Breakpoint Analysis for the COVID-19 Pandemic and Its Effect on the Stock Markets

Abstract

1. Introduction

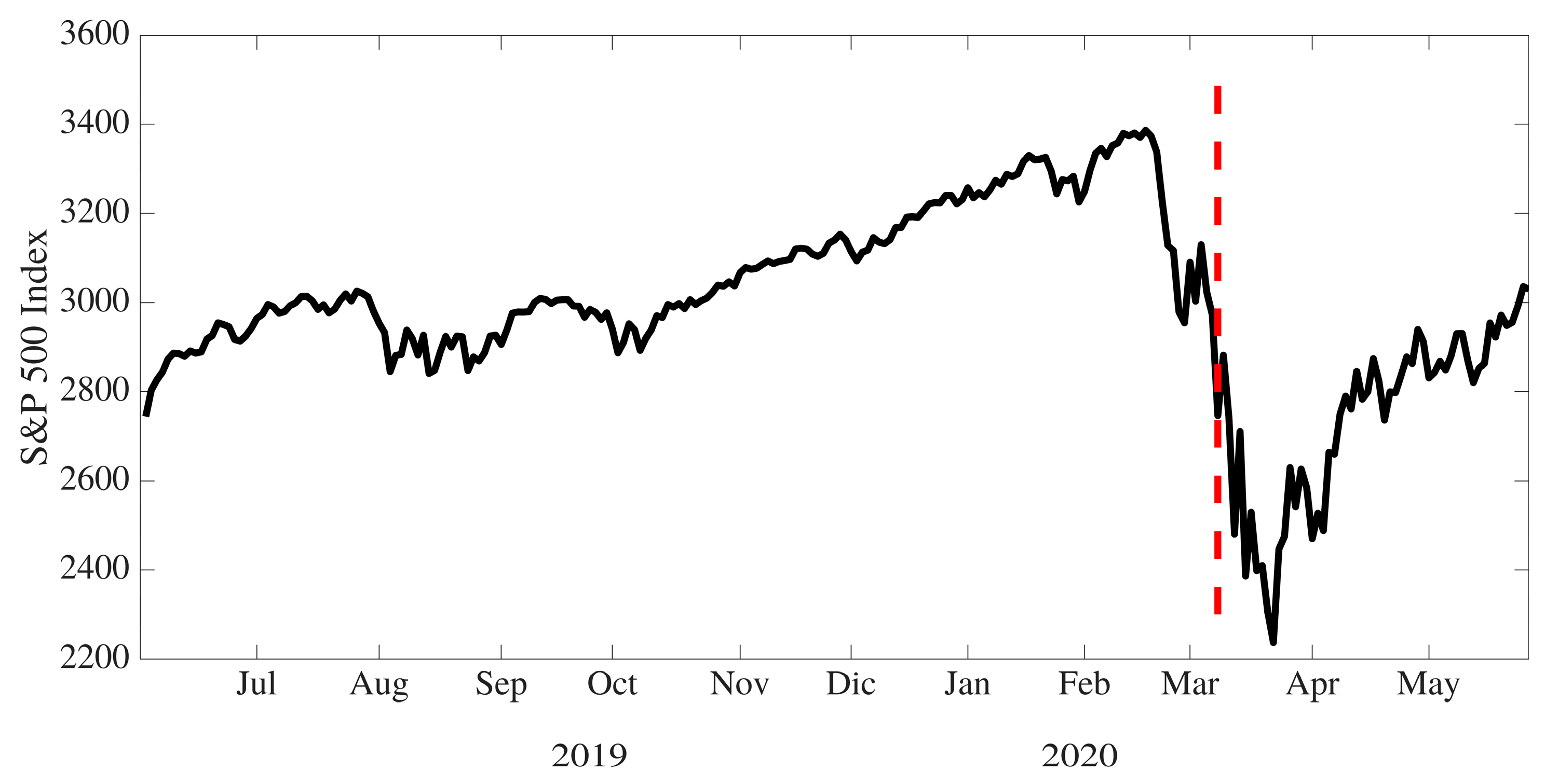

2. Modeling and Methodology

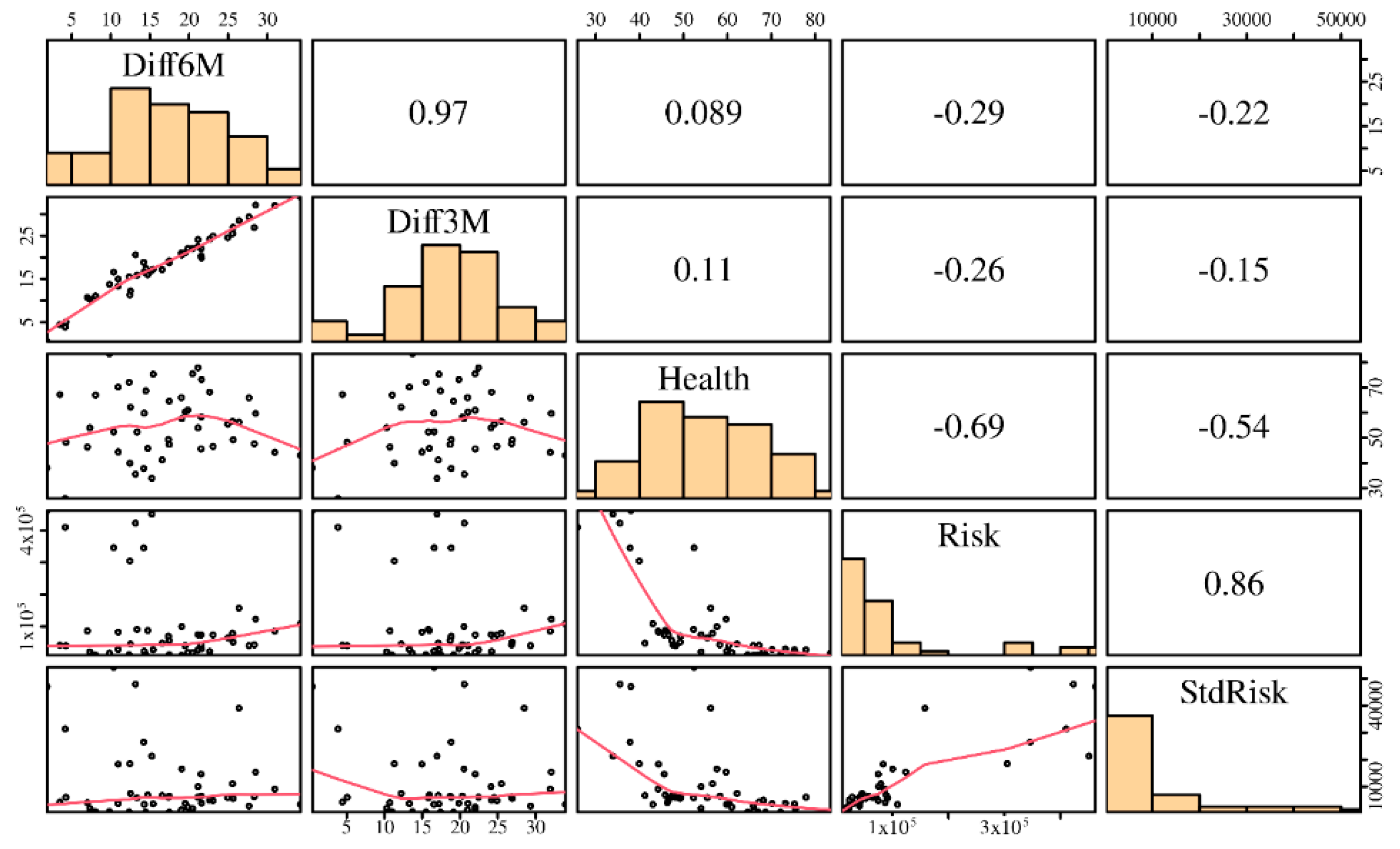

3. Results of the Study and Model Specification

4. Discussions, Conclusions, Limitations, and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Chen, M.P.; Lee, C.C.; Lin, Y.H.; Chen, W.Y. Did the SARS Epidemic Weaken the Integration of Asian Stock Markets? Evidence from Smooth Time-Varying Cointegration Analysis. Econ. Res. Ekon. Istraz. 2018, 31, 908–926. [Google Scholar]

- Ait-Sahalia, Y.; Cacho-Diaz, J.; Laeven, R.J.A. Modeling Financial Contagion Using Mutually Exciting Jump Processes. J. Financ. Econ. 2015, 117, 585–606. [Google Scholar] [CrossRef]

- Keogh-Brown, M.R.; Wren-Lewis, S.; Edmunds, W.J.; Smith, R.D. The Macroeconomic Impact of Pandemic Influenza: Estimates from Models of the United Kingdom, France, Belgium and the Netherlands. Eur. J. Health Econ. 2010, 11, 543–554. [Google Scholar] [CrossRef] [PubMed]

