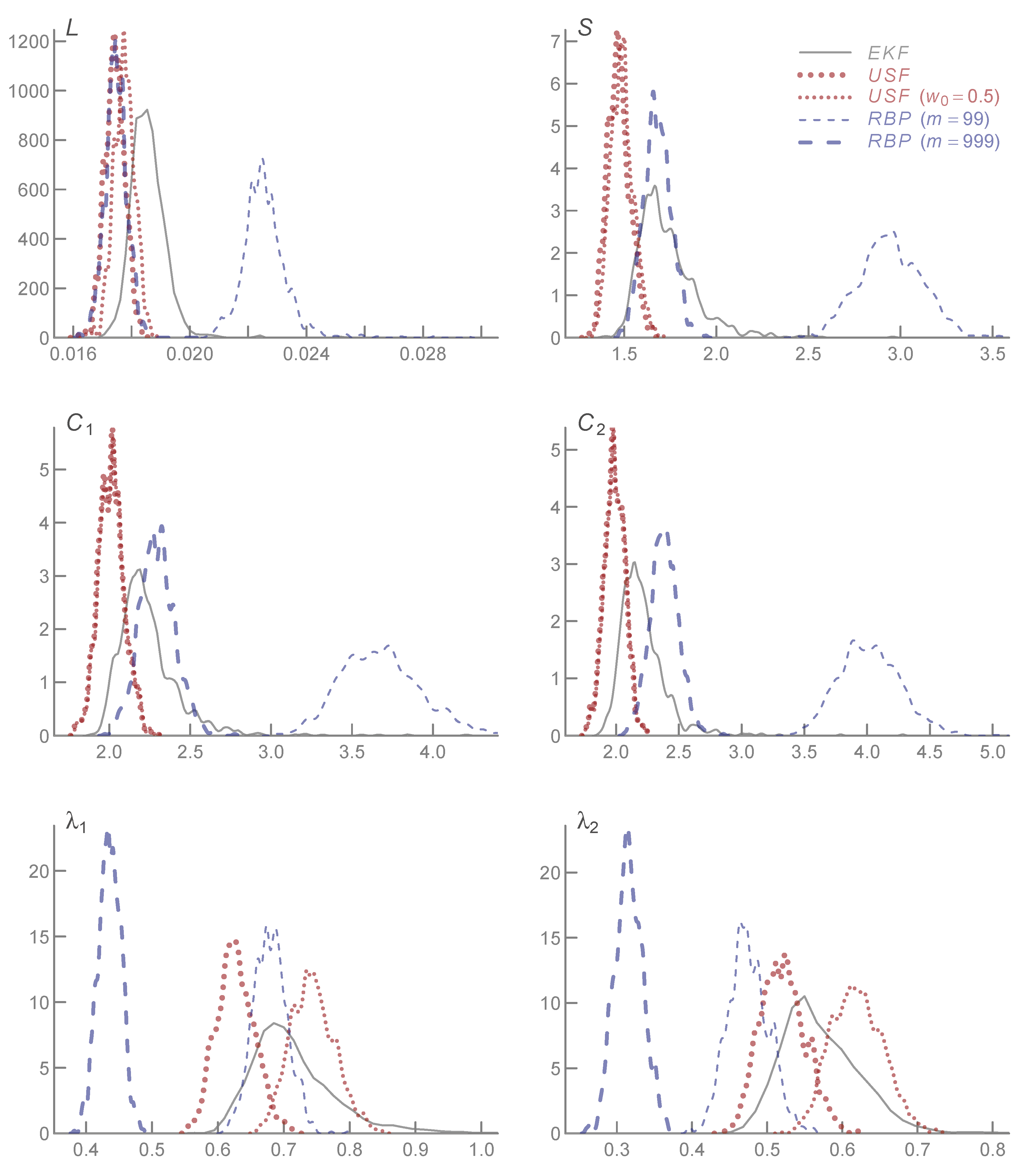

Appendix A.3. Rao-Blackwellized Particle Filter

The material in this section largely taken from Schon et al. [

26] for the reader’s convenience. Write the state space model as

This is model 3 of (18), p. 2282 in Schon et al. [

26] with

,

,

,

,

,

,

.

The conditional distributions for drawing the nonlinear state variables

are (25), p. 2283 in [

26]

and (12), p. 2281 in [

26]

Filtering algorithm p. 2280 in [

26].

- (1)

Initialize. Draw for particles. Set , .

- (2)

Evaluate importance weights . Simulated contribution to log-likelihood is . Normalize .

- (3)

Particle filter measurement update. Resample N particles with replacement .

- (4a)

Kalman filter measurement update (22), p. 2283 in [

26]

- (4b)

Particle filter time update (prediction) .

- (4c)

Kalman filter time update (23), p. 2283 in [

26]

- (5)

Set and go back to step (2).

Table A1.

AR(1) least squares estimates for Nelson-Siegel-Svensson factors from European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. for factors estimated from AAA bonds and for factors estimated from all bonds. is the sample mean, is the AR(1) coefficient of the demeaned factor series (without an intercept), is the standard error of regression and T is the sample size. Standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019.

Table A1.

AR(1) least squares estimates for Nelson-Siegel-Svensson factors from European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. for factors estimated from AAA bonds and for factors estimated from all bonds. is the sample mean, is the AR(1) coefficient of the demeaned factor series (without an intercept), is the standard error of regression and T is the sample size. Standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019.

| | | | | | T |

|---|

| 2.634 | 0.995 | 0.152 | 0.990 | 3701 |

| (0.025) | (0.002) | | | |

| −1.789 | 0.981 | 0.182 | 0.963 | 3701 |

| (0.015) | (0.003) | | | |

| 11.663 | 0.994 | 1.064 | 0.989 | 3701 |

| (0.166) | (0.002) | | | |

| −11.339 | 0.995 | 1.027 | 0.990 | 3701 |

| (0.166) | (0.002) | | | |

| 0.966 | 0.994 | 0.107 | 0.987 | 3701 |

| (0.016) | (0.002) | | | |

| 0.831 | 0.994 | 0.071 | 0.988 | 3701 |

| (0.011) | (0.002) | | | |

| 3.617 | 0.988 | 0.223 | 0.977 | 3701 |

| (0.024) | (0.003) | | | |

| −2.698 | 0.989 | 0.247 | 0.978 | 3701 |

| (0.027) | (0.002) | | | |

| 16.070 | 0.980 | 6.800 | 0.960 | 3701 |

| (0.560) | (0.003) | | | |

| −17.210 | 0.981 | 6.794 | 0.962 | 3701 |

| (0.573) | (0.003) | | | |

| 0.774 | 0.992 | 0.111 | 0.984 | 3701 |

| (0.015) | (0.002) | | | |

| 0.565 | 0.989 | 0.105 | 0.977 | 3701 |

| (0.011) | (0.002) | | | |

Table A2.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (AAA bonds). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 13 yields with maturities (years).

Table A2.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (AAA bonds). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 13 yields with maturities (years).

| | | | | |

|---|

| 0.038 | (0.007) | 0.063 | (0.001) | 0.076 | (0.003) | 0.106 | (0.003) |

| 0.011 | (0.001) | 0.020 | (0.001) | 0.024 | (0.001) | 0.037 | (0.001) |

| 0.002 | (0.000) | 0.004 | (0.001) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.004 | (0.000) | 0.008 | (0.000) | 0.011 | (0.000) | 0.024 | (0.000) |

| 0.002 | (0.000) | 0.004 | (0.000) | 0.007 | (0.000) | 0.022 | (0.000) |

| 0.001 | (0.000) | 0.003 | (0.000) | 0.002 | (0.001) | 0.014 | (0.000) |

| 0.000 | (0.000) | 0.001 | (0.000) | 0.005 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.001 | (0.000) | 0.004 | (0.000) | 0.002 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.003 | (0.000) | 0.005 | (0.000) | 0.005 | (0.000) |

| 0.003 | (0.000) | 0.057 | (0.001) | 0.020 | (0.001) | 0.069 | (0.001) |

| 0.007 | (0.002) | 0.168 | (0.002) | 0.017 | (0.004) | 0.176 | (0.002) |

| 0.018 | (0.005) | 0.305 | (0.004) | 0.069 | (0.008) | 0.303 | (0.003) |

| 0.998 | (0.020) | 0.999 | (0.001) | 1.000 | (0.000) | 0.999 | (0.000) |

| 0.998 | (0.004) | 0.999 | (0.001) | 0.999 | (0.001) | 0.999 | (0.001) |

| 1.000 | (0.000) | 0.994 | (0.002) | 0.998 | (0.001) | 0.995 | (0.002) |

| 0.985 | (0.002) | | | 0.996 | (0.002) | | |

| 1.000 | (0.000) | 0.996 | (0.001) | | | | |

| 1.000 | (0.000) | | | | | | |

| 2.998 | (1.945) | 3.066 | (0.666) | 3.025 | (1.715) | 3.515 | (1.223) |

| 0.917 | (0.390) | −0.760 | (1.658) | −2.115 | (0.668) | −2.648 | (0.728) |

| −3.115 | (0.091) | −4.345 | (0.168) | 3.561 | (1.247) | −3.057 | (0.519) |

| 0.000 | (0.000) | | | −2.679 | (0.813) | | |

| 0.001 | (0.000) | 0.000 | (0.000) | 0.162 | (0.002) | 0.415 | (0.002) |

| 0.001 | (0.000) | | | 0.340 | (0.002) | | |

| 0.061 | (0.006) | 0.049 | (0.001) | 0.040 | (0.002) | 0.056 | (0.001) |

| 0.081 | (0.010) | 0.054 | (0.001) | 0.042 | (0.002) | 0.067 | (0.002) |

| 0.155 | (0.003) | 0.150 | (0.004) | 0.177 | (0.005) | 0.159 | (0.005) |

| 0.282 | (0.022) | | | 0.189 | (0.009) | | |

| 0.029 | (0.002) | 0.033 | (0.002) | | | | |

| 0.035 | (0.003) | | | | | | |

Table A3.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (AAA bonds). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is from 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 9 yields with maturities (years).

