2.1. The League Equilibrium without Revenue Sharing

The first economic model of a professional sports league [

19] incorporated an N-team league and could not provide exact solutions for a revenue sharing league equilibrium due to its complexity. Simplifying the exposition to a two-team model has become standard practice as it allows for easier solutions for the league equilibrium without sacrificing generality. A commonly used model assumes two clubs, one large-market, the other small-market, that each choose a stock of talent to maximize profit. Talent is costly but is assumed to be available in any amount without poaching talent from the competing club. The stock of talent results in a club winning percentage through a contest success function. Clubs will equalize their marginal revenues from winning contests and their optimal winning percentages will be revealed at the league equilibrium. At this point, revenue sharing is introduced in the model and its effect on parity is revealed at the new solution for the league equilibrium. Assuming numerical values for the parameters in the league model allows for the solution of the revenue transfer from the large- to small-market club. A league model by Kesenne [

20] is a simple example of league models in the literature.

The two-team league model derives a profit-maximization combination of winning percentages that add up to one. Team revenue is a positive function of the team winning percentage at a diminishing rate, reaching a maximum at a winning percentage of 1.0. The team market size acts as a scalar, shifting the revenue function upward with a larger market size. We assume that team A operates in a larger market size than team B, but it makes no difference to the exposition if this assumption is reversed. If both clubs have identical market sizes, the equilibrium will be identical winning percentages, . Each club produces outputs (hits, runs, goals, etc.) that translate into wins through an unspecified production function. Revenue is obtained through tickets sales via a demand curve that is also unspecified. This approach to the two-team league model ignores the deeper workings of production and demand, but it has become the standard approach. One can think of the market size as a scalar in the ticket demand function. Each club is assumed to be a local monopoly but together they act as a sort of joint venture since output cannot be produced by one club without the other.

Figure 3 provides a representation of the revenue functions, with the team A revenue function lying everywhere above team B’s revenue function due to its larger market size. The total revenue curve for team A is steeper than that for team B at any winning percentage, hence

at any winning percentage.

