1. Introduction

Accounting, with its principles and rules as we know it today, experienced rapid growth in the 20th century along with the other sciences. However, its first steps and major milestones can be traced back to 5000 years ago. The first book on accounting was published in Venice on 10 November 1494, entitled Summa de Arithmetica, Geometria, Proportioni e Proportionalita. The author was Lucca Pacioli (1445–1517), a Franciscan monk and a famous mathematician of his time. In essence, he was the first in the entire business community at the time to reveal the new practice of recording business events, a practice that would become the pedestal on which the entire accounting structure was built.

However, today, integrated enterprise resource planning (ERP) systems can do much more by incorporating several modules such as financial accounting, cost accounting, and asset accounting directly into the software. The use of the accounting functions of an ERP solution offers a number of advantages. Most of these benefits relate to one key issue, namely ‘integration’. Accounting systems require data input from various sources. These include production management, inventory management, logistics, order processing, human resources, order processing and human resources. ERP-based accounting automatically integrates information from multiple data sources.

Nevertheless, the present ERP systems still have their limitations, as the ERP business model is usually focused within the boundaries of an enterprise [

1]. With the integration of blockchain technology (BT), we are entering a new era of decentralized systems [

1]. Hence, BT is a distributed, decentralized, transparent, secured, and immutable record-keeping mechanism that creates trust in a trustless environment [

2,

3] with no centralized repository, meaning that all data are accessible to all participant nodes. BT uses a real-time scalable linear database [

4] that maintains a continuously growing set of data records instead of a relational database. As a result, experts indicate that BT could be a game-changer in several industries, with the potential to transform contemporary business models and the structure of markets [

5,

6].

Thus, TEA has attracted the attention of academics and researchers in the last few years [

7,

8,

9,

10,

11,

12] emphasizing the importance of blockchain in the accounting domain. In particular, Dai and Vasarhely [

6] (pp. 5–6) stated that “

blockchain’s functions of protecting data integrity, instant sharing of necessary information, as well as programmable and automatic controls of processes, could facilitate the development of a new accounting ecosystem”.

Moreover, BT through a distributed ledger could be used in accounting to record, store, use, and share accounting data and transactions, ensuring transparency and enhancing data quality [

13] without any human intervention [

14]. According to Dai and Vasarhelyi [

6], BT has the ability to reinvent invoicing, payment processing, inventory information, reporting, contracts, and other documentation, which has significant implications in the accounting sphere. Likewise, Cai [

11] stated that triple-entry accounting within BT, when properly implemented, can improve the trust and transparency of the current accounting systems. Hence, the transition from double-entry to triple-entry accounting is only a matter of time [

15].

Similar, Tapscott and Tapscott [

16] stated that BT could automate accounting and auditing processes. Secinaro et al. [

17] indicated that the notions of truth, trust, and transparency are crucial factors influencing the success of this revolution in accounting and auditing. In this direction, the validity and accuracy of the information provide the basis for the accounting system that is part of the BT [

18], enabling distributed network accounting [

19]. This allows the two parties to make the transactions with a triple-entry ledger system that provides independent verification, enhancing trust and transparency [

6], which in turn improves security and accuracy.

Additionally, Tanner and Valtanen [

20] stated that BT can be applicable and useful in several fields of the manufacturing industry. Mondragon and Coronado [

21] indicated that the trade of composite materials in the manufacturing industry using a blockchain platform could elevate the quality of products that can be secured through BT. Similarllly, Abeyratne and Monfared [

22] recommended the applications of BT to supply chains in the manufacturing industry by analyzing the positive effects of BT on the transparency of a supply chain and the quality of products. Similarly, Korpela et al. [

23] examined the digitalization of supply chain systems through BT.

BT could also improve the transparency and traceability issues within the manufacturing and management sectors. This can be achieved through the use of the immutable record of data, distributed storage, and controlled user access. Recent advances in edge computing and fog computing provide a new impetus to reconsider blockchain applications in manufacturing systems [

24]. Likewise, Papakostas et al. [

25] proposed a conceptual blockchain application for managing product information. As a result, practitioners and scholars do not fully recognize the sustainability advantages of blockchain in relation to the manufacturing sector yet [

26].

However, the potential benefits and challenges that BT could bring to the accounting sphere have not yet been adequately explored. Further, this paper attempts to fill research gaps in the existing literature by providing insights for practitioners and scholars in the development of an innovative cloud computing platform with BT incorporating a real-time accounting ecosystem. In particular, this study attempts a comprehensive literature review of blockchain technology (BT) in the accounting field, providing insights on research trends and key topics in scholarly exploration that are missing from the current body of literature. Specifically, this paper focuses on exploring, analyzing, and deploying a BaaE platform integrating the Triple Entry Accounting (TEA), as well as its impact on cost management, supply chain, and inventory management in an ecosystem platform. This study also highlights the advantages, limitations, and future research opportunities resulting from the current literature.

In particular, the BaaE model is a distributed and decentralized system based on the transmission, verification, and storage mechanism. The recommended system architecture is operating on the blockchain in a private permissioned blockchain network, cooperating and sharing resources and data in a distributed and secured predefined ecosystem. Based on these issues, this study attempts to answer the following research question:

RQ. To what extent could BT support the context of TEA, Decentralized Cost Management (DCM), Supply Chain, and Inventory Management in an ecosystem platform?

