A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry

Abstract

1. Introduction

2. Materials

2.1. Blockchain Technology

2.1.1. Peer to Peer Network

2.1.2. Consensus Mechanism

2.1.3. Permissions

2.1.4. Smart Contract

2.2. Supply Chain Finance

2.3. Blockchain-Driven Supply Chain Finance Application

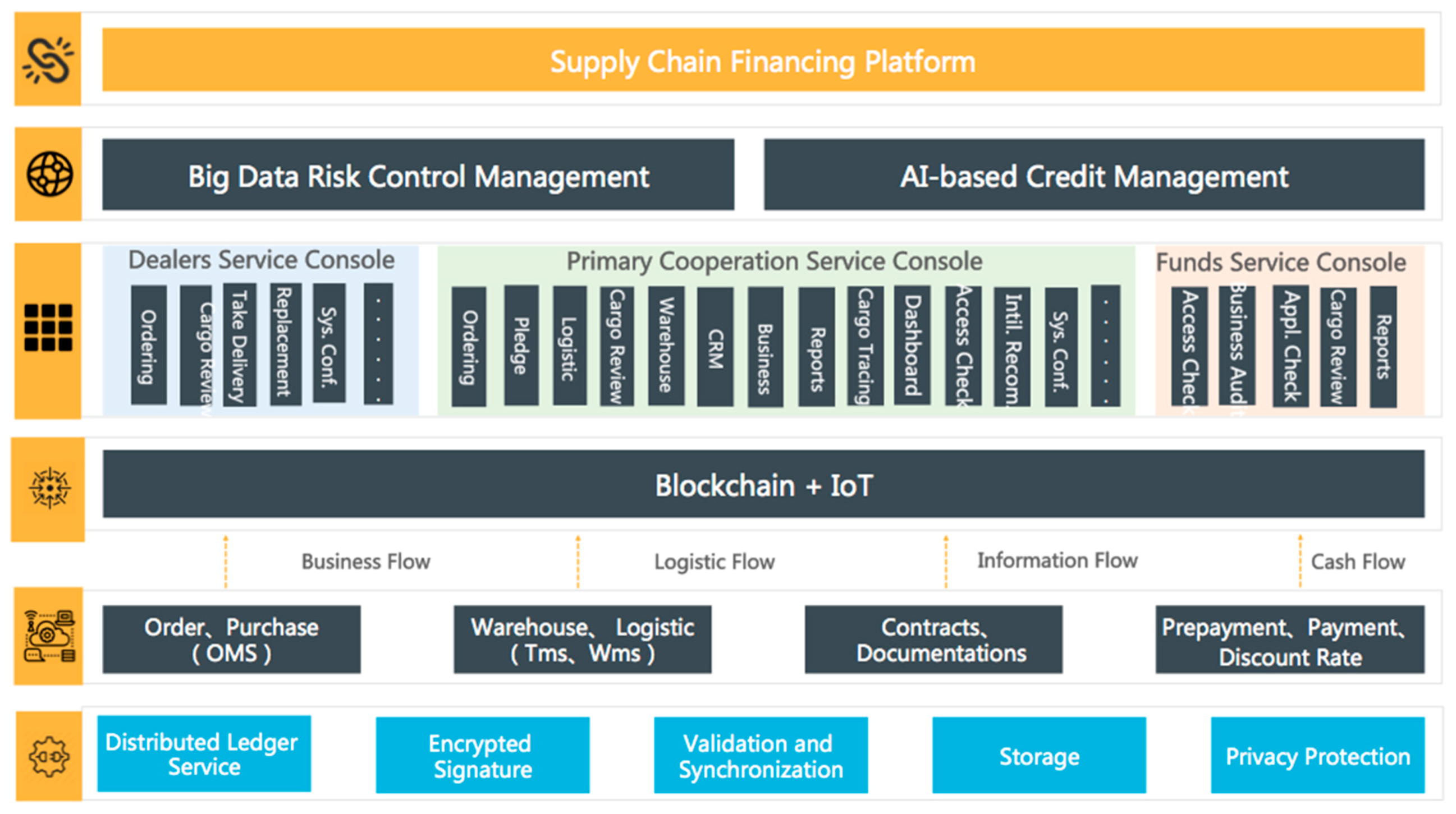

