This section presents empirical findings concerning sequential regularity and predictability of the 36 European stock markets and the U.S. market within the turbulence periods.

4.1. Empirical Experiments

In this subsection, the research hypothesis proposed in Introduction is examined. Changes in the SampEn values for the pre-turbulence and turbulence periods are estimated to assess whether entropy of equity market indices decreased during extreme event periods. To calculate the changes in entropy before and during the particular turbulence period, the following pairs of sub-periods of equal length are investigated:

As was emphasized in Introduction, the aforementioned turbulence periods are based on the references [

26,

27,

32,

33,

34].

An important expected feature of the SampEn algorithm is the relative consistency (e.g., [

20,

50]). This property follows from the Kolmogorov-Sinai definition of entropy [

17]. The notion of relative consistency was introduced by Pincus [

19]. In terms of the SampEn procedure, this can be written as the following property:

For dynamical processes , if , then .

This property means that if series

A exhibits more sequential regularity than series

B for one set of the parameters

, then this holds true for any other set

[

20]. This expected property enables us to compare two processes for a single set

and draw conclusions for all sets of input parameters.

As mentioned in

Section 3.1, the SampEn statistic depends on three parameters:

N,

m, and

r, where

N is a time series length,

m is the length of sequences to be compared, and a real number

denotes the tolerance for accepting matches. Based on the literature, the suggestion is that

m should be 1 or 2, since there are more template matches for

, but

(or greater) reveals more of the dynamics of the data. Moreover, the authors of the SampEn procedure suggest that

r should be 0.2 times the standard deviation

of the empirical data set [

47]. Therefore, in this research, the

and

parameters are used.

Table 2 includes the SampEn empirical findings within the Global Financial Crisis and COVID-19 pandemic outbreak. The columns entitled ‘Change’ report changes in entropy before and during particular turbulence period. The down arrows show entropy decrease, while the (rare) up arrows visualize entropy increase.

The results presented in

Table 2 require some explanations and interpretations. In general, the empirical findings are unambiguous and confirm no reason to reject the research hypothesis. The evidence is that entropy decreased within the GFC period for the U.S. and the vast majority of the European markets, except for nine countries (i.e., Switzerland, Sweden, Finland, Ireland, Serbia, Malta, Cyprus, Estonia, Bosnia and Herzegovina). Both developed and emerging markets are among them. The probable reason of the differences in the obtained results is that the GFC periods for some countries were slightly different (for details see, e.g., [

33]).

However, the comparative results for the pre-COVID-19 and COVID-19 sub-periods are homogenous and they decidedly support the evidence that regularity and predictability of the U.S. and almost all European stock markets (apart from Ukraine) increased during the COVID-19 outbreak. Due to the investigated period (2020-2021), the isolated case of Ukraine is rather coincidental and is not connected with the Russian aggression in Ukraine on 24 February 2022.

The ranges of the SampEn values for the European market indices are: (Pre-GFC), (GFC), (Pre-COVID), and (COVID). The minimum, maximum, median, and mean values decreased substantially during both extreme event periods.

To formally test whether the mean results of SampEn for the whole group of markets during the turbulence period differ significantly compared to the corresponding pre-turbulence period, the

t statistic for sample means given by Equation (

9) is utilized:

where

and

are sample means,

and

are sample variances, while

denotes the stock markets sample size.

The following two-tailed hypothesis is tested:

where

and

are the expected values of SampEn for the whole group of stock market indices during the compared periods, and the null hypothesis states that two expected values are equal. Calculations of the

t statistic values (Equation (

9)) are based on the results presented in

Table 2. The null hypothesis is rejected when

, where the critical value of

t-statistic at the

significance level is equal to

. In our research, the critical values are equal to:

(

),

(

), and

(

), respectively.

The obtained empirical t-statistics are equal to: (1) for the pair of periods (pre-GFC, GFC), and (2) for the pair of periods (pre-COVID, COVID). This indicates that the hypothesis was rejected in both cases and the SampEn mean values substantially differed (specifically, decreased) during both extreme event periods.

What is important, the SampEn findings are consistent with the literature as they confirm that entropy of stock market indices usually decreases during the economic downturns (see, e.g., [

41,

45]). The equity market crash initiates a declining trend, which reduces entropy but increases time series regularity. As a consequence, predictability of a market increases within turbulence periods since a number of repeated patterns increases. It is worth noting that this evidence is in accordance with investors’ intuition.

4.2. Sample Entropy of Developed versus Emerging European Stock Markets

An interesting and important question is whether developed stock markets differ substantially from emerging markets in their predictability, in the sense of their sequential regularity. Therefore, in this subsection, the comparative assessment of regularity/irregularity in the European developed and emerging markets is presented.

