The Effect of Data Transformation on Singular Spectrum Analysis for Forecasting

,

,  , and

, and

Abstract

:1. Introduction

2. SSA Forecasting

2.1. Decomposition and Reconstruction of Time Series

2.2. Recurrent Forecasting

2.3. Vector Forecasting

3. Transformation of Time Series

3.1. Standardisation

3.2. Logarithmic Transformation

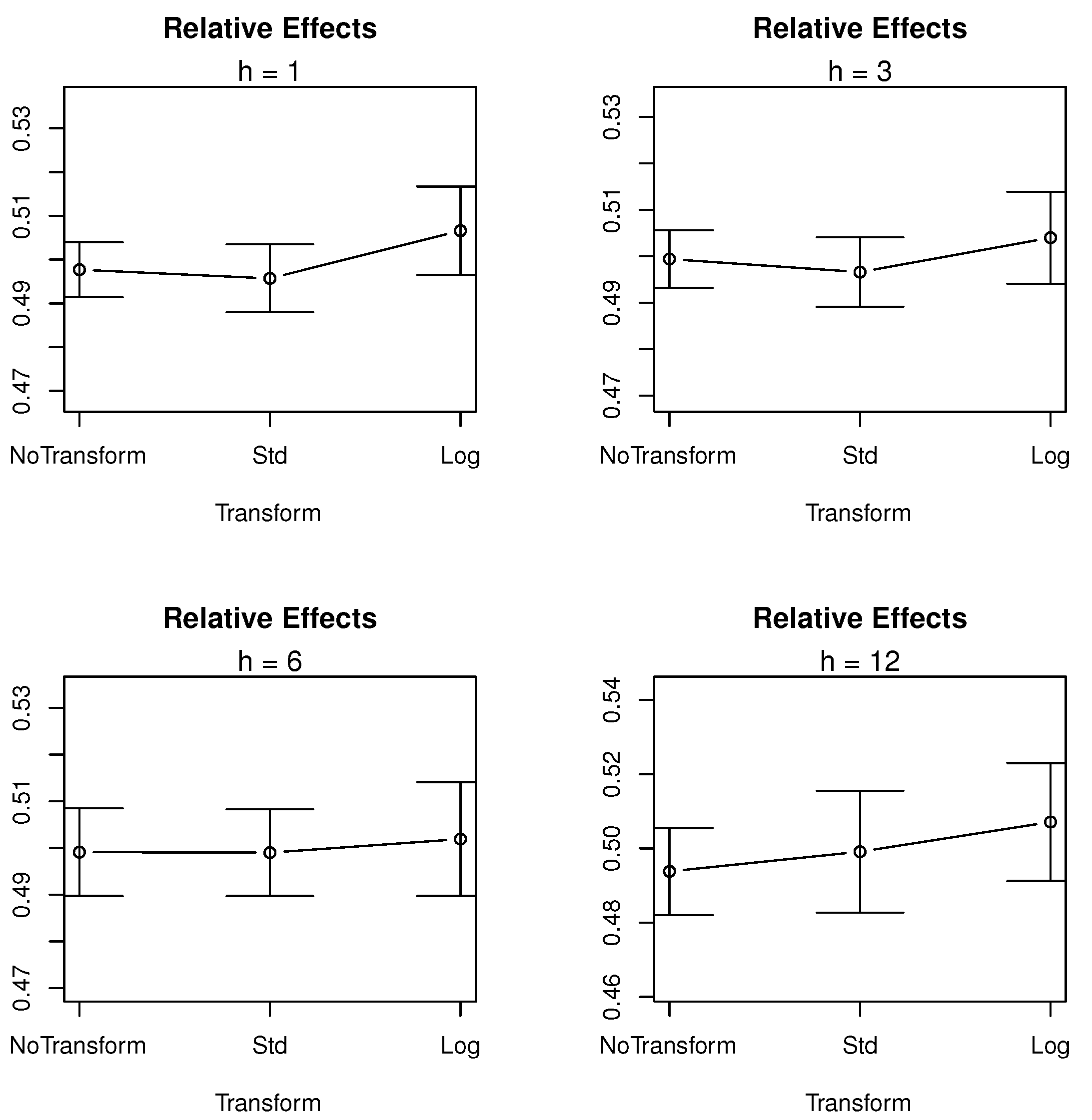

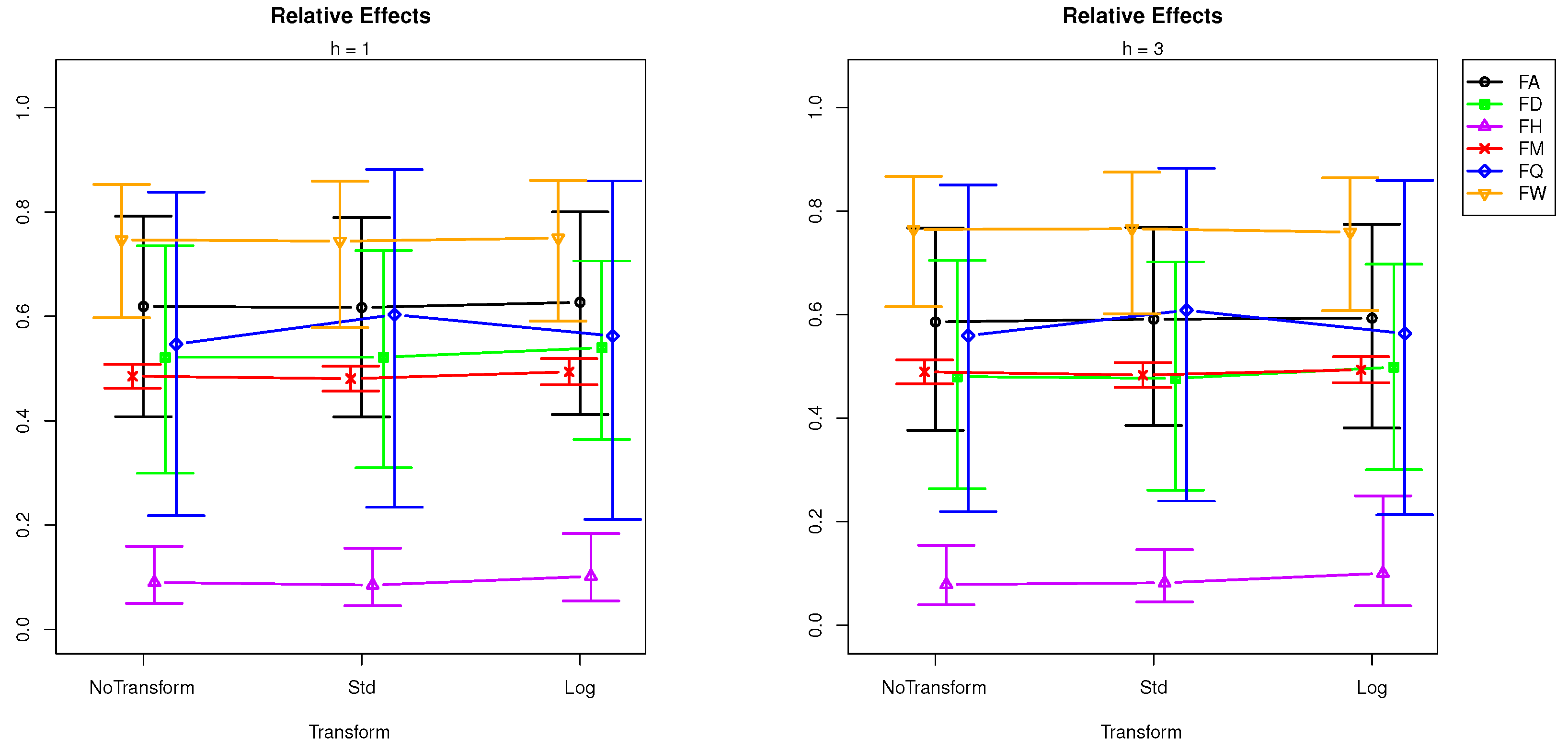

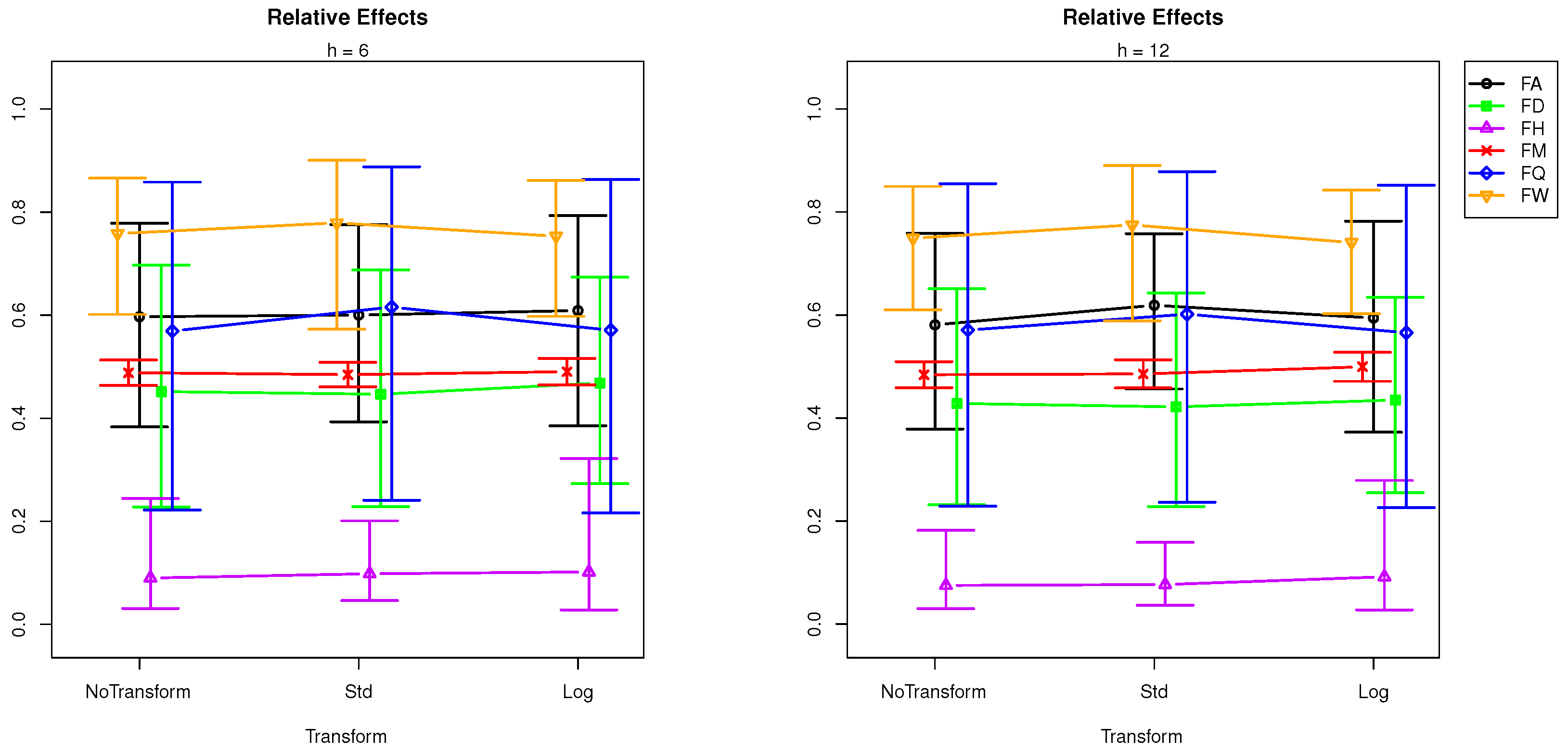

4. Comparison between Transformations

4.1. Root Mean Squared Forecast Error (RMSFE)

4.2. Nonparametric Repeated Measure Factorial Test

5. Data Analysis

- normality does not affect SSA forecasting performance;

- stationarity affects SSA forecasting performance in long-term forecasting (h = 12) but not at shorter horizons;

- skewness and sampling (observation) frequency affect SSA forecasting performance;

- transformation does not affect SSA forecasting performance, but the interaction between sampling frequencies and transformation is significant, which means the SSA performance is affected by transformation at some sampling frequencies.

6. Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Code | Name of Time Series |

|---|---|

| A001 | US Economic Statistics: Capacity Utilization. |

