A Systematic Literature Review of Empirical Research on Stablecoins

Abstract

1. Introduction and Background

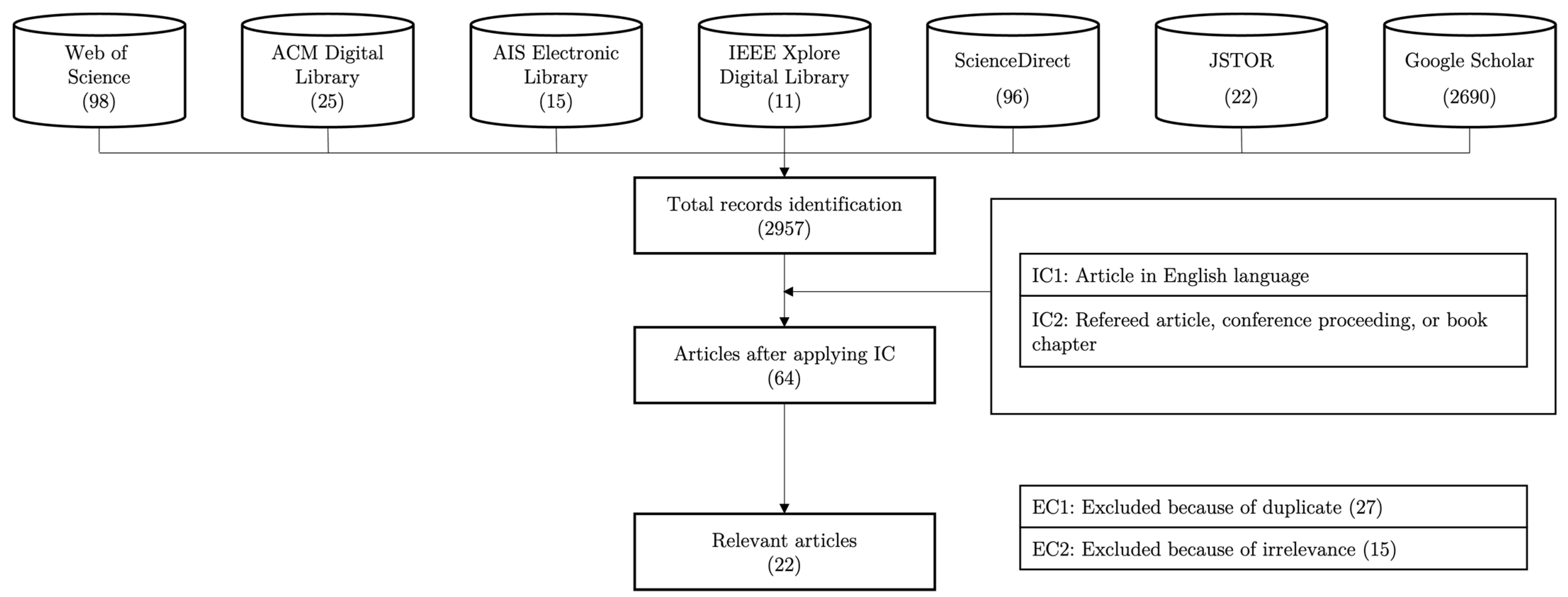

2. Methodology

3. Results

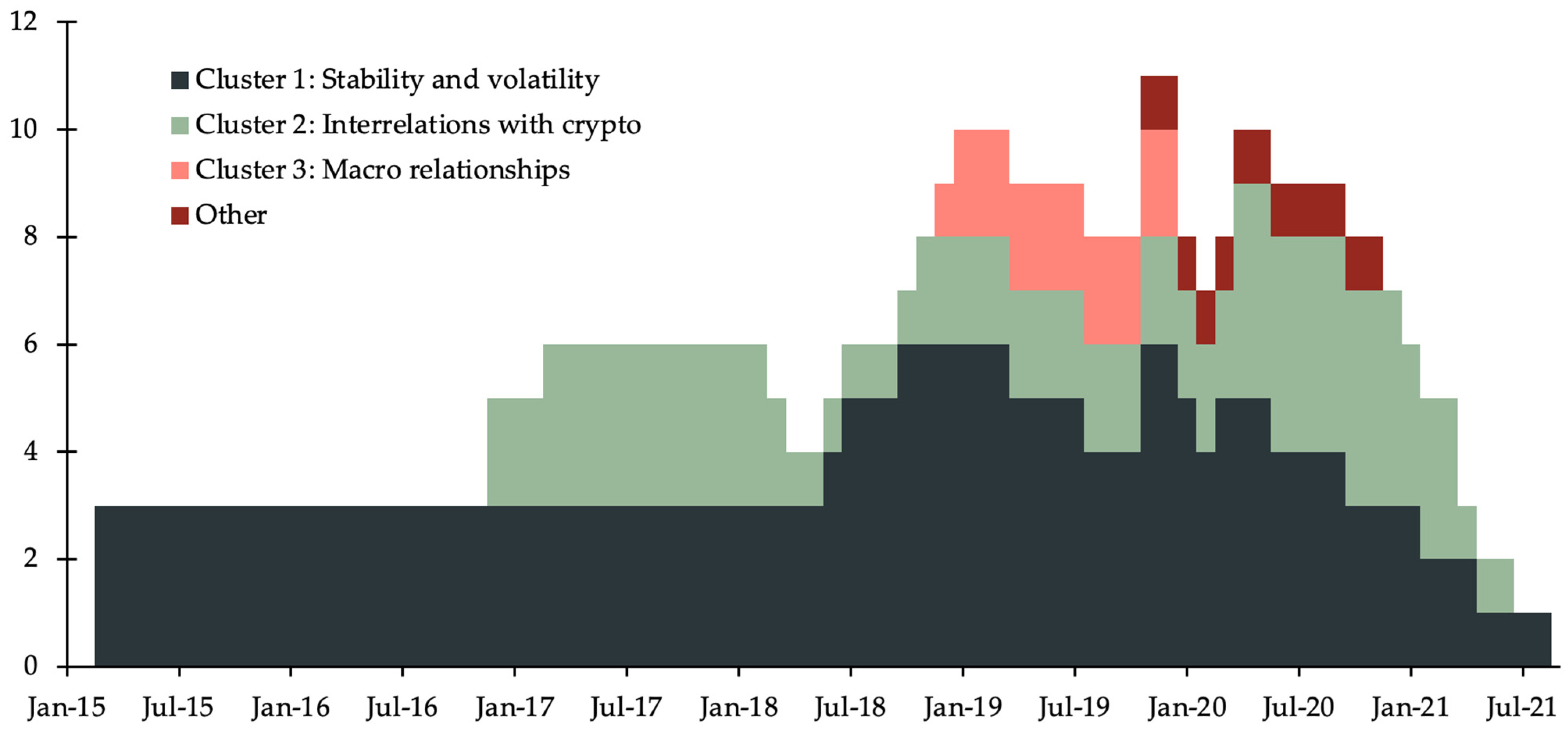

3.1. Thematic Clusters of Stablecoin Research

3.2. Statistical Approaches

3.3. Variables, Data, and Data Sources

3.4. Future Research on Stablecoins Mentioned in the Surveyed Literature

4. Literature Gaps and Open Research Paths

- Applies different methodological approaches for a range of research topics (e.g., price clustering detection, distributional characteristics, seasonality, intraday market efficiency and mean-reverting behavior, portfolio optimization, or interrelations with other market and assets);

- Includes data from more blockchains (e.g., Tron, Algorand, Solana, Avalanche);

- Includes data from more stablecoins (i.e., not “only” USDT and USDC, cf. Table 2);

- Builds on expanded datasets that are more granular (e.g., minute, tick, or block data), as well as longer time horizons that cover multiple years. Since crypto markets are ever-changing, research should best try to validate or challenge studies that rely on specific time frames since market dynamics may differ, and thus, “older” findings may not be valid anymore.

