Information Transfer between Stock Market Sectors: A Comparison between the USA and China

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Method and Data

2.1. Symbolic Transfer Entropy

2.2. Data Description

3. Results and Discussion

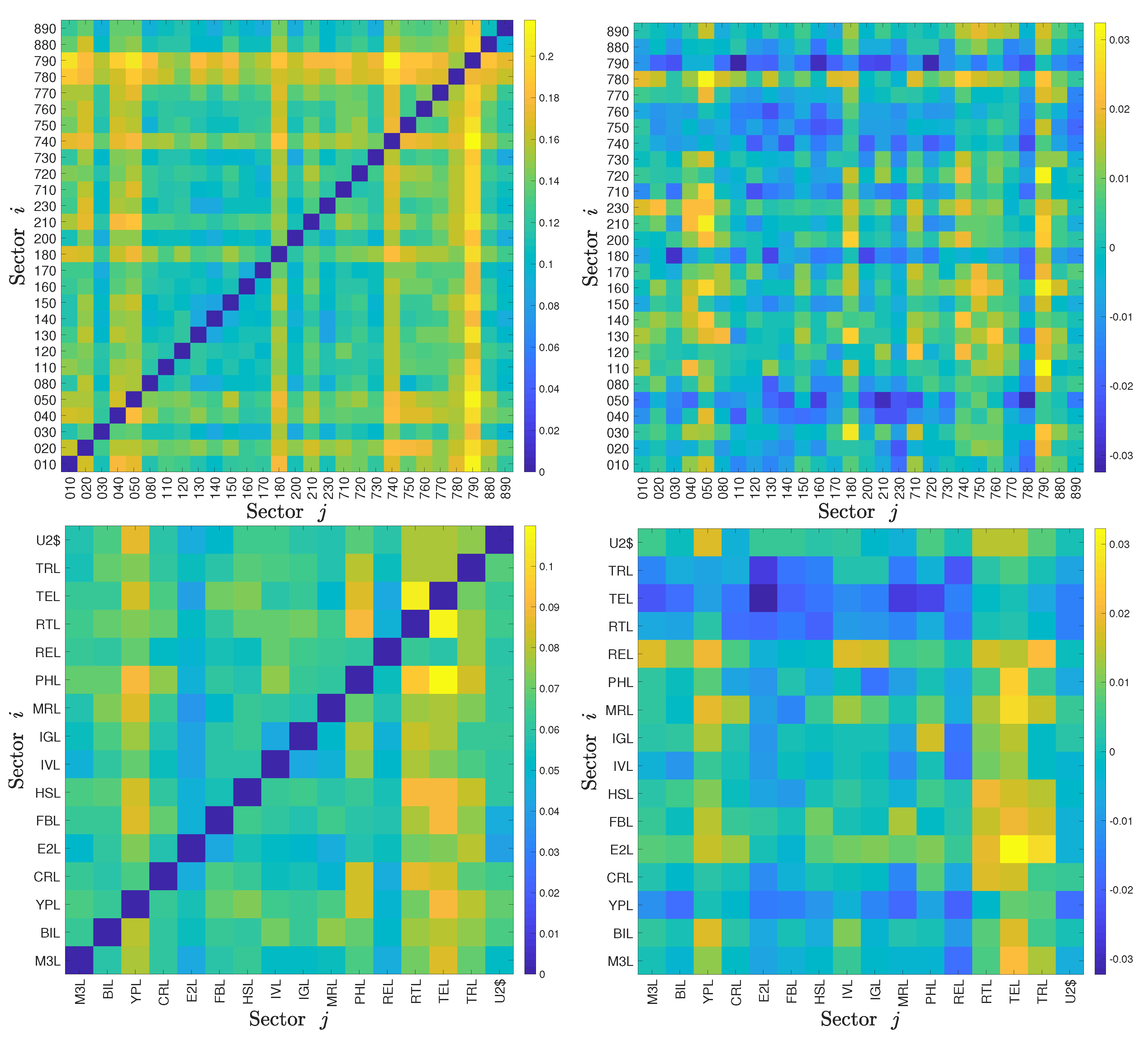

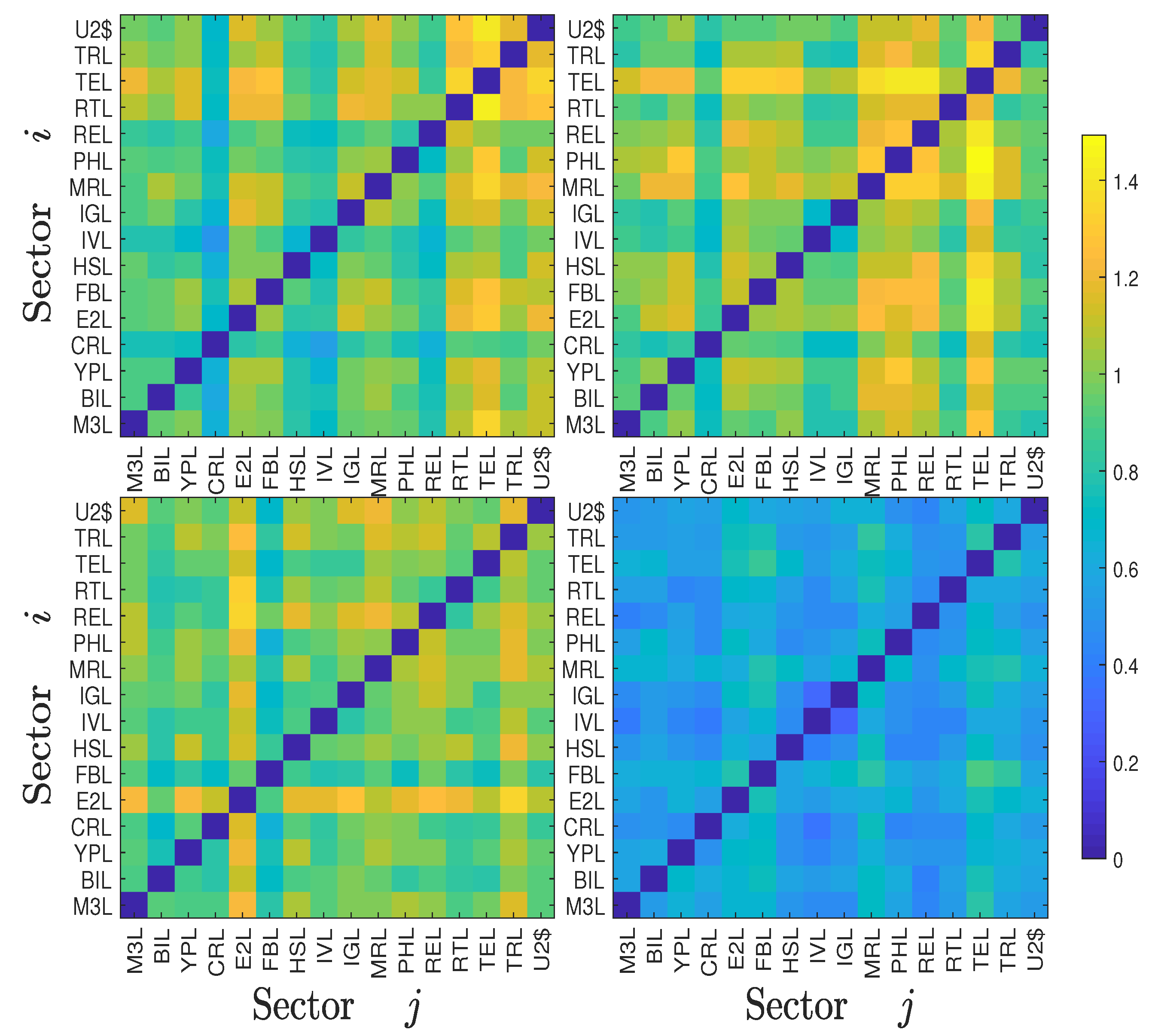

