Comparative Study of Key Supply Chain Management Elements in Sustainability Reports

Abstract

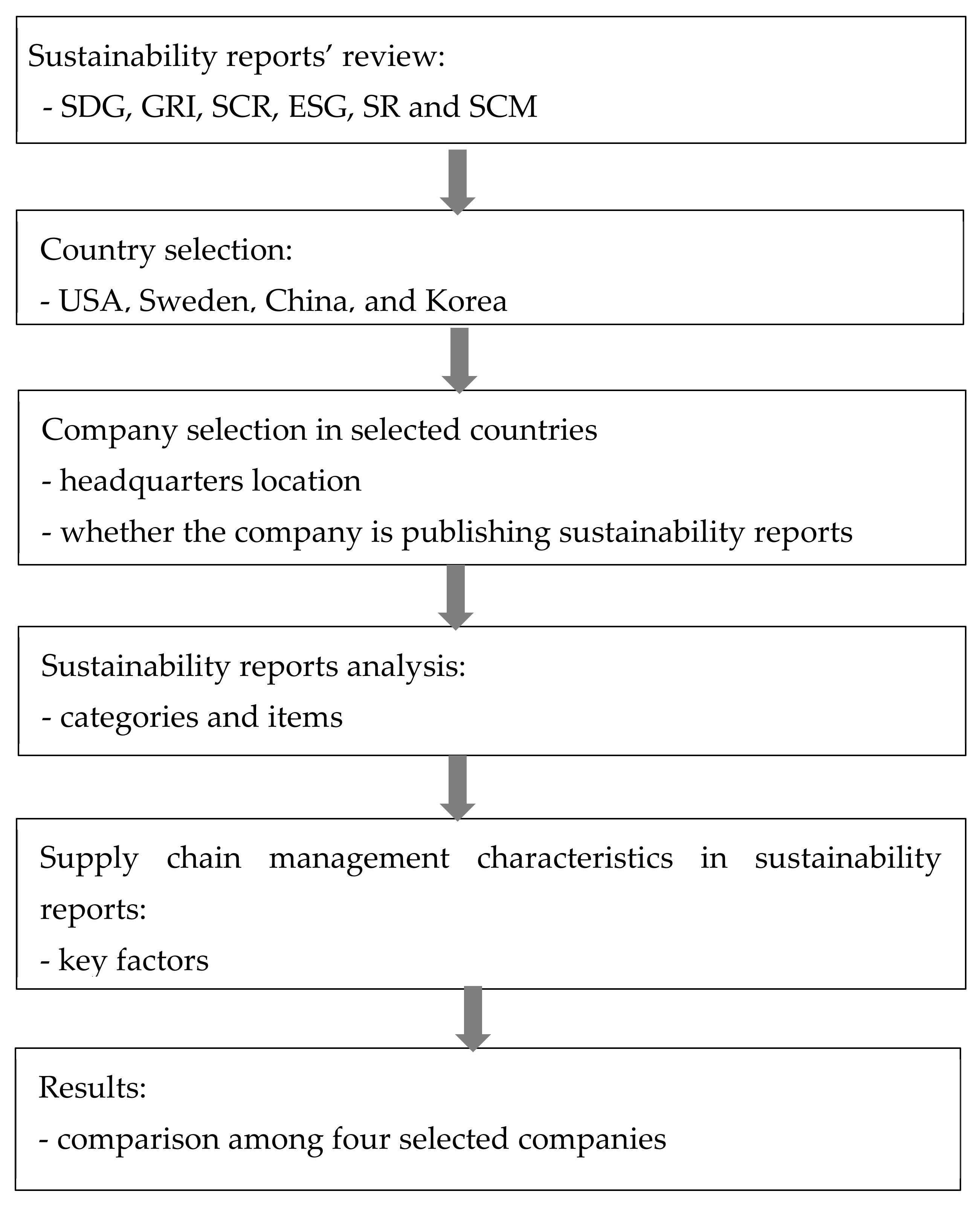

:1. Introduction

2. Review of the Sustainability Background

2.1. USA

2.2. Sweden

2.3. China

2.4. South Korea

3. Comparison of the Sustainability Reports

3.1. Description of the Selected Companies by Country

3.1.1. USA

3.1.2. Sweden

3.1.3. China

3.1.4. South Korea

3.2. Key Elements of the Sustainability Reports

3.2.1. Johnson & Johnson, USA

3.2.2. IKEA, Sweden

3.2.3. Haier Group, China

3.2.4. Samsung SDI Corporation, South Korea

4. Characteristics of SCM in the Sustainability Reports

4.1. Johnson & Johnson

4.2. IKEA

4.3. Haier Group Corporation

4.4. Samsung SDI Corporation

4.5. Results

5. Conclusions and Discussion

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Sections | Contents | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Environment | Environment management | Product stewardship (earthwards approach) | ✓ | ✓ | ✓ |

| Packaging and recycling | ✓ | ✓ | ✓ | ||

| Ingredients and sourcing of raw materials | ✓ | ✓ | ✓ | ||

| Waste management | ✓ | ✓ | ✓ | ||

| Biodiversity conservation | ✓ | ✓ | |||

| Water | Water usage amd discharge | ✓ | ✓ | ✓ | |

| Water conservation | ✓ | ✓ | ✓ | ||

| Greenhouse gas emissions/ climate change | Climate policy and initiatives/(climate resilience) | ✓ | ✓ | ✓ | |

