Real Estate Market Responses to the COVID-19 Crisis: Which Prospects for the Metropolitan Area of Naples (Italy)?

Abstract

:1. Introduction

2. Overview of Recent Studies on the Effects of the Pandemic on the Real Estate Market

3. Methodology

4. Analysis of the Pre-COVID-19 Real Estate Market

4.1. The Pre-COVID-19 Real Estate Market in Italy

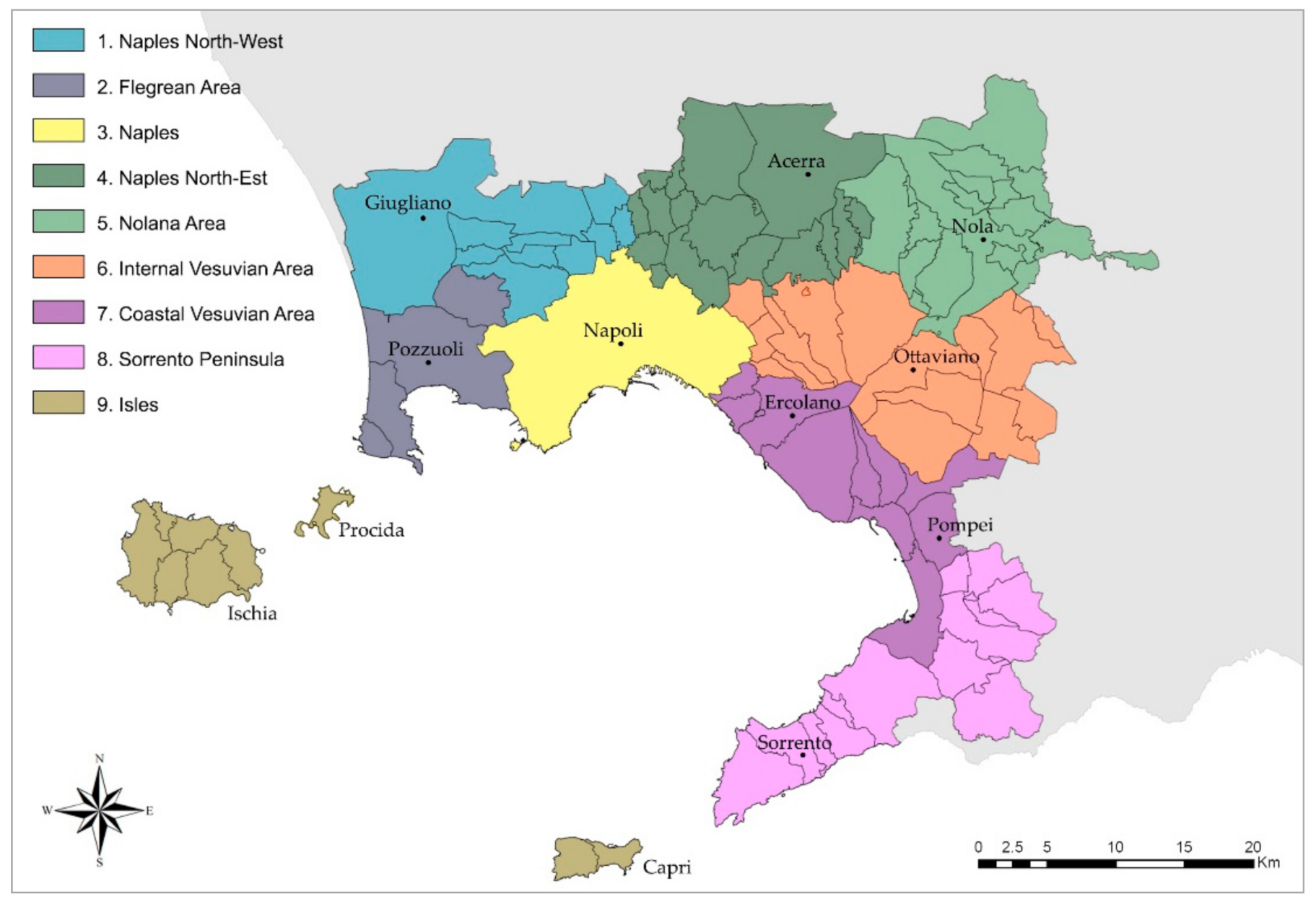

