Women in Top Management: Performance of Firms and Open Innovation

,

,  , ,

, ,

Abstract

1. Introduction

2. Literature Review

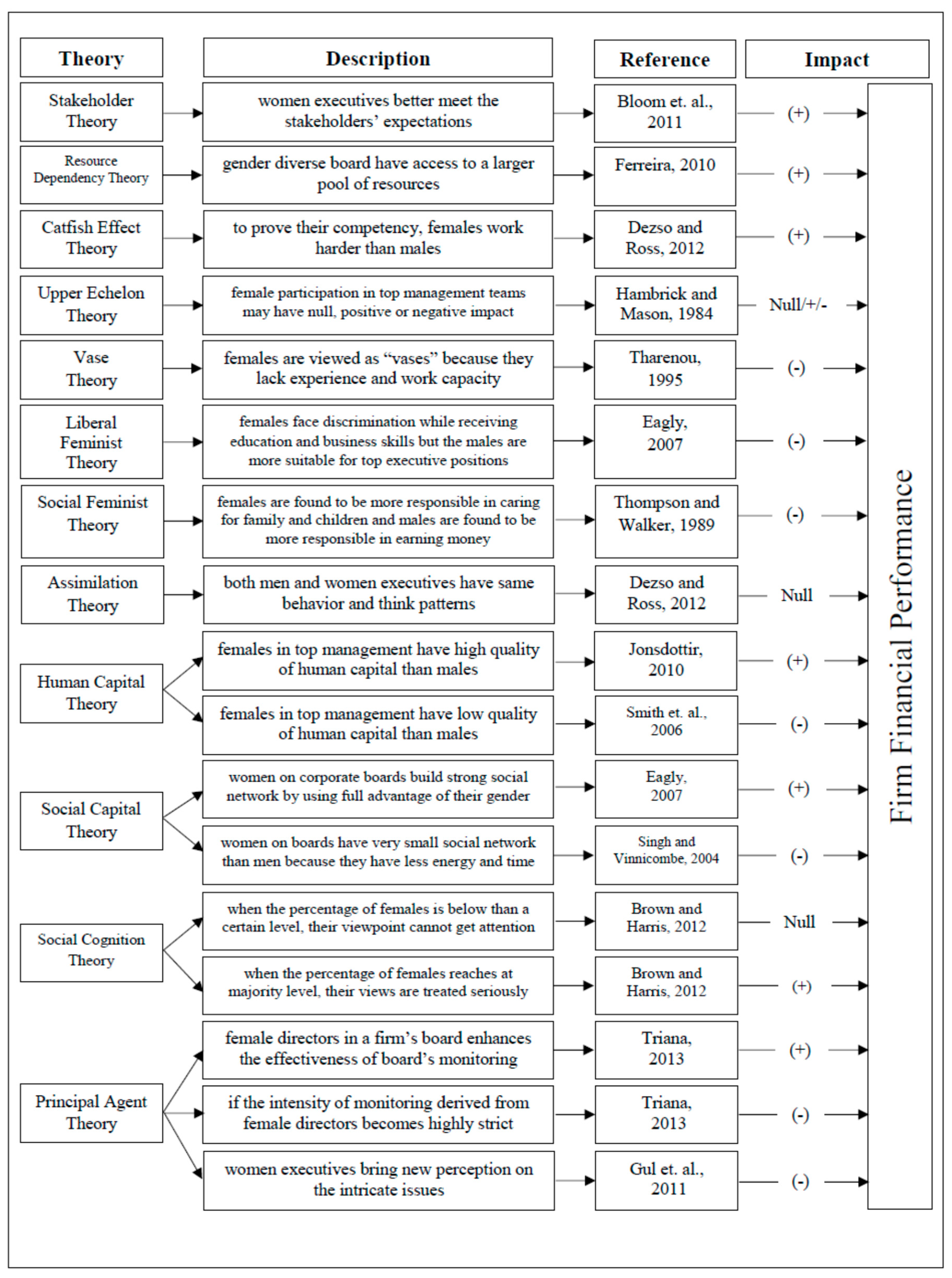

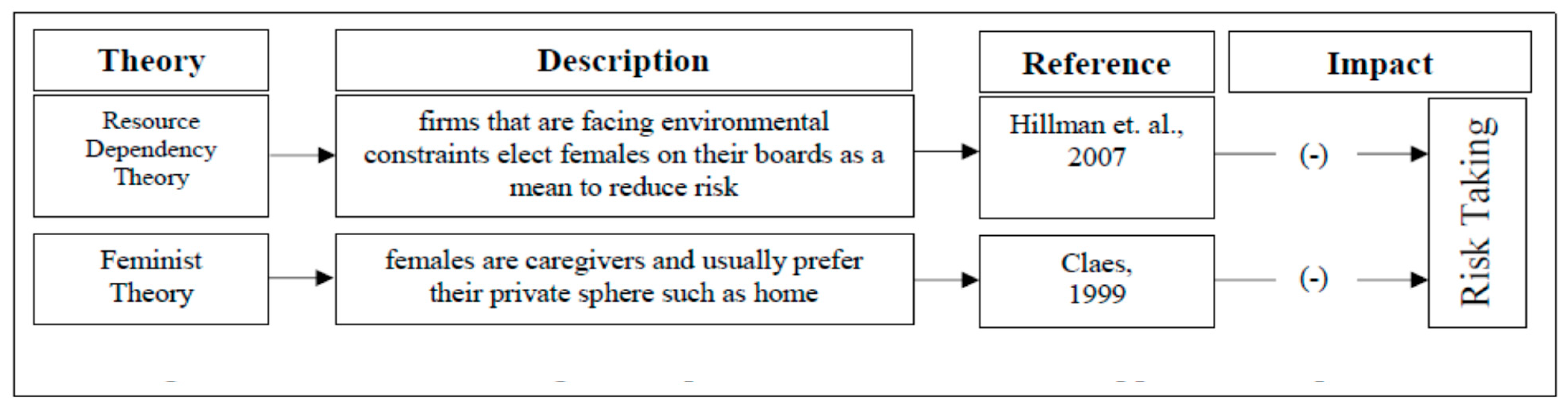

2.1. Theoretical Review

2.2. Empirical Review

{kind=link}

{kind=link}

{kind=link}

| Femininity | Authors | Performance | Risk-Taking | Stability |

|---|---|---|---|---|

| Board Gender Diversity | [32] | ---- | Negative | Positive |

| [27] | Positive | Negative | ---- | |

| [31] | Negative | ---- | ---- | |

| [28] | Positive | ---- | ---- | |

| [29] | Positive | ---- | ---- | |

| [30] | Positive | ---- | ---- | |

| Female CEO | [35] | ---- | Negative | Positive |

| [34] | Negative | Negative | ---- | |

| [45] | “No difference between the risk attitudes of male and female CEOs.” | |||

| [36] | ---- | Negative | ---- | |

| [37] | ---- | Negative | ---- | |

| [38] | ---- | Negative | ---- | |

| [33] | Positive | ---- | ---- | |

| Female Director-General | [39] | Positive | ---- | ---- |

| [40] | Positive | Positive | ---- | |

| [41] | Positive | ---- | ---- | |

| [42] | Positive | ---- | Positive | |

| [43] | Positive | Negative | ---- | |

| [46] | Positive | ---- | ---- | |

| Female in Audit Committee | [44] | Negative | Negative | |

| [47] | No impact | |||

| [46] | Negative | ---- | ---- | |

| [48] | Negative | ---- | ---- | |

3. Methodology

| Variable Name | Explanation/Measurement | Source | |

|---|---|---|---|

| Financial Behavior | |||

| Explained | Financial Performance (FP): Return on Assets (ROA) | ROA = Net Income/Total Assets | [49] |

| Firm Stability (FSTB) | FSTB = Ln (1 + Z) Where: Z = (K/TA + ROA)/SD (ROA) Where: K = Capital, TA = Total Assets, ROA = Return on Assets and SD = 3 years rolling standard deviation | [33] | |

| Risk-Taking Behavior (RTB) | Where: T = 3 “Where: i indexes firms and t indexes year. Nk,t indexes firm numbers within industry k and year t. For each firm with available earnings and total assets for at least three years in 2013 to 2019. We estimate the firm’s EBITDA/ASSETS deviation from the industry average (for the corresponding year) first. Then the standard deviation of this measure for each firm is calculated”. | [1] | |