- The use of stablecoins in emerging markets: Emerging markets, such as Turkey or Argentina, suffer from high inflation rates, which could lead their citizens to turn their savings into U.S. dollars. At the same time, not all parts of the population have broad access to the banking system, financial markets, or simply U.S. dollar accounts, for example, due to regulations, such as capital controls. However, countries, such as Turkey, have a comparatively high cryptocurrency adoption rate [36]. Stablecoins might provide an option for people in these countries to access capital markets in the first place and obtain U.S. dollars over their domestic currencies in particular. A potential angle to explore this hypothesis are analyses of centralized or peer-to-peer markets of stablecoins against a respective currency, such as the Turkish lira. A survey would be another option. An important dimension should also be the possibility of regulatory intervention to support local currencies as a potential limitation to growth and adoption of stablecoins in emerging economies.

- The effect of stablecoins on the stability of currencies: The market capitalization of stablecoins amounts to USD 150 billion by October 2022 [37]. At this size, it becomes possible that stablecoins can influence the stability of currencies in general and those of emerging markets in particular. For example, capital might be channeled from a small domestic currency toward the U.S. dollar, causing a drop in the exchange rate between the currency and the U.S. dollar. A possible approach to study this relationship is to triangulate data from foreign exchange (forex) rates with data from stablecoin markets against a specific currency.

- Analyses of stablecoin users: Little is known about stablecoins users and their motivations. Users of stablecoins might be a homogenous group or differ in various respects. One or more (representative) surveys among stablecoin users in general or within specific populations/countries are a promising way to find out about the socioeconomic profiles of stablecoin users and their behavioral intentions and usage patterns of stablecoins. If such analyses are replicated and standardized across countries, it could contribute to understanding socioeconomic or cultural differences in relation to the maturity of domestic banking systems and capital markets in various geographic regions. Another, apparently geographically limiting, option could be to analyze on-chain behavior of wallets.

- Adoption and use cases of stablecoins outside of cryptocurrency trading: While stablecoins were born in cryptocurrency markets to meet the need to move fiat-denominated value between crypto exchanges at a fast pace, they are starting to expand into other areas. Little is known yet about the countries and markets where stablecoins find adoption outside of trading cryptocurrencies. For example, they could be feasible for remittances or cross-border payments in general, but they might also already be used in specific industries that are either prone to experience banking and payment issues (e.g., the cannabis industry) or that are simply attracted by the simplicity and effectiveness of stablecoin transfers. Such questions could potentially be analyzed using qualitative interviews with managers from specific industries, individuals, or companies that issue stablecoins and thus potentially know who their customers are.

- Algorithmic stablecoins. Algorithmic stablecoins represent the “holy grail” of stablecoins, promising capital-efficient, decentralized, and price-stable assets without the risk of an intermediary that necessarily comes with counterparty risk. In the past, various algorithmic stablecoins have failed, as illustrated by the collapse of Terra in 2022 [8,9]. Based on this, one can even ask the research question whether algorithmic stablecoins should actually be called “stablecoins” or if they should represent something of their own. Accordingly, we see a need to better understand, plan, classify and analyze algorithmic stablecoins. The (empirical) academic literature on the topic is still quite scarce [15,17]; however, promising (non-peer reviewed) approaches and foundations for researchers in this area can also be found [38,39,40].

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ante, L.; Fiedler, I.; Strehle, E. The Influence of Stablecoin Issuances on Cryptocurrency Markets. Financ. Res. Lett. 2021, 41, 101867. [Google Scholar] [CrossRef]

- Coingecko Tether Price Chart (USDT). Available online: https://www.coingecko.com/en/coins/tether (accessed on 7 November 2022).

