Abstract

Environmental, social, and governance (ESG) has become a concern for companies, investors, and regulators. Its significance cannot be underestimated, as stakeholders increasingly demand accountability and transparency regarding corporate practices in these areas. Government agencies enforce laws mandating companies adhere to established ESG standards in response. However, despite these regulatory pressures, several obstacles have hindered organizations from effectively implementing sustainability initiatives, often resulting in lackluster outcomes. In this study, we developed a framework to implement ESG principles across various companies, utilizing the critical success factor (CSF) theory. By incorporating the perspectives of stakeholders, we identified the essential elements to achieve ESG. The developed framework in ESG studies employed the hybrid Delphi technique and the analytical hierarchy process (AHP), a structured method for organizing and analyzing complex decisions. Based on the results obtained from targeted questions, variables that influence ESG performance were identified. The effectiveness of different sustainability initiatives was also assessed to understand stakeholder engagement strategies and evaluate the impact of organizational culture on ESG adoption.

1. Introduction

In the supply chain, raw materials are transferred for industrial manufacturing [1] and converted into waste after manufacturing in a linear economy. However, the linear economy model cannot balance supply and demand for natural resources [2]. Furthermore, a business strategy to preserve natural resources and the environment, innovative manufacturing techniques, models, and services are related to climate change and ecosystem degradation globally [3,4,5]. Okorie et al. stated that supply chains are the origin of the circular economy (CE), which offers environmentally friendly corporate solutions and strategies [6]. According to Kouhizadeh et al. [7], CE aims to extend the life cycle of products and materials, add value to them, and renew them till the end of their useful lives. Due to the growing cost, complexity, unpredictability, and susceptibility of the supply chain due to the CE attribution, managers look for better, faster, and less expensive vertical and horizontal supply chain collaboration.

To overcome the aforementioned challenges [8,9], provide sustainable output [10], and minimize human–machine interaction for the adoption of sustainability practices and CE principles [11], supply chains must also be innovative. The digital supply chain is a powerful means for sustainability. It aims to reduce environmental impact, improve efficiency, and promote social responsibility. Digital technologies provide tools and frameworks to enable and enhance circularity within supply chains.

Environmental, social, and governance (ESG) factors increasingly play a significant role in corporate decision-making and performance evaluation. ESG policies boost companies’ stock liquidity [12] and cumulative abnormal returns [13]. However, stakeholders are worried about ESG and how companies handle them. For example, investors look for ESG data to identify sustainable companies. Therefore, ESG factors are included in risk management, performance evaluation, and strategic decision-making. The leading cause is the pressure from numerous stakeholders, such as workers, investors, clients, and regulators, who demand that companies demonstrate accountability and openness about ESG matters.

ESG principles are adopted to enhance supply chain resilience by positively impacting a company’s willingness to adopt innovative technologies with technology adoption and improved supply chain resilience [14]. ESG management in the supply chain positively impacts supply chain resilience through information network capability and emerging information technologies. Supply chain collaboration, supply chain management capabilities, supply chain risks, and green-product innovation positively impact a company’s willingness to adopt innovative technologies, subsequently leading to positive effects on supply chain resilience and performance [15].

Therefore, it is necessary to understand the obstacles to putting ESG into practice in the manufacturing supply chain based on variables and research questions in the previous studies, is the basis of this study.

2. Methodology

We employed methods that combine qualitative and quantitative research techniques. By integrating various methodologies, factors influencing ESG implementation across various organizations were determined. Stakeholder interviews and focus group discussions were conducted along with data collection through surveys. The data collected were analyzed using the Delphi technique and the analytical hierarchy process (AHP). The variables identified were used to construct the questionnaire (Figure 1). We conducted a literature review by gathering and examining publications from reliable academic sources, including Google Scholar, Web of Science, and ScienceDirect. We chose publications to assess and compare the results of this study with those of previous studies. The Delphi and AHP techniques were used to identify important variables. The Delphi technique was used to collect expert opinions agreed on variables. At the same time, AHP was used to assign weights to these variables according to their relative importance.

Figure 1.

Method used in this study.

