Modelling Asymmetric Unemployment Dynamics: The Logarithmic-Harmonic Potential Approach

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Methods

2.1. Proposed Model

2.2. Logarithmic-Harmonic Potential

3. Results

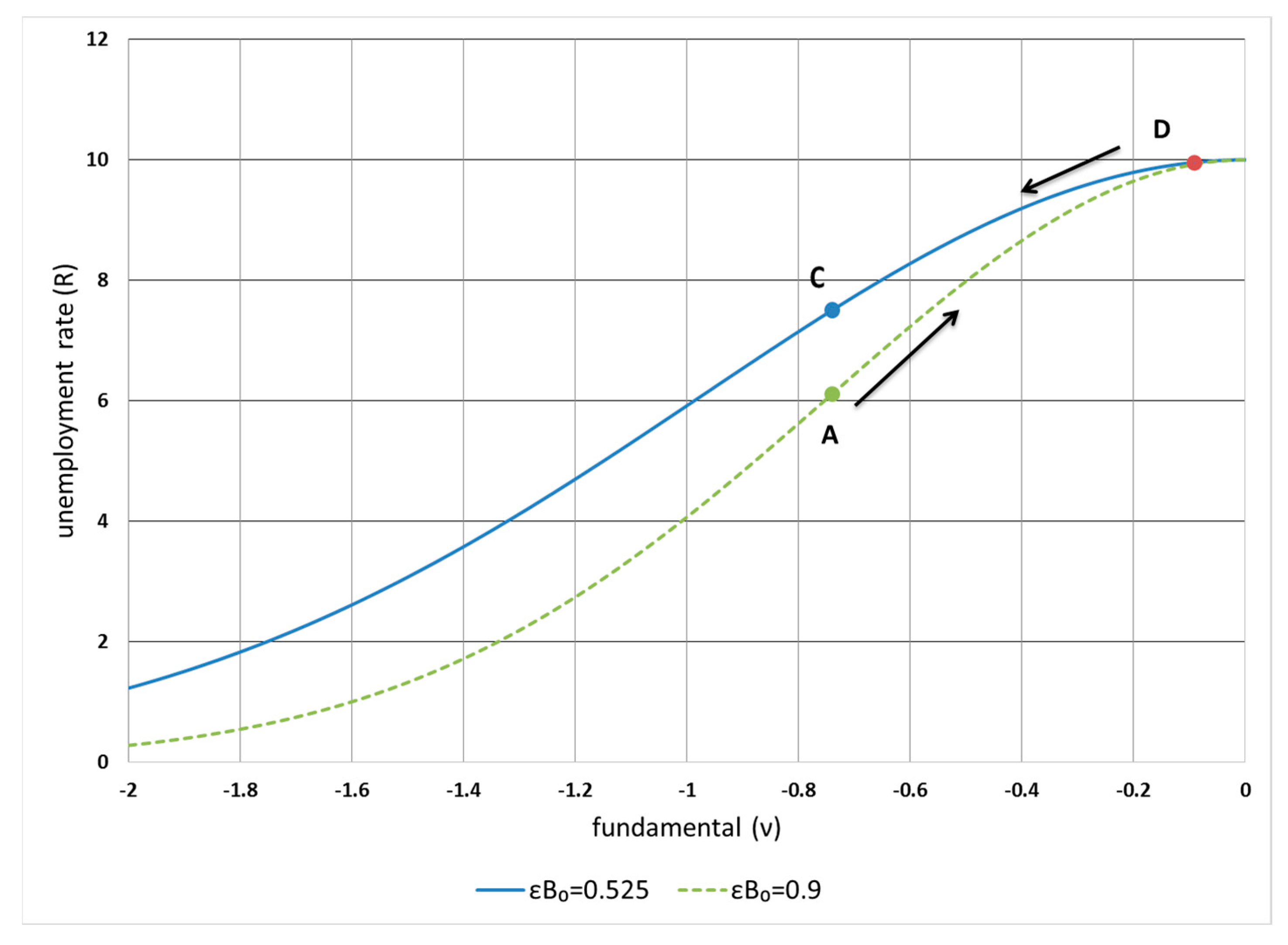

3.1. Asymmetric Unemployment Rates

3.2. Unemployment Rate Dynamics

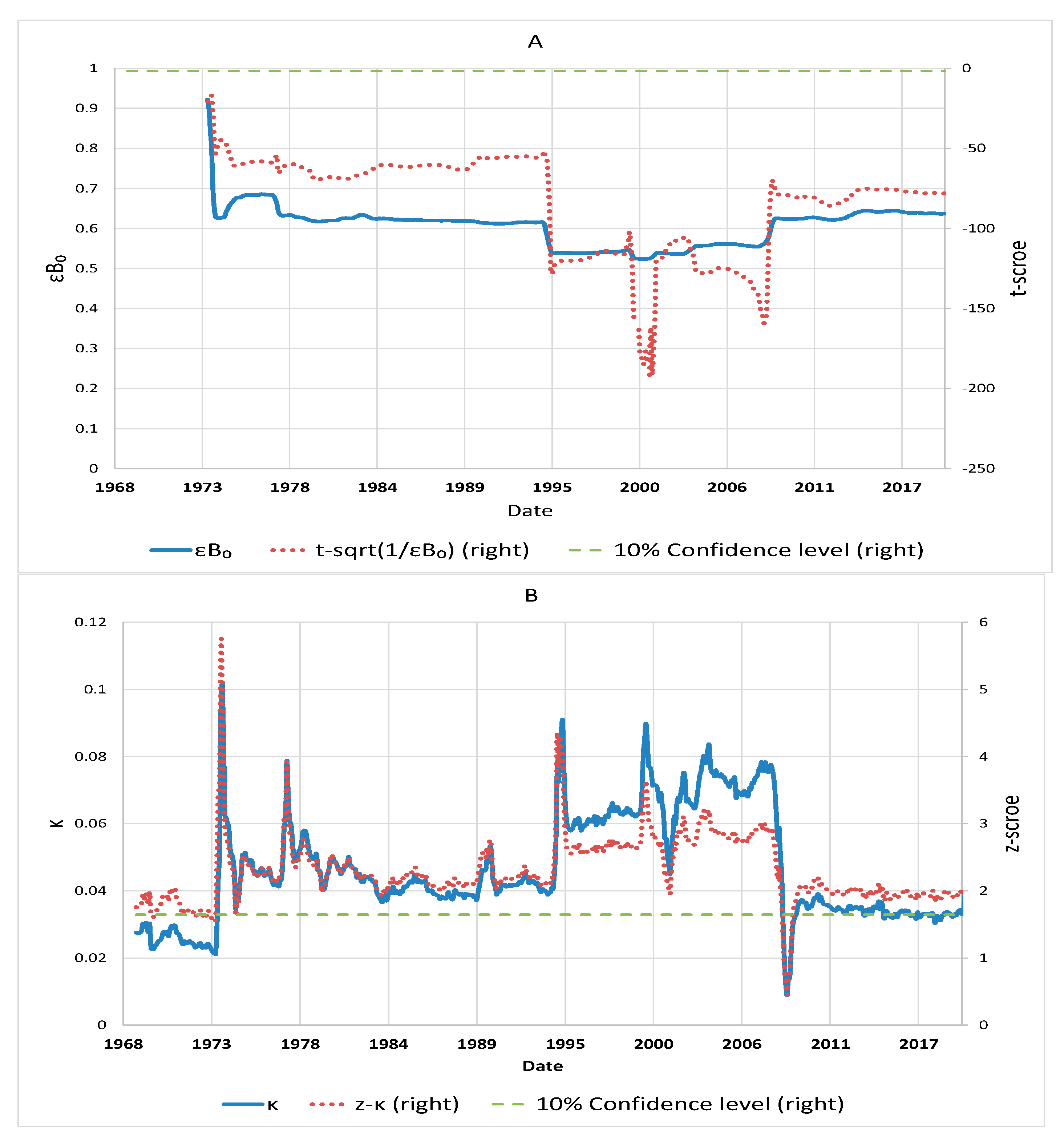

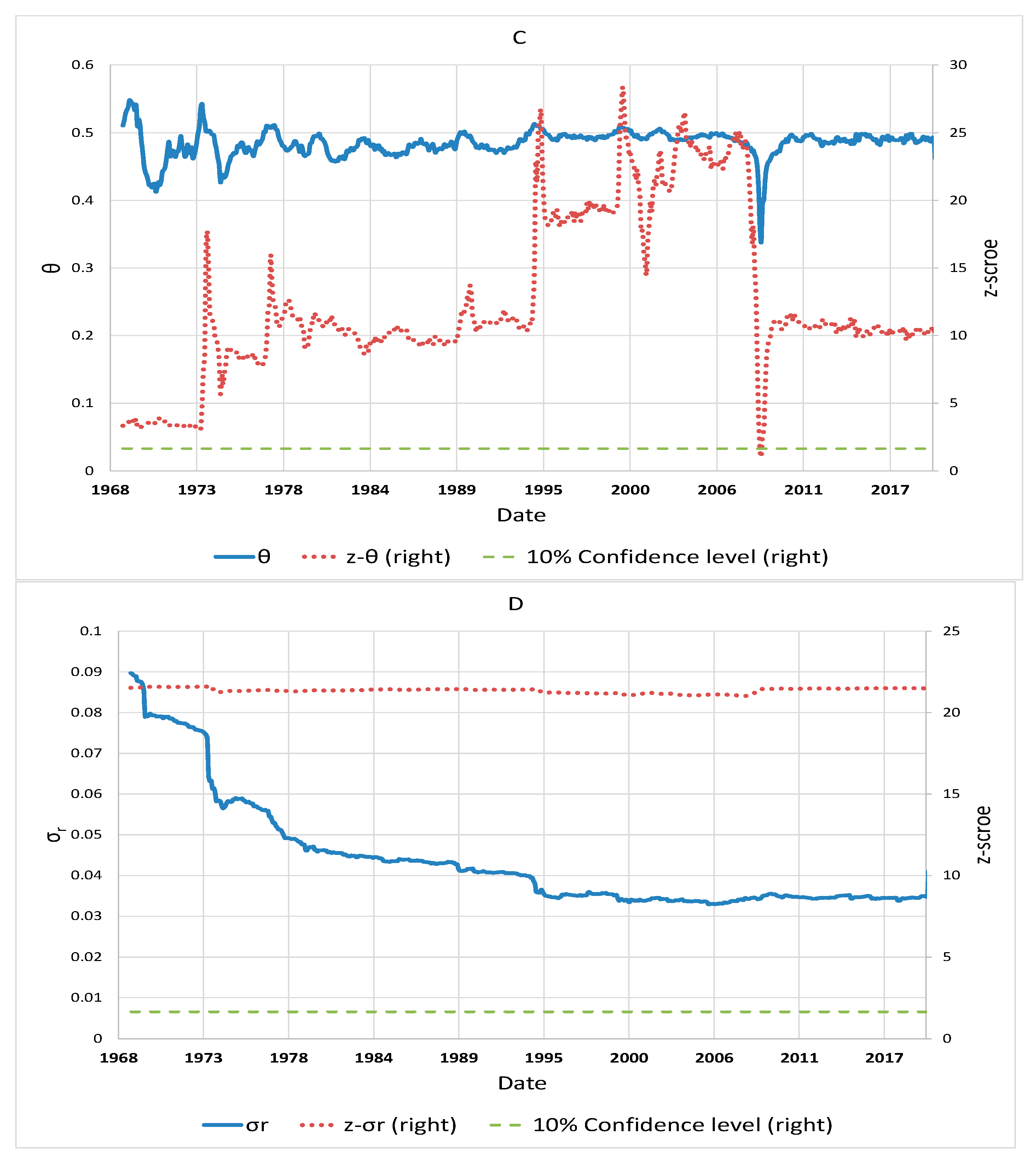

3.3. Model Validation

3.4. Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Neftci, S.N. Are Economic Time Series Asymmetric over the Business Cycle? J. Political Econ. 1984, 92, 307–328. [Google Scholar] [CrossRef]

- Sichel, D.E. Business Cycle Asymmetry: A Deeper Look. Econ. Inq. 1993, 31, 224–236. [Google Scholar] [CrossRef]

- Pissarides, C.A. Equilibrium Unemployment Theory; MIT Press: Cambridge, MA, USA, 2000. [Google Scholar]

- McKay, A.; Reis, R. The brevity and violence of contractions and expansions. J. Monetary Econ. 2008, 55, 738–751. [Google Scholar] [CrossRef] [Green Version]

- Dupraz, S.; Nakamura, E.; Steinsson, J. A Plucking Model of Business Cycles; Working Paper 26351; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Romer, C.D.; Romer, D.H. NBER Business Cycle Dating: History and Prospect; Working Paper; University of California: Berkeley, CA, USA, 2019. [Google Scholar]