3. Proposed Solution

Participants

4. Implementation

4.1. Functionalities and Workflow

4.2. Transaction Tractability

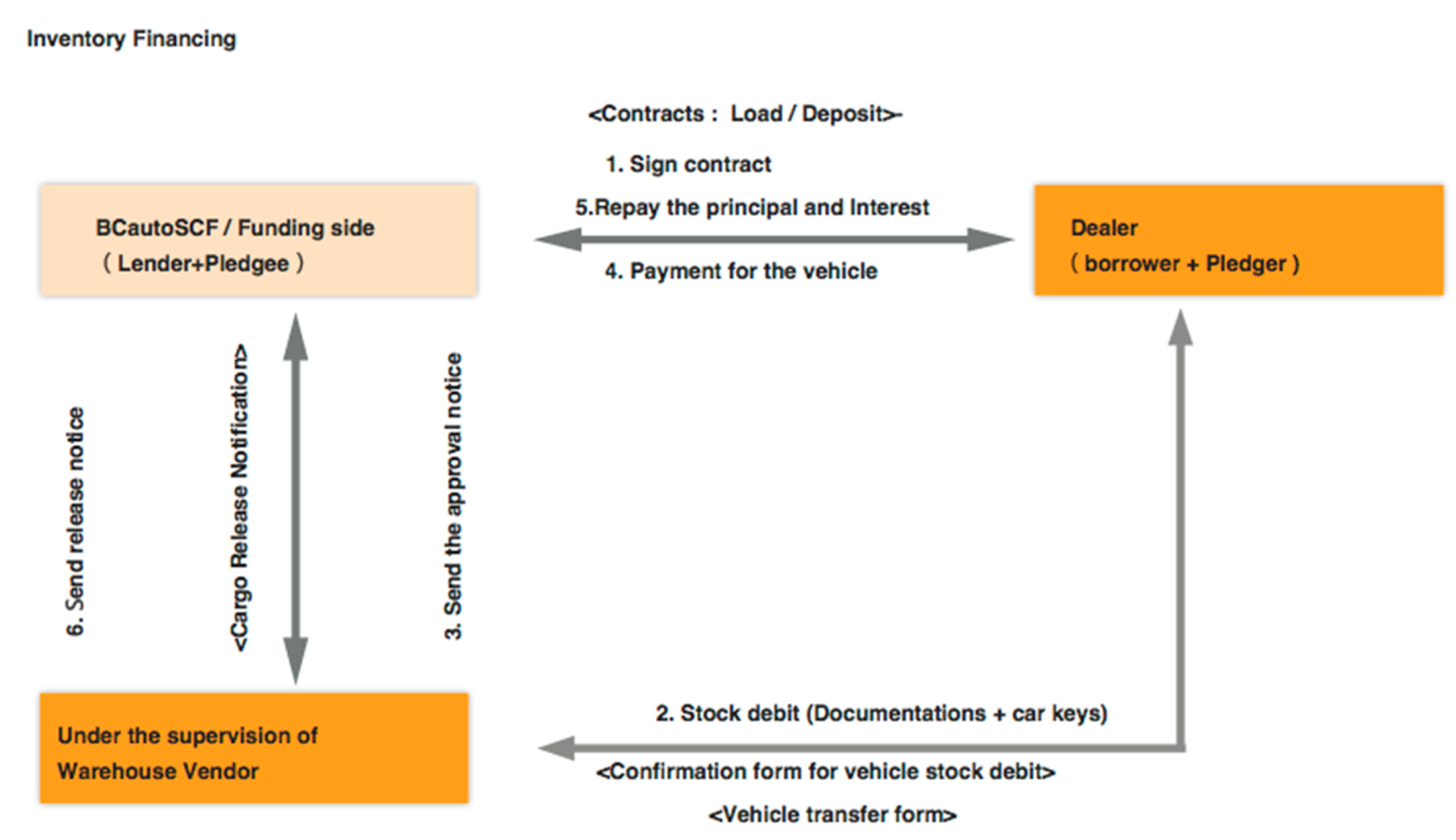

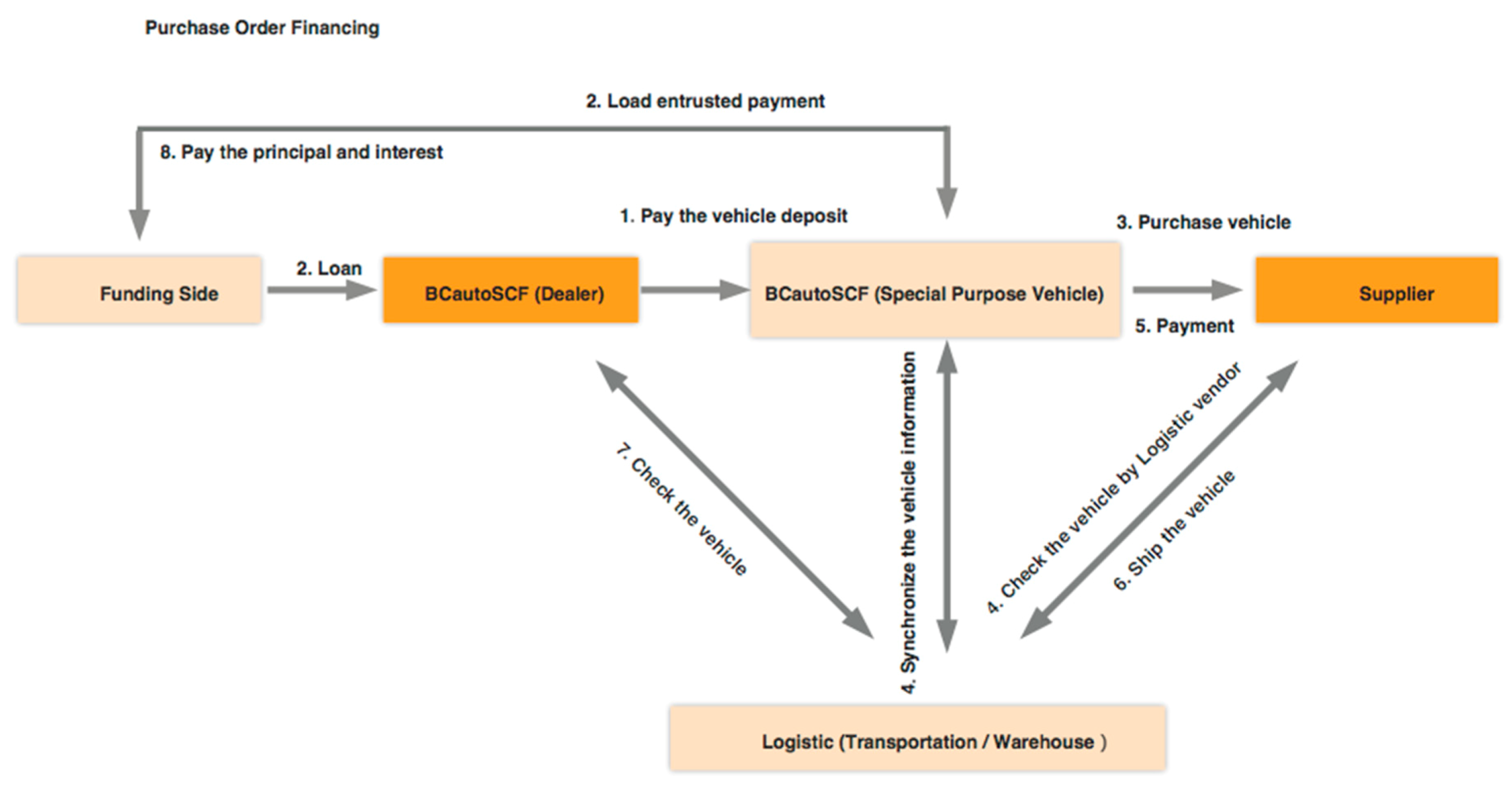

