1. Introduction

We consider the first-order autoregressive process defined by

where

are random errors with mean 0 and variance

. It is well known that the regression coefficient

characterizes the properties of the process

. When

,

is called a stationary process (see Brockwell and Davis [

1]). For example, assume that

are independent and identically distributed errors with

,

, and

, with some

. Then, the least squares (LS) estimator

of

defined by

has a normal limiting distribution:

where

(see Phillips and Magdalinos [

2]). When

,

is called a random walk process (see Dickey and Fuller [

3], Wang et al. [

4]). When

,

is called an explosive process. Let

be independent and identically distributed Gaussian errors

with

, and the initial condition

. White [

5] and Anderson [

6] showed that the LS estimator

of

has a Cauchy limiting distribution:

where

is a standard Cauchy random variable. Moreover, let

c be a constant, and

, where

. If

, then

is called a near-stationary process (see Chan and Wei [

7]). Let

be independent and identically distributed errors with

,

, and

, with some

. Phillips and Magdalinos [

2] showed that the LS estimator

of

has a normal limiting distribution:

where

. If

, then

is called a near-explosive process or mildly explosive process. Phillips and Magdalinos [

2] also showed that the LS estimator

of

has a Cauchy limiting distribution:

where

.

It is interesting to study the near-stationary process and mildly explosive process based on dependent errors. For example, Buchmann and Chan [

8] considered the near-stationary process whose errors were strongly dependent random variables; Phillips and Magdalinos [

9] and Magdalinos [

10] studied the mildly explosive process whose errors were moving average process with martingale differences; Aue and Horvàth [

11] considered the mildly explosive process based on stable errors; Oh et al. [

12] studied the mildly explosive process-based strong mixing (

-mixing) errors and obtained the Cauchy limiting distribution in (

6) for the LS estimator

. It is known that the sequence of

-mixing is a weakly dependent sequence. However, they assumed that

was geometrically

-mixing, i.e.,

for some

. Obviously, it was a very strong condition. It will be more general if

is arithmetically

-mixing, i.e.,

for some

. Thus, the aim of this paper is to weaken this mixing condition. We continue to investigate the mildly explosive process based on arithmetically

-mixing errors. Compared with Oh et al. [

12], we use different inequalities of

-mixing sequences to prove the key Lemmas 1 and 2 (see

Section 2 and

Section 6). As important applications, some simulations and real data of the NASDAQ composite index from April 2011 to April 2021 are also discussed in this paper. Next, we recall the definition of

-mixing as follows:

Let

and denote

to be the

-field generated by random variables

,

. For

, we define

Definition 1. If as , then is called a strong mixing or α-mixing sequence. If for some , then is called an arithmetically α-mixing sequence. If for some , then is called a geometrically α-mixing sequence.

The

-mixing sequence is a weakly dependent sequence and several linear and nonlinear time series models satisfy the mixing properties. For more works on

-mixing and applications of regression, we refer the reader to Hall and Heyde [

13], Györfi et al. [

14], Lin and Lu [

15], Fan and Yao [

16], Jinan et al. [

17], Escudero et al. [

18], Li et al. [

19], and the references therein. Many researchers have studied mildly explosive models. For example, Arvanitis and Magdalinos [

20] studied the mildly explosive process under the stationary conditional heteroskedasticity errors; Liu et al. [

21] investigated the mildly explosive process under the anti-persistent errors; Wang and Yu [

22] studied the explosive process without Gaussian errors; Kim et al. [

23] studied the explosive process without identically distributed errors. Furthermore, many researchers have used the mildly explosive model to study the behavior of economic growth and rational bubble problems, see Magdalinos and Phillips [

24], Phillips et al. [

25], Oh et al. [

12], Liu et al. [

21], and the references therein.

The rest of this paper is organized as follows. First, some conditions in Assumption (1) and two important Lemmas 1 and 2 are presented in

Section 2. Consequently, the Cauchy limiting distribution for LS estimator

and the confidence interval of

are obtained in

Section 2 (see Theorem 1). We also give some remarks about the existing studies of the Cauchy limiting distribution in

Section 2. As applications, some simulations on the empirical probability of the confidence interval for

and the empirical density for

and

are presented in

Section 3, which agree with the Cauchy limiting distribution in (

6). In

Section 4, the mildly explosive process is used to analyze the real data from the NASDAQ composite index from April 2011 to April 2021. It is a takeoff period of technology stocks and a faster increase in U.S. Treasury yields. Some conclusions and future research are discussed in

Section 5. Finally, the proofs of main results are presented in

Section 6. Throughout the paper, as

, let

and

respectively denote the convergence in probability and in distribution. Let

denote some positive constants not depending on

n, which may be different in various places. If

X and

Y have the same distribution, we denote it as

.

