3.1. Empirical Model

With a plethora of growth studies available, the endogenous growth model is employed, where GDP per capita is used to measure growth. The use of GDP per capita provides a more comparative measure of living standards as opposed to total GDP. With regards to the endogenous growth theory, there are several numbers of variables that are significantly correlated with growth regression models, including but not limited to initial level of income, investment rate, various measures of education and certain policy indicators [

37,

38]. Furthermore, based on the work of Aziz and Dahalan [

25], Donayre and Wilmot [

22], and Nusair [

10], it is apparent that oil price also plays an important role in the determination of the economic growth of net oil-exporting countries. In line with that, the following multivariate specification is employed, as inspired by the growth regression model, which is broadly similar to Levine and Renelt [

39], Campos [

40], and Azman-Saini et al. [

41], with the addition of oil price as an explanatory variable:

where

LnGDPPC denotes the natural log of real gross domestic product per capita,

LnBRENT denotes the natural log of real Brent crude oil price,

LnLE denotes natural log of life expectancy,

LnPOP denotes natural log of total population as a measure of the labour force, and

LnGFCF denotes natural log of real gross fixed capital formation as a measure of investment.

The Brent crude oil price is used to proxy for oil price as 70% per cent of international trade in oil is directly or indirectly priced from the Brent basket, making Brent the main price benchmarks for crude oil [

42]. Furthermore, several studies on oil-exporting countries also favoured Brent crude oil price in their research [

43,

44]. The estimate for b, in this case, could be positive as mentioned earlier as oil exporting country often gains from an increase in crude oil price. This scenario is primarily because, in oil-exporting countries, part of the government’s revenue consists of oil revenue. Thus, when the oil price increase, the oil revenue will also increase due to the higher oil price. As such, the government can invest the extra revenue obtained from the increase in the oil price to develop the country and in the process, contribute to economic growth.

Life expectancy is used as a measure of human capital following the work of Azman-Saini et al. [

41] and Hajamini and Falahi [

45], which is often viewed as one of the main drivers of economic growth in the development of economics literature [

46,

47,

48]. A more productive labour force as a result of adequate education and good health will stimulate national economic growth [

49]. Hence, a positive coefficient estimate is expected for life expectancy in the growth model.

On the other hand, labour growth, which is a critical determinant of growth [

50], is proxied by the total population in this case. When population increases, it translates to a reduction in the capital/labour ratio because capital must now be distributed more thinly across the bigger population of workers, thus affecting GDP per capita negatively [

48].

Similarly,

LnGFCF is used to proxy for the capital stock, which is an essential component of the production function.

LnGFCF leads to influence the multifactor productivity and hence the production indirectly, resulting in higher productivity and efficiency [

51]. Therefore, a positive coefficient estimate, e, is expected for

LnGFCF.

As noted earlier, the effect of oil price on economic growth could be asymmetric. Hence, to examine the asymmetric effect of oil price on the economic growth of the oil-exporting countries of ASEAN, the NARDL model of Shin et al. [

24] will be employed, which is an extension of Pesaran et al. [

52] linear ARDL bound testing approach. However, the linear ARDL model is first estimated before the NARDL model to determine if the oil price is deemed significant in a linear context.

There are several advantages in employing an ARDL model to estimate the linear effect of oil price on economic growth. The first advantage is the variables could be integrated of order zero, one or a combination of both, and the results yield remains valid. In other words, an ARDL model can be used to determine the presence of a long-run relationship among variables despite having a different order of integration of variables, unlike other cointegration tests which require that all the variables are of the same order of integration. Second, the ARDL model is suitable for this research as it performs better when estimating small sample sizes compared to other cointegration tests [

53].

The models proposed above are long-run models, and as such, its coefficient estimates only the long-run effects. Thus, the equations shall be reparameterized into an unrestricted error-correction modelling format. The following error-correction models shall be used along with the Pesaran et al. [

52] bound testing approach.

where Δ denotes the first different operator,

DUMMY is the dummy variable to account for a possible structural break, and

μt represents the white noise residuals.