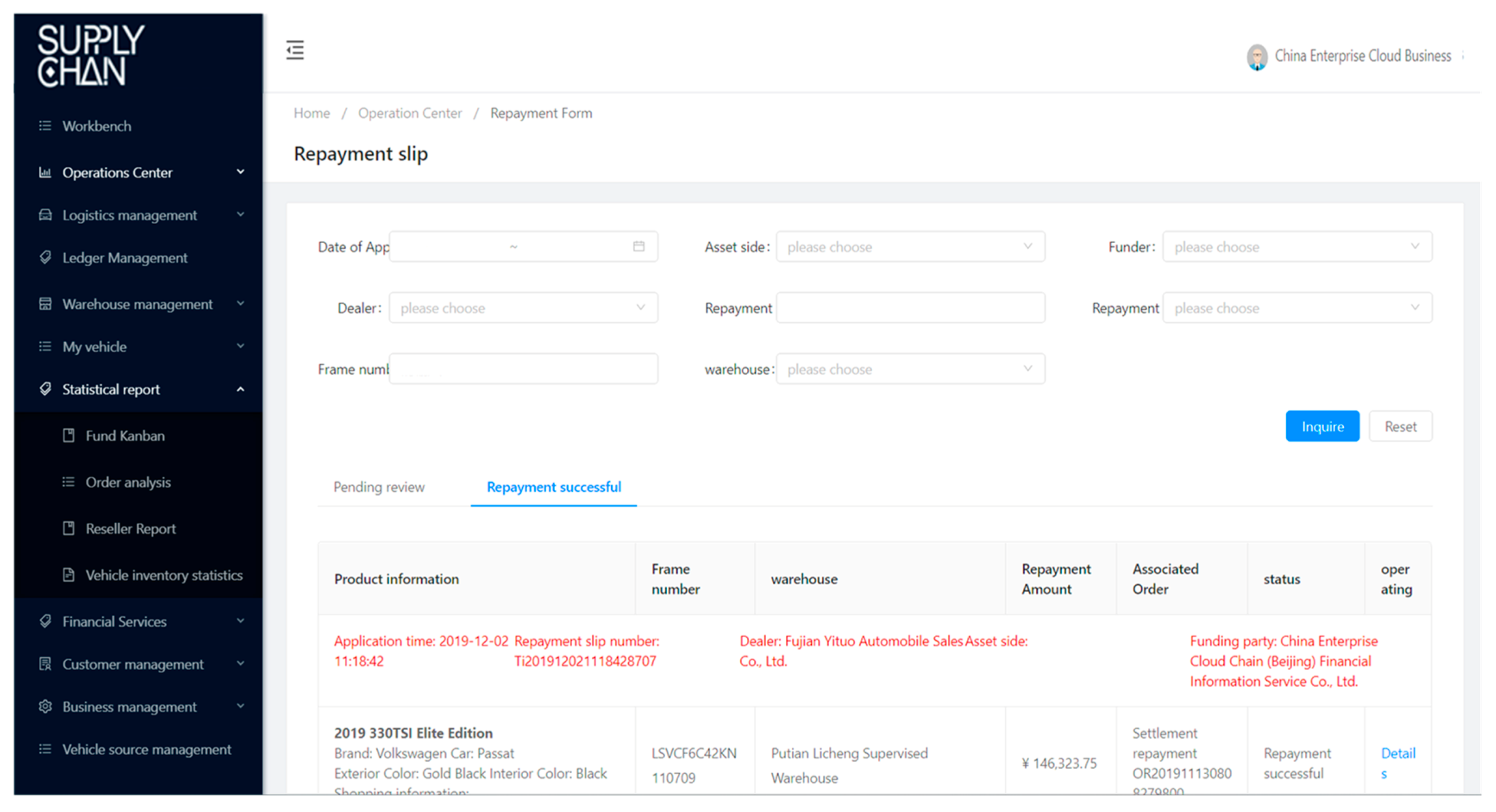

4.3. Financing Modes

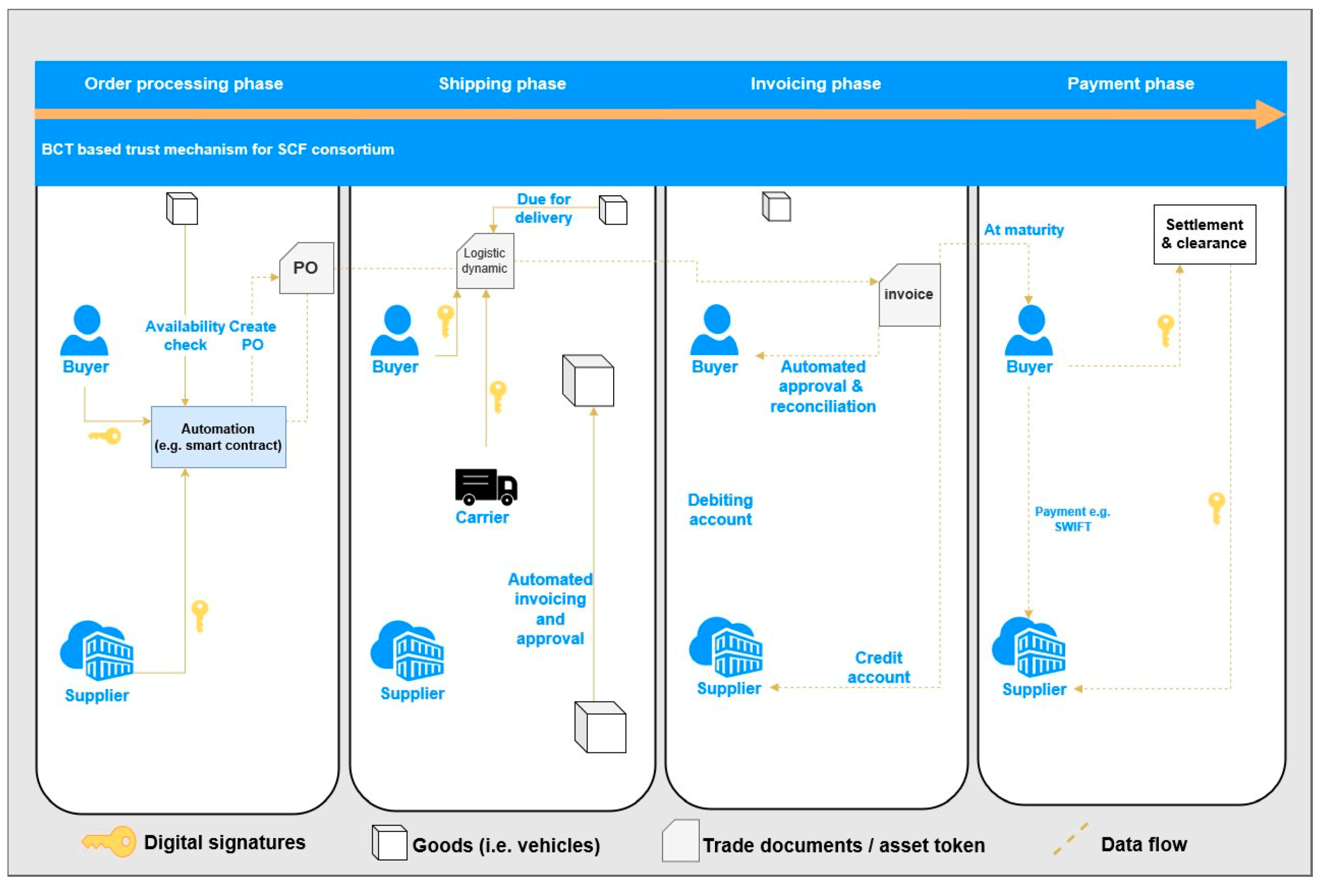

4.4. Automated Transaction

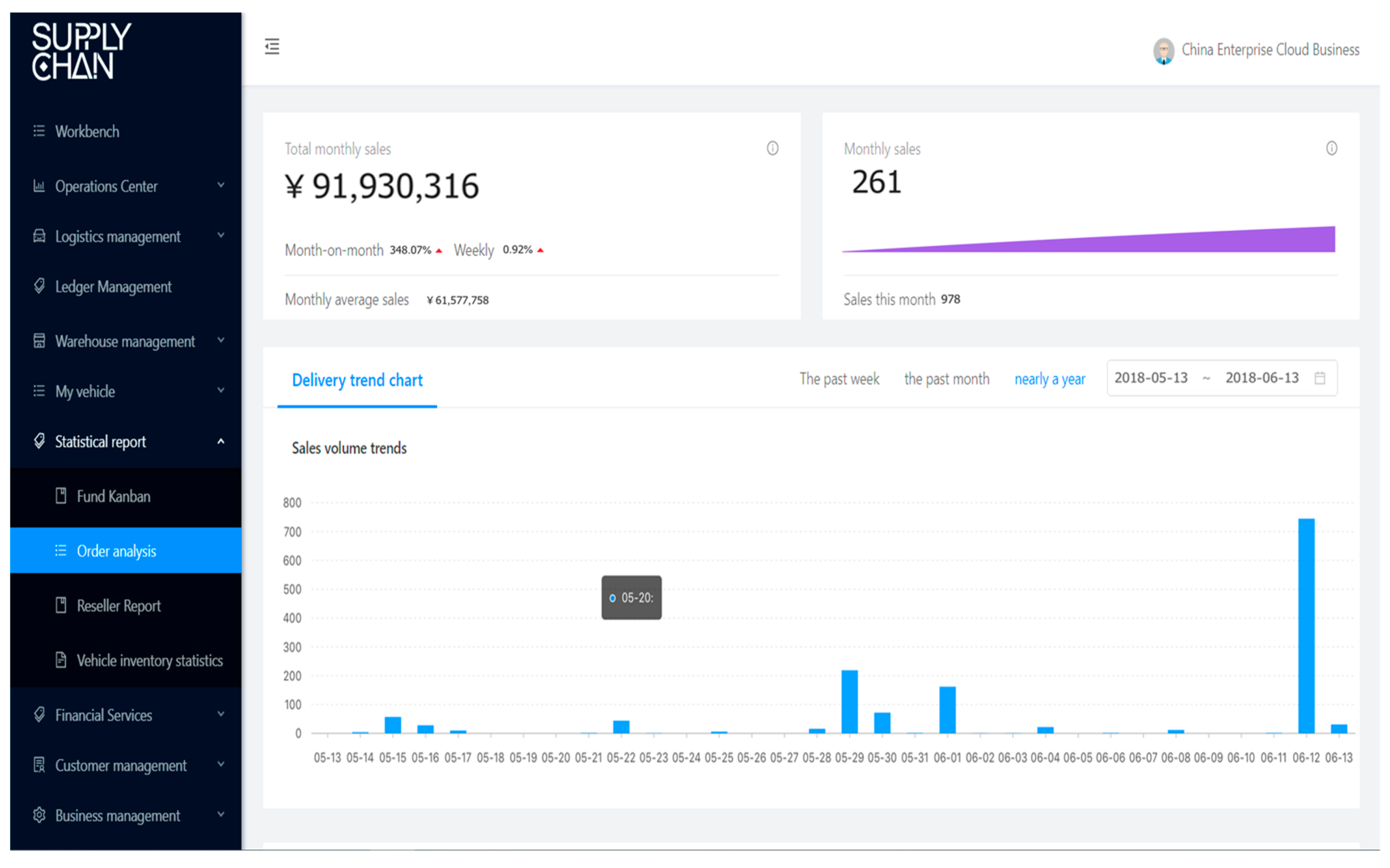