2. Results

We consider the mildly explosive process

where

for some

,

, and

. In addition,

are mean zeros of

-mixing errors. Some conditions in Assumption 1 are listed as follows:

Assumption 1. Let and for some ;

Let be a strictly stationarity sequence of arithmetically α-mixing with , where δ is defined by ;

Let for some , and , where δ is defined by ; in addition, let .

In order to prove the limiting distribution of the LS estimator

of

, the normalized sample covariance

can be approximated by the product of the stochastic sequences

Then, we have the following lemmas:

Lemma 1. Let the conditions (A1)–(A3) hold. Then, as ,where means convergence in the mean square. Lemma 2. Let the the conditions (A1)–(A3) hold. Then, as , the sequences and defined by (

8)

satisfywhere X and Y are two independent random variables with and Combining this with Lemmas 1 and 2, we have the following Cauchy limiting distribution for the LS estimator of as follows:

Theorem 1. Let the conditions of Lemmas 1 and 2 be satisfied. Then, as , we havewhere X and Y are two independent random variables defined by (

11),

and is a standard Cauchy random variable. Remark 1. Let : Let be a strictly stationarity sequence of geometrically α-mixing; Let with some , , and . Under the assumptions , , and , Oh et al. [12] considered the mildly explosive process (7) and obtained Lemmas 1 and 2 and Theorem 1, which extended Theorem 4.3 of Phillips and Magdalinos [2] based on independent errors to geometrically α-mixing errors. In order to weaken geometrically α-mixing, we use the inequalities from Doukhan and Louhichi [26] and Yang [27] to re-prove the key Lemmas 1 and 2. Thus, the mixing coefficients need to satisfy for some . For details, please the proofs of Lemmas 1 and 2 in Section 6. If positive parameter δ coming from moment condition is large, then the mixing coefficient is weak. Similarly, if positive parameter δ is small, then the mixing coefficient becomes strong. If , then is a geometrically decaying. So the condition in assumption becomes . Thus, we extend the results of Phillips and Magdalinos [2] and Oh et al. [12] to arithmetically α-mixing case. In Section 3, we give some simulations for the LS estimator in a mildly explosive process, which agree with Theorem 1. Meanwhile, the mildly explosive model is used to analyze the data of the NASDAQ composite index from April 2011 to April 2021 in Section 4. Remark 2. For some , , and , we take in (

14)

and obtainandwhere it uses the fact that . Here, means , as . Moreover, by Proposition A.1 of Phillips and Magdalinos [2], it has . Combining with , we have and (or see Oh et al. [12]). Let be the significance level. Then, as in Phillips et al. [25], (

14)

in Theorem 1 suggests that a confidence interval for can be constructed aswhere and are the lower bound and upper bound for respectively, and is the two-tailed α percentile critical value of the standard Cauchy distribution. For example, , , and . 3. Simulations

In this section, we conduct some simulations to evaluate the LS estimator

defined by (

2). The experimental data

are a realization from the following first-order autoregressive model

where

,

for some

,

, and

. In addition,

are mean zero random errors. Let the error vector

satisfy the Gaussian model such that

Here,

, and

is the covariance matrix satisfying

for some

.

is a positive symmetric matrix. Moreover, it is easy to check that the sequence

is geometrically

-mixing. For any moment of Gaussian random variable, it is finite. Combining this with Remark 1,

is

.

Firstly, we show the simulation of the empirical probability of the confidence interval (CI) for

defined by (

17). We consider the following parameter settings

The number of replications is always set at 10000 and the level of significance is 0.05. Let

be the indicator function. Applying (

17), we calculate the empirical probability of the true value

, i.e.,

where

and

are the two CI bounds of

in the

replication. The results are shown in

Table 1 and

Table 2.

From

Table 1 and

Table 2, we see that the CIs under

were relatively better than

. It may be that the volatility of

with

is relatively larger than the one with

. The CIs had good finite sample performance when

c was relatively large, and

was between 0.5 and 0.7. When

, it can be seen that the empirical probability was close to the nominal probability

.