Table A3.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (AAA bonds). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is from 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 9 yields with maturities (years).

| | | | | |

|---|

| 0.122 | (0.026) | 0.278 | (0.012) | 0.274 | (0.015) | 0.267 | (0.006) |

| 0.000 | (0.000) | 0.068 | (0.001) | 0.052 | (0.002) | 0.082 | (0.002) |

| 0.003 | (0.001) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.003 | (0.001) | 0.029 | (0.001) | 0.008 | (0.001) | 0.043 | (0.001) |

| 0.000 | (0.000) | 0.020 | (0.001) | 0.002 | (0.001) | 0.030 | (0.001) |

| 0.001 | (0.000) | 0.005 | (0.001) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.001) | 0.004 | (0.001) | 0.005 | (0.000) | 0.007 | (0.001) |

| 0.004 | (0.000) | 0.011 | (0.001) | 0.012 | (0.002) | 0.030 | (0.001) |

| 0.142 | (0.002) | 0.168 | (0.002) | 0.163 | (0.003) | 0.215 | (0.004) |

| 1.000 | (0.000) | 0.999 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) |

| 0.998 | (0.002) | 1.000 | (0.000) | 0.999 | (0.000) | 1.000 | (0.000) |

| 1.000 | (0.001) | 0.997 | (0.001) | 0.997 | (0.002) | 0.996 | (0.001) |

| 0.997 | (0.002) | | | 0.992 | (0.006) | | |

| 0.976 | (0.005) | 0.998 | (0.001) | | | | |

| 0.998 | (0.001) | | | | | | |

| 2.588 | (1.561) | 2.843 | (0.820) | 3.390 | (1.568) | 3.337 | (1.769) |

| −2.808 | (0.848) | −2.410 | (0.099) | −2.739 | (0.702) | −2.632 | (0.812) |

| 3.406 | (2.469) | −2.751 | (0.214) | −3.675 | (0.716) | −2.828 | (0.560) |

| −4.948 | (0.601) | | | 0.910 | (0.328) | | |

| 0.276 | (0.053) | 0.000 | (0.000) | 0.451 | (0.002) | 0.410 | (0.002) |

| 0.000 | (0.000) | | | 0.794 | (0.008) | | |

| 0.042 | (0.001) | 0.024 | (0.001) | 0.040 | (0.001) | 0.033 | (0.001) |

| 0.061 | (0.005) | 0.028 | (0.002) | 0.045 | (0.002) | 0.041 | (0.001) |

| 0.103 | (0.006) | 0.119 | (0.003) | 0.156 | (0.005) | 0.134 | (0.003) |

| 0.144 | (0.006) | | | 0.170 | (0.007) | | |

| 0.037 | (0.003) | 0.025 | (0.001) | | | | |

| 0.021 | (0.001) | | | | | | |

Table A4.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (all ratings). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 13 yields with maturities (years).

Table A4.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (all ratings). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 13 yields with maturities (years).

| | | | | |

|---|

| 0.004 | (0.001) | 0.245 | (0.011) | 0.116 | (0.003) | 0.126 | (0.003) |

| 0.000 | (0.000) | 0.100 | (0.006) | 0.037 | (0.001) | 0.044 | (0.001) |

| 0.001 | (0.000) | 0.038 | (0.002) | 0.014 | (0.001) | 0.018 | (0.002) |

| 0.000 | (0.000) | 0.009 | (0.001) | 0.028 | (0.001) | 0.041 | (0.001) |

| 0.000 | (0.000) | 0.004 | (0.000) | 0.025 | (0.000) | 0.039 | (0.001) |

| 0.000 | (0.000) | 0.003 | (0.000) | 0.014 | (0.000) | 0.025 | (0.000) |

| 0.000 | (0.000) | 0.001 | (0.000) | 0.000 | (0.000) | 0.003 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.001 | (0.000) | 0.002 | (0.000) |

| 0.001 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.002 | (0.000) | 0.001 | (0.000) | 0.002 | (0.000) | 0.005 | (0.000) |

| 0.026 | (0.001) | 0.031 | (0.001) | 0.006 | (0.001) | 0.054 | (0.001) |

| 0.089 | (0.002) | 0.099 | (0.002) | 0.046 | (0.001) | 0.121 | (0.002) |

| 0.178 | (0.004) | 0.192 | (0.004) | 0.117 | (0.002) | 0.206 | (0.004) |

| 0.998 | (0.001) | 0.998 | (0.001) | 0.999 | (0.001) | 0.999 | (0.001) |

| 1.000 | (0.001) | 0.998 | (0.004) | 0.998 | (0.001) | 0.998 | (0.001) |

| 0.999 | (0.000) | 0.993 | (0.005) | 0.996 | (0.002) | 0.993 | (0.002) |

| 0.997 | (0.001) | | | 0.993 | (0.002) | | |

| 0.817 | (0.022) | 0.991 | (0.002) | | | | |

| 0.989 | (0.003) | | | | | | |

| 3.960 | (0.400) | 3.628 | (0.499) | 4.154 | (0.611) | 4.023 | (0.946) |

| −6.188 | (3.230) | −0.427 | (1.488) | −2.951 | (0.499) | −2.851 | (0.638) |

| 32.304 | (8.643) | −5.720 | (0.976) | 1.422 | (0.853) | −3.293 | (0.441) |

| −13.254 | (1.995) | | | −2.715 | (0.685) | | |

| 0.118 | (0.019) | 0.000 | (0.000) | 0.241 | (0.005) | 0.451 | (0.002) |

| 0.000 | (0.000) | | | 0.417 | (0.003) | | |

| 0.060 | (0.002) | 0.064 | (0.002) | 0.059 | (0.002) | 0.054 | (0.001) |

| 0.105 | (0.006) | 0.084 | (0.003) | 0.072 | (0.003) | 0.085 | (0.003) |

| 0.230 | (0.012) | 0.202 | (0.008) | 0.217 | (0.008) | 0.186 | (0.007) |

| 0.155 | (0.008) | | | 0.290 | (0.009) | | |

| 0.059 | (0.006) | 0.041 | (0.002) | | | | |

| 0.053 | (0.003) | | | | | | |

Table A5.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (all ratings). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 9 yields with maturities (years).

Table A5.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the European Central Bank (all ratings). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations). The measurement consists of 9 yields with maturities (years).

| | | | | |

|---|

| 0.061 | (0.013) | 0.528 | (0.009) | 0.243 | (0.007) | 0.496 | (0.009) |

| 0.006 | (0.001) | 0.161 | (0.003) | 0.000 | (0.000) | 0.151 | (0.003) |

| 0.004 | (0.000) | 0.000 | (0.000) | 0.039 | (0.001) | 0.011 | (0.002) |

| 0.002 | (0.000) | 0.049 | (0.001) | 0.014 | (0.001) | 0.056 | (0.001) |

| 0.001 | (0.000) | 0.033 | (0.001) | 0.022 | (0.001) | 0.042 | (0.001) |

| 0.001 | (0.000) | 0.022 | (0.000) | 0.001 | (0.003) | 0.009 | (0.001) |

| 0.001 | (0.000) | 0.006 | (0.001) | 0.016 | (0.000) | 0.020 | (0.000) |

| 0.004 | (0.000) | 0.031 | (0.001) | 0.016 | (0.001) | 0.014 | (0.001) |

| 0.102 | (0.002) | 0.025 | (0.002) | 0.129 | (0.002) | 0.154 | (0.002) |

| 0.998 | (0.001) | 1.000 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) |

| 0.998 | (0.001) | 0.999 | (0.001) | 0.999 | (0.000) | 0.999 | (0.000) |

| 0.990 | (0.002) | 0.997 | (0.001) | 0.996 | (0.001) | 0.996 | (0.001) |

| 1.000 | (0.000) | | | 0.989 | (0.006) | | |

| 0.996 | (0.001) | 1.000 | (0.000) | | | | |

| 0.931 | (0.015) | | | | | | |

| 4.214 | (0.480) | 4.191 | (0.776) | 3.760 | (1.348) | 3.871 | (1.325) |

| −3.486 | (0.116) | −2.776 | (0.105) | −3.152 | (0.637) | −3.042 | (0.698) |

| −4.892 | (0.543) | −3.219 | (0.167) | −3.552 | (0.558) | −2.714 | (0.567) |

| 5.434 | (3.799) | | | 1.425 | (0.263) | | |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.496 | (0.003) | 0.409 | (0.002) |

| 0.278 | (0.002) | | | 1.227 | (0.016) | | |

| 0.054 | (0.002) | 0.033 | (0.001) | 0.035 | (0.001) | 0.035 | (0.001) |

| 0.076 | (0.005) | 0.048 | (0.002) | 0.039 | (0.001) | 0.054 | (0.002) |

| 0.194 | (0.011) | 0.107 | (0.003) | 0.162 | (0.004) | 0.136 | (0.004) |

| 0.144 | (0.014) | | | 0.171 | (0.008) | | |

| 0.037 | (0.002) | 0.027 | (0.001) | | | | |

| 0.055 | (0.008) | | | | | | |

Table A6.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the Bank of Canada. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 4 January 2000 to 31 December 2018 (4,719 observations). The measurement consists of 16 yields with maturities (years).

Table A6.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the Bank of Canada. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 4 January 2000 to 31 December 2018 (4,719 observations). The measurement consists of 16 yields with maturities (years).

| | | | | |

|---|

| 0.000 | (0.000) | 0.001 | (0.000) | 0.001 | (0.000) | 0.002 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.001 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.001 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.001 | (0.000) | 0.001 | (0.000) | 0.002 | (0.000) | 0.002 | (0.000) |

| 0.002 | (0.000) | 0.001 | (0.000) | 0.002 | (0.000) | 0.002 | (0.000) |

| 0.004 | (0.000) | 0.004 | (0.000) | 0.004 | (0.000) | 0.003 | (0.000) |

| 1.000 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) |

| 1.000 | (0.000) | 1.000 | (0.000) | 0.999 | (0.001) | 0.999 | (0.000) |

| 1.000 | (0.000) | 0.988 | (0.001) | 0.996 | (0.002) | 0.998 | (0.001) |

| 0.999 | (0.000) | | | 0.999 | (0.001) | | |

| 0.959 | (0.004) | 0.994 | (0.001) | | | | |

| 0.996 | (0.002) | | | | | | |

| 0.125 | (0.302) | 0.053 | (0.012) | 0.043 | (0.013) | 0.042 | (0.012) |

| 0.429 | (0.015) | 0.062 | (0.021) | −0.020 | (0.006) | −0.017 | (0.007) |

| −0.083 | (0.023) | −0.028 | (0.002) | −0.010 | (0.005) | −0.011 | (0.009) |

| −0.093 | (0.017) | | | −0.025 | (0.012) | | |

| 0.632 | (0.000) | 0.000 | (0.000) | 1.466 | (0.009) | 0.419 | (0.003) |

| 0.001 | (0.013) | | | 0.514 | (0.003) | | |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.001 | (0.000) | 0.000 | (0.000) | 0.001 | (0.000) | 0.001 | (0.000) |

| 0.001 | (0.000) | 0.001 | (0.000) | 0.001 | (0.000) | 0.001 | (0.000) |

| 0.001 | (0.000) | | | 0.001 | (0.000) | | |

| 0.021 | (0.002) | 0.029 | (0.001) | | | | |

| 0.027 | (0.001) | | | | | | |

Table A7.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the Bank of England. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 4 January 2000 to 31 December 2018 (4,801 observations). The measurement consists of 13 yields with maturities (years).