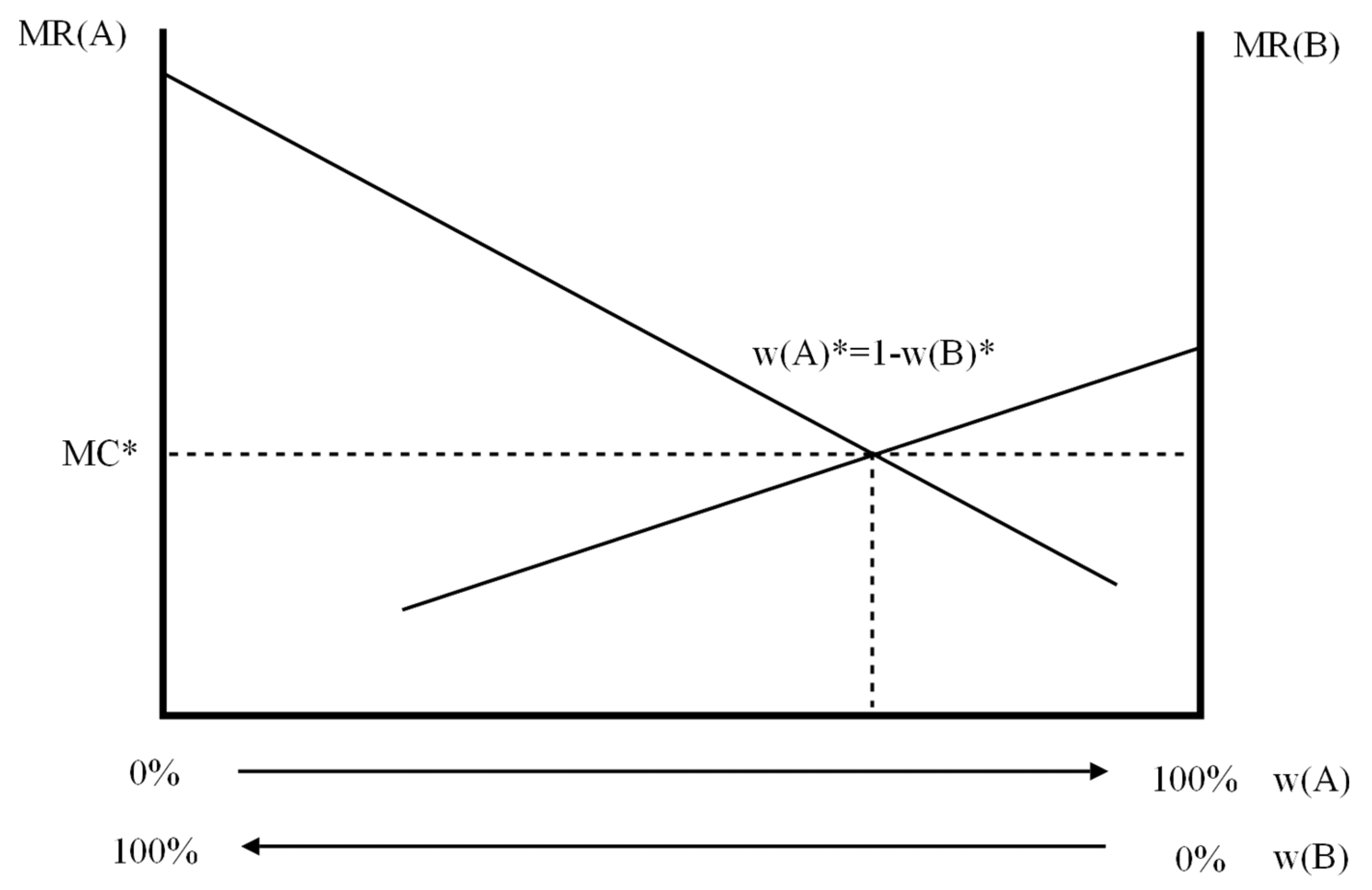

The league equilibrium can be found graphically by placing both marginal revenue lines in the same diagram, as depicted in

Figure 4. Ties are not allowed and the winning percentage for each club,

and

, can be placed on the horizontal axis in opposite directions due to the adding up property.

As a local monopolist, each will hire quality talent up to the point where . It is important to note that this is the marginal cost of winning, not the marginal cost of talent, although they are often treated the same way in the literature. Both clubs can maximize profit only where the marginal revenue lines intersect. We denote the equilibrium winning percentages for the two clubs as and . The marginal cost of winning will be for both teams. Here, we introduce the original statement of the invariance principle: the ultimate allocation of talent will be invariant to the initial allocation if player cash sales are allowed. Suppose initially that due to team A having a larger stock of talent than team B. It is profitable for team A to buy quality players from team B to improve its winning percentage since . Total revenue for team A will increase until is reached, at which point there is no further incentive to purchase talent from team B. If , then and the opposite will occur, team B will purchase talent from team A, increasing its revenue until the league equilibrium is reached. The league equilibrium is reached regardless of the initial allocation of talent. The total league revenue is the area under the two marginal revenue lines at the league equilibrium. Any other combination of winning percentages will fail to maximize the league revenue.

The upshot is that it is profit-maximizing for the two-team league to have the larger-market team A have a larger talent stock and win a majority of its games. The invariance principle requires that cash sales of players be allowed in the league so that talent can move to its most valued team. Cash sales have become infrequent in North American professional sports leagues since the 1970s, except for minor-league players or players of lesser talent. European football leagues maintain a transfer system that allows cash sales of players within and across borders.

Further results can be found by specifying an algebraic model of the two-team sports league. Team A’s revenue is a function of its market size,

, and its winning percentage,

.