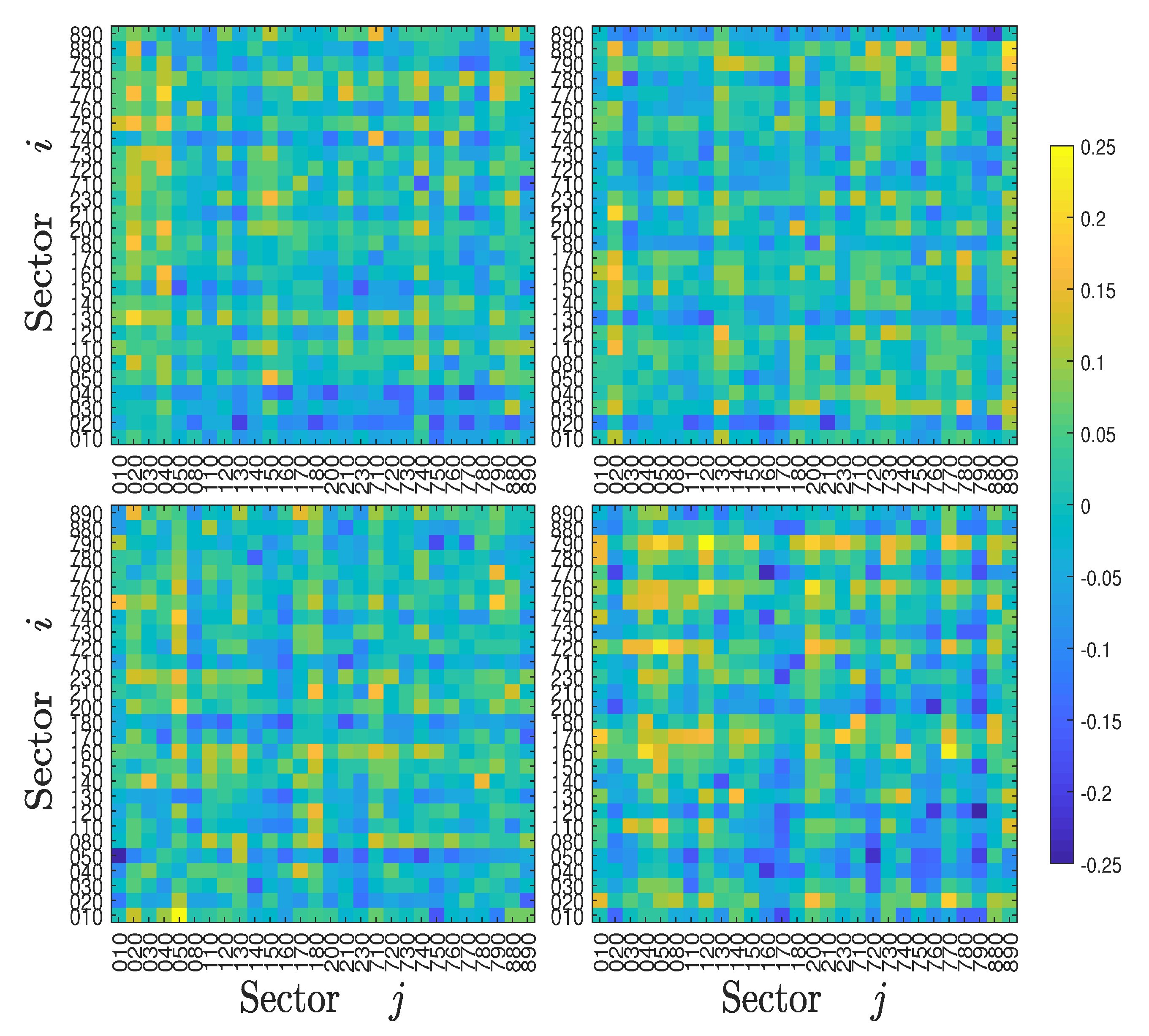

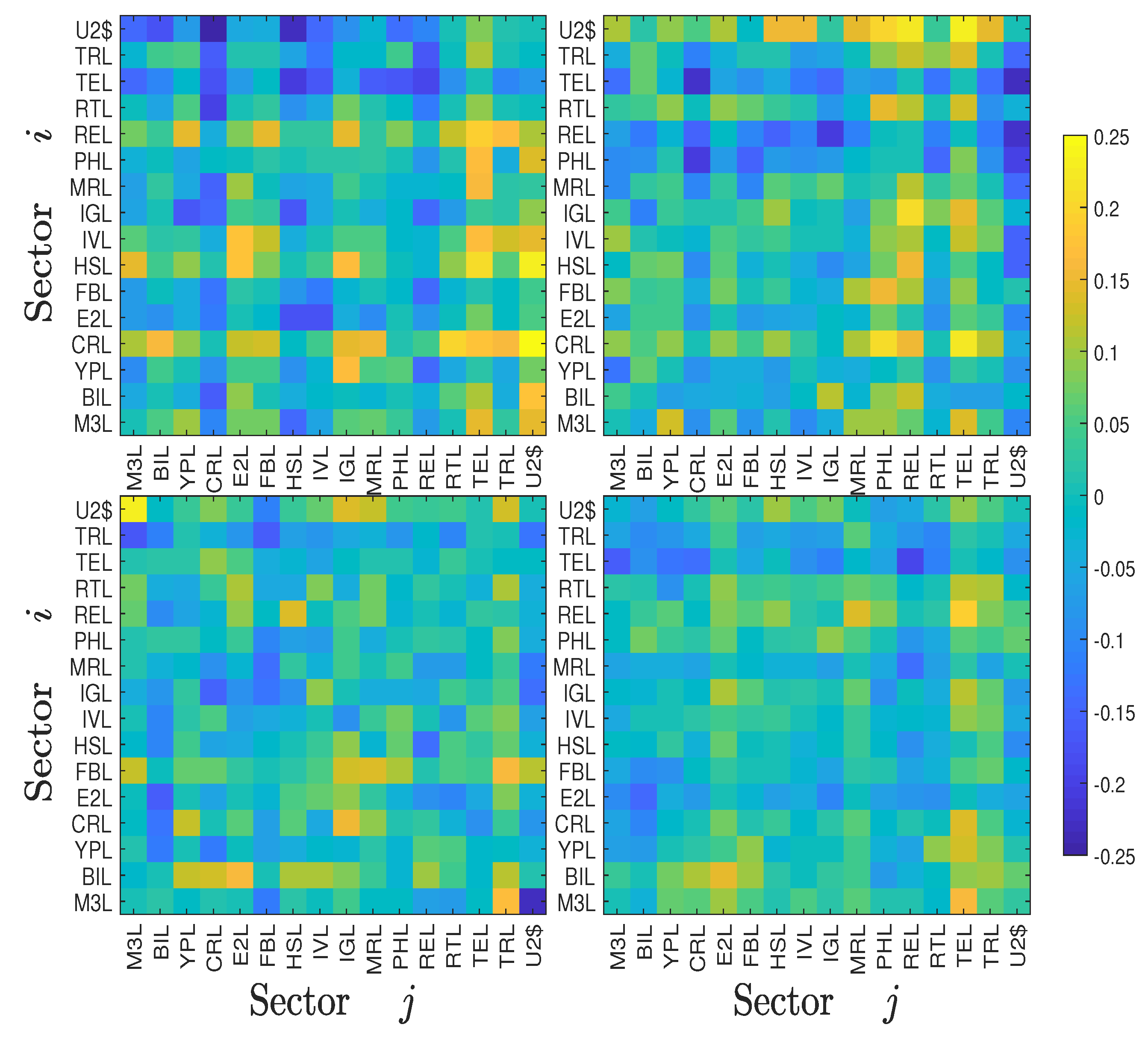

3.1. Symbolic Transfer Entropy and Degree of Asymmetric Information Flow of the Whole Samples

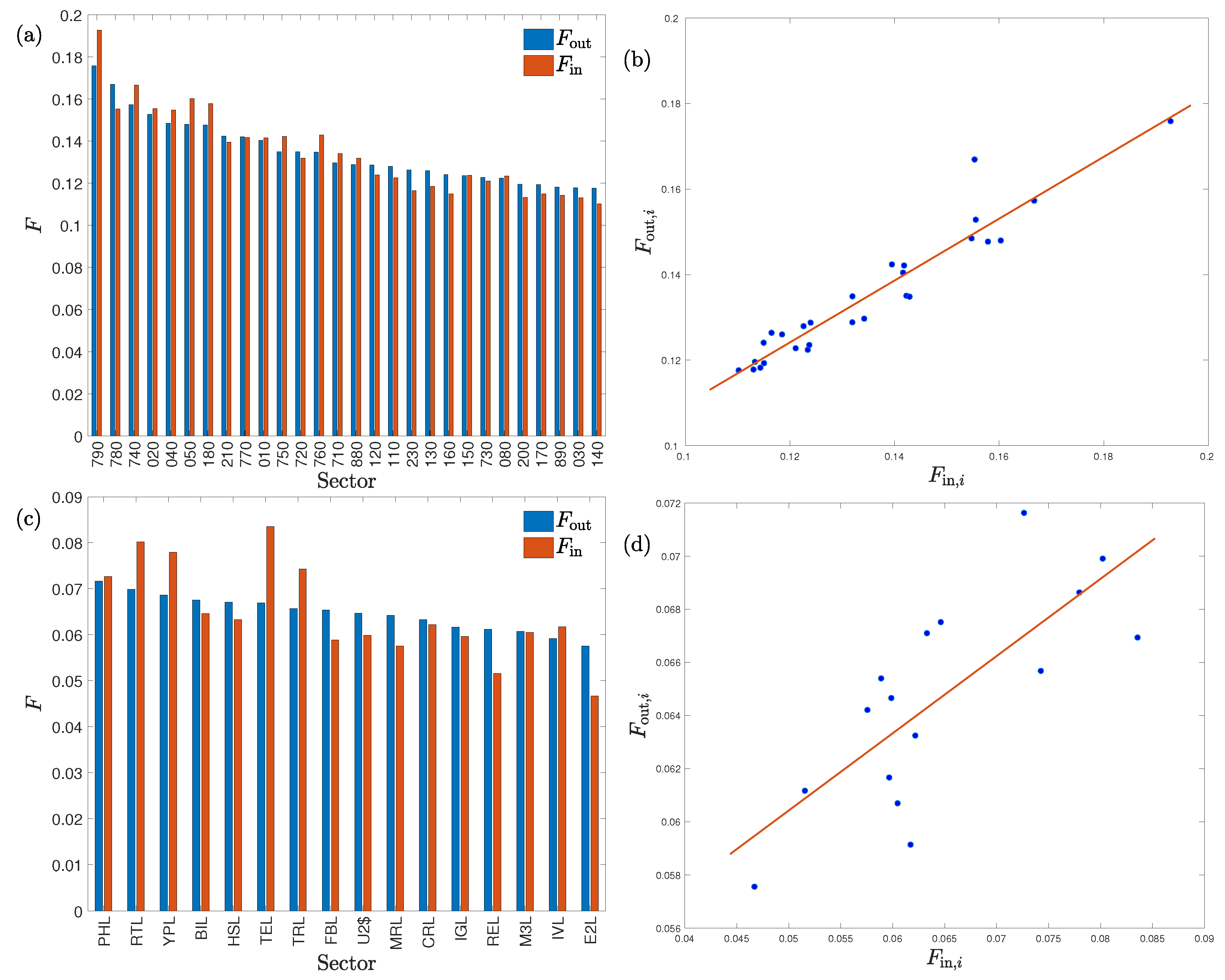

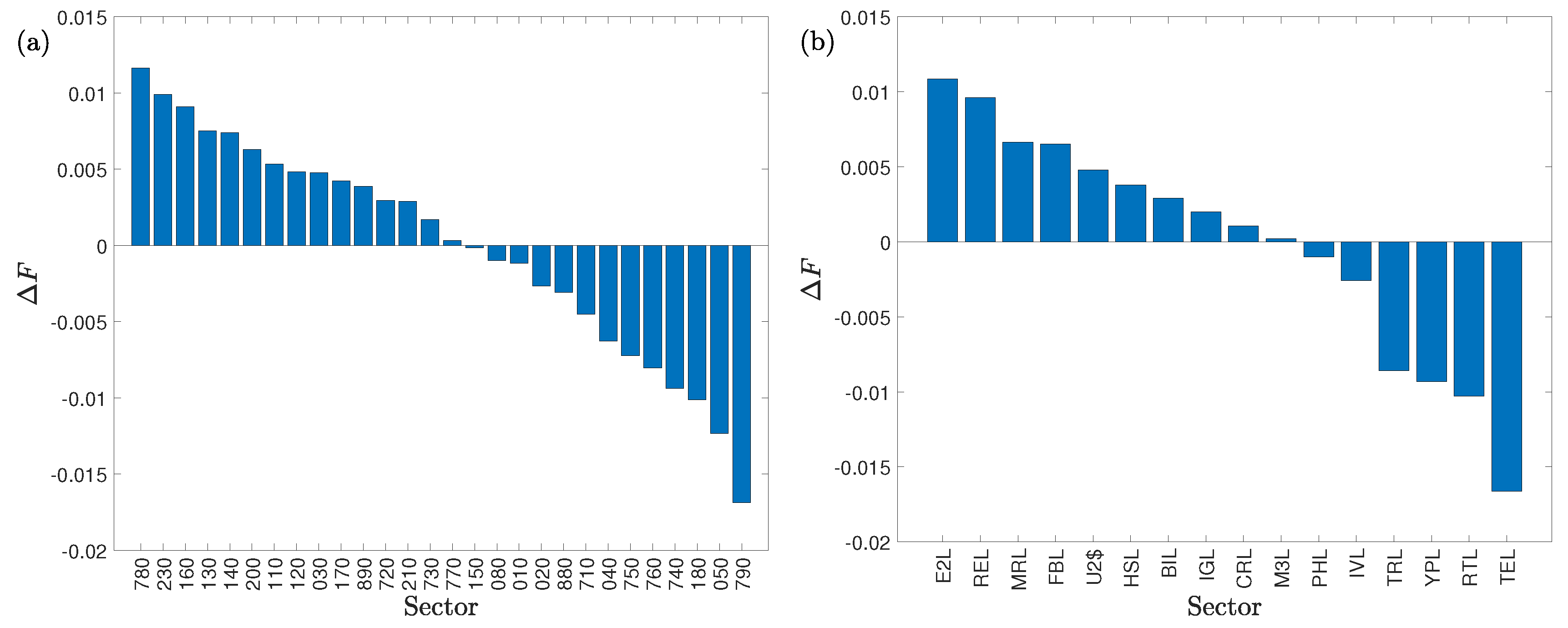

3.2. Average Inflow and Outflow