Table A7.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the Bank of England. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 4 January 2000 to 31 December 2018 (4,801 observations). The measurement consists of 13 yields with maturities (years).

| | | | | |

|---|

| 0.081 | (0.003) | 0.079 | (0.001) | 0.095 | (0.001) | 0.114 | (0.002) |

| 0.020 | (0.001) | 0.030 | (0.001) | 0.023 | (0.000) | 0.040 | (0.001) |

| 0.003 | (0.002) | 0.000 | (0.000) | 0.000 | (0.000) | 0.000 | (0.000) |

| 0.004 | (0.001) | 0.027 | (0.001) | 0.008 | (0.000) | 0.031 | (0.001) |

| 0.002 | (0.000) | 0.027 | (0.001) | 0.003 | (0.000) | 0.031 | (0.001) |

| 0.002 | (0.000) | 0.017 | (0.001) | 0.006 | (0.000) | 0.020 | (0.001) |

| 0.001 | (0.000) | 0.001 | (0.000) | 0.005 | (0.000) | 0.000 | (0.000) |

| 0.001 | (0.000) | 0.002 | (0.000) | 0.000 | (0.000) | 0.003 | (0.000) |

| 0.000 | (0.000) | 0.000 | (0.000) | 0.007 | (0.000) | 0.000 | (0.000) |

| 0.002 | (0.000) | 0.005 | (0.000) | 0.014 | (0.000) | 0.007 | (0.000) |

| 0.021 | (0.001) | 0.058 | (0.001) | 0.034 | (0.001) | 0.088 | (0.001) |

| 0.023 | (0.004) | 0.130 | (0.002) | 0.015 | (0.002) | 0.187 | (0.002) |

| 0.059 | (0.002) | 0.218 | (0.002) | 0.087 | (0.001) | 0.283 | (0.003) |

| 1.000 | (0.001) | 0.996 | (0.001) | 0.998 | (0.002) | 0.999 | (0.001) |

| 0.999 | (0.001) | 0.997 | (0.001) | 1.000 | (0.000) | 0.999 | (0.000) |

| 1.000 | (0.000) | 0.999 | (0.000) | 0.997 | (0.001) | 0.999 | (0.001) |

| 1.000 | (0.000) | | | 0.998 | (0.001) | | |

| 0.973 | (0.012) | 0.998 | (0.000) | | | | |

| 0.998 | (0.001) | | | | | | |

| 4.255 | (149.500) | 4.417 | (0.174) | 3.453 | (0.486) | 4.016 | (0.450) |

| 7.922 | (5.027) | −2.280 | (0.134) | 0.394 | (4.183) | −0.962 | (1.868) |

| −39.922 | (3.827) | 4.444 | (0.677) | 2.355 | (1.028) | −0.507 | (2.401) |

| 10.262 | (1.698) | | | 0.525 | (1.207) | | |

| 0.037 | (0.005) | 0.000 | (0.000) | 0.137 | (0.001) | 0.396 | (0.002) |

| 0.001 | (0.006) | | | 2.333 | (0.009) | | |

| 0.056 | (0.003) | 0.054 | (0.001) | 0.060 | (0.003) | 0.059 | (0.001) |

| 0.056 | (0.003) | 0.067 | (0.002) | 0.075 | (0.002) | 0.077 | (0.002) |

| 0.164 | (0.021) | 0.123 | (0.003) | 0.216 | (0.008) | 0.120 | (0.003) |

| 0.219 | (0.022) | | | 0.176 | (0.006) | | |

| 0.029 | (0.013) | 0.025 | (0.001) | | | | |

| 0.016 | (0.001) | | | | | | |

Table A8.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the U.S. Department of Treasury. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 31 July 2001 to 31 December 2018 (4,357 observations). The measurement consists of 9 yields with maturities (years).

Table A8.

Maximum likelihood estimates of four dynamic Nelson-Siegel-Svensson type specifications for zero yield curve data from the U.S. Department of Treasury. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The likelihood functions were evaluated using the extended Kalman filter. are the estimated measurement equation innovation variances (assumed to be diagonal), are the estimated AR(1) parameters of the state series, are the estimated unconditional mean of the state series, are the estimated standard deviations of the state equation innovations. QML standard errors in parentheses. The daily sample is 31 July 2001 to 31 December 2018 (4,357 observations). The measurement consists of 9 yields with maturities (years).

| | | | | |

|---|

| 0.001 | (0.000) | 0.240 | (0.005) | 0.241 | (0.005) | 0.251 | (0.005) |

| 0.054 | (0.001) | 0.000 | (0.000) | 0.000 | (0.000) | 0.007 | (0.005) |

| 0.014 | (0.002) | 0.044 | (0.001) | 0.055 | (0.001) | 0.064 | (0.001) |

| 0.029 | (0.001) | 0.048 | (0.003) | 0.045 | (0.001) | 0.056 | (0.001) |

| 0.015 | (0.001) | 0.035 | (0.003) | 0.020 | (0.002) | 0.000 | (0.000) |

| 0.038 | (0.001) | 0.030 | (0.001) | 0.040 | (0.001) | 0.071 | (0.001) |

| 0.001 | (0.003) | 0.042 | (0.001) | 0.000 | (0.000) | 0.076 | (0.002) |

| 0.077 | (0.001) | 0.083 | (0.003) | 0.091 | (0.002) | 0.036 | (0.008) |

| 0.014 | (0.002) | 0.045 | (0.014) | 0.023 | (0.004) | 0.159 | (0.002) |

| 1.000 | (0.000) | 0.999 | (0.000) | 1.000 | (0.000) | 0.999 | (0.000) |

| 1.000 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) | 1.000 | (0.000) |

