1. Introduction

The organizations that are part of the social economy are essential agents to carry out environmental and business sustainability plans at a global level. This assertion is supported by opinions not only from supranational institutions such as the one issued in 2015 by the United Nations but also by various publications that stress the same argument [

1,

2]. In the proximity ecosystems, sustainability plays an even more important role in development, and it is there where the social economy entities occupy a privileged place.

Rural and marine environments have the greatest impact on the communities in their environment, influencing the configuration of social networks and economic contacts. Not only because they balance the use of natural communal resources, aligned with the works of the Nobel Prize winner Elionor Ostrom [

3], but also because they are consubstantial with the survival and the social well-being of the communities. The positive impact of social economy companies for the sustainability of the territories has been the subject of attention by various specialists [

4,

5], currently being one of the most controversial topics in the advances in the knowledge of social economy from an academic and scientific perspective.

Decision making must be done through the verification of results that can be evaluated, and, even more, quantified. However, so far there are not enough indicators to perform quantitative approaches on the organizational performance of these entities with regard to sustainability. In recent years, a considerable effort has been made in various national and international spheres in the search for models that allow a standardized evaluation of the environmental, social, and sustainability actions carried out by organizations. The combination of the objectives of sustainability and the creation of social benefit requires entities to work in a more strategic way. On the other hand, society requires that economic organizations become humanized, satisfying the needs of citizens.

This work studies two social economy entities that can be a reference to channel strategies to the 2030 SDGs. An Agrarian Transformation Society (SAT), a hybrid associative business model in what refers to its corporate structure between a cooperative and the mercantile company [

6,

7] and a fishermen’s guild. Both carry out their productive activity in the Canary Islands and they are closely linked to the agricultural and marine environments in which they operate. The choice of both entities was not arbitrary. Until the mid-nineteenth century fishing and agrarian activity represented the main growth engines of the Canary archipelago before the arrival of tourism and port activity. The selection of entities responds to the need to show two examples that meet one of the fundamental requirements in the decalogue of the social economy: proximity. The proximity to consumers, partners, and workers who are part of companies.

In this way, the local aspect appears as a sign of identity and it is oversized by linking the productive activity with improving people’s income and quality of life. The feeling of belonging to a community beyond the business organization implies emotional ties that can be quantified, as it will be seen throughout this work. This study emphasizes the importance of monetizing the social value of organizations and their connection with the ethical dimension, as well as with strategic decision-making for sustainability. All this has repercussions on local communities, on the environment, on public administrations, on interest groups, on families, on employment, and even on basic citizen income. The Social Accounting system allows organizations to communicate their contributions and achievements in sustainability. Its integration into the business strategy makes it easier for organizations to make decisions to advance in the deployment and achievement of the 2030 SDGs.

This work has been structured as follows. First, we contextualize the links between the SDGs and the social economy from a theoretical point of view, emphasizing the two entities that are the object of the analysis. We then evaluate the system of sustainable development indicators, to finally enter the empirical study of the research quantifying the contribution of each entity social accounting value variables to the SDGs. We finally provide the conclusions and future lines of research.

4. Methodology

In this work, the SPOLY model [

85] is used as a framework to make visible and measure the contribution of the SAT and the Guild to the SDGs. It is a specific model of Social Accounting [

86], which complements and expands the accounting information system, both in the nature of the value considered and in the interest groups contemplated. It is characterized by objectifying in a single monetary measure the economic and social value attributable to management, the integrated social value or blended value [

87], and satisfying the information demands of stakeholders [

88].

In the field of social economy, this accounting information system has been used to propose specific metrics of the socio-economic impact of various families of entities of a social nature, such as cooperatives [

89], foundations and other non-profit organizations [

90]. Within the research carried out in this field, the relationship between the value variables generated by organizations and the SDGs is still in a very early stage, with hardly any studies addressing it.