| Energy use | ✓ | ✓ | ✓ | ||

| Facility CO2 emissions | ✓ | ✓ | ✓ | ||

| Air emissions | ✓ | ✓ | ✓ | ||

| Green buildings | ✓ | ✓ | |||

| Green chemistry | ✓ | ||||

| Society | Employee | Safety | ✓ | ✓ | ✓ |

| Health | ✓ | ✓ | ✓ | ||

| Employment policies and practices | ✓ | ✓ | ✓ | ||

| Ergonomics | ✓ | ||||

| Diversity and inclusion | ✓ | ✓ | ✓ | ||

| Labor practices and workforce | ✓ | ✓ | ✓ | ||

| Employee retention, development, and recruitment | ✓ | ✓ | |||

| Compensation | ✓ | ✓ | ✓ | ||

| Community (human health and well-being) | Disaster relief, volunteerism | ✓ | ✓ | ✓ | |

| Global public health | ✓ | ✓ | ✓ | ||

| Access to, and affordability of, healthcare (HIV, TB) | ✓ | ✓ | ✓ | ||

| Product pipeline/(innovation) | ✓ | ✓ | ✓ | ||

| R&D and clinical trials | ✓ | ✓ | ✓ | ||

| Market access | ✓ | ✓ | |||

| Preventing disease and promoting wellness | ✓ | ✓ | |||

| Preventing and responding to pandemic threats (United in defeating COVID-19) | ✓ | ||||

| Community involvement and engagement | ✓ | ✓ | ✓ | ||

| Customers | Assuring product quality and safety | ✓ | ✓ | ✓ | |

| Meeting customers’ needs/satisfaction | ✓ | ✓ | ✓ | ||

| Marketing communication/direct to consumer advertising | ✓ | ✓ | |||

| Share holders | Financial performance | ✓ | ✓ | ✓ | |

| Corporate governance | ✓ | ✓ | ✓ | ||

| Business conduct | ✓ | ✓ | ✓ | ||

| Political contribution | ✓ | ✓ | ✓ | ||

| Supplier | Ethics amd compliance | Ethics and integrity | ✓ | ✓ | ✓ |

| Anti-corruption/transparency | ✓ | ✓ | |||

| Ethical marketing | ✓ | ✓ | ✓ | ||

| Human rights | ✓ | ✓ | ✓ | ||

| Environmental and safety compliance | ✓ | ✓ | ✓ | ||

| Supply chain and supplier management | Procurement practices DMA | ✓ | ✓ | ✓ | |

| Freedom of association | ✓ | ✓ | ✓ | ||

| Labor practice and workforce | ✓ | ✓ | ✓ | ||

| Human rights | ✓ | ✓ | ✓ | ||

| Environmental assessment | ✓ | ✓ | ✓ | ||

| Information security and data privacy | ✓ | ✓ | ✓ | ||

| Enhancing supplier diversity and inclusion | ✓ | ✓ | ✓ | ||

| Intellectual property | ✓ | ✓ |

| Sections | Contents | Key Factors | 2006 | 2013 | 2020 |

|---|---|---|---|---|---|

| Ecology | Products and materials (2006): A more sustainable life at home (2013) | e-Wheel system | ✓ | ||

| Renewable materials used in products | ✓ | ✓ | ✓ | ||

| Waste recycling, reclaiming, or use in energy production. | ✓ | ✓ | ✓ | ||

| Recall management | ✓ | ||||

| WEEE system | ✓ | ||||

| Circular products (reuse, refurbish, remanufacture, and recycle) | ✓ | ||||

| The five dimensions of democratic design | ✓ | ||||

| Product innovations (evaluation system to check how green a product is) | ✓ | ||||

| Inorganic raw materials and virgin fossil materials | ✓ | ||||

| IKEA Food | Aquaculture Stewardship Council (ASC, 2013) + Marine Stewardship Council | ✓ | |||

| UTZ certification | ✓ | ✓ | |||

| Organic products | ✓ | ✓ | ✓ | ||

| Organic dish served | ✓ | ✓ | ✓ | ||

| Agriculture and animals | ✓ | ✓ | ✓ | ||

| Forestry | FSC certification scheme | ✓ | ✓ | ✓ | |

| WWF and IKEA | ✓ | ✓ | ✓ | ||

| Rainforest Alliance | ✓ | ✓ | ✓ | ||

| Reducing wood waste | |||||

| Energy | Renewable energy/Renewable Electricity Certificates/“Bundled” renewable power | ✓ | ✓ | ✓ | |

| IKEA introduced a mandatory energy usage checklist | ✓ | ||||

| WebEss system | ✓ | ||||

| Reduced energy use/effective energy consumption/energy efficient construction/motion detectors to save electricity | ✓ | ✓ | ✓ | ||

| Air quality | ✓ | ||||

| Save, reuse, or purify water | ✓ | ✓ | |||

| Transport | Environmental Protection Agency Smart Way Partnership | ✓ | |||

| Customer carbon footprint | ✓ | ✓ | ✓ | ||

| Supplier carbon footprint | ✓ | ✓ | ✓ | ||

| Employee carbon footprint | ✓ | ✓ | |||

| Product transport carbon footprint | ✓ | ✓ | |||

| Packing flat and filling space | ✓ | ✓ | |||

| Space-saving packages | ✓ | ✓ | |||

| GLES 3-pack plastic box | ✓ | ||||

| Rail initiatives | ✓ | ||||

| Delivery | ✓ | ✓ | ✓ | ||

| Green company cars | ✓ | ✓ |

| Sections | Contents | Key Factors | 2006 | 2013 | 2020 |

|---|---|---|---|---|---|

| Social | Governance and Ethics (since 2013) | People and Planet Positive strategy (introduced in 2012) | ✓ | ||

