Impact of the COVID-19 Pandemic on Cryptocurrency Markets: A DCCA Analysis

Abstract

:1. Introduction

2. Brief Literature Review

3. Data and Methods

4. Results and Discussion

4.1. Descriptive Statistics

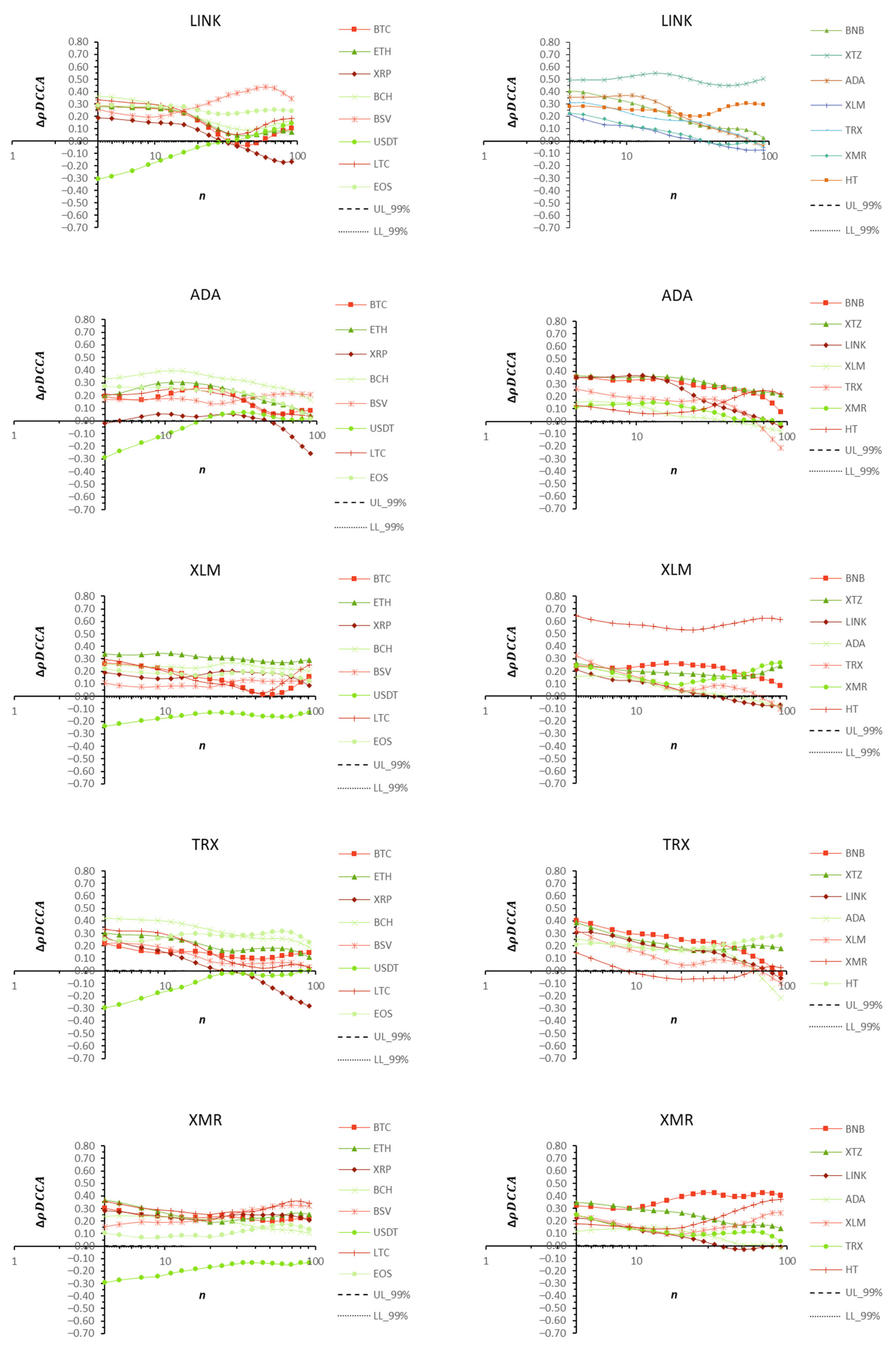

4.2. ∆ρDCCA Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Kumar, A.; Iqbal, N.; Mitra, S.K.; Kristoufek, L.; Bouri, E. Connectedness among major cryptocurrencies in standard times and during the COVID-19 outbreak. J. Int. Financ. Mark. Inst. Money 2022, 77, 101523. [Google Scholar] [CrossRef]