The SPOLY model is developed based on a cost-benefit analysis [

91] and the following four methodological hypotheses:

- (i)

a participatory action research process [

92], characterized by the combination of theory and practice and which involves solving a problem from the participatory construction of new knowledge,

- (ii)

an approach to the concept of social value from the theory of stakeholders [

87], which enables the social value that an entity generates to those who participate and are affected by its activity to be specified,

- (iii)

the phenomenological paradigm [

93,

94,

95], which involves considering social value as a construct elaborated subjectively by the stakeholders who are recipients of said value, and

- (iv)

the hypothesis of fuzzy logic [

96,

97], which makes it possible to monetize social value by making use of instruments typical of fuzzy set systems, such as similarity as an allocation criterion between the two sets of mental objects or the application of the criterion [

98] for value selection.

The blended value in this model is made up of two components, the social market value and the specific or non-market social value. The first of them collect the social value that the organization generates with the performance of its economic activity, transfers it as a counterpart to a real market price. This value includes generated and distributed value both directly [

85] and indirectly—through input purchases [

91]. For the determination of this first component of the integrated social value, metrics are used in relation to outcomes (direct and indirect), common to all organizations. The specific or non-market social value is the value transferred by the organization to its stakeholders without a counterpart to the real market price.

For the quantification of the integrated social value, a standardized procedure [

85] consisting of four stages is followed. First, a working team is formed, made up of external experts and members of the organizations involved. Subsequently, the entity’s interest groups are identified—the individuals or groups that receive some type of value generated by the organization, monetary or not. In the third stage, the variables of perceived value are identified, establishing the ways in which the organization creates value for its stakeholders. In accordance with the phenomenological perspective, this analysis is carried out through in-depth interviews. The analytical structuring of the information collected in these interviews, after having triangulated it with the internal and external documents of the organization, is carried out by delimiting thematic areas of perceived value. This is done by integrating synonymous, related, or strongly similar expressions-, expressing them in terms of third, and reformulating them in scientific language [

99]. The fourth stage involves quantifying and monetizing the value variables found, identifying the organization’s outputs linked to the value variables, selecting the proxies—attention to the socio-temporal context in which the outputs are generated—, and using the formula o the corresponding algorithm [

86].

The SPOLY model of Social Accounting is an especially appropriate system to evaluate the contribution of SATs and fishermen’s guild to the SDGs. The subjective approach for objectifying the social value on which it is based, being conceptually aligned with the philosophy of sustainability, allows, through a standardized and scientifically based process, the identification of stakeholders, the analysis of their interests and perceptions, and the approach of indicators of social sustainability for the organization—in whose design the stakeholders themselves intervene. This model guarantees compliance with the criteria of the relevance of the indicator, transparency, stakeholder participation, soundness, and methodological rigor. However, its limitations must be taken into account. In particular, the subjectivity and discretion present in the process, together with the fact that it is still in a developing phase. That implies that there are insufficiently standardized methodological aspects and conditions the applicability of the results to a certain organization at a specific moment in time. Additionally, comparability between organizations is not possible when their characteristics are not similar.