- Kostova, D.; Cassell, C.H.; Redd, J.T.; Williams, D.E.; Singh, T.; Martel, L.D.; Bunnell, R.E. Long-Distance Effects of Epidemics: Assessing the Link between the 2014 West Africa Ebola Outbreak and US Exports and Employment. Health Econ. 2019, 28, 1248–1261. [Google Scholar] [CrossRef] [PubMed]

- Tan, S.; Yu-Hung, A.L. Economic Repercussions of Extreme Events for an Island Nation: Case of Singapore. Singap. Econ. Rev. 2016, 61, 19. [Google Scholar] [CrossRef]

- Keogh-Brown, M.R.; Smith, R.D. The economic impact of SARS: How does the reality match the predictions. Health Policy 2008, 88, 110–120. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. Covid-19 Pandemic, Oil Prices, Stock Market, Geopolitical Risk and Policy Uncertainty Nexus in the Us Economy: Fresh Evidence from the Wavelet-Based Approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Lahmiri, S.; Bekiros, S. Randomness, Informational Entropy, and Volatility Interdependencies among the Major World Markets: The Role of the COVID-19 Pandemic. Entropy 2020, 22, 833. [Google Scholar] [CrossRef]

- Rassy, D.; Smith, R.D. The Economic Impact of H1N1 on Mexico’s Tourist and Pork Sectors. Health Econ. 2013, 22, 824–834. [Google Scholar] [CrossRef]

- Wang, Y.H.; Yang, F.J.; Chen, L.J. An Investor’s Perspective on Infectious Diseases and Their Influence on Market Behavior. J. Bus. Econ. Manag. 2013, 14, S112–S127. [Google Scholar] [CrossRef]

- De Luca, G.; Loperfido, N. A Skew-in-Mean GARCH Model for Financial Returns. In Skew-Elliptical Distributions and Their Applications: A Journey beyond Normality; CRC/Chapman and Hall: London, UK, 2004; pp. 205–222. [Google Scholar]

- De Luca, G.; Loperfido, N. Modelling Multivariate Skewness in Financial Returns: A SGARCH Approach. Eur. J. Financ. 2015, 21, 1113–1131. [Google Scholar] [CrossRef]

- Nortey, E.N.N.; Asare, K.; Mettle, F.O. Extreme Value Modelling of Ghana Stock Exchange Index. Springerplus 2015, 4, 17. [Google Scholar] [CrossRef]

- Sewraj, D.; Gebka, B.; Anderson, R.D.J. Identifying Contagion: A Unifying Approach. J. Int. Financ. Mark. Inst. Money 2018, 55, 224–240. [Google Scholar] [CrossRef]

