A More General Quantum Credit Risk Analysis Framework

, , ,

, , ,  ,

,

Abstract

1. Introduction

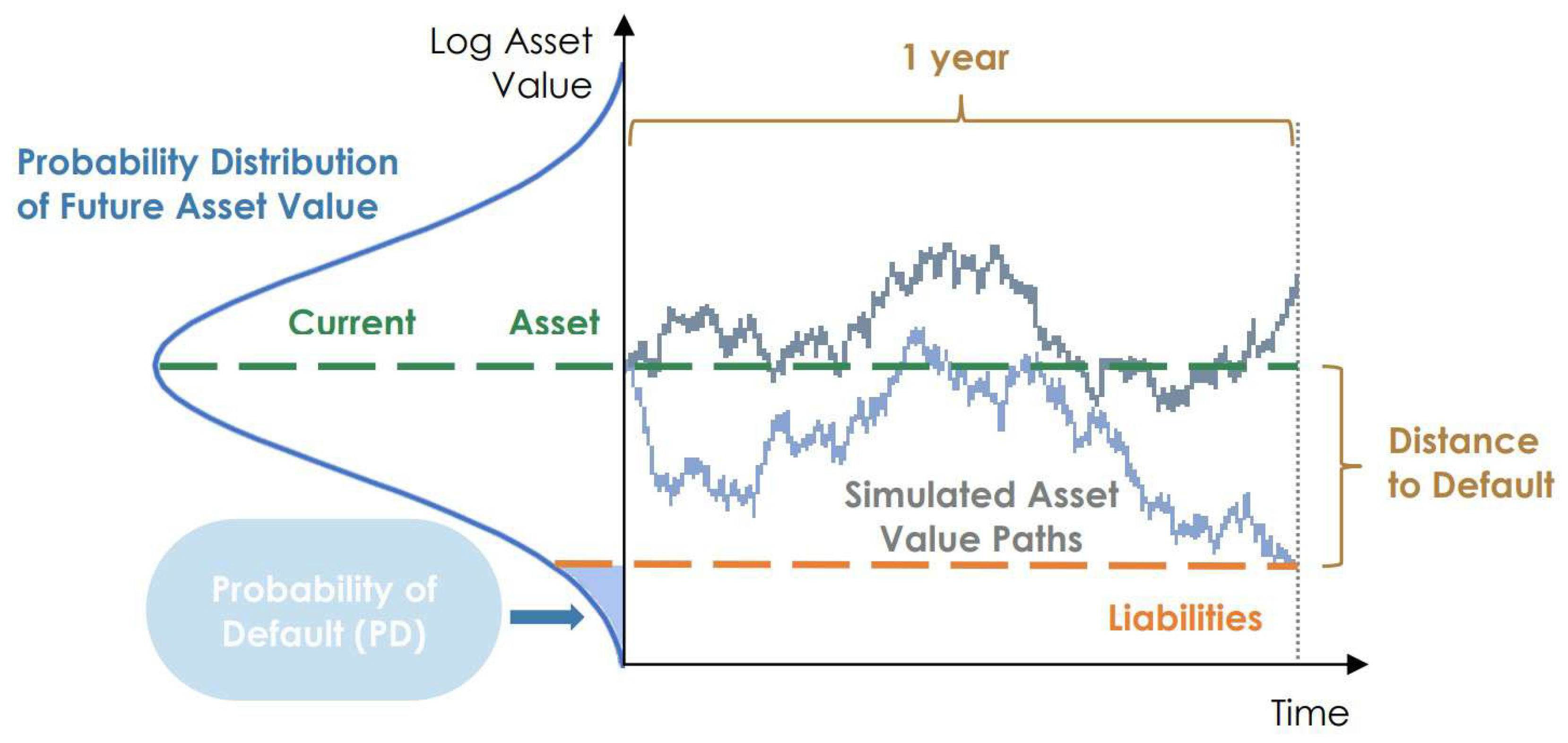

Quantum Finance and Credit Risk Analysis

2. Methods

2.1. SOTA Quantum Credit Risk Analysis

- , which loads the domain-dependent uncertainty model.

- , which computes the total loss over qubits.

- , which flips a target qubit if the total loss is equal to or lower than a certain threshold x.

