A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

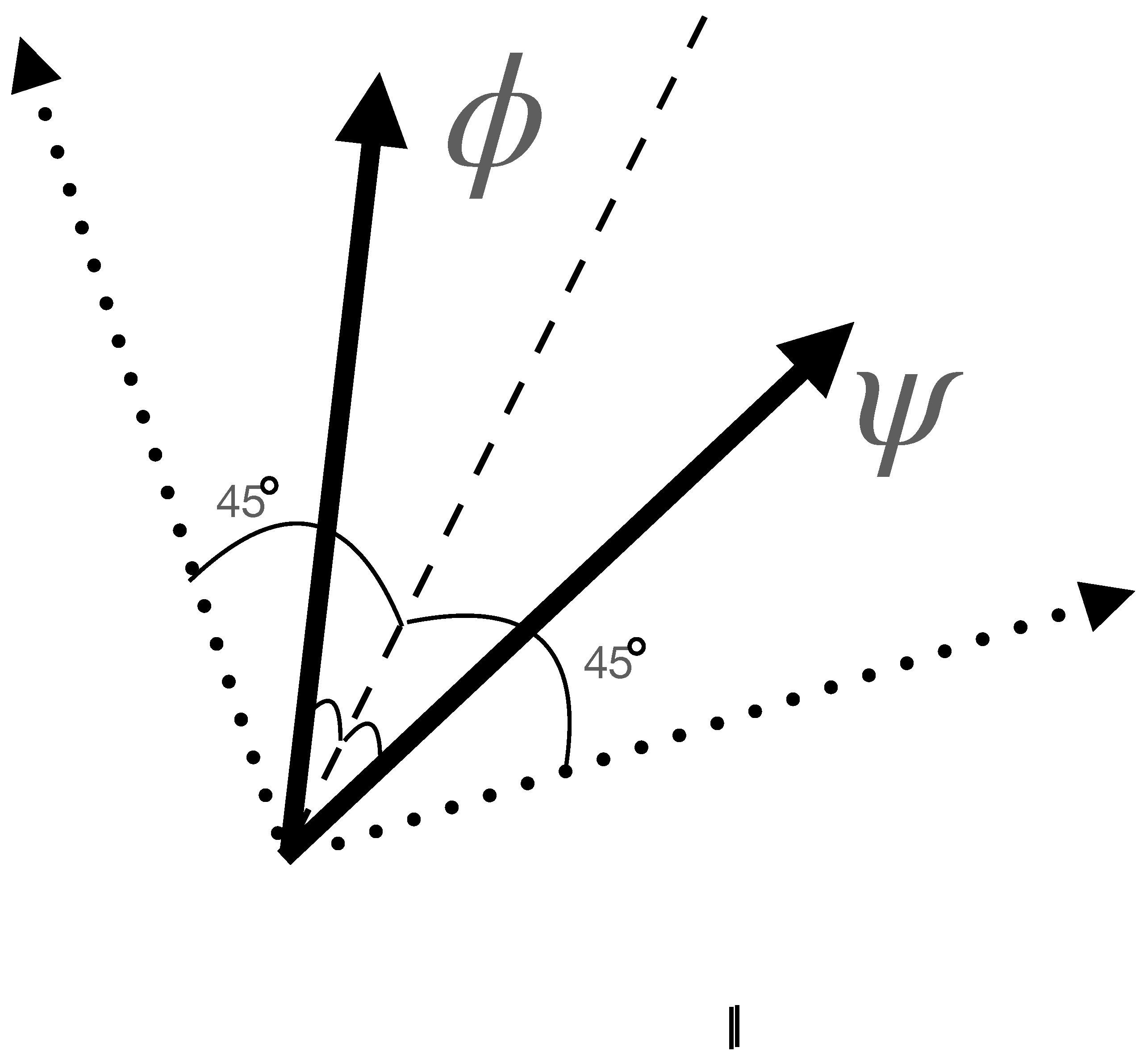

2. Gambling with Spin-1/2 Particles

3. The ‘Double-or-Nothing’ Game with Spin-1/2 Particles

4. The Optimal Strategy: A Heuristic Description

5. Numerical Simulation: Algorithm and Pseudo-Code

| Algorithm 1 Quantum Kelly Optimisation across N steps |