| A002 | Births by months 1853–2012. |

| A003 | Electricity: electricity net generation: total (all sectors). |

| A004 | Energy prices: average retail prices of electricity. |

| A005 | Coloured fox fur returns, Hopedale, Labrador, 1834–1925. |

| A006 | Alcohol demand (log spirits consumption per head), UK, 1870–1938. |

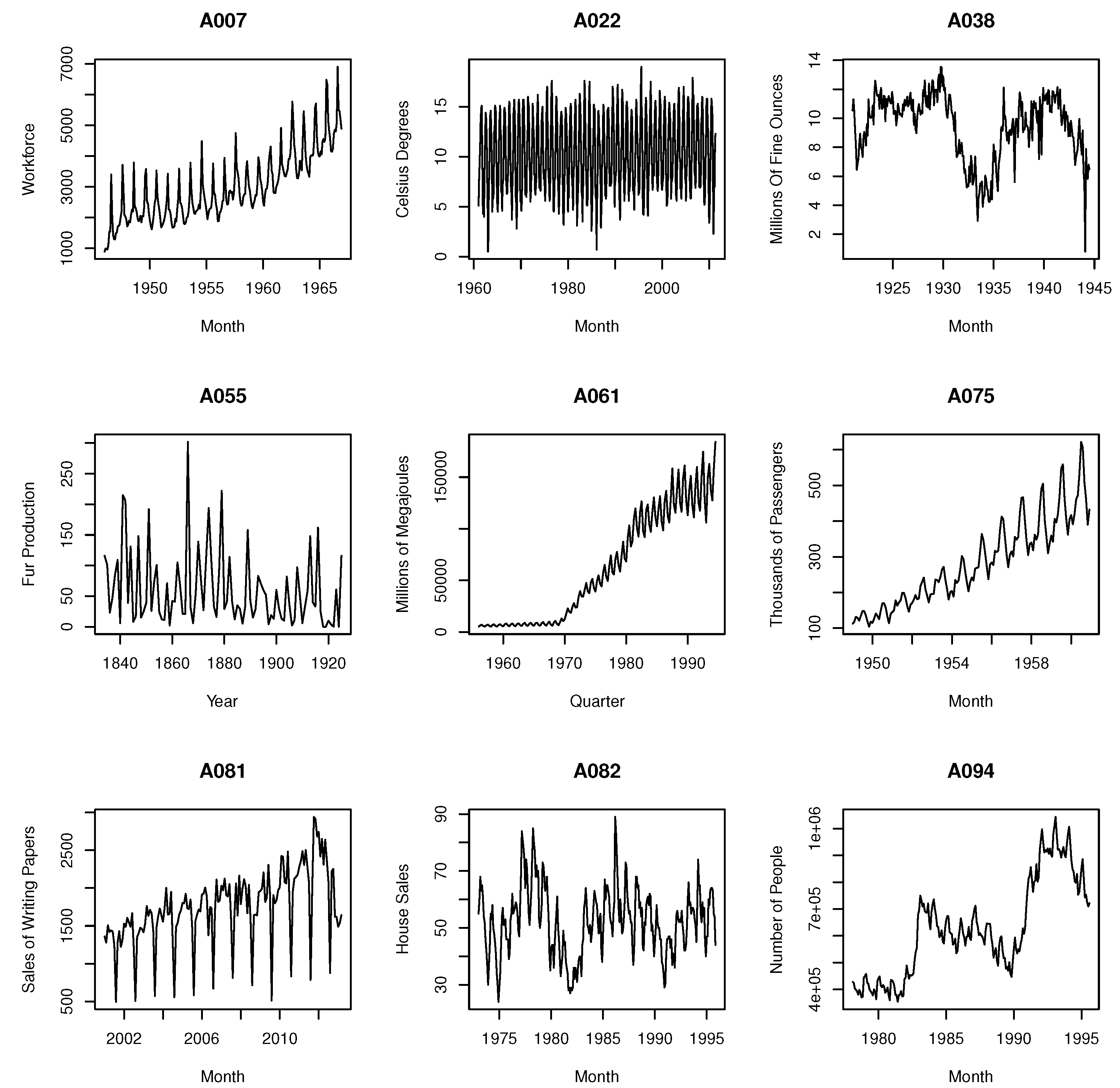

| A007 | Monthly Sutter county workforce, Jan. 1946–Dec. 1966 priesema (1979). |

| A008 | Exchange rates—monthly data: Japanese yen. |

| A009 | Exchange rates—monthly data: Pound sterling. |

| A010 | Exchange rates—monthly data: Romanian leu. |

| A011 | HICP (2005 = 100)—monthly data (annual rate of change): European Union (27 countries). |

| A012 | HICP (2005 = 100)—monthly data (annual rate of change): UK. |

| A013 | HICP (2005 = 100)—monthly data (annual rate of change): US. |

| A014 | New Homes Sold in the United States. |

| A015 | Goods, Value of Exports for United States. |

| A016 | Goods, Value of Imports for United States. |

| A017 | Market capitalisation—monthly data: UK. |

| A018 | Market capitalisation—monthly data: US. |

| A019 | Average monthly temperatures across the world (1701–2011): Bournemouth. |

| A020 | Average monthly temperatures across the world (1701–2011): Eskdalemuir. |