- Fiedler, I.; Ante, L. Stablecoins. In The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges; Baker, K.H., Benedetti, H., Nikbakht, E., Stein Smith, S., Eds.; Emerald Publishing Limited: Bingley, UK, 2023; Volume 1. [Google Scholar]

- Bitfinex Pausing Wire Deposits to Bitfinex. Available online: https://www.bitfinex.com/posts/200 (accessed on 18 May 2020).

- Griffin, J.M.; Shams, A. Is Bitcoin Really Un-Tethered? J. Financ. 2020, 75, 1913–1964. [Google Scholar] [CrossRef]

- Brennecke, M.; Schellinger, B.; Guggenberger, T.; Urbach, N. The De-Central Bank in Decentralized Finance: A Case Study of MakerDAO. In Proceedings of the 55th Annual Hawaii International Conference on System Sciences, Maui, HI, USA, 4–7 January 2022. [Google Scholar]

- MakerDAO. The Maker Protocol: MakerDAO’s Multi-Collateral Dai (MCD) System. 2020. Available online: https://makerdao.com/whitepaper/White%20Paper%20-The%20Maker%20Protocol_%20MakerDAO%E2%80%99s%20Multi-Collateral%20Dai%20(MCD)%20System-FINAL-%20021720.pdf (accessed on 7 November 2022).

- Uhlig, H. A Luna-Tic Stablecoin Crash; NBER Working Paper Series; National Bureau of Economic Research: Cambridge, MA, USA, 2022. [Google Scholar]

- Briola, A.; Vidal-Tomás, D.; Wang, Y.; Aste, T. Anatomy of a Stablecoin’s Failure: The Terra-Luna Case. Financ. Res. Lett. 2022, 51, 103358. [Google Scholar] [CrossRef]

- Webster, J.; Watson, R.T. Analyzing the Past to Prepare for the Future: Writing a Literature Review. MIS Q. 2002, 26, xiii–xxiii. [Google Scholar]

- vom Brocke, J.; Simons, A.; Riemer, K.; Niehaves, B.; Plattfaut, R.; Cleven, A. Standing on the Shoulders of Giants: Challenges and Recommendations of Literature Search in Information Systems Research. Commun. Assoc. Inf. Syst. 2015, 37, 9. [Google Scholar] [CrossRef]

- Kitchenham, B. Procedures for Performing Systematic Reviews; Keele University Technical Report; Keele University: Keele, UK, 2004. [Google Scholar]

- Hoang, L.T.; Baur, D.G. How Stable Are Stablecoins? Eur. J. Financ. 2021, 1–17. [Google Scholar] [CrossRef]

- Ante, L.; Fiedler, I.; Strehle, E. The Impact of Transparent Money Flows: Effects of Stablecoin Transfers on the Returns and Trading Volume of Bitcoin. Technol. Soc. Chang. 2021, 170, 120851. [Google Scholar] [CrossRef]

- Jarno, K.; Kołodziejczyk, H. Does the Design of Stablecoins Impact Their Volatility? J. Risk Financ. Manag. 2021, 14, 42. [Google Scholar] [CrossRef]

- Pernice, I.G.A. On Stablecoin Price Processes and Arbitrage. In International Conference on Financial Cryptography and Data Security; Springer: Berlin/Heidelberg, Germany, 2021; pp. 124–135. [Google Scholar]

- Zhao, W.; Li, H.; Yuan, Y. Understand Volatility of Algorithmic Stablecoin: Modeling, Verification and Empirical Analysis. In International Conference on Financial Cryptography and Data Security; Springer: Berlin/Heidelberg, Germany, 2021. [Google Scholar]

- Thanh, B.N.; Hong, T.N.V.; Pham, H.; Cong, T.N.; Anh, T.P.T. Are the Stabilities of Stablecoins Connected? J. Ind. Bus. Econ. 2022. [Google Scholar] [CrossRef]

- Jalan, A.; Matkovskyy, R.; Yarovaya, L. “Shiny” Crypto Assets: A Systemic Look at Gold-Backed Cryptocurrencies during the COVID-19 Pandemic. Int. Rev. Financ. Anal. 2021, 78, 101958. [Google Scholar] [CrossRef]

