Financial Innovation in Digital Payment with WeChat towards Electronic Business Success

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. Development of Third-Party Digital Payment Platforms

2.1.1. Service Quality

2.1.2. Perceived Ease of Use

2.1.3. Perceived Risk

2.1.4. Perceived Security

2.1.5. Social Influence

2.1.6. Compatibility

2.1.7. Age

3. Methodology

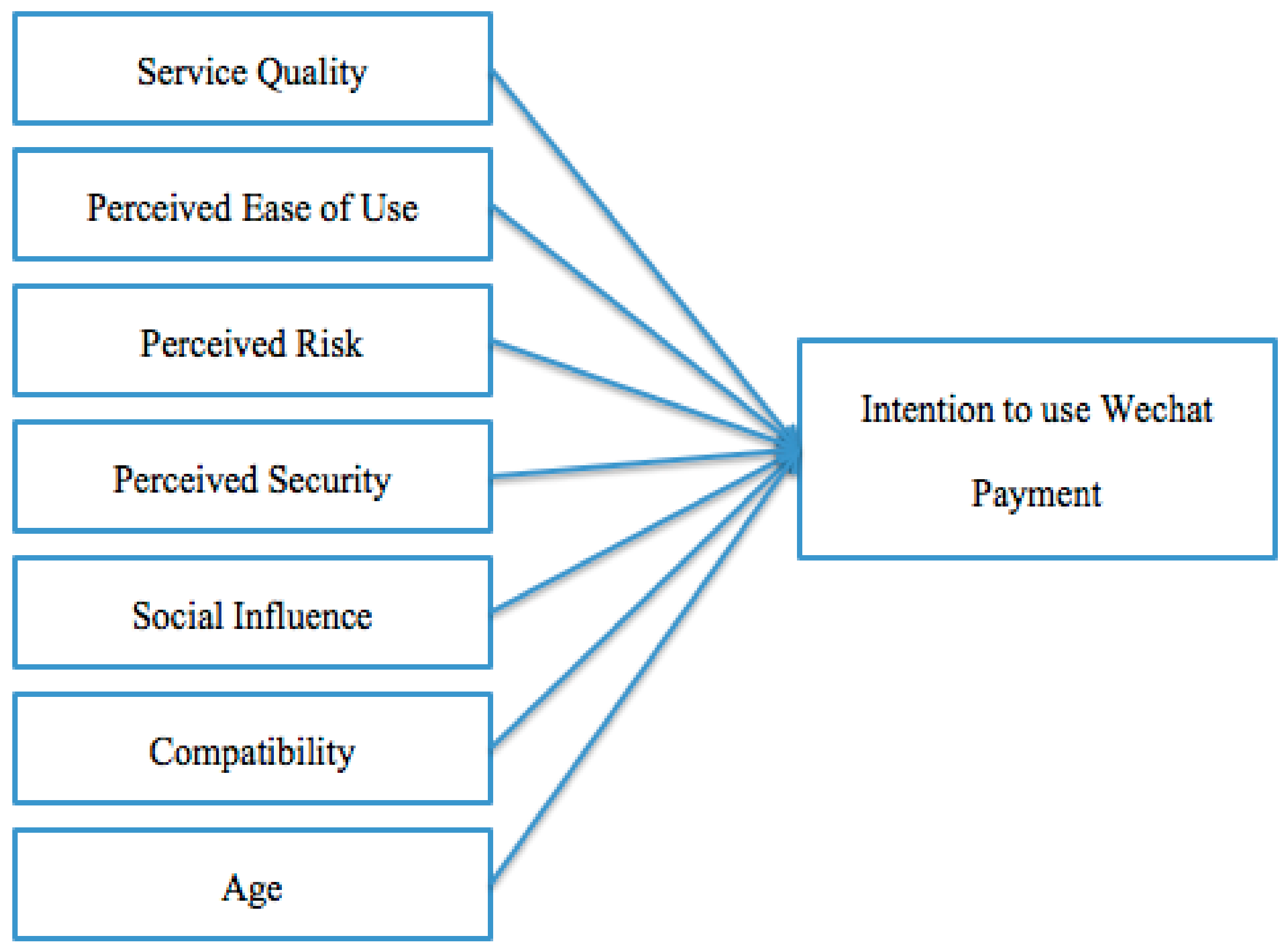

3.1. Conceptual Framework

3.2. Research Methodology

3.3. Questionnaire Development

3.4. Demographic Factors

3.5. Regression Model

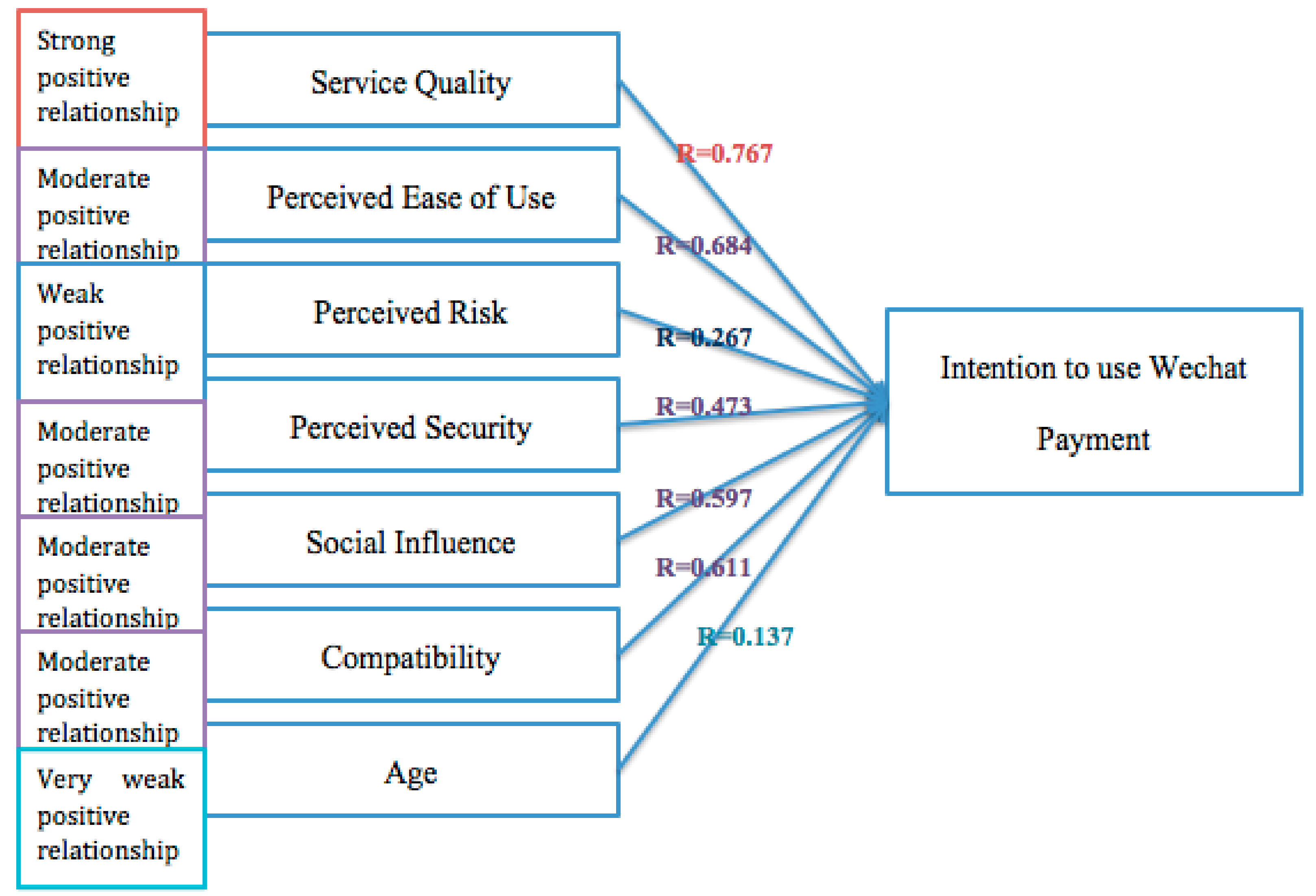

3.6. Correlation Analysis

4. Results and Analysis

4.1. Individual Interviews

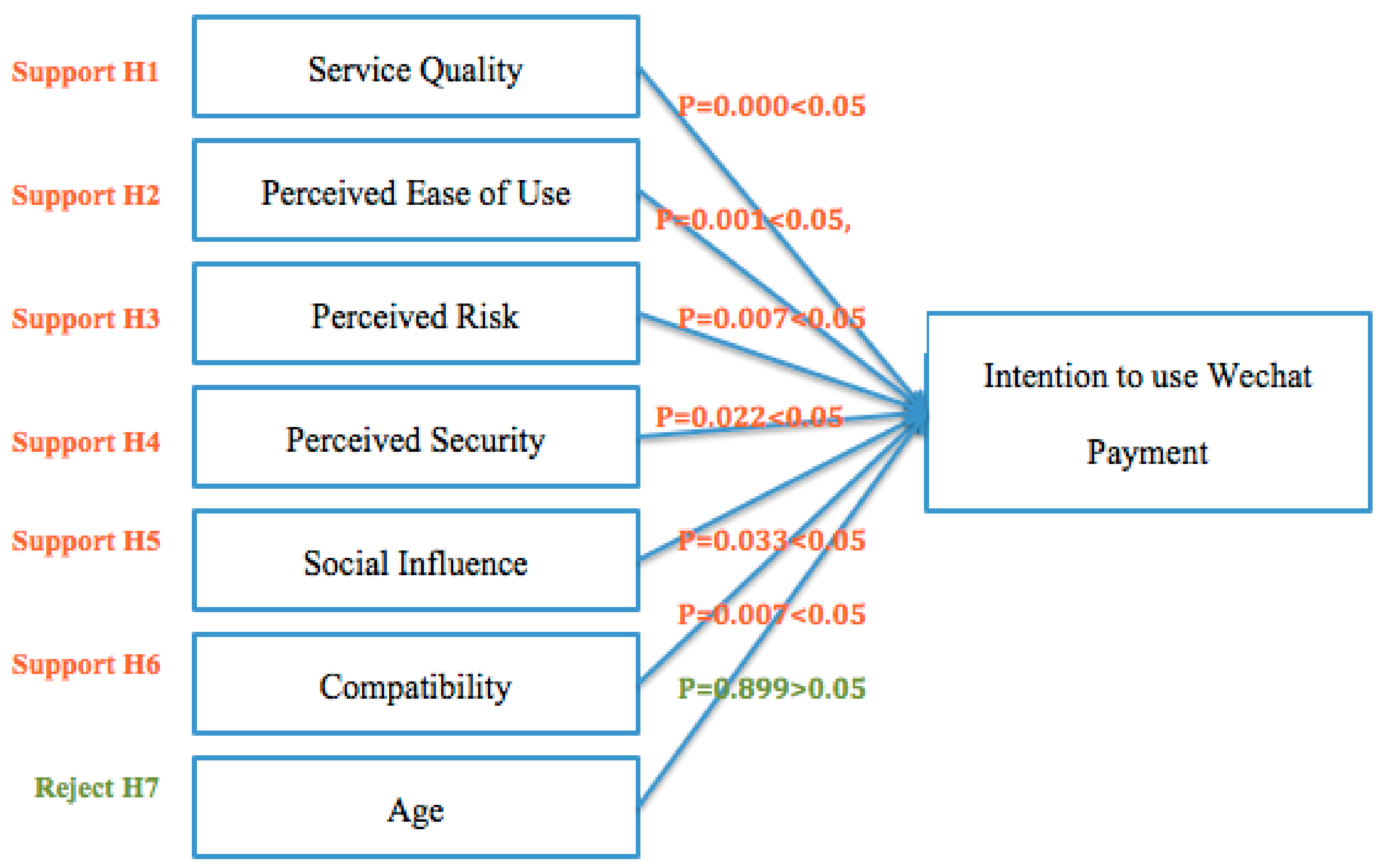