| 0.995 | (0.001) | 0.996 | (0.001) | 0.998 | (0.001) | 0.994 | (0.001) |

| 0.999 | (0.001) | | | 0.994 | (0.002) | | |

| 0.995 | (0.001) | 0.998 | (0.001) | | | | |

| 0.998 | (0.001) | | | | | | |

| 9.630 | (5.932) | 4.492 | (0.765) | 4.524 | (0.957) | 4.433 | (0.934) |

| 0.688 | (0.549) | −2.343 | (0.181) | −2.315 | (0.795) | −2.233 | (0.860) |

| −0.814 | (0.483) | −3.273 | (0.225) | −2.456 | (0.804) | −2.475 | (0.511) |

| −5.540 | (0.391) | | | −0.051 | (0.502) | | |

| 0.805 | (0.079) | 0.000 | (0.000) | 0.512 | (0.006) | 0.506 | (0.003) |

| 0.000 | (0.000) | | | 0.218 | (0.013) | | |

| 0.073 | (0.014) | 0.037 | (0.003) | 0.039 | (0.004) | 0.042 | (0.002) |

| 0.096 | (0.007) | 0.041 | (0.003) | 0.045 | (0.003) | 0.050 | (0.002) |

| 0.107 | (0.005) | 0.136 | (0.013) | 0.150 | (0.005) | 0.213 | (0.013) |

| 0.142 | (0.008) | | | 0.227 | (0.023) | | |

| 0.022 | (0.001) | 0.038 | (0.003) | | | | |

| 0.023 | (0.001) | | | | | | |

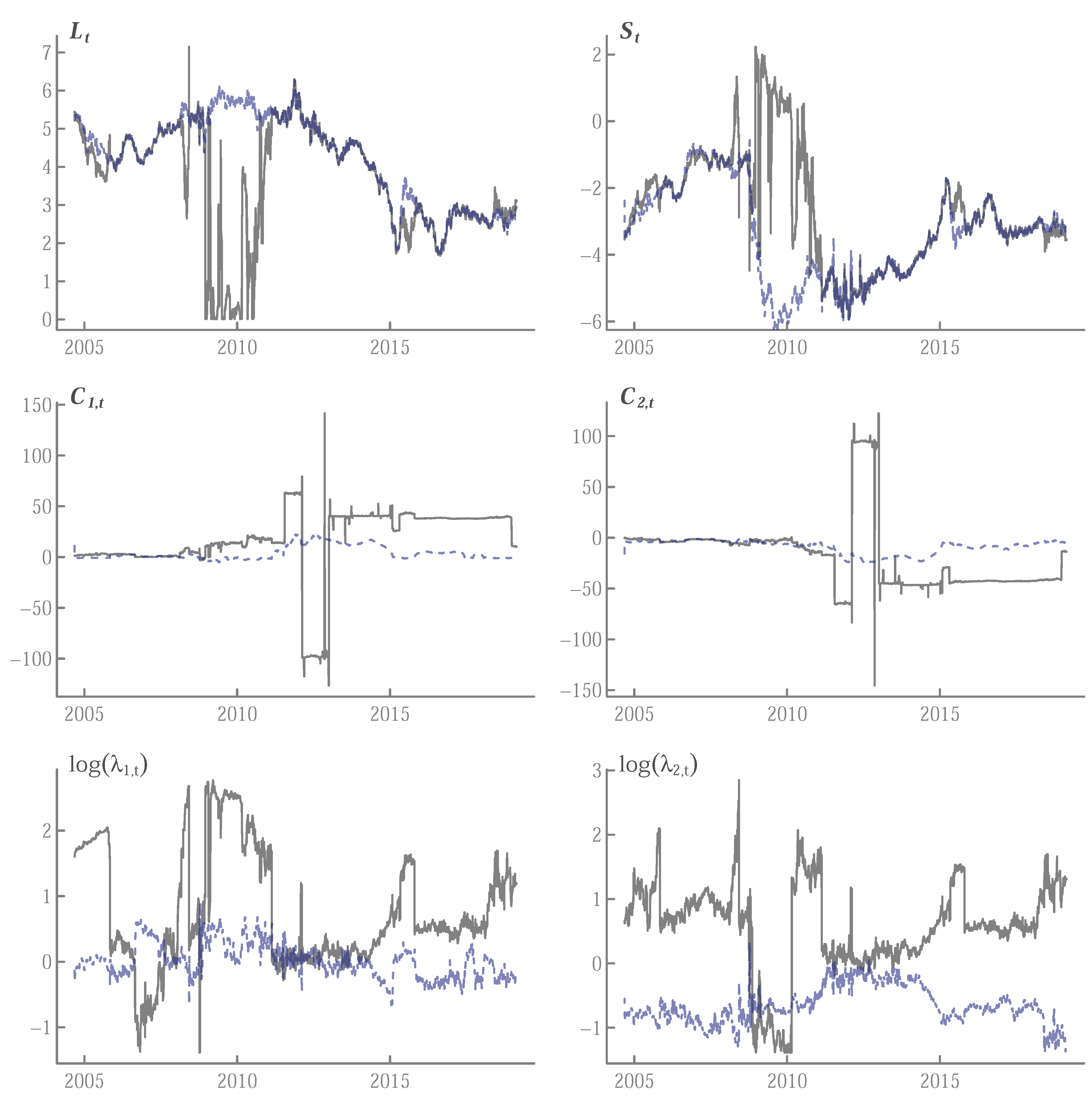

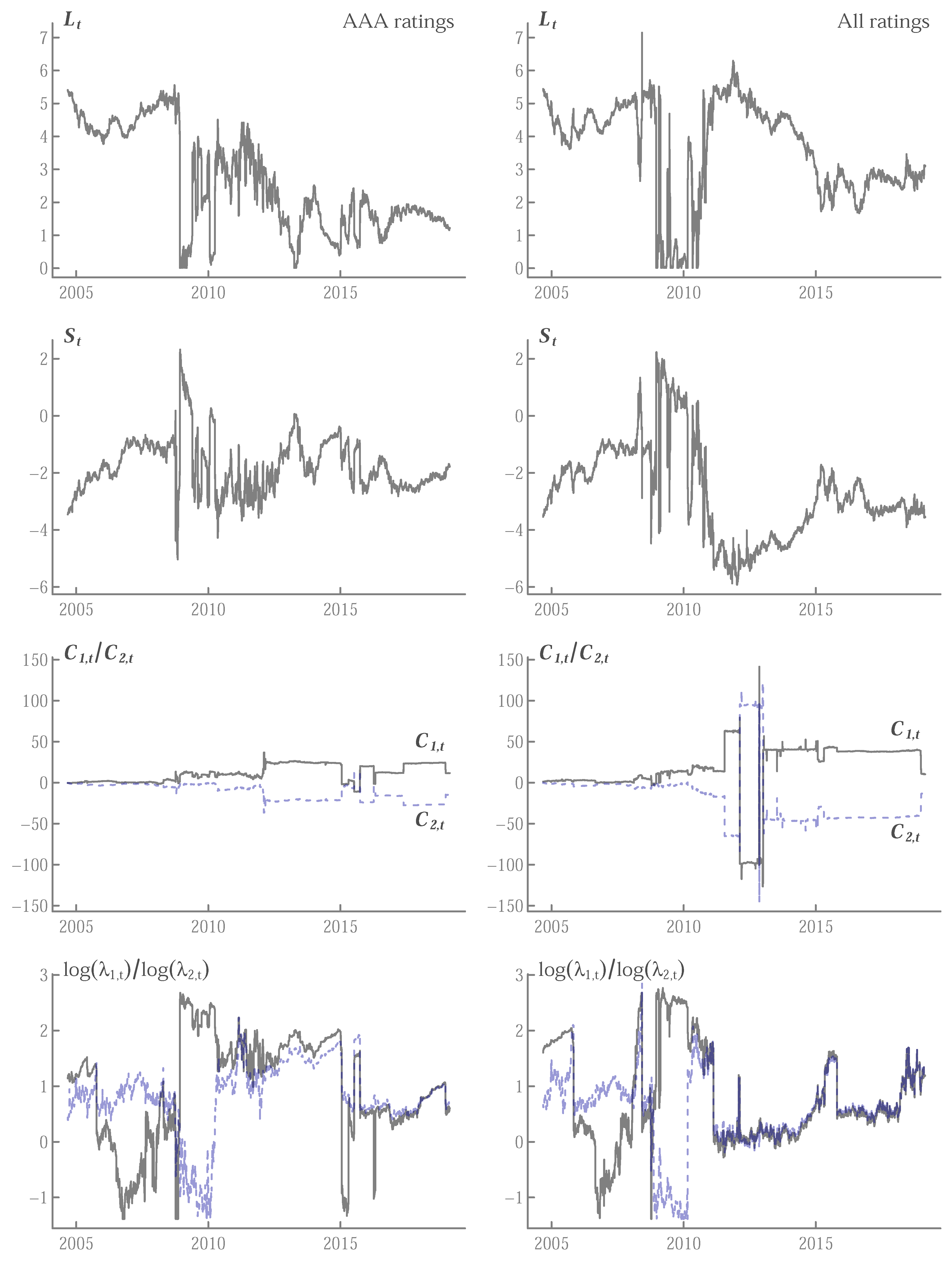

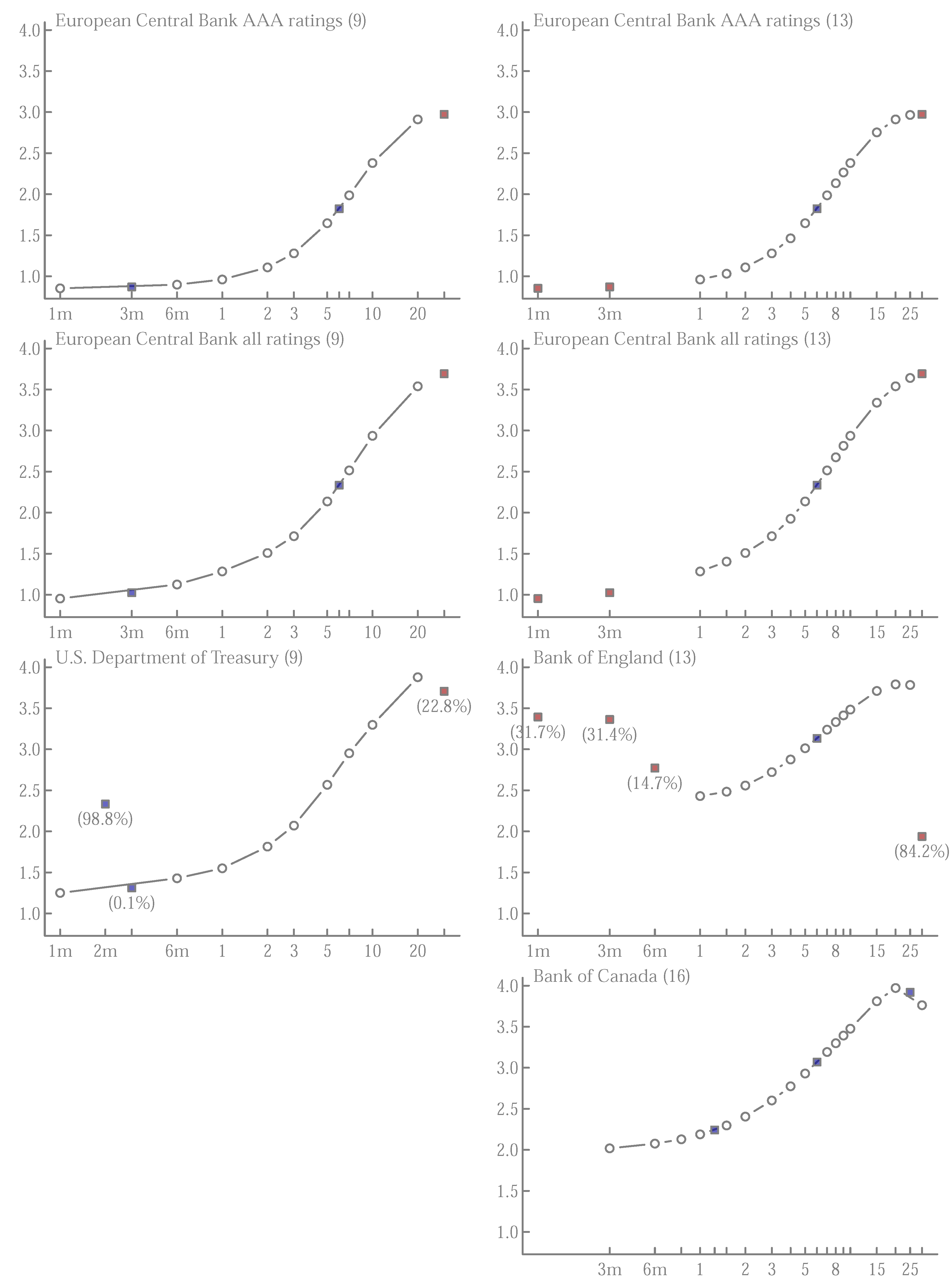

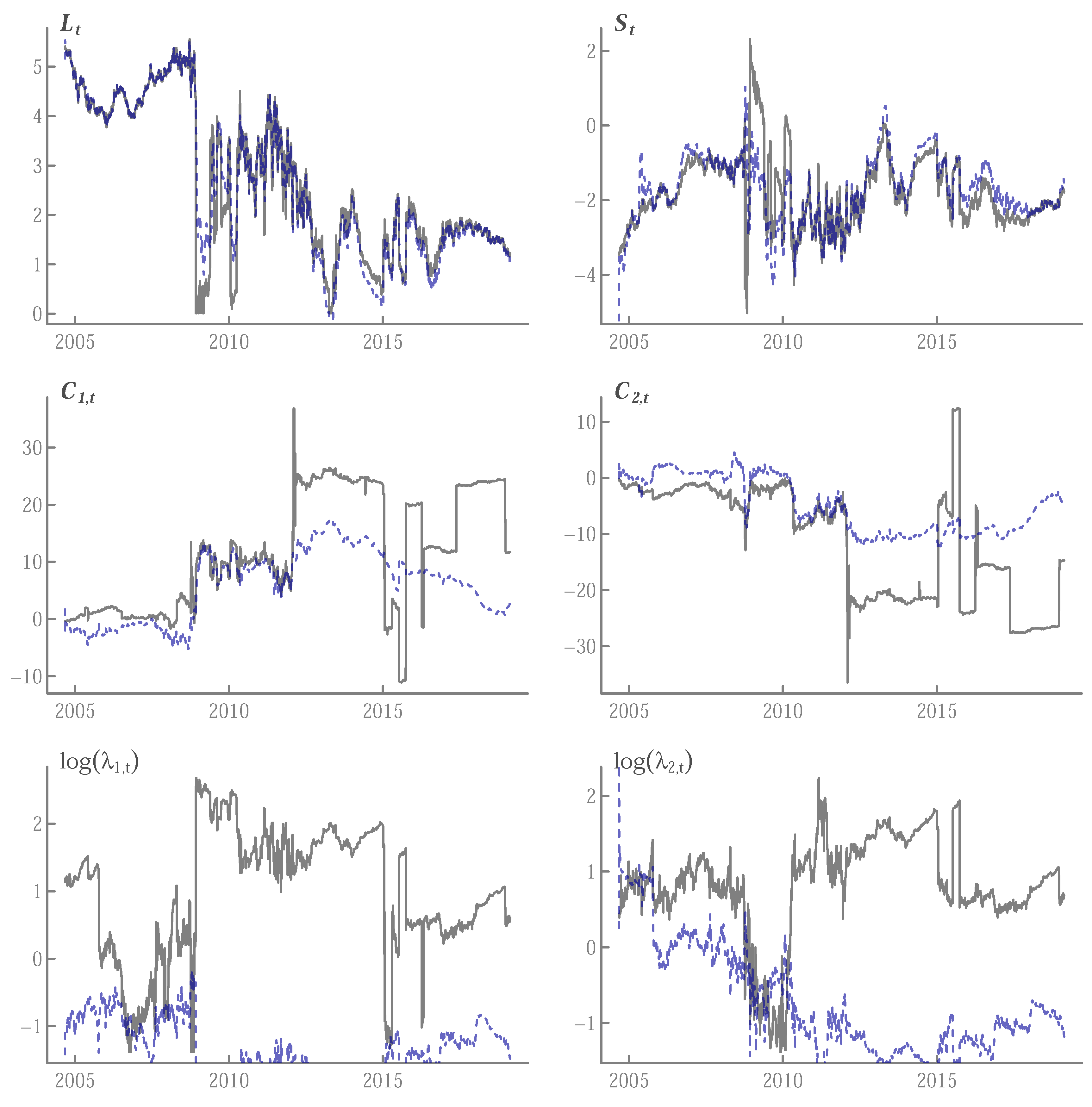

Figure A1.

Nelson-Siegel-Svensson factors (all ratings) from the European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. The gray solid lines are the actual factors and the blue dashed lines are filtered estimates from the extended Kalman filter. The parameters of the state space model were estimated using 13 zero yield curves with maturities (years). The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A1.