3. Result and Discussion

3.1. Variable

Critical success factors (CSFs) are essential for organizations to enhance sustainability and long-term value creation through ESG integration. These factors guide the effective implementation and management of ESG strategies: corporate governance [16], long-term value creation [17,18], stakeholder engagement [17,19], transparency and reporting [17,18], senior management involvement [17,18], risk management [17], use of technology and data [18]. Martiny et al. [20] selected 14 variables for the implementation of ESG: company strategy, company characteristics, CEO features, CEO compensation, corporate governance, audit committees, investor relationship, regulatory framework, country governance, industry, period, economic development, financial performance, and market performance. Khamisu et al. [21] chose 20 variables: financial performance, market performance, environmental performance, earnings quality, ESG reporting guidelines, board size, board diversity, board independence, signaling future performance, third-party ratings, mandatory disclosure policies, managerial attributes, company characteristics, demand by stakeholders, presence of CSR committee, ESG materials, reputation insurance, disclosure costs, audit and assurance, reduced information system.

The following variables were chosen based on discussion with experts in the Delphi method: company strategy, company characteristics, chief executive officer (CEO) features, CEO compensation, corporate governance, audit committees, investor relationship, regulatory framework, country governance, industry, period, economic development, financial performance, market performance, environmental performance, earnings quality, ESG reporting guidelines, board size, board diversity, board independence, signaling future performance, third-party ratings, mandatory disclosure policies, managerial attributes, company characteristics, demand by stakeholders, presence of CSR committee, ESG materials, reputation insurance, disclosure costs, audit and assurance, reduced information system. The variables were validated using AHP.

3.2. AHP

The variables were chosen using AHP [22] and ranked based on their weight. After using AHP, variables prioritized in the model development process were identified. These variables were validated by using the consistency ratio. The consistency index (CI) was calculated using Equation (1).

where The term “maximum value of Eigenvalue” refers to the highest eigenvalue of a matrix, and n represents the order or size of the matrix. Finally, it is necessary to compute the consistency ratio (CR) by dividing the consistency index by the random consistency index using Equation (2).

The CR was 0.07, which indicated that the weights were consistent. The weight of the variables was calculated based on the Pareto rule.

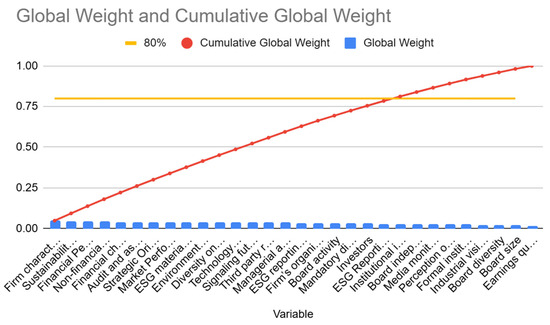

Institutional investors, board independence, media monitoring, perception of CSR, formal institutions, industrial visibility, board diversity, board size, and earnings quality had low weights (Figure 2). Therefore, they were not used in the next stage. Table 1 shows the variables grouped by organizational characteristics, performance, strategy, corporate governance, investor relations, ESG adoption, and technology. These variable were used for constructing questions (Table 2).

Figure 2.

Global weight and cumulative global weight.

Table 1.

Variables and categories.

Table 2.

Variables and questions.

4. Conclusions

A framework for implementing ESG principles across various companies was developed based on the CSF theory. By incorporating the perspectives of stakeholders, we identified the variables for the achievement of ESG goals. Twenty variables were selected for this research and classified into seven groups. The variables were used for data collection related to ESG. These variables ensured that ESG was embedded into the supply chain process and aligned with business goals. By prioritizing these variables, companies need to enhance their competitiveness, reduce risks, and develop long-term value, in addition to meeting ESG goals. Integrating ESG factors into digital supply chains is crucial for sustainable, ethical, and responsible business practices while enhancing efficiency.

Author Contributions

Conceptualization, R.M.S.; methodology, H.-L.C.; software, R.M.S.; validation, Y.-T.J., R.S. and A.S.; formal analysis, R.S.; investigation, R.M.S.; resources, H.-L.C.; data curation, R.S.; writing—original draft preparation, R.M.S.; writing—review and editing, R.M.S.; visualization, R.S.; supervision, Y.-T.J.; project administration, S.P.D.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Goyal, S.; Esposito, M.; Kapoor, A. Circular economy business models in developing economies: Lessons from India on reduce, recycle, and reuse paradigms. Thunderbird Int. Bus. Rev. 2018, 60, 729–740. [Google Scholar] [CrossRef]

- Rajput, S.; Singh, S.P. Connecting circular economy and industry 4.0. Int. J. Inf. Manag. 2019, 49, 98–113. [Google Scholar] [CrossRef]