| A021 | Average monthly temperatures across the world (1701–2011): Lerwick. |

| A022 | Average monthly temperatures across the world (1701–2011): Valley. |

| A023 | Average monthly temperatures across the world (1701–2011): Death Valley. |

| A024 | US Economic Statistics: Personal Savings Rate. |

| A025 | Economic Policy Uncertainty Index for United States (Monthly Data). |

| A026 | Coal Production, Total for Germany. |

| A027 | Coke, Beehive Production (by Statistical Area). |

| A028 | Monthly champagne sales (in 1000’s) (p. 273: Montgomery: Fore. and T.S.). |

| A029 | Domestic Auto Production. |

| A030 | Index of Cotton Textile Production for France. |

| A031 | Index of Production of Chemical Products (by Statistical Area). |

| A032 | Index of Production of Leather Products (by Statistical Area). |

| A033 | Index of Production of Metal Products (by Statistical Area). |

| A034 | Index of Production of Mineral Fuels (by Statistical Area). |

| A035 | Industrial Production Index. |

| A036 | Knit Underwear Production (by Statistical Area). |

| A037 | Lubricants Production for United States. |

| A038 | Silver Production for United States. |

| A039 | Slab Zinc Production (by Statistical Area). |

| A040 | Annual domestic sales and advertising of Lydia E, Pinkham Medicine, 1907 to 1960. |

| A041 | Chemical concentration readings. |

| A042 | Monthly Boston armed robberies January 1966-October 1975 Deutsch and Alt (1977). |

| A043 | Monthly Minneapolis public drunkenness intakes Jan.’66–Jul’78. |

| A044 | Motor vehicles engines and parts/CPI, Canada, 1976–1991. |

| A045 | Methane input into gas furnace: cu. ft/min. Sampling interval 9 s. |

| A046 | Monthly civilian population of Australia: thousand persons. February 1978–April 1991. |

| A047 | Daily total female births in California, 1959. |

| A048 | Annual immigration into the United States: thousands. 1820–1962. |

| A049 | Monthly New York City births: unknown scale. January 1946–December 1959. |

| A050 | Estimated quarterly resident population of Australia: thousand persons. |

| A051 | Annual Swedish population rates (1000’s) 1750–1849 Thomas (1940). |

| A052 | Industry sales for printing and writing paper (in Thousands of French francs). |

| A053 | Coloured fox fur production, Hebron, Labrador, 1834–1925. |

| A054 | Coloured fox fur production, Nain, Labrador, 1834–1925. |

| A055 | Coloured fox fur production, oak, Labrador, 1834–1925. |

| A056 | Monthly average daily calls to directory assistance Jan.’62–Dec’76. |

| A057 | Monthly Av. residential electricity usage Iowa city 1971–1979. |

| A058 | Montly av. residential gas usage Iowa (cubic feet) * 100 ’71–’79. |

| A059 | Monthly precipitation (in mm), January 1983–April 1994. London, United Kingdom. |

| A060 | Monthly water usage (ml/day), London Ontario, 1966–1988. |

| A061 | Quarterly production of Gas in Australia: million megajoules. Includes natural gas from July 1989. March 1956–September 1994. |

| A062 | Residential water consumption, Jan 1983–April 1994. London, United Kingdom. |

| A063 | The total generation of electricity by the U.S. electric industry (monthly data for the period Jan. 1985–Oct. 1996). |

| A064 | Total number of water consumers, January 1983–April 1994. London, United Kingdom. |

| A065 | Monthly milk production: pounds per cow. January 62–December 75. |

| A066 | Monthly milk production: pounds per cow. January 62–December 75, adjusted for month length. |

| A067 | Monthly total number of pigs slaughtered in Victoria. January 1980–August 1995. |

| A068 | Monthly demand repair parts large/heavy equip. Iowa 1972–1979. |

| A069 | Number of deaths and serious injuries in UK road accidents each month. January 1969–December 1984. |

| A070 | Passenger miles (Mil) flown domestic U.K. Jul. ’62–May ’72. |

| A071 | Monthly hotel occupied room av. ’63–’76 B.L.Bowerman et al. |

| A072 | Weekday bus ridership, Iowa city, Iowa (monthly averages). |

| A073 | Portland Oregon average monthly bus ridership (/100). |

| A074 | U.S. airlines: monthly aircraft miles flown (Millions) 1963–1970. |

| A075 | International airline passengers: monthly totals in thousands. January 49–December 60. |

| A076 | Sales: souvenir shop at a beach resort town in Queensland, Australia. January 1987–December 1993. |

| A077 | Der Stern: Weekly sales of wholesalers A, ’71–’72. |

| A078 | Der Stern: Weekly sales of wholesalers B, ’71–’72’ |

| A079 | Der Stern: Weekly sales of wholesalers ’71–’72. |

| A080 | Monthly sales of U.S. houses (thousands) 1965–1975. |

| A081 | CFE specialty writing papers monthly sales. |

| A082 | Monthly sales of new one-family houses sold in USA since 1973. |

| A083 | Wisconsin employment time series, food and kindred products, January 1961–October 1975. |

| A084 | Monthly gasoline demand Ontario gallon millions 1960–1975. |

| A085 | Wisconsin employment time series, fabricated metals, January 1961–October 1975. |

| A086 | Monthly empolyees wholes./retail Wisconsin ’61–’75 R.B.Miller. |

| A087 | US monthly sales of chemical related products. January 1971–December 1991. |

| A088 | US monthly sales of coal related products. January 1971–December 1991. |

| A089 | US monthly sales of petrol related products. January 1971–December 1991. |

| A090 | US monthly sales of vehicle related products. January 1971–December 1991. |

| A091 | Civilian labour force in Australia each month: thousands of persons. February 1978–August 1995. |

| A092 | Numbers on Unemployment Benefits in Australia: monthly January 1956–July 1992. |

| A093 | Monthly Canadian total unemployment figures (thousands) 1956–1975. |

| A094 | Monthly number of unemployed persons in Australia: thousands. February 1978–April 1991. |

| A095 | Monthly U.S. female (20 years and over) unemployment figures 1948–1981. |

| A096 | Monthly U.S. female (16–19 years) unemployment figures (thousands) 1948–1981. |

| A097 | Monthly unemployment figures in West Germany 1948–1980. |

| A098 | Monthly U.S. male (20 years and over) unemployment figures 1948–1981. |

| A099 | Wisconsin employment time series, transportation equipment, January 1961–October 1975. |

| A100 | Monthly U.S. male (16–19 years) unemployment figures (thousands) 1948–1981. |

| Code | F | N | Mean | Med. | SD | CV | Skew. | SW(p) | ADF | Code | F | N | Mean | Med. | SD | CV | Skew. | SW(p) | ADF |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A001 | M | 539 | 80 | 80 | 5 | 6 | −0.55 | <0.01 | −0.60 | A002 | M | 1920 | 271 | 249 | 88 | 33 | 0.16 | <0.01 | −1.82 |

| A003 | M | 484 | 2.59 × 10 | 2.61 × 10 | 6.88 × 10 | 27 | 0.15 | <0.01 | −0.90 | A004 | M | 310 | 7 | 7 | 2 | 28 | −0.24 | <0.01 | 0.56 |

| A005 | D | 92 | 47.63 | 31.00 | 47.33 | 99.36 | 2.27 | <0.01 | −3.16 | A006 | Q | 207 | 1.95 | 1.98 | 0.25 | 12.78 | −0.58 | <0.01 | 0.46 |

| A007 | M | 252 | 2978 | 2741 | 1111 | 37.32 | 0.79 | <0.01 | −0.80 | A008 | M | 160 | 128 | 128 | 19 | 15 | 0.34 | <0.01 | −0.59 |

| A009 | M | 160 | 0.72 | 0.69 | 0.10 | 13 | 0.66 | <0.01 | 0.53 | A010 | M | 160 | 3.41 | 3.61 | 0.83 | 24 | −0.92 | <0.01 | 1.58 |

| A011 | M | 201 | 4.7 | 2.6 | 5.0 | 106 | 2.24 | <0.01 | −2.66 | A012 | M | 199 | 2.1 | 1.9 | 1.0 | 49 | 0.92 | <0.01 | −0.79 |

| A013 | M | 176 | 2.5 | 2.4 | 1.6 | 66 | −0.52 | <0.01 | −2.27 | A014 | M | 606 | 55 | 53 | 20 | 35 | 0.79 | <0.01 | −1.41 |

| A015 | M | 672 | 3.39 | 1.89 | 3.48 | 103 | 1.09 | <0.01 | 2.46 | A016 | M | 672 | 5.18 | 2.89 | 5.78 | 111 | 1.13 | <0.01 | 1.91 |

| A017 | M | 249 | 130 | 130 | 24 | 19 | 0.35 | <0.01 | 0.24 | A018 | M | 249 | 112 | 114 | 25 | 22 | −0.01 | 0.01* | 0.06 |