Nelson-Siegel-Svensson factors (all ratings) from the European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. The gray solid lines are the actual factors and the blue dashed lines are filtered estimates from the extended Kalman filter. The parameters of the state space model were estimated using 13 zero yield curves with maturities (years). The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

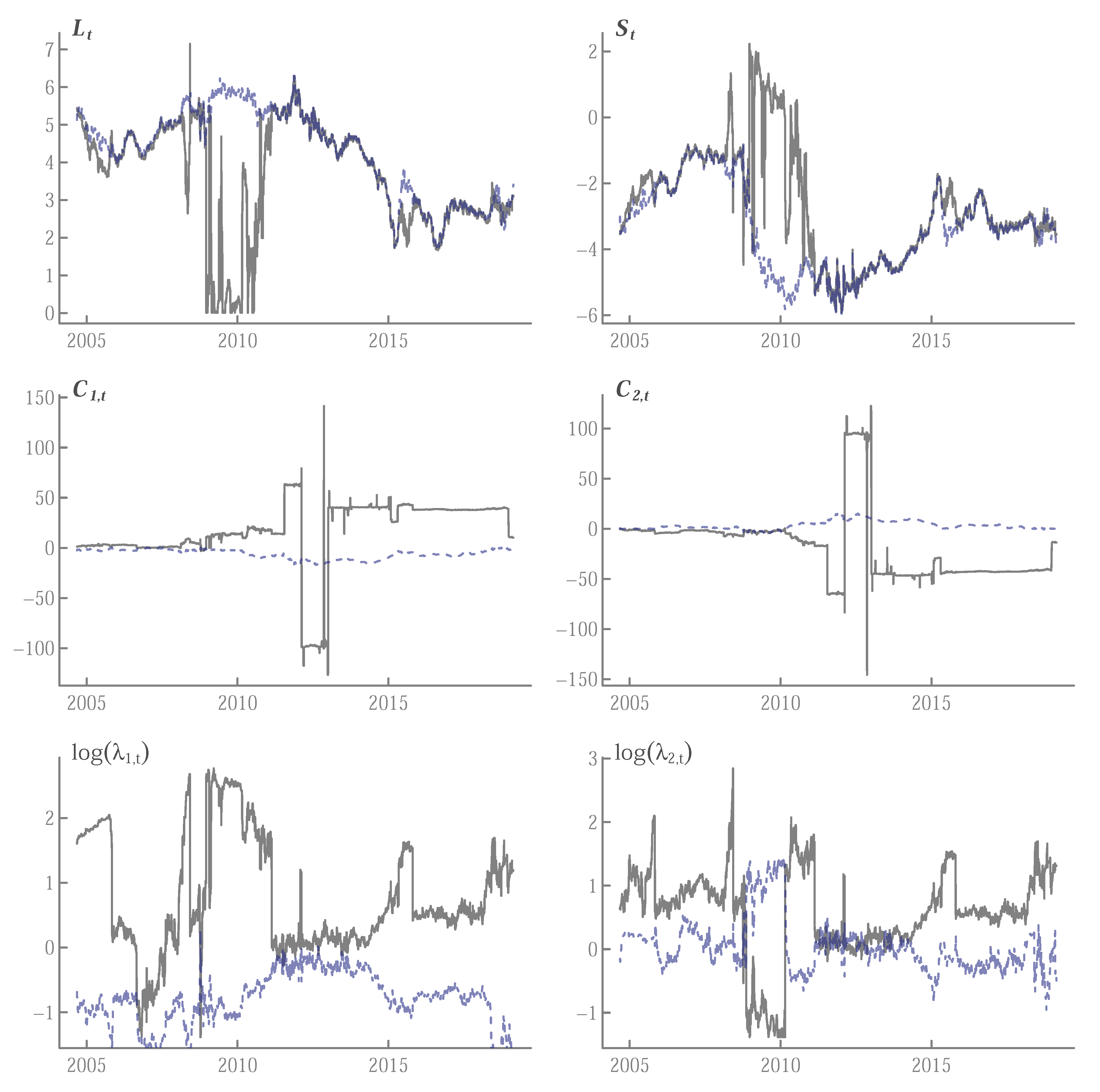

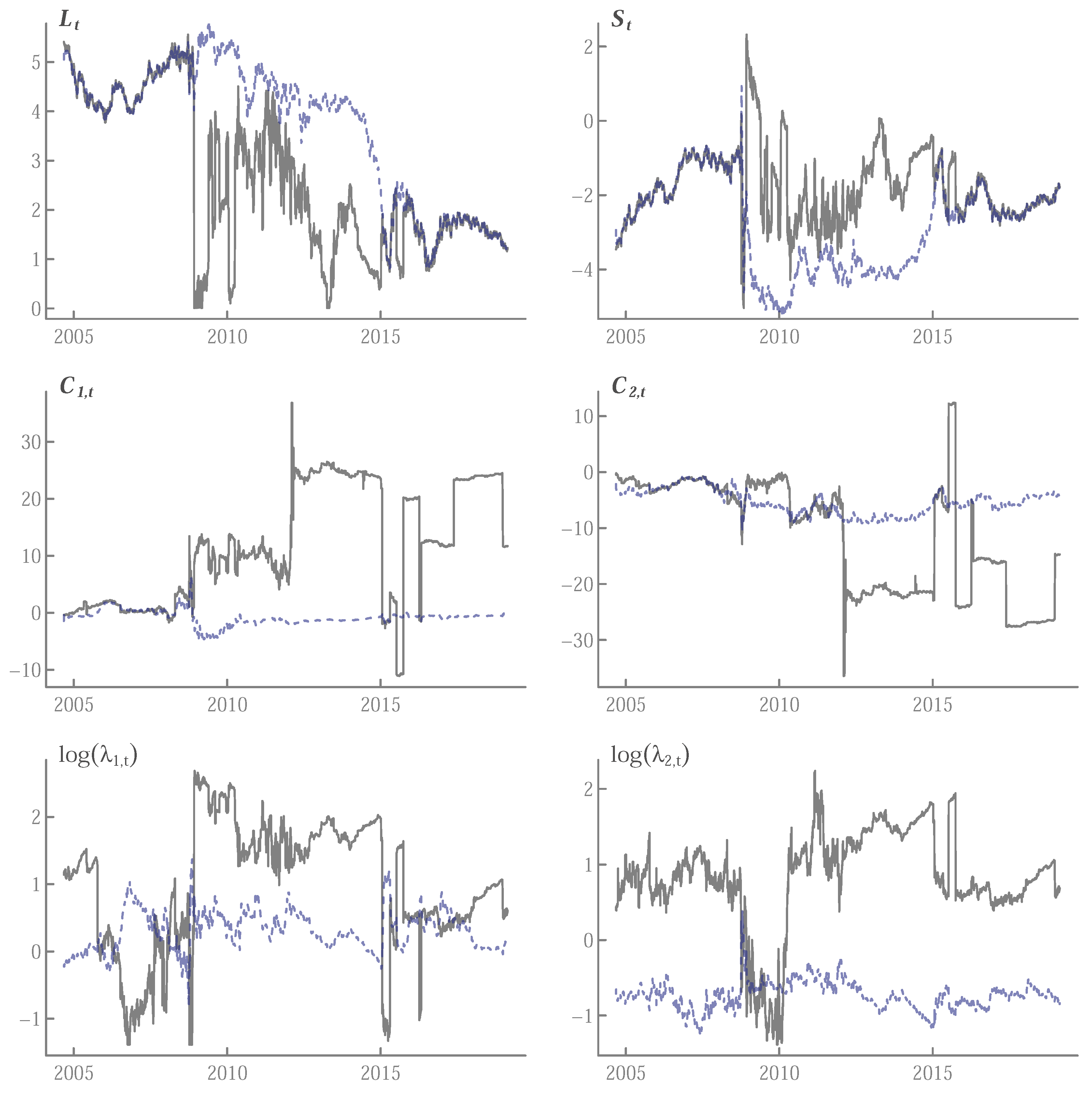

Figure A2.

Nelson-Siegel-Svensson factors (all ratings) from the European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. The gray solid lines are the actual factors and the blue dashed lines are filtered estimates from the extended Kalman filter. The parameters of the state space model were estimated using 9 zero yield curves with maturities (years). The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A2.

Nelson-Siegel-Svensson factors (all ratings) from the European Central Bank. is the level, the slope, , curvature factors with decay parameters , , respectively. The gray solid lines are the actual factors and the blue dashed lines are filtered estimates from the extended Kalman filter. The parameters of the state space model were estimated using 9 zero yield curves with maturities (years). The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

