1. Introduction

In this work, we study with statistical methods a problem concerning the elastic scattering of two particles in the relativistic regime and we discuss the similarities between this physical process and the economic interactions occurring in the so-called wealth exchange models [

1,

2]. A unifying element in this analysis is the generalized

-distribution [

3,

4,

5,

6], which has proven to be helpful for the description of both kinds of phenomena. We start from the familiar assumption of statistical mechanics according to which the macroscopic distributions (of energy or income) are determined by the microscopic interactions (between molecules or, respectively, individuals). Such interactions can be of many different sorts, but we are mostly interested into properties which are independent from the details of the specific system; namely we are interested into the conditions under which a “fat” power-law tail can appear in the macroscopic distribution, instead of the thin exponential tail typical of the Boltzmann distribution.

In our computation we shall suppose that all the permitted final states of a binary collision (those compatible with conservation laws) have the same probability. For this reason we mention in the title the “statistics of binary exchange”, and not the dynamics of this exchange. “Statistics” is meant here in the same sense as in the term “Statistical Mechanics”. In fact, it is known from experimental data on relativistic gases and cosmic rays that the fat tails in their energy distributions have some universal features; it is also known that Pareto tails in income distributions have existed in various epochs and in countries with very different economic systems. (For some very recent data and related analysis see [

7].) This suggests that the formation mechanism of the tails is essentially kinematical. In [

3] G. Kaniadakis has shown that the deformation of the distribution function introduced by the parameter

emerges naturally within Einstein’s special relativity, so that one can see the

-deformation as a pure relativistic effect. To this end, one first proves that the

-deformed sum of the momenta of two particles is the additivity law for the relativistic momenta (the

-sum is used in a generalized entropy minimization procedure leading to the

-distribution). By considering, in the framework of special relativity, the

-statistics of an ensemble of identical particles, one therefore arrives at a distribution with a power-law tail without any assumption on dynamics, but using only kinematics.

From the physical point of view, what are the main differences between a “classical” collision and a strongly relativistic collision? The answer is not unique. The techniques of relativistic kinetic theory [