4.2. Regression Analysis

4.3. Service Quality

4.4. Perceived Ease of Use

4.5. Perceived Risk

4.6. Perceived Security

4.7. Social Influence

4.8. Compatibility

4.9. Age

4.10. One-Way ANOVA

5. Discussion

- Introduce an improved technical support system for mobile payment. The technical support system should consist of technologies for identification authentication, identity management, and secure protection of other information. These technologies collectively operate on the platform to ensure the security of trade information and user information.

- Inform users of the system about the importance of data and information. This will ensure that they update the system to prevent any security issues.

6. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Lerner, J.; Tufano, P. The Consequences of Financial Innovation: A Counterfactual Research Agenda. Annu. Rev. Financ. Econ. 2011, 3, 41–85. [Google Scholar] [CrossRef]

- Oyelami, L.O.; Adebiyi, S.O.; Adekunle, B.S. Electronic payment adoption and consumers’ spending growth: Empirical evidence from Nigeria. Futur. Bus. J. 2020, 6, 1–14. [Google Scholar] [CrossRef]

- Giudici, P. Fintech Risk Management: A Research Challenge for Artificial Intelligence in Finance. Front. Artif. Intell. 2018, 1, 1. [Google Scholar] [CrossRef] [PubMed]

- Alt, R.; Beck, R.; Smits, M.T. FinTech and the transformation of the financial industry. Electron. Mark. 2018, 28, 235–243. [Google Scholar] [CrossRef]