Based on the recent MSCI reports, and especially on the report “MSCI Global Market Accessibility Review. Country comparison” [

51], the following 15 European countries are classified as developed markets (in the order of decreasing value of stock market capitalisation in 31 December 2020 reported in

Table 1): France, United Kingdom, Germany, Switzerland, Netherlands, Sweden, Spain, Italy, Denmark, Belgium, Finland, Norway, Ireland, Austria, and Portugal. The remaining 21 European countries are recognized as emerging, including also frontier and stand-alone equity markets (see

Table A3 in

Appendix B).

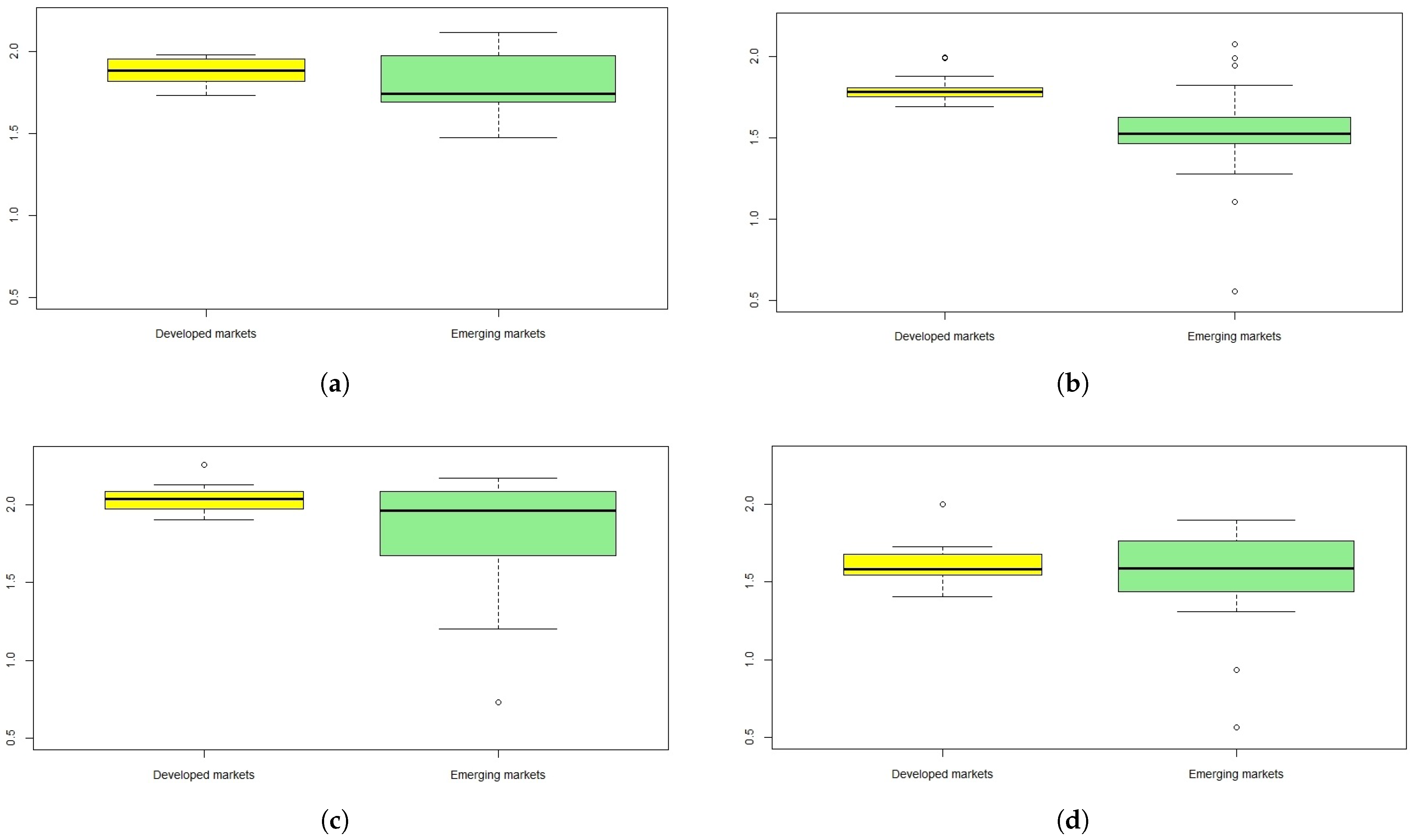

Figure 1 presents the boxplots of the SampEn results within the pre-turbulence and turbulence periods, for two groups of the European developed (the yellow boxplots) and emerging (the green boxplots) stock markets. The boxplots that visualize the SampEn results are based on

Table A4 and

Table A5 (

Appendix B). The boxplot width depends on the number of the stock market indices, and these numbers are: 15 (the European developed markets) and 21 (the European emerging markets).