| Inequality | ✓ | ||||

| Moral leadership | ✓ | ||||

| Green growth | ✓ | ||||

| Customer communications | ✓ | ✓ | |||

| Human rights | ✓ | ||||

| International Recruitment Integrity System (IRIS) | |||||

| International Labor Organization (ILO), | |||||

| Employees | Homeworker agenda | ✓ | |||

| Ensure sustainability is part of our everyday work | ✓ | ||||

| Diversity and inclusion | ✓ | ||||

| Learning and development | ✓ | ||||

| Health and safety | ✓ | ||||

| Communication and engagement | |||||

| Survey to hear the voice of co-workers | ✓ | ||||

| Community involvement | Financial self-help groups | ✓ | ✓ | ||

| Alternative learning centers | ✓ | ✓ | |||

| Income generation initiative | ✓ | ✓ | |||

| Refugees | ✓ | ||||

| Immunization project | ✓ | ||||

| Children | Preventing child labor | ✓ | ✓ | ✓ | |

| Annual donation to improve children’s lives | ✓ | ||||

| Responsible marketing | |||||

| Ensuring children rights | ✓ | ✓ | ✓ | ||

| Education | Scholarships to study responsible forest management | ✓ | |||

| Developing forestry education in Russian schools | ✓ | ||||

| Developing LED lighting education | ✓ | ✓ | |||

| Customer education provision about sustainability | ✓ | ✓ | |||

| Suppliers | Control systems | Supplier Sustainability Index | ✓ | ✓ | |

| Indirect materials and services suppliers | ✓ | ||||

| Strategic Sustainability Council | ✓ | ||||

| IWAY supplier evaluation system (IWAY 6.0, since 2019) | ✓ | ✓ | ✓ | ||

| IConduct | ✓ | ||||

| Wood suppliers | Long-term relationship | ✓ | ✓ | ||

| Must not originate from intact natural forests (INF) | ✓ | ✓ | ✓ | ||

| 4Wood transportation | ✓ | ||||

| Tracing | ✓ | ||||

| Wood supply chain audits/third party auditor | ✓ | ✓ | ✓ | ||

| Economic | Stakeholders | Stakeholder engagement | ✓ | ✓ | |

| New sustainable revenue | Resale program | ✓ | |||

| Furniture as a service (subscription model) | ✓ |

| Sections | Contents | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Economy | Business model and Strategy | Improving performance through innovation | ✓ | ✓ | ✓ |

| Integrating order and personnel in the business model | ✓ | ✓ | |||

| Strategic transition to an Internet-based platform company | ✓ | ✓ | |||

| Environment | Environment management | Environmental management system | ✓ | ✓ | ✓ |

| Green purchasing (raw materials purchasing) | ✓ | ✓ | ✓ | ||

| Green innovation (energy-saving); environmental protection technology and equipment development | ✓ | ✓ | |||

| Training on environmental protection | ✓ | ||||

| Environmental protection public welfare activities | ✓ | ||||

| Hazardous chemical management | ✓ | ✓ | |||

| Energy saving | Energy consumption management | ✓ | ✓ | ||

| Water usage and conservation | ✓ | ||||

| Renewable energy usage | ✓ | ✓ | ✓ | ||

| Waste | Pollutants and waste management | ✓ | ✓ | ||

| Gas emissions/ climate change | Low-carbon management and carbon emissions | ✓ | ✓ | ||

| Climate policy and initiatives | ✓ | ||||

| Social | Community | Community Investment | ✓ | ||

| Employee | Employee recruitment and development | ✓ | ✓ | ✓ | |

| Employee benefits | ✓ | ✓ | |||

| Health | ✓ | ||||

| Managing employee working conditions | ✓ | ||||

| Talent development | ✓ | ✓ | |||

| Labor standards | ✓ | ||||

| Employee rights | ✓ | ✓ | |||

| Diversity and equality for opportunities | ✓ | ||||

| Suppliers | Information shared system | ✓ | |||

| Green purchasing policy | ✓ | ✓ | |||

| Supply chain transparency | ✓ | ||||

| Fair competition | ✓ | ||||

| Anti-corruption | ✓ | ||||

| Global synergy | ✓ | ||||

| Conflict minerals | ✓ | ||||

| Supplier audit | ✓ | ||||

| Supply chain platform (risk management, win-win relationship, transparency, information sharing, long-term trust relationship, etc.) | ✓ | ||||

| Customers | Quality management | ✓ | ✓ | ||

| After-sales service | ✓ | ||||

| Customer satisfaction management | ✓ | ✓ | |||

| Shareholders | Standardization of enterprise management | ✓ | |||

| Strengthening the internal supervision of enterprises | ✓ | ||||

| Information disclosure | ✓ | ||||

| Social activities | Social public welfare activities | ✓ | ✓ | ✓ | |

| Ethics amd compliance | Advertisement compliance | ✓ | |||

| Anti-corruption | ✓ | ||||

| Governance | Products innovation | ✓ | |||

| Intellectual property | ✓ | ||||

| Information security and data privacy | ✓ | ||||

| Enterprise management | ✓ | ||||

| Safe production | ✓ | ✓ |

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Environmental | Materials | Total materials use other than water, by type | ✓ | ||

| Materials used by weight or volume | ✓ | ||||

| Percentage of materials used that are recycled input materials | ✓ | ||||

| Materials used by weight or volume | ✓ | ||||

| Energy | Direct energy use | ✓ | ✓ | ✓ | |

| Indirect energy use | ✓ | ✓ | ✓ | ||

| Initiatives to use renewable energy sources and to increase energy efficiency | ✓ | ✓ | |||

