1. Introduction

In the first decade of this century, a large share of the open interest in energy futures (or “paper”) markets became tied to purely financial firms [

1,

2]. For commodities overall, [

3] document that a key aspect of this so-called financialization was a tripling of the futures commodity open interest share held by hedge funds that also trade equity futures, and that this development was associated with stronger commodity–equity cross-market linkages. We revisit that widely cited paper by specializing its analysis to the specific case of energy markets.

As [

4] observe, there are theoretical reasons to expect that financialization might strengthen equity-commodity co-movements. Their arguments run as follows. One, unlike most commodity market participants, financial firms typically trade in other asset markets, so financialization could improve risk sharing and make commodity-specific shocks less important (as in [

5,

6]) and systemic shocks more important (as in [

7]) for the determination of commodity risk premia and returns. Two, institutional financial investors’ risk management practices can amplify price shocks [

8] and transmit them across markets, including from financial to commodity markets [

9]. Three, even on normal days (when markets are not under stress), the theoretical model of [

10] (p. 1511) predicts that an “inflow of institutional funds into commodity futures markets” should boost commodity–equity correlations because financial institutions active in commodity markets rate the performance of their traders versus passive commodity indices. This last insight appears especially relevant in the context of the energy commodities on which the present paper focuses, as they make up a large portion of the major commodity benchmark indices.

As a whole, those three theoretical arguments suggest that not only economic fundamentals (as in [

11]) but also “variations in the make-up of the commodity futures open interest (should) help predict long-term fluctuations in commodity–equity return co-movements” (Büyükşahin and Robe [

3] (p. 40)). The second theoretical argument, furthermore, suggests that the degree of financialization might matter differentially for cross-market linkages depending on credit market conditions. We provide empirical support for both hypotheses.

We start by estimating weekly dynamic conditional correlations (DCC) between the returns on passive energy and equity investments, using data from 1991 (when the first commodity index products were introduced) to 2020. We find that these DCCs fluctuate substantially over time and increase sharply during recessions. These results extend prior findings in [

11,

12,

13].

Next, we turn to the possible relation between financialization and equity-commodity co-movements that a substantial number of other papers have studied using various methodologies (see [

14,

15] for recent reviews of that literature). Precisely, we adopt the econometric methodology proposed by Büyükşahin and Robe (2014) [

3], and we adapt it to energy markets. While that paper looks at the joint distribution of equity returns with the returns on various portfolios of many heterogenous commodities (including energy together with metals, agriculture, livestock, and softs), our analysis here is specific to energy commodities.

We find that, controlling for physical-market and macroeconomic fundamentals, energy-commodity return DCCs are positively related to greater energy market participation by hedge funds. That relation is especially strong in the case of hedge funds that take positions in both equity and energy futures markets. Interestingly, the intensity of the relation between hedge fund activity and energy–equity return DCCs is lower when credit risk is elevated—a result that does not seem to be driven solely by the financial market freeze during the Great Recession. Those results confirm, for energy markets, the findings of Büyükşahin and Robe [

3] for broadly diversified portfolios of commodities.

Importantly for the debate on the impact of commodity index traders (CIT) in commodity markets, we do not find support for the notion that the magnitude of CIT positions is statistically significantly linked to energy–equity return correlations. This result extends to energy markets the conclusion of Büyükşahin and Robe [

3] that, unlike active institutional investors (namely, hedge funds), passive institutions (namely, CITs) do not make commodity markets co-move more with equity markets. It also complements evidence, based on intraday data and a very different methodology, that “while the large flows from index traders appear to affect commodity markets, they do not permanently change commodity prices, and smaller flows, such as those from CLNs (commodity-linked notes), appear to negligibly affect prices” ([

16] (p. 4753)).

Key to our analysis is a comprehensive dataset of individual positions in the most liquid U.S. futures markets for energy (crude oil, heating oil, natural gas) and equities (S&P 500 e-Mini) that is maintained by the U.S. derivatives market regulator, the Commodity Futures Trading Commission (CFTC). We focus on futures markets in 2000–2010 for three reasons: because that decade is associated with the financialization of commodities [

17]; because, in that decade, energy price discovery continued to generally take place on futures exchanges rather than partly over the counter [

18]; and because, fifteen years after the end of our sample period, commodities remain “financialized” (using public CFTC data, [

15] find that, across all commodities, the non–commercial share of the futures open interest is even higher (almost one third greater) in 2012–2021 than it was in 2006–2011, i.e., in the

post-financialization half of our own sample. It is worth noting that part of that non–commercial share increase reflects the fact that, while before 2009 virtually all CITs were classified as (commercial) commodity swap dealers in CFTC reports, many CITs are nowadays classified as non–commercials. In agricultural futures markets, for example, nearly half of CIT positions in 2015–2018 were held by non–commercial traders (mostly managed money funds)—see [

19], whose evidence is based on the same non-public CFTC position data as the present paper. Regardless, [

15]’s point is valid: first, financial traders’ overall share of the open interest is higher than it was

pre–financialization; second, [

15] show that equity-commodity return correlations remain higher than in the

pre-financialization period). Those facts, combined, mean that the relations that we document and the novel evidence that we provide remain highly relevant today even though they relate specifically to the first decade of financialization.