- Ivanov, I.; Kabaivanov, S.; Bogdanova, B. Stock Market Recovery from the 2008 Financial Crisis: The Differences across Europe. Res. Int. Bus. Financ. 2016, 37, 360–374. [Google Scholar] [CrossRef]

- Imran, M.; Wu, M.Y.; Gu, S.B.; Saud, S.; Abbas, M. Influence of Economic and Non-Economic Factors on Firm Level Equity Premium: Evidence from Pakistan. Econ. Bull. 2019, 39, 1774. [Google Scholar]

- Su, X.F. Dynamic Behaviors and Contributing Factors of Volatility Spillovers across G7 Stock Markets. N. Am. J. Econ. Financ. 2020, 53, 16. [Google Scholar] [CrossRef]

- Hajizadeh, E.; Seifi, A.; Zarandi, M.N.F.; Turksen, I.B. A Hybrid Modeling Approach for Forecasting the Volatility of S&P 500 Index Return. Expert Syst. Appl. 2012, 39, 431–436. [Google Scholar]

- Vera Leyton, M. Contagio del Mercado Accionario: Casos de Colombia, Mexico, Peru, Chile y Argentina. Dimens. Empresarial 2020, 18, 1–32. [Google Scholar]

- Forbes, K.; Rigobon, R. No Contagion, Only Interdependence: Measuring Stock Market Comovements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Feng, L.; Zhang, X.; Liu, B. Multivariate Tests of Independence and Their Application in Correlation Analysis between Financial Markets. J. Multivar. Anal. 2020, 179, 104652. [Google Scholar] [CrossRef]

- Kaminsky, G.L.; Reinhart, C.M. On Crises, Contagion, and Confusion. J. Int. Econ. 2000, 51, 145–168. [Google Scholar] [CrossRef]

- Blommestein, H.; Eijffinger, S.; Qian, Z.X. Regime-Dependent Determinants of Euro Area Sovereign CDS Spreads. J. Financ. Stab. 2016, 22, 10–21. [Google Scholar] [CrossRef]

- Galariotis, E.C.; Makrichoriti, P.; Spyrou, S. Sovereign Cds Spread Determinants and Spill-over Effects during Financial Crisis: A Panel Var Approach. J. Financ. Stab. 2016, 26, 62–77. [Google Scholar] [CrossRef]

- Allen, F.; Gale, D. Financial Contagion. J. Political Econ. 2000, 108, 1–33. [Google Scholar] [CrossRef]

- Anastasopoulos, A. Testing for Financial Contagion: New Evidence from the Greek Crisis and Yuan Devaluation. Res. Int. Bus. Financ. 2018, 45, 499–511. [Google Scholar] [CrossRef]

- Jin, X.Y.; An, X.M. Global Financial Crisis and Emerging Stock Market Contagion: A Volatility Impulse Response Function Approach. Res. Int. Bus. Financ. 2016, 36, 179–195. [Google Scholar] [CrossRef]

- Karanasos, M.; Yfanti, S.; Karoglou, M. Multivariate Fiaparch Modelling of Financial Markets with Dynamic Correlations in Times of Crisis. Int. Rev. Financ. Anal. 2016, 45, 332–349. [Google Scholar] [CrossRef]

- Zhu, Y.G.; Yang, F.; Ye, W.Y. Financial Contagion Behavior Analysis Based on Complex Network Approach. Ann. Oper. Res. 2018, 268, 93–111. [Google Scholar] [CrossRef]

- Kokholm, T. Pricing and Hedging of Derivatives in Contagious Markets. J. Bank. Financ. 2016, 66, 19–34. [Google Scholar] [CrossRef]

- Oikonomikou, L.E. Modeling Financial Market Volatility in Transition Markets: A Multivariate Case. Res. Int. Bus. Financ. 2018, 45, 307–322. [Google Scholar] [CrossRef]