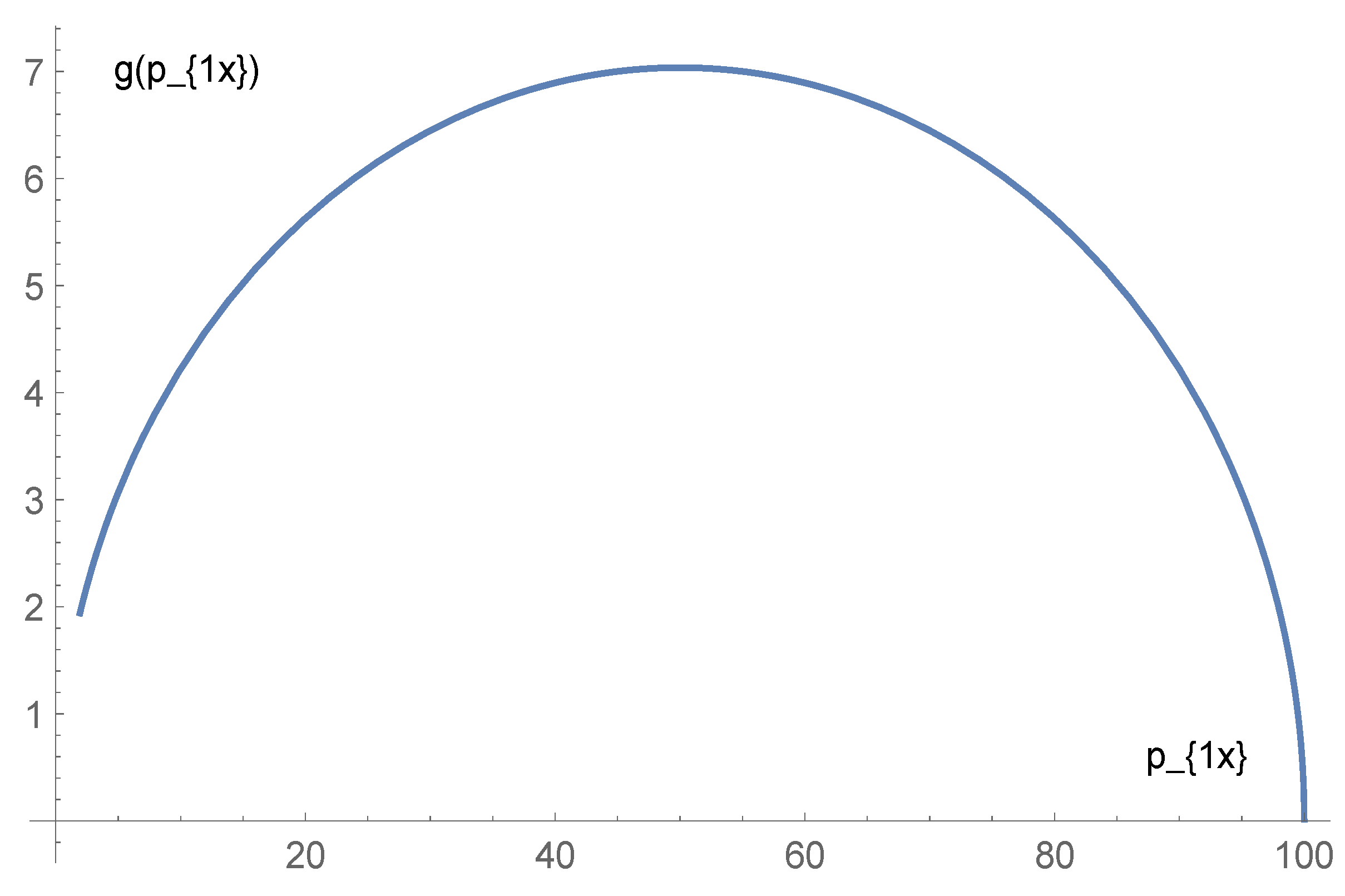

8] allow us to write the Boltzmann equation in relativistic form and to conduct a similar analysis as done in the classical theory. Nevertheless, the approach by Kaniadakis et al. shows that there is still room for a better understanding of the basic concepts. In our opinion, it is important to consider also quantities that are not Lorentz-invariant, and are therefore often disregarded in the traditional relativistic kinetic theory. We will focus our attention on the non-invariant fraction

R of energy which is transferred from one particle to the other during a binary collision between identical particles. If one looks at the collision in the center of mass system,

R is trivially zero, because the conservation laws of the total energy and momentum impose that the energy is equally distributed between the two particles before and after the scattering. What changes in the collision, as seen from the center of mass system, is only the direction of the momenta. Any other change is entirely due to the choice of a different reference system.

Nevertheless, for a gas contained in a finite volume there exists a privileged reference system, namely the system where the gas is, on average, at rest. If we look at a scattering process as the analogue of an economic interaction, the fraction

R of money exchanged by an individual is obviously an important quantity. We point out that in any realistic income distribution the majority of the individuals have low or middle income, therefore it is important to evaluate

R for an interaction between a poor individual (slow molecule) and a rich one (fast molecule). It has been suggested by some authors [

9] that Pareto tails are formed when the rich part of a population enacts an effective policy for preserving its wealth in the interactions. This attitude can also be described as a high “saving propensity”. In [

10] we have argued that something similar happens in relativistic collisions, but the technique employed did not allow us to carry the analogy very far. In this work we improve the technique for the calculation of the

R factor and we obtain further results. In

Section 2 we evaluate the probability distribution of energy transfer in an elastic collision. We solve numerically the conservation law for energy and compute the integral over final states parametrized as a one-parameter line in phase space. In

Section 3 we give the results of agent-based simulations based on money exchange rules which are the analogues of the energy balance in the collisions.

Section 4 comprises our conclusions. The Appendices contain some background material on relativistic energy and momentum (

Appendix A) and wealth exchange models in econophysics (

Appendix B) that can be helpful for an interdisciplinary audience.

The question raised at the beginning of the abstract of this paper is therefore answered in two steps. In the first step (

Section 2) we show that the probability of final states of a binary collision is different in the case of a low-energy and high-energy collision. In the second step (

Section 3) we pass “from micro to macro” by simulating a large number of collisions occurring with this probability, and we look at what kind of equilibrium distribution they lead to in a large population of molecules.

3. Agent-Based Simulations and Saving Propensity

The analogies between the energy distribution in a gas and the income distribution in a society have been one of the main subjects of econophysics, since the pioneering works of the 1990s [

9]. In several works, agent-based simulations have been employed to investigate the relation between the rules of the microscopic interactions and the resulting equilibrium income distribution. A well established result is that a fixed saving propensity in the interactions gives rise to a distribution of the Gamma-kind, namely

, where

E is here the income and

T an effective temperature. This distribution does not have a flat tail. (

is the probability density distribution of energy or money, in the econophysics analogy. The probability that an individual chosen at random has income in the infinitesimal interval

is given by

. The “temperature”

T corresponds essentially, in the analogy, to the average wealth, whereby the Boltzmann constant is set by convention equal to 1.)