- Leirvik, T. Cryptocurrency returns and the volatility of liquidity. Financ. Res. Lett. 2021, 44, 102031. [Google Scholar] [CrossRef]

- Giannellis, N. Cryptocurrency market connectedness in COVID-19 days and the role of Twitter: Evidence from a smooth transition regression model. Res. Int. Bus. Financ. 2022, 63, 101801. [Google Scholar] [CrossRef]

- Gajardo, G.; Kristjanpoller, W.D.; Minutolo, M. Does Bitcoin exhibit the same asymmetric multifractal cross-correlations with crude oil, gold and DJIA as the Euro, Great British Pound and Yen? Chaos Solitons Fractals 2018, 109, 195–205. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D.; Kristoufek, L.; Lucey, B. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. Q. Rev. Econ. Financ. 2020, 77, 156–164. [Google Scholar] [CrossRef]

- Neto, D. Are Google searches making the Bitcoin market run amok? A tail event analysis. N. Am. J. Econ. Financ. 2021, 57, 101454. [Google Scholar] [CrossRef]

- Mensi, W.; Al-Yahyaee, K.H.; Al-Jarrah, I.M.W.; Vo, X.V.; Kang, S.H. Does volatility connectedness across major cryptocurrencies behave the same at different frequencies? A portfolio risk analysis. Int. Rev. Econ. Financ. 2021, 76, 96–113. [Google Scholar] [CrossRef]

- Vidal-Tomás, D.; Ibáñez, A.M.; Farinós, J.E. Herding in the cryptocurrency market: CSSD and CSAD approaches. Financ. Res. Lett. 2019, 30, 181–186. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D. Co-explosivity in the cryptocurrency market. Financ. Res. Lett. 2019, 29, 178–183. [Google Scholar] [CrossRef]

- Ferreira, P.; Pereira, É. Contagion Effect in Cryptocurrency Market. J. Risk Financ. Manag. 2019, 12, 115. [Google Scholar] [CrossRef]

- Le, T.H.; Do, H.X.; Nguyen, D.K.; Sensoy, A. COVID-19 pandemic and tail-dependency networks of financial assets. Financ. Res. Lett. 2021, 38, 101800. [Google Scholar] [CrossRef]

- Kristoufek, L. Tethered, or Untethered? On the interplay between stablecoins and major cryptoassets. Financ. Res. Lett. 2021, 43, 101991. [Google Scholar] [CrossRef]

- Park, S.; Jang, K.; Yang, J.-S. Information flow between bitcoin and other investment assets. Phys. Stat. Mech. Appl. 2021, 566, 1116. [Google Scholar] [CrossRef]

- Mensi, W.; Rehman, M.U.; Maitra, D.; Al-Yahyaee, K.H.; Sensoy, A. Does bitcoin co-move and share risk with Sukuk and world and regional Islamic stock markets? Evidence using a time-frequency approach. Res. Int. Bus. Financ. 2020, 53, 101230. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Shahbaz, M.; Nasir, M.A.; Ullah, S. Financial modelling, risk management of energy instruments and the role of cryptocurrencies. Ann. Oper. Res. 2020, 313, 47–75. [Google Scholar] [CrossRef]

- Calvo, G.A.; Mendoza, E.G. Rational contagion and the globalization of securities markets. J. Int. Econ. 2000, 51, 79–113. [Google Scholar] [CrossRef]

- Lee, K.-J.; Lu, S.-L.; Shih, Y. Contagion Effect of Natural Disaster and Financial Crisis Events on International Stock Markets. J. Risk Financ. Manag. 2018, 11, 16. [Google Scholar] [CrossRef]

- Nguyen, D.T.; Phan, D.H.B.; Ming, T.C.; Nguyen, V.K.L. An assessment of how COVID-19 changed the global equity market. Econ. Anal. Policy 2021, 69, 480–491. [Google Scholar] [CrossRef]