Next, by (

15), (

16),

, and

, we give some histograms to illustrate

where

is a standard Cauchy random variable. We consider the following parameter settings

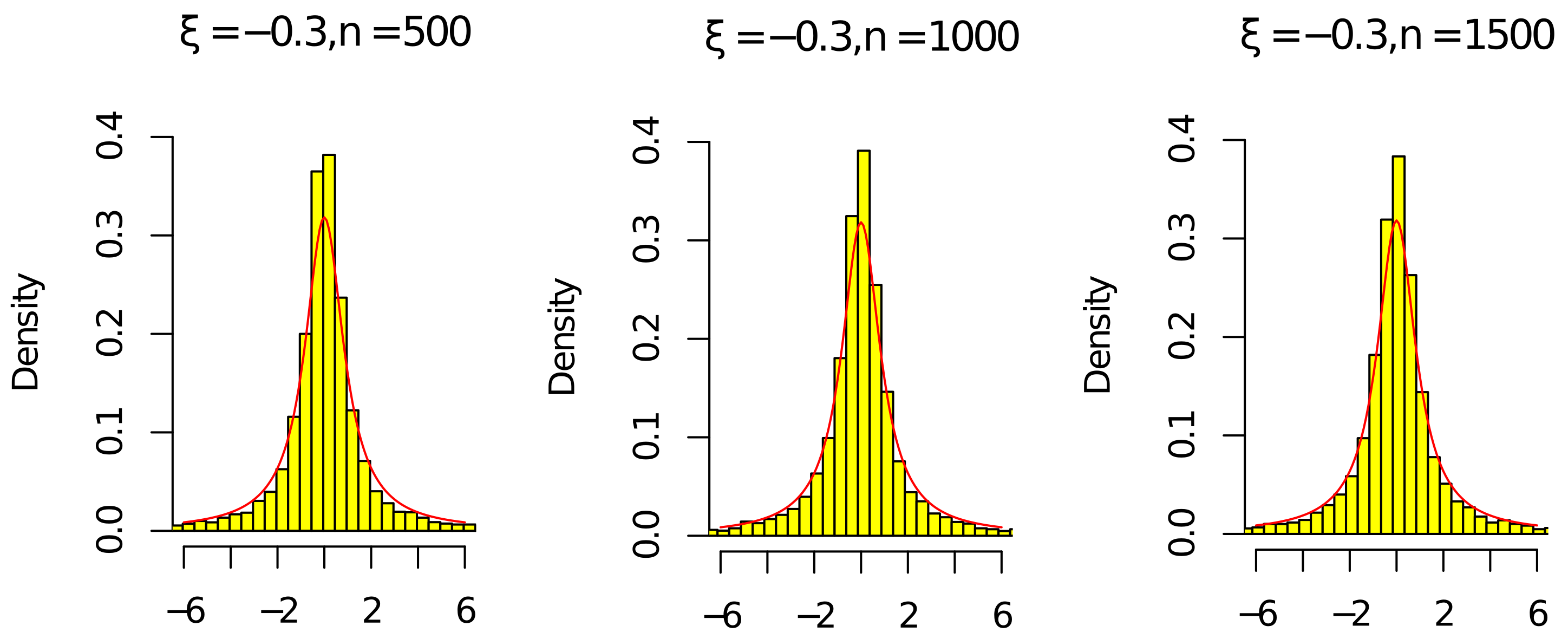

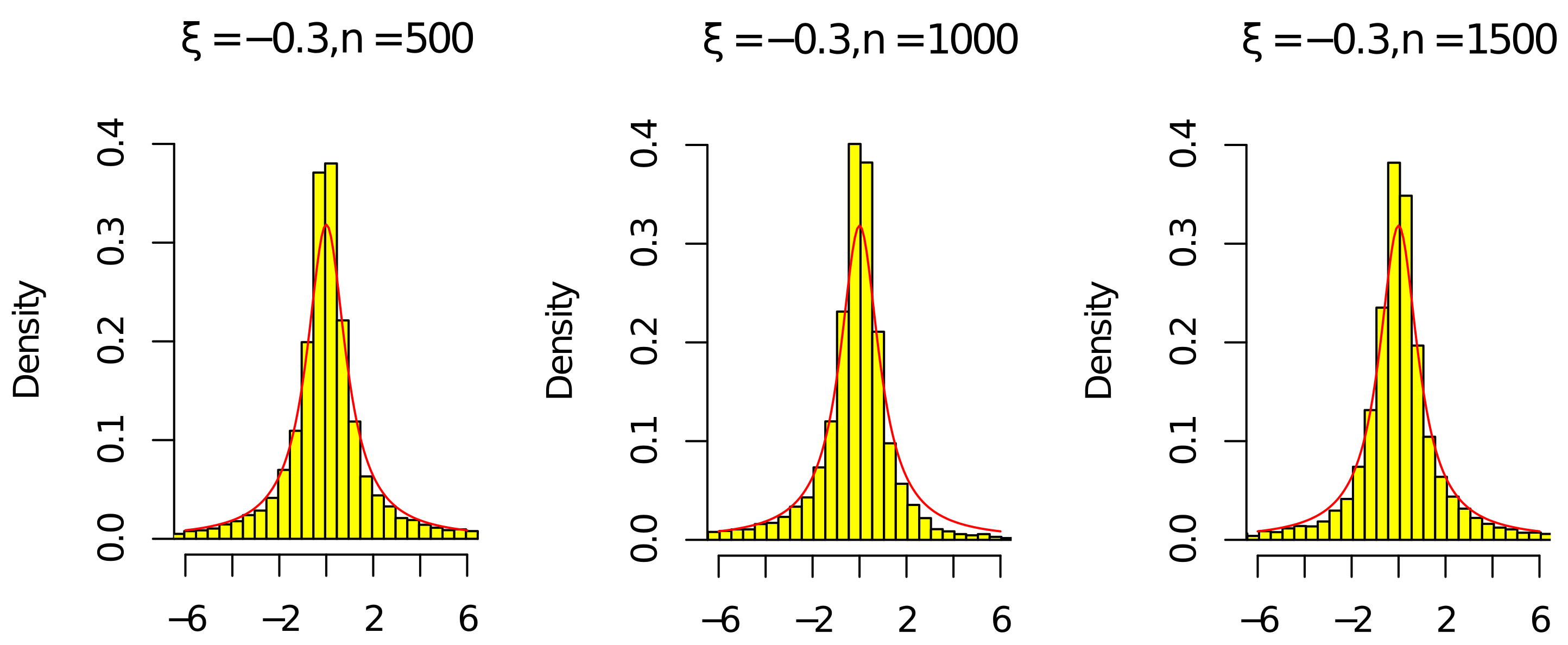

According to

Figure 1,

Figure 2,

Figure 3 and

Figure 4, the histograms

and

under

were relatively better than the ones under

(the volatility of

with

was relatively larger than the one with

). As the sample

n increased, the histograms

and

were close to the red line of the density of the standard Cauchy random variable. Thus, the results in

Figure 1,

Figure 2,

Figure 3 and

Figure 4 and

Table 1 and

Table 2 agree with (

14) in Theorem 1. Since the histograms with different

c and

were similar, we omit them here.

4. Real Data Analysis

In this section, we use the mildly explosive model (

7) and confidence interval estimation in (

17) to study the NASDAQ composite index during an inflation period. Similar to Phillips et al. [

25] and Liu et al. [

21], we consider the log-NASDAQ composite index for the period from April 2011 to April 2021, which contained 2522 observations denoted by

,

. In addition, we let

and

. The scatter plots of

are shown in

Figure 5. According to

Figure 5, the process of

was increasing. Then, we used the Augmented Dickey Fuller Test (ADF Test, see [

28]) to conduct the unit root test. The ADF test was −3.069 with Lag order 1, while the