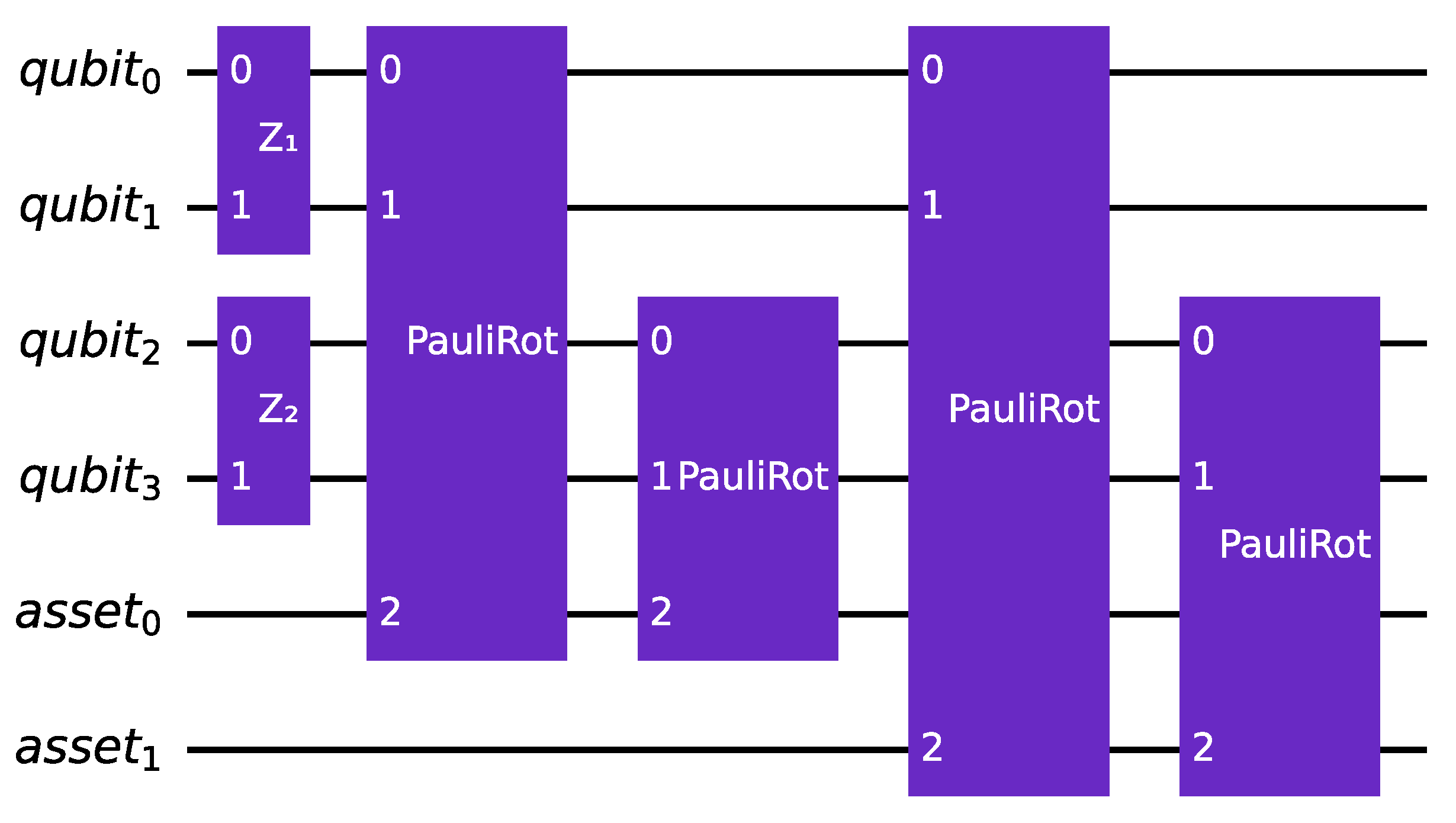

2.2. Multiple Risk Factors

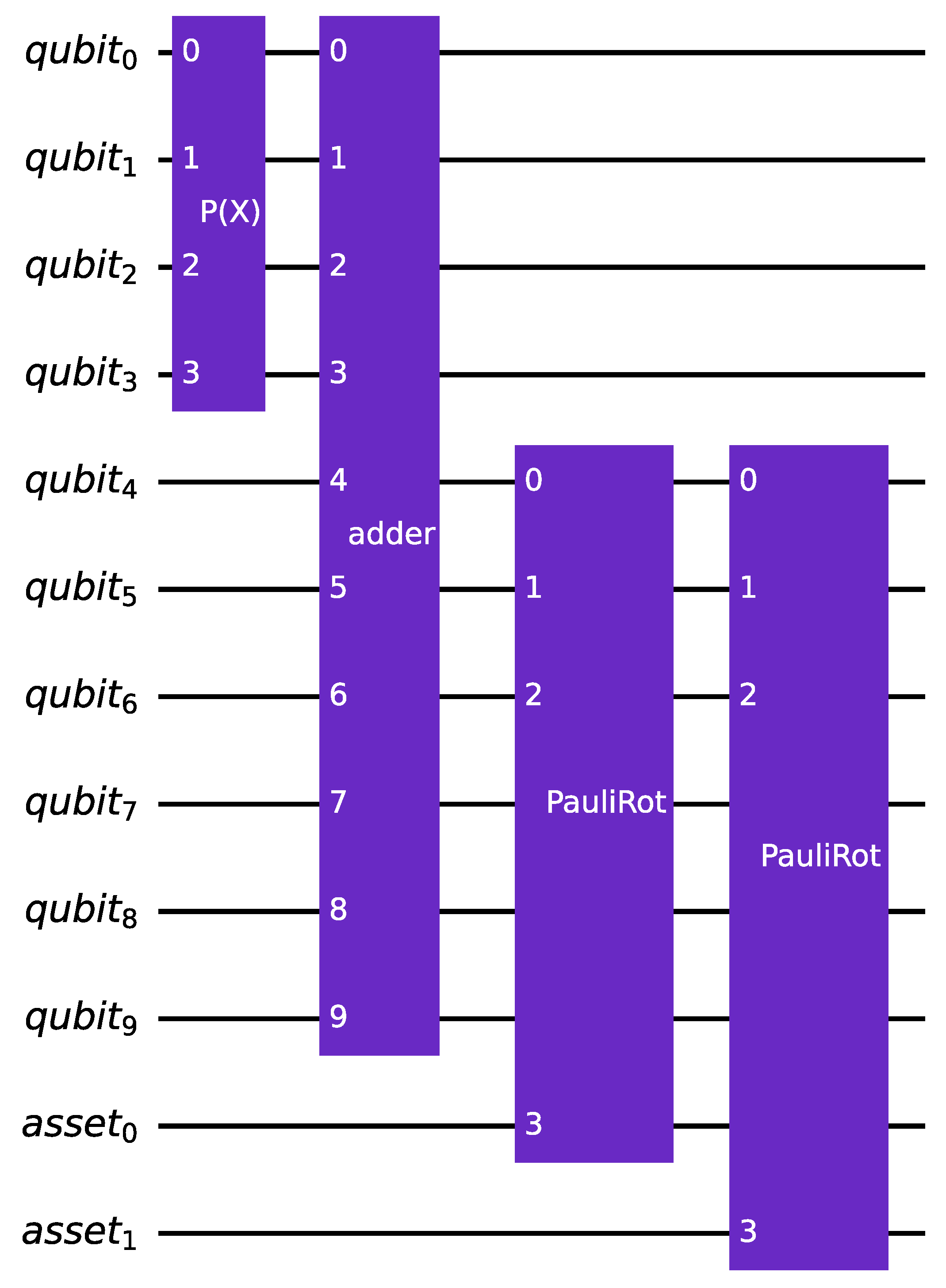

2.3. Arbitrary LGD

3. Results

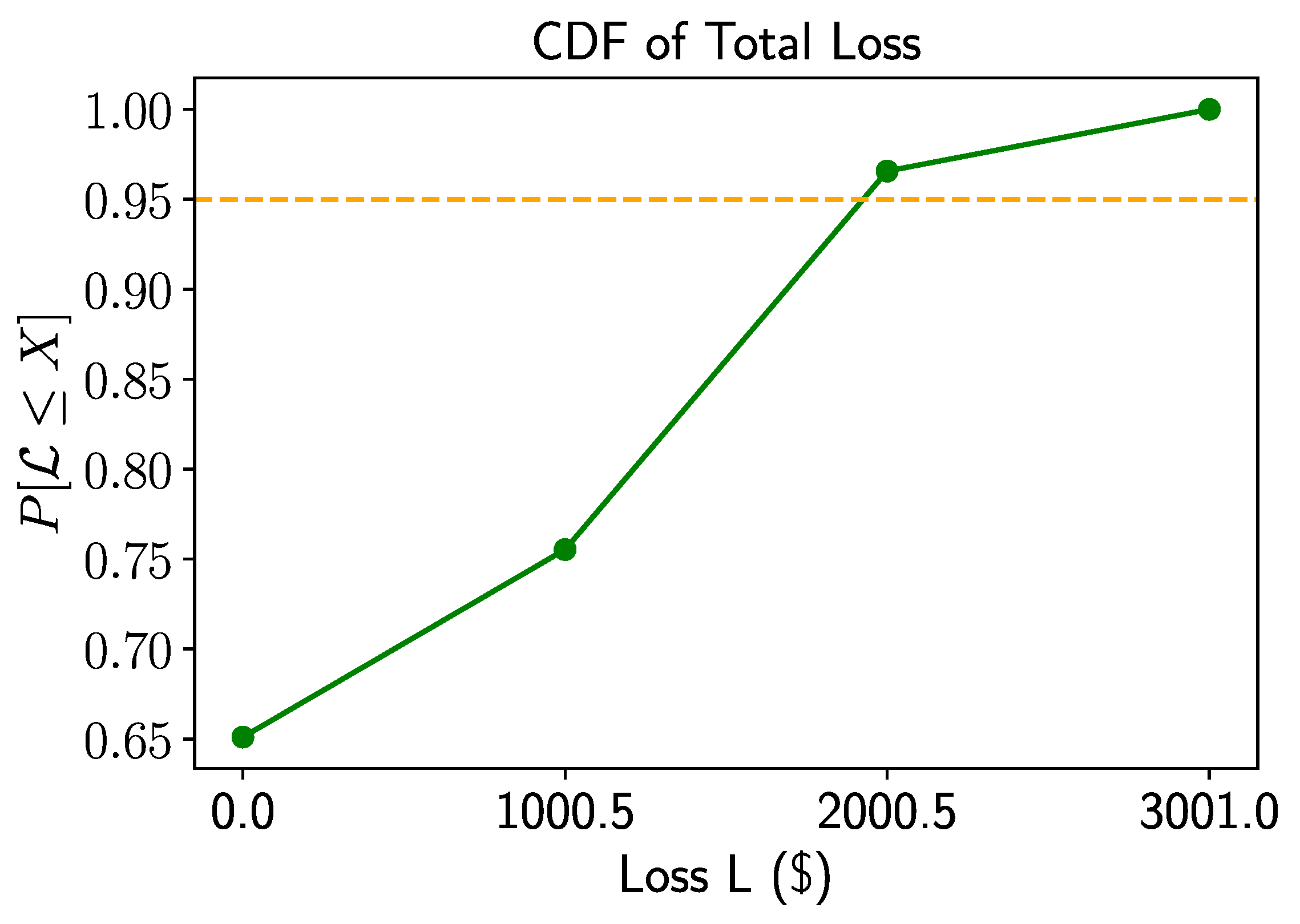