An increase in

shifts the revenue function upward, assumedly due to an upward shift in the demand curve for tickets, for a given winning percentage. The units for

are left unspecified, but typically are the local metropolitan population in empirical studies. Revenue is a weighted average

of the team A winning percentage, with the second term measuring the closeness of the winning percentages. This property of (1) is known as the uncertainty of outcome hypothesis or UOH. Since

, the product of the two winning percentages reaches a maximum when

and the contribution of the UOH to revenue is maximized. After collecting the

terms, (1) can be rewritten as (2) below.

Each club acquires a stock of talent that generates a winning percentage specified by a logistic contest success function

. At this point, it is necessary to distinguish between an open or closed talent market. For this, we consider the effect on

when team A increases its stock of talent

.

In the open talent market case, there is no need for team A to poach talent from team B as there is an infinite supply of talent in the market, hence

and (3) reduces to

. Team A can only increase its talent stock by poaching talent from team B in the closed market talent case, hence

. The result is that (3) reduces to

. It is easy to show that

increases by more in the closed talent market case. Both are extreme cases, and the availability of talent is somewhere in between. Rockerbie and Easton [

21] specify a club talent stock,

, that is a function of the team payroll relative to the total league payroll that allows for a flexible talent market: open, closed, or in between. The approach is not directly applicable here as it addresses the complementarity between stadium investments and investments in club talent. One could also interpret the derivative as a talent conjecture, that is, the anticipated response of team B to an increase in

, instead of a physical talent market constraint. Easton and Rockerbie [

22] consider the cases of the Cournot competitive and cartel conjectures. Szymanski [

23] argues that the Cournot conjecture is the only consistent conjecture to reach a league equilibrium in the open talent market case. The closed talent market case is more difficult to solve with Cournot conjectures [

24].

The marginal revenue for team A is given by

. The marginal revenue for team B is

. Assume for simplicity that

for both teams. If

, then

when

or 100%. This is thought to be a desirable property. We have already shown that league revenue is maximized where

. Simplifying, this gives the league equilibrium condition below.

Simplifying further gives the league equilibrium in (5) below.

The extent to which the winning percentage for team A rises above 0.5 is determined by the square root of the market size ratio, referred to as the competitive balance ratio. The relative talent stocks are found by inserting the logistic contest success function for the winning percentages in (5) and simplifying.

The ratio of the profit-maximizing talent stocks is the square root of the local market size ratio. This result assumes an open talent market where each team can acquire all the talent it desires without increasing the market wage rate for talent. The closed talent market result can be found in Vrooman [

25], who showed that the league equilibrium is characterized by less parity than in the open talent market case above. This has come to be the standard algebraic model of the two-team professional sports league [

26,

27]. Its advantage is that it incorporates the UOH in the revenue functions for both clubs. Unfortunately, it is difficult algebraically to solve for the league equilibrium with revenue sharing, so we use a simpler model in the next section and follow that with the above model, solved using simulation.

2.2. The League Equilibrium with Revenue Sharing

We now consider revenue sharing without any other league policies to redistribute revenues or to restrict the behaviors of club owners. Marburger [

28] considers revenue sharing and a luxury tax in a two-team sports league model. The luxury tax used in MLB, now known as the competitive balance tax, taxes the overage of club payroll above a threshold value, providing an incentive for clubs not to spend lavishly on players. The tax rate increases for repeat offenders. The luxury tax improves league parity if it is binding for the large-market club. The NBA adopted a payroll cap and individual salary cap in 1984, followed by the NFL in 1994 and the NHL in 2006. MLB does not feature a payroll or salary cap. Dietl et al. [

29] construct a two-team league model of profit-maximizing club owners that use revenue sharing and a club payroll cap and find that the effect on league parity depends upon whether the payroll cap is binding for both clubs or only one club, and in each case is based on the difference in market sizes. The NFL, NBA, and NHL also feature a fixed sharing of anticipated league revenue to the players (48%, 57%, and 57%, respectively). This amount is divided evenly between the member clubs to establish a club salary cap. Spending above the club salary cap is punished with a variety of financial penalties. The club salary cap is determined by anticipated league revenue, which is determined by the profit-maximizing behavior of club owners. This endogeneity issue is addressed by Fujimoto [

30] in an N-team sports league model that incorporates a time to accumulate talent and a fixed new flow of available talent each season (an amateur draft). The invariance principle is rejected.