One can observe that entropy measured by the SampEn statistic substantially fell during the turbulence periods compared to the pre-turbulence periods, respectively. The down arrows in

Table A4 and

Table A5 illustrate the substantial falls of median and percentile values.

The SampEn median for the European developed markets was equal to 1.88 (within the pre-GFC period) versus 1.79 (within the GFC period). Similarly, the corresponding SampEn median values for the European emerging markets were equal to: 1.74 (within the pre-GFC period) and 1.53 (within the GFC period), respectively (see

Table A4).

As for the pre-COVID-19 and COVID-19 sub-periods, the changes in entropy were even more significant. For the European developed markets the SampEn median values were equal to 2.04 versus 1.58, while for the European emerging markets, 1.96 versus 1.59 (see

Table A5).

To formally test the hypothesis concerning the median values within pre-turbulence and turbulence periods, the following conditions are proposed:

where

is a SampEn median value before particular turbulence period, while

denotes a SampEn median value during a turbulence period, respectively. The null hypothesis states that two median values are equal. To examine the hypothesis, the Wilcoxon-Mann-Whitney test [

52] is used and the calculations are reported in

Table 3. The numbers in brackets are

p-values. The test results indicate that the null hypothesis

should be rejected in all cases, both for developed and emerging markets. Hence, the evidence is that the median values during the turbulence periods were significantly lower compared to the corresponding pre-turbulence periods.

The boxplot height means the interquartile range, which is a measure of statistical dispersion as it is equal to the difference between Q3 (75th) and Q1 (25th) percentiles. The evidence is that the level of entropy dispersion for the European developed market indices was similar and low, regardless of the time period choice. The results for the European emerging markets are mixed, but the main probable reason is that these markets are much more diverse. However, one can observe that the interquartile range for the emerging markets has substantially decreased during the turbulence periods (see

Table A4 and

Table A5).

The singular points denote outliers. The SampEn outliers were: (1) within the GFC period: Switzerland, Finland, Turkey, Poland, Cyprus (significantly higher values of the SampEn) and Slovakia (significantly lower value of the SampEn), (2) within the pre-pandemic period: Finland (significantly higher value of the SampEn) and Bosnia and Herzegovina (significantly lower value of the SampEn), and (3) within the pandemic period: Denmark (significantly higher value of the SampEn) and Slovakia and Bosnia and Herzegovina (significantly lower values of the SampEn). Within the pre-GFC period outliers did not appear.

To formally test the hypothesis concerning the comparison between the SampEn median values of the European developed and emerging stock markets within various sub-periods, the following

and

conditions (Equation (

12)) are proposed:

where

is a SampEn median value of the group of the European developed markets, while

denotes a SampEn median value of the group of the European emerging markets, respectively. The null hypothesis states that two median values are equal. To examine the hypothesis, the Wilcoxon-Mann-Whitney test [

52] for two independent groups is used, and the calculations are reported in

Table 4. The numbers in brackets are

p-values. The test results indicate that the null hypothesis

should be rejected only during the GFC period (

p-value 0.0019), while there is no reason to reject the null hypothesis for other periods. Therefore, the evidence is that the SampEn median values did not differ significantly between developed and emerging markets during the remaining three sub-periods.

To summarize, the findings for both the European developed and emerging equity markets are homogenous. The analyzed groups of market indices do not differ substantially in their sequential regularity. The aforementioned SampEn results indicate that entropy visibly fell during each extreme event period compared to the corresponding pre-event period. It implies that predictability of market indices rose, which confirmed no reason to reject the main research hypothesis.

4.3. The Evolution of Sample Entropy over Time

In this subsection, the evolution of SampEn over time is analyzed. A rolling-window dynamic approach is employed to capture the changes in market index regularity (measured by SampEn) through time, for daily logarithmic index returns.

In line of the existing literature, the sample size

N should be within the range of

(see, e.g., [

5,

45]). As pointed out in

Section 4.1, in this research

, hence the minimal time window length should be equal to 100. Therefore, a window

business days is utilized in this study.

The broad group of 36 stock markets is explored. The use of the rolling-window method requires the corresponding figures that show the changes in SampEn over time. Hence, it should be 36 × 2 = 72 figures reported in the paper as the graphic representation of the rolling-window procedure. Therefore, only selected dynamic SampEn results for developed and emerging markets are illustrated, i.e., the results for stock markets with the highest absolute value of the change in SampEn (based on

Table 2). Due to the space restriction, the remaining figures are available upon a request.