| A019 | M | 605 | 10.1 | 9.6 | 4.5 | 44 | 0.05 | <0.01 | −4.77 | A020 | M | 605 | 7.3 | 6.9 | 4.3 | 59 | 0.04 | <0.01 | −6.07 |

| A021 | M | 605 | 7.2 | 6.8 | 3.3 | 46 | 0.13 | <0.01 | −4.93 | A022 | M | 605 | 10.3 | 9.9 | 3.8 | 37 | 0.04 | <0.01 | −4.19 |

| A023 | M | 605 | 24 | 24 | 10 | 40 | −0.02 | <0.01 | −7.15 | A024 | M | 636 | 6.9 | 7.4 | 2.6 | 38 | −0.29 | <0.01 | −1.18 |

| A025 | M | 343 | 108 | 100 | 33 | 30 | 0.99 | <0.01 | −1.23 | A026 | M | 277 | 11.7 | 11.9 | 2.3 | 20 | −0.16 | 0.06 * | −0.40 |

| A027 | M | 171 | 0.21 | 0.13 | 0.19 | 88 | 1.26 | <0.01 | −1.81 | A028 | M | 96 | 4801 | 4084 | 2640 | 54.99 | 1.55 | <0.01 | −1.66 |

| A029 | M | 248 | 391 | 385 | 116 | 30 | −0.03 | 0.08 * | −1.22 | A030 | M | 139 | 89 | 92 | 12 | 13 | −0.82 | <0.01 | −0.28 |

| A031 | M | 121 | 134 | 138 | 27 | 20 | 0.05 | <0.01 | 1.51 | A032 | M | 153 | 113 | 114 | 10 | 9 | −0.29 | 0.45 * | −0.52 |

| A033 | M | 115 | 117 | 118 | 17 | 15 | −0.29 | 0.03 * | −0.46 | A034 | M | 115 | 110 | 111 | 11 | 10 | −0.53 | 0.02 * | 0.30 |

| A035 | M | 1137 | 40 | 34 | 31 | 78 | 0.56 | <0.01 | 5.14 | A036 | M | 165 | 1.08 | 1.10 | 0.20 | 18.37 | −1.15 | <0.01 | −0.59 |

| A037 | M | 479 | 3.04 | 2.83 | 1.02 | 33.60 | 0.46 | <0.01 | 0.61 | A038 | M | 283 | 9.39 | 10.02 | 2.27 | 24.15 | −0.80 | <0.01 | −1.01 |

| A039 | M | 452 | 54 | 52 | 19 | 36 | −0.15 | <0.01 | 0.08 | A040 | Q | 108 | 1382 | 1206 | 684 | 49.55 | 0.83 | <0.01 | −0.80 |

| A041 | H | 197 | 17.06 | 17.00 | 0.39 | 2.34 | 0.15 | 0.21 * | 0.09 | A042 | M | 118 | 196.3 | 166.0 | 128.0 | 65.2 | 0.45 | <0.01 | 0.41 |

| A043 | M | 151 | 391.1 | 267.0 | 237.49 | 60.72 | 0.43 | <0.01 | −1.17 | A044 | M | 188 | 1344 | 1425 | 479.1 | 35.6 | −0.41 | <0.01 | −1.28 |

| A045 | H | 296 | −0.05 | 0.00 | 1.07 | −1887 | −0.05 | 0.55 * | −7.66 | A046 | M | 159 | 11890 | 11830 | 882.93 | 7.42 | 0.12 | <0.01 | 5.71 |

| A047 | D | 365 | 41.98 | 42.00 | 7.34 | 17.50 | 0.44 | <0.01 | −1.07 | A048 | A | 143 | 2.5 × 10 | 2.2 × 10 | 2.1 × 10 | 83.19 | 1.06 | <0.01 | −2.63 |

| A049 | M | 168 | 25.05 | 24.95 | 2.31 | 9.25 | −0.02 | 0.02 * | 0.07 | A050 | Q | 89 | 15274 | 15184 | 1358 | 8.89 | 0.19 | <0.01 | 9.72 |

| A051 | A | 100 | 6.69 | 7.50 | 5.88 | 87.87 | −2.45 | <0.01 | −3.06 | A052 | M | 120 | 713 | 733 | 174 | 24.39 | −1.09 | <0.01 | −0.78 |

| A053 | A | 91 | 81.58 | 46.00 | 102.07 | 125.11 | 2.80 | <0.01 | −3.44 | A054 | A | 91 | 101.80 | 77.00 | 92.14 | 90.51 | 1.43 | <0.01 | −3.38 |

| A055 | A | 91 | 59.45 | 39.00 | 60.42 | 101.63 | 1.56 | <0.01 | −3.99 | A056 | M | 180 | 492.50 | 521.50 | 189.54 | 38.48 | −0.17 | <0.01 | −0.65 |

| A057 | M | 106 | 489.73 | 465.00 | 93.34 | 19.06 | 0.92 | <0.01 | −1.21 | A058 | M | 106 | 124.71 | 94.50 | 84.15 | 67.48 | 0.52 | <0.01 | −3.88 |

| A059 | M | 136 | 85.66 | 80.25 | 37.54 | 43.83 | 0.91 | <0.01 | −1.88 | A060 | M | 276 | 118.61 | 115.63 | 26.39 | 22.24 | 0.86 | <0.01 | −0.47 |

| A061 | Q | 155 | 61728 | 47976 | 53907 | 87.33 | 0.44 | <0.01 | 0.06 | A062 | M | 136 | 5.72 × 10 | 5.53 × 10 | 1.2 × 10 | 21.51 | 1.13 | <0.01 | −0.84 |

| A063 | M | 142 | 231.09 | 226.73 | 24.37 | 10.55 | 0.52 | 0.01 | −0.39 | A064 | M | 136 | 31388 | 31251 | 3232 | 10.30 | 0.25 | 0.22 * | −0.16 |

| A065 | M | 156 | 754.71 | 761.00 | 102.20 | 13.54 | 0.01 | 0.04 * | 0.04 | A066 | M | 156 | 746.49 | 749.15 | 98.59 | 13.21 | 0.08 | 0.04 * | −0.38 |

| A067 | M | 188 | 90640 | 91661 | 13926 | 15.36 | −0.38 | 0.01 * | −0.38 | A068 | M | 94 | 1540 | 1532 | 474.35 | 30.79 | 0.38 | 0.05 * | 0.54 |

| A069 | M | 192 | 1670 | 1631 | 289.61 | 17.34 | 0.53 | <0.01 | −0.74 | A070 | M | 119 | 91.09 | 86.20 | 32.80 | 36.01 | 0.34 | <0.01 | −1.93 |

| A071 | M | 168 | 722.30 | 709.50 | 142.66 | 19.75 | 0.72 | <0.01 | −0.52 | A072 | W | 136 | 5913 | 5500 | 1784 | 30.17 | 0.67 | <0.01 | −0.68 |

| A073 | M | 114 | 1120 | 1158 | 270.89 | 24.17 | −0.37 | <0.01 | 0.76 | A074 | M | 96 | 10385 | 10401 | 2202 | 21.21 | 0.33 | 0.18 * | −0.13 |

| A075 | M | 144 | 280.30 | 265.50 | 119.97 | 42.80 | 0.57 | <0.01 | −0.35 | A076 | M | 84 | 14315 | 8771 | 15748 | 110 | 3.37 | <0.01 | −0.29 |

| A077 | W | 104 | 11909 | 11640 | 1231 | 10.34 | 0.60 | <0.01 | −0.16 | A078 | W | 104 | 74636 | 73600 | 4737 | 6.35 | 0.64 | <0.01 | −0.59 |

| A079 | W | 104 | 1020 | 1012 | 71.78 | 7.03 | 0.60 | 0.01 * | −0.41 | A080 | M | 132 | 45.36 | 44.00 | 10.38 | 22.88 | 0.17 | 0.15 * | −0.81 |

| A081 | M | 147 | 1745 | 1730 | 479.52 | 27.47 | −0.39 | <0.01 | −1.15 | A082 | M | 275 | 52.29 | 53.00 | 11.94 | 22.83 | 0.18 | 0.13 * | −1.30 |

| A083 | M | 178 | 58.79 | 55.80 | 6.68 | 11.36 | 0.93 | <0.01 | −0.92 | A084 | M | 192 | 1.62 × 10 | 1.57 × 10 | 41661 | 25.71 | 0.32 | <0.01 | 0.25 |

| A085 | M | 178 | 40.97 | 41.50 | 5.11 | 12.47 | −0.07 | <0.01 | 1.45 | A086 | M | 178 | 307.56 | 308.35 | 46.76 | 15.20 | 0.17 | <0.01 | 1.51 |

| A087 | M | 252 | 13.70 | 14.08 | 6.13 | 44.73 | 0.16 | <0.01 | 1.13 | A088 | M | 252 | 65.67 | 68.20 | 14.25 | 21.70 | −0.53 | <0.01 | −0.53 |