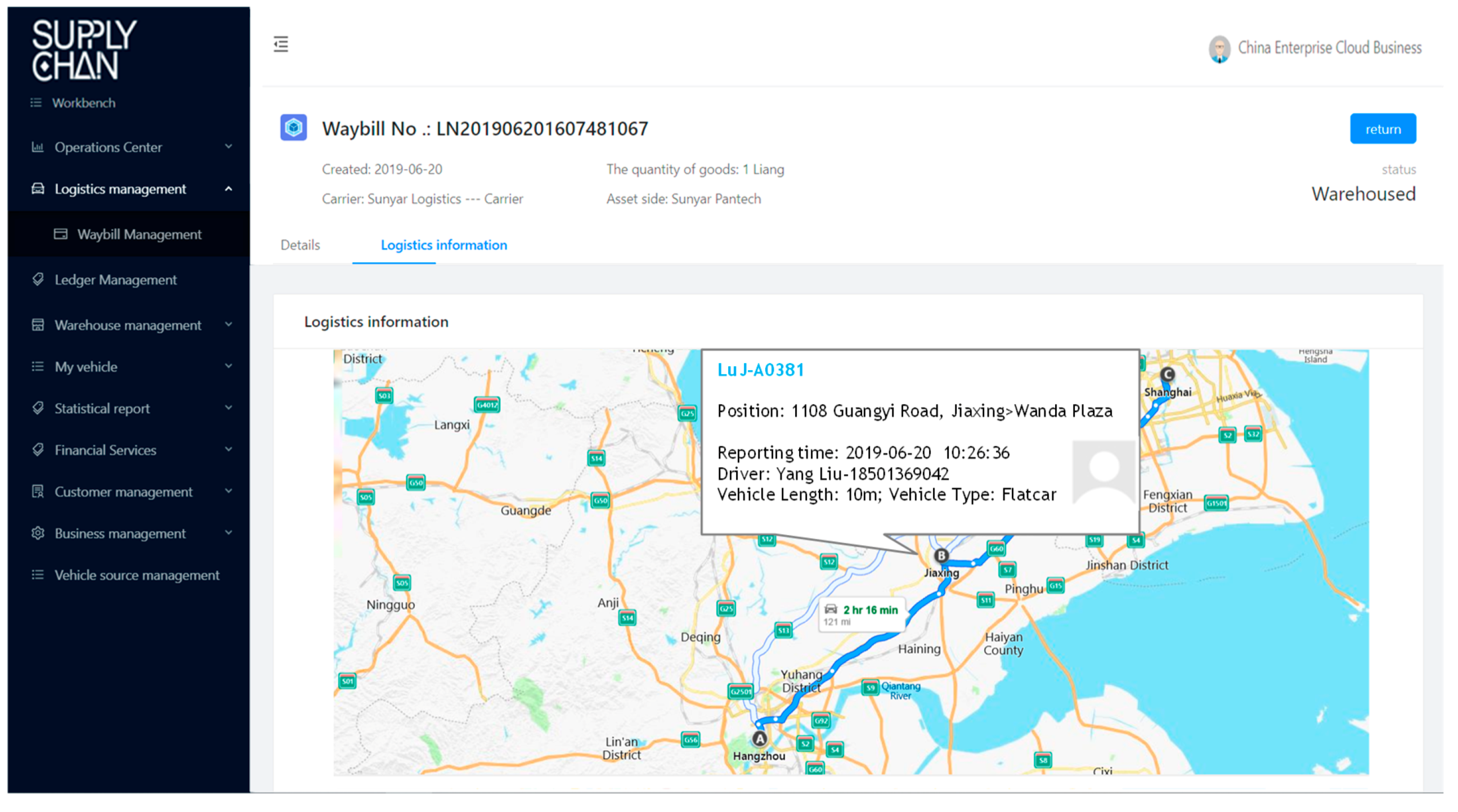

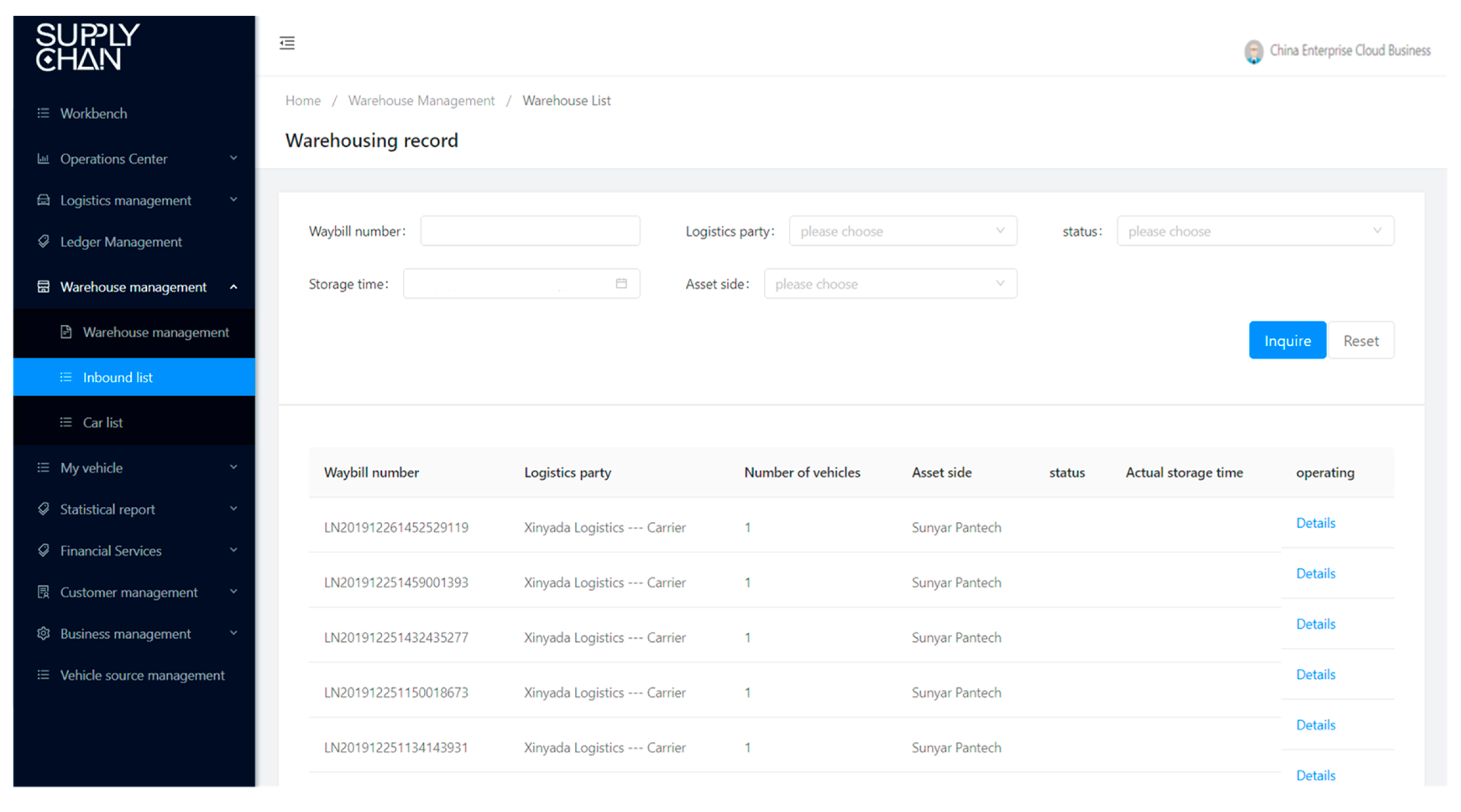

4.5. Functional Snapshots

4.6. Data Schema

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Jüttner, U.; Maklan, S. Supply chain resilience in the global financial crisis: An empirical study. Supply Chain Manag. 2013, 16, 246–259. [Google Scholar] [CrossRef]