The CFTC dataset contains detailed information about every large futures trader’s end-of-day futures positions, main line(s) of business, and purpose(s) for trading. Following Büyükşahin and Robe [

3], we exploit this regulatory information to construct weekly aggregate measures of index fund, hedge fund, and traditional commercial trader activities in near-dated (three nearest-dated futures maturities) and far-dated (all other maturities) energy futures. Using these measures, we find that the paper market activities of only some groups of traders are statistically related to market co-movements at the weekly frequency.

Formally, we estimate an autoregressive distributed lag (ARDL) model to establish the existence of a long-run relationship between the variables (DCC, macroeconomic conditions, physical oil market fundamentals, trader positions) and to provide “consistent, unbiased estimates of the long run parameters” (Büyükşahin and Robe [

3] (p. 64)). In addition, after establishing the existence of a long-run relation, we run an error-correction model (ECM) to analyze the short-term dynamics.

We find that, whereas CIT positions have little explanatory power, hedge fund positions do.

Ceteris paribus, a one percent (1%) increase in the overall energy-futures open interest share of hedge funds is associated in equilibrium with an increase in energy–equity return correlations of more than six percent (6%). This figure, which we obtain for a well-defined set of energy commodities using a setup in which we are able to control for physical market fundamentals, exceeds the corresponding percentage (4%) found by Büyükşahin and Robe [

3] when looking at a diversified portfolio of 17 commodities for which no such control is possible.

The present paper further extends Büyükşahin and Robe [

3] by showing that, in the short term, it is financial variables that drive changes in correlations. Intuitively, the existence of a long-run relationship has implications for the short run behavior of the variables: there must be a mechanism that drives them to their long-run equilibrium relationship. After establishing that the variables are cointegrated, we model this mechanism using an error-correction mechanism (ECM) in which the equilibrium error also drives the short run dynamics of the series. Our ECM analysis buttresses our long-run result by singling out hedge fund activity and credit risk (captured by the TED spread) as the drivers of the short-run dynamics.

As in Büyükşahin and Robe [

3] (p. 40), our long-run analysis shows that “it is not just changes in the overall amount of financial activity in commodity futures markets that helps predict the observed correlation patterns”. No, the explanatory power of financial institutions’ energy futures positions relates more narrowly to one type of trader: hedge funds, especially those that hold overnight positions in both equity and energy futures markets. To our knowledge, our findings provide the first empirical evidence of the need to account—not just for commodities in general (Büyükşahin and Robe [

3]) but in energy futures markets specifically (the present paper)—for heterogeneity among different sorts of hedge funds (i.e., of market participants that all share the same public CFTC classification of “managed money traders”).

Finally, our analysis confirms the importance of taking into account overall economic and financial conditions when explaining the intensity and the drivers of energy–equity return linkages. On the one hand, energy–equity return DCC are positively related to the TED spread, a proxy for credit risk. On the other hand, over and above that general importance of credit risk, we find that something about the Great Recession is exceptional with respect to energy–equity correlations: the coefficient for a dummy variable capturing that 18-month episode is highly significant and positive even though our regressions also control for the TED spread. This finding confirms the conclusion of Büyükşahin and Robe [

3] that the financial crisis of 2008–2011 is qualitatively “different from earlier episodes of financial market stress since 1991 and that this difference is reflected, in part, in an increase in cross-market correlations” ([

3] (p. 40)).

The remainder of the paper proceeds as follows.

Section 2 provides evidence on return co-movements in energy and equity markets.

Section 3 discusses our regulatory data on individual trader positions and documents the financialization of energy markets in 2000–2010.

Section 4 ties fluctuations in the strength of energy–equity co-movements to energy market and macroeconomic fundamentals, and to the aggregate positions of commodity futures traders.

Section 5 concludes the paper.

2. Three Decades of Energy–Equity Return Correlation

This section describes our sources for energy and equity weekly returns data, how we estimate dynamic conditional correlations between the return series, and how those correlations evolve over time.

Our weekly returns sample covers three decades starting in 1991, when commodity index vehicles first became readily available to investors. This 30-year time interval brackets our sample of trader positions (2000–2010) by one decade on each end. This long period allows us to extend the prior literature documenting changes over time in the degree to which commodities co-move with equities—see, e.g., [

11], data from 1959 to 2004 that have been updated through 2014 in [

13]; [

20], data from 1982 to 2004; [

21], data from 1991 to 2006); [

3], data from 1991 to 2010; and [

15], data from 1986 to 2021; for a detailed survey, see [

14]). In the context of energy markets, this section also provides context to numerous studies on the susceptibility of stock markets to oil shocks—see, e.g., [

22,

23], and references cited in those papers.