|

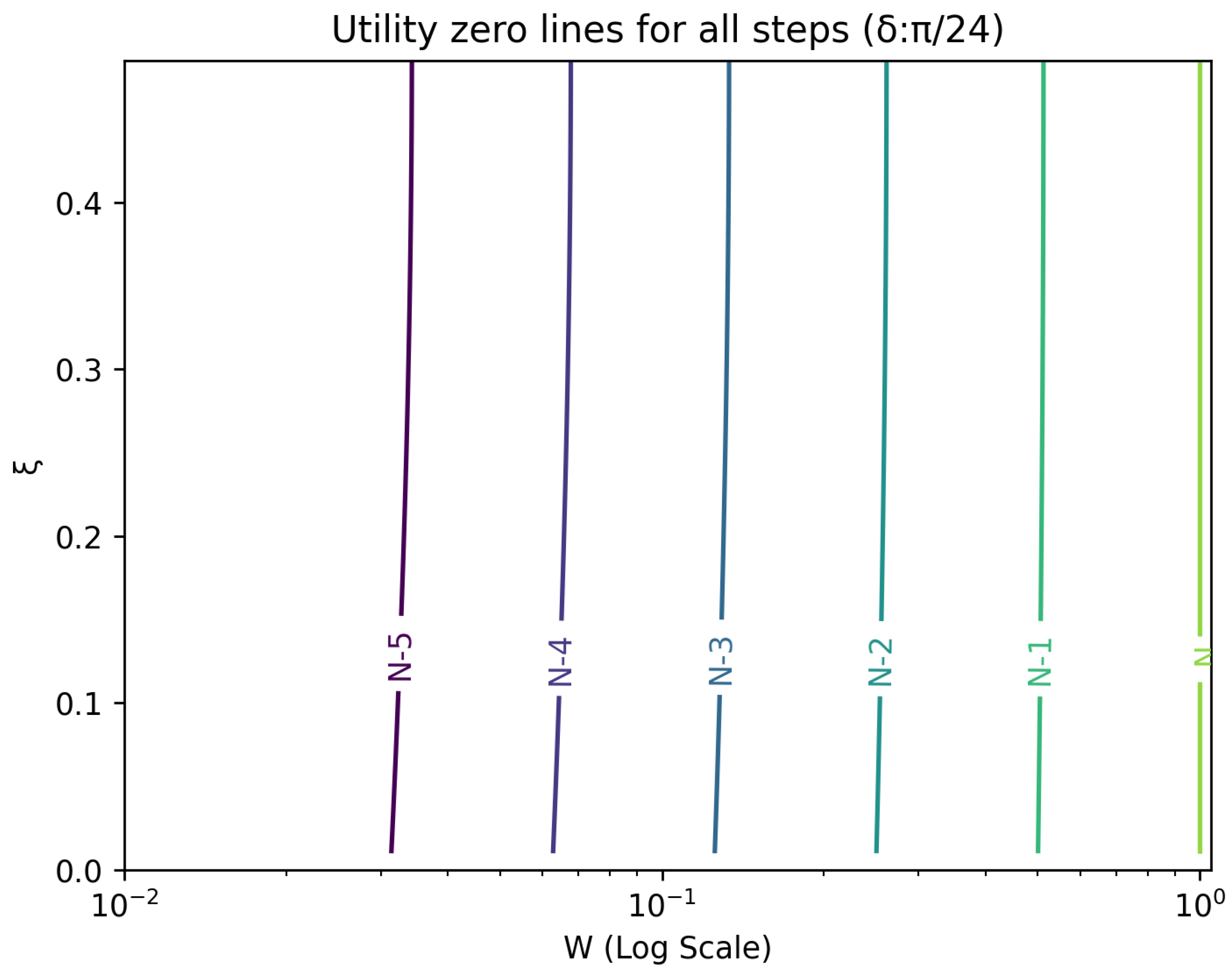

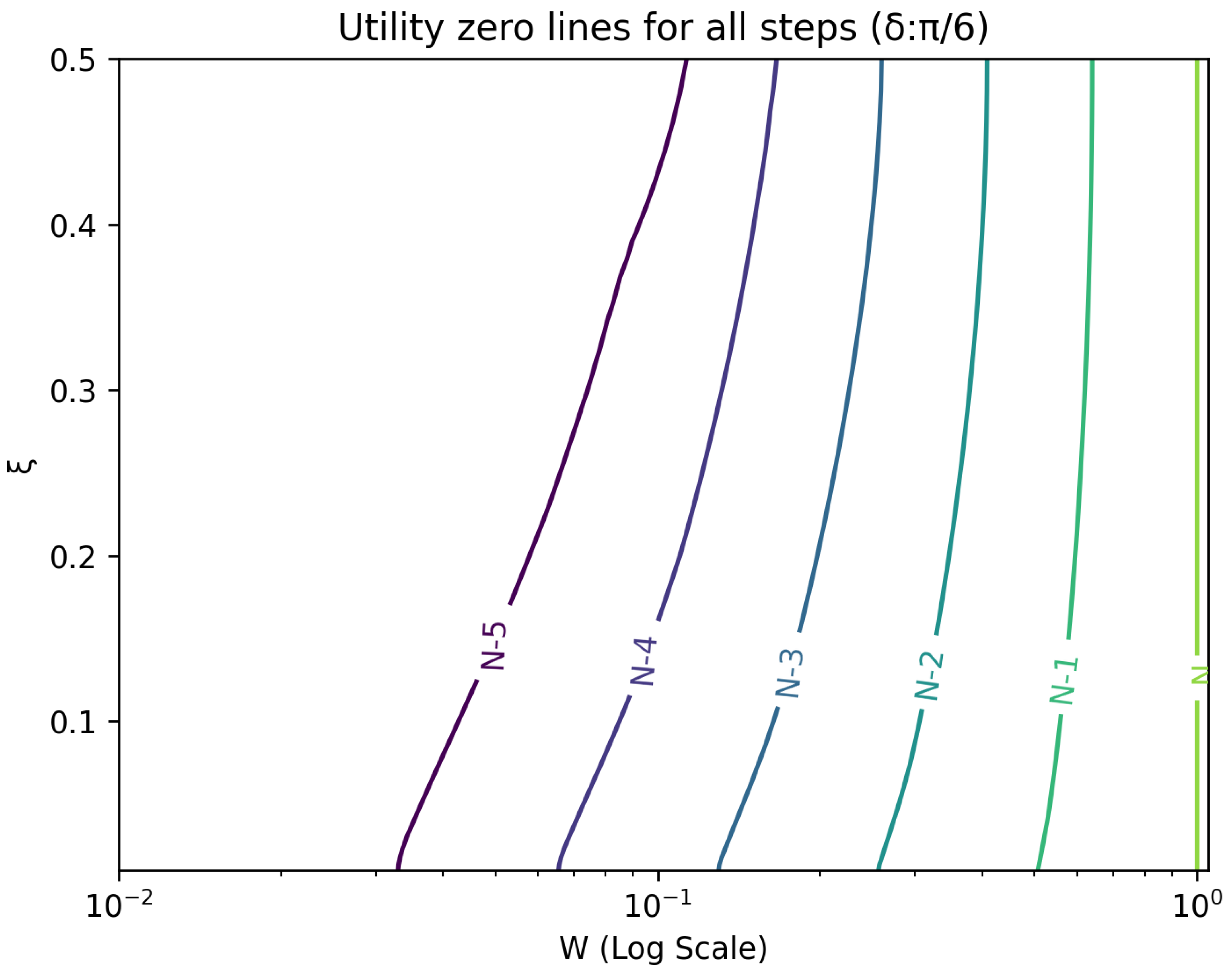

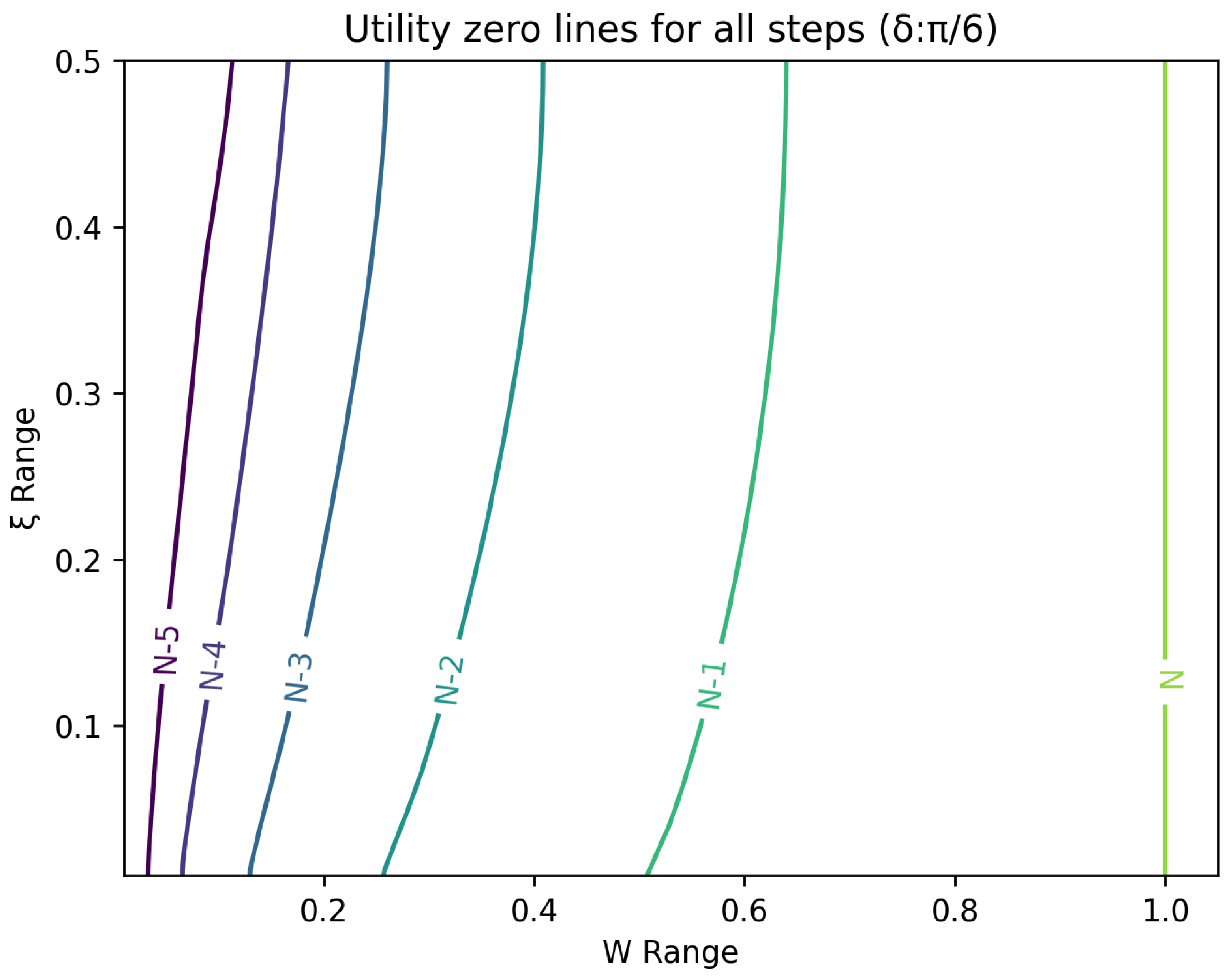

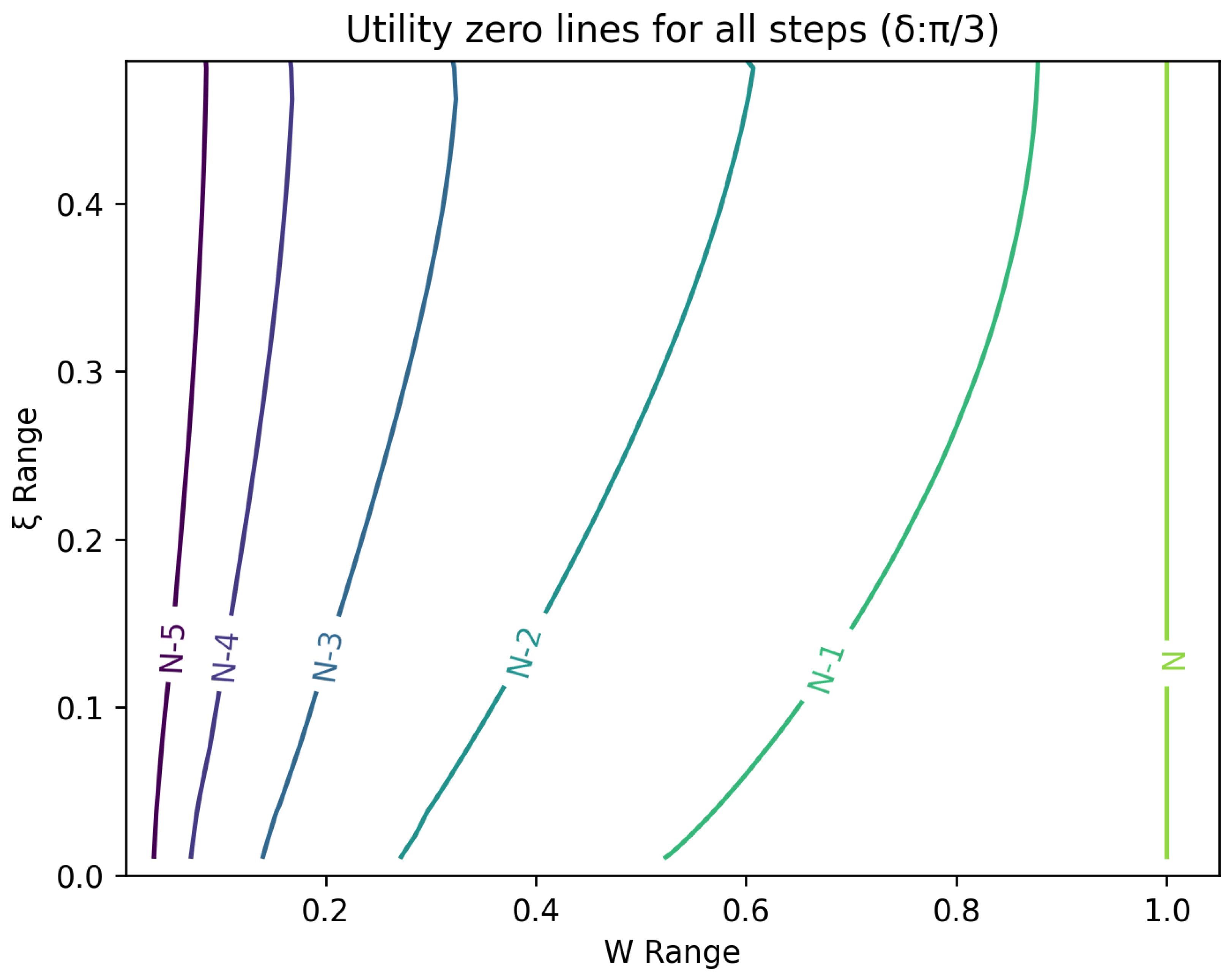

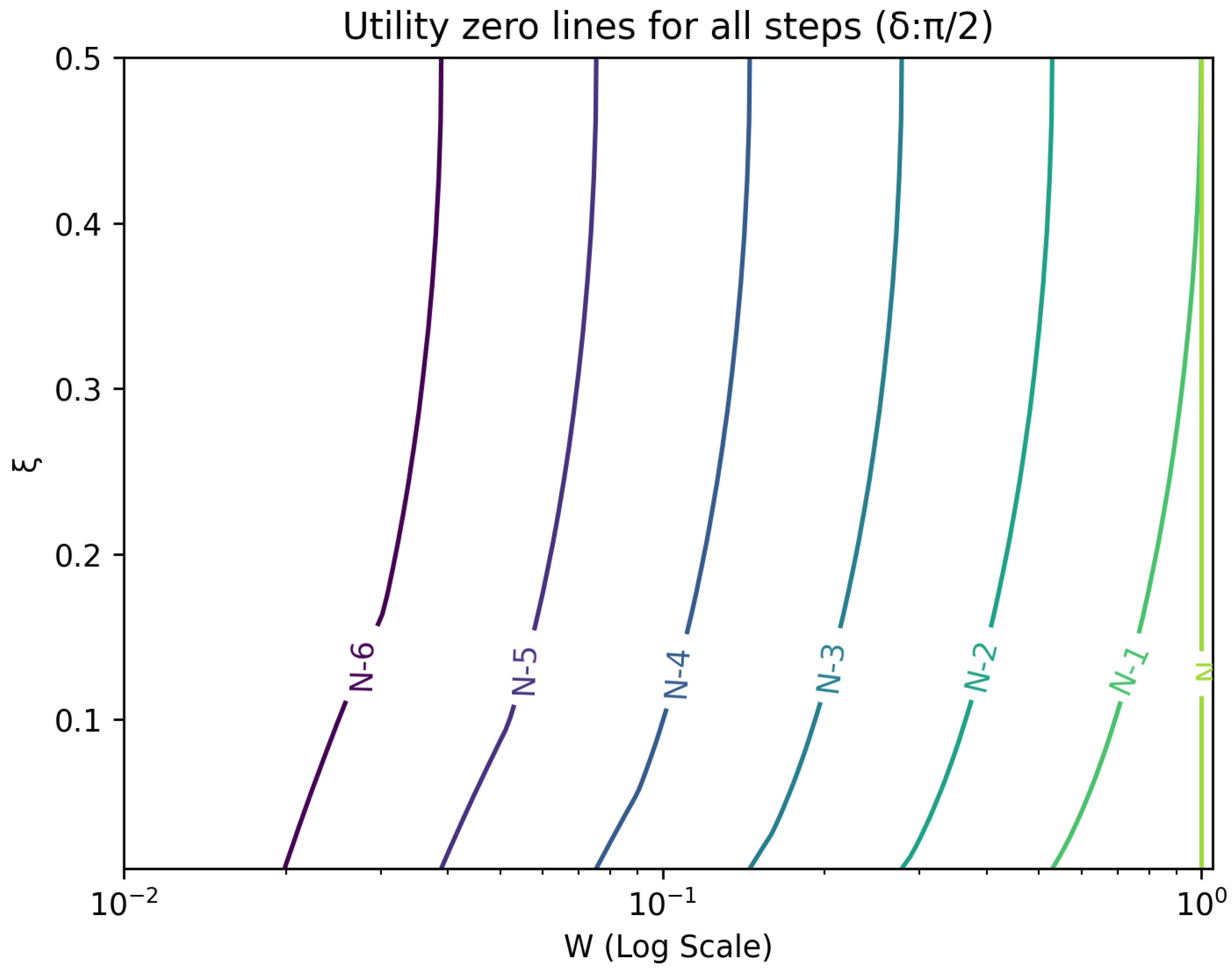

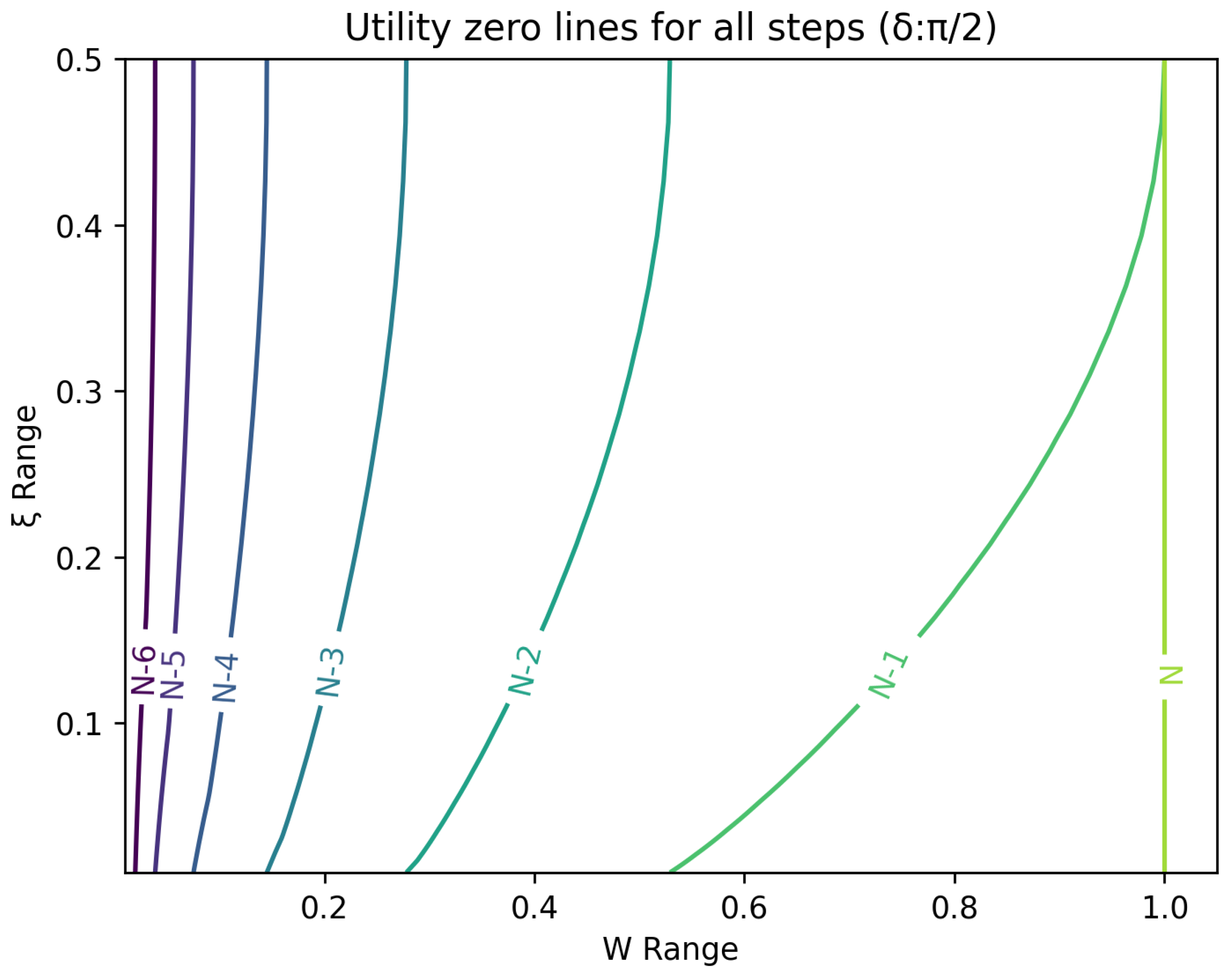

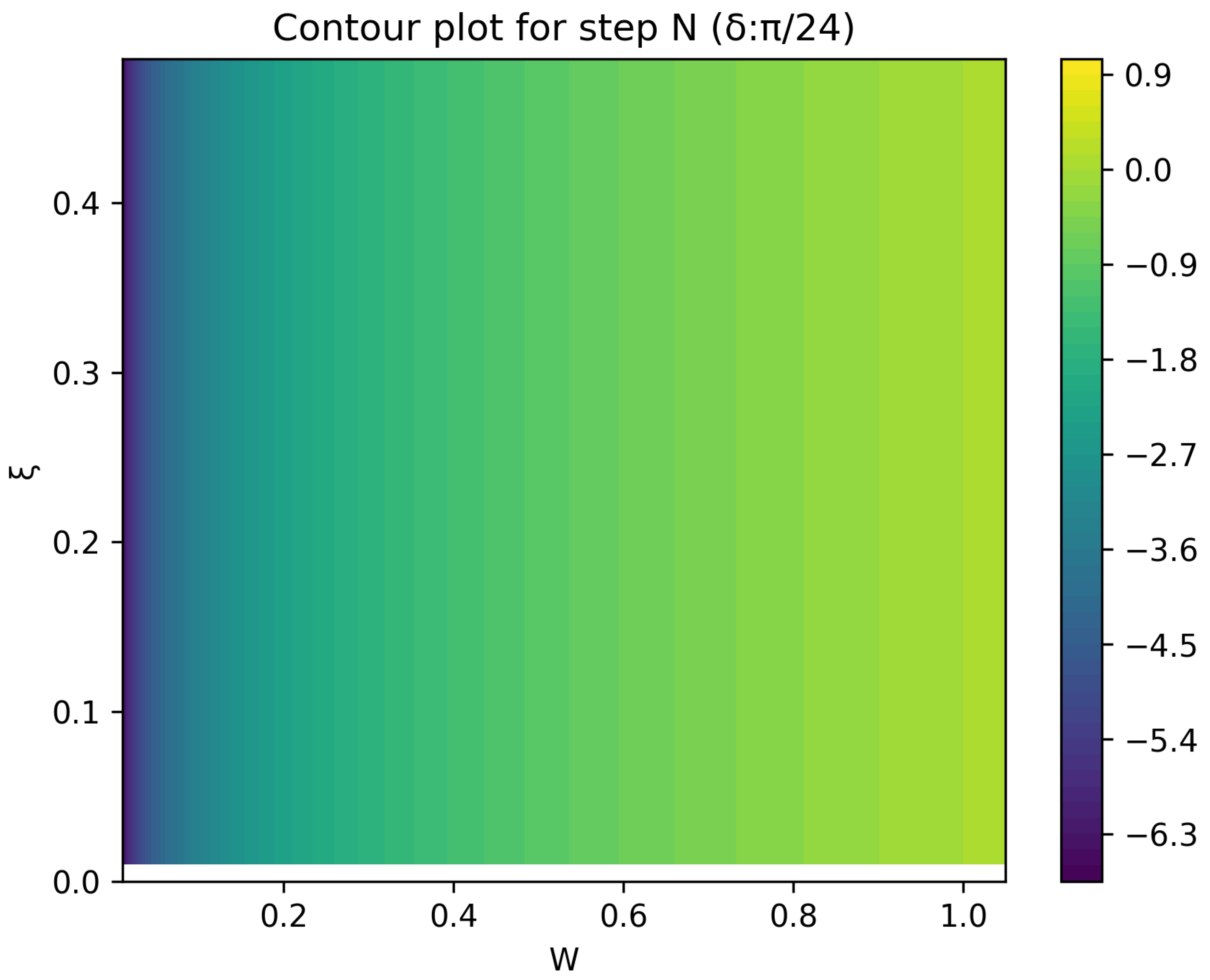

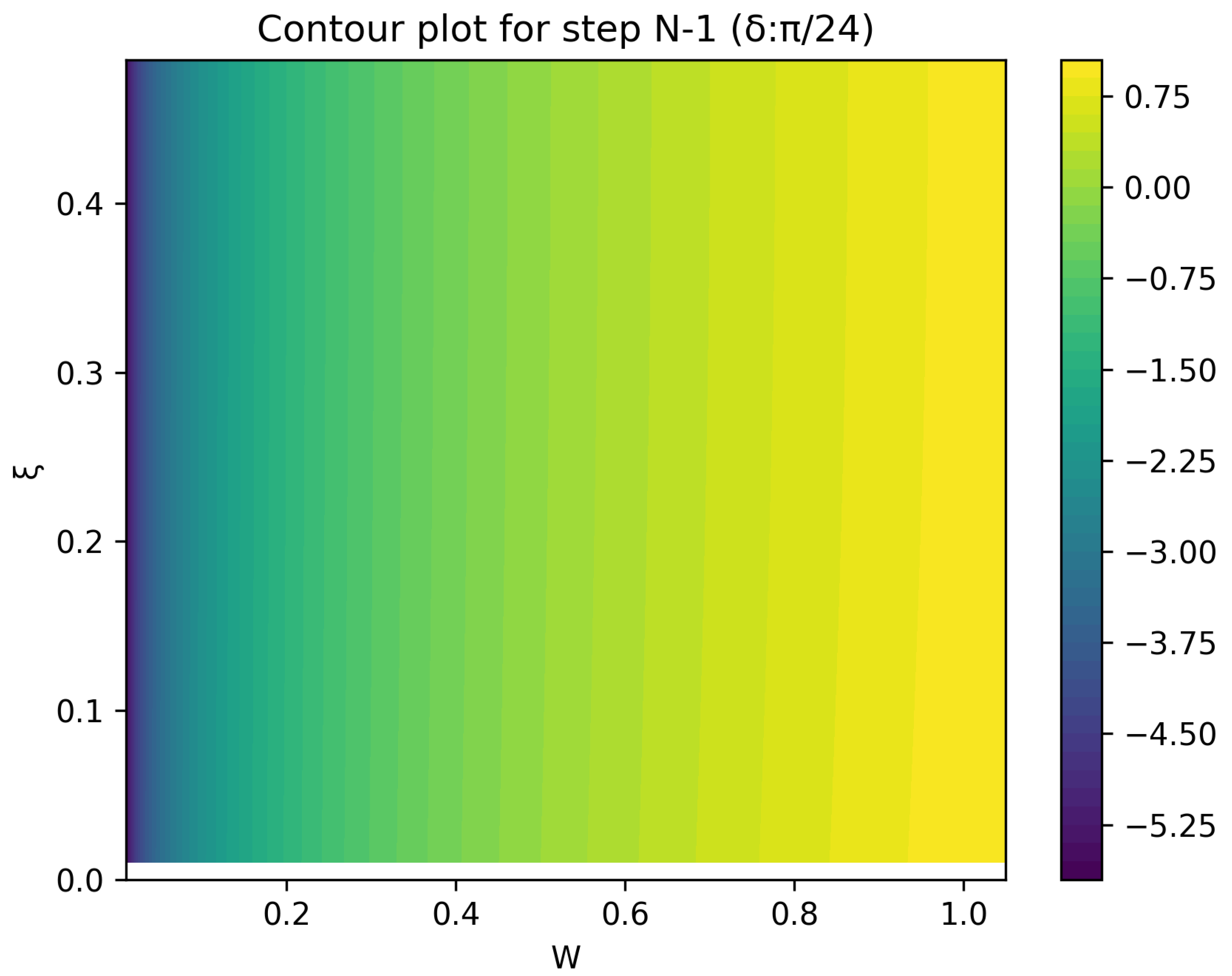