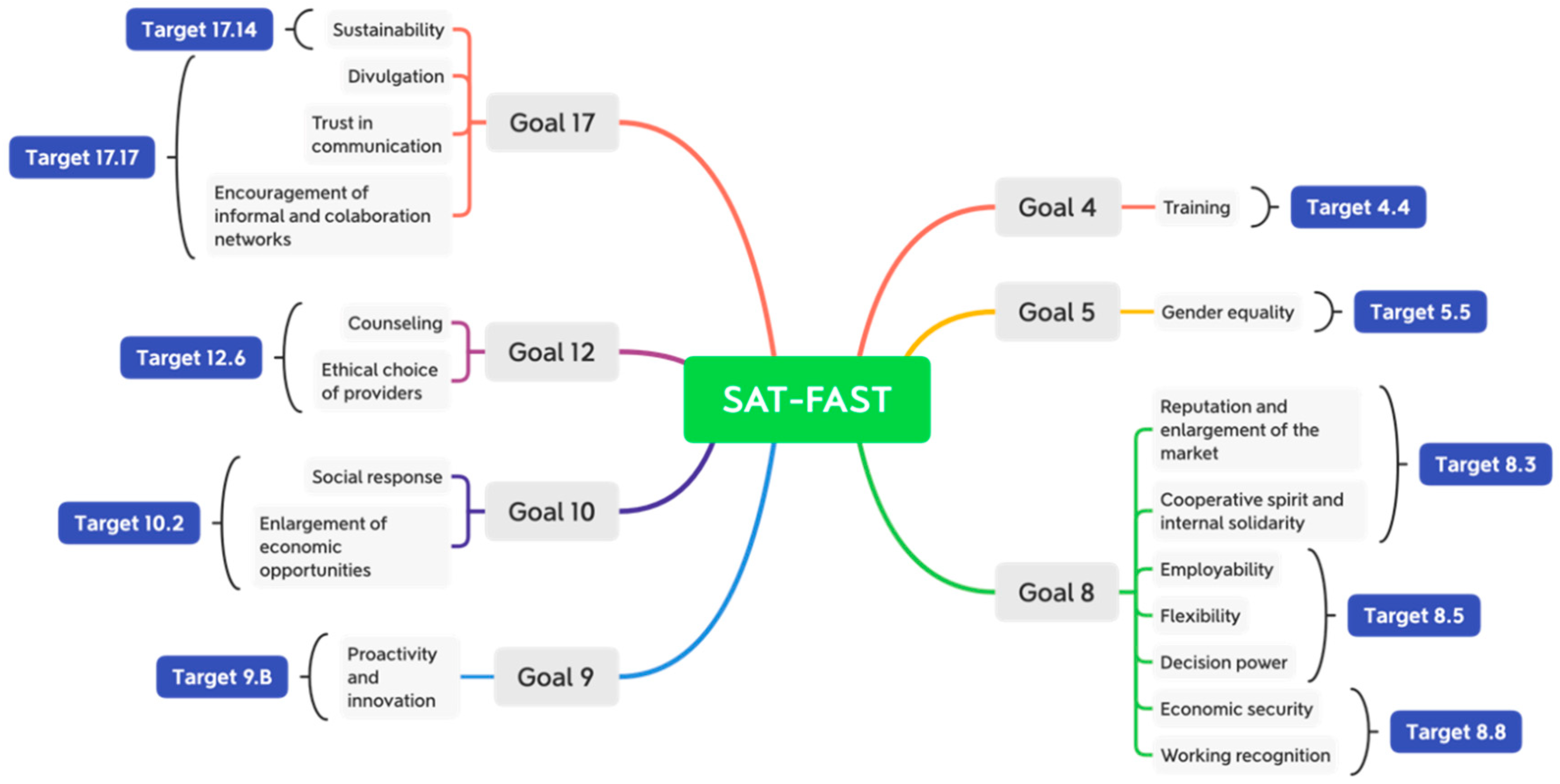

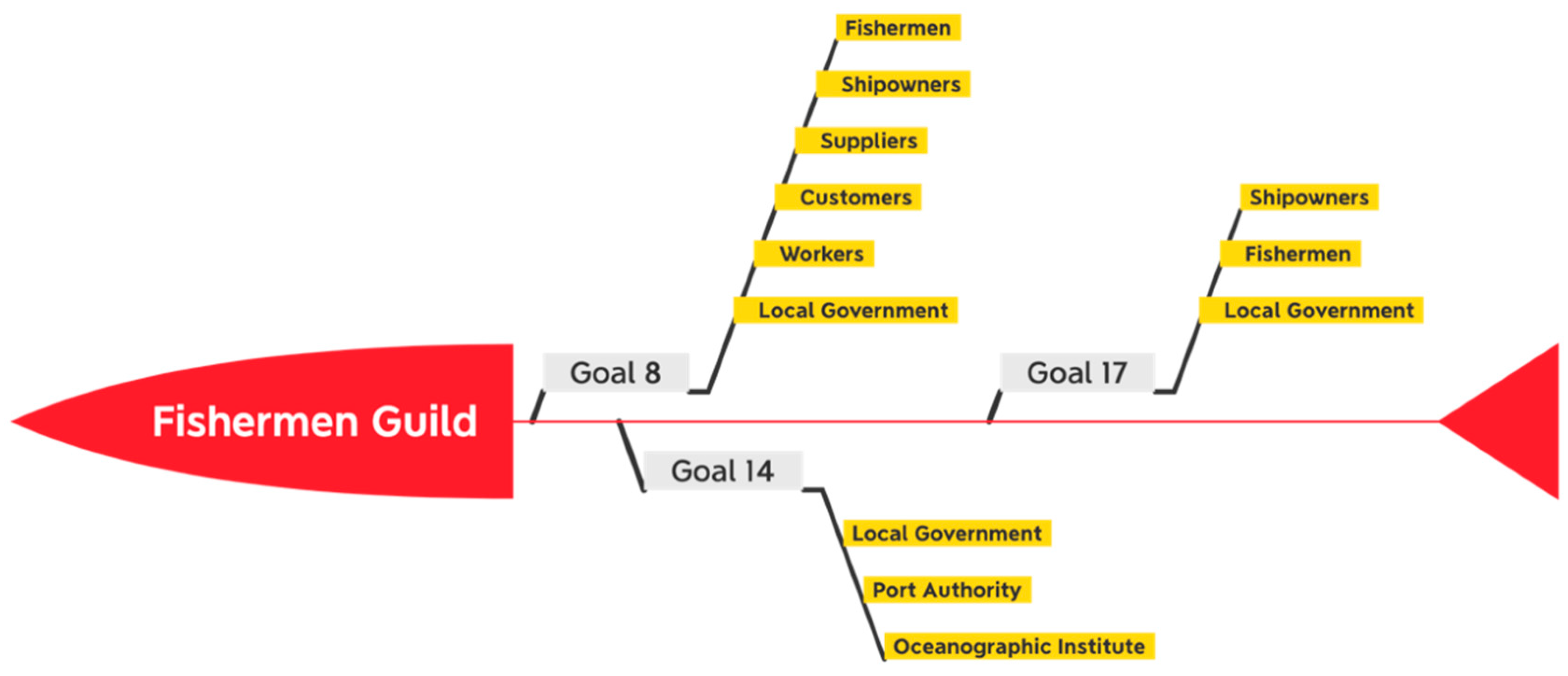

To determine the contribution of each of the study entities to the SDGs, we start with the variables of the social value of non-market identified for the guild [

100] and the SAT [

101]. This option has been chosen to estimate considering that this component of blended value reflects the qualitative differences between organizations. Subsequently, each variable is included in the SDGs and, where appropriate, in the corresponding target, taking into account the nature of the variable itself. The quantification in monetary terms of the value variables in the two aforementioned studies allows us to express in this same unit of measurement the contribution to the SDGs of each of the entities, both in absolute values and in percentage. Finally, the relationship of value variables with the stakeholders is taken into account to show the contribution to the SDGs, taking the stakeholders as the center. Throughout the analysis, a comparison will be made between both entities to expose the similarities and differences between them.

6. Discussion

The use of the results extracted from Social Accounting in the framework of the SDG allows the generation of an information system on the effective contribution that the activities of the different entities have on sustainability. Throughout this article, the importance of the monetization of the social value of organizations for strategic decision-making in the ethical and sustainability fields has been highlighted. Its integration into the business strategy will make it easier for organizations to make decisions to take action towards achieving the 2030 SDGs.