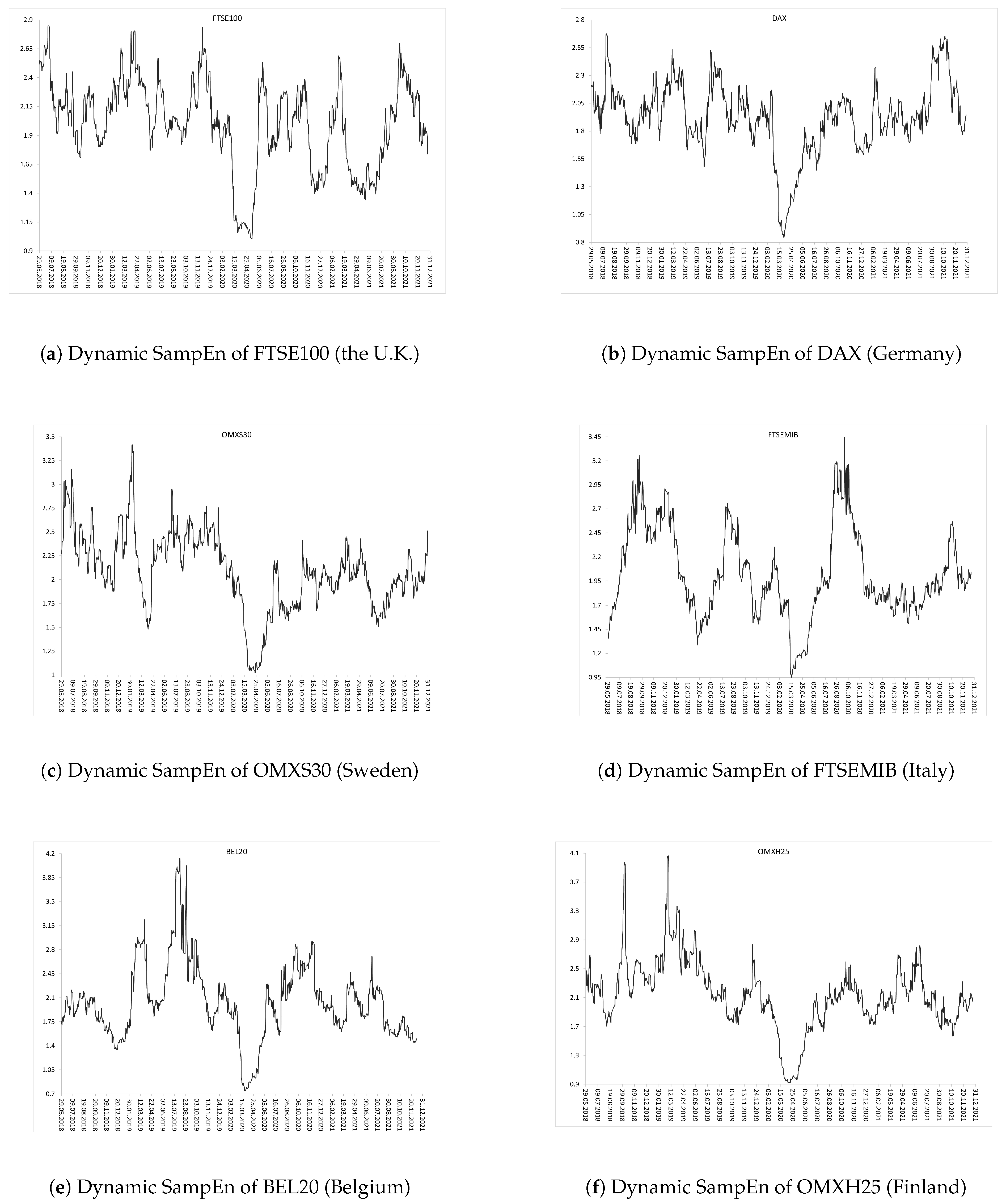

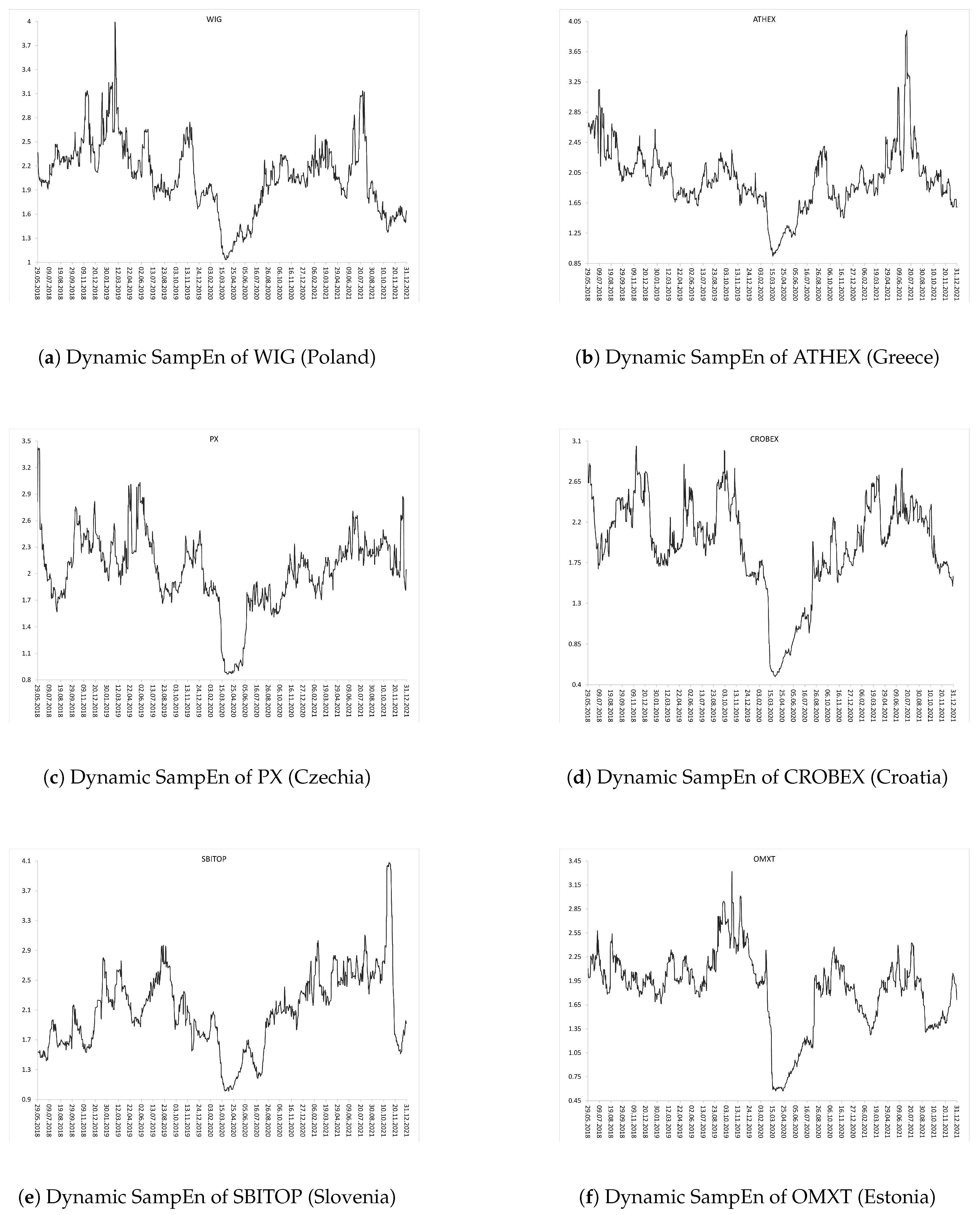

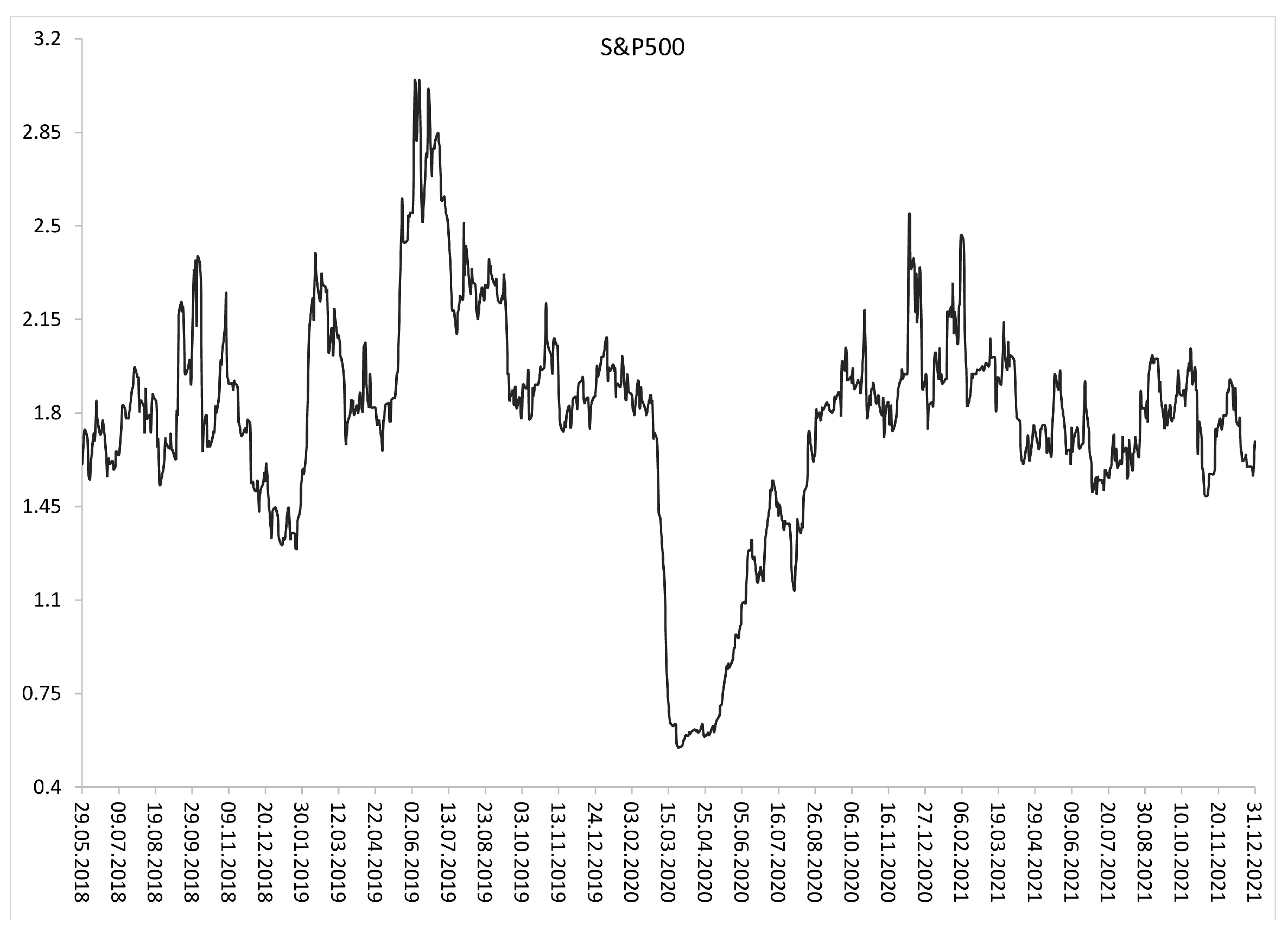

Subsequent

Figure 2,

Figure 3 and

Figure 4 show the evolution of SampEn over time within the period from January 2018 to December 2021 (two combined pre-COVID-19 and COVID-19 sub-periods).

Figure 2 and

Figure 3 present graphs for the European developed and emerging markets, respectively. Finally,

Figure 4 plots the dynamics of SampEn for S&P500 index. The SampEn procedure implemented on the rolling-window scheme indicates and confirms that entropy visibly decreased during the COVID-19 pandemic, especially in March-April 2020, both for developed and emerging markets. It is rather clear that the main reason of such homogenous results is that all investigated stock markets have been affected by the COVID-19 pandemic in the same time and to the similar extent.