- Bassetti, T.; Blasi, S.; Sedita, S.R. The management of sustainable development: A longitudinal analysis of the effects of environmental performance on economic performance. Bus. Strategy Environ. 2021, 30, 21–37. [Google Scholar] [CrossRef]

- Dwyer, R.; Lamond, D.; Molina-Azorín, J.F.; Claver-Cortés, E.; Lopez-Gamero, M.D.; Tarí, J.J. Green management and financial performance. A literature review. Manag. Decis. 2009, 47, 1080–1100. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Griffiths, A.; Winn, M. Extreme weather events and the critical importance of anticipatory adaptation and organizational resilience in responding to impacts. Bus. Strategy Environ. 2012, 21, 17–32. [Google Scholar] [CrossRef]

- Okorie, O.; Salonitis, K.; Charnley, F.; Moreno, M.; Turner, C.; Tiwari, A. Digitisation and the circular economy: A Review of Current Research and Future Trends. Energies 2018, 11, 3009. [Google Scholar] [CrossRef]

- Kouhizadeh, M.; Zhu, Q.; Sarki, J. Blockchain and the circular economy. Potential tensions and critical reflections from practice. Prod. Plan. Control 2020, 31, 950–966. [Google Scholar] [CrossRef]

- Butner, K. The more intelligent supply chain of the future. Strategy Leadersh. 2010, 38, 22–31. [Google Scholar] [CrossRef]

- Wu, L.; Yue, X.; Jin, A.; Yen, D.C. Smart supply chain management: A review and implications for future research. Int. J. Logist. Manag. 2016, 27, 395–417. [Google Scholar] [CrossRef]

- Zouari, D.; Ruel, S.; Viale, L. Does digitalizing the supply chain contribute to its resilience? Int. J. Phys. Distrib. Logist. Manag. 2021, 51, 149–180. [Google Scholar] [CrossRef]

- Yadav, G.; Luthra, S.; Jakhar, S.K.; Mangla, S.K.; Rai, D.P. A framework to overcome sustainable supply chain challenges through solution measures of industry 4.0 and circular economy. An automotive case. J. Clean. Prod. 2020, 254, 120112. [Google Scholar] [CrossRef]

- Krueger, P.; Sautner, Z.; Tang, D.Y.; Zhong, R. The Effects of Mandatory ESG Disclosure Around the World, European Corporate Governance Institute. Financ. Work. Pap. 2021, 754, 421–442. [Google Scholar]

- Li, Z.; Feng, L.; Pan, Z.; Sohail, H.M. ESG performance and stock prices: Evidence from the COVID-19 outbreak in China. Humanit. Soc. Sci. Commun. 2022, 9, 242. [Google Scholar] [CrossRef] [PubMed]

- Li, W.; Liu, Z. Social, Environmental, and Governance Factors on Supply-Chain Performance with Mediating Technology Adoption. Sustainability 2023, 14, 10865. [Google Scholar] [CrossRef]

- Zhou, Y.; Zhang, N.; Wu, C.; Wang, Y.; Zhang, X.; Zhang, D. The Impact of Supply Chain ESG Management on Supply Chain Resilience With Emerging IT Technologies. J. Organ. End User Comput. 2024, 36, 1–31. [Google Scholar] [CrossRef]

- Kim, S.; Li, Z. Understanding the Impact of ESG Practices in Corporate Finance. Sustainability 2021, 13, 3746. [Google Scholar] [CrossRef]

- Liu, J.; Xie, J. The Effect of ESG Performance on Bank Liquidity Risk. Sustainability 2024, 16, 4927. [Google Scholar] [CrossRef]

- Dong, B. A Systematic Review of the ESG Strategy Literature and Future Outlook. Front. Sustain. Dev. 2023, 3, 105–112. [Google Scholar] [CrossRef]

- Zaccone, M.C.; Pedrini, M. ESG Factor Integration into Private Equity. Sustainability 2020, 12, 5725. [Google Scholar] [CrossRef]

- Martiny, A.; Taglialatela, J.; Testa, F.; Iraldo, F. Determinants of environmental social and governance (ESG) performance. A systematic literature review. J. Clean. Prod. 2024, 456, 142213. [Google Scholar] [CrossRef]

- Khamisu, M.S.; Paluri, R.A.; Sonwaney, V. Stakeholders’ perspectives on critical success factors for environmental social and governance (ESG) implementation. J. Environ. Manag. 2024, 365, 121583. [Google Scholar] [CrossRef]

- Saaty, T.L. The Analytic Hierarchy Process; McGraw-Hill: New York, NY, USA, 1980. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).