The saving propensity, usually denoted with

, is the fraction of its income that each individual “hedges” in the economic interactions, or in other words, individuals put at stake in the interactions a fraction

of their income. It is relatively straightforward to reproduce some of the mentioned result. For instance,

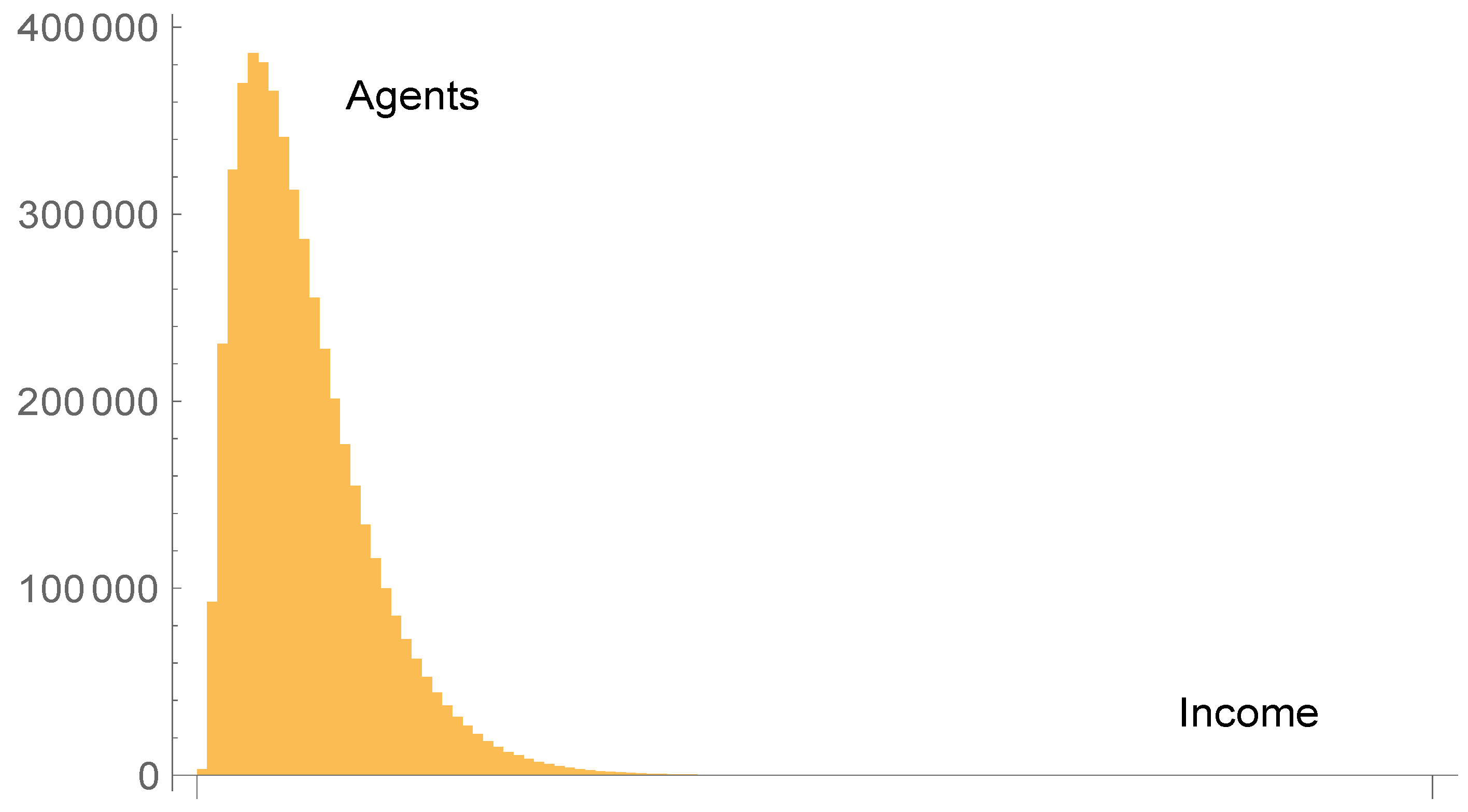

Figure 4 shows the income distribution we have obtained from a simulation with

agents exchanging energy/money according to the rule [

11]

(

i and

j label two agents randomly chosen at each step;

is a random variable in the interval

). The system has been evolved to equilibrium with a series of

binary exchanges, and the whole procedure averaged for 50 times in order to minimize the effect of fluctuations.