- Wei, W.C. The Impact of Tether Grants on Bitcoin. Econ. Lett. 2018, 171, 19–22. [Google Scholar] [CrossRef]

- Kristoufek, L. Tethered, or Untethered? On the Interplay between Stablecoins and Major Cryptoassets. Financ. Res. Lett. 2021, 43, 101991. [Google Scholar] [CrossRef]

- Jeger, C.; Rodrigues, B.; Scheid, E.; Stiller, B. Analysis of Stablecoins during the Global COVID-19 Pandemic. In Proceedings of the 2020 Second International Conference on Blockchain Computing and Applications (BCCA), Antalya, Turkey, 2–5 November 2020; pp. 30–37. [Google Scholar]

- Kjäer, M.; di Angelo, M.; Salzer, G. Empirical Evaluation of MakerDAO’s Resilience. In Proceedings of the 2021 3rd Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS), Paris, France, 27–30 September 2021; pp. 193–200. [Google Scholar]

- Grobys, K.; Huynh, T.L.D. When Tether Says “JUMP!” Bitcoin Asks “How Low?”. Financ. Res. Lett. 2021, 47, 102644. [Google Scholar] [CrossRef]

- Grobys, K.; Junttila, J.; Kolari, J.W.; Sapkota, N. On the Stability of Stablecoins. J. Empir. Financ. 2021, 64, 207–223. [Google Scholar] [CrossRef]

- Wasiuzzaman, S.; Haji Abdul Rahman, H.S.W. Performance of Gold-Backed Cryptocurrencies during the COVID-19 Crisis. Financ. Res. Lett. 2021, 43, 101958. [Google Scholar] [CrossRef]

- Aloui, C.; ben Hamida, H.; Yarovaya, L. Are Islamic Gold-Backed Cryptocurrencies Different? Financ. Res. Lett. 2021, 39, 101615. [Google Scholar] [CrossRef]

- Baur, D.G.; Hoang, L.T. A Crypto Safe Haven against Bitcoin. Financ. Res. Lett. 2021, 38, 101431. [Google Scholar] [CrossRef]

- Wang, G.-J.; Ma, X.; Wu, H. Are Stablecoins Truly Diversifiers, Hedges, or Safe Havens against Traditional Cryptocurrencies as Their Name Suggests? Res. Int. Bus. Financ. 2020, 54, 101225. [Google Scholar] [CrossRef]

- Nguyen, T.V.H.; Nguyen, T.V.H.; Nguyen, T.C.; Pham, T.T.A.; Nguyen, Q.M.P. Stablecoins versus Traditional Cryptocurrencies in Response to Interbank Rates. Financ. Res. Lett. 2022, 47, 102744. [Google Scholar] [CrossRef]

- Bojaj, M.M.; Muhadinovic, M.; Bracanovic, A.; Mihailovic, A.; Radulovic, M.; Jolicic, I.; Milosevic, I.; Milacic, V. Forecasting Macroeconomic Effects of Stablecoin Adoption: A Bayesian Approach. Econ. Model. 2022, 109, 105792. [Google Scholar] [CrossRef]

- Yousaf, I.; Yarovaya, L. Spillovers between the Islamic Gold-Backed Cryptocurrencies and Equity Markets during the COVID-19: A Sectorial Analysis. Pac.-Basin. Financ. J. 2022, 71, 101705. [Google Scholar] [CrossRef]

- Fry, J.; Cheah, E.T. Negative Bubbles and Shocks in Cryptocurrency Markets. Int. Rev. Financ. Anal. 2016, 47, 343–352. [Google Scholar] [CrossRef]

- Corbet, S.; Lucey, B.; Yarovaya, L. Datestamping the Bitcoin and Ethereum Bubbles. Financ. Res. Lett. 2018, 26, 81–88. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E.; Shephard, N. Econometrics of Testing for Jumps in Financial Economics Using Bipower Variation. J. Financ. Econom. 2006, 4, 1–30. [Google Scholar] [CrossRef]

- Ante, L.; Fiedler, F.; Steinmetz, F.; Fiedler, I. Profiling and Characterizing Turkish Cryptocurrency Owners, BRL Working Paper Series No. 27; Blockchain Research Lab.: Hamburg, Germany, 2022.