- Krivosheya, E.; Belyakova, P. Financial innovations role in consumer behavior at Russian retail pay-ments market. In Proceedings of the Economics and Finance Conferences (No. 9511955), Dubrovnik, Croatia, 27–30 August 2019; International Institute of Social and Economic Sciences: London, UK, 2019. [Google Scholar]

- Ozili, P.K. Impact of digital finance on financial inclusion and stability. Borsa Istanb. Rev. 2018, 18, 329–340. [Google Scholar] [CrossRef]

- Yao, M.; Di, H.; Zheng, X.; Xu, X. Impact of payment technology innovations on the traditional financial industry: A focus on China. Technol. Forecast. Soc. Chang. 2018, 135, 199–207. [Google Scholar] [CrossRef]

- The European Payments Landscape in Perspective—Emerging Payments UK. Emergingpayments.org. 2020. Available online: https://www.emergingpayments.org/whitepaper/the-european-payments-landscape-in-perspective/ (accessed on 1 January 2020).

- Statista. Digital Payments Report 2020. Available online: https://www.statista.com/study/41122/fintech-report-digital-payments/ (accessed on 1 January 2021).

- Bezovski, Z. The future of the mobile payment as electronic payment system. Eur. J. Bus. Manag. 2016, 8, 127–132. [Google Scholar]

- Lien, C.H.; Cao, Y. Examining WeChat users’ motivations, trust, attitudes, and positive word-of-mouth: Evidence from China. Comput. Hum. Behav. 2014, 41, 104–111. [Google Scholar] [CrossRef]

- Liu, W.; He, X.; Zhang, P. Application of Red Envelopes—New Weapon of WeChat Payment. In Proceedings of the 2015 International Conference on Education, Management, Information and Medicine, Shenyang, China, 24–26 April 2015. [Google Scholar]

- Wang, Y.; Hahn, C.; Sutrave, K. Mobile payment security, threats, and challenges. In Proceedings of the 2016 Second International Conference on Mobile and Secure Services (MobiSecServ), Gainesville, FL, USA, 26–27 February 2016. [Google Scholar]

- IResearch. WeChat Payment Is Opened For M-Commerce Development. 2014. Available online: http://www.iresearchchina.com/views/5510.html (accessed on 10 October 2014).

- CAICT. 2019–2020 WeChat Employment Impact Report. 2020. Available online: http://www.caict.ac.cn/kxyj/qwfb/ztbg/202005/t20200514_281774.htm (accessed on 1 May 2020).

- Kow, Y.M.; Gui, X.; Cheng, W. Special digital monies: The design of alipay and wechat wallet for mobile payment practices in china. In Proceedings of the IFIP Conference on Human-Computer Interaction, Mumbai, India, 25–29 September 2017. [Google Scholar]

- Montag, C.; Becker, B.; Gan, C. The Multipurpose Application WeChat: A Review on Recent Research. Front. Psychol. 2018, 9, 2247. [Google Scholar] [CrossRef]

- Bollen, K.A.; Pearl, J. Eight Myths About Causality and Structural Equation Models. In Handbooks of Sociology and Social Research; Springer: Berlin/Heidelberg, Germany, 2013; pp. 301–328. [Google Scholar]

- Uyanık, G.K.; Güler, N. A Study on Multiple Linear Regression Analysis. Procedia Soc. Behav. Sci. 2013, 106, 234–240. [Google Scholar] [CrossRef]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Lu, J.; Wei, J.; Yu, C.-S.; Liu, C. How do post-usage factors and espoused cultural values impact mobile payment continuation? Behav. Inf. Technol. 2017, 36, 140–164. [Google Scholar] [CrossRef]

- Musa, A.; Khan, H.U.; AlShare, K.A. Factors influence consumers’ adoption of mobile payment devices in Qatar. Int. J. Mob. Commun. 2015, 13, 670. [Google Scholar] [CrossRef]

- Lin, R.; Xie, J. Understanding the Adoption of Third-Party on-Line Payment: An Empirical Study of User Acceptance of Alipay in China. 2014. Available online: http://urn.kb.se/resolve?urn=urn:nbn:se:hj:diva-24231 (accessed on 12 April 2021).