The specific objectives of this study are as follows:

Identify the technical and business aspects of BT in organizations.

Describe and analyze the technical characteristics and the architecture of BaaE.

Develop a novel BT architecture for TEA allowing a real-time, verifiable, and transparent accounting ecosystem.

Describe the implications of implementing BT.

By addressing the above research question and objectives, this study contributes to the existing literature in several important ways. First, this study complements and contributes to prior BT literature reviews by proposing a comprehensive BaaE platform and highlighting its distributed and decentralized nature by incorporating the TEA. This enables real time transactions to be recorded and verified in an accounting information system and, more broadly, the use of cost management, supply chain, and inventory management in an ecosystem. Second, based on the literature review, it appears that there is a gap in the research concerning the technical and business aspects of the TEA. Third, this study expands upon the existing knowledge and offers new pathways and insights for practice and innovation in the field by initiating a useful starting point for future research themes and assisting researchers, developers, and experts in engaging with this innovative technology. Finally, this study attempts to contribute to a better understanding of the major themes of existing research while highlighting areas that may be useful for future research to explore.

The remainder of the paper includes a descriptive literature review that explores the concept of BT and its impact on the business environment. This is followed by the materials and methods section. The next section proposes the architecture of the BaaE platform, describing the structure and the technical features. The integration of the BaaE platform in TEA, Decentralized Cost Management, Manufacturing, Supply Chain, and Inventory Management are examined in a subsequent section. Finally, the paper concludes with the discussion, theoretical implications, practical implications, limitations, and further research.