2.1. Return Data

We use Bloomberg data from January 1991 to July 2020 to compute weekly Tuesday-to-Tuesday log returns on benchmark passive energy and stock market indices. We follow [

3] for the choice of passive investment benchmarks.

For equities, we use Standard and Poor’s S&P 500 index. We find qualitatively similar energy–equity DCC patterns using the Dow-Jones Industrial Average equity index, so there is no loss of generality in discussing only the S&P 500. All of our results are likewise qualitatively robust to using the MSCI World Equity index rather than the S&P 500 U.S. index as the proxy for a passive equity portfolio.

For energy, we use the unlevered total return on the Standard and Poor S&P GSCI-Energy index (GSENTR), i.e., the return on a “fully collateralized energy futures investment that is rolled forward from the fifth to the ninth business day of each month”. The GSENTR averages the nearby prices of six energy futures contracts, using weights based on worldwide production figures. It gives a large weight to crude oil. In unreported robustness checks, we use as an alternative the total (unlevered) returns on the second most widely used investable benchmark, Dow-Jones’s DJAIG (since May 2009, DJ-UBSCI) Total-Return Energy Index. This second index is designed to provide a more “diversified benchmark for the commodity futures market”. We find similar results for both indices, so the remainder of this paper focuses on the GSCI index. This robustness analysis is analogous to the one that [

3] carry out to tackle a similar quandary related to the dominance of energy products in the GSCI Total Return index.

2.2. Dynamic Conditional Correlations

In order to estimate the time-varying intensity of commodity–equity return co-movements, we follow [

24] and compute dynamic conditional correlations (DCC). First, we estimate time-varying variances using a GARCH(1,1) model. Then, we estimate a time-varying correlation matrix using the standardized residuals from the first-stage estimation.

The above approach is the same as [

3], down to the choice of parameter values. This said, [

25] caution that conditional variances and correlations (DCC) may exhibit “asymmetric responses”, while those authors’ alternative asymmetric dynamic conditional correlations (ADCC) model “permits conditional asymmetries in correlation dynamics” [

25] (p. 537)). For this reason, [

4] use ADCC to analyze the financialization of agricultural commodities. In the present paper, we use both approaches and confirm our DCC results using ADCC.