| Energy saved due to conservation and efficiency improvements | ✓ | ||||

| Initiatives to provide energy-efficient products and the results | ✓ | ||||

| Energy consumption within the organization | ✓ | ||||

| Energy intensity | ✓ | ||||

| Reduction of energy consumption | ✓ | ||||

| Water and effluents | Total water use | ✓ | ✓ | ✓ | |

| Water sources and related ecosystems/habitats affected by use of water | ✓ | ||||

| Annual withdrawals of ground and surface water | ✓ | ||||

| Total water withdrawal by source | ✓ | ||||

| Percentage and total amount of reusable water | ✓ | ||||

| Interactions with water as a shared resource | ✓ | ||||

| Management of water discharge-related impacts | ✓ | ||||

| Water consumption | ✓ | ||||

| Biodiversity | Total amount of land for production activities | ✓ | |||

| Amount of impermeable surface | ✓ | ||||

| Objectives and programs for protecting biodiversity and species | ✓ | ||||

| Locations and size of land owned, leased and managed in protected areas | ✓ | ||||

| Impact of SDI’s activities, products, and services | ✓ | ||||

|

Emissions and waste | Greenhouse gas emissions | ✓ | ✓ | ||

| Use and emissions of ozone-depleting substances | ✓ | ✓ | |||

| NOx, SOx, and other significant air emissions by type | ✓ | ✓ | |||

| Total amount of waste by type and destination | ✓ | ✓ | |||

| Climate change mitigation and adaptation | ✓ | ||||

| International environmental compliance | ✓ | ✓ | |||

| Significant discharges to water | ✓ | ✓ | |||

| Activities to curb greenhouse gas emission and reduced amount | ✓ | ||||

| Total weight discharge by quality and destination | ✓ | ||||

| Total weight of waste by type and disposal method | ✓ | ||||

| Total number and volume of significant spills | |||||

| Waste generation and significant waste-related impacts | ✓ | ||||

| Management of significant waste-related impacts | ✓ | ||||

| Waste generated | ✓ | ||||

| Waste diverted from disposal | ✓ | ||||

| Waste directed to disposal | ✓ | ||||

| Products and services | Significant environmental impacts of major products and services | ✓ | |||

| Percentage of the weight of products | ✓ | ||||

| Initiatives to mitigate environmental impacts of products and services | ✓ | ||||

| Reclaiming rate of products sold and their package materials | ✓ | ||||

| Compliance | Incidents of and fines for non-compliance | ✓ | |||

| Amount of fines and total number of non-monetary sanctions | ✓ | ||||

| Non-compliance with environmental laws and regulations | ✓ | ||||

| Overall | Total environmental expenditures by type | ✓ | |||

| Total environmental protection expenditures and investment by type | ✓ | ||||

| New suppliers that were screened using environmental criteria | ✓ | ||||

| Negative environmental impacts in the supply chain and actions taken | ✓ |

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Social | Employment | Total workforce by employment type, contract, and region | ✓ | ✓ | ✓ |

| Total number and rate of employee turnover | ✓ | ✓ | |||

| Net employment creation and average turnover segmented | ✓ | ✓ | |||

| Employee benefits beyond those legally mandated | ✓ | ✓ | |||

| Parental leave | ✓ | ||||

| Labor/management relations | Percentage of employees covered by collective bargaining agreements | ✓ | ✓ | ✓ | |

| Minimum notice period regarding operational change | ✓ | ||||

| Health and safety | Official labor and management health and safety committee | ✓ | ✓ | ||

| Rates of injury, occupational diseases, lost days, and absenteeism, and number of work-related fatalities | ✓ | ✓ | |||

| Disease control programs for employees, families, community members | ✓ | ||||

| Compliance with ILO guidelines | ✓ | ✓ | |||

| Occupational health and safety management system | ✓ | ||||

| Hazard identification, risk assessment, and incident investigation | ✓ | ||||

| Promotion of worker health | ✓ | ||||

| Work-related injuries | ✓ | ||||

| Work-related ill health | ✓ | ||||

| Training | Average hours of training per employee | ✓ | ✓ | ||

| Programs to support continued employability of employees and to manage career | ✓ | ||||

| Policies and programs for skills management or for lifelong learning | ✓ | ||||

| Average hours of training per year per employee | ✓ | ||||

| Programs for upgrading employee skills/transition assistance programs | ✓ | ||||

| Diversity and equal opportunity | Diversity in BOD composition and employees. | ✓ | ✓ | ✓ | |

| Equal opportunity policies or programs, systems to ensure compliance | ✓ | ||||

| Ratio of basic salary of men to women by employee category | ✓ | ✓ | |||

| Strategy and management | Human rights policy, guidelines, and monitoring systems | ✓ | |||

| Evidence of consideration of human rights | ✓ | ||||

| Policies and procedures | ✓ | ||||

| Employee training on human rights | ✓ | ||||

| Investment and procurement practices | Percentage and total number of investment agreements | ✓ | |||

| Rates of significant suppliers and contractors | ✓ | ||||

| Non-discrimination | Total number of incidents of discrimination and actions taken | ✓ | ✓ | ✓ | |

|

Human rights assessment | Operations: human rights reviews or impact assessments | ✓ | |||

| Employee training on human rights policies or procedures | ✓ | ||||

| Collective bargaining | Operations identified: freedom of association and collective bargaining | ✓ | |||

| Child labor | Operations that are likely to have child labor and measures taken | ✓ | |||