4. The Architecture of Blockchain as an Ecosystem (BaaE): Structure and Technical Features

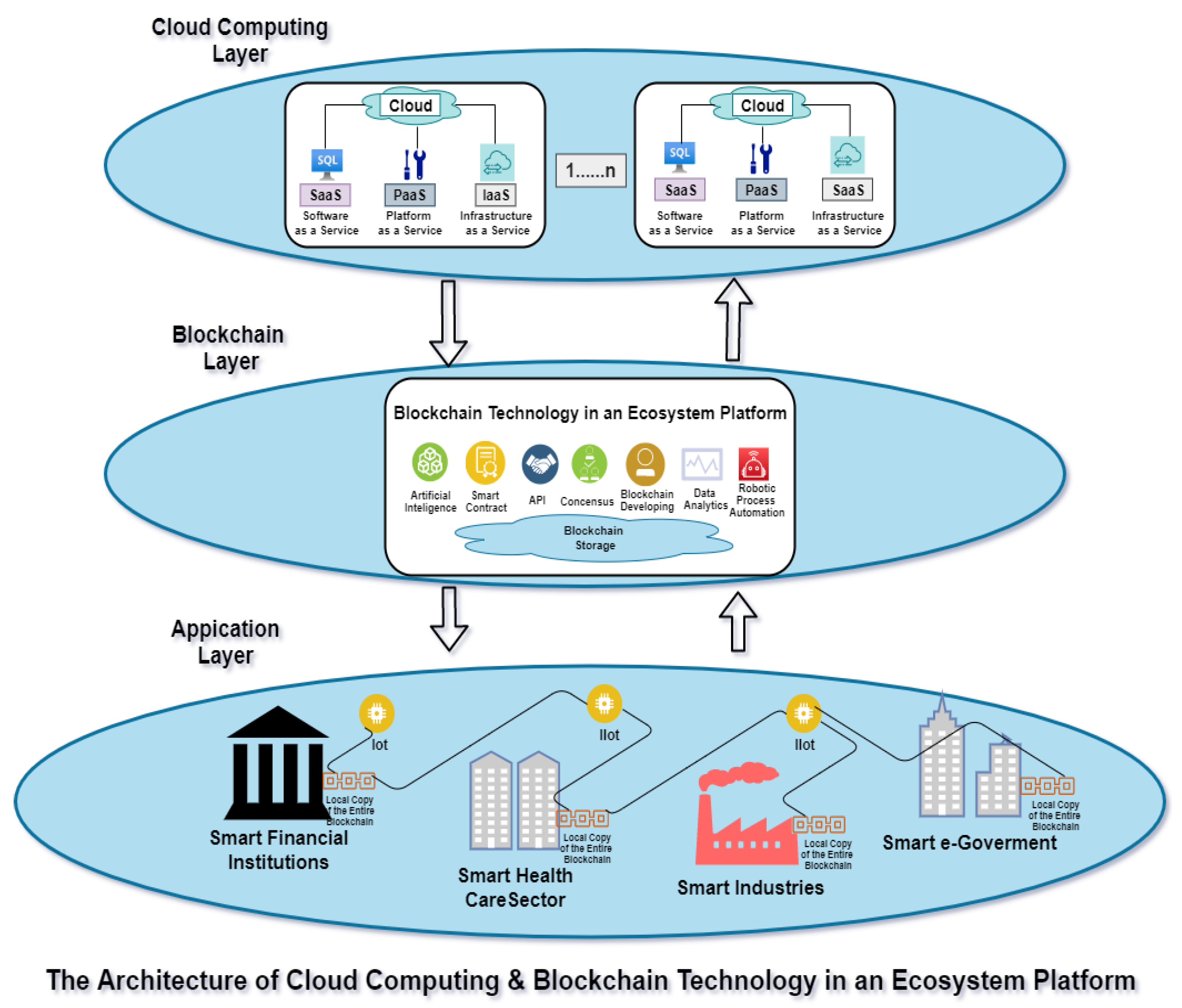

Integrating the next digital generation of Industry 4.0, such as Cloud Computing, Artificial Intelligence (AI), Machine Learning (ML), Predictive Analytics (PA), and the Internet of Things (IoT) with the BaaE platform could lead to unlimited computing resources to execute distributed applications and systems concerning virtual machines, unlimited storage, and low-cost access to infrastructure while overcoming the existing limitations of the present technology and generating emerging distributed, and decentralized information system such as Triple Entry Accounting (TEA), Decentralized Cost Management (DCM), Supply Chain and Inventory Management providing a holistic setup for the next-digital generation of a decentralized ecosystem platform.

Specifically, the Architecture of the BaaE platform comprises a distributed and decentralized system. Specifically, the architecture of BaaE is composed of three tiers: the Upper Layer, Middle Layer, and Bottom Layer.

Figure 2 depicts the conceptual model of cloud computing and BaaE platform incorporating a plethora of innovative functionalities.

The Upper Layer consists of cloud computing, which refers to the availability of computer resources and services via the internet using a peer-to-peer network (P2P). It contains the infrastructure and is the base support for the BaaE, providing the physical and software resources. The cloud computing services are hosted in large data centers known as “data farms”. There are four different categories of cloud computing models—public, private, hybrid, and community—and three different types of web services of cloud computing that could be accessed over the internet—Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). IaaS offers infrastructure resources (i.e., network, storage, memory, processor, executing tasks, and workloads) in a cost and time-optimized manner, for example, the IaaS of Amazon. PaaS offers the framework where users could implement their application with required scalability, for example, the PaaS of Microsoft. Finally, SaaS offers software functionality as a high-quality service with no maintenance and initial cost, for example, the SaaS of Gmail.

The BaaE is allocated in the Middle Layer, which is embedded with several advanced technical components (i.e., AI, DA, RPA, IoT, IloT, learning, analyzing, predicting, and managing all digital business processes at any time from any location), which provides the foundations for new future technologies [

42]. The BaaE is a distributed decentralized system based on the transmission, verification, and storage mechanism. The BaaE requires authority management and control procedures to participate in the network since it is a private permissioned blockchain.

The core of BaaE consists of the blockchain, smart contracts, and the consensus mechanism. The blockchain is responsible for the information storage of the blockchain system, using P2P networks that allow two or more devices to share resources, and data blocks chain one by one in chronological order [

31]. The blockchain will enable cryptographic hash functions [

31] and asymmetric encryptions, forming the backbone and containing the entire history from the first block to the latest one [

43].

The consensus mechanism is responsible for coordinating and confirming the consistency of all nodes’ data records or data blocks in the whole network. BaaE is deploying time-stamping, proof-of-work (PoW), and proof-of-stake (PoS) to prevent malicious people from creating numerous fictitious identities and influencing the blockchain modification process [

44,

45].

The smart contract is responsible for compiling, deploying, and implementing the business logic behind the BaaE. The comprised smart contracts are automated protocols [

46] to perform contract terms through an automated or agreed upon protocol [

16], minimizing the manual intervention and validating transactions without the need of a third party.

Moreover, through the process of mining, BaaE is utilizing its own modeling operation and validation procedures, executing inter-organizational business processes [

47]. Further, BaaE is including data storage, the needed blockchain services, the system management, which is responsible for managing the blockchain architecture, and the interface needed to provide the interaction within the application layer.

Finally, the Bottom Layer is the Application Layer which is responsible for communicating with other business entities that are participating in the BaaE. The participating businesses could maintain their own local copy of the entire BaaE at all times, according to the authorizations that they have over the blockchain network.

5. Blockchain Technology and Triple-Entry Accounting (TEA) in an Ecosystem

This study proposes a decentralized TΕA ecosystem based on Grigg’s [

12] and Cai’s [

11] conceptualizations of TEA. The recommended development is based on the aforementioned architecture (The Architecture of Cloud Computing and BaaE illustrated in

Figure 2). The authors recommend a private permissioned cloud computing blockchain ledger. According to the study, this configuration is the ideal approach to depict the proposed decentralized accounting model, maintaining a local copy of the entire BaaE configuration.

Using BaaE as private permissioned on a cloud-based network that integrates TEA only authorized business entities (i.e., suppliers, manufacturers, and stakeholders) will be able to submit transactions, records, and related accounting data within the same blockchain ledger. This will also enable aggregating information from multiple sources and information of different natures, providing data easily, accurately, and securely to all concerned parties in a predefined environment. Figure 6 depicts the conceptual model of cloud computing and the BaaE platform incorporating TEA.