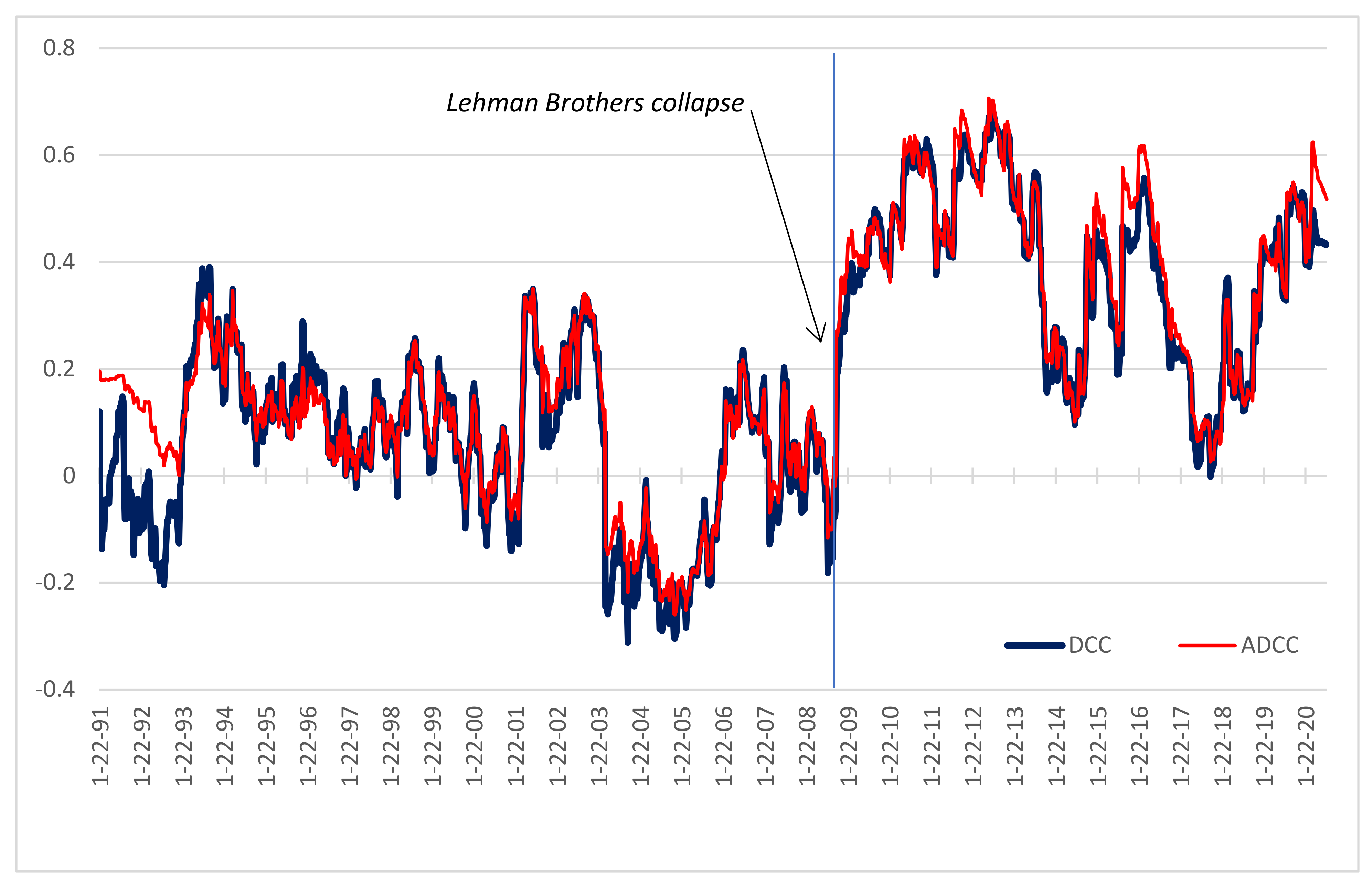

Figure 1 plots, from 22 January 1991 to 28 July 2020, the DCC and the ADCC between the weekly unlevered rates of return on the GSCI-Energy investable index and on the S&P 500 (“SP”) equity index. Several facts emerge from

Figure 1.

First, the energy–equity return DCC and ADCC values track one another very closely. The correlation is 0.97 for the whole sample (1991–2020).

Second, both series fluctuate substantially, and both exhibit a sharp increase after a fall in 2008. Prior to Lehman Brothers’ default in 2008, the average for DCC (resp. ADCC) is 0.05 (resp. 0.08) and the range is −0.31 to 0.39 (resp. −0.26 to 0.35), without any obvious trend in the first 18 years of the sample. Strikingly, however, the energy–equity return correlations shoot up in fall 2008. Furthermore, there appears to be a level shift in the mean correlations from that point onward, with DCC (resp. ADCC) averaging 0.38 (resp. 0.41) in the 12 years following that financial catastrophe, with similarly much higher extreme values (−0.08 to 0.68 for DCC and −0.02 to 0.71 for ADCC).

These findings contribute to the ongoing debate about the financialization of commodities in two ways. First, most importantly, they contradict claims in some papers that commodities have started to become “definancialized given that” commodity–equity correlations are down from their 2008–2011 highs (see [

14] for a survey of those papers). In reality, well over a decade after the onset of the 2008 Financial Crisis, energy–equity return correlations remain at historically high levels. Second, as a corollary relevant to econometric analyses such as the one that we carry out in

Section 3 below, the period after Lehman’s demise should be treated differently than prior years to account for the fact that energy–equity return correlations reach levels unseen in the prior two decades.

4. Linking Fundamentals, Speculation, and Commodity–Equity Co–Movements

As discussed in the Introduction, a substantial theoretical literature predicts that the make-up of the commodity futures open interest, macroeconomic conditions, physical energy-market fundamentals, and/or overall financial market stress should affect correlations between commodity and equity prices. Ref. [

3] find evidence supporting several such conjectures. However, because they study a cross-section of diverse commodities, they cannot include controls for physical market fundamentals. In this paper, we focus on closely related energy commodities, which allows us to control for the possibility that low energy supplies may impact cross-market linkages. Another difference between the two approaches is that we not only analyze the long-run relation between the various variables but also estimate an error-correction model to look at short-term adjustments.

Similar to our approach in

Section 3 above, this section of the present paper hews closely to [

3]. Precisely, the structure of our

Section 4 follows that of Section 5 in that other paper. We use the same acronyms for all common variables. As well, our wording here paraphrases (when an adaptation is needed due to differences in terms of the relevant literature, commodity samples, or results) or directly repeats that companion paper (either with quotation marks for whole sentences, or without quotes when we repeat just a few words at a time).

Section 4.1 introduces the variables we use to control for financial-sector (4.1.1) and real-sector (4.1.2) factors in assessing the impact of energy markets’ financialization (that we document in

Section 3) on energy–equity return correlations (that we document in

Section 2).

Table 4 provides summary statistics of the variables described in

Section 4.1.

Table 5 provides a correlation matrix of our left- and right-hand side variables.

Section 4.2 discusses the ARDL regression methodology on which we rely given (i) possible endogeneity issues and (ii) the fact that some of the variables are stationary in levels while others are stationary in first differences only.