In pool revenue sharing, a share

of its local revenue is kept by each club, with the rest, (

), contributed to a central pool managed by the league. Team A’s net revenue after sharing (a superscript

S denotes after revenue sharing) depends upon its own local revenue as well as that of team B. The same is true for team B’s revenue after sharing. We assume that the central fund is split evenly between the two teams at the end of the playing season.

The marginal revenues are given below.

Why does

appear in (9)? Team A increases its net revenue by

when it increases its winning percentage, due to its share of the higher local revenue in the first term in (9), part of which is returned from the central pool. Team B’s winning percentage falls by the same amount as the increase for team A (

, due to the adding up property) and its local revenue decreases, resulting in a smaller contribution to the central fund. Team A must absorb

of the fall in team B’s local revenue from the central fund since

The same effect holds for team B in (10).

Figure 5 depicts the downward shifts in marginal revenues. The marginal cost of winning is also reduced at the profit-maximizing league equilibrium, much to the displeasure of the players.

The profit-maximizing winning percentages at the new league equilibrium,

and

, cannot be determined without addressing the magnitudes of the shifts in the marginal revenue lines. A smaller shift in marginal revenue for one of the clubs will result in an improvement in the club’s winning percentage. Both marginal revenue lines shift down by the same amount in

Figure 5, resulting in

and

being unchanged from the initial league equilibrium. This is not a general result but can occur if

, an assumption used by Fort and Quirk [

6]. Equations (9) and (10) then reduce to (11) and (12) below.

The league equilibrium is established when (11) is set equal to (12). The resulting expression after simplification is , the pre-revenue sharing marginal revenues, and Equations (4)–(6) result. League parity is left unaffected, and the invariance principle holds.

Pool revenue sharing worsens parity in the two-team league model, a now accepted theoretical result. Team A transfers revenue to team B equal to the area between its original and new marginal revenue lines up to . Using the same logic, team B transfers revenue to team A by a lesser amount resulting in a net gain in revenue for team B. Revenue sharing benefits the smaller-market team B much to the displeasure of the larger-market team A.

To ease the exposition, we respecify the revenue functions for team A and team B as

and

, where

and

. We still use (7) and (8) to express team revenues after revenue sharing. Profit is maximized after revenue sharing by choosing a club stock of talent. The marginal revenues in (9) and (10) after revenue sharing are given below.

Equating the marginal revenues in (13) and (14) gives (15) below (assuming an open talent supply).

Simplifying gives

or

or

or

Without revenue sharing, and (16) reduces to . One need only show that to find that league parity has worsened. It is easy to find the result holds if (or ), our assumption.

Competitive balance has worsened with revenue sharing. The logic is simple. With greater revenue sharing, both teams must absorb some of the other team’s losses in revenue when their opponent increases its stock of talent that also increases its winning percentage. Suppose that the small-market team B increases its stock of talent and winning percentage. Team B will earn more revenue from its own market but must absorb the loss in revenue from team A, a much larger-revenue team. The result is that team B loses net revenue and the

line in

Figure 3 shifts down by a lot (algebraically

<

if

). Team A’s marginal revenue shifts down as well with revenue sharing, but not by as much as team B since it absorbs a smaller loss in revenue from the small-market team B when team A increases its stock of talent. The net result of greater revenue sharing is a worsening of parity.