- Rust, R.T.; Oliver, R.L. Service Quality: New Directions in Theory and Practice; Sage Publications: Thousand Oaks, CA, USA, 1994. [Google Scholar]

- Cronin, J.J.; Taylor, S.A. Measuring Service Quality: A Reexamination and Extension. J. Mark. 1992, 56, 55. [Google Scholar] [CrossRef]

- Zeithaml, V.A. Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. J. Mark. 1988, 52, 2–22. [Google Scholar] [CrossRef]

- Zeithmal, V.A.; Parasuraman, A.; Berry, L.L. Delivering Quality Service: Balancing Customer Perceptions and Expectations; Free Press: New York, NY, USA, 1990. [Google Scholar]

- Zeithmal, V.A.; Bitner, M.J. Services Marketing: Integrating Customer Focus across the Firm; McGraw-Hill: New York, NY, USA, 2000. [Google Scholar]

- Grubor, A.; Salai, S.; Leković, B. Service quality as a factor of marketing competitiveness. Rom. Assoc. Econ. Univ. 2010, 273–281. [Google Scholar]

- Nitin, S.; Deshmukh, S.G.; Prem, V. Service Quality Models: A Review. Int. J. Qual. Reliab. Manag. 2005, 22, 913–949. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–339. [Google Scholar] [CrossRef]

- Moore, G.C.; Benbasat, I. Development of an Instrument to Measure the Perceptions of Adopting an Information Technology Innovation. Inf. Syst. Res. 1991, 2, 192–222. [Google Scholar] [CrossRef]

- Vijayasarathy, L.R. Predicting consumer intentions to use on-line shopping: The case for an augmented technology acceptance model. Inf. Manag. 2004, 41, 747–762. [Google Scholar] [CrossRef]

- Ramayah, T.; Aafaqi, B.; Jantan, M. Internet usage among students of institution of higher learning: The role of mo-tivational variables. In Proceedings of the 1st International Conference on Asian Academy of Applied Business Conference, Sabah, Malaysia, 10–12 July 2003. [Google Scholar]

- Trautman, L.J. E-Commerce, cyber, and electronic payment system risks: Lessons from PayPal. UC Davis Bus. LJ 2015, 16, 261. [Google Scholar]

- Luarn, P.; Lin, H.-H. Toward an understanding of the behavioral intention to use mobile banking. Comput. Hum. Behav. 2005, 21, 873–891. [Google Scholar] [CrossRef]

- IResearch. IResearh Wisdom: Date of Chinese Netizens Use Cell Phone Banking in 2009. [R/OL] (2009-09-16). 2009. Available online: http://www.iresearch.com.cn/html/consulting/online_payment/DetailNews_id_101315.html (accessed on 26 September 2009).

- Bauer, R.A. Consumer behavior as risk taking. In Dynamic Marketing for a Changing World; Hancock, R., Ed.; American Marketing Association: Chicago, IL, USA, 1960; pp. 389–398. [Google Scholar]

- Shin, D.-H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Zhang, H.; Li, H. Factors affecting payment choices in on-line auctions: A study of eBay traders. Decis. Support Syst. 2006, 42, 1076–1088. [Google Scholar] [CrossRef]

- Hernandez, J.M.C.; Mazzon, J.A. Adoption of internet banking: Proposition and implementation of an integrated methodology approach. Int. J. Bank Mark. 2007, 25, 72–88. [Google Scholar] [CrossRef]

- Chen, Y.H.; Barnes, S. Initial trust and on-line buyer behaviour. Ind. Manag. Data Syst. 2007, 107, 21–36. [Google Scholar] [CrossRef]

- Siau, K.; Sheng, H.; Nah, F.; Davis, S. A qualitative investigation on consumer trust in mobile commerce. Int. J. Electron. Bus. 2004, 2, 283. [Google Scholar] [CrossRef]

- Lwin, M.; Wirtz, J.; Williams, J.D. Consumer on-line privacy concerns and responses: A power-responsibility equilibrium perspective. J. Acad. Mark. Sci. 2007, 35, 572–585. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G. Davis User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425. [Google Scholar] [CrossRef]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to explain mobile banking user adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Hong, S.-J.; Tam, K.Y. Understanding the Adoption of Multipurpose Information Appliances: The Case of Mobile Data Services. Inf. Syst. Res. 2006, 17, 162–179. [Google Scholar] [CrossRef]

- Lu, J.; Yao, J.; Yu, C. Personal innovativeness, social influences and adoption of wireless Internet services via mo-bile technology. J. Strateg. Inf. Syst. 2005, 14, 245–268. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 4th ed.; Free Press: New York, NY, USA, 1995. [Google Scholar]

- Bao, Y.; Zhou, K.Z.; Su, C. Face consciousness and risk aversion: Do they affect consumer decision-making? Psychol. Mark. 2003, 20, 733–755. [Google Scholar] [CrossRef]

- Tornatzky, L.G.; Klein, K.J. Innovation characteristics and innovation adoption- implementation: A me-ta-analysis of findings. IEEE Trans. Eng. Manag. 1982, 29, 28–45. [Google Scholar] [CrossRef]