| Forced labor | Operations that are likely to have forced labor and measures taken | ✓ | |||

| Disciplinary practices | Description of appeal practices | ✓ | |||

| Non-retaliation policy, confidential employee grievance system | ✓ | ||||

| Indigenous rights | Share of revenues from the area of operations | ✓ | |||

| Policies, guidelines, and procedures | ✓ | ||||

| Community | Programs that evaluate and manage operations on communities | ✓ | ✓ | ||

| Operations: engagement, assessments, and development programs | ✓ | ||||

| Supplier social assessment | New suppliers that were screened using social criteria | ✓ | |||

| Negative social impacts in the supply chain and actions taken | ✓ | ||||

| Corruption | Percentage and total number of business units prone to corruption | ✓ | ✓ | ||

| Percentage of employees trained in anti-corruption policies and procedures | ✓ | ||||

| Actions taken in response to incidents of corruption | ✓ | ||||

| Public policy | Public policy positions and participation | ✓ | |||

| Policies, management systems, and compliance mechanism | ✓ | ||||

| Political contributions | ✓ | ||||

| Competition and pricing | Policies, management systems, and compliance mechanism | ✓ | |||

| Compliance | Monetary values of significant fines for non-compliance | ✓ | |||

|

Customer health and safety | Percentage of products in compliance with procedures | ✓ | |||

| Voluntary code compliance, product labels or awards | ✓ | ||||

|

Product and service labeling | Type of products required by procedures, and percentage of products subject | ✓ | |||

| Policies on product information and labeling, compliance mechanism | ✓ | ✓ | |||

| Policies on customer satisfaction, compliance mechanism | ✓ | ✓ | |||

| Advertising | Policies on standards | ✓ | |||

| Respect for privacy | Policies, management system, and compliance mechanism | ✓ | ✓ | ||

| Marketing communications | Programs to be compliant with marketing communications | ✓ | ✓ | ||

| Compliance | Monetary values of significant fines for non-compliance | ✓ | ✓ |

| Section | Content | Key Factors | 2005 | 2013 | 2020 |

|---|---|---|---|---|---|

| Economic |

Economic performance | Direct economic value generated and distributed | ✓ | ✓ | ✓ |

| Financial implications and other risks and opportunities due to climate change | ✓ | ✓ | |||

| Defined benefit plan obligations and other retirement plans | ✓ | ✓ | ✓ | ||

| Significant financial assistance received from government | ✓ | ||||

| Market presence | Policy, practices, and proportion of local sourcing in major sites | ✓ | |||

| Proportion of senior management hired from the local community | ✓ | ||||

|

Indirect economic impacts | Local hiring procedures and proportion of managed seniors | ✓ | ✓ | ||

| Development and impact of community service activities and social investment | ✓ | ✓ | |||

| Understanding and describing significant, indirect economic impact | ✓ | ||||

| Significant indirect economic impacts | ✓ | ✓ | |||

| Procurement practices | Proportion of spending on local suppliers | ✓ | |||

| Anti-corruption | Operations assessed for risks related to corruption | ✓ | |||

| Communication and training about anti-corruption policies and procedures | ✓ | ||||

| Confirmed incidents of corruption and actions taken | ✓ | ||||

| Anti-competitive behavior | Legal actions for anti-competitive behavior, anti-trust, and monopoly practices | ✓ | |||

| Tax | Approach to tax | ✓ | |||

| Country-by-country reporting | ✓ |

References

- Adams, C.A.; Frost, G.R. Integrating sustainability reporting into management practices. Account. Forum 2008, 32, 288–302. Available online: https://www.sciencedirect.com/science/article/pii/S0155998208000306?casa_token=n7W9j157YrQAAAAA:oYq4x6wiGqwnlWHWMl05RX7ClZkBHQIQ4THwzTJEbAOOwHy37Eca9VwXLosjCvM6lB9QeUB4uc (accessed on 24 May 2021). [CrossRef]

- Lee, D.; Schniederjans, M. How corporate social responsibility commitment influences sustainable supply chain management performance within the social capital framework: A propositional framework. Int. J. Corp. Strateg. Soc. Responsib. 2017, 1, 208–233. [Google Scholar]

- Xie, Z. China’s historical evolution of environmental protection along with the forty years’ reform and opening-up. Environ. Sci. Ecotechnol. 2020, 1, 100001. Available online: https://www.sciencedirect.com/science/article/pii/S2666498419300018 (accessed on 10 July 2021). [CrossRef]

- A Practical Guide to Sustainability Reporting Using GRI and SASB Standards; Global Reporting Initiative and Sustainability Accounting Standards Board. 2021. Available online: https://www.globalreporting.org/media/mlkjpn1i/gri-sasb-joint-publication-april-2021.pdf (accessed on 10 July 2021).

- Spaargaren, G. Sustainable Consumption: A Theoretical and Environmental Policy Perspective. In The Ecological Modernisation Reader; Routledge: London, UK, 2020; pp. 318–333. Available online: https://www.taylorfrancis.com/chapters/edit/10.4324/9781003061069-21/sustainable-consumption-theoretical-environmental-policy-perspective-gert-spaargaren (accessed on 19 May 2021).

- Charm, T.; Coggins, B.; Robinson, K.; Wilkie, J. The Great Consumer Shift: Ten Charts That Show How US Shopping Behavior Is Changing; McKinsey and Company: New York, NY, USA, 2020. [Google Scholar]

- The KPMG Survey of Sustainability Reporting 2020. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2020/11/the-time-has-come.pdf (accessed on 6 April 2021).