The marginal cost of talent does not appear in the first-order conditions in (4) and (13)–(14) due to the assumption that it is constant over whatever stock of talent is acquired. Cavagnac [

31] builds a league model where the marginal cost of talent is an increasing function of the total league stock of talent, that is,

. This function internalizes the negative externality team B places on team A when it bids up the price of talent with a limited talent supply. The first-order conditions for profit-maximization are more complex and the result is that invariance does not hold with revenue sharing. It is not clear if the use of revenue sharing increases league profits. The reduction in club payrolls increases profitability in the short-run but could reduce revenue and profitability in the long-run. Peeters [

32] considers the issue in a profit-maximizing league model and finds that revenue sharing can increase profitability if the member clubs are heterogeneous in market sizes. Revenue sharing can reduce profitability if market sizes are homogeneous.

2.3. Revenue Sharing in the Sportsman League Model

Club owners in a “sportsman” professional sports league maximize wins subject to a break-even constraint. The PSR rule used in the EPL could be interpreted as a form of break-even constraint over three consecutive seasons. However, the tying of club expenses—mostly payroll—to club revenues is more complex than just breaking even. Club payroll is a function of club profit, which is a function of the club payroll and revenue. This is a tricky endogeneity problem that has yet to be modeled in the literature but is well worthy of study.

An exposition of the win-maximizing league model is Vrooman [

25]. The break-even constraint forces each club to acquire talent up to the point where average revenue (AR) of winning equals the average cost of talent (AC). Using (2) and if

, a constant, the break-even conditions are below (note that MC = AC of talent when

c is a constant). Define total league talent as

.

The league equilibrium is established where the average revenues are equal. This does not maximize total league revenue since each club will acquire a talent stock above its profit-maximizing stock. Using the adding-up property for the winning percentages yields the condition below.

Ignoring the

cT term yields the solution for the league equilibrium.

In comparison to the profit-maximizing equilibrium in (5), parity is skewed more heavily to the large-market club—competitive balance is lower.

The win-maximizing conditions in (17) and (18) are now modified to incorporate pool revenue sharing below. Essentially, the two clubs are sharing average revenues.

The league equilibrium is established where the average revenues after revenue sharing are equal.

The equilibrium winning percentages can be found through simulation, and then, compared to those from (20). We chose the parameter values , , and . The solution in the case with no revenue sharing is . With revenue sharing, . Parity is improved by using pool revenue sharing in a win-maximizing league. As , parity approaches its level without revenue sharing.

Empirically testing the effects of pool revenue sharing on league parity and player salaries is difficult since revenue sharing contribution rates do not change often. The NFL adopted the policy in 1994, with MLB following in 1997, the NHL in 2006, and the NBA in 2013. The NHL and NBA systems are too complex to be subjected to empirical testing, leaving changes in the contribution rates in the NFL and MLB to test for parity effects. A review of the difficulties in testing revenue sharing parity effects is given in Rockerbie [

33]. A large hurdle is obtaining accurate financial data for club revenues, although Forbes magazine produces estimates for the four major North American leagues. In addition, the NFL, NBA, and NHL use salary caps that have parity effects, confounding the revenue sharing effect.

Attempts to estimate parity effects are scant in the literature. Fort et al. [

34] provide a survey of early papers that mostly find a rejection of the invariance principle based on indirect evidence related to revenue sharing, such as player movements and talent investments. Solow and Krautmann [