Specifically, using a TEA on the BaaE platform means that all parties involved in the accounting process will be cryptographically secure and chained via a smart contract to a third entry. The third entry in the TEA contains both the transaction and the invoice entered into the blockchain. As a result, all parties will have proof of the transaction that is saved on the network.

Figure 4 depicts the conceptual model of cloud computing and BaaE platform integrating TEA. In particular, the conceptual model integrates TEA in a decentralized ledger using smart contracts in the BaaE platform. According to the demo, the Aircraft Supplier Parts Company issued an invoice to the Aircraft Manufacturing Company for buying raw materials and components parts. The invoice sent to the Aircraft Manufacturing Company cryptographically uses hash encryption with the terms and the conditions agreed upon. A payment made using tokens once the transaction is verified and proof of the transaction is sent to both parties. Finally, the transaction is recorded in chronological order and saved permanently into the blockchain

Thus, triple entry bookkeeping accounting means direct joint among two or more parties P2P that are utilizing the BT by using “proof-of-work” for proof of transactions by the network, leading to the validation of records without the need of any third party [

49]. TEA on BaaE does not simply add a third entry to the traditional double-entry bookkeeping approach; instead, BT ledger records accounting entries for both transacting parties. This creates an interlocking system of enduring accounting records [

50,

51], where trust moves from an external authority to all participants in the blockchain network [

52] enduring accounting records [

51]. All entries in BaaE and TEA will be cryptographically sealed, and changing or deleting them will be almost impossible due to the fact that all transactions are electronically and cryptographically stamped in a predefined environment.

Therefore, TEA on a BaaE platform will allow business entities to record both sides of a transaction simultaneously. Upon validation of a sale and purchase under Generally Accepted Accounting Principles (GAAP) criteria using smart-contract, the initiation of recording of journal entries can occur to reflect the financial statement impact of the transactions instead of keeping records of financial transactions in separate private databases. This review process by consensus creates a document of notarization that provides greater accuracy and transparency. This document is created due to the transaction data being stored in cryptographical protected blocks whose integrity is verified through the process of mining and using operational and validation procedures to secure business entities that participate in the shared blockchain ledger.

Consequently, by using the BaaE platform and TEA, accounting records and transactions will be automated and authenticated without the need for third parties, transferring the ownership of assets while assuring a ledger of accurate financial information in a trusted and secure manner [

53]. Hence, firms’ records and Balance Sheets, Income and Cash Flow Statements will be visible to all concerned parties (i.e., suppliers, customers, accountants, controllers, internal and external auditors and shareholders), improving the accuracy and the transparency of the information. This will reduce the cost of maintaining transactions (physical or digital) and records kept only once in blocks of a blockchain-decentralized lender, making it accessible to any authorized partner.