- Lee, D. The effect of safety management and sustainable activities on sustainable performance: Focusing on suppliers. Sustainability 2018, 10, 4796. [Google Scholar] [CrossRef] [Green Version]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Christopher, M.; Towill, D. An integrated model for the design of agile supply chains. Int. J. Phys. Distrib. Logist. Manag. 2001, 31, 235–246. [Google Scholar] [CrossRef] [Green Version]

- Mangla, S.K.; Kusi-Sarpong, S.; Luthra, S.; Bai, C.; Jakhar, S.K.; Khan, S.A. Operational excellence for improving sustainable supply chain performance. Resour. Conserv. Recycl. 2020, 162, 105025. Available online: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7342035/ (accessed on 25 May 2021). [CrossRef] [PubMed]

- Pedersen, E.R.; Andersen, M. Safeguarding corporate social responsibility (CSR) in global supply chains: How codes of conduct are managed in buyer-supplier relationships. J. Public Aff. 2006, 6, 228–240. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/pa.232 (accessed on 25 May 2021). [CrossRef]

- EPA’s Budget and Spending; United States Environmental Protection Agency: Washington, DC, USA, 2020.

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. Available online: https://www.uio.no/studier/emner/matnat/ifi/INF9200/v10/readings/papers/DeMaggio.pdf (accessed on 6 September 2021). [CrossRef] [Green Version]

- Ruiz, S.; Romero, S.; Fernandez-Feijoo, B. Stakeholder engagement is evolving: Do investors play a main role? Bus. Strateg. Environ. 2021, 30, 1105–1120. Available online: https://onlinelibrary.wiley.com/doi/full/10.1002/bse.2674 (accessed on 6 September 2021). [CrossRef]

- Ahn, S.A. Status and analysis of sustainability report issuance of domestic listed companies. CG Rev. 2013, 68, 88–111. Available online: http://www.cgs.or.kr/CGSDownload/eBook/REV/C201307006.pdf (accessed on 11 March 2021).

- Brockett, A.; Rezaee, Z. Brief history of sustainability reporting. In Corporate Sustainability: Integrating Performance and Reporting; New York, NY, USA, 2012; pp. 27–35. Available online: https://learning.oreilly.com/library/view/corporate-sustainability-integrating/9781118238066/chapter02.html (accessed on 6 April 2021).

- INC. 90% of S&P 500 Index Companies Publish Sustainability/Responsibility Reports in 2019; Governance & Accountability Institute: New York, NY, USA, 2020. [Google Scholar]

- Ghazi, P. Sustainability Reporting by the Largest U.S. Companies Hits New Highs; 3BL Media & TriplePundit: Northampton, MA, USA, 2020. [Google Scholar]

- Hąbek, P.; Wolniak, R. Assessing the quality of corporate social responsibility reports: The case of reporting practices in selected European Union member states. Qual. Quant. 2015, 50, 399–420. Available online: https://link.springer.com/article/10.1007/s11135-014-0155-z (accessed on 14 April 2021). [CrossRef] [PubMed] [Green Version]

- Escaler, G. Council post: Transforming sustainability into a competitive advantage. Forbes 2020. Available online: https://www.forbes.com/sites/forbescommunicationscouncil/2020/09/09/transforming-sustainability-into-a-competitive-advantage/?sh=22c55444282e (accessed on 27 April 2021).

- Sweden and Sustainability. Sweden.Se 2021. Available online: https://sweden.se/climate/ (accessed on 14 April 2021).

- Grafström, J.; Sandström, C.; Wieslander, A.; Paulson, R. (Much) More for Less: HOW Sustainable Is Swedish Economic Growth? The Ratio Institute. 2020. Available online: http://www.diva-portal.org/smash/get/diva2:1430960/FULLTEXT02.pdf (accessed on 14 April 2021).

- Sustainable Development Report; Cambridge University Press: Cambridge, UK, 2021.

- Mänsson, M. Sweden—The world’s most sustainable country: Political statements and goals for a sustainable society. Earth Common J. 2016, 6, 16–22. Available online: http://www.inquiriesjournal.com/articles/1555/sweden-the-worlds-most-sustainable-country-political-statements-and-goals-for-a-sustainable-society (accessed on 14 April 2021). [CrossRef]

- Zhang, Z.D. Historical review and current situation analysis of corporate social responsibility in China. Lenin Eastern Soc.—China-Jpn. Soc. Forum. 2010, 14–16. [Google Scholar]

- Yin, G.F.; Guan, Z.S.; Li, J. The Surge of Thought: A Study of the Development of Corporate Social Responsibility in China (1978–2019). Sustainable Development Economic Guide. 2019. Available online: https://www.cnki.com.cn/Article/CJFDTotal-WTOK201912020.htm (accessed on 4 May 2021).

- Jintao, H.N. 42 Companies Law of the People’s Republic of China Order of the President of the People’s Republic of China. 2006. Available online: https://www.ilo.org/dyn/natlex/docs/ELECTRONIC/92643/108008/F-186401967/CHN92643%20Eng.pdf (accessed on 30 May 2021).

- Syntao, A Journey to Discover Values. 2007. Available online: http://www.syntao.com/newsinfo/2111223.html (accessed on 23 March 2021).

- Yin, G.F. 2012: The first year of CSR management in China. WTO Econ. Guide 2012, 7, 72. [Google Scholar]

- China Social Responsibility 100 Forum. 2019. Available online: https://www.sohu.com/a/356524860_186085 (accessed on 7 April 2021).