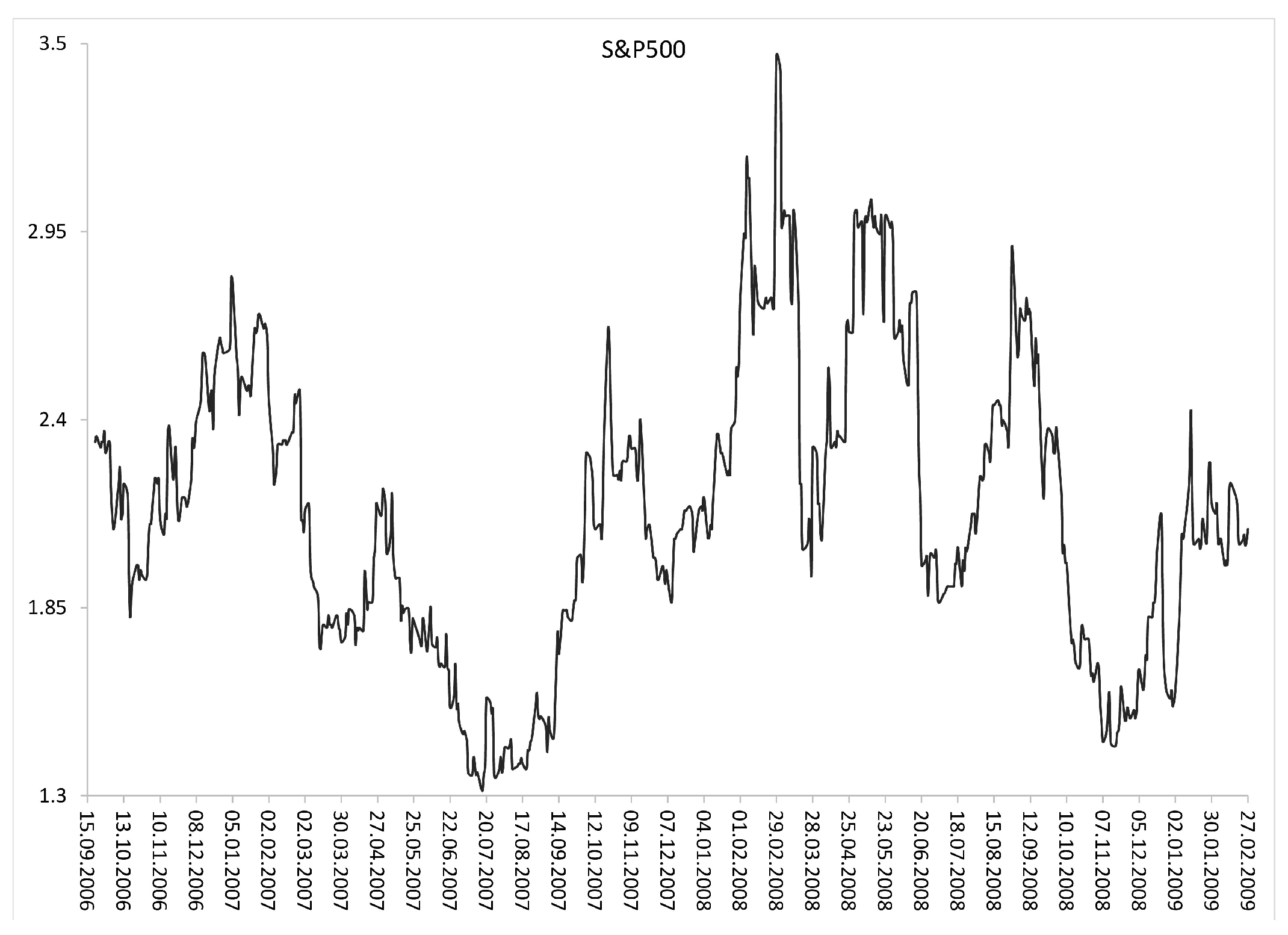

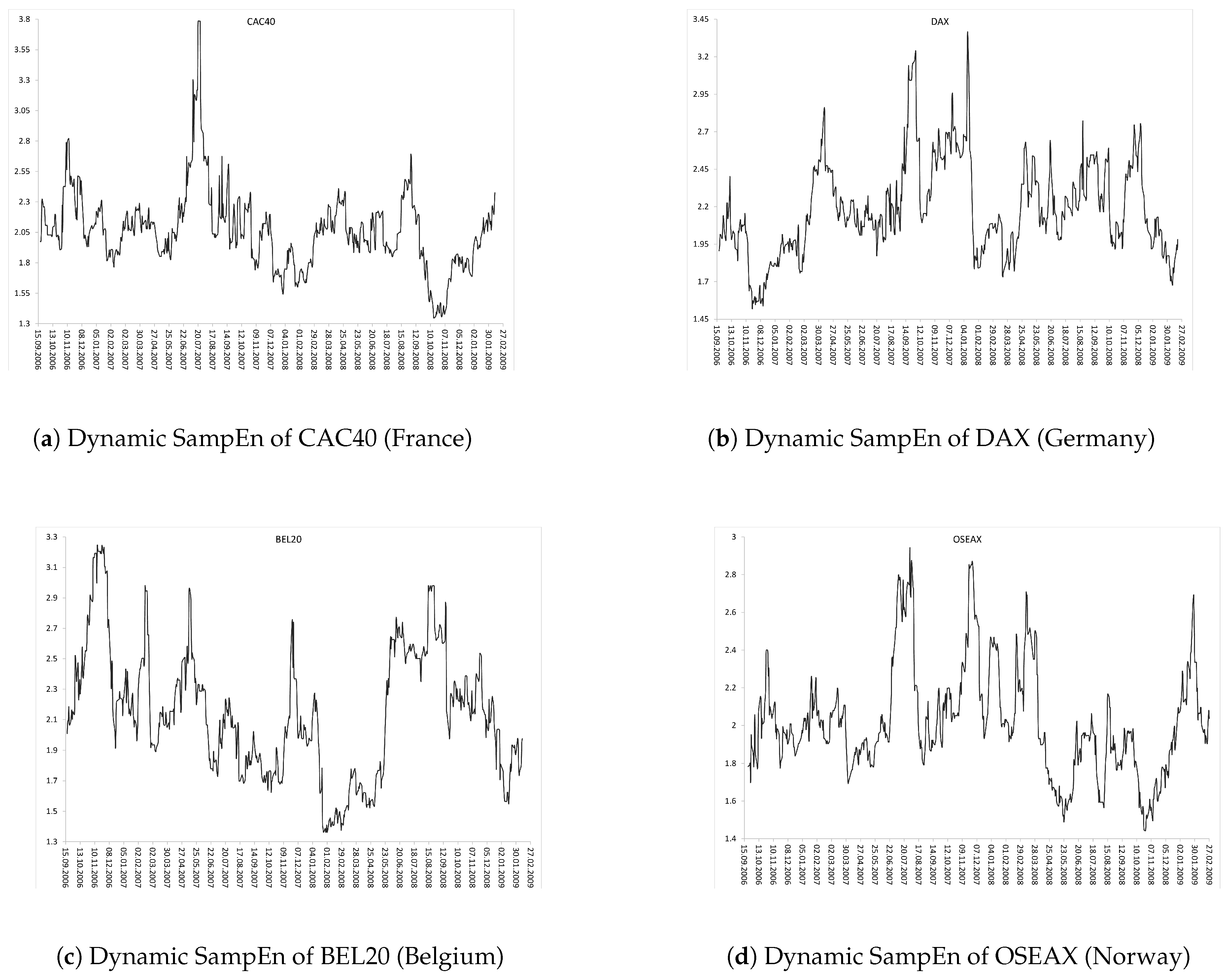

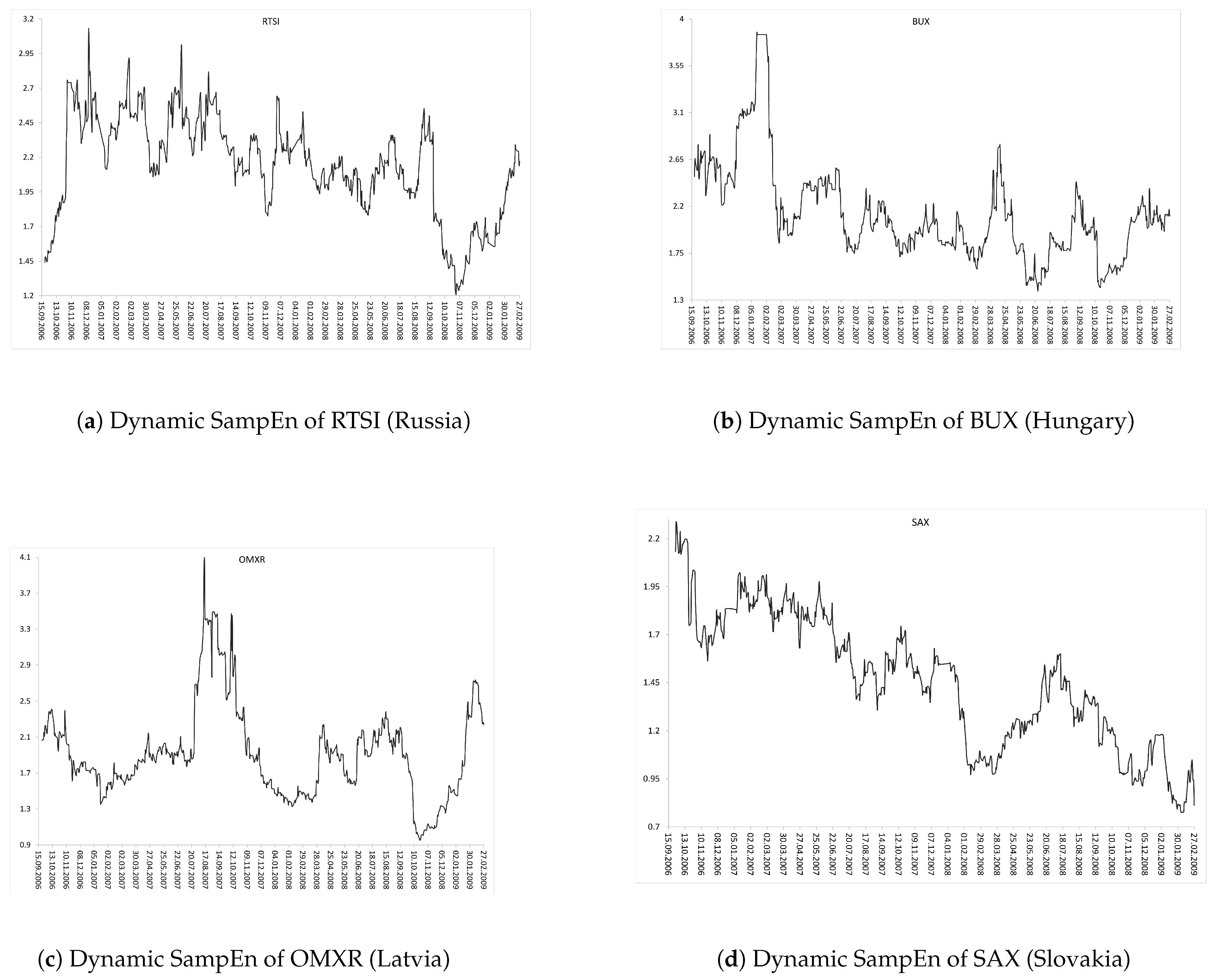

By analogy, the rolling-window procedure is utilized to investigate the evolution of the SampEn during the period from May 2006 to February 2009 (two combined pre-GFC and GFC sub-periods). The findings are reported and discussed in

Appendix C.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}