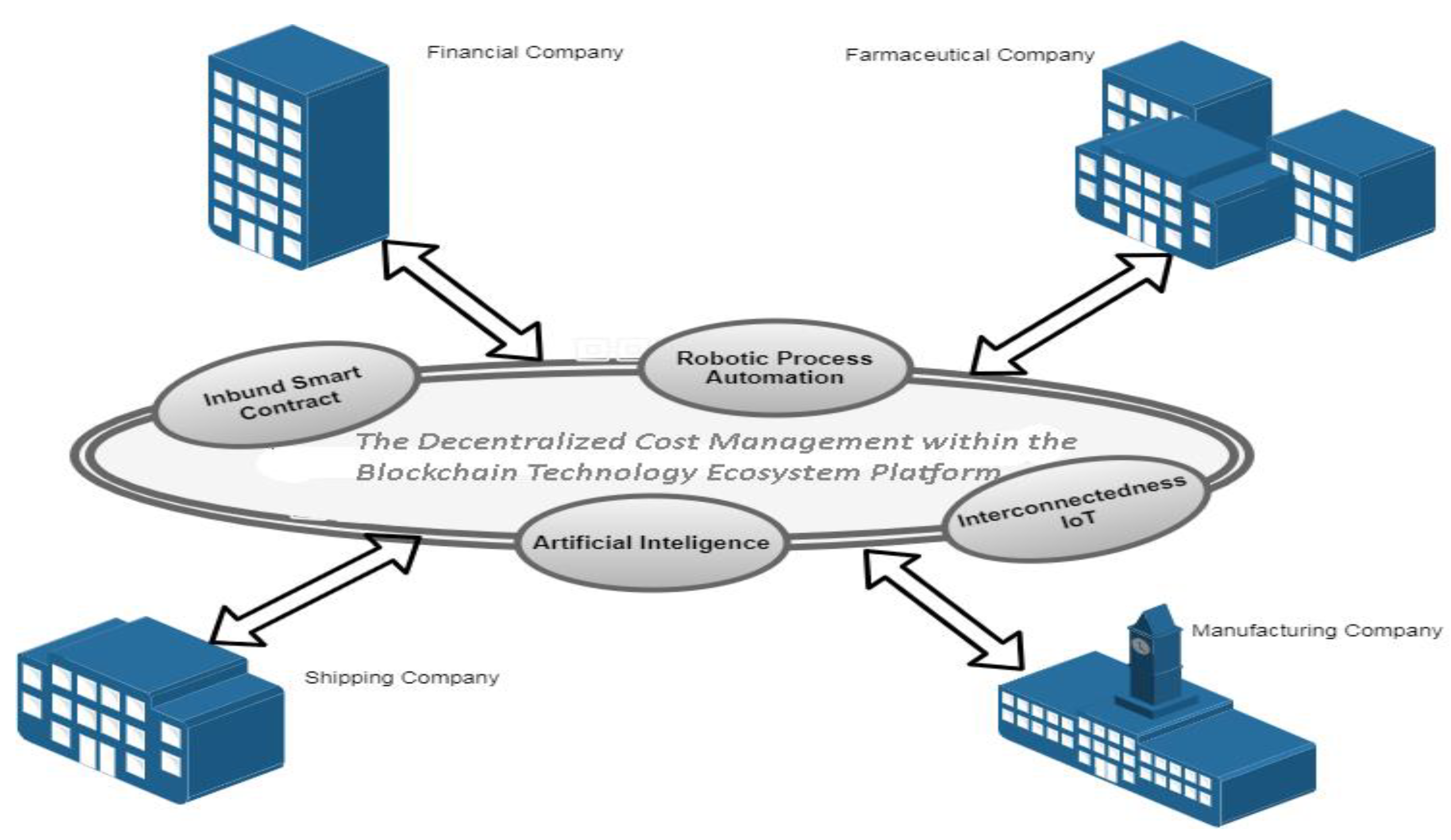

6. Decentralized Cost Management System

In the following section, the possible integration of cloud computing and BaaE in the cost management field is examined. In particular, a decentralized theoretical model within cost management is introduced by exploring potential applications of this technology and emphasizing how information is propagated via BaaE, enabling an innovative Decentralized Cost Management (DCM) digital information system.

The DCM could be applied according to the above-aforementioned decentralized architecture (

Figure 2. The Architecture of Cloud Computing and BaaE) in a private permissioned cloud computing distributed ledger. By integrating cloud computing and DCM into BaaE, business entities will not only be able to include financial and accounting transactions between two or more parties (Broby and Paul, 2017) such as payments, assets, and financial transactions among enterprises on secure distributed ledgers, but also, BaaE could enable a DCM information system optimizing business practices and enhancing the enterprise value chain by utilizing a completely new approach.

Moreover, the DCM information system in a decentralized ledger could change the core structure of the existing cost management. It could offer better data reliability, reduce cost and human error, and automate costing transactions and business processes. This pertains to the use of raw materials and the assembly of new smart products, which will be identifiable and traceable with the capability of self-awareness and optimization through the use of smart contracts [

46], AI, DA, RPA, and IoT [

42,

46] improving business processes that may not have been measured correctly by removing any overhead costs and labor costs. This highlights the real-time decision making and automation of the business process.

Figure 5 illustrates the Decentralized Cost Management within the BaaE.

Dhilon et al. [

54] stated that a blockchain network is comprised of several peer nodes in which each peer node includes different smart contracts and ledgers. Therefore, establishing collaboration between business entities is essential in a safe, permanent, tamper-proof manner by using a blockchain distributed ledger. Each business entity is accessed upon a single or multiple blockchain networks [

54], which broadcasts recorded cost accounting transactions that are updated in the network according to their authorizations. Hence, it will be difficult to alter or remove transactions when a new block is proposed according to a consensus mechanism [

55].

Similarly, Andoni et al. [

56] stated that smart contracts that use P2P networks will enable multi-trusted parties to manage data simultaneously. Therefore, by incorporating into DCM, inbound smart contracts could serve as automated controls to monitor cost accounting processes based on predefined rules, and lIoT industrial-based connected sensors/devices could capture data automatically without human intervention. Doing so will provide at-a-glance visibility, tracking the cost of raw materials, and goods, and recording provenance data from the source to the business entity and vice versa to the consumer by collecting and sharing information through the value chain using AI, RPA, and DA that could change the processes of cost accounting applications.

In particular, authorized business entities using DCM could locate the cost of their digital products at any stage of the value chain, recording the origin of location and ownership of raw materials of items, the life cycle records of products (from raw material to consumption and to the waste process) and costs in near real-time. Thus, DCM could automate large-scale processes, speed up the execution of the production, eliminate the manual and error-ridden process, improve efficiency, and track the cost of raw materials from multiple sources, which would significantly change the cost structure.

Decentralized Cost Management in Manufacturing

Using BaaE and DCM with granular costing, we can subdivide the costs of smart products, goods, and resources, obtaining accuracy and a high level of detailed information. According to Cidav et al. [

57], this granular method at procedure-level costs is preferable as opposed to broad categories, as it enables stakeholders to realize what actual resources have been used and for what purposes. This approach involves segmenting the costs of smart products into smaller and more manageable pieces and then analyzing each activity’s impact on cost and value. In other words, breaking down a single product, service, object, or component into smaller chunks could be the ideal technology for production-centric industries such as the food and beverage industry, automobiles, and aerospace manufacturers. Each of these examples has long product lifecycles and large, complex cost objects.

Specifically, DCM with granular costing on the BaaE platform could be the next technology to support decentralized cost management in manufacturing. According to the above-aforementioned model (

Figure 3 illustrates: The Integration of BT Vertically and Horizontally in the Value Chain), the blockchain could act as a centralized distributed ledger that is managed and initiated by a manufacturer. It will have the capability to seamlessly collate data from multiple systems belonging to suppliers, customers, and distributors.