- Lee, M.S.Y.; McGoldrick, P.J.; Keeling, K.A.; Doherty, J. Using ZMET to explore barriers to the adoption of 3G mo-bile banking services. Int. J. Retail Distrib. Manag. 2003, 31, 340–348. [Google Scholar] [CrossRef]

- Wu, J.-H.; Wang, S.-C. What drives mobile commerce? An empirical evaluation of the revised technology acceptance model. Inf. Manag. 2005, 42, 719–729. [Google Scholar] [CrossRef]

- Chen, L. A model of consumer acceptance of mobile payment. Int. J. Mob. Commun. 2008, 1, 32–52. [Google Scholar] [CrossRef]

- Arning, K.; Ziefle, M. Understanding age differences in PDA acceptance and performance. Comput. Hum. Behav. 2007, 23, 2904–2927. [Google Scholar] [CrossRef]

- Phang, C.; Sutanto, J.; Kankanhalli, A.; Li, Y.; Tan, B.; Teo, H.-H. Senior Citizens’ Acceptance of Information Systems: A Study in the Context of e-Government Services. IEEE Trans. Eng. Manag. 2006, 53, 555–569. [Google Scholar] [CrossRef]

- Dean, D.H. Shopper age and the use of self-service technologies. Manag. Serv. Qual. Int. J. 2008, 18, 225–238. [Google Scholar] [CrossRef]

- Mensah, I.K. Predictors of the Continued Adoption of WECHAT Mobile Payment. Int. J. E-Business Res. 2019, 15, 1–23. [Google Scholar] [CrossRef]

- Abrahão, R.D.S.; Moriguchi, S.N.; Andrade, D.F. Intention of adoption of mobile payment: An analysis in the light of the Unified Theory of Acceptance and Use of Technology (UTAUT). Rev. Adm. Innov. RAI 2016, 13, 221–230. [Google Scholar] [CrossRef]

- Kim, H.K.; Lee, M. Factors associated with health services utilization between the years 2010 and 2012 in Korea: Using Andersen’s behavioral model. Osong Public Health Res. Perspect. 2016, 7, 18–25. [Google Scholar] [CrossRef]

- Buhrmester, M.; Kwang, T.; Gosling, S.D. Amazon’s Mechanical Turk: A new source of inexpensive, yet high-quality data? Perspect. Psychol. Sci. 2016, 6, 3–5. [Google Scholar] [CrossRef]

- DiCicco-Bloom, B.; Crabtree, B.F. The qualitative research interview. Med. Educ. 2006, 40, 314–321. [Google Scholar] [CrossRef]

- Nykvist, R.; Stalfors, P. Consumer Acceptance of Mobile Payment Services. Bachelor’s Thesis, Handelshögskolan Vidgöteborgs Universitet, Göteborg, Sweden, 2011. [Google Scholar]

- Zheng, H.M.; Chen, G.S. How Has the Third Party Reduced the Perceived Risk of Young Consumers in China? School of Sustainability Development of Society and Technology, Mälardalen University: Västerås, Sweden, 2012; pp. 18–25. [Google Scholar]

- Kurnia, S.; Smith, S.P.; Lee, H. Consumers’ perception of mobile internet in Australia. E-Bus. Rev. 2006, 5, 19–32. [Google Scholar]

- Draper, N.R.; Smith, H. Applied Regression Analysis; John Wiley & Sons: Hoboken, NJ, USA, 1996; Volume 326. [Google Scholar]

- Zhou, W. Correlation Analysis: From Computational Hardness to Practical Success. Ph.D. Thesis, Graduate School, Rutgers University, Newark, NJ, USA, 2011. [Google Scholar]

- Venkatesh, V. Determinants of Perceived Ease of Use: Integrating Control, Intrinsic Motivation, and Emotion into the Technology Acceptance Model. Inf. Syst. Res. 2000, 11, 342–365. [Google Scholar] [CrossRef]

- Pagani, M.; Schipani, D. Motivations and barriers to the adoption of 3G mobile multimedia services. In E-Commerce and M-Commerce Technologies; Deans, P.C., Ed.; Idea Group: Hershey, PA, USA, 2005; pp. 80–95. [Google Scholar]

- Oliveira, T.; Manoj, T.; Goncalo, B.; Filipe, C. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Wu, R.; Lee, J. The Comparative Study on Third Party Mobile Payment Between UTAUT2 and TTF. J. Distrib. Sci. 2017, 15, 5–19. [Google Scholar] [CrossRef]

- Chen, Y.-F.; Lan, Y.-C. An empirical study of the factors affecting mobile shopping in Taiwan. In Mobile Commerce: Concepts, Methodologies, Tools, and Applications; IGI Global: Hershey, PA, USA, 2018; pp. 1329–1340. [Google Scholar]