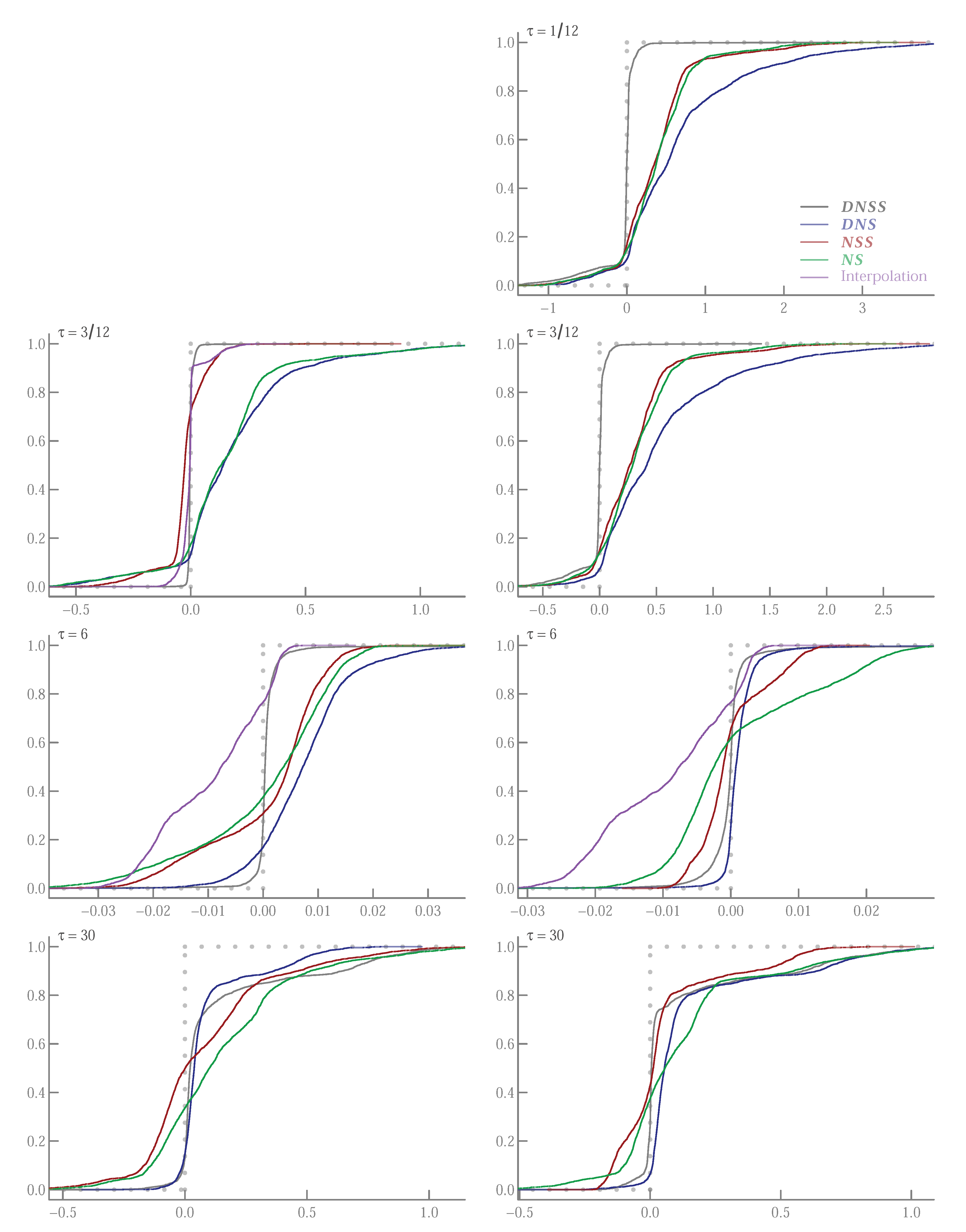

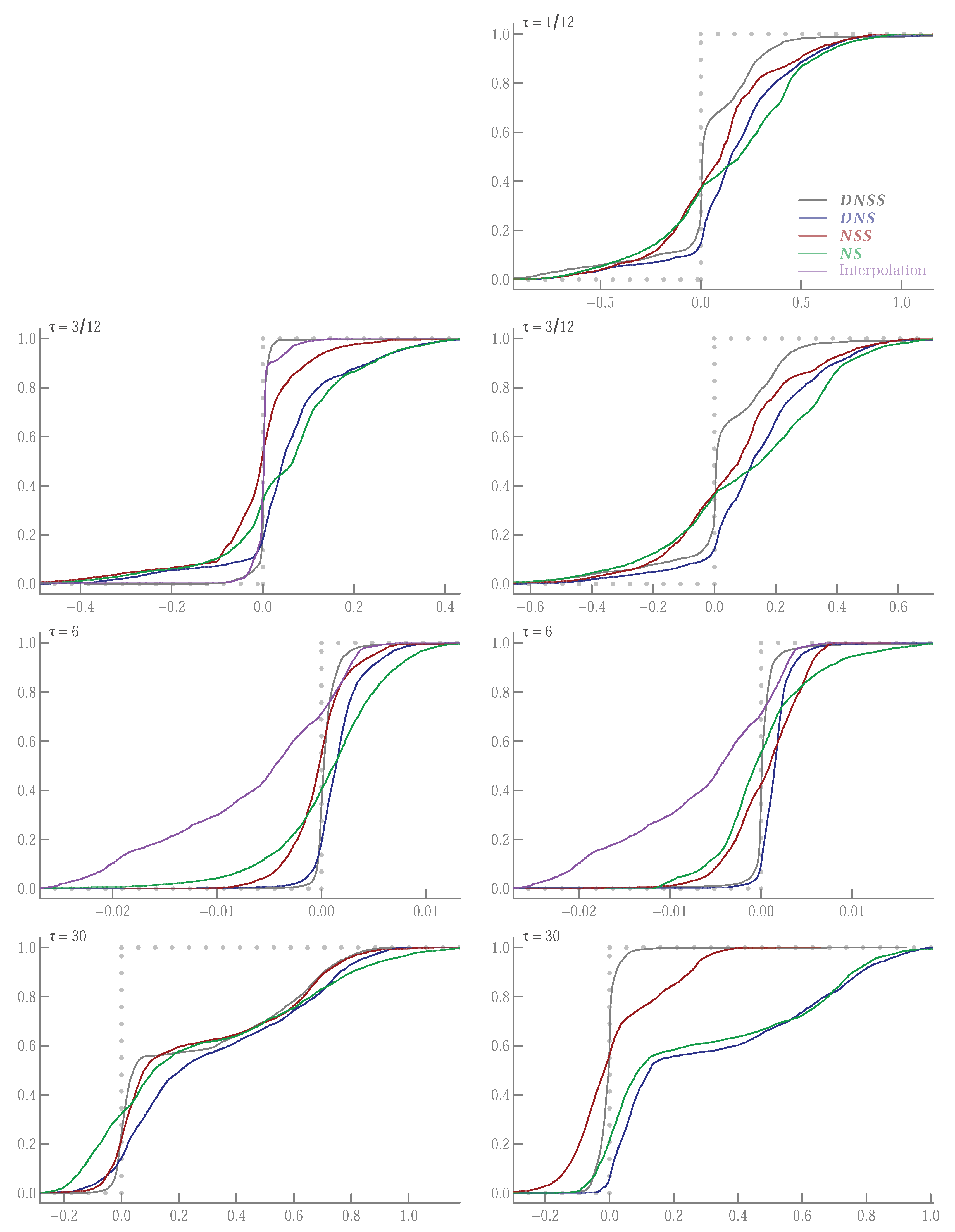

Figure A3.

Empirical cdf of prediction errors. Predictions from European Central Bank (all ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The distribution of a perfect prediction with no error would be a vertical line at indicated as a dotted line. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A3.

Empirical cdf of prediction errors. Predictions from European Central Bank (all ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The distribution of a perfect prediction with no error would be a vertical line at indicated as a dotted line. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