| A089 | M | 252 | 10.76 | 10.92 | 5.11 | 47.50 | −0.19 | <0.01 | −0.05 | A090 | M | 252 | 11.74 | 11.05 | 5.11 | 43.54 | 0.38 | <0.01 | −0.88 |

| A091 | M | 211 | 7661 | 7621 | 819 | 10.70 | 0.03 | <0.01 | 3.27 | A092 | M | 439 | 2.21 × 10 | 5.67 × 10 | 2.35 × 10 | 106.32 | 0.77 | <0.01 | 1.61 |

| A093 | M | 240 | 413.28 | 396.50 | 152.84 | 36.98 | 0.36 | <0.01 | −1.60 | A094 | M | 211 | 6787 | 6528 | 604.62 | 8.91 | 0.56 | <0.01 | 2.69 |

| A095 | M | 408 | 1373 | 1132 | 686.05 | 49.96 | 0.91 | <0.01 | 0.60 | A096 | M | 408 | 422.38 | 342.00 | 252.86 | 59.87 | 0.65 | <0.01 | −1.95 |

| A097 | M | 396 | 7.14 × 10 | 5.57 × 10 | 5.64 × 10 | 78.97 | 0.79 | <0.01 | −2.51 | A098 | M | 408 | 1937 | 1825 | 794 | 41.04 | 0.64 | <0.01 | −1.15 |

| A099 | M | 178 | 40.60 | 40.50 | 4.95 | 12.19 | −0.65 | <0.01 | −0.10 | A100 | M | 408 | 520.28 | 425.50 | 261.22 | 50.21 | 0.64 | <0.01 | −1.65 |