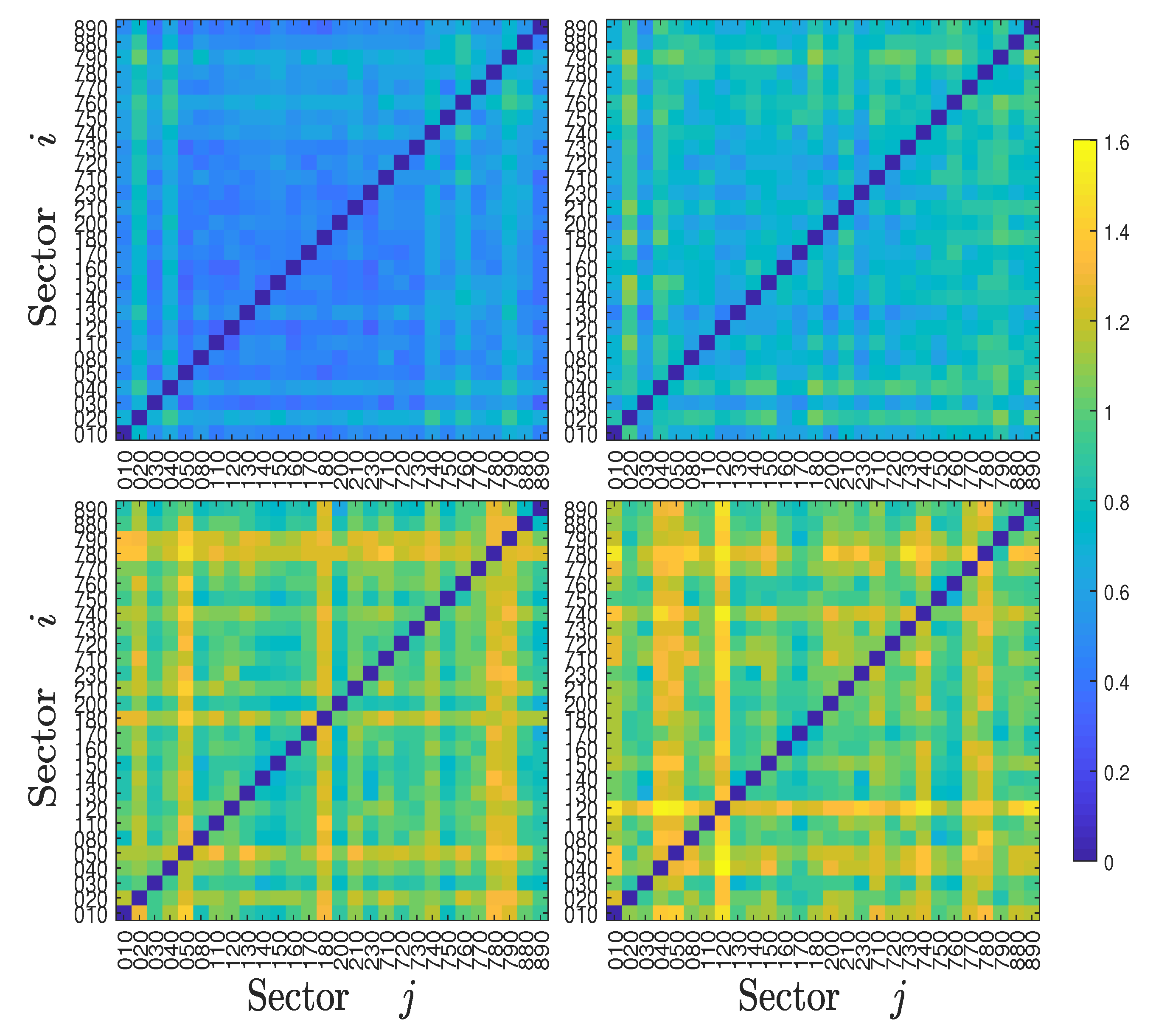

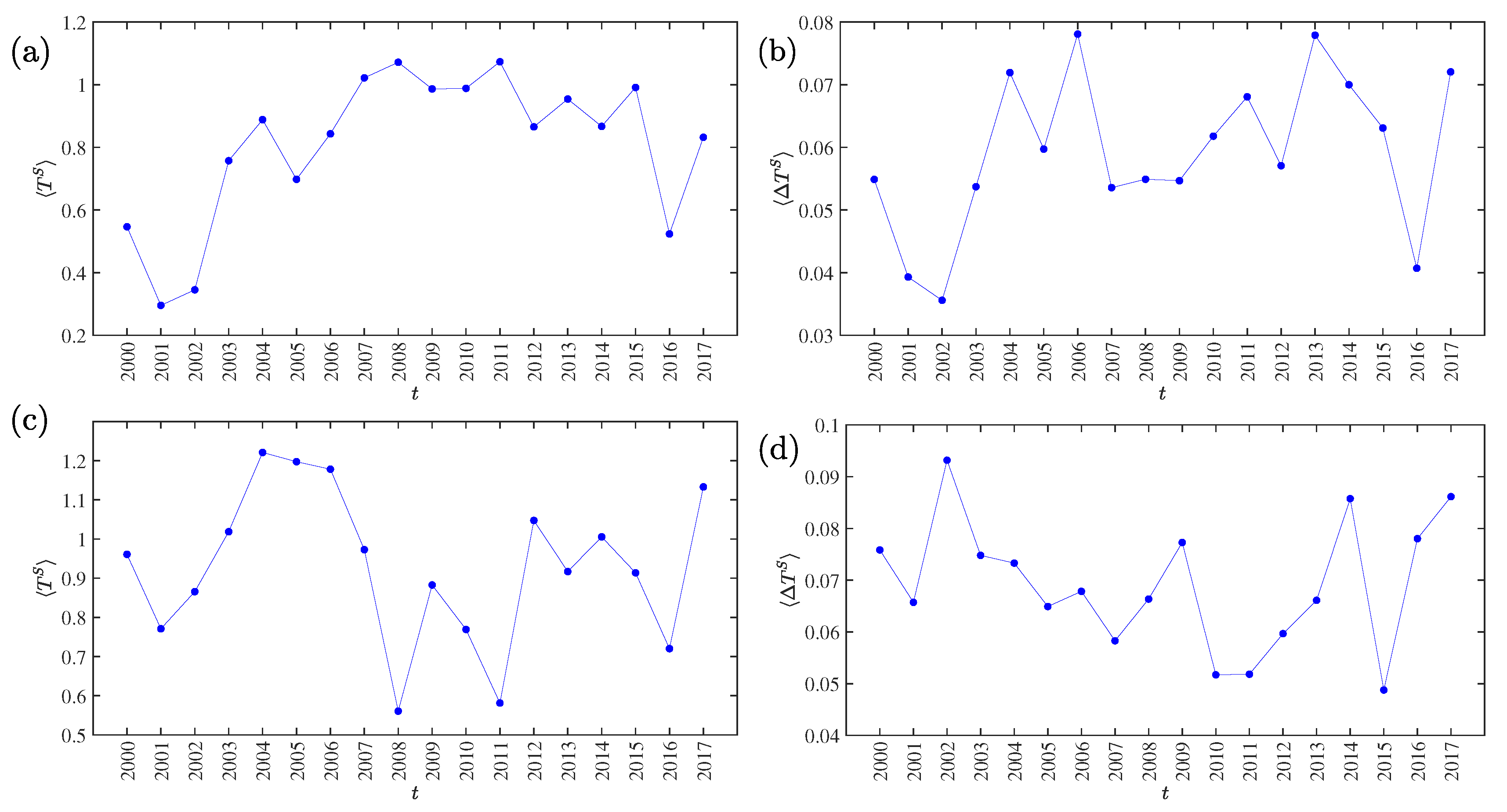

3.3. Yearly Evolution of Symbolic Transfer Entropy and Degree of Asymmetric Information Flow

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Mantegna, R.N.; Stanley, H.E. An Introduction to Econophysics: Correlations and Complexity in Finance; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Zhang, Z.C.; Zhang, Y.J.; Shen, D.H.; Zhang, W. The dynamic cross-correlations between mass media news, new media news, and stock returns. Complexity 2018, 2018, 7619494. [Google Scholar] [CrossRef]

- Shan, J.; Pappas, N. The relative impacts of Japanese and US interest rates on local interest rates in Australia and Singapore: A Granger causality test. Appl. Financ. Econ. 2000, 10, 291–298. [Google Scholar] [CrossRef]

- Sornette, D.; Zhou, W.X. Non-parametric determination of real-time lag structure between two time series: The “optimal thermal causal path” method. Quant. Financ. 2005, 5, 577–591. [Google Scholar] [CrossRef]

- Meng, H.; Xu, H.C.; Zhou, W.X.; Sornette, D. Symmetric thermal optimal path and time-dependent lead-lag relationship: Novel statistical tests and application to UK and US real-estate and monetary policies. Quant. Financ. 2017, 17, 959–977. [Google Scholar] [CrossRef]