Moreover, the interaction among manufacturers has become a new source of value creation, by utilizing Industry 4.0, Smart Contracts, IIoT, sensors-devices [

58,

59], RPA, AI, and DA that optimize many cost accounting processes in an enhanced blockchain distributed ledger. Further, cognitive manufacturing, which has been proposed as an innovative change to Industry 4.0 [

60], data mining process, and BT in the context of equipment operation and worker motion, which can be captured by massive sensors, can advance decision support, including process monitoring and fault diagnosis.

Thus, by using the above mentioned modern technologies, the whole manufacturing process could be automated between end users, service providers, and manufacturing services that are encapsulated on BT. In addition, using smart contracts can enforce pre-defined rules, without the need of human intervention assisting manufacturers to track the cost of products from multiple sources and hence, controlling the cost of the end-product. This would enable the accuracy of costing information stored in the blockchain. Additionally, it would allow real-time decision-making, providing a common trustworthy environment and ensuring a transparent, secure, and controlled exchange of cost information.

For instance, an automobile or an airplane can be built based on the sum of individual components from different suppliers or partners. Using BaaE with DCM and granular costing will track not only the cost of the raw materials or ingredients for a smart item through the value chain using smart contacts, but also make decisions about the entire process including cost allocation, pricing, resource management, and promoting end-to-end visibility by providing a single source of truth to all parties. French automaker Renault [

61] is already using a blockchain solution. It is based on the Microsoft Azure blockchain, in order to manage car ownership, track its products in the market and simplify the release of new designs.

An example of production-centric industries using DCM with granular costing on the BaaE platform in cloud computing could be an automobile or aircraft manufacturer like Airbus or Boeing, which can have hundreds of thousands or even millions of parts. Utilizing the technology described could give airlines, manufacturers, and suppliers the level of transparency they need. A standard commercial jet is made up of more than 300,000 parts. Even though they use integrated systems, connected devices, sensors, interfaces, and cloud computing, there is still a lack of real-time access and transparency to information regarding the differential and multiple parts that an aircraft or an automobile might use, thus leaving numerous single points of failure in tracking operations.

Therefore, getting a holistic, real-time picture regarding the manufacturing of aircraft or automobiles is impossible, regardless of who might need that information. This is due to the fact that every business entity in the production chain is often using different applications, legacy systems, or ERP systems.

Using DCM within BaaE with granular costing might provide a solution to the manufacturers by creating an immutable ledger of all aircraft or automobile components and partners. This may allow all parties to trust each other. These parties could be competitors in the marketplace, but must cooperate within the common ecosystem of the airplane or an automobile by balancing transparency and privacy on a blockchain distributed ledger.

This would allow manufacturers to track the cost and the provenance of individual components by giving a snapshot of all the parts that an airplane or an automobile needs through the blockchain. Thus, most of the larger aircraft and automobile manufacturers have announced plans to develop and test blockchain distributed ledger enabled trading platforms. For instance, Honeywell has presented an online marketplace for aviation parts that utilizes blockchain to ensure accurate quality documentation for every single part. In addition, utilizing inbuilt Smart Contracts, IIoT, sensors-devices, RPA, AI, DA, and modern technologies will optimize many cost accounting processes in an enhanced blockchain distributed ledger. All of these will increase the efficiency and value of the cost accounting function regarding the authenticity of information and eliminate fraud tracing costs on a real-time basis, and authorize business entities to access cost records in the distributed ledger.