- Hall, R.E.; Kudlyak, M. Why Has the US Economy Recovered so Consistently from Every Recession in the Past 70 Years; National Bureau of Economic Research: Cambridge, MA, USA, 2021. [Google Scholar]

- Mortensen, D.T.; Pissarides, C.A. Job Creation and Job Destruction in the Theory of Unemployment. Rev. Econ. Stud. 1994, 61, 397–415. [Google Scholar] [CrossRef] [Green Version]

- Abbritti, M.; Fahr, S. Downward wage rigidity and business cycle asymmetries. J. Monetary Econ. 2013, 60, 871–886. [Google Scholar] [CrossRef]

- Schmitt-Grohé, S.; Uribe, M. Downward Nominal Wage Rigidity, Currency Pegs, and Involuntary Unemployment. J. Political Econ. 2016, 124, 1466–1514. [Google Scholar] [CrossRef] [Green Version]

- Jung, P.; Kuhn, M. Earnings Losses and Labor Mobility Over the Life Cycle. J. Eur. Econ. Assoc. 2018, 17, 678–724. [Google Scholar] [CrossRef] [Green Version]

- Jarosch, G. Searching for Job Security and the Consequences of Job Loss; Working Paper; Princeton University: Princeton, NJ, USA, 2021. [Google Scholar]

- Krugman, P.R. Target Zones and Exchange Rate Dynamics. Q. J. Econ. 1991, 106, 669–682. [Google Scholar] [CrossRef]

- Froot, K.A.; Obstfeld, M. Exchange-rate dynamics under stochastic regime shifts: A unified approach. J. Int. Econ. 1991, 31, 203–229. [Google Scholar] [CrossRef]

- Bertola, G.; Svensson, L.E.O. Stochastic Devaluation Risk and the Empirical Fit of Target-Zone Models. Rev. Econ. Stud. 1993, 60, 689–712. [Google Scholar] [CrossRef]

- Pesz, K. A class of Fokker-Planck equations with logarithmic factors in diffusion and drift terms. J. Phys. A Math. Gen. 2002, 35, 1827–1832. [Google Scholar] [CrossRef]

- Lo, C. Exact propagator of the Fokker–Planck equation with logarithmic factors in diffusion and drift terms. Phys. Lett. A 2003, 319, 110–113. [Google Scholar] [CrossRef]

- Silva, E.M.; Rocha Filho, T.M.; Santana, A.E. Lie symmetries of Fokker–Planck equations with logarithmic diffusion and drift terms. J. Phys. Conf. Ser. 2006, 40, 150–155. [Google Scholar] [CrossRef]

- Cardeal, J.A.; De Montigny, M.; Khanna, F.C.; Filho, T.M.R.; Santana, A.E. Galilei-invariant gauge symmetries in Fokker–Planck dynamics with logarithmic diffusion and drift terms. J. Phys. A Math. Theor. 2007, 40, 13467–13478. [Google Scholar] [CrossRef]

- Lo, C.F. Dynamics of Fokker–Planck Equation with Logarithmic Coefficients and Its Application in Econophysics. Chin. Phys. Lett. 2010, 27, 080503. [Google Scholar] [CrossRef]

- Lo, C.; Hui, C.; Fong, T.; Chu, S. A quasi-bounded target zone model—Theory and application to Hong Kong dollar. Int. Rev. Econ. Financ. 2015, 37, 1–17. [Google Scholar] [CrossRef]

- Hui, C.H.; Lo, C.F.; Fong, T. Swiss franc’s one-sided target zone during 2011–2015. Int. Rev. Econ. Financ. 2016, 44, 54–67. [Google Scholar] [CrossRef]

- Hui, C.H.; Lo, C.F.; Chau, P.H.; Wong, A. Does Bitcoin behave as a currency?: A standard monetary model approach. Int. Rev. Financ. Anal. 2020, 70, 101518. [Google Scholar] [CrossRef]

- Hui, C.-H.; Lo, C.-F.; Cheung, C.-H.; Wong, A. Crude oil price dynamics with crash risk under fundamental shocks. N. Am. J. Econ. Financ. 2020, 54, 101238. [Google Scholar] [CrossRef]

- Lo, C.F. A Modified Stochastic Gompertz Model for Tumour Cell Growth. Comput. Math. Methods Med. 2010, 11, 3–11. [Google Scholar] [CrossRef] [Green Version]