| Femininity | |||

| Explanatory | Board Gender Diversity (BGD) | The proportion of Females on Board | [50] |

| Female CEO (FCEO) | “1” If CEO is Female, otherwise “0”. | ||

| Female Director General (FDG) | “1” If Director-General is Female, otherwise “0”. | ||

| Females in Audit Committee (FIAC) | No. of Females Sits in Audit Committee | [2] | |

| Control Variables | |||

| Control | Firm Age (FAGE) | No. of years since the firm (incorporated) | [51] |

| Size of Board (SOB) | No. of Board Members | ||

| Size of Firm (SOF) | Natural Logarithms of Total Assets | ||

Econometric Models

4. Results and Analysis

4.1. Summary Statistics and Multicollinearity

4.2. Regression Analysis

4.2.1. Impact of Femininity on Firm Performance

4.2.2. Impact of Femininity on Firm Risk-Taking

4.2.3. Impact of Femininity on Firm Stability

5. Discussions: Women in Top Management, Performance, and Open Innovation

6. Conclusions

6.1. Females and Financial Behavior

6.2. Theoretical Assumptions

6.3. Key Findings

6.4. Theoretical Implications

6.5. Practical Implications

6.6. Suggestion and Recommendations

- The study recommends that having at least one female on corporate boards (by Pakistani Companies Act, 2017) should be continuously utilized and enforced by the firms to get the benefits of having a mixture of males and females in the boards’ composition better financial behavior;

- The firms are advised to invest in a good pool of female talent and search for qualified females who bring additional expertise to the corporate boardrooms and the audit committees;

- The study suggests increasing the women ratio in the audit committee and board of directors.

6.7. Limitations and Future Research Directions

- The study’s findings highlight the need to develop a more comprehensive and differentiated conceptual model based on a multi-approach perspective, integrating the potential performance, stability, and risk effects of females’ representation;

- Future researchers should focus on providing the practitioners with systematic and clean suggestions and tools on improving the positive consequences of a firm’s financial behavior and simultaneously weaken the adverse effects of females’ participation in top-level management and integrating 14 theoretical perspectives expansively;

- The study uses only one measure of each dependent variable, i.e., ROA for financial performance, RTB for risk-taking behavior, and FSTB for firm stability. Future researchers may challenge the findings by using alternative measures to obtain better outcomes;

- The analysis covers the data of seven years only; future studies may increase the data period to get more complete results;

- The study also faces difficulties in finding sample firms with female executives.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- Ali, S.; Liu, B.; Su, J.J. What determines stock liquidity in Australia? Appl. Econ. 2016, 48, 3329–3344. [Google Scholar] [CrossRef]

- Carter, D.A.; D’Souza, F.; Simkins, B.J.; Simpson, W.G. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corp. Gov. Int. Rev. 2010, 18, 396–414. [Google Scholar] [CrossRef]

- Adams, R.B.; Ferreira, D. Women in the boardroom and their impact on governance and performance. J. Financ. Econ. 2009, 94, 291–309. [Google Scholar] [CrossRef]

- Srinidhi, B.I.N.; Gul, F.A.; Tsui, J. Female directors and earnings quality. Contemp. Account. Res. 2016, 28, 1610–1644. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Zaman, M. Board gender diversity and sustainability reporting quality. J. Contemp. Account. Econ. 2016, 12, 210–222. [Google Scholar] [CrossRef]

- Gul, F.A.; Srinidhi, B.; Ng, A.C. Does board gender diversity improve the informativeness of stock prices? J. Account. Econ. 2011, 51, 314–338. [Google Scholar] [CrossRef]

- Jurkus, A.F.; Park, J.C.; Woodard, L.S. Women in top management and agency costs. J. Bus. Res. 2011, 64, 180–186. [Google Scholar] [CrossRef]

- Handa, P.; Schwartz, R.A. Limit order trading. J. Financ. 1996, 51, 1835–1861. [Google Scholar] [CrossRef]