- CoinGecko Stablecoins. Available online: https://www.coingecko.com/en/categories/stablecoins (accessed on 6 October 2022).

- Bullmann, D.; Klemm, J.; Pinna, A. In Search for Stability in Crypto-Assets: Are Stablecoins the Solution? ECB Occasional Paper Series; European Central Bank: Frankfurt, Germany, 2019. [Google Scholar] [CrossRef]

- Clements, R. Built to Fail: The Inherent Fragility of Algorithmic Stablecoins. Wake For. Law Rev 2021, 11, 131. [Google Scholar] [CrossRef]

- Frax Frax: Fractional-Algorithmic Stablecoin Protocol—A New Category of Decentralized Stablecoin with a Novel Mechanism. Available online: https://docs.frax.finance/ (accessed on 7 November 2022).

- Jumde, A.; Cho, B.Y. Can Cryptocurrencies Overtake the Fiat Money. Int. J. Bus. Perform. Manag. 2020, 21, 6. [Google Scholar] [CrossRef]

- Senner, R.; Sornette, D. The Holy Grail of Crypto Currencies: Ready to Replace Fiat Money? J. Econ. Issues 2019, 53, 966–1000. [Google Scholar] [CrossRef]

- Gunay, S.; Kaskaloglu, K.; Muhammed, S. Bitcoin and Fiat Currency Interactions: Surprising Results from Asian Giants. Mathematics 2021, 9, 1395. [Google Scholar] [CrossRef]

- Akyildirim, E.; Aysan, A.F.; Cepni, O.; Darendeli, S.P.C. Do Investor Sentiments Drive Cryptocurrency Prices? Econ. Lett. 2021, 206, 109980. [Google Scholar] [CrossRef]

- Anamika; Chakraborty, M.; Subramaniam, S. Does Sentiment Impact Cryptocurrency? J. Behav. Financ. 2021, 1–17. [Google Scholar] [CrossRef]

- Gurdgiev, C.; O’Loughlin, D. Herding and Anchoring in Cryptocurrency Markets: Investor Reaction to Fear and Uncertainty. J. Behav. Exp. Financ. 2020, 25, 100271. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| ID | Reference | Title | Journal/Conference | Topic |

|---|---|---|---|---|

| 1 | Hoang and Baur [13] | How stable are stablecoins? | The European Journal of Finance | Stability of stablecoins and proposal of a framework to test for absolute and relative stability |

| 2 | Ante et al. [14] | The impact of transparent money flows: Effects of stablecoin transfers on the returns and trading volume of Bitcoin | Technological Forecasting and Social Change | Effect of large stablecoin transfers and their effect on Bitcoin returns and trading volume |

| 3 | Ante et al. [1] | The Influence of Stablecoin Issuances on Cryptocurrency Markets | Finance Research Letters | Influence of large stablecoin issuances on the return of major cryptocurrencies |

| 4 | Jarno and Kołodziejczyk [15] | Does the Design of Stablecoins Impact Their Volatility? | Journal of Risk and Financial Management | Average volatility of different stablecoin designs |

| 5 | Pernice [16] | On Stablecoin Price Processes and Arbitrage | Financial Cryptography and Data Security | Analysis of arbitrage processes and price determination |

| 6 | Zhao et al. [17] | Understand Volatility of Algorithmic Stablecoin: Modeling, Verification and Empirical Analysis | International Conference on Financial Cryptography and Data Security | Key design of three algorithmic stablecoin designs, volatile by design in theory and/or in practice? |

| 7 | Thanh et al. [18] | Are the stabilities of stablecoins connected? | Journal of Industrial and Business Economics | Connections between stability of different stablecoins |