- Giorno, V.; Nobile, A.G.; Ricciardi, L.M.; Sacerdote, L. Some remarks on the Rayleigh process. J. Appl. Probab. 1986, 23, 398–408. [Google Scholar] [CrossRef]

- Dechant, A.; Lutz, E.; Kessler, D.A.; Barkai, E. Superaging correlation function and ergodicity breaking for Brownian motion in logarithmic potentials. Phys. Rev. E 2012, 85, 051124. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Mondal, D. Enhancement of entropic transport by intermediates. Phys. Rev. E 2011, 84, 011149. [Google Scholar] [CrossRef]

- Mondal, D.; Ray, D.S. Asymmetric stochastic localization in geometry controlled kinetics. J. Chem. Phys. 2011, 135, 194111. [Google Scholar] [CrossRef] [PubMed]

- Fogedby, C.; Metzler, R. DNA bubble dynamics as a quantum coulomb problem. Phys. Rev. Lett. 2007, 98, 07060. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bar, A.; Kafri, Y.; Mukamel, D. Dynamics of DNA melting. J. Phys. Condens. Matter 2008, 21, 034110. [Google Scholar] [CrossRef]

- Giampaoli, J.A.; Strier, D.E.; Batista, C.; Drazer, G.; Wio, H.S. Exact expression for the diffusion propagator in a family of time-dependent anharmonic potentials. Phys. Rev. E 1999, 60, 2540–2546. [Google Scholar] [CrossRef] [Green Version]

- DeChant, A.; Lutz, E.; Barkai, E.; Kessler, D.A. Solution of the Fokker-Planck Equation with a Logarithmic Potential. J. Stat. Phys. 2011, 145, 1524–1545. [Google Scholar] [CrossRef]

- Ryabov, A.; Dierl, M.; Chvosta, P.; Einax, M.; Maass, P. Work distribution in a time-dependent logarith-mic-harmonic potential: Exact results and asymptotic analysis. J. Phys. A Math. Theor. 2013, 46, 075002. [Google Scholar] [CrossRef] [Green Version]

- Guarnieri, F.; Moon, W.; Wettlaufer, J.S. Solution of the Fokker-Planck equation with a logarithmic potential and mixed eigenvalue spectrum. J. Math. Phys. 2017, 58, 093301. [Google Scholar] [CrossRef] [Green Version]

- Ray, S.; Reuveni, S. Diffusion with resetting in a logarithmic potential. J. Chem. Phys. 2020, 152, 234110. [Google Scholar] [CrossRef] [PubMed]

- Karlin, S.; Taylor, H.M. A Second Course in Stochastic Processes; Academic Press: New York, NY, USA, 1981. [Google Scholar]

- Holubec, V. An exactly solvable model of a stochastic heat engine: Optimization of power, power fluctuations and efficiency. J. Stat. Mech. Theory Exp. 2014, 2014, P05022. [Google Scholar] [CrossRef]

- Cohen, A.E. Control of Nanoparticles with Arbitrary Two-Dimensional Force Fields. Phys. Rev. Lett. 2005, 94, 118102. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Blickle, V.; Bechinger, C. Realization of a micrometre-sized stochastic heat engine. Nat. Phys. 2012, 8, 143–146. [Google Scholar] [CrossRef] [Green Version]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hui, C.-H.; Lo, C.-F.; Ip, H.-Y. Modelling Asymmetric Unemployment Dynamics: The Logarithmic-Harmonic Potential Approach. Entropy 2022, 24, 400. https://doi.org/10.3390/e24030400

Hui C-H, Lo C-F, Ip H-Y. Modelling Asymmetric Unemployment Dynamics: The Logarithmic-Harmonic Potential Approach. Entropy. 2022; 24(3):400. https://doi.org/10.3390/e24030400

Chicago/Turabian StyleHui, Cho-Hoi, Chi-Fai Lo, and Ho-Yan Ip. 2022. "Modelling Asymmetric Unemployment Dynamics: The Logarithmic-Harmonic Potential Approach" Entropy 24, no. 3: 400. https://doi.org/10.3390/e24030400

APA StyleHui, C.-H., Lo, C.-F., & Ip, H.-Y. (2022). Modelling Asymmetric Unemployment Dynamics: The Logarithmic-Harmonic Potential Approach. Entropy, 24(3), 400. https://doi.org/10.3390/e24030400