- Aslam, F.; Aziz, S.; Nguyen, D.K.; Mughal, K.S.; Khan, M. On the efficiency of foreign exchange markets in times of the COVID-19 pandemic. Technol. Forecast. Soc. Chang. 2020, 161, 120261. [Google Scholar] [CrossRef]

- Mensi, W.; El Khoury, R.; Ali, S.R.M.; Vo, X.V.; Kang, S.H. Quantile dependencies and connectedness between the gold and cryptocurrency markets: Effects of the COVID-19 crisis. Res. Int. Bus. Financ. 2023, 65, 101929. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Bouri, E.; Kang, S.H.; Saeed, T. Regime specific spillover across cryptocurrencies and the role of COVID-19. Financ. Innov. 2021, 7, 5. [Google Scholar] [CrossRef] [PubMed]

- Ullah, S. Impact of COVID-19 Pandemic on Financial Markets: A Global Perspective. J. Knowl. Econ. 2022, 13, 0123456789. [Google Scholar] [CrossRef]

- Khan, A.; Khan, N.; Shafiq, M. The Economic Impact of COVID-19 from a Global Perspective. Contemp. Econ. 2021, 15, 64–75. [Google Scholar] [CrossRef]

- Pak, A.; Adegboye, O.A.; Adekunle, A.I.; Rahman, K.M.; McBryde, E.S.; Eisen, D.P. Economic Consequences of the COVID-19 Outbreak: The Need for Epidemic Preparedness. Front. Public Health 2020, 8, 241. [Google Scholar] [CrossRef] [PubMed]

- Seth, N.; Panda, L. Financial contagion: Review of empirical literature. Qual. Res. Financ. Mark. 2018, 10, 15–70. [Google Scholar] [CrossRef]

- Forbes, K.J.; Rigobon, R. No Contagion, Only Interdependence: Measuring Stock Market Comovements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Bae, K.-H.; Karolyi, G.A.; Stulz, R. A New Approach to Measuring Financial Contagion. Rev. Financ. Stud. 2003, 16, 717–763. [Google Scholar] [CrossRef]

- Davidson, S.N. Interdependence or contagion: A model switching approach with a focus on Latin America. Econ. Model. 2020, 85, 166–197. [Google Scholar] [CrossRef]

- Yousaf, I.; Ali, S. The COVID-19 outbreak and high frequency information transmission between major cryptocurrencies: Evidence from the VAR-DCC-GARCH approach. Borsa Istanb. Rev. 2020, 20, S1–S10. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Financ. Res. Lett. 2020, 35, 101554. [Google Scholar] [CrossRef]

- Akhtaruzzaman; Boubaker, S.; Nguyen, D.K.; Rahman, M.R. Systemic risk-sharing framework of cryptocurrencies in the COVID–19 crisis. Financ. Res. Lett. 2022, 47, 102787. [Google Scholar] [CrossRef] [PubMed]

- James, N.; Menzies, M.; Chan, J. Changes to the extreme and erratic behaviour of cryptocurrencies during COVID-19. Phys. A Stat. Mech. Appl. 2021, 565, 125581. [Google Scholar] [CrossRef] [PubMed]

- Assaf, A.; Charif, H.; Demir, E. Information sharing among cryptocurrencies: Evidence from mutual information and approximate entropy during COVID-19. Financ. Res. Lett. 2022, 47, 102556. [Google Scholar] [CrossRef]

- Caferra, R.; Vidal-Tomás, D. Who raised from the abyss? A comparison between cryptocurrency and stock market dynamics during the COVID-19 pandemic. Financ. Res. Lett. 2021, 43, 101954. [Google Scholar] [CrossRef] [PubMed]

- Conlon, T.; Corbet, S.; McGee, R.J. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Res. Int. Bus. Financ. 2020, 54, 101248. [Google Scholar] [CrossRef] [PubMed]

- Bouri, E.; Tiwari, A.K.; Roubaud, D. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Financ. Res. Lett. 2017, 23, 87–95. [Google Scholar] [CrossRef]

- Goodell, J.W.; Goutte, S. Co-movement of COVID-19 and Bitcoin: Evidence from wavelet coherence analysis. Financ. Res. Lett. 2021, 38, 101625. [Google Scholar] [CrossRef]