More in detail, we define, in a suitable programming language (

Mathematica in our case) a vector

with

components. The component

represents the wealth of the

i-th agent of our idealized society. At the beginning all agents have the same wealth, e.g.,

units for any

i in our simulation. Then the simulation algorithm choses at random two integer indices

i,

j between 1 and

. These are the agents who are currently interacting. Their wealths are changed according to Equation (15). The random choice of agents and the modification of their wealths is repeated for

times. This means that, on average, each agent has interacted with others for

times. (Thermalization times larger than

steps are found to give no changes in the final results.) A histogram of the wealth distribution is generated by rounding the wealth of each agent to the nearest integer and then using a counting function to define the frequency, for instance in

Mathematica in our case with the code

frequency = Table[Count[X,n],{n,0,120}], where

X is the rounded income vector and 120 is a safe maximum value for the income. The

frequency vector is the one whose components are shown in the histograms in

Figure 4 and

Figure 5. Next we average the frequency vector over many realizations, in order to reduce the fluctuations, we normalize it by dividing each component by the sum of all components, and we use a

FindFit function to fit it to the

-distribution (16). This function employs a least-squares method and returns the best fit values of the three parameters in the

-distribution. When the fit fails to show a power-law tail, it is because it returns negative values for

and

, which are not admissible for a

-distribution.

A fit of the resulting distribution with the

-distribution

fails, and this confirms that no Pareto tail is present. Similar results can be obtained with other values of

.