| Series’ | h = 1 | h = 3 | |||||

|---|---|---|---|---|---|---|---|

| Code | NT | Std | Log | NT | Std | Log | |

| A001 | 1.283 | 0.542 | 1.144 | 1.884 | 1.157 | 1.715 | |

| A002 | 36.275 | 35.019 | 28.844 | 36.991 | 35.900 | 30.741 | |

| A003 | 12,521.688 | 13,643.067 | 13,616.737 | 16,041.250 | 16,584.228 | 17,449.138 | |

| A004 | 0.250 | 0.150 | 0.139 | 0.792 | 0.354 | 0.333 | |

| A005 | 61.625 | 61.548 | 60.476 | 53.906 | 53.268 | 58.074 | |

| A006 | 0.068 | 0.063 | 0.067 | 0.100 | 0.107 | 0.099 | |

| A007 | 338.358 | 511.055 | 288.753 | 511.033 | 560.970 | 331.925 | |

| A008 | 7.129 | 5.667 | 7.505 | 19.200 | 16.096 | 17.845 | |

| A009 | 0.042 | 0.040 | 0.042 | 0.051 | 0.051 | 0.051 | |

| A010 | 0.122 | 0.107 | 0.155 | 0.268 | 0.306 | 0.417 | |

| A011 | 0.338 | 0.229 | 0.286 | 0.831 | 0.407 | 0.560 | |

| A012 | 0.984 | 0.963 | 1.049 | 1.374 | 1.410 | 1.386 | |

| A013 | 1.345 | 1.101 | 1.395 | 3.141 | 2.971 | 7.484 | |

| A014 | 8.096 | 6.829 | 6.410 | 9.515 | 9.810 | 9.638 | |

| A015 | 7.24 × 10 | 6.45 × 10 | 6.31 × 10 | 1.1 × 10 | 8.45 × 10 | 7.08 × 10 | |

| A016 | 1.28 × 10 | 1.46 × 10 | 1.56 × 10 | 1.76 × 10 | 1.74 × 10 | 1.81 × 10 | |

| A017 | 12.423 | 9.066 | Inf | 19.782 | 15.435 | Inf | |

| A018 | 7.950 | 8.093 | 10.205 | 15.132 | 12.983 | 16.137 | |

| A019 | 1.429 | 1.425 | 1.375 | 1.531 | 1.510 | 1.469 | |

| A020 | 1.319 | 1.389 | 1.669 | 1.363 | 1.482 | 1.429 | |

| A021 | 1.070 | 1.076 | 1.051 | 1.129 | 1.147 | 1.122 | |

| A022 | 1.133 | 1.209 | 1.152 | 1.280 | 1.270 | 1.275 | |

| A023 | 6.097 | 5.936 | 5.309 | 6.551 | 6.674 | 5.980 | |

| A024 | 0.959 | 0.771 | 0.954 | 1.067 | 0.971 | 1.096 | |

| A025 | 22.689 | 26.924 | 56.529 | 26.056 | 43.196 | 49.542 | |

| A026 | 1.174 | 1.212 | 2.490 | 1.686 | 1.787 | 3.475 | |

| A027 | 0.050 | 0.100 | 0.064 | 0.114 | 0.509 | 0.226 | |

| A028 | 4137.576 | 4218.129 | 4038.143 | 4474.756 | 4199.967 | 4183.622 | |

| A029 | 59.124 | 44.474 | 52.390 | 62.490 | 69.349 | 78.321 | |

| A030 | 15.207 | 31.175 | 16.755 | 24.388 | 51.218 | 32.464 | |

| A031 | 8.783 | 5.662 | 8.633 | 80.118 | 8.464 | 18.103 | |

| A032 | 9.779 | 10.315 | 9.972 | 12.431 | 13.093 | 12.748 | |

| A033 | 5.820 | 5.432 | 5.791 | 9.729 | 8.527 | 10.148 | |

| A034 | 3.061 | 2.785 | 3.320 | 5.796 | 5.286 | 6.157 | |

| A035 | 0.965 | 1.455 | 5.973 | 1.536 | 2.155 | 6.234 | |

| A036 | 0.151 | 0.175 | 0.186 | 0.169 | 0.279 | 0.249 | |

| A037 | 0.293 | 0.310 | 0.308 | 0.417 | 0.395 | 0.368 | |

| A038 | 1.923 | 1.243 | 3.462 | 2.427 | 1.370 | 2.474 | |

| A039 | 4.853 | 3.508 | 5.107 | 7.494 | 6.099 | 9.125 | |

| A040 | 489.909 | 614.577 | 717.710 | 815.463 | 785.927 | 929.787 | |

| A041 | 0.329 | 0.322 | 0.328 | 0.390 | 0.408 | 0.389 | |

| A042 | 68.459 | 82.182 | 67.108 | 132.417 | 212.367 | 118.468 | |

| A043 | 33.081 | 33.066 | 33.750 | 41.996 | 40.189 | 43.350 | |

| A044 | 420.634 | 389.750 | 545.116 | 538.590 | 552.070 | 726.264 | |

| A045 | 0.522 | 0.522 | 0.886 | 0.999 | 0.998 | 1.297 | |

| A046 | 15.552 | 1.906 | 1.169 | 18.721 | 5.275 | 3.773 | |

| A047 | 8.206 | 8.222 | 11.116 | 8.679 | 8.640 | 10.166 | |

| A048 | 3.15 × 10 | 1.66 × 10 | 1.79 × 10 | 3.82 × 10 | 1.95 × 10 | 595,729.790 | |

| A049 | 1.189 | 1.248 | 1.199 | 1.277 | 1.377 | 1.285 | |

| A050 | 18.038 | 128.254 | 17.562 | 37.219 | 295.980 | 35.731 | |

| Series’ | h = 1 | h = 3 | ||||

|---|---|---|---|---|---|---|

| Code | NT | Std | Log | NT | Std | Log |

| A051 | 3.983 | 3.976 | 4.003 | 5.694 | 5.612 | 5.605 |

| A052 | 272.279 | 276.113 | 574.713 | 268.784 | 271.246 | 445.832 |

| A053 | 35.559 | 39.680 | 36.963 | 26.795 | 32.500 | 31.927 |

| A054 | 124.519 | 89.800 | 125.412 | 110.606 | 88.796 | 107.684 |

| A055 | 43.121 | 37.090 | 44.808 | 34.715 | 37.302 | 40.039 |

| A056 | 266.333 | 99.502 | 1.43E+12 | 287.931 | 214.556 | 9.42 × 10 |

| A057 | 125.600 | 84.462 | 126.023 | 131.253 | 92.122 | 129.780 |

| A058 | 38.474 | 35.384 | 71.104 | 119.964 | 99.107 | 139.656 |

| A059 | 44.950 | 41.240 | 45.696 | 45.079 | 40.224 | 45.094 |

| A060 | 7.598 | 8.085 | 7.845 | 8.248 | 9.090 | 8.709 |

| A061 | 6819.116 | 7597.052 | 23,730.348 | 10,097.877 | 11,645.535 | 16,058.889 |

| A062 | 8.44 × 10 | 7.04 × 10 | 1.37 × 10 | 1.42 × 10 | 8.94 × 10 | 1.76 × 10 |

| A063 | 21.829 | 21.831 | 13.583 | 26.600 | 26.655 | 10.258 |

| A064 | 4393.038 | 3077.310 | 4376.077 | 5016.437 | 2925.211 | 4980.827 |

| A065 | 28.982 | 11.405 | 27.430 | 30.717 | 16.662 | 30.903 |

| A066 | 12.033 | 10.131 | 15.854 | 19.196 | 16.703 | 28.192 |

| A067 | 11,923.554 | 11,039.522 | 10,617.132 | 17,077.208 | 13,448.762 | 13,328.422 |

| A068 | 362.752 | 357.340 | 369.231 | 462.893 | 433.739 | 473.690 |

| A069 | 160.579 | 203.037 | 208.287 | 203.002 | 208.562 | 230.166 |

| A070 | 14.483 | 13.741 | 14.152 | 29.635 | 26.206 | 29.278 |

| A071 | 26.793 | 27.217 | 23.647 | 27.381 | 33.930 | 25.245 |

| A072 | 1379.200 | 1382.348 | 1472.325 | 1565.464 | 1624.687 | 1401.969 |

| A073 | 69.327 | 69.141 | 68.699 | 122.183 | 114.652 | 115.324 |

| A074 | 3294.883 | 2015.225 | 3445.829 | 3741.524 | 2288.009 | 3749.168 |

| A075 | 48.901 | 59.574 | 58.507 | 41.848 | 117.860 | 64.366 |

| A076 | 25,153.667 | 29,044.831 | 19,684.339 | 35,607.579 | 58,525.282 | 21,322.355 |

| A077 | 394.752 | 387.456 | 395.114 | 873.390 | 813.589 | 836.260 |

| A078 | 701.741 | 1275.259 | 790.650 | 1805.609 | 4921.674 | 1802.354 |

| A079 | 35.709 | 34.064 | 35.661 | 45.108 | 43.559 | 45.010 |

| A080 | 8.947 | 7.183 | 9.725 | 13.505 | 11.505 | 19.930 |

| A081 | 498.376 | 530.862 | 473.551 | 380.003 | 447.889 | 438.681 |

| A082 | 9.233 | 7.292 | 5.204 | 11.262 | 9.342 | 6.710 |

| A083 | 1.291 | 1.137 | 1.225 | 1.621 | 1.477 | 1.518 |

| A084 | 21,495.185 | 9111.162 | 11,832.143 | 32,355.027 | 9641.016 | 11,414.744 |

| A085 | 0.883 | 0.862 | 0.641 | 2.054 | 1.640 | 1.273 |

| A086 | 3.725 | 2.874 | 3.613 | 5.016 | 4.500 | 4.665 |

| A087 | 1.035 | 1.273 | 0.768 | 1.408 | 1.958 | 1.148 |

| A088 | 7.109 | 7.672 | 6.258 | 5.385 | 7.010 | 5.581 |

| A089 | 0.862 | 1.170 | 1.025 | 2.248 | 2.282 | 2.331 |

| A090 | 2.164 | 2.428 | 2.081 | 2.755 | 2.609 | 2.373 |

| A091 | 240.568 | 124.286 | 129.086 | 1376.708 | 148.271 | 160.964 |

| A092 | 3.35 × 10 | 31,233.891 | 16,483.627 | 2.38× 10 | 71,880.798 | 40,209.373 |

| A093 | 63.119 | 5.79× 10 | 54.632 | 300.893 | 1.35× 10 | 76.301 |

| A094 | 44,254.670 | 66,245.621 | 66,414.588 | 76,182.034 | 86,009.422 | 91,714.035 |

| A095 | 136.663 | 139.571 | 144.039 | 287.480 | 311.372 | 265.696 |

| A096 | 58.558 | 80.578 | 67.889 | 65.715 | 79.429 | 70.496 |

| A097 | 1.42× 10 | 144,364.409 | 143,654.990 | 192,501.733 | 182,442.168 | 192,581.617 |

| A098 | 441.676 | 476.749 | 173.231 | 691.051 | 595.127 | 372.177 |

| A099 | 3.199 | 3.168 | 4.478 | 3.236 | 3.075 | 5.052 |

| A100 | 79.931 | 90.467 | 79.684 | 132.074 | 118.099 | 109.238 |

| Series’ | h = 6 | h = 12 | ||||

|---|---|---|---|---|---|---|

| Code | NT | Std | Log | NT | Std | Log |

| A001 | 3.083 | 2.326 | 2.919 | 5.593 | 4.355 | 5.503 |

| A002 | 37.593 | 36.769 | 33.318 | 39.847 | 38.221 | 37.346 |

| A003 | 16,770.672 | 17,357.863 | 16,657.420 | 15,925.414 | 18,493.303 | 16,868.789 |

| A004 | 0.709 | 0.455 | 0.446 | 0.715 | 0.639 | 0.585 |

| A005 | 63.208 | 61.157 | 63.065 | 61.792 | 60.274 | 61.740 |

| A006 | 0.140 | 0.144 | 0.138 | 0.209 | 0.194 | 0.204 |

| A007 | 642.282 | 522.970 | 388.967 | 613.790 | 550.802 | 482.934 |

| A008 | 36.757 | 22.657 | 32.054 | 31.678 | 25.325 | 31.028 |

| A009 | 0.063 | 0.064 | 0.063 | 0.091 | 0.092 | 0.091 |

| A010 | 0.381 | 0.489 | 0.515 | 0.492 | 0.908 | 2.268 |

| A011 | 0.964 | 0.817 | 0.689 | 0.929 | 1.592 | 0.977 |

| A012 | 1.856 | 1.994 | 1.782 | 2.536 | 2.947 | 2.197 |

| A013 | 4.561 | 3.983 | 142.109 | 3.901 | 3.624 | 2.37 × 10 |

