Non-Linear Diffusion and Power Law Properties of Heterogeneous Systems: Application to Financial Time Series

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Microscopic Dynamics

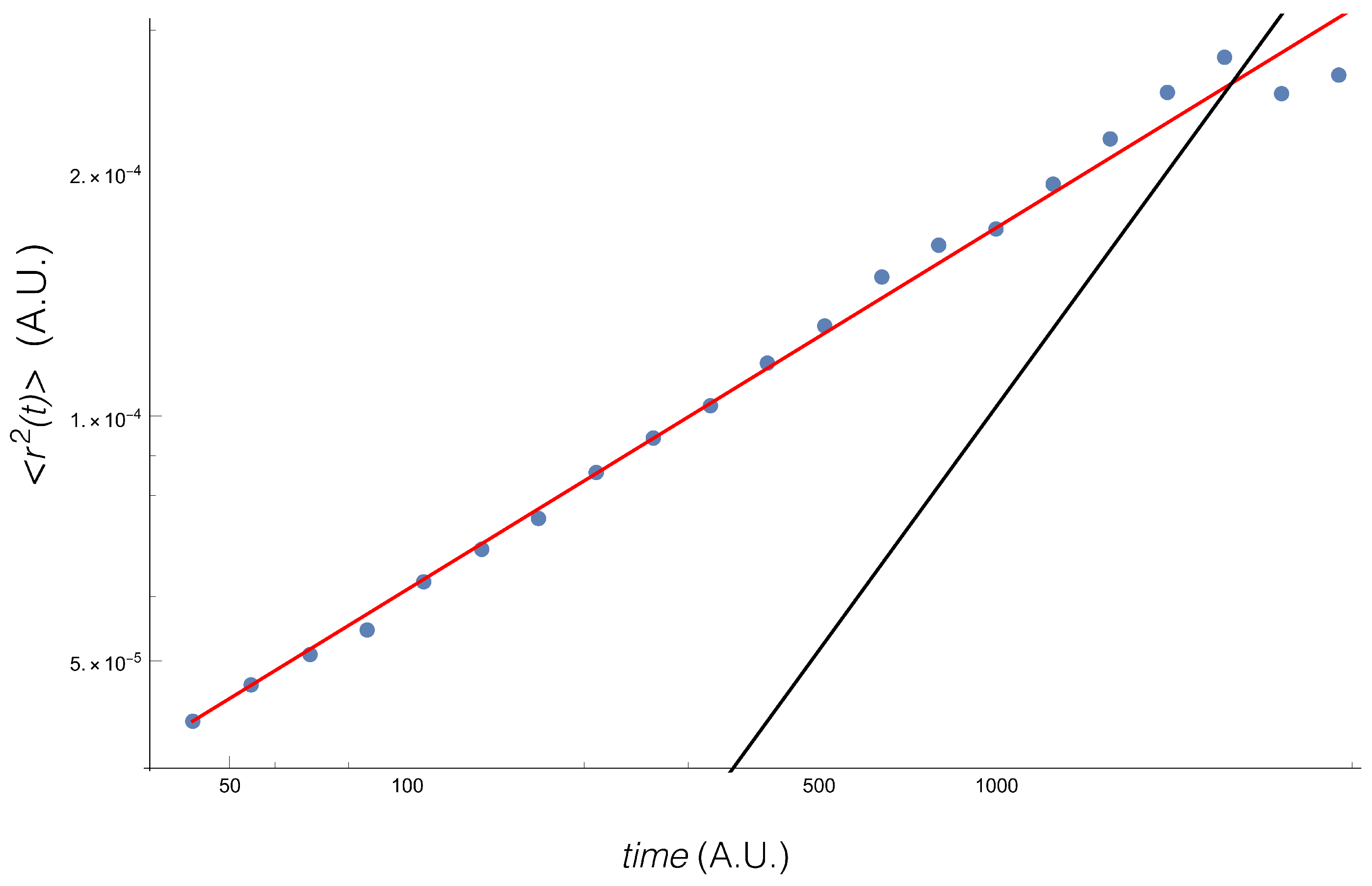

3. Power Law Behavior in the Movement of Ensemble of Particles

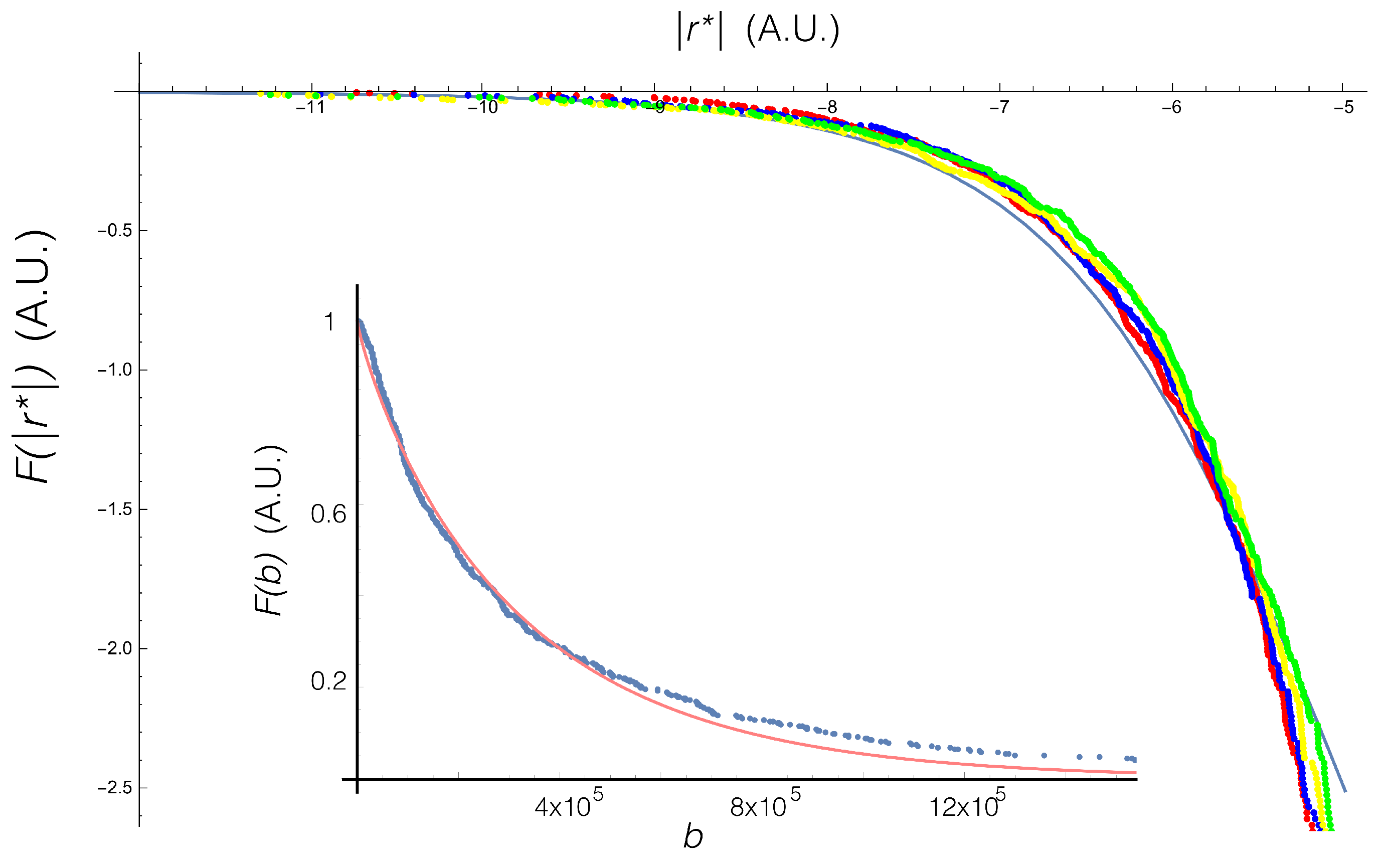

4. A Marginalization of Weakly Coupled Systems

5. Application to the Financial Time Series

6. Final Remarks

Funding

Acknowledgments

Conflicts of Interest

References

- Horbach, J.; Siboni, N.H.; Schnyder, S.K. Anomalous transport in heterogeneous media. Eur. Phys. J. Spec. Top. 2017, 226, 3113–3128. [Google Scholar] [CrossRef]