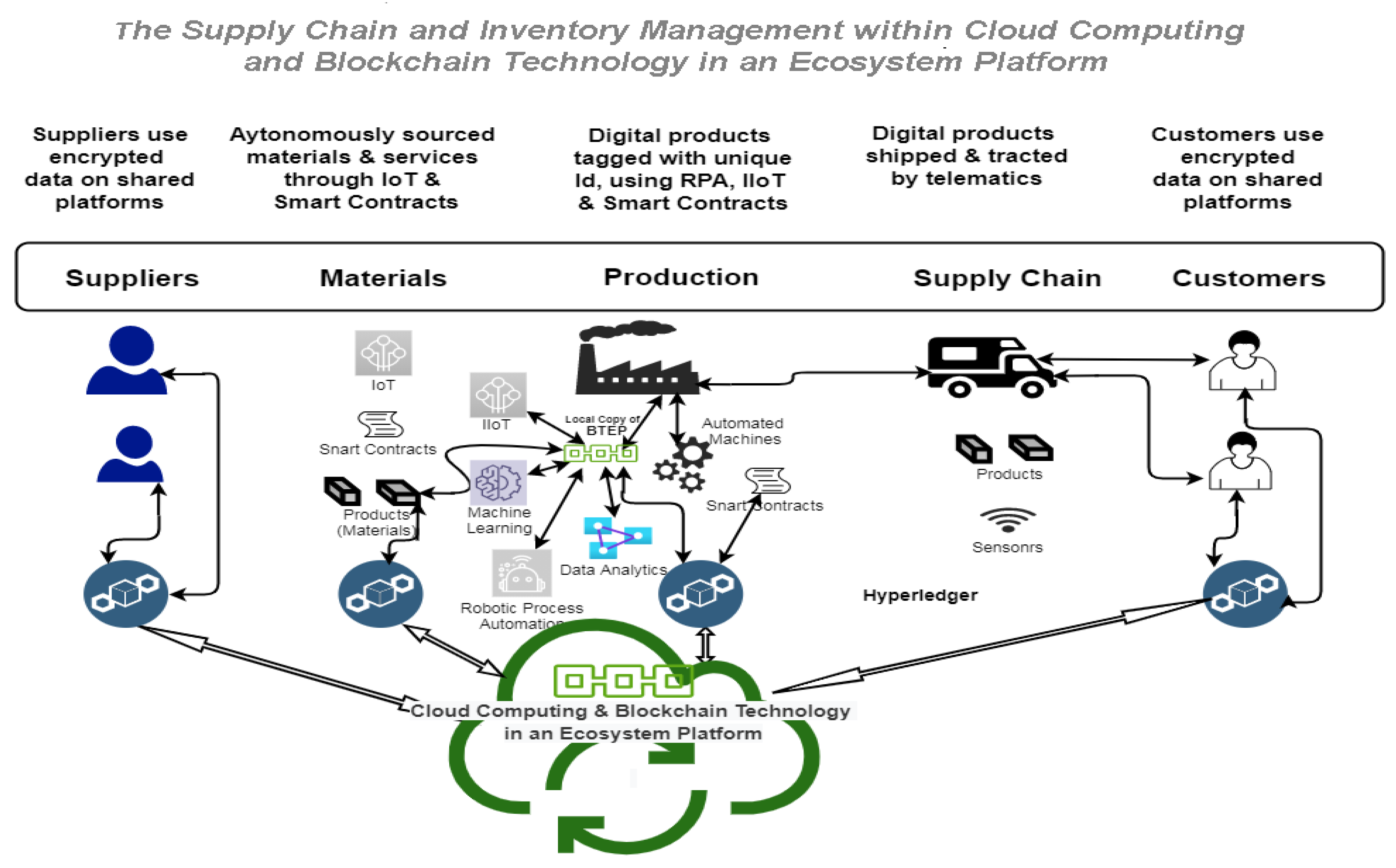

7. Supply Chain and Inventory Management

These days, supply and logistics chains are critical to support the entire life-cycle of the extended manufacturing enterprise [

62]. BT could play a crucial role in supply chain management, from warehousing to shop floor operations. According to the above, a decentralized architecture (

Figure 2. The Architecture of Cloud Computing and BaaE) in a private permissioned cloud computing distributed ledger, supply chain, and inventory management could be supported. BT could provide the required data authenticity and security in the supply chain and logistics providing immutable transactions [

63]. These operations could include machine-level monitoring, production lines, tracking raw materials, tracking the origin and destinations authenticated, and proof of all transactions can be stored and not manipulated [

64].

Moreover, BT could also improve supply chain visibility and fraud detection [

65], increase the speed of material flow reduce inventories and improve trust payment processing. It could reduce counterfeiting and trace the origin of the product, its ingredients, and ownership, eliminating product ambiguity. BT could prove the authenticity and determine the origin of products or services increasing the flexibility of the existing value chain. This can occur by ensuring greater efficiency and transparency [

65], in the entire value chain management system coordinated by all participants. Hence, BT would be a key factor in reducing the time of products spent in the transit process, improving inventory management, stock waste, and efficiency. Instead of adopting lean philosophies such as just-in-time (JIT) or zero inventory manufacturing, this system would adjust the inventory at the required quantity and at the right time.

Figure 6 illustrates the Supply Chain and Inventory Management within cloud computing and BT.

Inventory could also be constantly measured by the BT, collecting real-time data regarding production lines and slow-moving products and demand forecasting [

66]; eliminating products and services that do not add value, determining the product status of its lifecycle, verifying which part of the raw components went into digital finished products, monitoring and improving product quality, and identifying machine faults, which would save costs [

67] and provide better decision-making. Thus, shareholders, accountants, and managers could have a holistic, real-time picture of the production processes and the value chain. This could maximize the transparency of the business process [

22] and operations across the entire enterprise and eliminate fraud in a common ecosystem.

8. Conclusions

8.1. Discussion

This study sought to accomplish several goals. First, as there is limited research on this topic, this study attempted to fill a gap in the academic literature and provided an overview and insights for researchers, developers, and practitioners. Second, after a thorough literature review, this study introduced and explored the deployment of an innovative BaaE platform in the context of the TEA that could essentially change current accounting practices, cost management, supply chain, and inventory management functions.

Particularly, the authors discussed and analyzed how BaaE through TEA could automate accounting transactions and records, eliminating the need for third parties and enabling a real-time, verifiable, and transparent accounting ecosystem. Therefore, this study complements the existing literature in terms of comparative contrast using the outcomes of Grigg and Cai’s research on TEA. Hence, the deployment of BaaE with TEA could be implemented within a homogeneous group of organizations. As a result, our study recommends a private permissioned blockchain in which only authorized organizations will be allowed to participate in TEA, using smart contracts in an ecosystem. In contrast, Cai’s model is using a public third ledger with smart contracts to enable TEA, which will be very risky in exposing the private data of an organization.