- Lewis, V.; Roth, M. The Financial Market Effects of the ECB’s Asset Purchase Programs. J. Financ. Stab. 2019, 43, 40–52. [Google Scholar] [CrossRef]

- Ahundjanov, B.B.; Akhundjanov, S.B.; Okhunjanov, B.B. Information Search and Financial Markets under COVID-19. Entropy 2020, 22, 791. [Google Scholar] [CrossRef] [PubMed]

- Drożdż, S.; Kwapień, J.; Oświęcimka, P.; Stanisz, T.; Wątorek, M. Complexity in Economic and Social Systems: Cryptocurrency Market at around COVID-19. Entropy 2020, 22, 1043. [Google Scholar] [CrossRef]

- Mounier-Jack, S.; Coker, R.J. How prepared is Europe for pandemic influenza? Analysis of national plans. Lancet 2006, 367, 1405–1411. [Google Scholar] [CrossRef]

- Umaña-Hermosilla, B.; De la Fuente-Mella, H.; Elórtegui-Gómez, C.; Fonseca-Fuentes, M. Multinomial Logistic Regression to Estimate and Predict the Perceptions of Individuals and Companies in the Face of the COVID-19 Pandemic in the Ñuble Region, Chile. Sustainability 2020, 12, 9553. [Google Scholar] [CrossRef]

- Global Health Security Index: Building Collective Action and Accountability. Nuclear Threat Initiative and Johns Hopkins School of Public Health. 2019. Available online: https://www.ghsindex.org/wp-content/uploads/2019/10/2019-Global-Health-Security-Index.pdf (accessed on 23 September 2020).

- Pan, J. and K.J. Singleton. Default and Recovery Implicit in the Term Structure of Sovereign CDS Spreads. J. Financ. 2008, 63, 2345–2384. [Google Scholar] [CrossRef]

- Fontana, A.; Scheicher, M. An Analysis of Euro Area Sovereign Cds and Their Relation with Government Bonds. J. Bank. Financ. 2016, 62, 126–140. [Google Scholar] [CrossRef]

- Quandt, R. Tests of the hypothesis that a linear regression system obeys two separate regimes. J. Am. Stat. Assoc. 1960, 55, 324–330. [Google Scholar] [CrossRef]

- Andrews, D.W.K. Tests for Parameter Instability and Structural Change with Unknown Change Point. Econometrica 2003, 71, 395–397. [Google Scholar] [CrossRef]

- Paz, A.; De la Fuente-Mella, H.; Singh, A.; Conover, R.; Monteiro, H. Highway expenditures and associated customer satisfaction: A case study. Math. Probl. Eng. 2016, 2016, 4630492. [Google Scholar] [CrossRef]

- Coughenour, C.; De la Fuente-Mella, H.; Paz, A. Analysis of self-reported walking for transit in a sprawling urban metropolitan area in the western US. Sustainability 2019, 852, 2–16. [Google Scholar]

- Huerta, M.; Leiva, V.; Liu, S.; Rodriguez, M.; Villegas, D. On a partial least squares regression model for asymmetric data with a chemical application in mining. Chemom. Intell. Lab. Syst. 2019, 190, 55–68. [Google Scholar] [CrossRef]

- De la Fuente-Mella, H.; Vallina, A.; Solis, R. Stochastic analysis of the economic growth of OECD countries. Econ. Res. Ekon. Istraž. 2020, 33, 2189–2202. [Google Scholar] [CrossRef]

- Greene, W.H. Econometric Analysis; Pearson: New York, NY, USA, 2018. [Google Scholar]

- Altonji, J.G.; Segal, L.M. Small-sample bias in GMM estimation of covariance structures. J. Bus. Econ. Stat. 1996, 14, 353–366. [Google Scholar]

- Clark, T.E. Small-Sample Properties of Estimators of Nonlinear Models of Covariance Structure. J. Bus. Econ. Stat. 1996, 14, 367–373. [Google Scholar]