3.1. Noiseless Simulation

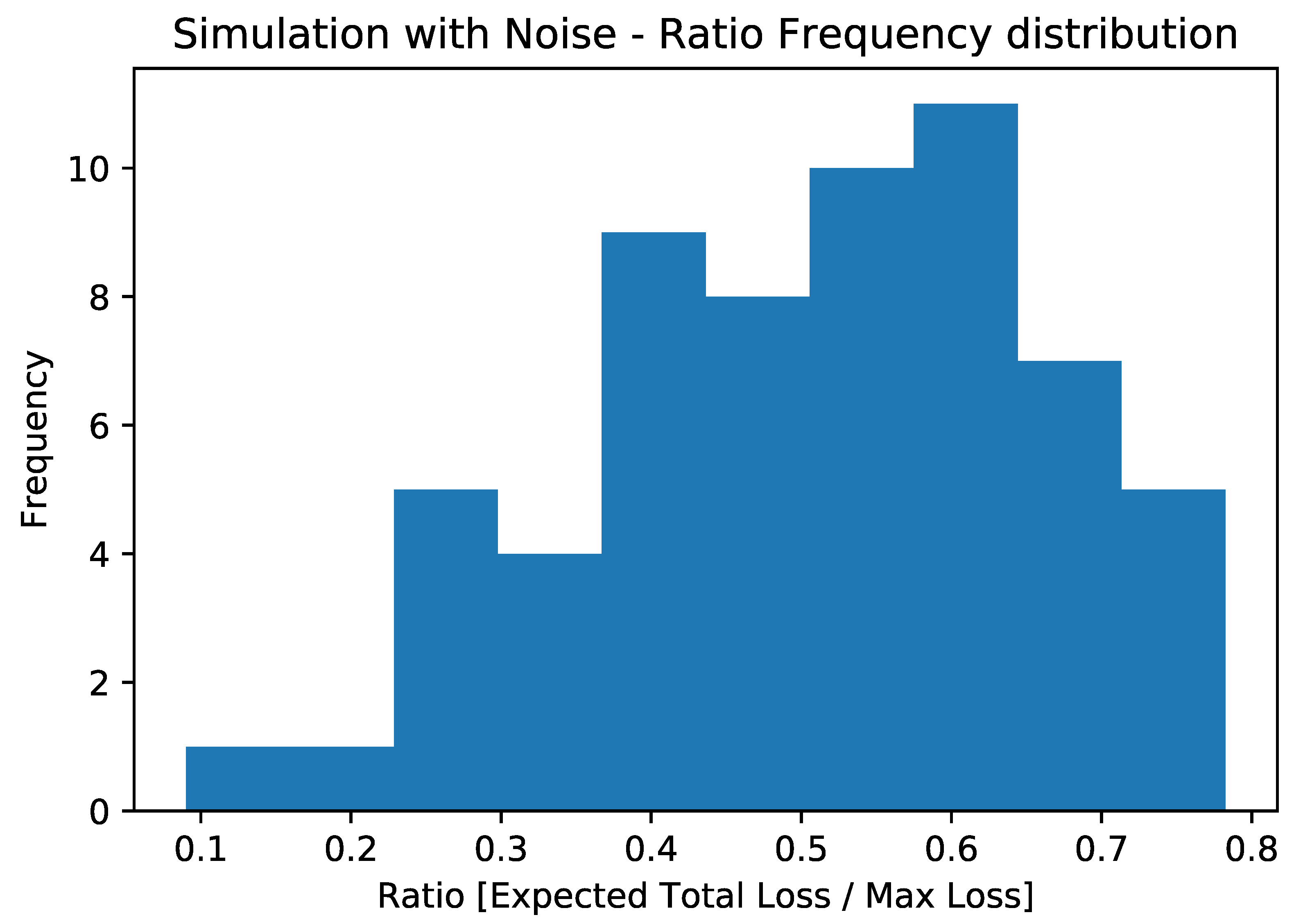

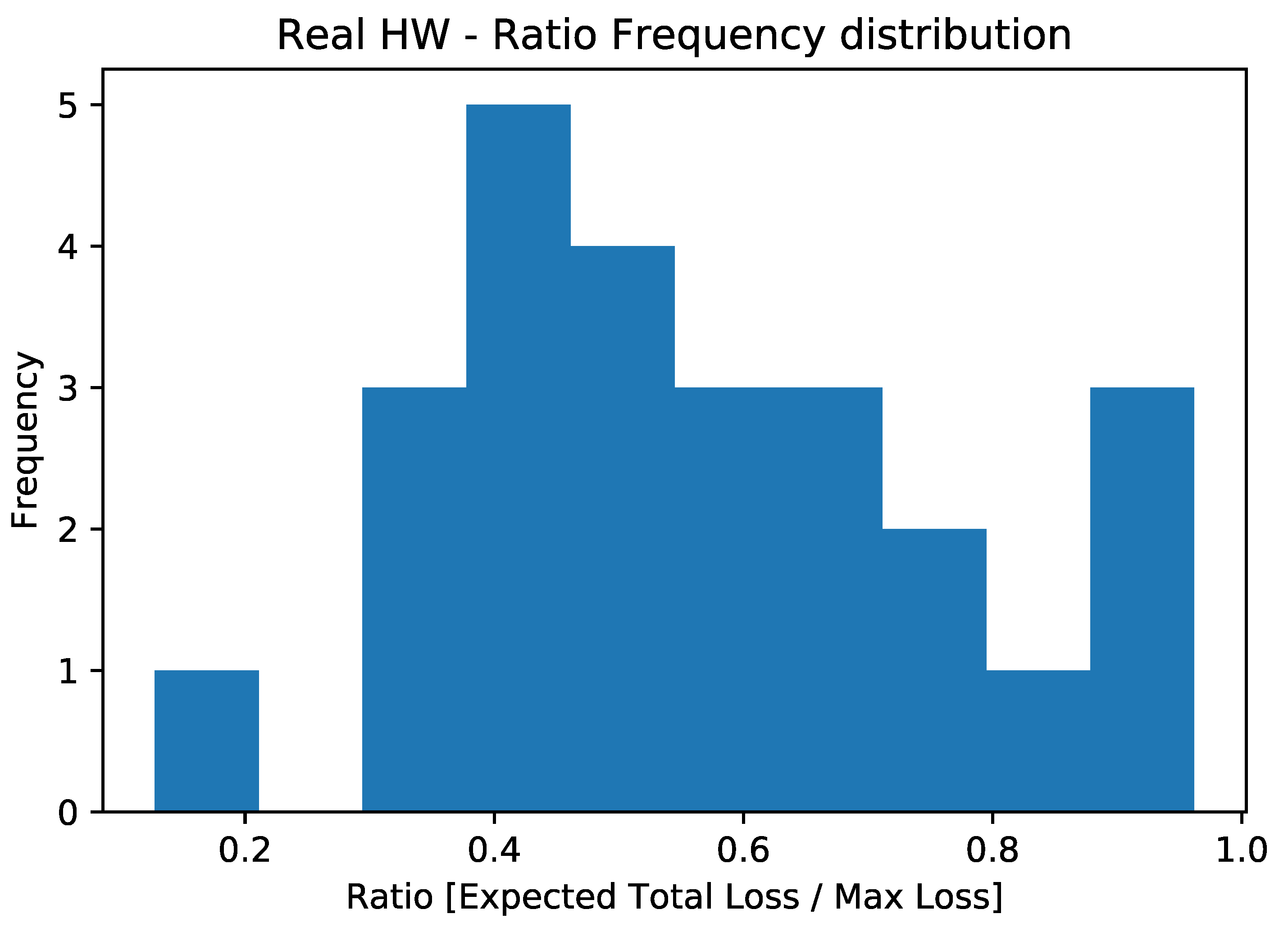

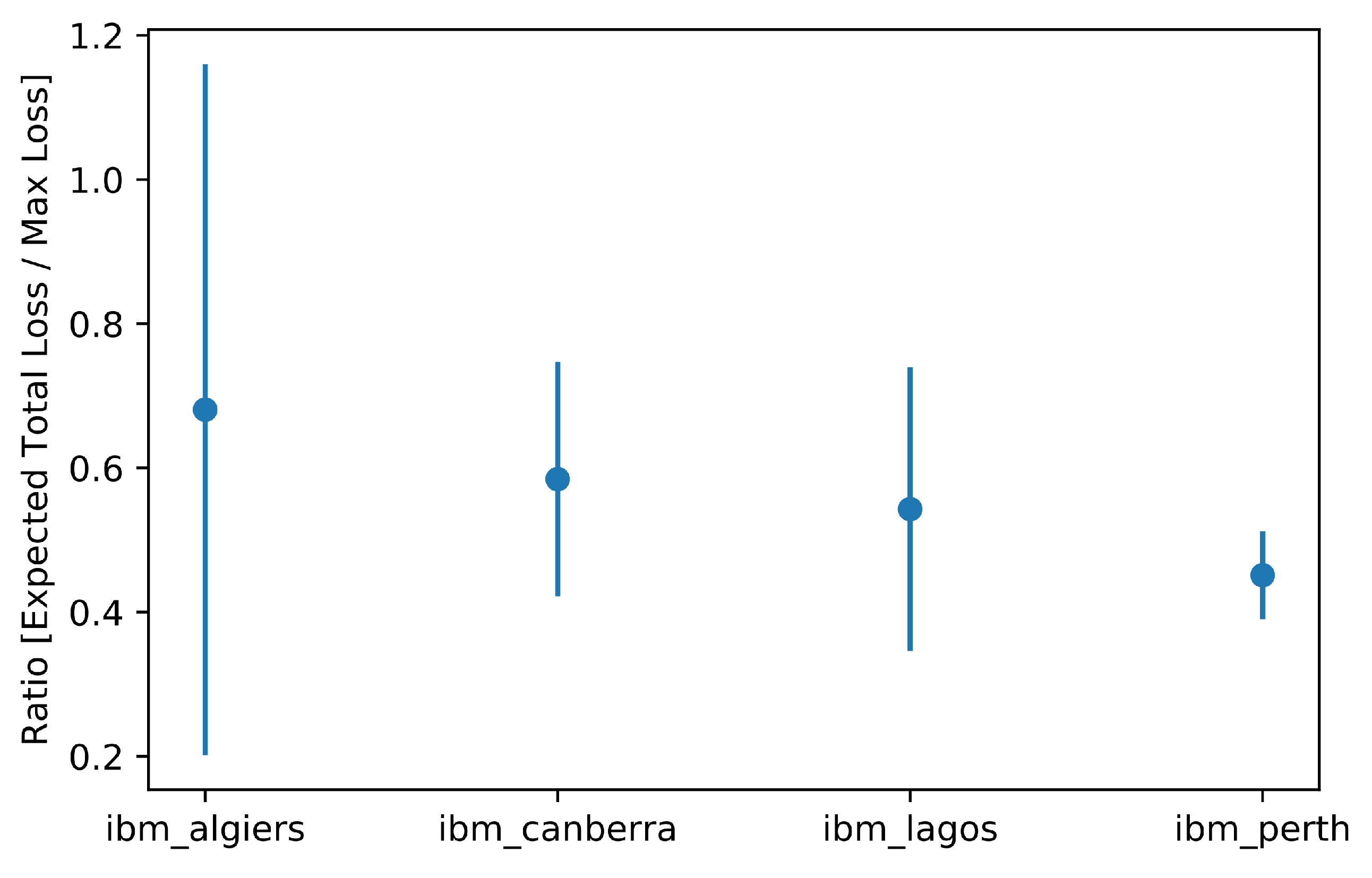

3.2. Real Hardware and Noisy Simulations

- Ibm_perth and ibm_lagos, each with 7 qubits and a quantum volume of 32.

- Ibm_canberra and ibm_algiers, each with 27 qubits and quantum volumes of 32 and 128, respectively.

4. Discussion

4.1. Scalability and Complexity

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| QPU | Quantum processing unit |