Section 4.3 discusses our regression results.

4.1. Macroeconomic, Physical-Market and Financial-Market Conditions

Various theoretical models show the importance of macroeconomic and commodity-specific fundamentals for energy price levels and volatility [

33] and commodity risk premia (see, e.g., [

34,

35]). Although there is no unifying theory predicting time-variations in the correlations between the returns on commodity vs. other investments [

20], the extant literature suggests several variables for our empirical analysis.

4.1.1. Macroeconomic Fundamentals

Equity and commodity investments perform differentially over the business cycle (see, e.g., [

11,

13,

36]). Furthermore, the response of U.S. stock returns to energy price increases depends on whether the increase is the result of a demand shock or of a supply shock in the energy space [

22]. These empirical regularities point to the need to control for the global business cycle when seeking to explain time-variations in the strength of equity-commodity linkages.

To capture the global business cycle at the frequency needed for our analysis, we draw on the Kilian [

32] index of real economic activity. That index is based on “dry cargo single voyage ocean freight rates and is explicitly designed to capture shifts in the demand for industrial commodities in global business markets” [

32] (p. 1055). The Kilian index is available monthly from 1968: we compute weekly values (which we denote

REA) based on Baltic Dry Index quotes following the same procedure as in [

3].

4.1.2. Physical-Market Fundamentals

Conditions in physical energy markets could affect equity-energy correlations in two ways. On the one hand, when changes in nearby energy futures prices mostly reflect physical inventory conditions, they are unlikely to be met by contemporaneous changes in equity valuations. To wit, [

4] show that the futures returns from grain, oilseed, and livestock markets in 1995 to 2015 are consistent with this intuition, which motivates our approach here (precisely, using a structural vector-autoregression model and weekly data, [

4] find no evidence that inventories have a statistically significant impact on commodity–equity correlations). Hence, we refrain from including inventory measures in the econometric analysis. On the other hand, when energy demand increases amid strong economic growth, it can eventually exhaust the crude oil “spare” production capacity that OPEC has historically tried to maintain—leading to a sharp increase in oil prices; conversely, lower energy prices amid greater “surplus” production capacity likely reflect a poor macroeconomic environment. These facts suggest a positive relationship between spare oil output capacity and energy–equity return correlations.

Following [

2,

37], we use historical data from the International Energy Agency’s (EIA) Oil Market Reports to calculate the total spare crude oil production capacity outside of Saudi Arabia (“

SPARE”). We focus on non-Saudi figures because the clearest evidence of changes in energy market fundamentals is evident in this variable (as opposed to world oil consumption, Saudi surplus oil production capacity, OECD stocks of crude oil, etc.).

A major change in 2004–2008 is clearly seen in Figure 10 of [

2], which provides a scatter plot of the spot WTI crude oil price vs. the non-Saudi spare crude production capacity between 1995 and 2010. From January 1995 to February 2004, when spare capacity was relatively plentiful, prices fluctuated around

$29. Likewise, in 2009–2010, spare capacity was non-trivial; again, prices fluctuated in a narrow range (this time around

$75). From March 2004 to August 2008, in contrast,

SPARE was close to zero and spot oil prices ranged between

$27 and

$142,

4.1.3. Financial Stress and Lehman Crisis

Following a slump in a major asset market, levered and similarly constrained position holders may face pressures to liquidate other asset holdings. A number of theoretical papers show that those selling pressures may bring about cross-asset contagion even if the fundamental factors driving the returns on different assets are independent—see [

38] for a thorough discussion. Refs. [

39,

40] show that, depending on the make-up of market activity (i.e., who trades) and investor risk appetite, the resulting cross-asset correlations can remain elevated long after the initial shock (a number of empirical studies identify strong cross-market return correlations during crises: for early studies, see [

41] in the case of international equity-market linkages; [

42] for bond-equity linkages in developed countries; and [

12] for equity-commodity linkages).

Those theoretical results suggest that,

ceteris paribus, energy–equity correlations should be higher during periods of elevated levels of credit market risk and in the period after a major market crash. As in [

3], we include the

TED spread to test the first hypothesis, and a time dummy (

DUM) for the post-Lehman period (October 2008 to March 2010) to test the second.

4.2. Methodology

Augmented Dickey–Fuller (ADF) unit root tests for the variables used in our estimation equations are summarized at the bottoms of

Table 1,

Table 2 (Panels A and B), and

Table 4. They show that many of the variables are I(1) but that some are I(0).