- Borkowski, S.C.; Welsh, M.J.; Wentzel, K. Johnson & Johnson: A Case Study on Sustainability Reporting; Institute of Management Accountants: New York, NY, USA, 2010. [Google Scholar]

- Conn, S. Gartner Announces Rankings of the 2021 Supply Chain Top 25. Gartner 2021. Available online: https://www.gartner.com/en/newsroom/press-releases/2021-05-19-gartner-announces-rankings-of-the-2021-supply-chain-top-25 (accessed on 6 June 2021).

- Park, A. 2021 TIME100 Most Influential Companies. Time Magazine. 2021. Available online: https://time.com/collection/time100-companies/5953660/johnson-johnson/ (accessed on 6 June 2021).

- World’s Most Admired Companies. Fortune Magazine. 2021. Available online: https://fortune.com/worlds-most-admired-companies/2021/search/?ordering=asc (accessed on 6 June 2021).

- Gronvius, P.; Lernborg, C. IKEA and CSR: Like hand in glove? Stockh. Sch. Econ. 2009, in press. [Google Scholar]

- Sustainable Brand Index, Swed. Sustain. Brand Index: Stockholm, Sweden. 2021. Available online: https://www.sb-index.com/sweden-b2b (accessed on 14 April 2021).

- Qasim, M.; Amir, S. Can Sustainability be a Key Driver of Innovation and Competitive Advantage? Case of IKEA; Karlstad Business School: Karlstad, Sweden, 2011; Available online: https://www.diva-portal.org/smash/get/diva2:448159/FULLTEXT01.pdf (accessed on 14 April 2021).

- Andersen, M.; Skjoett-Larsen, T. Corporate social responsibility in global supply chains. Supply Chain Manag. 2019, 14, 75–86. [Google Scholar] [CrossRef] [Green Version]

- IKEA Sustainability Report. 2020. Available online: https://www.ikea.com/au/en/files/pdf/71/bb/71bb29d8/ikeasustainabilityreportnew2020july3.pdf. (accessed on 14 April 2021).

- Haier Corporate Social Responsibility Report. 2020. Available online: https://imagegroup1.haier.com/csr/W020210603343090073158.pdf?spm=net.31741_pc.hg2020_sr_download_20200908.3 (accessed on 8 April 2021).

- Hwang, Y.J. Samsung SDI Draws Attention to ESG Management. Asian Econ. 2021. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwjBkKfl56jxAhWOv5QKHTk2DoMQFjAAegQIAxAD&url=https%3A%2F%2Fwww.asiae.co.kr%2Farticle%2F2021012417313595496&usg=AOvVaw1RGYCC5253G5oYYdPDhM3x (accessed on 24 June 2021).

- SAMSUNG SDI Sustainability Report. 2003. Available online: https://www.samsungsdi.com/upload/download/sustainable-management/2003_Sustainability_Report_English.pdf (accessed on 10 July 2021).

- SAMSUNG SDI Sustainability Report. 2019. Available online: https://www.samsungsdi.co.kr/upload/download/sustainable-management/2019_Samsung_SDI_Sustainability_Report_English.pdf (accessed on 22 June 2021).

- IKEA Social & Environmental Responsibility. 2006. Available online: https://www.ikea.com/ms/en_JO/about_ikea/pdf/ikea_ser_2006.pdf (accessed on 22 June 2021).

- IKEA Group Sustainability Report. 2013. Available online: https://www.ikea.com/nl/en/files/pdf/3e/cf/3ecf9f9c/sustainability_report_2013.pdf (accessed on 10 July 2021).

- Haier Corporate Social Responsibility Report. 2005. Available online: https://www.docin.com/p-6009306.html?docfrom=rrela (accessed on 30 March 2021).

- Haier Corporate Social Responsibility Report. 2013. Available online: https://www.docin.com/p-802272045.html (accessed on 30 March 2021).

- SAMSUNG SDI Sustainability Report. 2005. Available online: https://www.samsungsdi.co.kr/upload/download/sustainable-management/2005_Sustainability_Report_English.pdf (accessed on 22 June 2021).

- SAMSUNG SDI Sustainability Report. 2013. Available online: https://www.samsungsdi.co.kr/upload/download/sustainable-management/2013_Sustainability_Report_English.pdf (accessed on 22 June 2021).

- Johnson & Johnson Sustainability Report. 2005. Available online: https://www.aeca.es/old/comisiones/rsc/biblioteca_memorias_rsc/informes_empresas_extranjeras_4/johnson_johnson_2005_environ.pdf (accessed on 1 June 2021).

- Johnson & Johnson Sustainability Report. 2013. Available online: https://www.responsibilityreports.com/Company/johnson-johnson (accessed on 1 June 2021).

- Johnson & Johnson Sustainability Report. 2020. Available online: https://www.responsibilityreports.com/Company/johnson-johnson (accessed on 1 June 2021).

- The Strategic Approach of Companies to Transition to Sustainability and ESG Management., Deloitte Insights. 2020. Available online: https://www2.deloitte.com/content/dam/Deloitte/kr/Documents/insights/deloitte-korea-review/16/kr_insights_ESG_SP_2020.pdf (accessed on 24 June 2021).

- Tennison, I.; Roschnik, S.; Ashby, B.; Boyd, R.; Hamilton, I.; Oreszczyn, T.; Owen, A.; Romanello, M.; Ruyssevelt, P.; Sherman, J.D. Health care’s response to climate change: A carbon footprint assessment of the NHS in England. Lancet Planet. Health 2021, 5, 84–92. Available online: https://www.thelancet.com/pdfs/journals/lanplh/PIIS2542-5196(20)30271-0.pdf (accessed on 28 April 2021). [CrossRef]

- World Bank, Global Economy to Expand by 4% in 2021; Vaccine Deployment and Investment Key to Sustaining the Recovery 2021. Available online: https://www.worldbank.org/en/news/press-release/2021/01/05/global-economy-to-expand-by-4-percent-in-2021-vaccine-deployment-and-investment-key-to-sustaining-the-recovery (accessed on 7 July 2021).