| CRA | Credit risk analysis |

| VaR | Value at risk |

| QAE | Quantum amplitude estimation |

| PD | Probability of default |

| LGD | Loss given default |

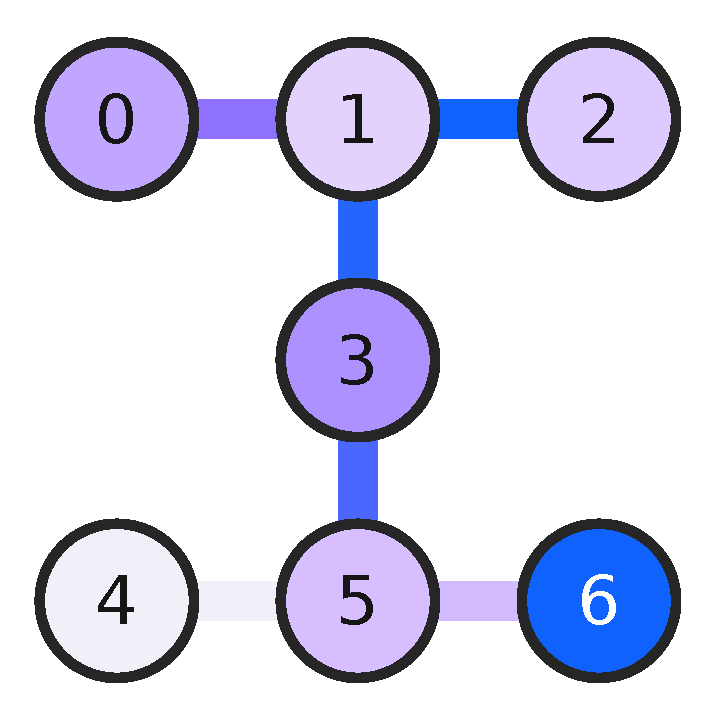

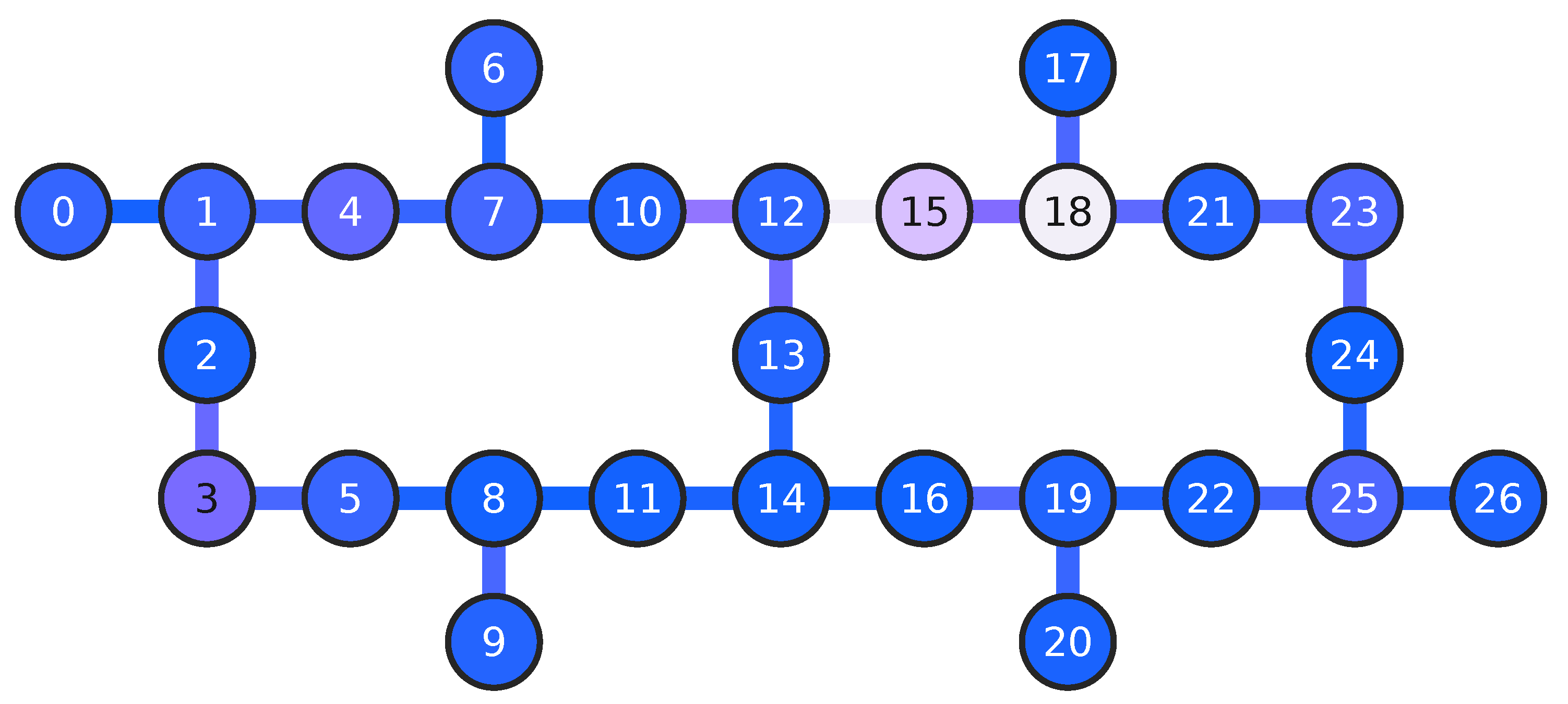

Appendix A. Quantum Processor Topologies

Appendix A.1. ibm_lagos and ibm_perth

Appendix A.2. ibm_algiers and ibm_canberra

References

- Dri, E.; Giusto, E.; Aita, A.; Montrucchio, B. Towards practical Quantum Credit Risk Analysis. J. Phys. Conf. Ser. 2022, 2416, 12002. [Google Scholar] [CrossRef]

- Orús, R.; Mugel, S.; Lizaso, E. Quantum computing for finance: Overview and prospects. Rev. Phys. 2019, 4, 100028. [Google Scholar] [CrossRef]

- Egger, D.J.; Gambella, C.; Marecek, J.; McFaddin, S.; Mevissen, M.; Raymond, R.; Simonetto, A.; Woerner, S.; Yndurain, E. Quantum Computing for Finance: State-of-the-Art and Future Prospects. IEEE Trans. Quantum Eng. 2020, 1, 3030314. [Google Scholar] [CrossRef]

- Egger, D.J.; Gutiérrez, R.G.; Mestre, J.C.; Woerner, S. Credit Risk Analysis Using Quantum Computers. IEEE Trans. Comput. 2021, 70, 2136–2145. [Google Scholar] [CrossRef]

- Gestel, T.V.; Baesens, B. Credit Risk Management; Oxford University Press: Oxford, UK, 2008. [Google Scholar] [CrossRef]

- Hong, L.J.; Hu, Z.; Liu, G. Monte Carlo Methods for Value-at-Risk and Conditional Value-at-Risk: A Review. ACM Trans. Model. Comput. Simul. 2014, 24, 2661631. [Google Scholar] [CrossRef]

- Jorion, P. Value at Risk, 3rd ed.; McGraw-Hill: New York, NY, USA, 2006. [Google Scholar] [CrossRef]

- Pykhtin, M. Multi-factor adjustment. Risk 2004, 17, 85–90. [Google Scholar]

- Glasserman, P. Monte Carlo Methods in Financial Engineering; Stochastic Modelling and Applied Probability; Springer: New York, NY, USA, 2010. [Google Scholar]

- Danilowicz, R.L. Demonstrating the Dangers of Pseudo-Random Numbers. SIGCSE Bull. 1989, 21, 46–48. [Google Scholar] [CrossRef]