- Babich, V.; Hilary, G. Distributed Ledgers and Operations: What Operations Management Researchers Should Know about Blockchain Technology. Manuf. Serv. Oper. Manag. 2019. [Google Scholar] [CrossRef]

- Mainelli, M.M.; Alistair, K.L. The Impact and Potential of Blockchain on the Securities Transaction Lifecycle. Available online: https://ssrn.com/abstract=2777404 (accessed on 1 October 2019).

- Kouvelis, P.; Zhao, W. Supply Chain Finance. In The Handbook of Integrated Risk Management in Global Supply Chains; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar] [CrossRef]

- Gomm, M.L. Supply chain finance: Applying finance theory to supply chain management to enhance finance in supply chains. Int. J. Logist. Res. Appl. 2010, 13, 133–142. [Google Scholar] [CrossRef]

- Yli-Huumo, J.; Ko, D.; Choi, S.; Park, S.; Smolander, K. Where is current research on blockchain technology?—A systematic review. PLoS ONE 2016, 11, e0163477. [Google Scholar] [CrossRef] [PubMed]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2009. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 1 October 2019).

- Schollmeier, R. A Definition of Peer-to-Peer Networking for the Classification of Peer-to-Peer Architectures and Applications. In Proceedings of the First International Conference on Peer-to-Peer Computing, Linkoping, Sweden, 7–29 August 2001. [Google Scholar]

- Montecchi, M.; Plangger, K.; Etter, M. It’s real, trust me! Establishing supply chain provenance using blockchain. Bus. Horiz. 2019, 62, 283–293. [Google Scholar] [CrossRef]

- Christidis, K.; Devetsikiotis, M. Blockchains and smart contracts for the Internet of things. IEEE Access 2016, 4, 2292–2303. [Google Scholar] [CrossRef]

- Hofmann, E.; Strewe, U.M.; Bosia, N. Supply chain finance and blockchain technology. O’Leary, D.E. ConFigureuring blockchain architectures for transaction information in blockchain consortiums: The case of accounting and supply chain systems. Intell. Syst. Account. Financ. Manag. 2017, 24, 138–147. [Google Scholar]

- Wang, Y.; Singgih, M.; Wang, J.; Rit, M. Making sense of blockchain technology: How will it transform supply chains? Int. J. Prod. Econ. 2019, 211, 221–236. [Google Scholar] [CrossRef]

- Choi, T.M.; Wen, X.; Sun, S.T.; Chung, S.H. The mean-variance approach for global supply chain risk analysis with air logistics in the blockchain technology era. Trans. Res. Part E 2019, 127, 178–191. [Google Scholar] [CrossRef]

- Pournader, M.; Shi, Y.; Seuring, S.; Koh, S.C. Blockchain applications in supply chains, transport and logistics: A systematic review of the literature. Int. J. Prod. Res. 2019, 1–19. [Google Scholar] [CrossRef]

- Flood, N.; Goodenough, O. Contracts as Automaton: The Computational Representation of Financial Agreement. Available online: https://financialresearch.gov/working-papers/files/OFRwp-2015-04_Contract-as-Automaton-The-Computational-Representation-of-Financial-Agreements.pdf (accessed on 1 October 2019).

- Yang, F.; Zhou, W.; Wu, Q.; Long, R.; Xiong, N.N.; Zhou, M. Delegated Proof of Stake with Downgrade: A Secure and Efficient Blockchain Consensus Algorithm with Downgrade Mechanism. IEEE Access 2019, 7, 118541–118555. [Google Scholar] [CrossRef]

- Chen, L.; Xu, L.; Shah, N.; Gao, Z.; Lu, Y.; Shi, W. On Security Analysis of Proof-of-Elapsed-Time (PoET). In Proceedings of the International Symposium on Stabilization Safety and Security of Distributed Systems, Boston, MA, USA, 5–8 November 2017. [Google Scholar]

- Szabo, N. Smart Contracts. 1994. Available online: http://szabo.best.vwh.net/smart.contracts.html (accessed on 16 August 2019).

- Buterin, V. A Next Generation Smart Contract and Decentralized Application Platform. 2013. Available online: https://ethereumbuilders.gitbooks.io/guide/content/en/whitepaper.html (accessed on 16 August 2019).