| A014 | 10.397 | 9.917 | 10.106 | 13.580 | 12.915 | 13.602 |

| A015 | 1.92 × 10 | 1.12 × 10 | 8.94 × 10 | 2.86 × 10 | 1.65 × 10 | 1.14 × 10 |

| A016 | 2.44 × 10 | 2.09 × 10 | 2.15 × 10 | 4.10 × 10 | 2.70 × 10 | 2.80 × 10 |

| A017 | 30.286 | 23.902 | Inf | 46.368 | 28.383 | Inf |

| A018 | 21.450 | 19.146 | 20.342 | 34.721 | 21.988 | 28.244 |

| A019 | 1.555 | 1.436 | 1.447 | 1.517 | 1.476 | 1.511 |

| A020 | 1.330 | 1.391 | 1.435 | 1.387 | 1.440 | 1.557 |

| A021 | 1.138 | 1.134 | 1.092 | 1.126 | 1.134 | 1.166 |

| A022 | 1.265 | 1.239 | 1.287 | 1.321 | 1.265 | 1.273 |

| A023 | 6.861 | 6.813 | 6.278 | 7.870 | 7.750 | 7.283 |

| A024 | 1.198 | 1.293 | 1.283 | 1.396 | 1.943 | 1.555 |

| A025 | 29.947 | 44.077 | 78.266 | 33.726 | 57.839 | 467.347 |

| A026 | 2.515 | 3.076 | 4.651 | 2.847 | 4.475 | 5.937 |

| A027 | 0.152 | 13.916 | 0.486 | 0.180 | 12187.788 | 0.889 |

| A028 | 4436.727 | 4208.136 | 3995.665 | 2687.645 | 3283.876 | 2860.657 |

| A029 | 70.063 | 104.764 | 108.981 | 80.046 | 153.812 | 222.842 |

| A030 | 40.923 | 103.102 | 82.010 | 50.163 | 1302.044 | 200.370 |

| A031 | 1557.631 | 12.751 | 9.338 | 2.16E+25 | 16.890 | 348,877.932 |

| A032 | 15.136 | 13.364 | 14.781 | 20.471 | 11.586 | 19.519 |

| A033 | 16.619 | 11.811 | 14.619 | 338.296 | 212.221 | 31,730.543 |

| A034 | 10.100 | 9.151 | 11.136 | 27.066 | 16.203 | 24.326 |

| A035 | 2.554 | 3.283 | 6.623 | 4.415 | 5.513 | 7.378 |

| A036 | 0.190 | 0.179 | 0.199 | 0.259 | 0.241 | 0.237 |

| A037 | 0.542 | 0.494 | 0.467 | 0.706 | 0.795 | 0.771 |

| A038 | 2.077 | 1.588 | 2.504 | 4.153 | 2.112 | 3.248 |

| A039 | 9.958 | 7.750 | 15.538 | 12.330 | 9.615 | 27.556 |

| A040 | 1185.420 | 967.918 | 1187.496 | 1781.242 | 1087.955 | 1476.007 |

| A041 | 0.437 | 0.491 | 0.437 | 0.537 | 0.630 | 0.536 |

| A042 | 282.364 | 652.016 | 211.125 | 1844.972 | 4.31 × 10 | 488.603 |

| A043 | 68.250 | 65.163 | 82.580 | 114.347 | 100.176 | 263.026 |

| A044 | 467.834 | 637.165 | 587.869 | 511.228 | 585.946 | 626.670 |

| A045 | 1.422 | 1.419 | 1.661 | 1.334 | 1.329 | 1.570 |

| A046 | 23.722 | 11.922 | 9.536 | 35.328 | 28.669 | 19.088 |

| A047 | 8.883 | 8.557 | 10.191 | 9.115 | 8.849 | 9.983 |

| A048 | 6.35 × 10 | 2.25 × 10 | Inf | 2.73 × 10 | 2.71 × 10 | Inf |

| A049 | 1.353 | 1.320 | 1.355 | 1.326 | 1.424 | 1.338 |

| A050 | 59.765 | 528.428 | 56.831 | 103.999 | 935.576 | 99.881 |

| Series’ | h = 6 | h = 12 | ||||

|---|---|---|---|---|---|---|

| Code | NT | Std | Log | NT | Std | Log |

| A051 | 6.645 | 6.646 | 6.689 | 8.259 | 39.667 | 8.384 |

| A052 | 327.886 | 333.472 | 349.271 | 519.432 | 455.743 | 539,109.574 |

| A053 | 55.656 | 71.070 | 56.373 | 77.760 | 88.068 | 80.306 |

| A054 | 135.441 | 107.388 | 114.467 | 121.277 | 114.368 | 111.057 |

| A055 | 47.052 | 47.075 | 49.962 | 44.947 | 49.411 | 44.323 |

| A056 | 318.035 | 442.579 | Inf | 369.935 | 1397.180 | Inf |

| A057 | 111.700 | 97.869 | 110.430 | 76.521 | 123.163 | 78.379 |

| A058 | 93.679 | 73.906 | 161.798 | 76.617 | 72.198 | 33.833 |

| A059 | 47.999 | 43.077 | 49.706 | 47.200 | 38.382 | 50.650 |

| A060 | 9.065 | 9.929 | 8.915 | 9.775 | 11.311 | 9.225 |

| A061 | 21,401.308 | 21,029.664 | 34,763.978 | 47,497.769 | 42,578.592 | 43,718.789 |

| A062 | 1.53 × 10 | 9.22 × 10 | 1.43 × 10 | 1.04 × 10 | 9.77 × 10 | 1.33 × 10 |

| A063 | 28.561 | 28.558 | 10.218 | 25.355 | 25.598 | 9.908 |

| A064 | 4121.217 | 2945.853 | 3866.332 | 21881.052 | 3065.284 | 6688.179 |

| A065 | 31.507 | 24.464 | 27.822 | 31.161 | 39.859 | 30.524 |

| A066 | 33.907 | 24.501 | 26.523 | 85.870 | 39.738 | 25.640 |

| A067 | 24,790.111 | 14,696.437 | 16,013.912 | 40,325.312 | 12,620.240 | 18,179.972 |

| A068 | 490.894 | 450.505 | 499.947 | 327.430 | 426.795 | 335.514 |

| A069 | 233.149 | 233.000 | 217.660 | 261.487 | 235.576 | 212.738 |

| A070 | 21.055 | 17.474 | 36.299 | 18.092 | 15.445 | 16.239 |

| A071 | 30.033 | 30.922 | 28.063 | 23.335 | 37.390 | 28.972 |

| A072 | 991.918 | 1186.083 | 1013.985 | 1022.795 | 1148.504 | 1004.258 |

| A073 | 191.317 | 173.546 | 170.028 | 371.023 | 236.600 | 288.816 |

| A074 | 4012.015 | 2191.142 | 3290.446 | 8470.587 | 2279.084 | 3402.155 |

| A075 | 40.891 | 115.551 | 33.467 | 44.112 | 228.585 | 43.708 |

| A076 | 69,298.230 | 2.26 × 10 | 24,927.158 | 2.63 × 10 | 3.64 × 10 | 7571.182 |

| A077 | 1714.226 | 1532.812 | 1561.112 | 3608.945 | 2515.070 | 3097.836 |

| A078 | 4173.555 | 654,416.059 | 3581.874 | 1.25 × 10 | 1.01 × 10 | 7095.955 |

| A079 | 58.260 | 52.793 | 58.023 | 97.730 | 97.056 | 96.553 |

| A080 | 16.268 | 13.189 | 14.747 | 12.158 | 13.096 | 15.346 |

| A081 | 450.450 | 494.004 | 450.436 | 523.863 | 609.279 | 614.195 |

| A082 | 10.665 | 10.620 | 7.961 | 10.362 | 7.757 | 10.242 |

| A083 | 1.871 | 1.698 | 1.958 | 7.386 | 1.967 | 3.098 |

| A084 | 74,374.861 | 11,949.864 | 15,030.189 | 4.54 × 10 | 15,064.148 | 35,040.170 |

| A085 | 2.972 | 2.375 | 2.443 | 5.394 | 3.867 | 4.246 |

| A086 | 6.089 | 5.903 | 5.641 | 7.324 | 9.107 | 7.144 |

| A087 | 1.517 | 2.552 | 1.521 | 2.522 | 3.060 | 2.358 |

| A088 | 5.616 | 6.772 | 5.806 | 4.916 | 7.063 | 5.706 |

| A089 | 3.882 | 2.942 | 3.045 | 5.597 | 3.709 | 4.223 |

| A090 | 2.866 | 3.398 | 2.659 | 2.830 | 3.763 | 2.913 |

| A091 | 28,312.543 | 254.885 | 326.947 | 1.39 × 10 | 369.785 | 724.020 |

| A092 | 7.46 × 10 | 1.41 × 10 | 73816.394 | 9.10 × 10 | 3.81 × 10 | 1.36 × 10 |

| A093 | 7814.412 | 1.30 × 10 | 95.842 | 7.95 × 10 | 2.84 × 10 | 128.056 |

| A094 | 1.02 × 10 | 9.46 × 10 | 1.10 × 10 | 1.41 × 10 | 1.30 × 10 | 1.75 × 10 |

| A095 | 406.105 | 441.419 | 404.087 | 503.204 | 588.870 | 604.329 |

| A096 | 78.448 | 90.126 | 75.130 | 100.969 | 104.199 | 83.458 |

| A097 | 2.06 × 10 | 1.92 × 10 | 2.06 × 10 | 2.44 × 10 | 2.43 × 10 | 2.42 × 10 |

| A098 | 858.043 | 625.258 | 751.271 | 1077.612 | 849.184 | 1205.582 |

| A099 | 3.761 | 3.337 | 4.914 | 4.370 | 3.253 | 5.528 |

| A100 | 140.073 | 132.262 | 141.576 | 188.195 | 173.609 | 194.600 |

References

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice; OTexts: Melbourne, Australia, 2014. [Google Scholar]

- Lütkepohl, H.; Xu, F. The role of the log transformation in forecasting economic variables. Empir. Econ. 2012, 42, 619–638. [Google Scholar] [CrossRef] [Green Version]

- Bowden, G.J.; Dandy, G.C.; Maier, H.R. Data transformation for neural network models in water resources applications. J. Hydroinform. 2003, 5, 245–258. [Google Scholar] [CrossRef]

- Kling, J.L.; Bessler, D.A. A comparison of multivariate forecasting procedures for economic time series. Int. J. Forecast. 1985, 1, 5–24. [Google Scholar] [CrossRef]

- Chatfield, F.; Faraway, J. Time series forecasting with neural networks: A comparative study using the airline data. J. R. Stat. Soc. Ser. 1998, 47, 231–250. [Google Scholar] [CrossRef]

- Granger, C.; Newbold, P. Forecasting Economic Time Series, 2nd ed.; Academic Press: Cambridge, MA, USA, 1986. [Google Scholar]

- Chatfield, C.; Prothero, D. Box-Jenkins seasonal forecasting: Problems in a case study. J. R. Stat. Soc. Ser. 1973, 136, 295–336. [Google Scholar] [CrossRef]

- Haida, T.; Muto, S. Regression based peak load forecasting using a transformation technique. IEEE Trans. Power Syst. 1994, 9, 1788–1794. [Google Scholar] [CrossRef]

- Nelson, H.L., Jr.; Granger, C.W.J. Experience with using the Box-Cox transformation when forecasting economic time series. J. Econom. 1979, 10, 57–69. [Google Scholar] [CrossRef]

- Chen, S.; Wang, J.; Zhang, H. A hybrid PSO-SVM model based on clustering algorithm for short-term atmospheric pollutant concentration forecasting. Technol. Forecast. Soc. Chang. 2019, 146, 41–54. [Google Scholar] [CrossRef]

- Brave, S.A.; Butters, R.A.; Justiniano, A. Forecasting economic activity with mixed frequency BVARs. Int. J. Forecast. 2019, 35, 1692–1707. [Google Scholar] [CrossRef]