To examine the link between commodity–equity return correlations, macroeconomic fundamentals, physical market fundamentals, financial market conditions and energy futures traders’ positions, we employ the autoregressive distributed lag (ARDL) approach developed by [

43,

44]. This approach allows us to “test the existence of a long-run relationship between underlying variables and to provide consistent, unbiased estimators of long-run parameters in the presence of I(0) and I(1) regressors. The ARDL estimation procedure reduces the bias in the long run parameter in finite samples and ensures that it has a normal distribution irrespective of whether the underlying regressors are I(0) or I(1). By choosing appropriate orders of the ARDL(

p,

q) model, [

43] show that the ARDL model simultaneously corrects for residual correlation and for the problem of endogenous regressors” ([

3] (p. 64)).

“First, the lag orders of

p and

q must be selected using some information criterion. Based on Monte Carlo experiments, [

43] argue that the Schwarz criterion performs better than other criteria” ([

3] (p. 64)). Using model-dependent information criteria, we end up selecting optimal lag lengths

p = 1 and

q = 1 in all our models—the same values selected in [

3] (the Schwarz Information Criterion (SIC) tends to pick a simpler model, resulting in underfitting the model; therefore, we sometimes employ Akaike’s Information Criterion (AIC) to make sure that the errors are serially uncorrelated).

We start with the problem of estimation and hypothesis testing in the context of the following ARDL(

p,

q) model:

where

p =

q = 1;

y is a

t x 1 vector of the dependent variable,

x is a

t x k vector of regressors, and

ω stands for a

t x s vector of deterministic variables such as an intercept, seasonal dummies, time trends, or exogenous variables with fixed lags (the error term is assumed to be serially uncorrelated).

For each of our models, we perform a bounds test of the existence of a long-run relationship between a dependent variable and a set of regressors. The bounds test results, reported in

Table 6,

Table 7 and

Table 8, suggest the existence of a long-run relationship between our dependent variable and regressors.

After we establish the existence of a long-run relationship between our variables, we estimate long-run coefficients as well as short-run dynamics coefficients. The short-run model coefficient on the error correction term is negative and statistically significant in all our models, consistent with the finding of a long-run relationship.

4.3. Regression Results

Table 6,

Table 7,

Table 8 and

Table 9 summarize our regression results.

Table 6 establishes the explanatory power of physical market fundamentals (captured by

SPARE), macroeconomic fundamentals (captured by

REA), and financial market stress (captured by

TED) (for completeness, all of our models also include a variable capturing momentum in equity markets (denoted UMD); this variable always has a positive coefficient (consistent with the notion that equity momentum could spill over into other risky assets such as commodities) but we seldom find UMD to be a statistically significant explainer of commodity–equity correlations and, when it is at all statistically significant, the significance level is only 10%).

Table 7 establishes the significant additional explanatory power of speculation in general and hedge fund positions in particular.

Table 8 shows the relevance of cross-market traders.

Table 9 presents some robustness checks. The variables are in levels or in percentages, as discussed in

Section 3.

4.3.1. Real Sector and Financial Stress Variables (Table 6)

Long run estimates for Model 1 in Panel A of

Table 6 show that, for our sample period (2000–2010), energy–equity DCCs are statistically significantly negatively related to

REA. Ref. [

45] provide comprehensive evidence that, at least in our sample period,

REA is a good “proxy for the state of the global business cycle” [

45] (p. 829). To the extent that

REA therefore “captures world demand for commodities, (our) finding confirms the intuition that cross-market correlations increase in globally bad economic times” ([

3] (p. 64)).

We argued intuitively that, insofar as SPARE measures tightness in the physical crude oil market and as this tightness extends to other energy markets, then DCC and SPARE should be positively related. Model 2 supports this prediction.

In both models, the time dummy for the post-Lehman period (

DUM) is always strongly statistically significant and positive. The fact that

DUM is significant despite including the

TED spread (a measure of financial market stress) supports the “graphical evidence in

Section 2 that this sub-period is exceptional” ([

3] (p. 65)).

4.3.2. Speculation, including Hedge Funds Activity (Table 7)

Table 7 is one of our main contributions to the literature. It shows that financial activity in energy futures markets is significantly related to long-term variations in energy–equity market linkages.

Intuitively, “there is no reason to expect that traditional commercial traders (…) should matter for co-movements between commodity and equity indices” ([

3] (p. 65)). Both panels of

Table 7 buttress this intuition in the specific case of energy markets. Panel A seldom finds much long run explanatory power for the

WMSS_TCOM variable, and the ECM short run model in Panel B supports this long run finding.

Likewise, “insofar as commodity swap dealing overwhelmingly reflects swap dealers’ over-the-counter relationships with traditional commercials or with

unlevered,

long-only,

passive commodity-index traders (CITs), we would not expect swap dealers’ positions to affect cross-market correlations. This is because CITs do not engage in value-arbitraging and do not alter their positions quickly under financial-market stress” (Büyükşahin and Robe [

3] (p. 65)).