- Babich, V.; Hilary, G. Blockchain and other Distributed Ledger Technologies in Operations. Found. Trends® Technol. Inf. Oper. Manag. 2019, 12, 152–172. [Google Scholar] [CrossRef]

- Choi, T.; He, Y. Peer-to-peer collaborative consumption for fashion products in the sharing economy: Platform operations. Trans. Res. Part E 2019, 126, 49–65. [Google Scholar] [CrossRef]

- Yang, C. Maritime shipping digitalization: Blockchain-based technology applications, future improvements, and intention to use. Trans. Res. Part E 2019, 131, 108–117. [Google Scholar] [CrossRef]

- Fan, X. Scalable Practical Byzantine Fault Tolerance with Short-Lived Signature Schemes. In Proceedings of the 28th Annual International Conference on Computer Science and Software Engineering, Markham, ON, Canada, 29–31 October 2018. [Google Scholar]

- Marak, Z.; Pillai, D. Factors, Outcome, and the Solutions of Supply Chain Finance: Review and the Future Directions. J. Risk Financ. Manag. 2019, 12, 3. [Google Scholar] [CrossRef]

- Dolgui, A.; Ivanov, D.; Potryasaev, S.A.; Sokolov, B.; Ivanova, M.; Werner, F. Blockchain-oriented dynamic modelling of smart contract design and execution in the supply chain. Int. J. Prod. Res. 2019, 1–16. [Google Scholar] [CrossRef]

- Choi, T.; Luo, S. Data quality challenges for sustainable fashion supply chain operations in emerging markets: Roles of blockchain, government sponsors and environment taxes. Trans. Res. Part E 2019, 131, 139–152. [Google Scholar] [CrossRef]

- Wang, F.; Yang, X.; Zhuo, X.; Xiong, M. Joint logistics and financial services by a 3PL firm: Effects of risk preference and demand volatility. Trans. Res. Part E 2019, 130, 312–328. [Google Scholar] [CrossRef]

- Choi, T.; Feng, L.; Li, R. Information disclosure structure in supply chains with rental service platforms in the blockchain technology era. Int. J. Prod. Econ. 2019. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | Elements | Description |

|---|---|---|

| Funding flow | Source | Where the funding originates from |

| Amount | The credit amount approved in this case | |

| Mode | The financing mode used in this case | |

| Receiver | The cooperation, which receives this funding | |

| Collateral | The collateral used in this case. | |

| Loan Interest | The interest rate used in this case. | |

| Logistic | Carrier ID | The actual carrier undertakes the shipment |

| IoT Garments | IoT garments (e.g., GPS, RFID, etc.) in the shipment | |

| Shipment | Records the routines, tools, traces, fee, etc. | |

| Vehicle ID | The identifier of the vehicle in an order, which is always associated with IoT garments. | |

| Shipper | The owner of the cargo in a shipment. | |

| Document flow | Contract | The contracts associated with this information flow |

| Initiator | The sender, who initiates the conversation. | |

| Receiver | The receiver, who will receive the information | |

| Type | The type of the information flow | |

| Participants | The interested parties get involved in this information flow | |

| Descriptions | The full content of this information flow | |

| Business flow | Status | The current status of this business case |

| Collateral | The collateral used in this case | |

| Dealer | The dealer, which submits this order | |

| Order | The specification of the order | |

| Financing | The financing information used in this order |

| Action | Parameters | Parameter Definitions |

|---|---|---|

| Registration | Identity | User information including user id, username, password, icon, and other profiles. |

| Asset Address List | A list of user’s digital asset in blockchain | |

| Asset Type | Identifying the type of user’s digital asset | |

| User Token | User’s token used in transaction | |

| User Address | User’s digital address in blockchain | |

| Credit Facility | Identity | User information including user id, username, password, icon, etc. |

| Receipt Address | The address of credit receipt in blockchain | |

| Credit Amount | The credit amount approved to the receipt | |

| CF Record | The record of a credit-facility transaction. | |

| Credit Inquiry | Identity | The identity information of credit receipt |

| CI Record | The transaction details of credit inquiry in a record | |

| User Address | The address of the credit receipt in blockchain | |

| CF record | The record of a credit-facility transaction. |

| Platform(s) | Type | Business Models and Policies | Income |

|---|---|---|---|

| BCautoSCF | Financing Platform (2B) |

| Service fee from users |

| www.chexiang.com | Primary Dealer (2C) |

| Profit from Auto aftermarket |

| www.yiautos.com www.chezhency.com | Secondary Dealer (2C) |

|

|

| www.niuniuqiche.com www.chehang168.com | SCF (2B) |

|

|

| www.tangeche.com www.maodou.com | Consumer Finance (2C) |

|

|

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, J.; Cai, T.; He, W.; Chen, L.; Zhao, G.; Zou, W.; Guo, L. A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry. Entropy 2020, 22, 95. https://doi.org/10.3390/e22010095

Chen J, Cai T, He W, Chen L, Zhao G, Zou W, Guo L. A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry. Entropy. 2020; 22(1):95. https://doi.org/10.3390/e22010095

Chicago/Turabian StyleChen, Jingjing, Tiefeng Cai, Wenxiu He, Lei Chen, Gang Zhao, Weiwen Zou, and Lingling Guo. 2020. "A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry" Entropy 22, no. 1: 95. https://doi.org/10.3390/e22010095

APA StyleChen, J., Cai, T., He, W., Chen, L., Zhao, G., Zou, W., & Guo, L. (2020). A Blockchain-Driven Supply Chain Finance Application for Auto Retail Industry. Entropy, 22(1), 95. https://doi.org/10.3390/e22010095