- Yarovaya, L.; Matkovskyy, R.; Jalan, A. The effects of a ‘black swan’ event (COVID-19) on herding behavior in cryptocurrency markets. J. Int. Financ. Mark. Inst. Money 2021, 75, 101321. [Google Scholar] [CrossRef]

- da Silva, M.F.; Pereira, J.D.A.L.; Filho, A.M.D.S.; de Castro, A.P.N.; Miranda, J.G.V.; Zebende, G.F. Quantifying cross-correlation between Ibovespa and Brazilian blue-chips: The DCCA approach. Phys. A Stat. Mech. Appl. 2015, 424, 124–129. [Google Scholar] [CrossRef]

- Ma, P.; Li, D.; Li, S. Efficiency and cross-correlation in equity market during global financial crisis: Evidence from China. Phys. A Stat. Mech. Appl. 2016, 444, 163–176. [Google Scholar] [CrossRef]

- Mohti, W.; Dionísio, A.; Vieira, I.; Ferreira, P. Financial contagion analysis in frontier markets: Evidence from the US subprime and the Eurozone debt crises. Phys. A Stat. Mech. Appl. 2019, 525, 1388–1398. [Google Scholar] [CrossRef]

- Zhang, Y.; Hamori, S. Do news sentiment and the economic uncertainty caused by public health events impact macroeconomic indicators? Evidence from a TVP-VAR decomposition approach. Q. Rev. Econ. Financ. 2021, 82, 145–162. [Google Scholar] [CrossRef]

- Cho, S.; Hyde, S.; Nguyen, N. Time-varying regional and global integration and contagion: Evidence from style portfolios. Int. Rev. Financ. Anal. 2015, 42, 109–131. [Google Scholar] [CrossRef]

- Ferreira, P. Portuguese and Brazilian stock market integration: A non-linear and detrended approach. Port. Econ. J. 2017, 16, 49–63. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Adewuyi, A.O.; Albulescu, C.T.; Wohar, M.E. Empirical evidence of extreme dependence and contagion risk between main cryptocurrencies. N. Am. J. Econ. Financ. 2019, 51, 101083. [Google Scholar] [CrossRef]

- Mensi, W.; Rehman, M.U.; Al-Yahyaee, K.H.; Al-Jarrah, I.M.W.; Kang, S.H. Time frequency analysis of the commonalities between Bitcoin and major Cryptocurrencies: Portfolio risk management implications. N. Am. J. Econ. Financ. 2019, 48, 283–294. [Google Scholar] [CrossRef]

- Qureshi, S.; Aftab, M.; Bouri, E.; Saeed, T. Dynamic interdependence of cryptocurrency markets: An analysis across time and frequency. Phys. A Stat. Mech. Its Appl. 2020, 559, 125077. [Google Scholar] [CrossRef]

- Koutmos, D. Return and volatility spillovers among cryptocurrencies. Econ. Lett. 2018, 173, 122–127. [Google Scholar] [CrossRef]

- Yi, S.; Xu, Z.; Wang, G.-J. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? Int. Rev. Financ. Anal. 2018, 60, 98–114. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Lau, C.K.M.; Roubaud, D. Dynamic connectedness and integration in cryptocurrency markets. Int. Rev. Financ. Anal. 2019, 63, 257–272. [Google Scholar] [CrossRef]

- Sensoy, A.; Silva, T.C.; Corbet, S.; Tabak, B.M. High-frequency return and volatility spillovers among cryptocurrencies. Appl. Econ. 2021, 53, 4310–4328. [Google Scholar] [CrossRef]

- Kakinaka, S.; Umeno, K. Asymmetric volatility dynamics in cryptocurrency markets on multi-time scales. Res. Int. Bus. Financ. 2022, 62, 101754. [Google Scholar] [CrossRef]

- Canh, N.P.; Wongchoti, U.; Thanh, S.D.; Thong, N.T. Systematic risk in cryptocurrency market: Evidence from DCC-MGARCH model. Financ. Res. Lett. 2019, 29, 90–100. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Nasir, M.A.; Vo, X.V.; Nguyen, T.T. “Small things matter most”: The spillover effects in the cryptocurrency market and gold as a silver bullet. N. Am. J. Econ. Financ. 2020, 54, 101277. [Google Scholar] [CrossRef]