- Brennan, M.; Huh, S.W.; Subrahmanyam, A. An analysis of the Amihud illiquidity premium. Rev. Asset Pricing Stud. 2013, 3, 133–176. [Google Scholar] [CrossRef]

- Amihud, Y.; Mendelson, H. The liquidity route to a lower cost of capital. J. Appl. Corp. Financ. 2013, 12, 8–25. [Google Scholar] [CrossRef]

- Nguyen, H.; Faff, R. Impact of board size and board diversity on firm value: Australian evidence. Corp. Ownersh. Control 2007, 4, 24–32. [Google Scholar] [CrossRef]

- Das, A.; Ghosh, S. Financial deregulation and efficiency: An empirical analysis of Indian banks during the post-reform period. Rev. Financ. Econ. 2006, 15, 193–221. [Google Scholar] [CrossRef]

- Chen, S.L.; Liu, C.K.; Liu, C.Y. Corporate social responsibility, employee productivity and firm valuation. Int. J. Bus. Excell. 2019, 19, 285–303. [Google Scholar] [CrossRef]

- Ghadage, Y.D.; Narkhede, B.E.; Raut, R.D. Risk management of innovative projects using FMEA; a case study. Int. J. Bus. Excell. 2020, 20, 70–97. [Google Scholar] [CrossRef]

- Goodstein, J.; Gautam, K.; Boeker, W. The effects of board size and diversity on strategic change. Strat. Manag. J. 1994, 15, 241–250. [Google Scholar] [CrossRef]

- Rosener, J.B. Ways women lead. In Leadership, Gender, and Organization; Springer: Dordrecht, The Netherlands, 2011; pp. 19–29. [Google Scholar]

- Appelbaum, S.H.; Shapiro, B.T. Why Can′t Men Lead Like Women? Leadersh. Organ. Dev. J. 1993, 14, 28–34. [Google Scholar] [CrossRef]

- Companies Act. An Act to Reform and Re-Enact the Law Relating to Companies and for Matters Connected Therewith, Repeals the Companies Ordinance, 1984 (XLVII of 1984). 2017. Available online: http://www.ilo.org/dyn/natlex/natlex4.detail?p_lang=en&p_isn=104943&p_count=9&p_classification=01 (accessed on 2 September 2020).

- Lee, L.E.; Marshall, R.; Rallis, D.; Moscardi, M. Global Trends in Gender Diversity on Corporate Boards. 2015. Available online: https://www.msci.com/documents/10199/04b6f646-d638-4878-9c61-4eb91748a82b (accessed on 17 July 2020).

- AICD. Boards Should Adopt 30 Percent Target for Female Directors. 2015. Available online: http://www.companydirectors.com.au/general/header/media/media-releases/2015/boards-should-adopt-30-per-cent-target-for-female-directors (accessed on 25 July 2020).

- Wang, Y.; Clift, B. Is there a “business case” for board diversity? Pac. Account. Rev. 2009, 21, 88–103. [Google Scholar] [CrossRef]

- Ullah, M.R.; Mahmood, S.; Azam, M. Women Presence on Board and Financial Performance: Panel Data from Karachi Stock Exchange of Pakistan. Int. J. Ling Soc. Nat. Sci. 2016, 1, 11–17. [Google Scholar]

- Kappal, J.M.; Rastogi, S. Investment behaviour of women entrepreneurs. Qual. Res. Financ. Mark. 2020, 12, 485–504. [Google Scholar] [CrossRef]

- Kot, S.; Meyer, N.; Broniszewska, A. A cross-country comparison of the characteristics of Polish and South African women entrepreneurs. Econ. Sociol. 2016, 9, 207–221. [Google Scholar] [CrossRef] [PubMed]

- Onyusheva, I.; Meyer, N. The features of female entrepreneurship development in Kazakhstan: An analytical survey. Pol. J. Manag. Stud. 2020, 21, 265–282. [Google Scholar] [CrossRef]

- Imm, C.L.; Wahid, N.A. The seeds of leadership: From the experiences of senior Malaysian women leaders. Pol. J. Manag. Stud. 2020, 22, 200–216. [Google Scholar]

- Schubert, R. Analyzing and managing risks–on the importance of gender differences in risk attitudes. Manag. Financ. 2006, 32, 706–715. [Google Scholar] [CrossRef]