- Santos, L.A.; Barrios, E.B. Small sample estimation in dynamic panel data models: A simulation study. Am. Open J. Stat. 2011, 1, 58–73. [Google Scholar] [CrossRef]

- Harvey, A. Estimating regression models with multiplicative heteroscedasticity. Econom. J. Econom. Soc. 1976, 461–465. [Google Scholar] [CrossRef]

- Hart, R.; Clark, D. Does size matter? Exploring the small sample properties of maximum likelihood estimation. In Proceedings of the Annual Meeting of the Midwest Political Science Association, Chicago, IL, USA, 20–22 April 1999. [Google Scholar]

- Vallina-Hernandez, A.M.; de la Fuente-Mella, H.; Fuentes-Solís, R. International Trade and Innovation: Delving in Latin American Commerce. Acad. Rev. Latinoam. Adm. 2020, 33, 535–547. [Google Scholar] [CrossRef]

- Wang, T.; Samworth, R.J. High-dimensional Changepoint Estimation via Sparse Projection. arXiv 2016, arXiv:1606.06246. [Google Scholar]

- De la Fuente-Mella, H.; Rojas Fuentes, J.L.; Leiva, V. Econometric Modeling of Productivity and Technical Efficiency in the Chilean Manufacturing Industry. Comput. Ind. Eng. 2020, 139, 105793. [Google Scholar] [CrossRef]

- Díaz-García, J.A.; Galea, M.; Leiva, V. Influence Diagnostics for Multivariate Elliptic Regression Linear Models. Commun. Stat. Theory Methods 2003, 32, 625–641. [Google Scholar] [CrossRef]

- Leiva, V.; Saulo, H.; Souza, R.; Aykroyd, R.G.; Vila, R. A New BISARMA Time Series Model for Forecasting Mortality using Weather and Particulate Matter Data. J. Forecast. 2020. [Google Scholar] [CrossRef]

- Sanchez, L.; Leiva, V.; Galea, M.; Saulo, H. Birnbaum-Saunders Quantile Regression Models with Application to Spatial Data. Mathematics 2020, 8, 1000. [Google Scholar] [CrossRef]

- Carrasco, J.M.F.; Figueroa-Zúñiga, J.I.; Leiva, V.; Riquelme, M.; Aykroyd, R.G. An Errors-in-Variables Model based on the Birnbaum-Saunders Distribution and its Diagnostics with an Application to Earthquake Data. Stoch. Environ. Res. Risk Assess. 2020, 34, 369–380. [Google Scholar] [CrossRef]

- Velasco, H.; Laniado, H.; Toro, M.; Leiva, V.; Lio, Y. Robust Three-step Regression based on Comedian and its Performance in Cell-wise and Case-wise Outliers. Mathematics 2020, 8, 1259. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Country | Index | Country | Index | Country | Index | Country | Index |

|---|---|---|---|---|---|---|---|

| Australia | Asx 200 | France | * EN 100 | Nigeria | Nse 30 | Serbia | Belex 15 |

| Belgium | Bel 20 | Germany | Dax | Norway | Oseax | Slovakia | Sax |

| Brazil | Ibov | Hungary | Bux | NZ | Nzx 50 | SK | Kospi 50 |

| Bulgaria | Sofix | Italy | Ftse Mib | Pakistan | Kse 100 | Spain | Ibex |

| Canada | Tsx | India | Nifty 50 | Peru | Igbvl | SL | Cse |

| Chile | Ipsa | IN | Jci | Philippines | Psei | Sweden | Omx 30 |

| China | Shanghai | Irak | Isx | Poland | Wig 30 | SW | Smi |

| Colombia | Colcap | Iceland | Icexi | Portugal | Psi 20 | Thailand | Set |

| Croatia | Crobex | Israel | Ta 100 | Qatar | Qe | Turkey | Xu 100 |

| Cyprus | Cymain | Japan | Nikkei 225 | Romania | Bet | Ukraine | Pfts |

| Egypt | Egx 70 | Malaysia | Fbm Klci | Russia | Moex | UK | Ftse 100 |

| Finland | Hex 25 | Mexico | Mexbol | SA | ** MT 30 | US | S&P500 |

| Country | Date | Country | Date | Country | Date | Country | Date |

|---|---|---|---|---|---|---|---|

| Australia | 03/09/20 | France | 03/09/20 | Nigeria | 03/11/20 | Serbia | 03/12/20 |