Table 7 supports this intuition: our variable for swap dealers’ collective share of the short-dated commodity open interest (

WMSS_AS)—which captures most CIT positions in our sample period, per [

2]—is never statistically significant in the long run (Panel A). This finding presents an interesting counterpoint to the empirical conclusions of [

17,

46] and the theoretical predictions of [

10], regarding the impact of commodity index trading on linkages across commodities or across asset classes.

The main finding in

Table 7 is that, after controlling for macroeconomic and physical fundamentals, speculative activity in general (captured by

WSIA in Models 4 and 6) and hedge fund positions in energy futures markets particularly (captured by

WMSS_MMT in Models 3 and 5) are highly significant in explaining fluctuations in the energy–equity DCC estimates over time. The significance is statistical as well as economic.

Ceteris paribus, an increase of 1% in the overall commodity-futures market share of hedge funds (

WMSS_MMT) is associated in the long run with dynamic conditional equity-commodity correlations that are approximately 6% to 7% higher (the mean hedge fund market share of about 20%). Again, those results are qualitatively similar to (but quantitatively a bit stronger than) the values estimated

on average for a cross-section of 17 commodities [

3].

As in [

3], Working’s “

T” index of overall speculative intensity in energy futures markets (

WSIA) “which aggregates the market shares of

all non-hedgers across

all maturities, has less explanatory power than hedge fund positions in short-dated contracts” ([

3] (p. 65)). Going beyond [

3], the ECM analysis in Panel B suggests that it is the positions of hedge funds specifically, rather than the activities of non-commercial traders in general, that make the system adjust.

4.3.3. Interaction between Hedge Funds and Financial Stress

Table 7 shows that greater hedge fund participation enhances cross-market linkages. “Yet if the same arbitrageurs or convergence traders, who bring markets together during normal times, face borrowing constraints or other pressures to liquidate risky positions during periods of financial market stress, then their exit from (energy) markets after a major shock in (financial) markets could lead to a decoupling of the markets that they had helped link in the first place” ([

3] (p. 66)).

To test this hypothesis, all of our specifications in

Table 7 include an interaction term that captures the behavior of hedge funds amid financial stress, as reflected in credit market conditions as proxied by the

TED spread. This interaction term is always significant and, as expected, negative. That is,

ceteris paribus, the ability of hedge funds’ aggregate energy-futures open interest to explain energy–equity DCCs is lower during periods of stress.

4.3.4. Cross-Market Trading

Table 8 uses specifications similar to

Table 7 but focuses on cross-market traders. Two interesting results emerge. First, as intuition would suggest, Models 7 and 9 in Panel A show that the market share of hedge funds that trade in both equity and energy paper markets (

WCMSA_MMT) helps explain long-term linkages between equity and energy returns. Second, the market share of commodity swap dealers that are also active in equity markets (

WCMSA_AS) is somewhat statistically significant but it has a

negative sign in all specifications (Models 7 to 10). These results suggests that “it is value arbitrageurs’ willingness to take positions in both equity and commodity markets, rather than the trading activities of more traditional commodity market participants” ([

3] (p. 66)) or of commodity index traders, that help tie energy to equity markets.

4.4. Robustness

The results in

Section 4.3 above are all consistent with, and extend, the empirical findings that [

3] obtain for financialized commodities in general (but not for any commodity subset in particular). Our results likewise are “qualitatively robust to using additional proxies for energy investment; to introducing dummies to control for unusual circumstances in financial markets; and, to using alternative measures of hedge fund activity in commodity futures markets” ([

3] (p. 66)).

4.4.1. Commodity Indexing Activity

“In the past decade, investors have sought an ever greater exposure to commodity prices. Part of this exposure has been acquired through passive commodity index investing. Some of this investment has, in turn, found its way into futures markets through commodity swap dealers” ([

3] (p. 66)). However, echoing the latter paper’s findings for a diversified portfolio of 17 commodities, our regressions have the coefficient of the

WMSS_AS variable (our proxy for CIT activity) either statistically insignificant or negative. “One possible reason is that, although a part of commodity swap dealers’ positions in short-dated energy futures reflects their over-the-counter interactions with index traders, the rest of their futures positions reflect over-the-counter deals with more traditional commercial commodity traders (so that

WMSS_AS) is only an imperfect proxy of commodity index trading activity in commodity futures markets” ([

3] (p. 66)).

In unreported results, we tried “another proxy for investor interest in commodities: the post-2004 daily trading volume in the SPDR Gold Shares exchange-traded fund (ETF). Although this volume grew massively between 2004 and 2010” [

3], we do not find evidence that it helps explain changes in energy–equity correlations in that period.

Taken together with the results for the

WMSS_AS variable, the likely “interpretation is that the activities of

passive commodity investors do not explain equity-commodity linkages. This result presents an interesting counterpoint to the findings of [

2], who show that increased commodity index trading activity in the WTI crude oil futures market provided additional liquidity that helped integrate crude oil prices across contract maturities” ([

3] (p. 67)).