- Green, C.P.; Homroy, S. Female directors, board committees and firm performance. Eur. Econ. Rev. 2018, 102, 19–38. [Google Scholar] [CrossRef]

- Magnanelli, B.S.; Raoli, E.; Tiscini, R. Female directors in Italy: The state of art after the mandatory gender quota. Corp. Ownersh. Control 2017, 14, 157–169. [Google Scholar] [CrossRef]

- Terjesen, S.; Couto, E.B.; Francisco, P.M. Does the presence of independent and female directors impact firm performance? A multi-country study of board diversity. J. Manag. Gov. 2016, 20, 447–483. [Google Scholar] [CrossRef]

- Kagzi, M.; Guha, M. Does board demographic diversity influence firm performance? Evidence from Indian-knowledge intensive firms. Benchmarking 2018, 25, 1028–1058. [Google Scholar] [CrossRef]

- Berger, A.N.; Kick, T.; Schaeck, K. Executive board composition and bank risk taking. J. Corp. Financ. 2014, 28, 48–65. [Google Scholar] [CrossRef]

- Ghosh, A. How does banking sector globalization affect economic growth? Int. Rev. Econ. Financ. 2017, 48, 83–97. [Google Scholar] [CrossRef]

- Lenard, M.J.; Yu, B.; York, E.A.; Wu, S. Impact of board gender diversity on firm risk. Manag. Financ. 2014, 40, 787–803. [Google Scholar] [CrossRef]

- Martín-Ugedo, J.F.; Mínguez-Vera, A.; Palma-Martos, L. Female CEOs, returns and risk in Spanish publishing firms. Eur. Manag. Rev. 2018, 15, 111–120. [Google Scholar] [CrossRef]

- Hoang, T.T.; Nguyen, C.V.; Van Tran, H.T. Are female CEOs more risk-averse than male counterparts? Evidence from Vietnam. Econ. Anal. Policy 2019, 63, 57–74. [Google Scholar] [CrossRef]

- Do, H.L.; Tran, T.P.; Tran, V.B.; Nguyen, S.P. Impact of women in the board of directors on business risk of Vietnamese firms. Econ. Mag. 2016, 160, 77–83. [Google Scholar] [CrossRef]

- Faccio, M.; Marchica, M.T.; Mura, R. CEO gender, corporate risk-taking, and the efficiency of capital allocation. J. Corp. Financ. 2016, 39, 193–209. [Google Scholar] [CrossRef]

- Bennouri, M.; Chtioui, T.; Nagati, H.; Nekhili, M. Female board directorship and firm performance: What really matters? J. Bank. Financ. 2018, 88, 267–291. [Google Scholar] [CrossRef]

- Lamiraud, K.; Vranceanu, R. Group gender composition and economic decision-making: Evidence from the Kallystée business game. J. Econ. Behav. Organ. 2018, 145, 294–305. [Google Scholar] [CrossRef]

- Zahoor, N. Relationship between Gender Diversity in Top Management Teams and Profitability of Pakistani Firms. J. Resour. Dev. Manag. 2016, 16, 89–93. [Google Scholar]

- Ismail, K.N.I.K.; Manaf, K.B.A. Market reactions to the appointment of women to the boards of Malaysian firms. J. Multinatl. Financ. Manag. 2016, 36, 75–88. [Google Scholar] [CrossRef]

- Penttila, E. How Do Women in Top Management Affect Firms’ Performance? Master’s Thesis, Svenska Handelshögskolan, 2016. Available online: https://helda.helsinki.fi/bitstream/handle/10138/161112/penttila.pdf?sequence=3 (accessed on 19 August 2020).

- Zalata, A.M.; Tauringana, V.; Tingbani, I. Audit committee financial expertise, gender, and earnings management: Does gender of the financial expert matter? Int. Rev. Financ. Anal. 2018, 55, 170–183. [Google Scholar] [CrossRef]

- Yang, H. Regional Economic Growth and Firm Performance. Anonymous. 2018. Available online: https://scholar.harvard.edu/files/heyang/files/chainstores.pdf (accessed on 10 November 2020).