| Belgium | 03/09/20 | Germany | 03/09/20 | Norway | 03/09/20 | Slovakia | 03/17/20 |

| Brazil | 03/04/20 | Hungary | 03/09/20 | NZ | 03/12/20 | SK | 03/12/20 |

| Bulgaria | 03/09/20 | Italy | 03/09/20 | Pakistan | 03/16/20 | Spain | 03/09/20 |

| Canada | 03/09/20 | India | 03/12/20 | Peru | 03/12/20 | SL | 01/31/20 |

| Chile | 03/13/20 | IN | 03/09/20 | Philippines | 03/09/20 | Sweden | 03/09/20 |

| China | 03/16/20 | Iraq | 12/18/19 | Poland | 03/09/20 | SW | 03/06/20 |

| Colombia | 03/09/20 | Iceland | 03/06/20 | Portugal | 03/09/20 | Thailand | 03/09/20 |

| Cyprus | 03/09/20 | Israel | 03/09/20 | Qatar | 03/02/20 | Turkey | 03/09/20 |

| Croatia | 03/09/20 | Japan | 03/06/20 | Romania | 03/09/20 | Ukraine | 02/10/20 |

| Egypt | 03/16/20 | Malaysia | 03/06/20 | Russia | 03/10/20 | UK | 03/09/20 |

| Finland | 03/09/20 | Mexico | 03/09/20 | SA | 03/09/20 | US | 03/09/20 |

| Variable | Minimum | Maximum | Mean | Standard Deviation |

|---|---|---|---|---|

| Health | 25.80 | 83.50 | 54.87 | 13.22 |

| Risk | 11,037.89 | 462,453.50 | 106,106.13 | 130,742.35 |

| StdRisk | 505.46 | 54,134.31 | 10,521.88 | 12,775.89 |

| Diff3M | 1.87 | 34.23 | 16.67 | 7.69 |

| Diff6M | 0.47 | 33.96 | 18.34 | 7.44 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| Variable | (Diff3M) | (Diff6M) | (Diff3M) | (Diff6M) | (Diff3M) | (Diff6M) |

| Health | 0.0618 | 0.0199 | 0.0312 | 0.0125 | 0.0243 | 0.0064 |

| (0.141) | (0.145) | (0.149) | (0.154) | (0.150) | (0.155) | |

| Log(Risk) | −1.631 | −2.574 | −1.477 | −2.537 | −0.61 | −1.773 |

| (3.026) | (3.111) | (3.056) | (3.156) | (3.239) | (3.353) | |

| Log(StdRisk) | 1.712 | 2.146 | 1.719 | 2.148 | 0.923 | 1.447 |

| (2.215) | (2.276) | (2.23) | (2.303) | (2.433) | (2.519) | |

| OECD | 1.806 | 0.437 | 1.36 | 0.0449 | ||

| (2.766) | (2.857) | (2.827) | (2.927) | |||

| Log(GDP) | 0.463 | 0.408 | ||||

| (0.556) | (0.576) | |||||

| Constant | 18.37 | 25.6 | 17.36 | 25.35 | 12.49 | 21.06 |

| (27.09) | (27.85) | (27.32) | (28.22) | (28.04) | (29.03) | |

| 0.026 | 0.028 | 0.035 | 0.029 | 0.051 | 0.040 | |

| F-statistic | 0.376 | 0.415 | 0.385 | 0.31 | 0.444 | 0.345 |

| Breusch–Pagan test | ||||||

| (1) | 4.10 | 3.92 | 7.10 | 4.60 | 5.29 | 3.68 |

| Prob | 0.0428 | 0.0476 | 0.0077 | 0.0320 | 0.0214 | 0.0551 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| Variable | (Diff3M) | (Diff6M) | (Diff3M) | (Diff6M) | (Diff3M) | (Diff6M) |