p-value of the ADF test was 0.1257. This means that the process of

was nonstationary. Thus, the mildly explosive model

was considered to fit the process of

. We let

be the residuals of errors

,

, where

is the LS estimator of

defined by (

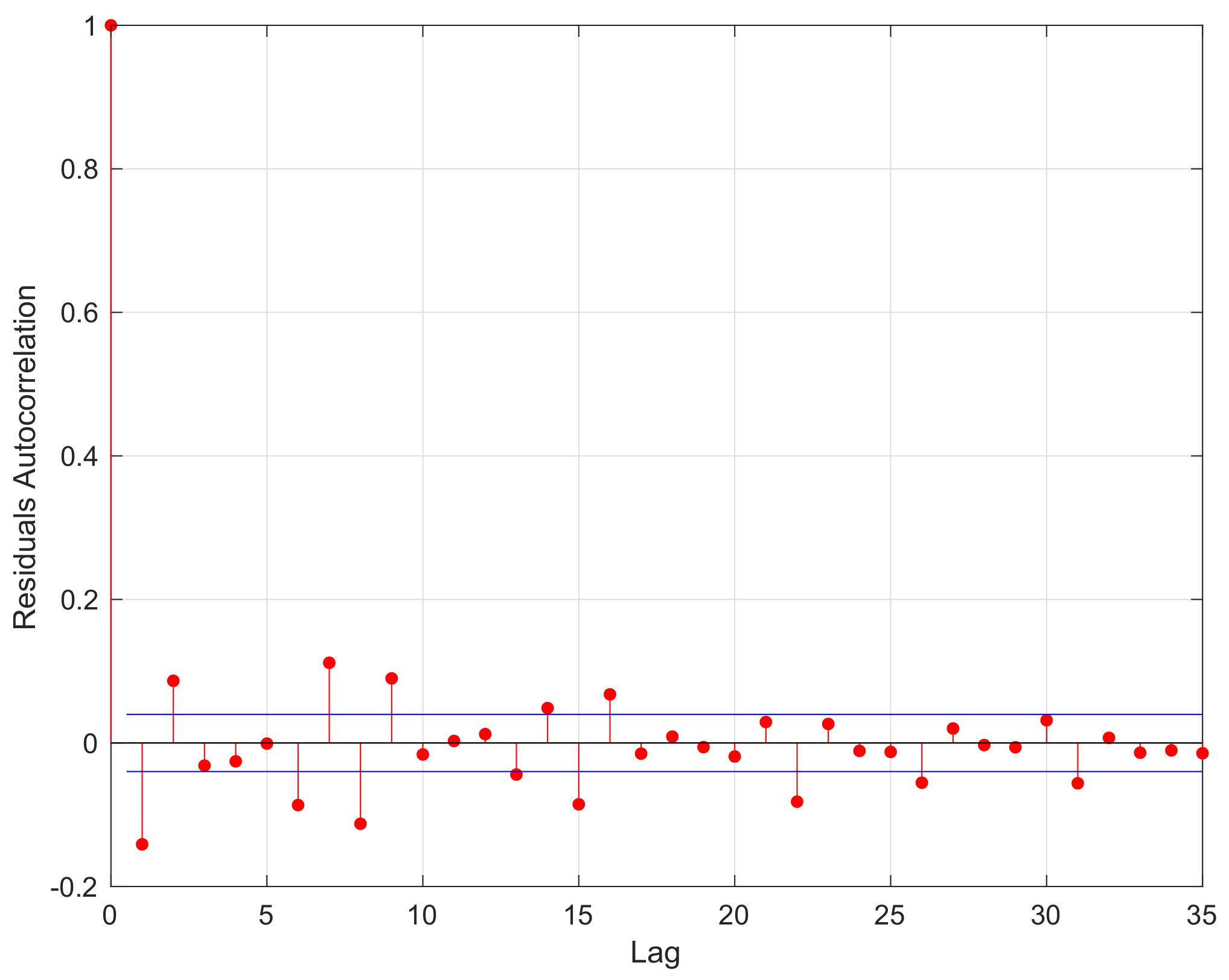

2). Then, the residuals’ autocorrelation function (ACF) of

is shown in

Figure 6.

According to

Figure 6, the autocorrelation coefficients for the residuals were around 0 as the Lag increased, which satisfied the property of

-mixing data. Then, the curves of the LS estimator

defined by (

2), lower bound

and upper bound

, for

are also shown in

Figure 7,

defined by (

17) is the value of the standard Cauchy distribution with significance level

. With

, the curves of

,

, and

are presented in

Figure 7.

According to

Figure 7, the values of

approached 1 as sample

n increased, while the lower bound

and upper bound

were around 1. In addition, by (

17), we let

, and

,

. The curves of

and

are also shown in

Figure 5. According to

Figure 5, the curve

was between curves

and

, while the curve widths of

and

were very small. Furthermore, the period from April 2011 to April 2021 was the takeoff period of technology stocks and a faster increase in U.S. Treasury yields. Thus, these real data are a good use of the mildly explosive model and the Cauchy limiting distribution of the LS estimator in Theorem 1.

5. Conclusions and Discussion

The study of the mildly explosive process has received much attention from researchers, as it can be used to test the explosive behavior of economic growth. Phillips and Magdalinos [

2] considered the mildly explosive process (

7) based on independent errors and obtained the Cauchy limiting distribution of the LS estimator

of

. Oh et al. [

12] extended Phillips and Magdalinos [

2] to geometrically

-mixing errors. Obviously, the assumption of geometrically

-mixing was very strong. Thus, we considered the mildly explosive process based on arithmetically

-mixing errors. Under the condition of the mixing coefficients

for some

, we re-proved the key Lemmas 1 and 2. Consequently, the Cauchy limiting distribution for

in Theorem 1 also held true. In order to illustrate the main result of the Cauchy limiting distribution, some simulations of the empirical probability of the confidence interval and the empirical density for

were presented in

Section 4. It had a good finite sample performances. As an application, we used the mildly explosive process to analyze real data from the NASDAQ composite index from April 2011 to April 2021. It was a takeoff period of technology stocks and a faster increase in U.S. Treasury yields. Moreover, it is of interest for researchers to study the random walk process, near-stationary process, mildly explosive process, and explosive process under heteroskedasticity errors (see Arvanitis and Magdalinos [

20]), anti-persistent errors (see Liu et al. [

21]), and other missing dependent data in the future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}