- Gupta, M.; Nene, M.J. Random Sequence Generation using Superconducting Qubits. In Proceedings of the 2021 Third International Conference on Intelligent Communication Technologies and Virtual Mobile Networks (ICICV), Tirunelveli, India, 4–6 February 2021; pp. 640–645. [Google Scholar] [CrossRef]

- Woerner, S.; Egger, D.J. Quantum risk analysis. NPJ Quantum Inf. 2019, 5, 15. [Google Scholar] [CrossRef]

- Lütkebohmert, E. The Asymptotic Single Risk Factor Model. In Concentration Risk in Credit Portfolios; Springer: Berlin/Heidelberg, Germany, 2009; pp. 31–42. [Google Scholar] [CrossRef]

- Jongh, R.D.; Verster, T.; Reynolds, E.; Joubert, M.; Raubenheimer, H. A Critical Review Of The Basel Margin Of Conservatism Requirement In A Retail Credit Context. Int. J. Bus. Econ. Res. (IBER) 2017, 16, 257–274. [Google Scholar] [CrossRef]

- Hamerle, A.; Liebig, T.; Roesch, D. Credit Risk Factor Modeling and the Basel Ii IRB Approach. SSRN Electron. J. 2003, 2, 2793952. [Google Scholar] [CrossRef]

- Researchers Program. Available online: https://quantum-computing.ibm.com/programs/researchers (accessed on 10 March 2023).

- Qiskit Runtime: A Cloud-Native, Pay-As-You-Go Service for Quantum Computing. 2022. Available online: https://www.ibm.com/cloud/blog/how-to-make-quantum-a-pay-as-you-go-cloud-service (accessed on 10 March 2023).

- Brassard, G.; Høyer, P.; Mosca, M.; Tapp, A. Quantum amplitude amplification and estimation. In Quantum Computation and Information; Contemporary Mathematics; American Mathematical Society: Providence, RI, USA, 2002; Volume 305, pp. 53–74. [Google Scholar]

- Grinko, D.; Gacon, J.; Zoufal, C.; Woerner, S. Iterative quantum amplitude estimation. NPJ Quantum Inf. 2021, 7, 52. [Google Scholar] [CrossRef]

- Rutkowski, M.; Tarca, S. Regulatory capital modeling for credit risk. Int. J. Theor. Appl. Financ. 2015, 18, 1550034. [Google Scholar] [CrossRef]

- De Basilea, C.d.S.B. Basel II: International Convergence of Capital Measurement and Capital Standards: A Revised Framework—Comprehensive Version; BIS: Basel, Switzerland, 2006. [Google Scholar]

- Grover, L.; Rudolph, T. Creating superpositions that correspond to efficiently integrable probability distributions. arXiv 2002, arXiv:quant-ph/0208112. [Google Scholar]

- Chen, N.F.; Roll, R.; Ross, S. Economic Forces and the Stock Market. J. Bus. 1986, 59, 383–403. [Google Scholar] [CrossRef]

- Aleksandrowicz, G.; Alexander, T.; Barkoutsos, P.; Bello, L.; Ben-Haim, Y.; Bucher, D.; Cabrera-Hernández, F.J.; Carballo-Franquis, J.; Chen, A.; Chen, C.F.; et al. Qiskit: An Open-Source Framework for Quantum Computing; Zenodo: Geneva, Switzerland, 2019. [Google Scholar] [CrossRef]

- WeightedAdder—Qiskit 0.36.1 Documentation. Available online: https://qiskit.org/documentation/stubs/qiskit.circuit.library.WeightedAdder.html (accessed on 10 March 2023).

- LinearAmplitudeFunction—Qiskit 0.36.1 Documentation. Available online: https://qiskit.org/documentation/stubs/qiskit.circuit.library.LinearAmplitudeFunction.html (accessed on 10 March 2023).

- Gacon, J.; Zoufal, C.; Woerner, S. Quantum-Enhanced Simulation-Based Optimization. In Proceedings of the 2020 IEEE International Conference on Quantum Computing and Engineering (QCE), Denver, CO, USA, 12–16 October 2020; IEEE: New York, NY, USA, 2020. [Google Scholar] [CrossRef]

- Dri, E.; Aita, A. QVaR, 2022. [CrossRef]

- Clerk, A.A.; Devoret, M.H.; Girvin, S.M.; Marquardt, F.; Schoelkopf, R.J. Introduction to quantum noise, measurement, and amplification. Rev. Mod. Phys. 2010, 82, 1155–1208. [Google Scholar] [CrossRef]

- Harper, R.; Flammia, S.T.; Wallman, J.J. Efficient learning of quantum noise. Nat. Phys. 2020, 16, 1184–1188. [Google Scholar] [CrossRef]

- Oliveira, D.; Giusto, E.; Dri, E.; Casciola, N.; Baheri, B.; Guan, Q.; Montrucchio, B.; Rech, P. QuFI: A Quantum Fault Injector to Measure the Reliability of Qubits and Quantum Circuits. In Proceedings of the 2022 52nd Annual IEEE/IFIP International Conference on Dependable Systems and Networks (DSN), Baltimore, MD, USA, 27–30 June 2022; pp. 137–149. [Google Scholar] [CrossRef]

- Endo, S.; Benjamin, S.C.; Li, Y. Practical Quantum Error Mitigation for Near-Future Applications. Phys. Rev. X 2018, 8, 031027. [Google Scholar] [CrossRef]

- Suzuki, Y.; Uno, S.; Raymond, R.; Tanaka, T.; Onodera, T.; Yamamoto, N. Amplitude estimation without phase estimation. Quantum Inf. Process. 2020, 19, 75. [Google Scholar] [CrossRef]

- Zoufal, C.; Lucchi, A.; Woerner, S. Quantum Generative Adversarial Networks for learning and loading random distributions. NPJ Quantum Inf. 2019, 5, 103. [Google Scholar] [CrossRef]

- Madden, L.; Simonetto, A. Best Approximate Quantum Compiling Problems. ACM Trans. Quantum Comput. 2022, 3, 3505181. [Google Scholar] [CrossRef]