4.4.2. The 2008–2010 Financial Crisis

In

Table 6,

Table 7 and

Table 8, we use a dummy variable (

DUM) to account for the uniqueness of the

post-Lehman crash period.

Table 9 takes a different approach: it repeats the analysis of

Table 7 (Panel A), with a sample that ends prior to November 2008. That is “the month when DCC estimates soared upward of 0.4 for the first time since the inception of the investable GSCI commodity index” ([

3] (p. 67)).

The results in

Table 9 are “qualitatively similar to those” in

Table 7. “The main difference is that the statistical significance of the hedge fund variables is stronger

pre-crisis. Combined with the strong statistical significance of the

post-Lehman dummy (

DUM) in every single specification” in

Table 7, “as well as with the negative sign of the

INT_TED_MMT interaction term” in both

Table 7 (Panel A) and

Table 9, “this finding suggests that hedge fund activity

per se is not responsible for the exceptionally high correlation levels observed from late 2008 to 2010 ([

3] (p. 67)).

4.4.3. Hedge Fund Activities in Near-Dated Commodity Futures vs. across the Maturity Curve

Table 10 repeats the analysis of

Table 9, “except that we measure speculative activity and different traders’ market shares using position information across all maturities (rather than just the three nearest-maturity contracts with non-trivial open interest). The statistical significance of all the position variables drops dramatically, except for the variable capturing hedge fund activity” ([

3] (p. 67)), although

WMSA_MMT is sometimes significant only at the 10% level. Again,

Table 10 “shows little statistical evidence that swap dealers or traditional commercial traders affect the dynamic cross-market correlations” ([

3] (p. 67)).

Taken together,

Table 7 (Panel A),

Table 9 and

Table 10 “imply that it is the positions of hedge funds in shorter-dated commodity futures (rather than their activities in commodity markets further along the futures maturity curve) that help predict equity-commodity market linkages. This result is intuitive, in that the GSCI index is constructed using short-dated futures contracts and, hence, “one expects that it is short-dated positions that are relevant for commodity-equity correlations” ([

3] (p. 65)).

5. Conclusions

We document that the sign and the strength of the correlation between the returns on passive investments in stock and energy markets fluctuate substantially between 1991 and 2020. Strikingly, the average intensity of this time-varying correlation between energy and equity markets is much higher (0.38) in the dozen years after the start of the Financial Crisis in 2008 than in the two decades prior to that event.

It is by now well known that there was a major upward shift in the commodity futures open interest shares of index funds, hedge funds, and other financial institutions after 2003 [

3,

17], and that ground zero for this “financialization of commodities” was the WTI crude oil market [

1,

2]. Thanks to a comprehensive regulatory dataset of all large trader positions in U.S. equity futures and in the three largest U.S. energy futures markets from late June 2000 through February 2010, we provide additional evidence on the financialization of energy paper markets. In particular, we provide novel evidence that their financialization entailed a sharp increase in the energy futures open interest of hedge funds that also invest in other asset classes. This empirical finding establishes that the

average financialization patterns documented by [

3] for a cross-section of numerous (17) GSCI commodities are especially strong in the

specific case of energy markets.

Like Büyükşahin and Robe (2014) [

3], we also utilize these data to tease out a possible relation between the financialization and the co-movements of commodity and equity prices. We find that, whereas index fund positions have little explanatory power in this respect, hedge fund positions do.

Ceteris paribus, a one percent (1%) increase in the overall energy-futures open interest share of hedge funds is associated in equilibrium with an increase in energy–equity return correlations of over six percent (6%). This figure, which we obtain for three energy commodities using a setup that allows us to control for energy-specific fundamentals, exceeds the corresponding figure (4%) that [

3] obtain for a broad portfolio of 17 diverse commodities for which no control for physical market fundamentals is possible.

The present paper further extends Büyükşahin and Robe (2014) [

3] by showing that, in the short term, it is financial variables that drive changes in correlations. Intuitively, the existence of a long-run relation has implications for the short run behavior of the variables: a mechanism must exist to drive them to their long-run equilibrium relation. After establishing that the variables are cointegrated, we model this mechanism using an error-correction model (ECM) in which the equilibrium error also drives the short run dynamics of the series. Our ECM analysis supports our long-run results by singling out hedge fund activity, together with credit risk (captured by the

TED spread), as the driver of the short-run dynamics.

Finally, we provide empirical evidence that the explanatory power of hedge funds’ energy futures positions relates more narrowly to hedge funds that hold overnight positions in both equity and energy futures markets. To our knowledge, our findings provide the first empirical evidence of the need to account, not just for commodities in general (as shown already in [

3]) but in energy futures markets specifically (the present paper), for this heterogeneity among different sorts of hedge funds (i.e., of market participants that all share the same public CFTC classification of “managed money traders”).

{kind=link}

{kind=link}