Based on the equations above, one observable advantage is that both the short-run and long-run estimates are provided at once within a single equation framework. The short-run effects will be the estimates of the coefficient for each first differenced while the long-run effect will be the estimates of

λ2 to

λ5 normalise on

λ1 for Equation (3). However, the long-run estimates are meaningful only if cointegration can be established. There are three separate tests to establish the existence of cointegration among the variables, namely, the F-test for joint significance of lagged variables and the t-test on the lagged level of the dependent variable as suggested by Pesaran et al. [

52] and another additional F-test on the lagged levels of the independent variable(s) as suggested by McNown et al. [

54].

In the F-test for joint significance of lagged variables, also known as a bound test, the calculated F-statistic is compared with the lower bound and the upper bound. Should the F-statistic be below the lower bound, the null hypothesis of no long-run relationship cannot be rejected while an F-statistic that is greater than the upper bound means that the null hypothesis can be rejected, signifying the existence of a long-run relationship. However, if the F-statistic falls between the lower and upper bound, the result is said to be inconclusive. Even though the cointegration analysis using the ARDL model is suitable for small sample studies such as this, the critical values provided by Pesaran et al. [

52] are generated with a sample size of 1000 observations along with 40,000 replications. As such, this study will instead use the Narayan [

55] critical value for the lower bound and the upper bound. The Narayan [

55] critical values provide the lower bound and the upper bound value for small sample sizes ranging from 30 to 80 with a 5-observation interval in between and have been generated with 40,000 replications as well.

An issue that arises from the F-test, however, is whether the significance of the test arises merely from either the lagged level of the dependent variable or the lagged level of the independent variable(s) alone. As such, performing a t-test is necessary to rule out the possibility of a degenerate lagged dependent variable case. One of the assumptions made by Pesaran et al. [

52] is the dependent variable must

I(1), which rules out degenerate lagged independent variable(s) case. The idea behind this is that the ARDL equation will be similar to a generalised Dickey–Fuller equation when the lagged level dependent variable is deemed significant. A significant lagged dependent variable indicates that the dependent variable is integrated of order zero, i.e.,

I(0). One notable issue that should be stated here is the lack of small sample critical value bounds for the t-statistic. Narayan [

55] only provided small sample critical values for the F-test for the joint significance of lagged variables and not the small sample critical value bounds for the

t-test of the lagged dependent variable. As such, the

t-test on the lagged level dependent variable for this study will use the Pesaran et al. [

52] critical value that is reported on [

52]. As with the earlier F-test on the joint significance of lagged variables, if the computed t-statistic exceeds the upper bound critical value, this study can establish statistical significance.

In addition to the two-test mentioned above, an F-test on the lagged levels of the independent variable(s) introduced by McNown et al. [

54] is employed. This additional test will circumvent the presumption of the dependent variable to be

I(1). As such, the use of such additional test will minimise the risk of false conclusions made from standard unit root tests, which are notorious for their low power. Like the bound test proposed by Pesaran et al. [

52], the F-statistic obtained from this test will refer to the critical values tabulated by Sam et al. [

56], which consist of a lower bound as well as an upper bound. If the F-statistic exceeds (lower than) the upper bound, the null hypothesis is rejected (accepted), and the test is significant (insignificant). If the F-statistic falls between the bounds, the test is inconclusive. Integrating this test with the two-test proposed by Pesaran et al. [

52] will provide a clearer picture of the system’s cointegration status. This new method of determining cointegration is coined as the augmented ARDL bounds test. The null hypothesis and the alternative hypothesis for all three tests are summarised in

Table 2.