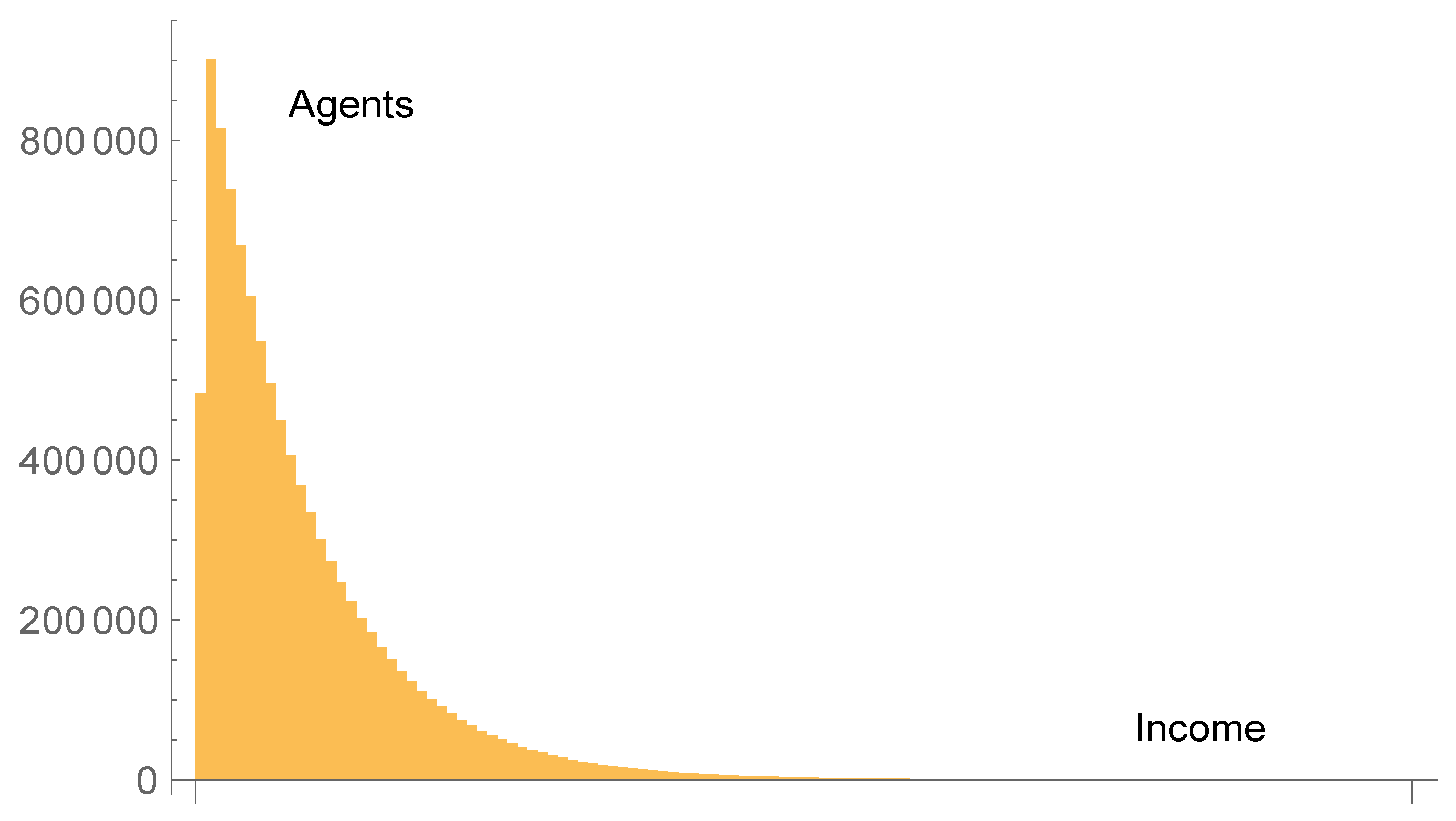

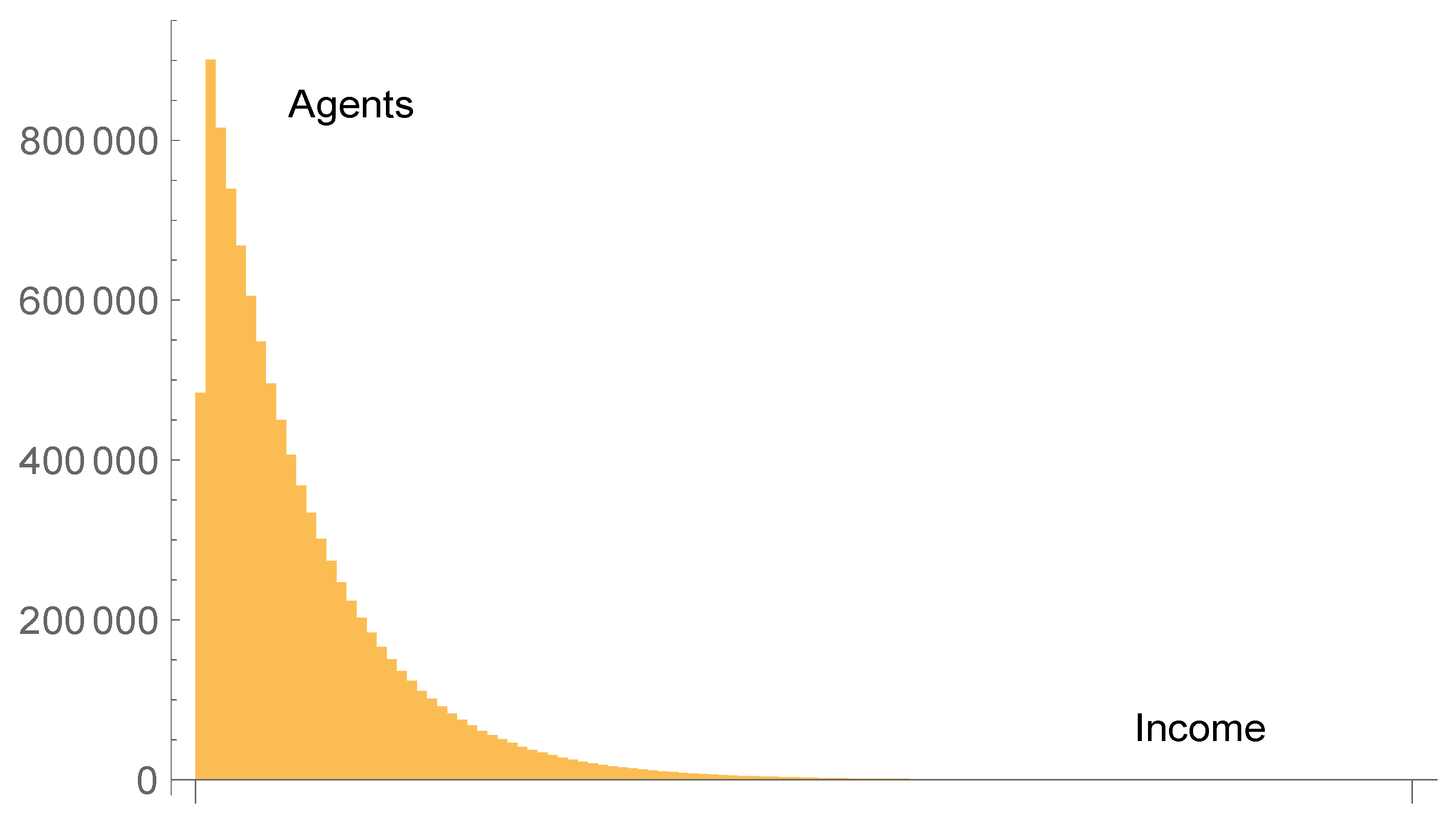

Now let us run a simulation with microscopic exchange rules corresponding to the extreme relativistic case of