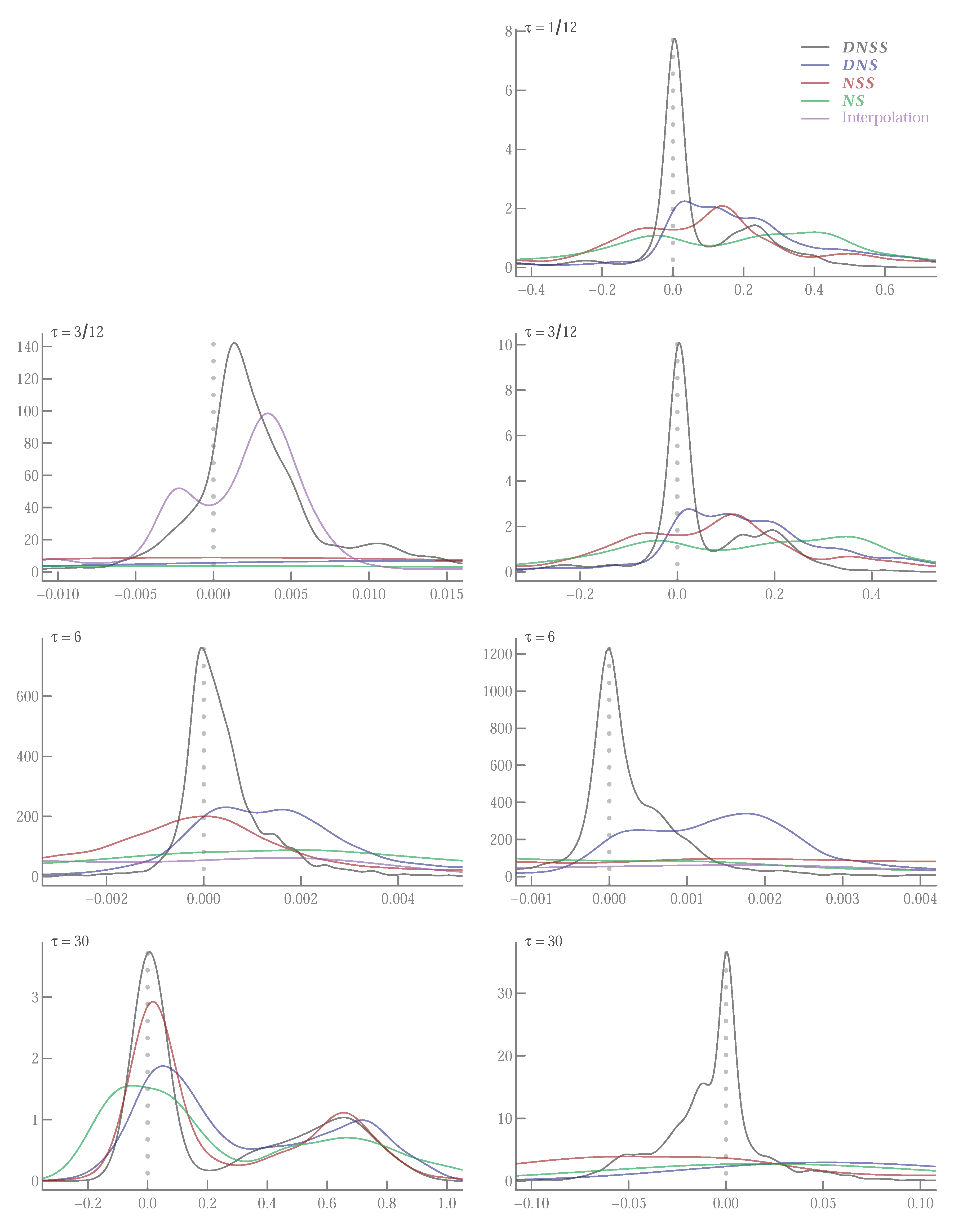

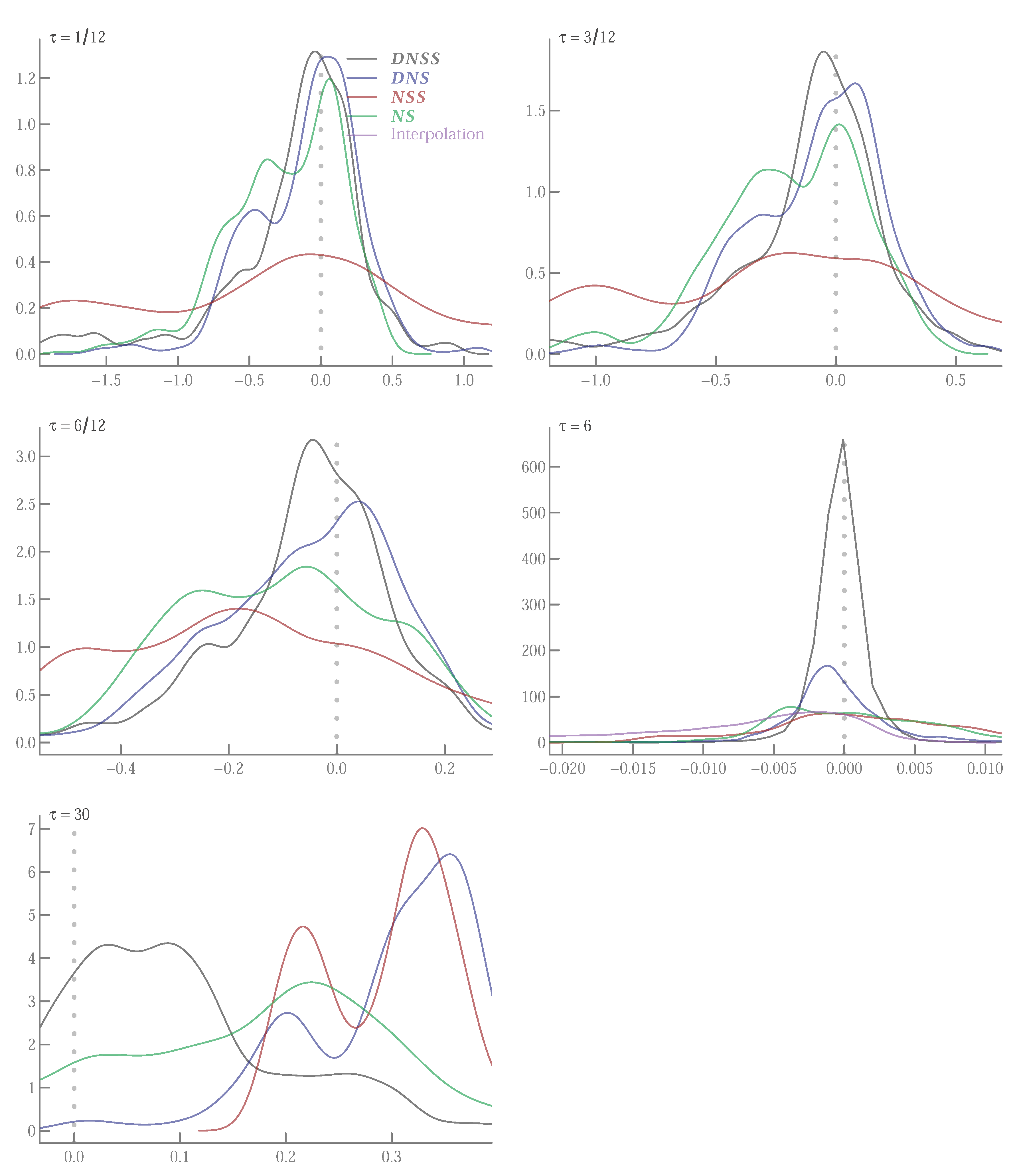

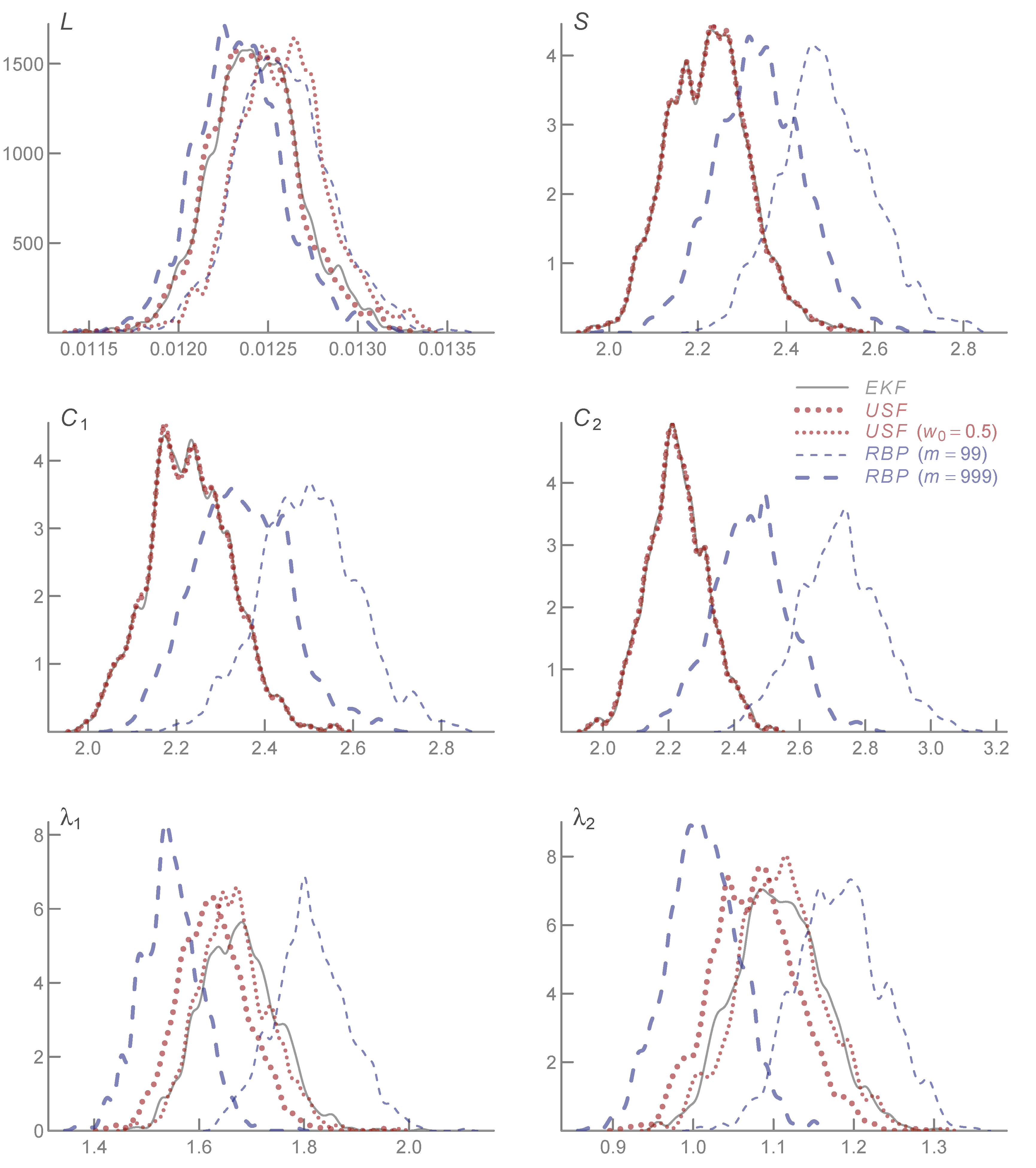

Figure A4.

Kernel density estimates of prediction error distributions. Predictions from European Central Bank (AAA ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A4.

Kernel density estimates of prediction error distributions. Predictions from European Central Bank (AAA ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

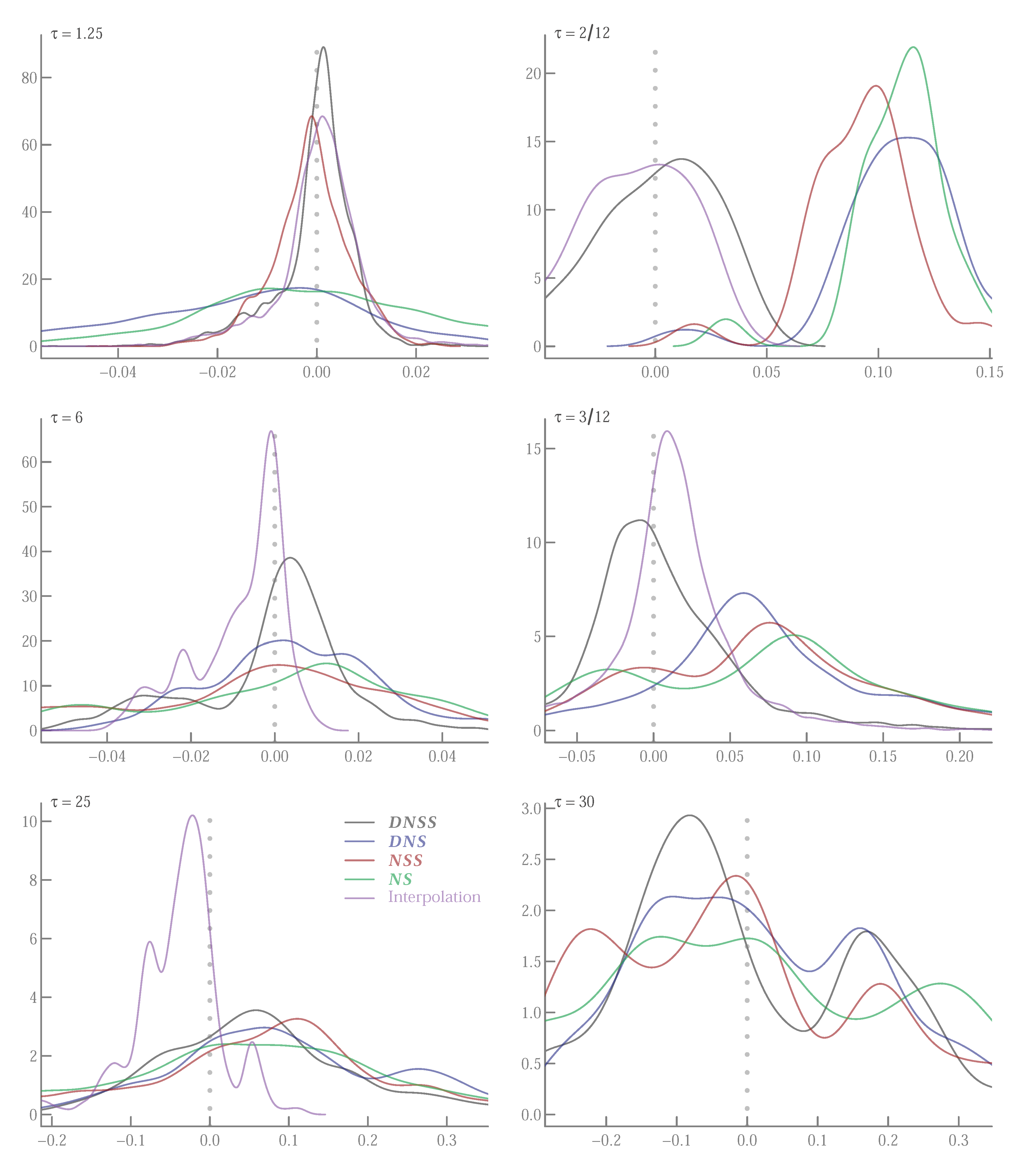

Figure A5.

Kernel density estimates of prediction error distributions. Predictions from European Central Bank (all ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A5.

Kernel density estimates of prediction error distributions. Predictions from European Central Bank (all ratings) estimates with maturities (left panel) and (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 6 September 2004 to 21 February 2019 (3701 observations).

Figure A6.

Kernel density estimates of prediction error distributions. Predictions from Bank of England data with maturities . is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4801 observations some of which may be missing).

Figure A6.

Kernel density estimates of prediction error distributions. Predictions from Bank of England data with maturities . is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4801 observations some of which may be missing).

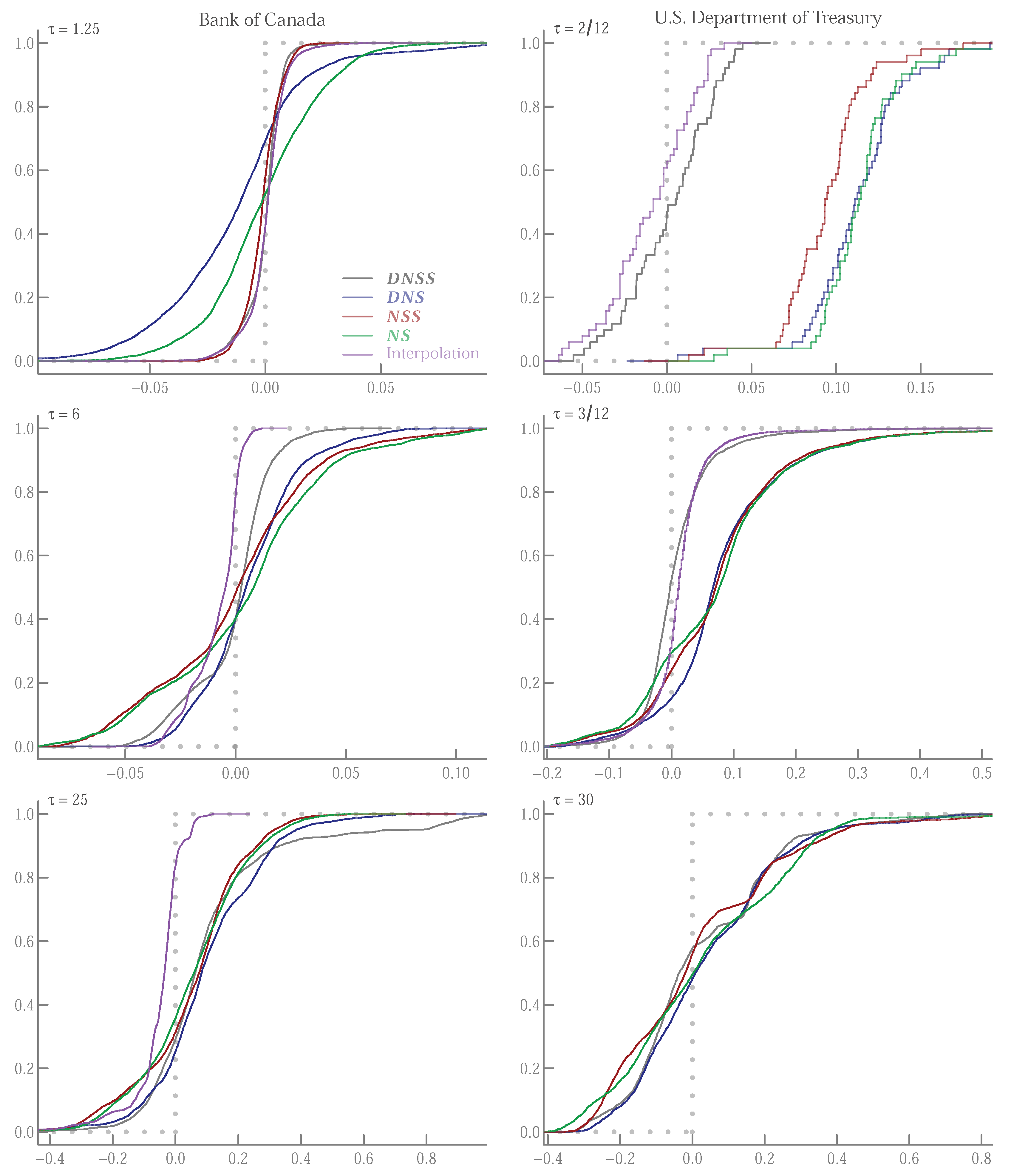

Figure A7.