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of the 21st Century; New Society: Stoney Creek, CT, USA, 1998. [Google Scholar]

| Category | Subcategory | 2005 | 2013 | 2020 |

|---|---|---|---|---|

| People and Planet Strategy | Citizenship and Sustainability Strategy | Health for Humanity Strategy | ||

| Supply Chain and Supplier Management | Procurement practices | ✓ | ✓ | |

| Freedom of association | ✓ | ✓ | ||

| Labor practice and workforce/child labor | ✓ | ✓ | ✓ | |

| Human rights | ✓ | ✓ | ✓ | |

| Environmental assessment | ✓ | ✓ | ✓ | |

| Information security and data privacy | ✓ | ✓ | ||

| Compliance | ✓ | ✓ | ✓ | |

| Enhancing supplier diversity and inclusion | ✓ | ✓ | ✓ | |

| Transparency and disclosure | ✓ | ✓ | ||

| Sourcing responsibly | ✓ | ✓ | ||

| Year | Characteristics | |||

| 2005 |

| |||

| 2013 |

| |||

| 2020 |

| |||

| Category | Subcategory | 2006 | 2013 | 2020 |

|---|---|---|---|---|

| People and the Environment Strategy | People and Planet Positive Strategy | |||

| Suppliers | SCM control systems (IWAY) | ✓ | ✓ | ✓ |

| Compliance with general conditions and legal requirements | ✓ | ✓ | ✓ | |

| Business ethics | ✓ | ✓ | ||

| Environment | ✓ | ✓ | ✓ | |

| Worker health, safety, facilities, and wages | ✓ | ✓ | ✓ | |

| Forced and bonded labor/child labor | ✓ | ✓ | ✓ | |

| Discrimination, harassment, and abuse | ✓ | ✓ | ✓ | |

| Freedom of association and collective bargaining | ✓ | ✓ | ✓ | |

| Continuous improvement | ✓ | ✓ | ✓ | |

| Worker involvement | ✓ | ✓ | ||

| IKEA General Forestry requirements for suppliers | ✓ | ✓ | ✓ | |

| Animal welfare section | ✓ | ✓ | ||

| Transport section | ✓ | ✓ | ✓ | |

| Year | Characteristics | |||

| 2006 |

| |||

| 2013 |

| |||

| 2020 |

| |||

| Category | Subcategory | 2005 | 2013 | 2020 |

|---|---|---|---|---|

| Green Purchasing Strategy | Win-Win Partnership Strategy | Sustainable Supply Chain Strategy | ||

| Suppliers | Information Shared System | ✓ | ||

| Green purchasing policy | ✓ | ✓ | ||

| Supply chain transparency | ✓ | |||

| Fair competition | ✓ | |||

| Anti-corruption | ✓ | |||

| Global synergy | ✓ | |||

| Conflict minerals | ✓ | |||

| Supplier audit | ✓ | |||

| Supply chain platform (that ensures risk management, win-win relationships, transparency, information sharing, long-term trust relationships, etc.) | ✓ | |||

| Year | Characteristics | |||

| 2005 |

| |||

| 2013 |

| |||

| 2020 |

| |||

| Category | Subcategory | 2005 | 2013 | 2020 | |

|---|---|---|---|---|---|

| Supply Chain Environmental | Win-Win Partnership | Sustainable Supply Chain | |||

| Supply Chain and Supplier management | Sustainable partnership | ✓ | ✓ | ✓ | |

| Environment preservation activities | ✓ | ✓ | ✓ | ||

| Shared Growth | ✓ | ✓ | ✓ | ||

| Responsible Minerals Sourcing | ✓ | ✓ | ✓ | ||

| Compliance with Fair Trade | ✓ | ✓ | ✓ | ||

| Win-win growth with suppliers | ✓ | ✓ | ✓ | ||

| Promoting social responsibility in the value chain | ✓ | ✓ | ✓ | ||

| Managing supply chain risks amid COVID-19 | ✓ | ||||

| Legal Compliance | ✓ | ✓ | ✓ | ||

| Year | Characteristics | ||||

| 2005 |

| ||||

| 2013 |

| ||||

| 2020 |

| ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, V.; Marasini, D.; Dong, W.; Lee, H.-J.; Lee, D. Comparative Study of Key Supply Chain Management Elements in Sustainability Reports. Businesses 2021, 1, 168-195. https://doi.org/10.3390/businesses1030013

Lee V, Marasini D, Dong W, Lee H-J, Lee D. Comparative Study of Key Supply Chain Management Elements in Sustainability Reports. Businesses. 2021; 1(3):168-195. https://doi.org/10.3390/businesses1030013

Chicago/Turabian StyleLee, Veronika, Durga Marasini, Wenye Dong, Hyun-Jung Lee, and DonHee Lee. 2021. "Comparative Study of Key Supply Chain Management Elements in Sustainability Reports" Businesses 1, no. 3: 168-195. https://doi.org/10.3390/businesses1030013

APA StyleLee, V., Marasini, D., Dong, W., Lee, H.-J., & Lee, D. (2021). Comparative Study of Key Supply Chain Management Elements in Sustainability Reports. Businesses, 1(3), 168-195. https://doi.org/10.3390/businesses1030013