- Guo, H.; Zhao, X.; Yu, H.; Zhang, X. Analysis of global stock markets’ connections with emphasis on the impact of COVID-19. Phys. A Stat. Mech. Appl. 2021, 569, 125774. [Google Scholar] [CrossRef]

- Szczygielski, J.J.; Brzeszczyński, J.; Charteris, A.; Bwanya, P.R. The COVID-19 storm and the energy sector: The impact and role of uncertainty. Energy Econ. 2021, 109, 105258. [Google Scholar] [CrossRef] [PubMed]

- Li, Z.; Wang, Y.; Huang, Z. Risk Connectedness Heterogeneity in the Cryptocurrency Markets. Front. Phys. 2020, 8, 243. [Google Scholar] [CrossRef]

- McKibbin, W.; Fernando, R. The Global Macroeconomic Impacts of COVID-19: Seven Scenarios Warwick. Asian Econ. Pap. 2021, 20, 1–21. [Google Scholar] [CrossRef]

- Naeem, M.A.; Bouri, E.; Peng, Z.; Shahzad, S.J.H.; Vo, X.V. Asymmetric efficiency of cryptocurrencies during COVID19. Phys. A Stat. Mech. Appl. 2021, 565, 125562. [Google Scholar] [CrossRef]

- Katsiampa, P.; Yarovaya, L.; Zięba, D. High-frequency connectedness between Bitcoin and other top-traded crypto assets during the COVID-19 crisis. J. Int. Financ. Mark. Inst. Money 2022, 79, 101578. [Google Scholar] [CrossRef]

- Sui, X.; Shi, G.; Hou, G.; Huang, S.; Li, Y. Impacts of COVID-19 on the Return and Volatility Nexus among Cryptocurrency Market. Complexity 2022, 2022, 5346080. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, H.; Agan, B. Effects of COVID-19 on cryptocurrency and emerging market connectedness: Empirical evidence from quantile, frequency, and lasso networks. Phys. A Stat. Mech. Appl. 2022, 604, 127885. [Google Scholar] [CrossRef]

- Nguyen, A.P.N.; Mai, T.T.; Bezbradica, M.; Crane, M. The Cryptocurrency Market in Transition before and after COVID-19: An Opportunity for Investors? Entropy 2022, 24, 1317. [Google Scholar] [CrossRef] [PubMed]

- Yarovaya, L.; Zięba, D. Intraday volume-return nexus in cryptocurrency markets: Novel evidence from cryptocurrency classification. Res. Int. Bus. Financ. 2022, 60, 101592. [Google Scholar] [CrossRef]

- Rubbaniy, G.; Khalid, A.A.; Samitas, A. Are Cryptos Safe-Haven Assets during COVID-19? Evidence from Wavelet Coherence Analysis. Emerg. Mark. Financ. Trade 2021, 57, 1741–1756. [Google Scholar] [CrossRef]

- García-Medina, A.; Hernández, J.B.C. Network analysis of multivariate transfer entropy of cryptocurrencies in times of turbulence. Entropy 2020, 22, 760. [Google Scholar] [CrossRef]

- Maghyereh, A.; Abdoh, H. COVID-19 and the volatility interlinkage between bitcoin and financial assets. Empir. Econ. 2022, 63, 2875–2901. [Google Scholar] [CrossRef]

- SDrozdz; Kwapień, J.; Oświecimka, P.; Stanisz, T.; Watorek, M. Complexity in economic and social systems: Cryptocurrency market at around COVID-19. Entropy 2020, 22, 1043. [Google Scholar] [CrossRef]

- Kwapień, J.; Wątorek, M.; Drożdż, S. Cryptocurrency market consolidation in 2020–2021. Entropy 2021, 23, 1674. [Google Scholar] [CrossRef]

- Raza, S.A.; Shah, N.; Guesmi, K.; Msolli, B. How does COVID-19 influence dynamic spillover connectedness between cryptocurrencies? Evidence from non-parametric causality-in-quantiles techniques. Financ. Res. Lett. 2021, 47, 102569. [Google Scholar] [CrossRef]

- Naeem, M.A.; Qureshi, S.; Rehman, M.U.; Balli, F. COVID-19 and cryptocurrency market: Evidence from quantile connectedness. Appl. Econ. 2022, 54, 280–306. [Google Scholar] [CrossRef]