- La Porta, A.; Voth, G.A.; Crawford, A.M.; Alexander, J.; Bodenschatz, E. Fluid particle accelerations in fully developed turbulence. Nature 2001, 409, 1017–1019. [Google Scholar] [CrossRef] [PubMed]

- Bouchaud, J.P.; Potters, M. Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- Zhao, Z.D.; Yang, Z.; Zhang, Z.; Zhou, T.; Huang, Z.G.; Lai, Y.C. Emergence of scaling in human-interest dynamics. Sci. Rep. 2013, 3, 3472. [Google Scholar] [CrossRef] [PubMed]

- Brockmann, D.; Hufnagel, L.; Geisel, T. The scaling laws of human travel. Nature 2006, 439, 462–465. [Google Scholar] [CrossRef] [PubMed]

- Van Kampen, N.G. Stochastic Processes in Physics and Chemistry; Elsevier: New York, NY, USA, 1992; Volume 1. [Google Scholar]

- Borland, L. Microscopic dynamics of the nonlinear Fokker-Planck equation: A phenomenological model. Phys. Rev. E 1998, 57, 6634. [Google Scholar] [CrossRef]

- Ribeiro, M.S.; Casas, G.A.; Nobre, F.D. Multi–diffusive nonlinear Fokker–Planck equation. J. Phys. A Math. Theor. 2017, 50, 065001. [Google Scholar] [CrossRef]

- Hanel, R.; Thurner, S. When do generalized entropies apply? How phase space volume determines entropy. Europhys. Lett. 2011, 96, 50003. [Google Scholar] [CrossRef]

- Gell-Mann, M.; Tsallis, C. (Eds.) Nonextensive Entropy: Interdisciplinary Applications; Oxford University Press on Demand: Oxford, UK, 2004. [Google Scholar]

- Zhang, Y.; Dong, Z.; Wang, S.; Ji, G.; Yang, J. Preclinical diagnosis of magnetic resonance (MR) brain images via discrete wavelet packet transform with Tsallis entropy and generalized eigenvalue proximal support vector machine (GEPSVM). Entropy 2015, 17, 1795–1813. [Google Scholar] [CrossRef]

- Ibrahim, R.W.; Jalab, H.A. Existence of Ulam stability for iterative fractional differential equations based on fractional entropy. Entropy 2015, 17, 3172–3181. [Google Scholar] [CrossRef]

- Fuentes, M.A.; Cáceres, M.O. Computing the non-linear anomalous diffusion equation from first principles. Phys. Lett. A 2008, 372, 1236–1239. [Google Scholar] [CrossRef]

- Bachelier, L. Théorie de la Spéculation; Gauthier-Villars: Paris, France, 1900. (In French) [Google Scholar]

- Osborne, M.F. Brownian motion in the stock market. Oper. Res. 1959, 7, 145–173. [Google Scholar] [CrossRef]

- Mandelbrot, B.B. The variation of certain speculative prices. In Fractals and Scaling in Finance; Springer: New York, NY, USA, 1997; pp. 371–418. [Google Scholar]

- Fama, E.F. The behavior of stock-market prices. J. Bus. 1965, 38, 34–105. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Scaling behaviour in the dynamics of an economic index. Nature 1995, 376, 46–49. [Google Scholar] [CrossRef]

- Zhao, P.; Zhou, B.; Wang, J. Non-Gaussian Closed Form Solutions for Geometric Average Asian Options in the Framework of Non-Extensive Statistical Mechanics. Entropy 2018, 20, 71. [Google Scholar] [CrossRef]

- Gençay, R.; Gradojevic, N. The tale of two financial crises: An entropic perspective. Entropy 2017, 19, 244. [Google Scholar] [CrossRef]

- Tateishi, A.A.; Lenzi, E.K.; da Silva, L.R.; Ribeiro, H.V.; Picoli, S., Jr.; Mendes, R.S. Different diffusive regimes, generalized Langevin and diffusion equations. Phys. Rev. E 2012, 85, 011147. [Google Scholar] [CrossRef] [PubMed]

- Tirnakli, U.; Bykkili, F.; Demirhan, D. Some bounds upon the nonextensivity parameter using the approximate generalized distribution functions. Phys. Lett. A 1998, 245, 62–66. [Google Scholar] [CrossRef]