- Xu, H.C.; Zhou, W.X.; Sornette, D. Time-dependent lead-lag relationship between the onshore and offshore Renminbi exchange rates. J. Int. Financ. Mark. Inst. Money 2017, 49, 173–183. [Google Scholar] [CrossRef]

- Dionisio, A.; Menezes, R.; Mendes, D.A. Mutual information: a measure of dependency for nonlinear time series. Physica A 2004, 344, 326–329. [Google Scholar] [CrossRef]

- Abigail, J. A complex network model for seismicity based on mutual information. Physica A 2013, 392, 2498–2506. [Google Scholar] [CrossRef]

- Fiedor, P. Networks in financial markets based on the mutual information rate. Phys. Rev. E 2014, 89, 052801. [Google Scholar] [CrossRef]

- Ghysels, E.; Hill, J.B.; Motegi, K. Testing for Granger causality with mixed frequency data. J. Econom. 2016, 192, 207–230. [Google Scholar] [CrossRef]

- Gotz, T.B.; Hecq, A.; Smeekes, S. Testing for Granger causality in large mixed-frequency VARs. J. Econom. 2016, 193, 418–432. [Google Scholar] [CrossRef]

- Barnett, L.; Bossomaier, T. Transfer entropy as a log-likelihood ratio. Phys. Rev. Lett. 2012, 109, 138105. [Google Scholar] [CrossRef] [PubMed]

- Schreiber, T. Measuring information transfer. Phys. Rev. Lett. 2000, 85, 461–464. [Google Scholar] [CrossRef] [PubMed]

- Ai, X.B. Inferring a drive-response network from time series of topological measures in complex networks with transfer entropy. Entropy 2014, 16, 5753–5776. [Google Scholar] [CrossRef]

- Hu, Y.Z.; Zhao, H.Y.; Ai, X.B. Inferring weighted directed association networks from multivariate time series with the small-shuffle symbolic transfer entropy spectrum method. Entropy 2016, 18, 328. [Google Scholar] [CrossRef]

- Yook, S.H.; Chae, H.; Kim, J.; Kim, Y. Finding modules and hierarchy in weighted financial network using transfer entropy. Physica A 2016, 447, 493–501. [Google Scholar] [CrossRef]

- Borge-Holthoefer, J.; Peera, N.; Goncalves, B.; Gonzalez-Bailon, S.; Arenas, A.; Moreno, Y.; Vespignani, A. The dynamics of information-driven coordination phenomena: A transfer entropy analysis. Sci. Adv. 2016, 2, e1501158. [Google Scholar] [CrossRef]

- Zhang, N.N.; Lin, A.J.; Shang, P.J. Multiscale symbolic phase transfer entropy in financial time series classification. Fluct. Noise Lett. 2017, 16, 1750019. [Google Scholar] [CrossRef]

- Toriumi, F.; Komura, K. Investment index construction from information propagation based on transfer entropy. Comput. Econ. 2018, 51, 159–172. [Google Scholar] [CrossRef]

- Servadio, J.L.; Convertino, M. Optimal information networks: Application for data-driven integrated health in populations. Sci. Adv. 2018, 4, e1701088. [Google Scholar] [CrossRef]

- Zhang, Y.P.; Shang, P.J.; Xiong, H.; Xia, J.A. Multiscale analysis of time irreversibility based on phase-space reconstruction and horizontal visibility graph approach. Fluct. Noise Lett. 2018, 17, 1850006. [Google Scholar] [CrossRef]

- He, J.Y.; Shang, P.J. Comparison of transfer entropy methods for financial time series. Physica A 2017, 482, 772–785. [Google Scholar] [CrossRef]

- Staniek, M.; Lehnertz, K. Symbolic transfer entropy. Phys. Rev. Lett. 2008, 100, 158101. [Google Scholar] [CrossRef] [PubMed]

- Marschinski, R.; Kantz, H. Analysing the information flow between financial time series. Eur. Phys. J. B 2002, 30, 275–281. [Google Scholar] [CrossRef]

- Mao, X.G.; Shang, P.J. Transfer entropy between multivariate time series. Commun. Nonlinear Sci. Numer. Simul. 2017, 47, 338–347. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. Using transfer entropy to measure information flows between financial markets. Stud. Nonlinear Dyn. Econom. 2013, 17, 85–102. [Google Scholar] [CrossRef]

- Kwon, O.; Yang, J.S. Information flow between stock indices. EPL (Europhys. Lett.) 2008, 82, 68003. [Google Scholar] [CrossRef]

- Kwon, O.; Yang, J.S. Information flow between composite stock index and individual stocks. Physica A 2008, 387, 2851–2856. [Google Scholar] [CrossRef]

- Kwon, O.; Oh, G. Asymmetric information flow between market index and individual stocks in several stock markets. EPL (Europhys. Lett.) 2012, 97, 28007. [Google Scholar] [CrossRef]

- Oh, G.; Oh, T.; Kim, H.Y.; Kwon, O. An information flow among industry sectors in the Korean stock market. J. Korean Phys. Soc. 2014, 65, 2140–2146. [Google Scholar] [CrossRef]

- Leibon, G.; Pauls, S.; Rockmore, D.; Savell, R. Topological structures in the equities market network. Proc. Natl. Acad. Sci. USA 2008, 105, 20589–20594. [Google Scholar] [CrossRef]