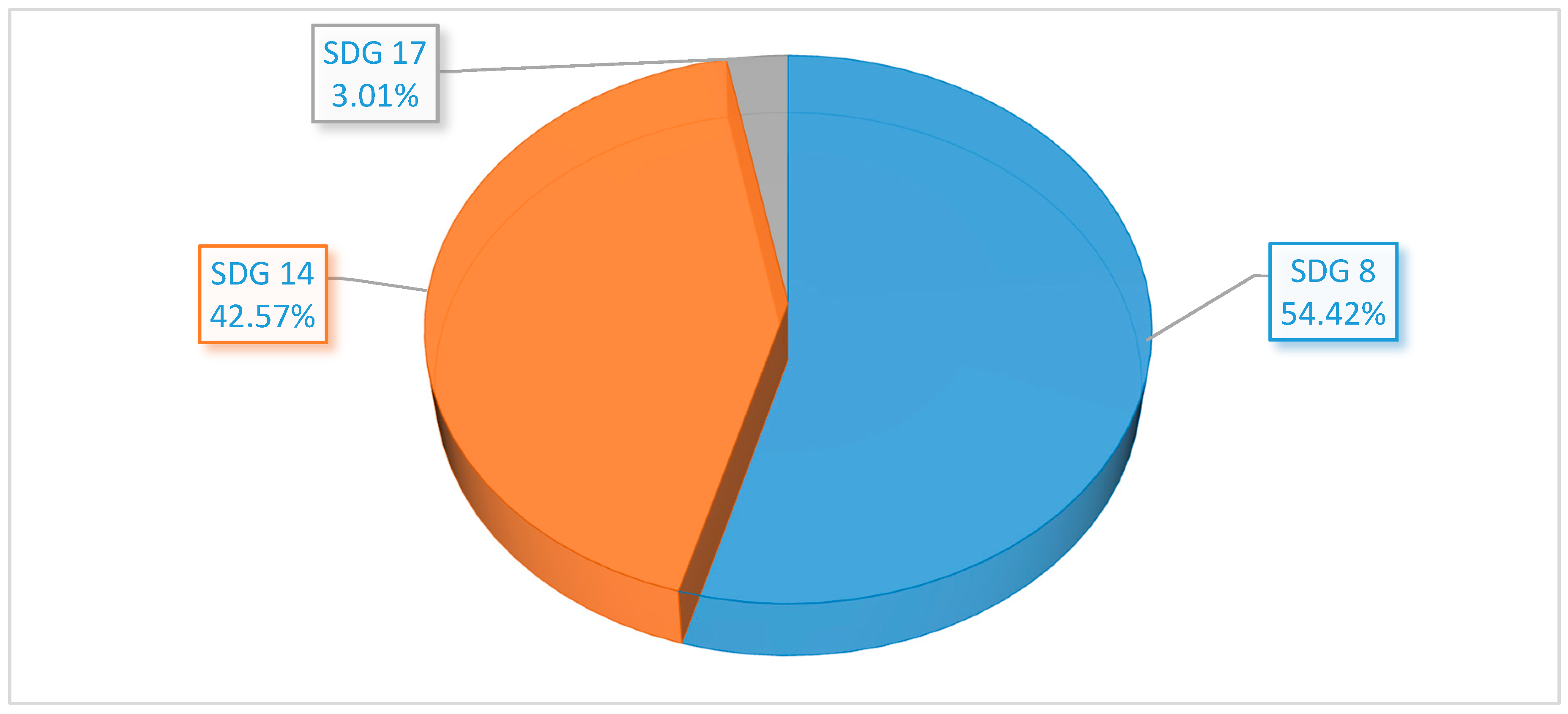

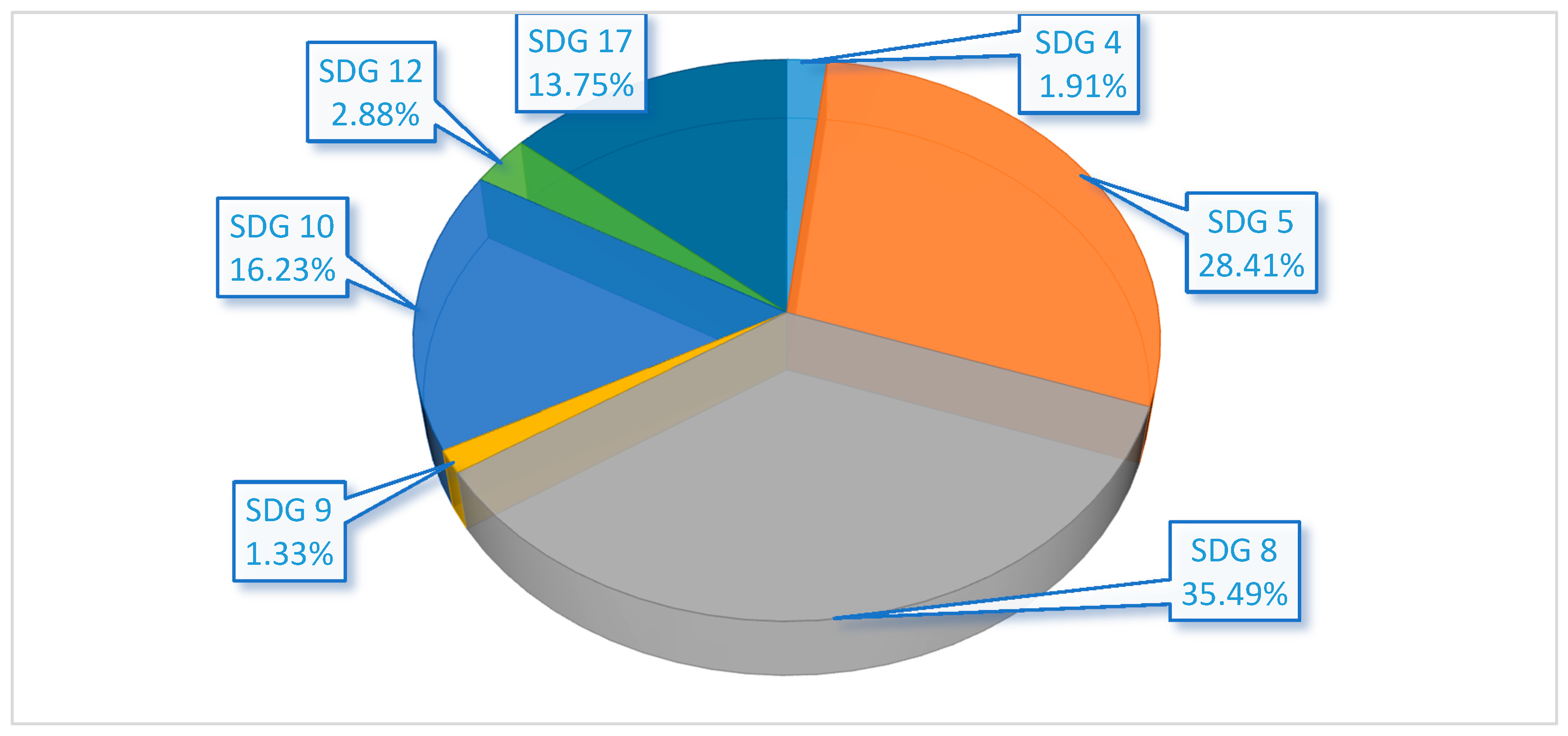

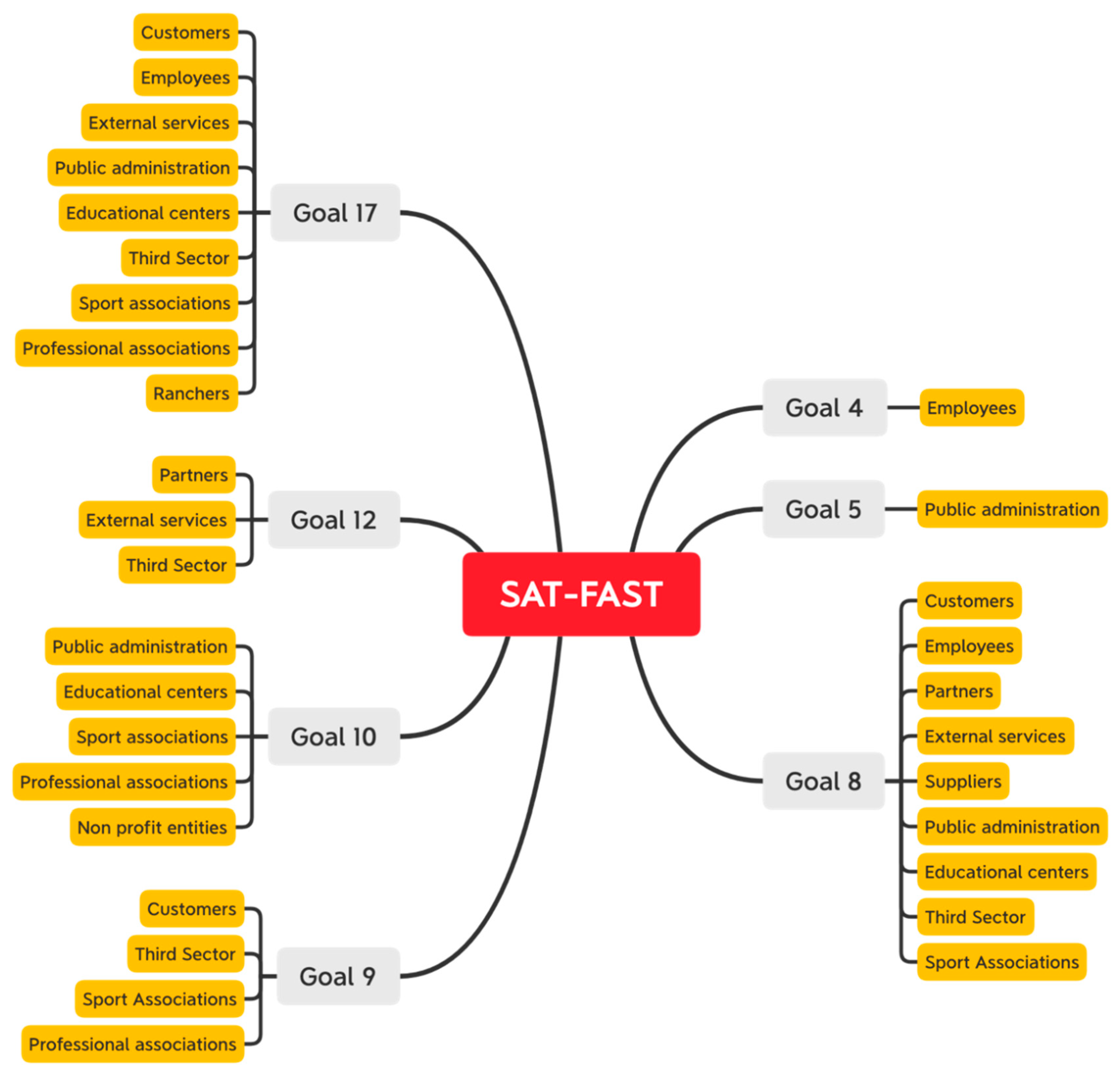

The contribution of both the fishermen’s guild and the SAT to the SDGs focuses, above all, on Goal 8, which is related to economic growth and quality employment. It is precisely this last factor, employment, where this type of entity seems to have a greater impact. However, the variables that bear this impact are of a different nature, since in the case of the SAT they are much more focused on workers, while in the case of the guild it is more related to the services it provides to its members.

The principles of Social Economy that govern the organizations analyzed are reflected in their contribution to the SDGs. On the guild’ side, the input to the sector in which it carries out its activity is reflected in the weight of Goal 14. On the other side, the greater size and diversity of SAT activities translates into a strong contribution to Goal 17, aimed at the creation of alliances for sustainability. The importance of cooperative nature is also reaffirmed with the contribution to Goal 12, which shows the influence that SAT can have throughout its value chain with the expansion of sustainability policies.

At this point, it should be noted that the fact that SAT has been the pioneer in undergoing the process of monetization of the social value that it generates to its stakeholders, enhances its role as a benchmark among its associations. This carries a positive driving effect in similar entities or others with which it is related so that these organizations could decide to monetize the generation of their social value.