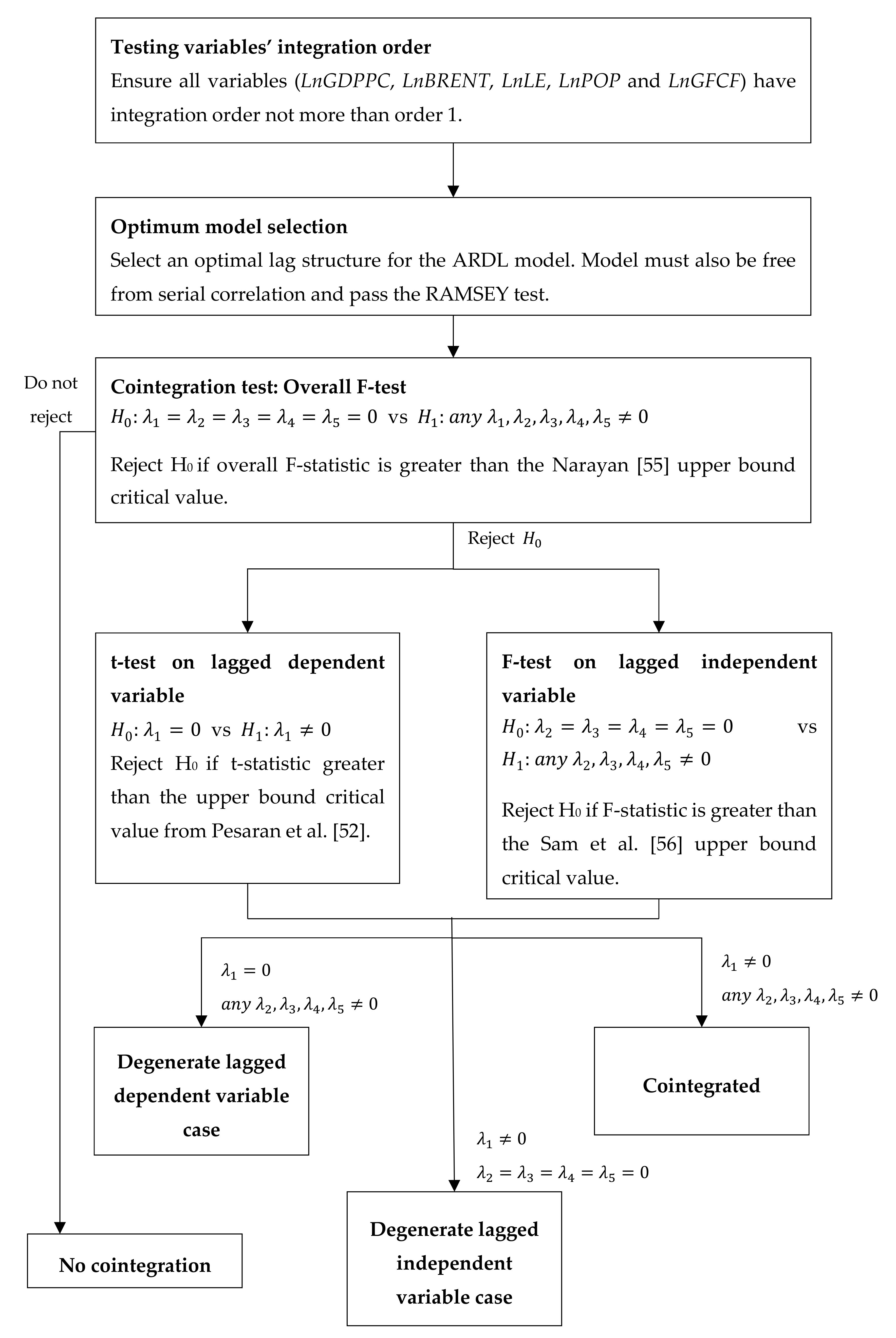

There are four probable outcomes based on the results obtained from the three cointegration test mentioned. The first outcome is when the F-test for joint significance of lagged variables and the F-test on the lagged levels of the independent variable(s) are significant, but the

t-test on the lagged dependent variable is insignificant. This outcome is known as degenerate lagged dependent variable or degenerate case #1 (See McNown et al. [

54], Goh et al. [

57]). The second outcome is when the F-test for joint significance of lagged variables and the t-test on the lagged level dependent variable is significant, but the F-test on the lagged level of the independent variable(s) are insignificant. This outcome is coined as degenerate lagged independent variable or degenerate case #2. The third outcome occurs when the F-test for the joint significance of lagged variables is insignificant. The fourth outcome is when all three tests are found to be significant. The first and second outcome are degenerate cases and, along with the third outcome, would imply no cointegration. Only the fourth outcome will imply cointegration among the variables. The four outcomes are summarised in

Table 3 for convenience purpose, and the procedures for the implementation of the augmented ARDL bounds test is summarised in

Figure 2 (See Sam et al. [

56]).