| 8 | Jalan et al. [19] | “Shiny” crypto assets: A systemic look at gold-backed cryptocurrencies during the COVID-19 pandemic | International Review of Financial Analysis | Performance of gold-backed stablecoins during the COVID-19 pandemic; compared to gold |

| 9 | Griffin and Shams [5] | Is Bitcoin Really Un-Tethered? | The Journal of Finance | Influence of stablecoin Tether on the prices of Bitcoin in 2017 |

| 10 | Wei [20] | The impact of Tether grants on Bitcoin | Economics Letters | Impact of Tether issuances on the price and trading volume of Bitcoin |

| 11 | Kristoufek [21] | Tethered, or Untethered? On the interplay between stablecoins and major cryptoassets | Finance Research Letters | Connection between stablecoin issuances and the price of other cryptocurrencies |

| 12 | Jeger et al. [22] | Analysis of Stablecoins during the Global COVID-19 Pandemic | Procedia Computer Science | Different stablecoin stability mechanics and their performance during the 2020 crisis |

| 13 | Kjäer et al. [23] | Empirical Evaluation of MakerDAO’s Resilience | Blockchain, Robotics and AI for Networking Security Conference (BRAINS) | MakerDAO’s resilience during first year from November 2019 to 2020 |

| 14 | Grobys and Huynh [24] | When Tether says “JUMP!” Bitcoin asks “How low?” | Finance Research Letters | Impact of high fluctuation in Tether price (jump) on Bitcoin price |

| 15 | Grobys et al. [25] | On the stability of stablecoins | Journal of Empirical Finance | Stablecoin volatility and connection to Bitcoin volatility |

| 16 | Wasiuzzaman and Haji Abdul Rahman [26] | Performance of gold-backed cryptocurrencies during the COVID-19 crisis | Finance Research Letters | Performance of gold-backed stablecoins during COVID-19 crisis, especially in 2020 (bear market) |

| 17 | Aloui et al. [27] | Are Islamic gold-backed cryptocurrencies different? | Finance Research Letters | Comparison of Islamic gold-backed stablecoins and conventional ones |

| 18 | Baur and Hoang [28] | A crypto safe haven against Bitcoin | Finance Research Letters | Analysis of stablecoins as a safe haven for crypto investors |

| 19 | Wang et al. [29] | Are stablecoins truly diversifiers, hedges, or safe havens against traditional cryptocurrencies as their name suggests? | Research in International Business and Finance | Diversifier, hedge, and save haven properties of different stablecoins against conventional cryptocurrencies |

| 20 | Nguyen et al. [30] | Stablecoins versus traditional cryptocurrencies in response to interbank rates | Finance Research Letters | The impacts of the United States (U.S.) federal funds rate and Chinese interbank rate on the behaviors of stablecoins and traditional cryptocurrencies |

| 21 | Bojaj et al. [31] | Forecasting macroeconomic effects of stablecoin adoption: A Bayesian approach | Economic Modelling | Effect of stablecoin adoption on key macroeconomic factors in Montenegro. |

| 22 | Yousaf and Yarovaya [32] | Spillovers between the Islamic gold-backed cryptocurrencies and equity markets during the COVID-19: A sectorial analysis | Pacific-Basis Finance Journal | Return and volatility transmission between the Islamic gold-backed cryptocurrencies and global Islamic equities. |

| Stablecoin | Stablecoin Characteristics | Prevalence in the Empirical Literature | ||||||

|---|---|---|---|---|---|---|---|---|

| Ticker | Mcap (USD m) | Peg | Collateral/Type | # | % | IDs (cf. Table 1) | ||

| 1 | Tether | USDT | 66,077 | USD | Cash and cash equivalents | 16 | 73 | 1–5,7–12,14,15,18–20 |

| 2 | USD Coin | USDC | 55,531 | USD | Cash and cash equivalents | 11 | 50 | 1–5,7,11,12,15,18,20 |