- Kusnezov, D.; Bulgac, A.; Do Dang, G. Quantum levy processes and fractional kinetics. Phys. Rev. Lett. 1999, 82, 1136. [Google Scholar] [CrossRef]

- Lutz, E. Anomalous diffusion through coupling to a fractal environment: Microscopic derivation of the “whip-back” effect. Europhys. Lett. 2001, 54, 293. [Google Scholar] [CrossRef]

- Leggett, A.J.; Chakravarty, S.D.A.F.M.G.A.; Dorsey, A.T.; Fisher, M.P.; Garg, A.; Zwerger, W. Dynamics of the dissipative two-state system. Rev. Mod. Phys. 1987, 59, 1. [Google Scholar] [CrossRef]

- Saichev, A.I.; Zaslavsky, G.M. Fractional kinetic equations: Solutions and applications. Chaos Interdiscip. J. Nonlinear Sci. 1997, 7, 753–764. [Google Scholar] [CrossRef] [PubMed]

- Samko, S.G.; Kilbas, A.A.; Marichev, O.I. Fractional Integrals and Derivatives: Theory and Applications; Gordon and Breach: Yverdon, Switzerland, 1993; p. 44. [Google Scholar]

- Slezak, J.; Metzler, R.; Magdziarz, M. Superstatistical generalised Langevin equation. New J. Phys. 2018, 20, 1–25. [Google Scholar] [CrossRef]

- Hilfer, R. Applications of Fractional Calculus in Physics; World Scientific Publishing: Singapore, 2000. [Google Scholar]

- Erdelyi, A. Higher Transcendental Functions; McGraw-Hill: New York, NY, USA, 1955; Volume 3. [Google Scholar]

- Gardiner, C.W. Handbook of Stochastic Methods; Springer: Berlin, Germany, 2005. [Google Scholar]

- Wang, K.G. Long-time-correlation effects and biased anomalous diffusion. Phys. Rev. A 1992, 45, 833. [Google Scholar] [CrossRef] [PubMed]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional Brownian motions, fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Oldham, K.; Spanier, J. The Fractional Calculus Theory and Applications of Differentiation and Integration to Arbitrary Order; Elsevier: New York, NY, USA, 1974; Volume 111. [Google Scholar]

- Miller, K.S.; Ross, B. An Introduction to the Fractional Calculus and Fractional Differential Equations; John Wiley & Sons: Hoboken, NJ, USA, 1993. [Google Scholar]

- Atangana, A.; Gómez-Aguilar, J.F. Decolonisation of fractional calculus rules: Breaking commutativity and associativity to capture more natural phenomena. Eur. Phys. J. Plus 2018, 133, 1–22. [Google Scholar] [CrossRef]

- Atangana, A. Non validity of index law in fractional calculus: A fractional differential operator with Markovian and non-Markovian properties. Phys. A Stat. Mech. Appl. 2018, 505, 688–706. [Google Scholar] [CrossRef]

- Beck, C. Lagrangian acceleration statistics in turbulent flows. Europhys. Lett. 2003, 64, 151. [Google Scholar] [CrossRef]

- Gerig, A.; Vicente, J.; Fuentes, M.A. Model for non-Gaussian intraday stock returns. Phys. Rev. E 2009, 80, 065102. [Google Scholar] [CrossRef] [PubMed]

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fuentes, M.A. Non-Linear Diffusion and Power Law Properties of Heterogeneous Systems: Application to Financial Time Series. Entropy 2018, 20, 649. https://doi.org/10.3390/e20090649

Fuentes MA. Non-Linear Diffusion and Power Law Properties of Heterogeneous Systems: Application to Financial Time Series. Entropy. 2018; 20(9):649. https://doi.org/10.3390/e20090649

Chicago/Turabian StyleFuentes, Miguel A. 2018. "Non-Linear Diffusion and Power Law Properties of Heterogeneous Systems: Application to Financial Time Series" Entropy 20, no. 9: 649. https://doi.org/10.3390/e20090649

APA StyleFuentes, M. A. (2018). Non-Linear Diffusion and Power Law Properties of Heterogeneous Systems: Application to Financial Time Series. Entropy, 20(9), 649. https://doi.org/10.3390/e20090649