- Yousaf, I.; Ali, S. Discovering interlinkages between major cryptocurrencies using high-frequency data: New evidence from COVID-19 pandemic. Financ. Innov. 2020, 6, 45. [Google Scholar] [CrossRef] [PubMed]

- Özdemir, O. Cue the volatility spillover in the cryptocurrency markets during the COVID-19 pandemic: Evidence from DCC-GARCH and wavelet analysis. Financ. Innov. 2022, 8, 12. [Google Scholar] [CrossRef] [PubMed]

- Bariviera, A.F.; Merediz-Solà, I. Where do we stand in cryptocurrencies economic research? A survey based on hybrid analysis. J. Econ. Surv. 2021, 35, 377–407. [Google Scholar] [CrossRef]

- Wątorek, M.; Kwapień, J.; Drożdż, S. Multifractal Cross-Correlations of Bitcoin and Ether Trading Characteristics in the Post-COVID-19 Time. Futur. Internet 2022, 14, 215. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Roubaud, D. Herding behaviour in cryptocurrencies. Financ. Res. Lett. 2018, 29, 216–221. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. Group transfer entropy with an application to cryptocurrencies. Phys. A Stat. Mech. Appl. 2019, 516, 543–551. [Google Scholar] [CrossRef]

- Wang, G.-J.; Xie, C.; Chen, S.; Yang, J.-J.; Yang, M.-Y. Random matrix theory analysis of cross-correlations in the US stock market: Evidence from Pearson’s correlation coefficient and detrended cross-correlation coefficient. Phys. A Stat. Mech. Appl. 2013, 392, 3715–3730. [Google Scholar] [CrossRef]

- Vidal-Tomás, D. Which cryptocurrency data sources should scholars use? Int. Rev. Financ. Anal. 2022, 81, 102061. [Google Scholar] [CrossRef]

- Pericoli, M.; Sbracia, M. A Primer on Financial Contagion. J. Econ. Surv. 2003, 17, 571–608. [Google Scholar] [CrossRef]

- Pal, D.; Mitra, S.K. Interdependence between crude oil and world food prices: A detrended cross correlation analysis. Phys. A Stat. Mech. Appl. 2018, 492, 1032–1044. [Google Scholar] [CrossRef]

- Costa, N.; Silva, C.; Ferreira, P. Long-Range Behaviour and Correlation in DFA and DCCA Analysis of Cryptocurrencies. Int. J. Financ. Stud. 2019, 7, 51. [Google Scholar] [CrossRef]

- Ferreira, P.; Dionisio, A. Revisiting Covered Interest Parity in the European Union: The DCCA Approach. Int. Econ. J. 2015, 29, 597–615. [Google Scholar] [CrossRef]

- Guedes, E.; Dionísio, A.; Ferreira, P.J.; Zebende, G.F. DCCA cross-correlation in blue-chips companies: A view of the 2008 financial crisis in the Eurozone. Phys. A Stat. Mech. Appl. 2017, 479, 38–47. [Google Scholar] [CrossRef]

- Podobnik, B.; Stanley, H.E. Detrended Cross-Correlation Analysis: A New Method for Analyzing Two Nonstationary Time Series. Phys. Rev. Lett. 2008, 100, 084102. [Google Scholar] [CrossRef]

- Peng, C.-K.; Buldyrev, S.V.; Havlin, S.; Simons, M.; Stanley, H.E.; Goldberger, A.L. Mosaic organization of DNA nucleotides. Phys. Rev. E 1994, 49, 1685–1689. [Google Scholar] [CrossRef]

- Zebende, G. DCCA cross-correlation coefficient: Quantifying level of cross-correlation. Phys. A Stat. Mech. Appl. 2011, 390, 614–618. [Google Scholar] [CrossRef]

- Zebende, G.; Filho, A.M. Cross-correlation between time series of vehicles and passengers. Phys. A Stat. Mech. Appl. 2009, 388, 4863–4866. [Google Scholar] [CrossRef]