- Abdullah, S.; Ismail, K.; Izah, K.N.; Nachum, L. Women on Boards of Malaysian Firms: Impact on Market and Accounting Performance. 2012. Available online: http://dx.doi.org/10.2139/ssrn.2145007 (accessed on 13 September 2020).

- Ammer, M.A.; Ahmad-Zaluki, N.A. The role of the gender diversity of audit committees in modelling the quality of management earnings forecasts of initial public offers in Malaysia. Gend. Manag. Int. J. 2017, 32, 420–440. [Google Scholar] [CrossRef]

- Thiruvadi, S.; Huang, H.W. Audit committee gender differences and earnings management. Gend. Manag. Int. J. 2011, 26, 483–498. [Google Scholar] [CrossRef]

- McInerney-Lacombe, N.; Bilimoria, D.; Salipante, P.F. Championing the discussion of tough issues: How women corporate directors contribute to board deliberations. Women Corp. Boards Dir. 2008, 123–139. [Google Scholar]

- Tahir, S.H.; Ullah, M.R.; Mahmood, S. Banks dividend policy and investment decision as determinants of financing decision: Evidence from Pakistan. Am. J. Ind. Bus. Manag. 2015, 5, 311–323. [Google Scholar] [CrossRef]

- Ahmed, A.; Ali, S. Boardroom gender diversity and stock liquidity: Evidence from Australia. J. Contemp. Account. Econ. 2017, 13, 148–165. [Google Scholar] [CrossRef]

- Chung, K.H.; Elder, J.; Kim, J.C. Corporate governance and liquidity. J. Financ. Quant. Anal. 2010, 45, 265–291. [Google Scholar] [CrossRef]

- Prommin, P.; Jumreornvong, S.; Jiraporn, P. The effect of corporate governance on stock liquidity: The case of Thailand. Int. Rev. Econ. Financ. 2014, 32, 132–142. [Google Scholar] [CrossRef]

- Mateos de Cabo, R.; Gimeno, R.; Nieto, M. Gender Diversity on European Banks’ Board of Directors: Traces of Discrimination. 2009. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1362593 (accessed on 25 July 2020).

- Watson, W.E.; Kumar, K.; Michaelsen, L.K. Cultural diversity’s impact on interaction process and performance: Comparing homogeneous and diverse task groups. Acad. Manag. J. 1993, 36, 590–602. [Google Scholar]

- Li, F. Endogeneity in CEO power: A survey and experiment. Investig. Anal. J. 2016, 45, 149–162. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z. Managerial attributes, incentives, and performance. Rev. Corp. Financ. Stud. 2020, 9, 256–301. [Google Scholar] [CrossRef]

- Huang, T.; Wang, W.C.; Ken, Y.; Tseng, C.-Y.; Lee, C.-L. Managing technology transfer in open innovation: The case study in Taiwan. Mod. Appl. Sci. 2010, 4, 2–11. [Google Scholar] [CrossRef][Green Version]

- Freel, M. Patterns of technological innovation in knowledge intensive business services. Ind. Innov. 2006, 13, 335–359. [Google Scholar] [CrossRef]

- Mohannak, K. Innovation networks and capability building in the Australian high-technology SMEs. Eur. J. Innov. Manag. 2007, 10, 236–245. [Google Scholar] [CrossRef]

- Moensted, M. Networking and entrepreneurship in small high-tech European firms: An empirical study. Int. J. Manag. 2010, 27, 16–32. [Google Scholar]

- Trott, P. Growing businesses by generating genuine business opportunities: A review of recent thinking. J. Appl. Manag. 1998, 7, 211–223. [Google Scholar]

- Chen, J.; Leung, W.S.; Evans, K.P. Female board representation, corporate innovation and firm performance. J. Empir. Financ. 2018, 48, 236–254. [Google Scholar] [CrossRef]

- Perrault, E. Why does board gender diversity matter and how do we get there? The role of shareholder activism in deinstitutionalizing Old Boys’ Networks. J. Bus. Ethics 2015, 128, 149–165. [Google Scholar] [CrossRef]

- Huse, M.; Solberg, A. How Scandinavian women make and can make contributions on corporate boards. Women Manag. Rev. 2006, 21, 113–130. [Google Scholar] [CrossRef]