- Sandoval, L., Jr. Structure of a global network of financial companies based on transfer entropy. Entropy 2014, 16, 4443–4482. [Google Scholar] [CrossRef]

- Song, D.M.; Tumminello, M.; Zhou, W.X.; Mantegna, R.N. Evolution of worldwide stock markets, correlation structure, and correlation-based graphs. Phys. Rev. E 2011, 84, 026108. [Google Scholar] [CrossRef] [PubMed]

- Zhou, W.X.; Sornette, D. Antibubble and prediction of China’s stock market and real-estate. Physica A 2004, 337, 243–268. [Google Scholar] [CrossRef]

- Jiang, Z.Q.; Zhou, W.X.; Sornette, D.; Woodard, R.; Bastiaensen, K.; Cauwels, P. Bubble diagnosis and prediction of the 2005-2007 and 2008-2009 Chinese stock market bubbles. J. Econ. Behav. Org. 2010, 74, 149–162. [Google Scholar] [CrossRef]

- Sornette, D.; Demos, G.; Zhang, Q.; Cauwels, P.; Filimonov, V.; Zhang, Q.Z. Real-time prediction and post-mortem analysis of the Shanghai 2015 stock market bubble and crash. J. Investig. Strateg. 2015, 4, 77–95. [Google Scholar] [CrossRef]

- Wei, L.J.; Zhang, W.; Xiong, X. The mechanism and solution for the liquidity stampede crisis in stock markets. J. Manag. Sci. China 2017, 13, 1–23. (In Chinese) [Google Scholar]

- Charles, A.; Darne, O. Large shocks and the September 11th terrorist attacks on international stock markets. Econ. Model. 2006, 23, 683–698. [Google Scholar] [CrossRef]

- Demyanyk, Y.; Hemert, O.V. Understanding the subprime mortgage crisis. Rev. Financ. Stud. 2011, 24, 1848–1880. [Google Scholar] [CrossRef]

- Jayech, S. The contagion channels of July-August-2011 stock market crash: A DAG-copula based approach. Eur. J. Oper. Res. 2016, 249, 631–646. [Google Scholar] [CrossRef]

- Han, R.Q.; Xie, W.J.; Xiong, X.; Zhang, W.; Zhou, W.X. Market correlation structure changes around the Great Crash: A random matrix theory analysis of the Chinese stock market. Fluct. Noise Lett. 2017, 16, 1750018. [Google Scholar] [CrossRef]

- Maasoumi, E.; Racine, J. Entropy and predictability of stock market returns. J. Econom. 2002, 107, 291–312. [Google Scholar] [CrossRef]

- Eom, C.; Oh, G.; Jung, W.S. Relationship between efficiency and predictability in stock price change. Physica A 2008, 387, 5511–5517. [Google Scholar] [CrossRef]

- Lahmiri, S. Entropy-based technical analysis indicators selection for international stock markets fluctuations prediction using support vector machines. Fluct. Noise Lett. 2014, 13, 1450013. [Google Scholar] [CrossRef]

- Zhou, R.X.; Zhan, Y.; Cai, R.; Tong, G.Q. A mean-variance hybrid-entropy model for portfolio selection with fuzzy returns. Entropy 2015, 17, 3319–3331. [Google Scholar] [CrossRef]

- Zou, Y.C.; Yu, L.A.; He, K.J. Wavelet entropy based analysis and forecasting of crude oil price dynamics. Entropy 2015, 17, 7167–7184. [Google Scholar] [CrossRef]

- Benedetto, F.; Giunta, G.; Mastroeni, L. On the predictability of energy commodity markets by an entropy-based computational method. Energy Econ. 2016, 54, 302–312. [Google Scholar] [CrossRef]

- Hou, Y.F.; Liu, F.Y.; Gao, J.B.; Cheng, C.X.; Song, C.Q. Characterizing complexity changes in Chinese stock markets by permutation entropy. Entropy 2017, 19, 514. [Google Scholar] [CrossRef]

- Gu, R.B. Multiscale Shannon entropy and its application in the stock market. Physica A 2017, 484, 215–224. [Google Scholar] [CrossRef]

- Begušić, S.; Kostanjćar, Z.; Kovač, D.; Stanley, H.E.; Podobnik, B. Information feedback in temporal networks as a predictor of market crashes. Complexity 2018, 2018, 2834680. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yue, P.; Fan, Y.; Batten, J.A.; Zhou, W.-X. Information Transfer between Stock Market Sectors: A Comparison between the USA and China. Entropy 2020, 22, 194. https://doi.org/10.3390/e22020194

Yue P, Fan Y, Batten JA, Zhou W-X. Information Transfer between Stock Market Sectors: A Comparison between the USA and China. Entropy. 2020; 22(2):194. https://doi.org/10.3390/e22020194

Chicago/Turabian StyleYue, Peng, Yaodong Fan, Jonathan A. Batten, and Wei-Xing Zhou. 2020. "Information Transfer between Stock Market Sectors: A Comparison between the USA and China" Entropy 22, no. 2: 194. https://doi.org/10.3390/e22020194

APA StyleYue, P., Fan, Y., Batten, J. A., & Zhou, W.-X. (2020). Information Transfer between Stock Market Sectors: A Comparison between the USA and China. Entropy, 22(2), 194. https://doi.org/10.3390/e22020194