| 3 | Binance USD | BUSD | 17,878 | USD | Cash | 5 | 23 | 2,3,5,11,15 |

| 4 | Dai | DAI | 6476 | USD | Cryptocurrency incl. stablecoins | 9 | 41 | 3–5,7,11–13,15,17 |

| 5 | Frax | FRAX | 1368 | USD | Algorithmic | 0 | 0 | - |

| 6 | TrueUSD | TUSD | 1220 | USD | Cash | 8 | 36 | 1,4,7,11,15,17–19 |

| 7 | Paxos Dollar | USDP | 853 | USD | Cash | 9 | 41 | 1–5,7,11,17,19 |

| 8 | Neutrino USD | USDN | 750 | USD | Algorithmic | 0 | 0 | - |

| 9 | USDD | USDD | 721 | USD | Algorithmic | 0 | 0 | - |

| 10 | Paxos Gold | PAXG | 587 | XAU | Gold | 2 | 9 | 8,12 |

| 11 | TerraClassic USD | USTC | 481 | USD | Algorithmic | 0 | 0 | - |

| 12 | Tether Gold | XAUT | 428 | XAU | Gold | 1 | 5 | 8 |

| 13 | Fei USD | FEI | 358 | USD | Algorithmic | 0 | 0 | - |

| 14 | Euro Tether | EURT | 210 | EUR | Cash | 0 | 0 | - |

| 15 | Magic Internet Money | MIM | 196 | USD | Cryptocurrency incl. stablecoins | 0 | 0 | - |

| 16 | Gemini Dollar | GUSD | 186 | USD | Cash | 7 | 32 | 1–5,11,17 |

| 17 | Alchemix USD | ALUSD | 186 | USD | Stablecoins (DAI) | 0 | 0 | - |

| 18 | Liquity USD | LUSD | 173 | USD | Cryptocurrency | 0 | 0 | - |

| 19 | STASIS EURO | EURS | 126 | EUR | Cash | 3 | 14 | 1,4,19 |

| 20 | HUSD | HUSD | 110 | USD | Cash | 4 | 18 | 2,3,5,11 |

| Main Stablecoin Metrics Considered | |||||

|---|---|---|---|---|---|

| Pricing/Returns | Market Cap/Supply | Trading Volume | Blockchain Transactions | ||

| Time interval | Minute * | [1] | [1] | [1] | |

| Hourly | [5,6,9,14,18] | [9] | [2,3,9] | ||

| Daily | [4,7,8,10,12,16,17,19,20] | [10–12,20] | [10,12] | ||

| Blocks | [13] | ||||

| Data source | Market data aggregators | [1,4,5–9,12,16,17,19,20,22] | [1,9,11,12,20] | [1,12] | [9] |

| Cryptocurrency exchanges | [14,18] | ||||

| Blockchain explorers | [9,10] | [2,3,9,13] | |||

| Blockchain nodes/clients | [13] | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ante, L.; Fiedler, I.; Willruth, J.M.; Steinmetz, F. A Systematic Literature Review of Empirical Research on Stablecoins. FinTech 2023, 2, 34-47. https://doi.org/10.3390/fintech2010003

Ante L, Fiedler I, Willruth JM, Steinmetz F. A Systematic Literature Review of Empirical Research on Stablecoins. FinTech. 2023; 2(1):34-47. https://doi.org/10.3390/fintech2010003

Chicago/Turabian StyleAnte, Lennart, Ingo Fiedler, Jan Marius Willruth, and Fred Steinmetz. 2023. "A Systematic Literature Review of Empirical Research on Stablecoins" FinTech 2, no. 1: 34-47. https://doi.org/10.3390/fintech2010003

APA StyleAnte, L., Fiedler, I., Willruth, J. M., & Steinmetz, F. (2023). A Systematic Literature Review of Empirical Research on Stablecoins. FinTech, 2(1), 34-47. https://doi.org/10.3390/fintech2010003