- Eagly, A.H. Achieving relational authenticity in leadership: Does gender matter? Leadersh. Q. 2015, 16, 459–474. [Google Scholar] [CrossRef]

- Bilimoria, D. Building the business case for women corporate directors. In Women on Corporate Boards of Directors; Springer: Dordrecht, The Netherlands, 2000; pp. 25–40. [Google Scholar]

- Post, C.; Byron, K. Women on boards and firm financial performance: A meta-analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar] [CrossRef]

- Bloom, N.; Kretschmer, T.; Van Reenen, J. Are family-friendly workplace practises a valuable firm resource? Strateg. Manag. J. 2011, 32, 343–367. [Google Scholar] [CrossRef]

- Ferreira, D. Board Diversity, Chapter 12 in Corporate Governance: A Synthesis of Theory, Research, and Practice; John Wiley & Sons: Hoboken, NJ, USA, 2010; Volume 8. [Google Scholar]

- Dezsö, C.L.; Ross, D.G. Does female representation in top management improve firm performance? A panel data investigation. Strateg. Manag. J. 2012, 33, 1072–1089. [Google Scholar] [CrossRef]

- Triana, M.D.C.; Miller, T.L.; Trzebiatowski, T.M. The double-edged nature of board gender diversity: Diversity, firm performance, and the power of women directors as predictors of strategic change. Organ. Sci. 2013, 25, 609–632. [Google Scholar] [CrossRef]

- Jonsdottir, T. The Impact of Gender Demography on Male and Female Role Interpretations and Contributions: A Qualitative Study of Non-Executive Directors of Icelandic Boards. 2010. Available online: http://dspace.lib.cranfield.ac.uk/handle/1826/4580 (accessed on 17 August 2020).

- Eagly, A.H. Female leadership advantage and disadvantage: Resolving the contradictions. Psychol. Women Q. 2007, 31, 1–12. [Google Scholar] [CrossRef]

- Brown, G.W.; Harris, T. Social Origins of Depression: A Study of Psychiatric Disorder in Women; Routledge: Abingdon, NY, USA, 2012; Volume 3. [Google Scholar]

- Tharenou, P. Correlates of women’s chief executive status: Comparisons with men chief executives and women top managers. J. Career Dev. 1995, 21, 201–212. [Google Scholar] [CrossRef]

- Thompson, L.; Walker, A.J. Gender in families: Women and men in marriage, work, and parenthood. J. Marriage Fam. 1989, 51, 845–871. [Google Scholar] [CrossRef]

- Smith, N.; Smith, V.; Verner, M. Do women in top management affect firm performance? A panel study of 2500 Danish firms. Int. J. Prod. Perform. Manag. 2006, 55, 569–593. [Google Scholar] [CrossRef]

- Singh, V.; Vinnicombe, S. Why so few women directors in top UK boardrooms? Evidence and theoretical explanations. Corp. Gov. Int. Rev. 2004, 12, 479–488. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Hillman, A.J.; Shropshire, C.; Cannella, A.A., Jr. Organizational predictors of women on corporate boards. Acad. Manag. J. 2007, 50, 941–952. [Google Scholar] [CrossRef]

- Claes, M.T. Women, men and management styles. Int. Lab. Rev. 1999, 138, 431. [Google Scholar] [CrossRef]

- Tahir, S.H.; Shoukat, A.; Mehmood, K.; Latif, K.; Ateeq, A. Does Women Risk Averse in Ownership Behavior: Myth or Reality? Eur. Online J. Nat. Soc. Sci. Proc. 2019, 8, 24–33. [Google Scholar]