- Sanei, S.; Hassani, H. Singular Spectrum Analysis of Biomedical Signals; CRC Press: Boca Raton, FL, USA, 2015. [Google Scholar] [CrossRef]

- Golyandina, N.; Osipov, E. The ‘Caterpillar’-SSA method for analysis of time series with missing values. J. Stat. Plan. Inference 2007, 137, 2642–2653. [Google Scholar] [CrossRef]

- Silva, E.S.; Hassani, H.; Heravi, S.; Huang, X. Forecasting tourism demand with denoised neural networks. Ann. Tour. Res. 2019, 74, 134–154. [Google Scholar] [CrossRef]

- Silva, E.S.; Ghodsi, Z.; Ghodsi, M.; Heravi, S.; Hassani, H. Cross country relations in European tourist arrivals. Ann. Tour. Res. 2017, 63, 151–168. [Google Scholar] [CrossRef]

- Silva, E.S.; Hassani, H. On the use of singular spectrum analysis for forecasting U.S. trade before, during and after the 2008 recession. Int. Econ. 2015, 141, 34–49. [Google Scholar] [CrossRef] [Green Version]

- Silva, E.S.; Hassani, H.; Heravi, S. Modeling European industrial production with multivariate singular spectrum analysis: A cross-industry analysis. J. Forecast. 2018, 37, 371–384. [Google Scholar] [CrossRef]

- Hassani, H.; Silva, E.S. Forecasting UK consumer price inflation using inflation forecasts. Res. Econ. 2018, 72, 367–378. [Google Scholar] [CrossRef] [Green Version]

- Silva, E.S.; Hassani, H.; Gee, L. Googling Fashion: Forecasting fashion consumer behaviour using Google trends. Soc. Sci. 2019, 8, 111. [Google Scholar] [CrossRef] [Green Version]

- Hassani, H.; Silva, E.S.; Gupta, R.; Das, S. Predicting global temperature anomaly: A definitive investigation using an ensemble of twelve competing forecasting models. Phys. Stat. Mech. Appl. 2018, 509, 121–139. [Google Scholar] [CrossRef]

- Ghil, M.; Allen, R.M.; Dettinger, M.D.; Ide, K.; Kondrashov, D.; Mann, M.E.; Robertson, A.W.; Saunders, A.; Tian, Y.; Varadi, F.; et al. Advanced spectral methods for climatic time series. Rev. Geophys 2002, 40, 3.1–3.41. [Google Scholar] [CrossRef] [Green Version]

- Xu, S.; Hu, H.; Ji, L.; Wang, P. Embedding Dimension Selection for Adaptive Singular Spectrum Analysis of EEG Signal. Sensors 2018, 18, 697. [Google Scholar] [CrossRef] [Green Version]

- Mao, X.; Shang, P. Multivariate singular spectrum analysis for traffic time series. Phys. Stat. Mech. Appl. 2019, 526, 121063. [Google Scholar] [CrossRef]

- Golyandina, N.; Korobeynikov, A.; Zhigljavsky, A. Singular Spectrum Analysis with R. Use R; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar] [CrossRef]

- Ghodsi, M.; Hassani, H.; Rahmani, D.; Silva, E.S. Vector and recurrent singular spectrum analysis: Which is better at forecasting? J. Appl. Stat. 2018, 45, 1872–1899. [Google Scholar] [CrossRef]

- Singular Spectrum Analysis for Time Series; Springer: Berlin/Heidelberg, Germany, 2013. [CrossRef]

- Guerrero, V.M. Time series analysis supported by power transformations. J. Forecast. 1993, 12, 37–48. [Google Scholar] [CrossRef]

- Golyandina, N.; Nekrutkin, V.; Zhigljavski, A. Analysis of Time Series Structure: SSA and Related Techniques; CRC Press: Boca Raton, FL, USA, 2001. [Google Scholar]

- Khan, M.A.R.; Poskitt, D. Forecasting stochastic processes using singular spectrum analysis: Aspects of the theory and application. Int. J. Forecast. 2017, 33, 199–213. [Google Scholar] [CrossRef]

- Ioffe, S.; Szegedy, C. Batch normalization: Accelerating deep network training by reducing internal covariate shift. In Proceedings of the ICML’15: 32nd International Conference on International Conference on Machine Learning, Lille, France, 6–11 July 2015; Volume 37, pp. 448–456. [Google Scholar]

- Akritas, M.G.; Arnold, S.F. Fully nonparametric hypotheses for factorial designs I: Multivariate repeated measures designs. J. Am. Stat. Assoc. 1994, 89, 336–343. [Google Scholar] [CrossRef]

- Brunner, E.; Domhof, S.; Langer, F. Nonparametric Analysis of Longitudinal Data in Factorial Experiments; John Wiley: New York, NY, USA, 2002. [Google Scholar]

- Jarque, C.M.; Bera, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econ. Lett. 1980, 6, 255–259. [Google Scholar] [CrossRef]

- Kwiatkowski, D.; Phillips, P.C.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- D’Agostino, R.B. Transformation to normality of the null distribution of g1. Biometrika 1970, 57, 679–681. [Google Scholar] [CrossRef]

- Korobeynikov, A. Computation- and space-efficient implementation of SSA. Stat. Interface 2010, 3, 257–368. [Google Scholar] [CrossRef] [Green Version]

- Golyandina, N.; Korobeynikov, A. Basic singular spectrum analysis and forecasting with R. Comput. Stat. Data Anal. 2014, 71, 934–954. [Google Scholar] [CrossRef] [Green Version]

- Golyandina, N.; Korobeynikov, A.; Shlemov, A.; Usevich, K. Multivariate and 2D extensions of singular spectrum analysis with the Rssa package. J. Stat. Softw. 2015, 67, 1–78. [Google Scholar] [CrossRef] [Green Version]

- Noguchi, K.; Gel, Y.R.; Brunner, E.; Konietschke, F. nparLD: An R software package for the nonparametric analysis of longitudinal data in factorial experiments. J. Stat. Softw. 2012, 50, 1–23. [Google Scholar] [CrossRef] [Green Version]

| Factor | Levels | |||||

|---|---|---|---|---|---|---|

| Sampling Frequency | Annual | Monthly | Quarterly | Weekly | Daily | Hourly |

| 5 | 83 | 4 | 4 | 2 | 2 | |

| Skewness | Positive Skew | Negative Skew | Symmetric | |||

| 61 | 21 | 18 | ||||

| Normality | Normal | Non-normal | ||||

| 18 | 82 | |||||

| Stationarity | Stationary | Non-Stationary | ||||

| 14 | 86 | |||||

| Model | Factor | P-Value | |||

|---|---|---|---|---|---|

| h = 1 | h = 3 | h = 6 | h = 12 | ||

| RMSFE ∼ Tr + Skew | Skew | 0.0037 | 0.0043 | 0.0056 | 0.0131 |

| + Tr × Skew | Tr | 0.0718 | 0.1447 | 0.4186 | 0.2098 |

| Tr × Skew | 0.4177 | 0.5106 | 0.2120 | 0.1482 | |

| RMSFE ∼ Tr + Stationarity | Stationarity | 0.0997 | 0.053 | 0.0501 | 0.0248 |

| + Tr × Stationarity | Tr | 0.2351 | 0.3754 | 0.7607 | 0.5276 |

| Tr × Stationarity | 0.5160 | 0.6808 | 0.7678 | 0.3792 | |

| RMSFE ∼ Tr + Normality | Normality | 0.5052 | 0.5320 | 0.4954 | 0.5820 |

| + Tr × Normality | Tr | 0.0747 | 0.1152 | 0.5849 | 0.4892 |

| Tr × Normality | 0.2492 | 0.3576 | 0.4042 | 0.4549 | |

| RMSFE ∼ Tr + Freq | Freq | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| + Tr × Freq | Tr | 0.0841 | 0.1194 | 0.1355 | 0.1143 |

| Tr × Freq | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| RMSFE ∼ Tr | Tr | 0.4271 | 0.6740 | 0.9535 | 0.4860 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hassani, H.; Yeganegi, M.R.; Khan, A.; Silva, E.S. The Effect of Data Transformation on Singular Spectrum Analysis for Forecasting. Signals 2020, 1, 4-25. https://doi.org/10.3390/signals1010002

Hassani H, Yeganegi MR, Khan A, Silva ES. The Effect of Data Transformation on Singular Spectrum Analysis for Forecasting. Signals. 2020; 1(1):4-25. https://doi.org/10.3390/signals1010002

Chicago/Turabian StyleHassani, Hossein, Mohammad Reza Yeganegi, Atikur Khan, and Emmanuel Sirimal Silva. 2020. "The Effect of Data Transformation on Singular Spectrum Analysis for Forecasting" Signals 1, no. 1: 4-25. https://doi.org/10.3390/signals1010002