On the other hand, Dai and Vasarhelyi’s research proposed a totally different scheme. They suggest an embedded blockchain layer within the ERP system, extending the existing double entry accounting system in enabling TEA. However, their proposed model is not consistent with the idea of TEA in Grigg’s work since they are using a different approach to allow TEA.

The authors then discussed and explored how a BT in a private distributed ledger could change the core structure of the existing cost management system, supply chain, and inventory management. They found out that BT could automate business processes, improve transparency, and track the cost of raw materials from multiple sources. Likewise, Abeyratne and Monfared stated that BT can improve the transparency of a supply chain and the quality of products. Additionally, the study explored the potential challenges, and obstacles, informing that TEA within BT is a new technology and it needs to deepen its understanding before an organization implements it. However, BT and TEA can offer new pathways and insight, improving various sectors of the economy.

8.2. Theoretical Implications

This study proposes a conceptual framework examining the architecture of BaaE in the use of TEA implementation and their potential influence on an organizations’ performance and sustainable approaches. Previous research in BT and accounting has provided some evidence to support the benefits of the modern TEA information system [

6,

11] and optimized cost management and supply chain as well as inventory management improving and enhancing organizational performance.

8.3. Practical Implications

Following research, this paper demonstrates that the BaaE in the context of TEA has a significant and positive influence on organizational performance. Nevertheless, the implementation of decentralized and distributed blockchain systems and the abandonment of the current centralized ERP systems and the traditional accounting practices are very risky. ERP systems are highly transactional with no computational overhead, automating the processes of various business transactions. ERPs are prepackaged business software providing a fully integrated solution for organizations. In contrast, BT is investing in accounting and other module applications. As a result, there are only a small number of instances in which the technology has been applied. Therefore, there are several drawbacks that must be addressed:

Lack of pilot, practical, functional applications and systems regarding BT on accounting, cost management, supply chain and inventory management systems. Pradhan et al. [

68] stated that “

Full blockchain development could take five to seven years or longer or may not occur at all”.

Agreeing upon and approving a suitable compensation scheme [

69] and building a proper BT ecosystem of multiple parties in a private permissioned blockchain is one of the biggest challenges.

Security challenges referring to cyber-security issues and threats [

70,

71,

72].

Interoperability, scalability, transparency, usability, computational efficiency, and storage size issues are the main reasons preventing the mass adoption of BT [

71,

73,

74,

75,

76].

The adoption and implementation of a new system or technology within any organization initiates “resistance-to-change” reactions from the employees. Negative personnel attitudes towards new technologies such as BT might be attributed to fatigue and apathy [

77].

Technical issues due to the fact that BT is a new decentralized and distributed technology. For instance, BT is not appropriate for massive transactions, due to the complex verification process (PoW) or (PoS) [

78,

79].

Lack of laws and regulatory support [

80,

81].

8.4. Limitations and Further Research

Despite these benefits, BT is still at an early stage and there are several limitations regarding the deployment of the BaaE platform that must be considered. The main limitation of this paper is the lack of empirical and practical functional applications and systems. The study mainly provided a theoretical study for BaaE architecture and its impact on the accounting field; nevertheless, further work is required to analyze, design, develop and codify it properly in order to be applicable within the accounting domain.

Moreover, the principal BT implementations in the accounting area have been studied by numerous researchers, but are not yet widespread. Therefore, more empirical evidence is needed to examine ΤΕA that could become the leading industry for transforming and integrating various accounting practices within BT. Additionally, several technical and business aspects should be resolved first, such as transparency, security, interoperability, and scalability, to implement this emerging technology.

Future research is required to examine and comprehend BT by analyzing more intensively the integration of cost management, and supply chain management, as well as its implications in businesses, since the literature on BT is continuously expanding in other fields of the economy. Academics and researchers should also search journals, articles, and practical applications that integrate cloud computing with BT in the accounting sphere. Research should also examine the integration of Industry 4.0, in particular AI, RPA, DA, loT, and lloT within BT, which could change the processes of accounting applications, supply chain, inventory management and financial services.

More research is required to examine the cyber security regarding BT and its implications for the privacy of organizations. For instance, it could be very risky for a business entity that uploads its accounting sensitive data to the blockchain by exposing its data in an untrusted environment, if it is not set up appropriately. Practitioners should examine the business model, resolve usability, interoperability and computational efficiency issues with other systems. Investigate in detail the use of smart contracts, due to the fact that is still in early stages. Developers and practitioners should examine and address issues such as the validity of transactions, flexibility, scalability and privacy regarding the code of smart contracts that might be available to public.

Finally, from the review of the literature, the use of BT is relatively recent. BT seems to be the next step in the digital era. In our opinion, the potential benefits could be enormous if BT could be successfully implemented. The proposed deployment of BT may motivate and assist developers and experts in further developing and employing this technology. Therefore, in addition to contributing to BT applications through innovation and transforming technologies and scientific fields, the findings from this literature review can generate value for academics, practitioners, and organizations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}