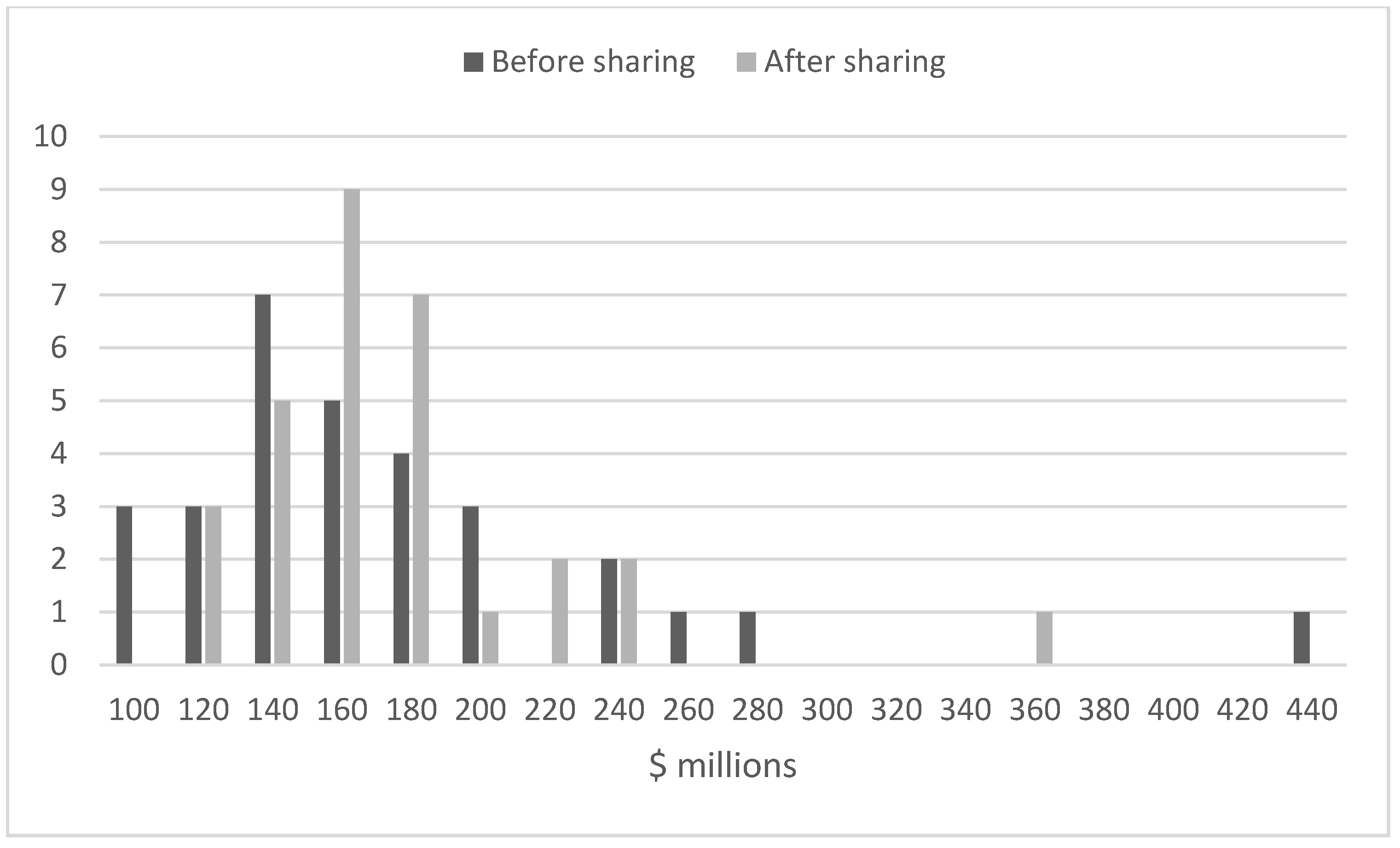

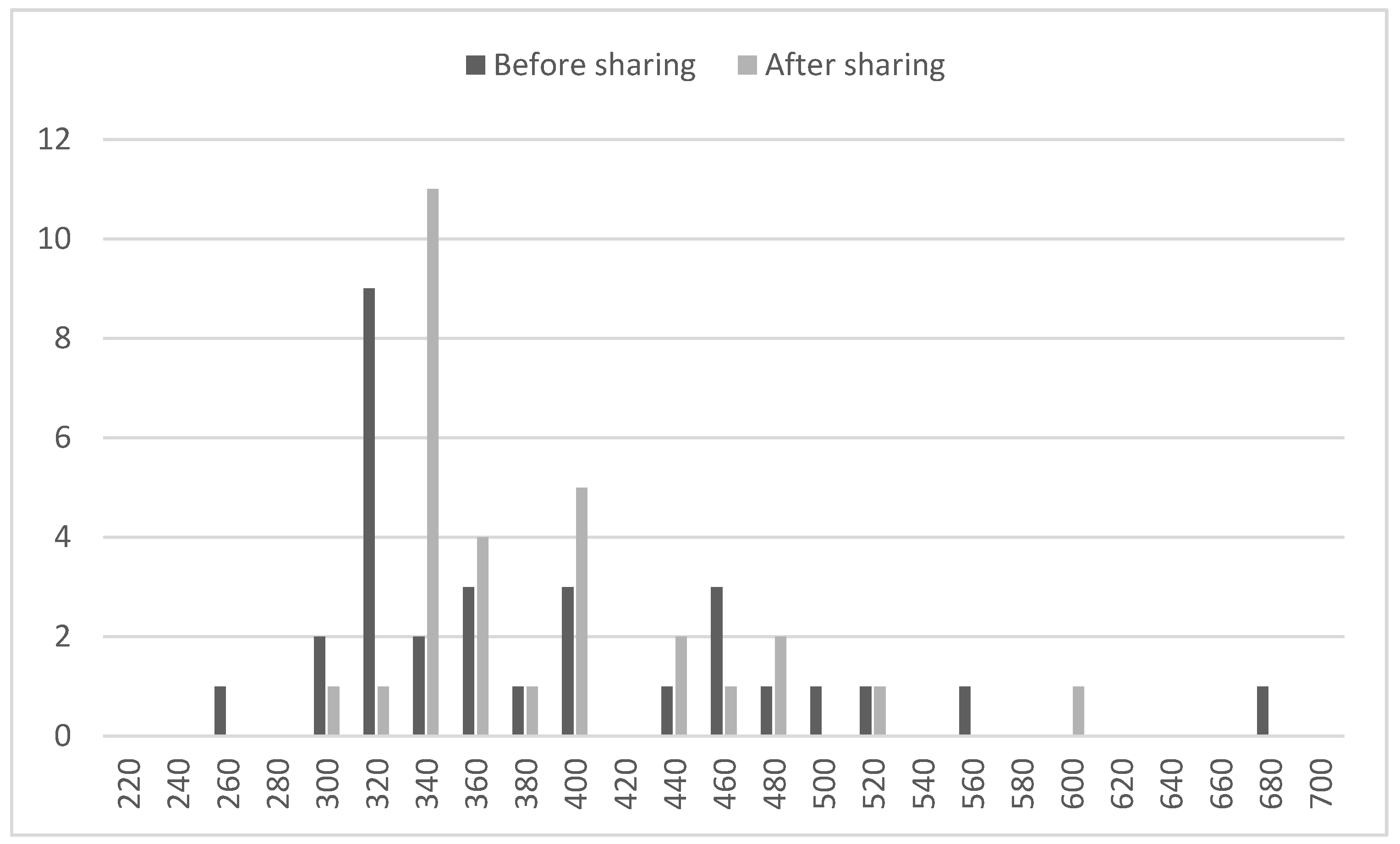

13] found that changes to the 1996 MLB revenue sharing agreement did not affect parity—a confirmation of the invariance principle—but did lower player salaries as the theoretical models predict. Rockerbie [

33] found that the reduction in the contribution rate in the 2007 MLB revenue sharing agreement worsened parity, contrary to what the theoretical model developed earlier predicts. Both papers relied on estimating the shifts in the marginal revenue product lines in

Figure 3. Hill and Jolly [

34] found that player salaries increased following the lowered 2007 MLB contribution rate, more so for hitters than pitchers, confirming the prediction of the two-team league model, although they did not consider parity effects. Jolly [

35] found that the dispersion of player salaries within clubs decreased following the 2007 MLB change, holding a set of variables constant, suggesting that clubs might be more equally balanced in play, although parity effects were not tested.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}