Section 2.3. We set the energies of two particles after a collision as

This means that, as found in

Section 2.3, all energy exchange rates are equally probable, and as a consequence there is no fixed saving propensity. The result of a simulation with

agents,

thermalization steps and 100 averages is given in

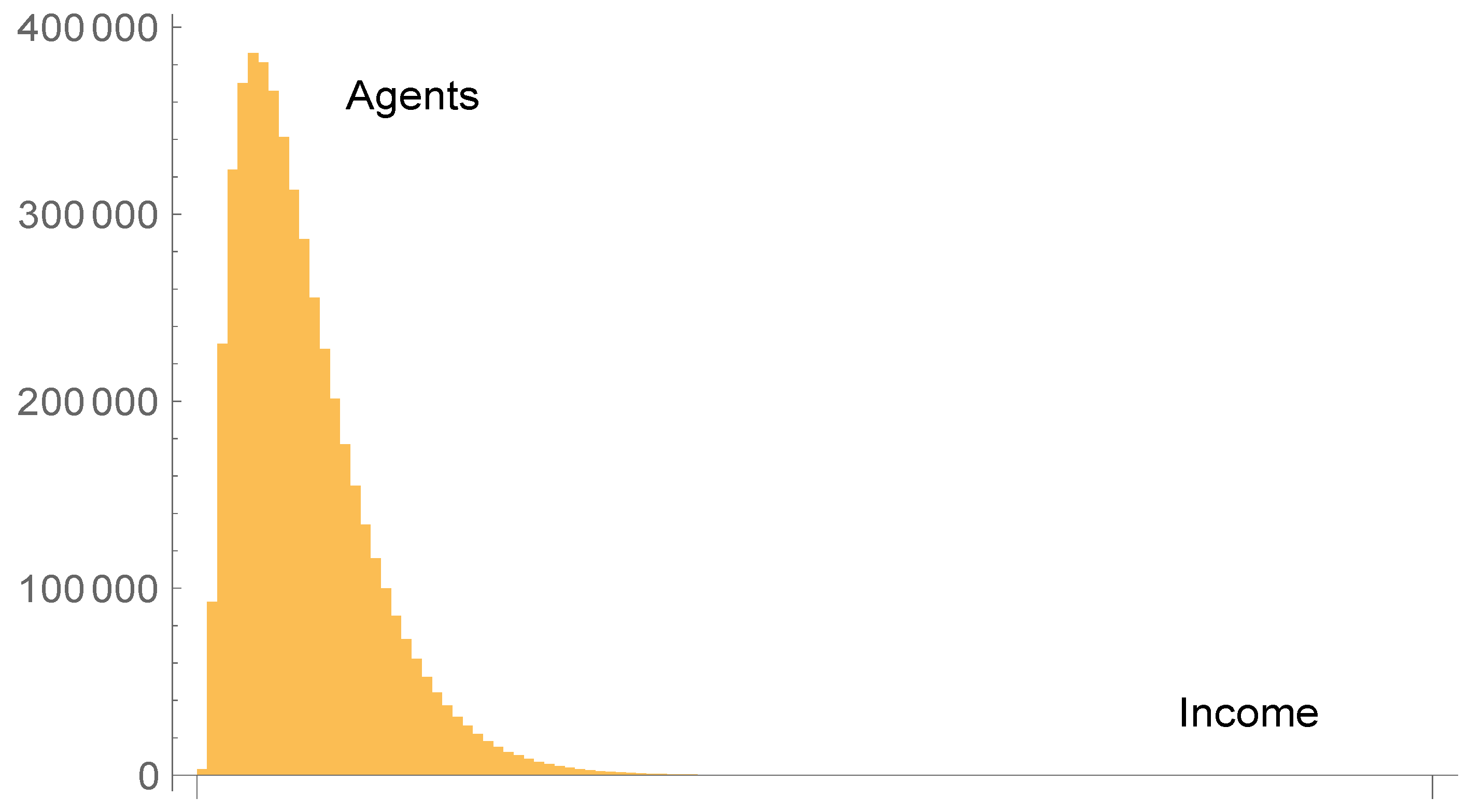

Figure 5. The curve can be fitted by a

-distribution with a ratio

, thus with a Pareto tail of exponent 2.75.