| Variables | Mean | Median | Maximum | Minimum | Std. Dev. |

|---|---|---|---|---|---|

| ROA | 0.0320 | 0.0230 | 0.5670 | −1.2100 | 0.3250 |

| FSTB | 1.6610 | 1.5270 | 7.3750 | −2.4600 | 1.3060 |

| RTB | 0.7000 | 0.5700 | 3.1600 | 0.0300 | 0.5200 |

| BGD | 0.2200 | 0.2220 | 0.7500 | 0.0000 | 0.1490 |

| FCEO | 0.0880 | 0.0000 | 1.0000 | 0.0000 | 0.2840 |

| FDG | 1.6180 | 2.0000 | 6.0000 | 0.0000 | 1.0900 |

| FIAC | 0.3120 | 1.0000 | 3.0000 | 0.0000 | 0.7930 |

| FAGE | 31.5020 | 27.0000 | 69.0000 | 9.0000 | 12.8120 |

| SOB | 8.2292 | 4.9400 | 11.5600 | 7.0000 | 0.2900 |

| SOF | 14.8800 | 14.8800 | 18.7600 | 10.7000 | 1.5800 |

| Variables | ROA | FSTB | RTB | BGD | FCEO | FDG | FIAC | FAGE | SOB | SOF |

|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1.00 | |||||||||

| FSTB | 0.13 | 1.00 | ||||||||

| RTB | 0.32 | 0.15 | 1.00 | |||||||

| BGD | −0.18 | 0.12 | 0.11 | 1.00 | ||||||

| FCEO | −0.17 | −0.07 | −0.24 | 0.25 | 1.00 | |||||

| FDG | 0.11 | 0.09 | 0.21 | 0.58 | 0.26 | 1.00 | ||||

| FIAC | 0.23 | 0.42 | −0.30 | 0.55 | 0.24 | 0.54 | 1.00 | |||

| FAGE | 0.13 | −0.17 | −0.37 | −0.16 | 0.06 | −0.14 | −0.15 | 1.00 | ||

| SOB | 0.08 | −0.37 | −0.21 | −0.10 | −0.09 | 0.08 | −0.22 | 0.12 | 1.00 | |

| SOF | 0.18 | −0.15 | −0.22 | −0.17 | −0.07 | −0.15 | −0.14 | 0.18 | 0.31 | 1.00 |

| Independent Variables | Dependent Variable | |||||

|---|---|---|---|---|---|---|

| Model 1: ROA | Model 2: RTB | Model 3: FSTB | ||||

| Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value | |

| Constant | −0.9793 | 0.0000 *** | 12.7849 | 0.0000 *** | −0.5108 | 0.0832 |

| BGD | 0.0513 | 0.0460 ** | −0.0336 | 0.0387 ** | 0.0805 | 0.0213 ** |

| FCEO | −0.0311 | 0.0306 ** | −0.4341 | 0.5437 | −0.0496 | 0.0505 ** |

| FDG | −0.0867 | 0.0220 ** | 0.5424 | 0.3231 | −0.0487 | 0.0749 * |

| FIAC | 0.0498 | 0.0199 *** | −0.0947 | 0.0000 *** | 0.0869 | 0.2537 |

| FAGE | 0.0006 | 0.0462 ** | −0.0025 | 0.5375 | −0.0147 | 0.0013 *** |

| SOB | 0.3718 | 0.0000 *** | 0.4403 | 0.0000 *** | 0.5581 | 0.1654 |

| SOF | 0.0206 | 0.0000 *** | 0.2049 | 0.0000 *** | 0.0461 | 0.2203 |

| R2 | 0.7863 | 0.6897 | 0.6365 | |||

| Adjusted R2 | 0.7435 | 0.6437 | 0.6037 | |||

| Hypothesis | H1a: Fully Accepted | H1b: Partially Accepted | H1c: Partially Accepted | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tahir, S.H.; Ullah, M.R.; Ahmad, G.; Syed, N.; Qadir, A. Women in Top Management: Performance of Firms and Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 87. https://doi.org/10.3390/joitmc7010087

Tahir SH, Ullah MR, Ahmad G, Syed N, Qadir A. Women in Top Management: Performance of Firms and Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(1):87. https://doi.org/10.3390/joitmc7010087

Chicago/Turabian StyleTahir, Safdar Husain, Muhammad Rizwan Ullah, Gulzar Ahmad, Nausheen Syed, and Alia Qadir. 2021. "Women in Top Management: Performance of Firms and Open Innovation" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 1: 87. https://doi.org/10.3390/joitmc7010087

APA StyleTahir, S. H., Ullah, M. R., Ahmad, G., Syed, N., & Qadir, A. (2021). Women in Top Management: Performance of Firms and Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1), 87. https://doi.org/10.3390/joitmc7010087