- Bhimasta, R.A.; Suprapto, B. What Drives Young Indonesian’S Intention to Use Mobile Payment? A Case of T-Cash. Adv. Sci. Lett. 2018, 24, 4802–4805. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Shankar, A.; Datta, B. Factors Affecting Mobile Payment Adoption Intention: An Indian Perspective. Glob. Bus. Rev. 2018, 19, S72–S89. [Google Scholar] [CrossRef]

- Acheampong, P.; Li, Z.W.; Kamal, K.H.; Obobisa, E.S.; Frank, B.; Isaac, A.B. Examining the intervening role of age and gender on mobile payment acceptance in Ghana: UTAUT model. Can. J. Appl. Sci. Technol. 2018, 5, 2. [Google Scholar]

- Sobti, N. Impact of demonetization on diffusion of mobile payment service in India: Antecedents of behavioral in-tention and adoption using extended UTAUT model. J. Adv. Manag. Res. 2019, 16. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| 1. Have you ever used Wechat online payment platform before? 2. Which factors will influence you to use it? 3. How do you think about the Wechat online payment platform? Do you think it provides a convenient lifestyle? 4. Are there any improvements that WeChat online payment platform needs to pay attention to? 5. Do you think age could be an important factor that influences people in adopting the Wechat online payment platform? |

| Screening Question | Have you ever used Wechat online Payment before? |

| Yes | |

| No, and why: a. Do not know how to operate the third-party online payment platforms; b. Do not trust it; c. Never shopping online; d. Others. | |

| Service Quality | 1. The Wechat online payment platform can always satisfy my daily transactions |

| 2. The Wechat online payment platform can save my time whereas improving transaction efficiency | |

| 3. I would choose Wechat online payment platform with a better layout design | |

| Perceived Ease of Use | 4. I deem that the Wechat online payment platform is easy to operate |

| 5. I would like to use the WeChat online payment platform if it is not complicated. | |

| Perceived Risk | 6. I am worried about the perceived risks of the Wechat online payment platform |

| 7. The Wechat online payment platform has ample operation functions that could reduce my perceived risks | |

| 8. The Wechat online payment platform’s ability to efficiently communicate with customers could reduce my perceived risks | |

| Perceived Security | 9. I am worried about the possibility of information leakage when using Wechat online payment platform |

| 10. I deem that the Wechat online payment platform is secure | |

| Social Influence | 11. I am more willing to accept the Wechat online payment platform when people around me have already adopted it |

| 12. The Wechat online payment platform is the leading brand in the industry which can stimulate me to adopt it | |

| Age | 13. I deem that Wechat online payment platform is a kind of technology innovation representing the outcome of current lifestyles and changes in users’ value system |

| 14. I deem that elder people are reluctant to accept the Wechat online payment platform | |

| Compatibility | 15. I enjoy making purchases through Wechat online payment platform |

| 16. I believe it is a good idea to use Wechat online payment platform for making payments | |

| Intention to Use | 17. I intend to use Wechat online payment platform more frequently |

| 18. I would like to recommend it to relatives or friends | |

| Gender | Male or Female |

| Age | 18, 18–25, 26–30, 31–40, 41–50, 51–60 |

| Education Level | Doctorate; Master; Bachelor; High Diploma/Associate Diploma; Secondary School or below |

| Occupation | Student in engineering department; Student in other areas; Engineering; Others |

| Respondent | Gender | Age | Influential Factors | Things to Improve | Age Is a Problem to Adopt Payment Platform |

|---|---|---|---|---|---|

| 1 | Female | 23 | Social influence Ease to use Habits | Needs to respond quickly to the market Need to develop own features that others cannot replicate | Yes |

| 2 | Female | 28 | Service quality Social image | Needs to be more professional | Yes |

| 3 | Male | 38 | Service quality Convenience | Unable to clear currency in different countries, needs to solve the problem | Yes |

| 4 | Male | 43 | Convenience Originality | Pay more attention to developing key functions | Yes |