Kernel density estimates of prediction error distributions. Predictions from Bank of Canada yield data with maturities (left panel) and U.S. Department of Treasury with maturities (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4719 observations) for Bank of Canada (left panel) and 31 July 2001 to 31 December 2018 (4357 observations some of which may be missing) for U.S. Department of Treasury (right panel).

Figure A7.

Kernel density estimates of prediction error distributions. Predictions from Bank of Canada yield data with maturities (left panel) and U.S. Department of Treasury with maturities (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4719 observations) for Bank of Canada (left panel) and 31 July 2001 to 31 December 2018 (4357 observations some of which may be missing) for U.S. Department of Treasury (right panel).

![Stats 03 00020 g0a7]()

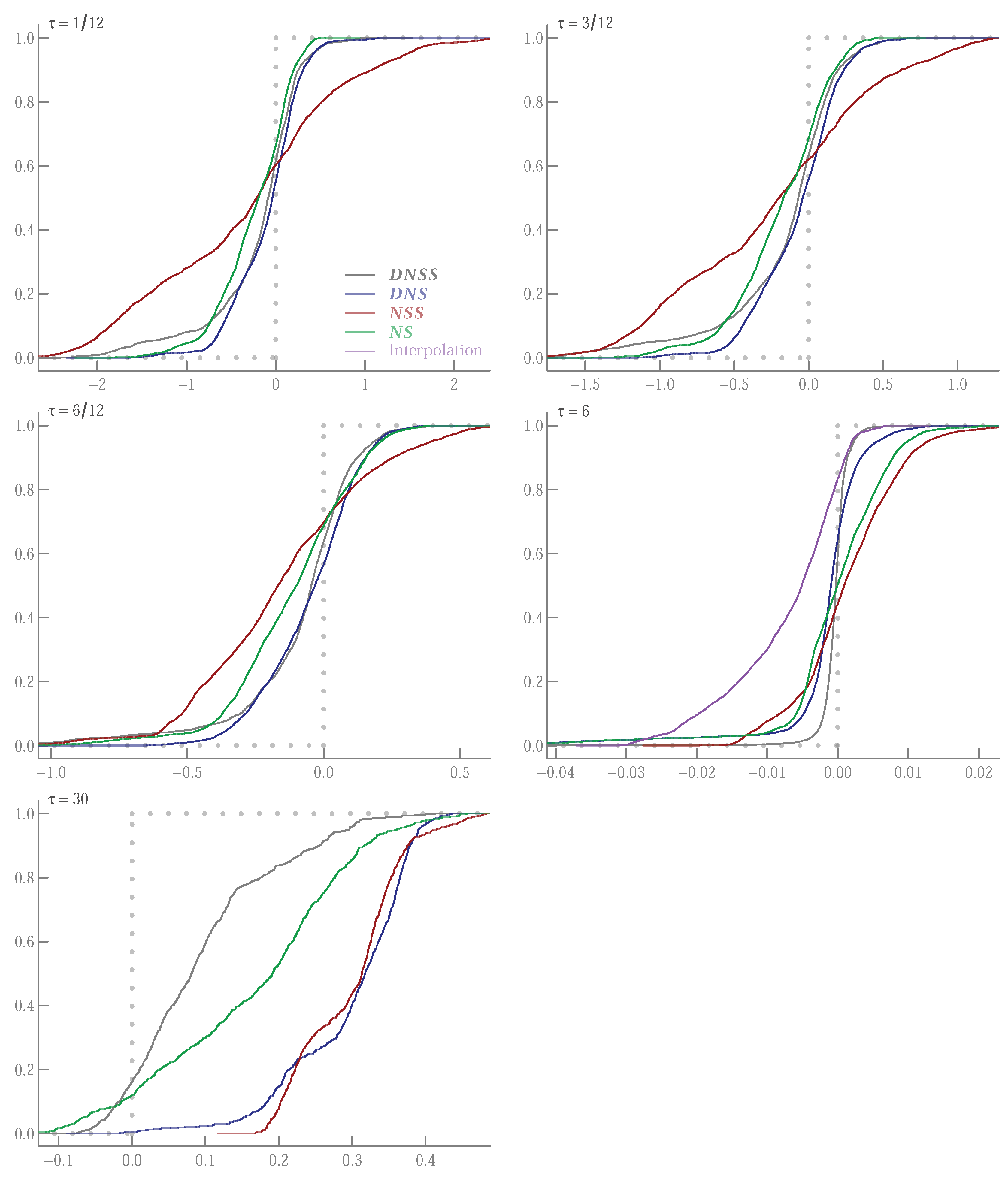

Figure A8.

Kernel density estimates of prediction error distributions. Predictions from Bank of Canada yield data with maturities (left panel) and U.S. Department of Treasury with maturities (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4719 observations) for Bank of Canada (left panel) and 31 July 2001 to 31 December 2018 (4357 observations some of which may be missing) for U.S. Department of Treasury (right panel).

Figure A8.

Kernel density estimates of prediction error distributions. Predictions from Bank of Canada yield data with maturities (left panel) and U.S. Department of Treasury with maturities (right panel). is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed. The daily sample is 4 January 2000 to 31 December 2018 (4719 observations) for Bank of Canada (left panel) and 31 July 2001 to 31 December 2018 (4357 observations some of which may be missing) for U.S. Department of Treasury (right panel).

![Stats 03 00020 g0a8]()

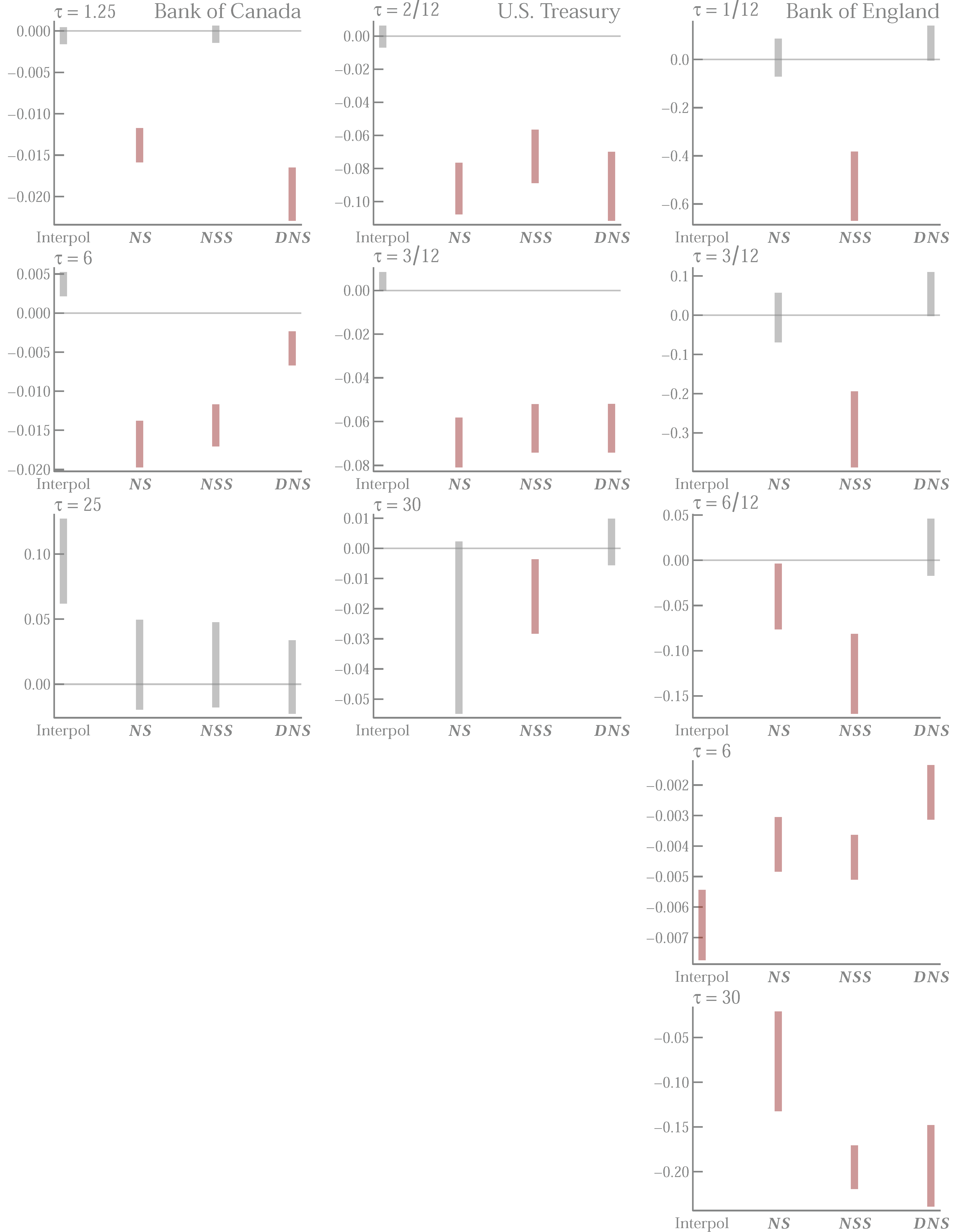

Figure A9.

Prediction mean squared error (MSE) differences. Plotted are 0.95 confidence intervals for the difference in MSE between and other models. A negative difference indicates better forecasts for relative to the comparison model. Red intervals indicate statistical significance at size 0.05. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed.

Figure A9.

Prediction mean squared error (MSE) differences. Plotted are 0.95 confidence intervals for the difference in MSE between and other models. A negative difference indicates better forecasts for relative to the comparison model. Red intervals indicate statistical significance at size 0.05. is the dynamic Nelson-Siegel-Svensson specification where both decay parameters and follow an AR(1) process, is the dynamc Nelson-Siegel specification with a single decay parameter that follows an AR(1) process, is the Nelson-Siegel-Svensson specification with the two decay parameters and assumed to be fixed, is the Nelson-Siegel specification with a single decay parameter assumed to be fixed.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}