- Bindseil, U.; Sotamaa, K.; Amado, R.; Honings, N.; Chiappa, G.; Boux, B.; Föttinger, W.; Ledoyen, P.; Schwartzlose, H.; van der Hoorn, H.; et al. The Use of Portfolio Credit Risk Models in Central Banks; Occasional Paper Series 64; European Central Bank: Main, Germany, 2007. [Google Scholar]

- Balzarotti, V.; Falkenheim, M.; Powell, A. On the Use of Portfolio Risk Models and Capital Requirements in Emerging Markets. World Bank Econ. Rev. 2002, 16, 197–211. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

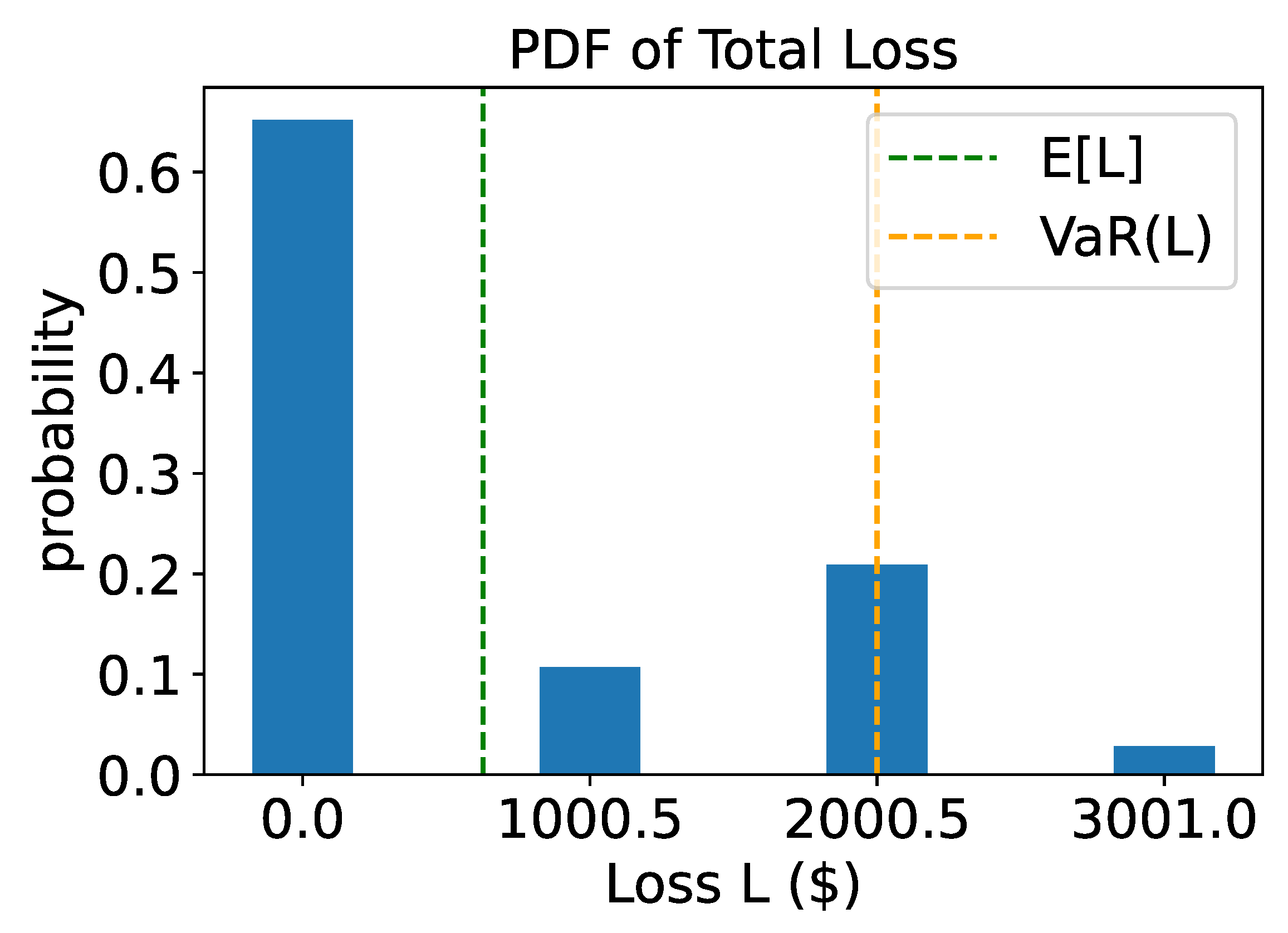

| Asset Number | Loss Given Default | Default Prob. | Sensitivity | Risk Factor Weights |

|---|---|---|---|---|

| 1 | 1000.5 | |||

| 2 | 2000.5 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dri, E.; Aita, A.; Giusto, E.; Ricossa, D.; Corbelletto, D.; Montrucchio, B.; Ugoccioni, R. A More General Quantum Credit Risk Analysis Framework. Entropy 2023, 25, 593. https://doi.org/10.3390/e25040593

Dri E, Aita A, Giusto E, Ricossa D, Corbelletto D, Montrucchio B, Ugoccioni R. A More General Quantum Credit Risk Analysis Framework. Entropy. 2023; 25(4):593. https://doi.org/10.3390/e25040593

Chicago/Turabian StyleDri, Emanuele, Antonello Aita, Edoardo Giusto, Davide Ricossa, Davide Corbelletto, Bartolomeo Montrucchio, and Roberto Ugoccioni. 2023. "A More General Quantum Credit Risk Analysis Framework" Entropy 25, no. 4: 593. https://doi.org/10.3390/e25040593

APA StyleDri, E., Aita, A., Giusto, E., Ricossa, D., Corbelletto, D., Montrucchio, B., & Ugoccioni, R. (2023). A More General Quantum Credit Risk Analysis Framework. Entropy, 25(4), 593. https://doi.org/10.3390/e25040593