- Guedes, E.F.; Brito, A.A.; Oliveira Filho, F.M.; Fernandez, B.F.; de Castro AP, N.; da Silva Filho, A.M.; Zebende, G.F. Statistical test for ΔρDCCA cross-correlation coefficient. Phys. A Stat. Mech. Appl. 2018, 501, 134–140. [Google Scholar] [CrossRef]

- Kristoufek, L. Measuring correlations between non-stationary series with DCCA coefficient. Phys. A Stat. Mech. Appl. 2014, 402, 291–298. [Google Scholar] [CrossRef]

- Zhao, X.; Shang, P.; Huang, J. Several Fundamental Properties of DCCA Cross-Correlation Coefficient. Fractals 2017, 25, 1750017. [Google Scholar] [CrossRef]

- Podobnik, B.; Jiang, Z.-Q.; Zhou, W.-X.; Stanley, H.E. Statistical tests for power-law cross-correlated processes. Phys. Rev. E 2011, 84, 066118. [Google Scholar] [CrossRef] [PubMed]

- da Silva, M.F.; Pereira, J.D.A.L.; Filho, A.M.D.S.; de Castro, A.P.N.; Miranda, J.G.V.; Zebende, G.F. Quantifying the contagion effect of the 2008 financial crisis between the G7 countries (by GDP nominal). Phys. A Stat. Mech. Appl. 2016, 453, 1–8. [Google Scholar] [CrossRef]

- Guedes, E.F.; Brito, A.A.; Oliveira Filho, F.M.; Fernandez, B.F.; de Castro AP, N.; da Silva Filho, A.M.; Zebende, G.F. Statistical test for ΔρDCCA: Methods and data. Data Brief 2018, 18, 795–798. [Google Scholar] [CrossRef] [PubMed]

- Almeida, D.; Dionísio, A.; Vieira, I.; Ferreira, P. COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches. Entropy 2023, 25, 98. [Google Scholar] [CrossRef]

- Yamey, G.; Schäferhoff, M.; Aars, O.K.; Bloom, B.; Carroll, D.; Chawla, M.; Dzau, V.; Echalar, R.; Gill, I.S.; Godal, T.; et al. Financing of international collective action for epidemic and pandemic preparedness. Lancet Glob. Heal. 2017, 5, e742–e744. [Google Scholar] [CrossRef]

- Smith, S.S. ESG & Other Emerging Technology Applications. In Blockchain Artificial Intelligence and Financial Services; Springer: Berlin/Heidelberg, Germany, 2020; pp. 175–191. [Google Scholar]

- Laboure, M.; Müller, M.H.; Heinz, G.; Singh, S.; Köhling, S. Cryptocurrencies and CBDC: The Route Ahead. Glob. Policy 2021, 12, 663–676. [Google Scholar] [CrossRef]

- Wang, Y.; Lucey, B.; Vigne, S.A.; Yarovaya, L. An index of cryptocurrency environmental attention (ICEA). China Financ. Rev. Int. 2022, 12, 378–414. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Cryptocurrency | Start Date | Market Capitalization (USD) | |||

|---|---|---|---|---|---|

| 1 | Bitcoin | BTC | 29 April 2013 | 162,684,945,903 | 61.77% |

| 2 | Ethereum | ETH | 7 August 2015 | 26,164,459,704 | 9.93% |

| 3 | Ripple | XRP | 4 August 2013 | 26,164,459,704 | 9.93% |

| 4 | Bitcoin Cash | BCH | 23 July 2017 | 6,059,789,428 | 2.30% |

| 5 | Bitcoin SV | BSV | 9 November 2018 | 4,290,029,659 | 1.63% |

| 6 | Tether | USDT | 25 February 2015 | 4,643,212,805 | 1.76% |

| 7 | Litecoin | LTC | 29 April 2013 | 3,889,681,824 | 1.48% |

| 8 | EOS | EOS | 1 July 2017 | 3,366,250,140 | 1.28% |

| 9 | BinanceCoin | BNB | 25 July 2017 | 3,138,663,736 | 1.19% |

| 10 | Tezos | XTZ | 2 October 2017 | 2,103,907,641 | 0.80% |

| 11 | ChainLink | LINK | 20 September 2017 | 1,520,607,569 | 0.58% |

| 12 | Cardano | ADA | 1 October 2017 | 1,268,987,677 | 0.48% |

| 13 | Stellar | XLM | 5 August 2014 | 1,183,231,787 | 0.45% |

| 14 | TRON | TRX | 13 September 2017 | 1,136,886,287 | 0.43% |

| 15 | Monero | XMR | 21 May 2014 | 1,143,443,765 | 0.43% |

| 16 | Huobi Token | HT | 3 February 2018 | 1,063,188,577 | 0.40% |

| Total | 249,821,746,206 | 94.86% | |||

| Cryptocurrency | Before 31 December 2019 | After 31 December 2019 | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | Stdev. | Skewness | Kurtosis | Mean | Stdev. | Skewness | Kurtosis | |