| Health | 0.038 | 0.0203 | −0.00258 | 0.00543 | −0.130 *** | −0.130 *** |

| (0.113) | (0.118) | (0.104) | (0.116) | (0.0190) | (0.0275) | |

| Log(Risk) | −1.545 | −2.903 | −1.811 | −3.105 | −3.628 *** | −5.336 *** |

| (2.744) | (2.946) | (2.588) | (2.900) | (0.403) | (0.584) | |

| Log(StdRisk) | 2.481 | 3.535 * | 3.114 * | 3.900 ** | 4.718 *** | 6.035 *** |

| (1.877) | (2.010) | (1.718) | (1.897) | (0.266) | (0.386) | |

| OECD | 3.367 | 1.924 | 8.157 ** | 7.115 * | ||

| (2.325) | (2.47) | (3.44) | (3.796) | |||

| Constant | 12.33 | 17.32 | 9.765 | 16.69 | 21.20 *** | 26.65 *** |

| (22.9) | (24.7) | (21.14) | (24.30) | (4.992) | (6.518) | |

| Health | −0.018 | −0.0244 | −0.0133 | −0.0165 | 0.00280 | 0.000176 |

| (0.0261) | (0.0256) | (0.0261) | (0.0261) | (0.0401) | (0.0441) | |

| Log(Risk) | 0.761 | 0.723 | 0.915 | 0.833 | −1.905 * | −1.545 |

| (0.586) | (0.575) | (0.624) | (0.608) | (1.055) | (1.083) | |

| Log(StdRisk) | −0.342 | −0.439 | −0.608 | −0.566 | 1.549 ** | 1.291 |

| (0.472) | (0.445) | (0.493) | (0.462) | (0.780) | (0.786) | |

| OECD | −0.847 * | −0.627 | −1.532 ** | −1.235 * | ||

| (0.467) | (0.454) | (0.714) | (0.716) | |||

| Log(GDP) | −2.253 *** | −2.136 *** | ||||

| (0.568) | (0.550) | |||||

| Constant | −0.598 | 1.117 | 0.103 | 0.851 | 25.78 *** | 23.13 ** |

| (4.978) | (4.997) | (4.918) | (4.958) | (8.948) | (9.030) | |

| Likelihood Ratio Test for | ||||||

| 0.0570 | 0.1180 | 0.0144 | 0.0824 | 0.0000 | 0.0001 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chahuán-Jiménez, K.; Rubilar, R.; de la Fuente-Mella, H.; Leiva, V. Breakpoint Analysis for the COVID-19 Pandemic and Its Effect on the Stock Markets. Entropy 2021, 23, 100. https://doi.org/10.3390/e23010100

Chahuán-Jiménez K, Rubilar R, de la Fuente-Mella H, Leiva V. Breakpoint Analysis for the COVID-19 Pandemic and Its Effect on the Stock Markets. Entropy. 2021; 23(1):100. https://doi.org/10.3390/e23010100

Chicago/Turabian StyleChahuán-Jiménez, Karime, Rolando Rubilar, Hanns de la Fuente-Mella, and Víctor Leiva. 2021. "Breakpoint Analysis for the COVID-19 Pandemic and Its Effect on the Stock Markets" Entropy 23, no. 1: 100. https://doi.org/10.3390/e23010100

APA StyleChahuán-Jiménez, K., Rubilar, R., de la Fuente-Mella, H., & Leiva, V. (2021). Breakpoint Analysis for the COVID-19 Pandemic and Its Effect on the Stock Markets. Entropy, 23(1), 100. https://doi.org/10.3390/e23010100