To test the asymmetric assumption, which is postulated, the NARDL model, which is an asymmetric expansion of the linear ARDL model, is employed. This methodology allows the decomposition of the independent variables into both positive and negative partial sum of processes to investigate the nonlinear characteristics.

where

POS and

NEG are partial sum processes of positive and negative changes in

BRENTt, respectively. Replacing

BRENTt variable with

POS and

NEG, the specifications are

Given that the NARDL model is an extension of the ARDL model, the NARDL model will also be subjected to the conditions under an ARDL model. In this case, the NARDL model will need to undergo the three cointegration test required under an augmented ARDL model to determine if cointegration exists.

Once the long-run relationship between the variables has been established, the potential for asymmetric effect shall then be investigated. To test for the short-run symmetry, a Wald test under the null hypothesis of . Similarly, the long-run symmetry is tested under the null hypothesis of .

This section may be divided by subheadings. It should provide a concise and precise description of the experimental results, their interpretation as well as the experimental conclusions that can be drawn.

3.2. Data and Sources

This study employs annual data with the sample period ranging from 1979 to 2017. The real gross domestic product per capita is derived by obtaining the real gross domestic product from the United Nations Statistics Division (UNSD) and dividing it by the total population obtained from the World Development Indicator (WDI). The Brent crude oil price is extracted from the World Bank Commodity Price Data (WBC). Total population and the life expectancy data are obtained from WDI while the gross fixed capital formation is obtained from UNSD. Descriptions of the data are summarised in

Table 4 below.

Table 5 provides the descriptive statistic for the variables employed in the estimation before the log transformation. Throughout the 39 years, the minimum

GDPPC for Brunei was 31,430.74 while the maximum

GDPPC is 72,437.55 USD, with an average of 39,588.59 USD. From this average, the changes in the

GDPPC were around plus or minus 8,450.31 USD. The

BRENT crude oil price ranges from a minimum of 15.48 USD to 101.58 USD, averaging 47.34 USD. The standard deviation for

BRENT is 26.19 USD. For Malaysia, the minimum

GDPPC is 3,194.60 USD, while the maximum

GDPPC is 11,528.34 USD, averaging 6,673.06 USD. The changes in the

GDPPC were around plus or minus 2,481.98 USD. As for Vietnam, the minimum

GDPPC is 309.52 USD while the maximum

GDPPC is 1,834.65 USD, averaging 817.49 USD. Changes in the

GDPPC for Vietnam were around plus or minus 462.11 USD.

Table 6 provides the descriptive statistics for the variables after log transformation.

Furthermore, this study employs the Pearson correlation coefficient to determine the existence of contemporaneous relationships among the variables. Before the correlation analysis is conducted, all variables are transformed using the log transformation. Results are reported in

Table 7. As shown in the table,

LnBRENT shows a significantly positive contemporaneous correlation with

LnGDPPC. Specifically, the mean of the Pearson correlation is 0.429 and 0.540 for Malaysia and Vietnam, respectively. These results are in line with the theoretical prediction, where an increase in oil prices improves the economy of an oil-exporting country. However, for the case of Brunei, the

LnBRENT does not appear to have any significant contemporaneous correlation with

LnGDPPC. These results, however, are merely correlation analysis and does not imply causation. A simple correlation which analyses the relationship between two variables will potentially disregard important explanatory variables. As such, a regression is required to ascertain the relationship between the variables.

{kind=link}

{kind=link}