The size of the organization, its contact networks, and the sustainability policies implemented can be considered as factors that decisively influence the contribution that each entity makes to the SDGs. In the case of the guild, this impact is more noticeable in the economic sector where it operates. In the case of the SAT, there is a greater influence of the size and diversity of activities, which translates into a greater variety of SDGs to which it contributes.

One of the fundamental arguments of Social Accounting is that the stakeholders are in charge of evaluating the activities of each entity, which means reverting the traditional concept of Corporate Social Responsibility whose focus is more focused on the organization. One of the most innovative contributions made by the study is to draw a map of the relationship between the impact produced in the SDG and the perception of stakeholders. The distribution of these with respect to the SDGs follows a structure similar to that of the economic value provided by companies. Thus, in both the guild and the SAT, most of them focus on Goal 8, although Goal 17 is highly relevant.

Knowing this information can be very useful for entities from a strategic point of view, not only to adapt their activities based on the perceptions that different stakeholders have but also in terms of communication. From a legal point of view, the information extracted can be used to comply with the requirements of non-financial information that European Directive 2014/95/EU regulates and that in Spain has been transposed into Law 11/2018, of 28 of December, amending the Commercial Code, the consolidated text of the Capital Companies Law approved by Royal Legislative Decree 1/2010, of July 2, and Law 22/2015, of July 20, of Accounts Audit, in matters of non-financial information and diversity.

Regarding the contribution to scientific knowledge, this work expands the orientation and reporting frameworks of the SDGs for Social Economy entities using the SPOLY model of Social Accounting, a model that is estimated to be effective in achieving the stated, participatory and transparent purpose. The foundations of this system make it possible to obtain relevant indicators with which organizations can guide their action towards the SDGs. Likewise, unlike the other frameworks, the stakeholder participation process is standardized, ensuring in-depth dialogue with stakeholders. Third, since the methodological stages are standardized and the monetization process is documented, traceability is also ensured and, consequently, transparency. Finally, within the SPOLY model, this work is a contribution, it opens the door: the connection of the value variables and the SDGs had not yet been published.

Therefore, the study advances in the quantification of the effective contribution to the sustainability of the Social Economy. The findings of the article can help to clarify how the actions of the different entities link with the SDG not only conceptually, but also measuring the distribution among them. This is different from the already in place Global indicator framework for the Sustainable Development Goals and targets proposed by the United Nations [

35], which are conceived mainly for the national and supranational levels and are still developing. The results provide, as well some clarification on the measuring of social sustainability, which is still in a lesser degree of development than the economic and environmental dimensions. This is also done taking as a reference an internationally recognized and accepted framework, which can help the comparison with other types of entities both within and outside the Social Economy. Thus, providing a basis for the future development of a system of indicators that can be systematized and extrapolated with less use of resources and effort.

There are also some limitations to the study. The reduced size of the sample, two organizations, implies that more analysis is needed to build a proper framework to allow comparison within the same “family” of the Social Economy and with other entities. Together with that, the data used for the quantification is extracted from the Social Accounting process, which slows the process since it needs to be carried out first. Another of the limits that can be pointed out is that there is not yet a well-developed theoretical framework to connect the value variables obtained in the Social Accounting process and the SDGs.

Second, the subjective approach to objectify the social value on which it is based, and the stage of development in which the model is located, makes difficult at the moment a direct application to other entities of the value variables and the proposed indicators and proxies for their monetization, For this, it would be necessary to have a sufficient set of case studies from which to extract a common table of value variables and, for their monetary quantification, adapt the value of the proxy to the reality of each entity, until it counts with standardized ranges. Therefore, this aspect limits comparability between organizations belonging to the same family of the social economy, a requirement urged on the indicators used in the non-financial report.

For the future lines of research, the study of more entities (not only) of the Social Economy would pave the way towards a necessary process of normalization that would both, strengthen the theoretical fundamentals of the proposed methodology and ease its application in the future. The comparison of organizations of different nature and productive sectors (for instance, between profit and nonprofit organizations) is another path to follow and it would allow building a more robust system of indicators that complement the existing ones at the international level.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}