| BTC | 0.0016 | 0.0427 | −0.1527 | 10.7409 | 0.0039 | 0.0414 | −3.4812 | 44.5290 |

| ETH | 0.0024 | 0.0714 | −3.4274 | 74.6109 | 0.0060 | 0.0551 | −2.5411 | 29.9171 |

| XRP | 0.0015 | 0.0727 | 2.0756 | 32.9133 | 0.0021 | 0.0660 | −0.3960 | 26.4318 |

| BCH | −0.0008 | 0.0794 | 0.6179 | 10.4098 | 0.0018 | 0.0603 | −1.8145 | 24.2868 |

| BSV | 0.0008 | 0.0901 | 0.8643 | 19.9132 | 0.0015 | 0.0814 | 2.8755 | 46.5471 |

| USDT | −0.0001 | 0.0211 | −12.2749 | 829.3628 | 0.0000 | 0.0055 | 0.1522 | 37.9746 |

| LTC | 0.0009 | 0.0645 | 1.7163 | 28.5632 | 0.0030 | 0.0540 | −1.5536 | 16.3358 |

| EOS | 0.0010 | 0.0827 | 2.2245 | 27.6377 | 0.0030 | 0.0545 | −2.0790 | 22.8957 |

| BNB | 0.0055 | 0.0787 | 1.3888 | 15.1944 | 0.0003 | 0.0502 | −3.3523 | 38.3843 |

| XTZ | −0.0004 | 0.0751 | 0.1255 | 10.5396 | 0.0019 | 0.0634 | −2.1090 | 24.3520 |

| LINK | 0.0027 | 0.0812 | 0.7048 | 7.1339 | 0.0065 | 0.0711 | −1.4227 | 18.0953 |

| ADA | 0.0003 | 0.0792 | 2.9094 | 29.3140 | 0.0061 | 0.0623 | −1.1089 | 14.6842 |

| XLM | 0.0015 | 0.0754 | 2.0089 | 19.6020 | 0.0050 | 0.0668 | 1.6195 | 21.9256 |

| TRX | 0.0023 | 0.0963 | 2.1343 | 19.3240 | 0.0022 | 0.0545 | −2.2636 | 24.9947 |

| XMR | 0.0016 | 0.0703 | 0.6497 | 9.6001 | 0.0029 | 0.0509 | −2.4056 | 26.4712 |

| HT | 0.0009 | 0.0518 | 0.6165 | 7.6063 | 0.0021 | 0.0431 | −3.5911 | 49.8863 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almeida, D.; Dionísio, A.; Ferreira, P.; Vieira, I. Impact of the COVID-19 Pandemic on Cryptocurrency Markets: A DCCA Analysis. FinTech 2023, 2, 294-310. https://doi.org/10.3390/fintech2020017

Almeida D, Dionísio A, Ferreira P, Vieira I. Impact of the COVID-19 Pandemic on Cryptocurrency Markets: A DCCA Analysis. FinTech. 2023; 2(2):294-310. https://doi.org/10.3390/fintech2020017

Chicago/Turabian StyleAlmeida, Dora, Andreia Dionísio, Paulo Ferreira, and Isabel Vieira. 2023. "Impact of the COVID-19 Pandemic on Cryptocurrency Markets: A DCCA Analysis" FinTech 2, no. 2: 294-310. https://doi.org/10.3390/fintech2020017

APA StyleAlmeida, D., Dionísio, A., Ferreira, P., & Vieira, I. (2023). Impact of the COVID-19 Pandemic on Cryptocurrency Markets: A DCCA Analysis. FinTech, 2(2), 294-310. https://doi.org/10.3390/fintech2020017