| 5 | Male | 49 | Ease of use Social image | N/A | Probably |

| Frequency | Percentage | ||

|---|---|---|---|

| Gender | Male | 53 | 32.9 |

| Female | 108 | 67.1 | |

| Age group | 18–25 | 113 | 70.2 |

| 26–30 | 32 | 19.9 | |

| 31–40 | 8 | 4.9 | |

| 41–50 | 8 | 4.9 | |

| Education level | Doctorate | 4 | 2.0 |

| Master | 92 | 57 | |

| Bachelor | 55 | 34 | |

| High Diploma/Associate Degree | 8 | 5 | |

| Secondary School or Below | 2 | 2.0 |

| Predictors | R | R Square | Adjusted R Square | Std. Error of the Estimate |

|---|---|---|---|---|

| Values | 0.824 a | 0.679 | 0.667 | 0.51969 |

| Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|

| Regression | 111.732 | 7 | 15.962 | 59.099 | 0.000 |

| Residual | 52.936 | 196 | 0.270 | ||

| Total | 164.668 | 203 |

| Unstandardized Coefficients | Standardized Coefficients | ||||

|---|---|---|---|---|---|

| B | Std. Error | Beta | t | Sig. | |

| (Constant) | 0.095 | 0.227 | 0.417 | 0.677 | |

| Service Quality | 0.514 | 0.070 | 0.481 | 7.354 | 0.000 |

| Perceived Ease of Use | 0.242 | 0.069 | 0.237 | 3.506 | 0.001 |

| Perceived Risk | −0.182 | 0.067 | −0.144 | −2.726 | 0.007 |

| Perceived Security | 0.244 | 0.086 | 0.162 | 2.835 | 0.022 |

| Social Influence | 0.125 | 0.058 | 0.133 | 2.145 | 0.033 |

| Compatibility | 0.154 | 0.056 | 0.171 | 2.741 | 0.007 |

| AGE | 0.005 | 0.041 | 0.006 | 0.127 | 0.899 |

| Construct | Cronbach’s Alpha | AVE |

|---|---|---|

| Service quality | 0.768 | 0.726 |

| Perceived ease of use | 0.767 | 0.525 |

| Perceived risk | 0.524 | 0.707 |

| Perceived security | 0.740 | 0.718 |

| Social influence | 0.807 | 0.638 |

| Compatibility | 0.505 | 0.671 |

| Age | 0.470 | 0.736 |

| Sum of Squares | df | Mean Square | F | Sig. | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Gender | Age | Gender | Age | Gender | Age | Gender | Age | Gender | Age | |

| Between Groups | 0.885 | 8.299 | 1 | 3 | 0.885 | 2.766 | 1.091 | 3.538 | 0.297 | 0.016 |

| Within Groups | 163.783 | 156.369 | 202 | 200 | 0.811 | 0.782 | ||||

| Total | 164.668 | 164.668 | 203 | 203 | ||||||

| Age (I) | Age (J) | Mean Difference (I–J) | Std. Error | Sig. |

|---|---|---|---|---|

| 18–25 | 26–30 | 0.160 | 0.172 | 0.351 |

| 31–40 | −0.902 * | 0.321 | 0.005 | |

| 41–50 | 0.348 | 0.321 | 0.279 | |

| 26–30 | 18–25 | −0.160 | 0.171 | 0.351 |

| 31–40 | −1.062 * | 0.350 | 0.003 | |

| 41–50 | 0.188 | 0.350 | 0.592 | |

| 31–40 | 18–25 | 0.902 * | 0.321 | 0.005 |

| 26–30 | 1.063 * | 0.350 | 0.003 | |

| 41–50 | 1.250 * | 0.442 | 0.005 | |

| 41–50 | 18–25 | −0.348 | 0.321 | 0.279 |

| 26–30 | −0.188 | 0.350 | 0.592 | |

| 31–40 | −1.250 * | 0.442 | 0.005 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tang, Y.M.; Chau, K.Y.; Hong, L.; Ip, Y.K.; Yan, W. Financial Innovation in Digital Payment with WeChat towards Electronic Business Success. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1844-1861. https://doi.org/10.3390/jtaer16050103

Tang YM, Chau KY, Hong L, Ip YK, Yan W. Financial Innovation in Digital Payment with WeChat towards Electronic Business Success. Journal of Theoretical and Applied Electronic Commerce Research. 2021; 16(5):1844-1861. https://doi.org/10.3390/jtaer16050103

Chicago/Turabian StyleTang, Yuk Ming, Ka Yin Chau, Luchen Hong, Yun Kit Ip, and Wan Yan. 2021. "Financial Innovation in Digital Payment with WeChat towards Electronic Business Success" Journal of Theoretical and Applied Electronic Commerce Research 16, no. 5: 1844-1861. https://doi.org/10.3390/jtaer16050103

APA StyleTang, Y. M., Chau, K. Y., Hong, L., Ip, Y. K., & Yan, W. (2021). Financial Innovation in Digital Payment with WeChat towards Electronic Business Success. Journal of Theoretical and Applied Electronic Commerce Research, 16(5), 1844-1861. https://doi.org/10.3390/jtaer16050103