6. Contours of Equivalence

The Curious Case of Growth without Information Gain or Information Gain without Growth

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Kelly, J.L. A new Interpretation of the Information rate. Bell Syst. Tech. J. 1956, 35, 917–926. [Google Scholar] [CrossRef]

- MacLean, L.C.; Thorp, E.O.; Ziemba, W.T. (Eds.) The Kelly Criterion: Theory and Practice; World Scientific Publishing Company: Singapore, 2011. [Google Scholar]

- Breiman, L. Optimal gambling systems for favourable games. In Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, Berkeley, CA, USA, 20 June–30 July 1960; University of California Press: Berkeley, CA, USA, 1961; Volume 1, pp. 65–78. [Google Scholar]

- Bell, R.M.; Cover, T.M. Competitive optimality of logarithmic investment. Math. Oper. Res. 1980, 5, 161–166. [Google Scholar] [CrossRef]

- Helstrom, C.W. Quantum Detection and Estimation Theory; Academic Press, Inc.: Cambridge, MA, USA, 1976. [Google Scholar]

- Brody, D.C.; Meister, B.K. Minimum decision cost for quantum ensembles. Phys. Rev. Lett. 1996, 76, 1–4. [Google Scholar] [CrossRef] [PubMed]

- Thorpe, E.O. The Kelly criterion in blackjack sports betting, and the stock market. In Handbook of Asset and Liability Management; North-Holland Publishing Company: Amsterdam, The Netherlands, 2008; pp. 385–428. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Meister, B.K.; Price, H.C.W. A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins. Entropy 2024, 26, 66. https://doi.org/10.3390/e26010066

Meister BK, Price HCW. A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins. Entropy. 2024; 26(1):66. https://doi.org/10.3390/e26010066

Chicago/Turabian StyleMeister, Bernhard K., and Henry C. W. Price. 2024. "A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins" Entropy 26, no. 1: 66. https://doi.org/10.3390/e26010066

APA StyleMeister, B. K., & Price, H. C. W. (2024). A Quantum Double-or-Nothing Game: An Application of the Kelly Criterion to Spins. Entropy, 26(1), 66. https://doi.org/10.3390/e26010066