2019, 522, 33–42. [Google Scholar] [CrossRef]

- Le Ny, J.; Pappas, G.J. Differentially private filtering. IEEE Trans. Autom. Control 2012, 59, 341–354. [Google Scholar] [CrossRef]

- Manitara, N.E.; Hadjicostis, C.N. Privacy-preserving asymptotic average consensus. In Proceedings of the Control Conference, Zurich, Switzerland, 17 July 2013; pp. 760–765. [Google Scholar]

- Duan, X.; He, J.; Cheng, P.; Mo, Y.; Chen, J. Privacy preserving maximum consensus. In Proceedings of the IEEE Conference on Decision and Control, Osaka, Japan, 15–18 December 2015; pp. 4517–4522. [Google Scholar]

- Huang, Z.; Mitra, S.; Dullerud, G. Differentially private iterative synchronous consensus. In Proceedings of the 2012 ACM Workshop on Privacy in the Electronic Society, New York, NY, USA, 15 October 2012; pp. 81–90. [Google Scholar]

- Liu, X.; Zhang, J.; Wang, J. Differentially private consensus algorithm for continuous-time heterogeneous multi-agent systems. Automatica 2020, 122, 109283. [Google Scholar] [CrossRef]

- Altafini, C. A system-theoretic framework for privacy preservation in continuous-time multiagent dynamics. Automatica 2020, 122, 109253. [Google Scholar] [CrossRef]

- Zhang, J.; Lu, J.; Lou, J. Privacy-preserving average consensus via finite time-varying transformation. IEEE Trans. Netw. Sci. Eng. 2022, 9, 1756–1764. [Google Scholar] [CrossRef]

- Xu, Y.; Gao, Q.; Xie, C.; Zhang, X.; Wu, X. Finite-time synchronization of complex networks with privacy-preserving. IEEE Trans. Circuits Syst. II Exp. Briefs 2023, 70, 4103–4107. [Google Scholar] [CrossRef]

- Xu, Y.; Xie, C.; Wang, Y. Evolution mechanism of financial system risk. Stat. Decis. 2016, 1, 172–175. [Google Scholar]

- Xu, Y.; Zhou, W.; Fang, J.; Xie, X.; Tong, D. Finite-time synchronisation of the complex dynamical network with non-derivative and derivative coupling. Neurocomputing 2016, 173, 1356–1361. [Google Scholar] [CrossRef]

- Yan, S.R.; Mohammadzadeh, A.; Ghaderpour, E. Type-3 fuzzy logic and Lyapunov approach for dynamic modeling and analysis of financial markets. Heliyon 2024, 10, e33730. [Google Scholar] [CrossRef] [PubMed]

- Stella, L.; Bauso, D.; Blanchini, F.; Colaneri, P. Cascading failures in the global financial system: A dynamical model. Oper. Res. Lett. 2024, 55, 107122. [Google Scholar] [CrossRef]

- Wen, F.; Zhang, M.; Deng, M.; Zhao, Y.; Jian, O. Exploring the dynamic effects of financial factors on oil prices based on a TVP-VAR model. Phys. A 2019, 532, 121881. [Google Scholar] [CrossRef]

- Baur, D.G. Financial contagion and the real economy. J. Bank. Financ. 2012, 36, 2680–2698. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wei, Y.; Xie, C.; Qing, X.; Xu, Y. Control of a New Financial Risk Contagion Dynamic Model Based on Finite-Time Disturbance. Entropy 2024, 26, 999. https://doi.org/10.3390/e26120999

Wei Y, Xie C, Qing X, Xu Y. Control of a New Financial Risk Contagion Dynamic Model Based on Finite-Time Disturbance. Entropy. 2024; 26(12):999. https://doi.org/10.3390/e26120999

Chicago/Turabian StyleWei, Yifeng, Chengrong Xie, Xia Qing, and Yuhua Xu. 2024. "Control of a New Financial Risk Contagion Dynamic Model Based on Finite-Time Disturbance" Entropy 26, no. 12: 999. https://doi.org/10.3390/e26120999

APA StyleWei, Y., Xie, C., Qing, X., & Xu, Y. (2024). Control of a New Financial Risk Contagion Dynamic Model Based on Finite-Time Disturbance. Entropy, 26(12), 999. https://doi.org/10.3390/e26120999