4. Conclusions

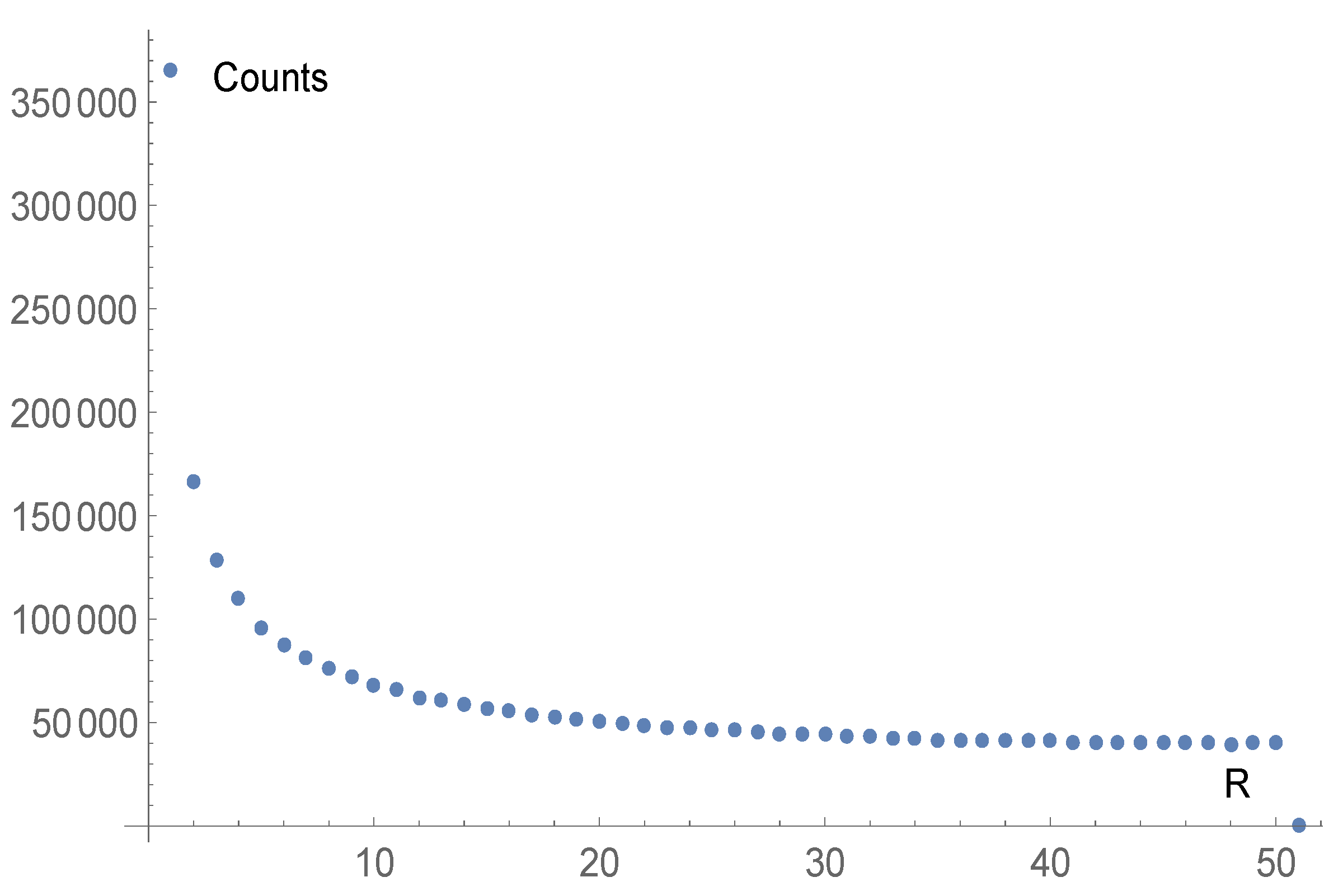

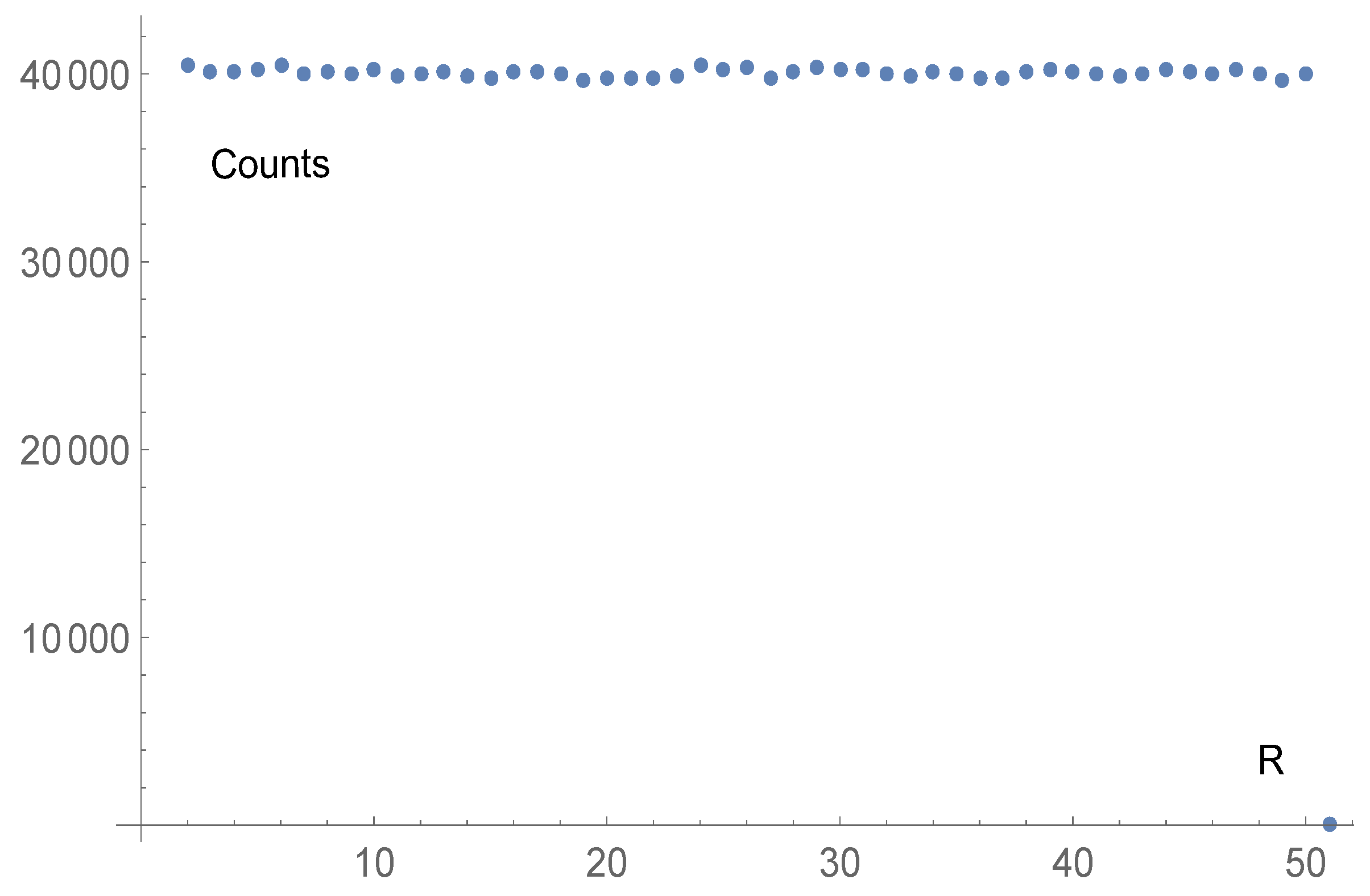

Pursuing an analogy between physics and economics, we have computed the probability that in a relativistic collision between two identical particles the fraction R of energy exchanged is equal to a given value in the interval , thus obtaining a distribution for R. This is accomplished under the assumption that all the possible final states of the collision are equiprobable, i.e., considering only kinematical constraints. The evaluation is done in the reference system where one of the particles is at rest; this choice is motivated by an economic analogy and by the fact that the privileged reference frame for a gas is the frame where most molecules have velocity close to zero.

We have represented the possible final states as a one-parameter line in the 4D space of the final momenta. A Monte Carlo algorithm then generates states uniformly distributed along this line, weighted by the invariant length element of the line. This allows us to obtain a histogram of the values of R. In the non-relativistic limit the histogram has a sharp peak for (and symmetrically for ). By contrast, in the relativistic case, when the incoming particle has a large factor, the histogram is essentially flat. This means that, from the kinematical point of view, in strongly relativistic collisions particles can easily exchange any fraction of their total energy.

The analogue of a relativistic collision in economic interactions is therefore a money exchange without a fixed saving propensity. We have checked through agent-based simulations that interactions of this kind lead to an income distribution with a Pareto tail. This confirms and extends the results of [

10], albeit with the limitation inherent to the analogy employed and to the specific physical process and reference frame considered. Moreover, the present results hold for collisions between identical particles, while in [

10] the particles were considered to be distinguishable.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}