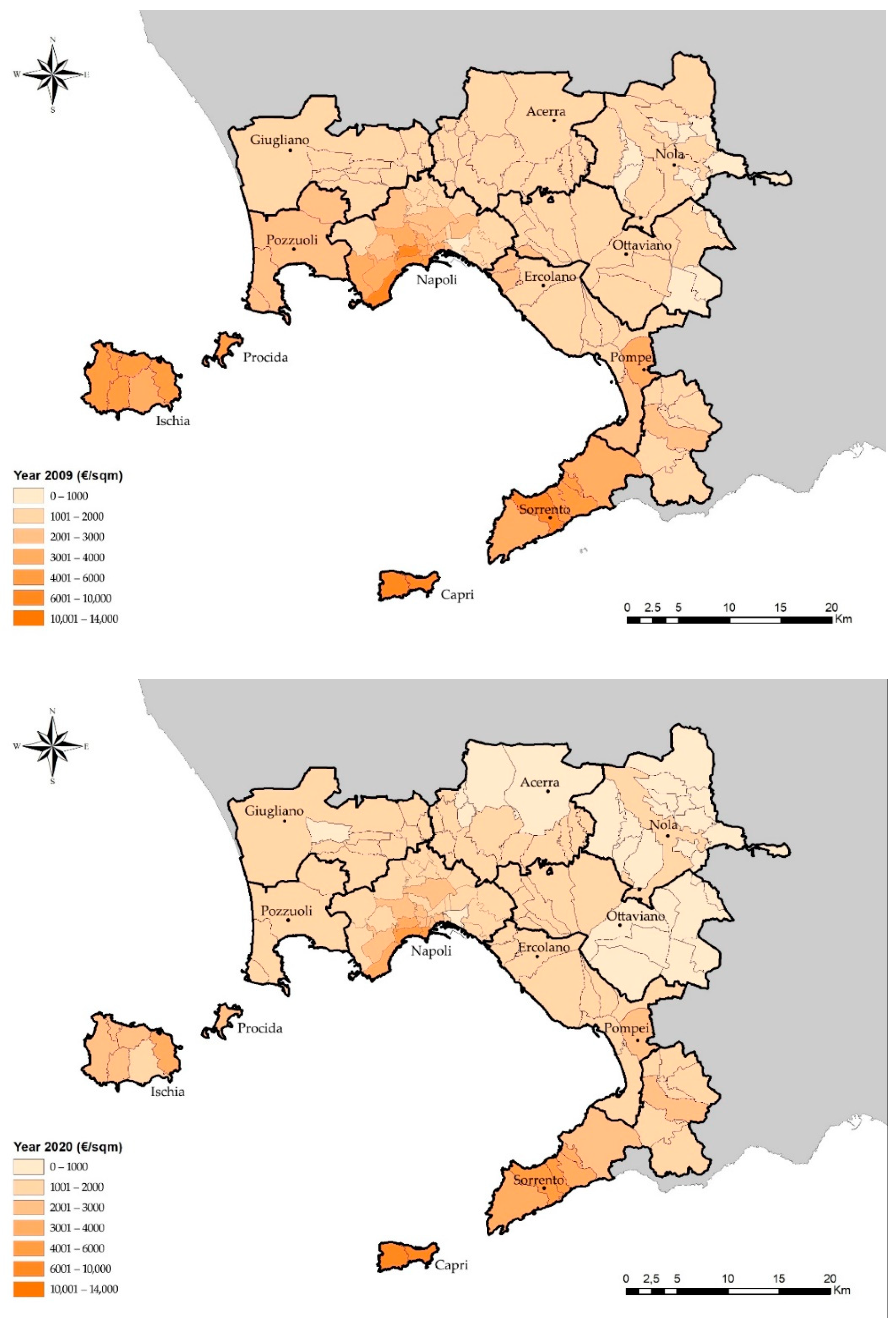

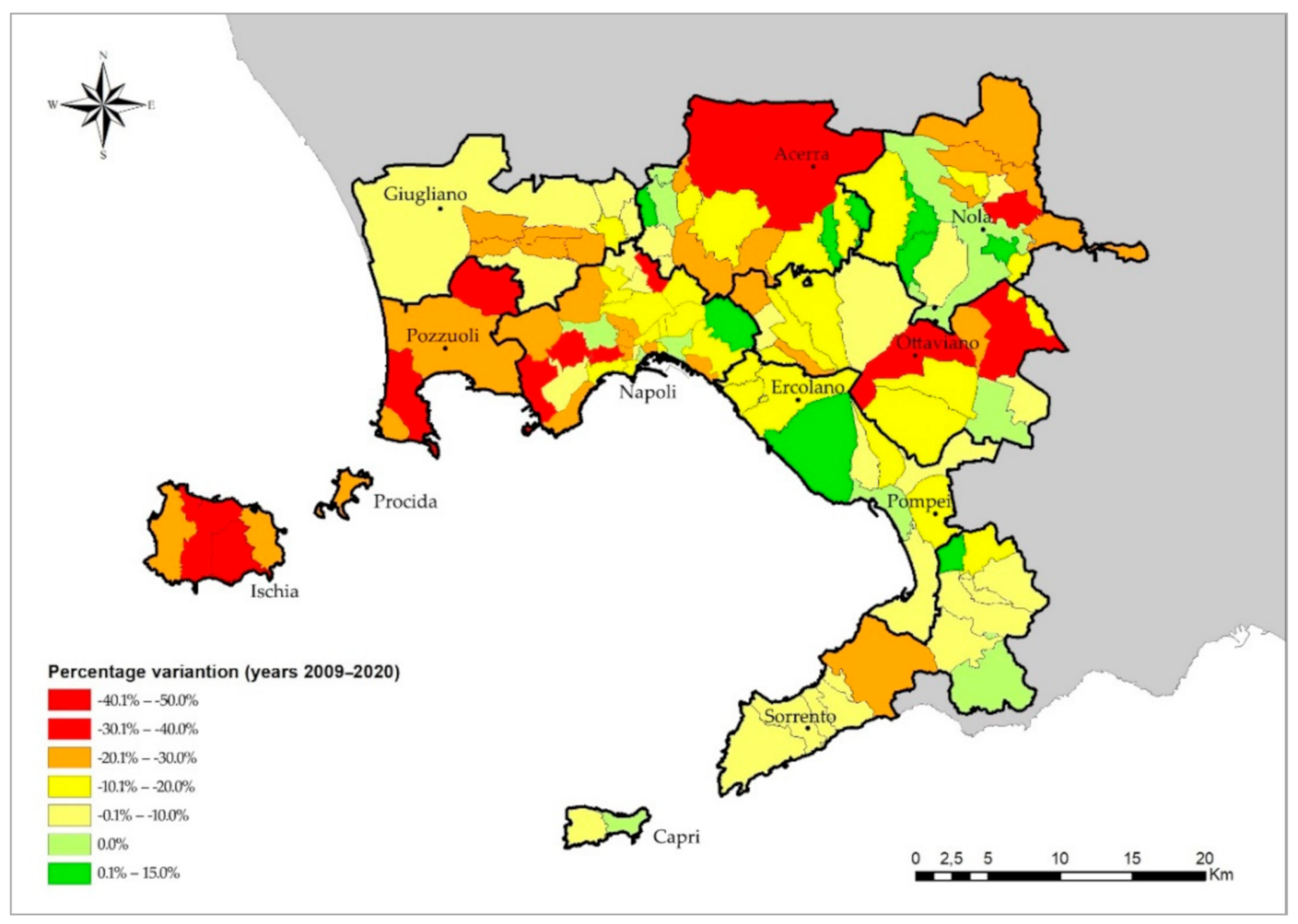

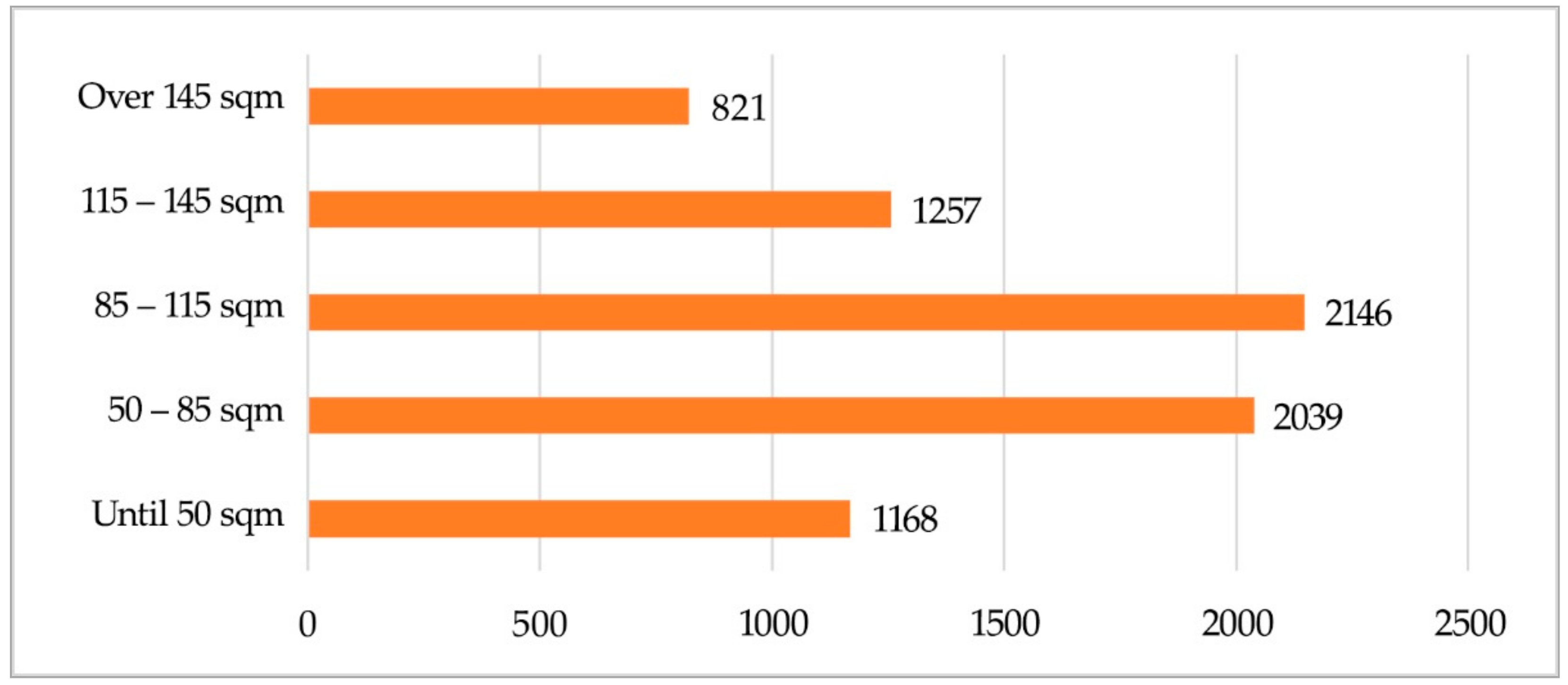

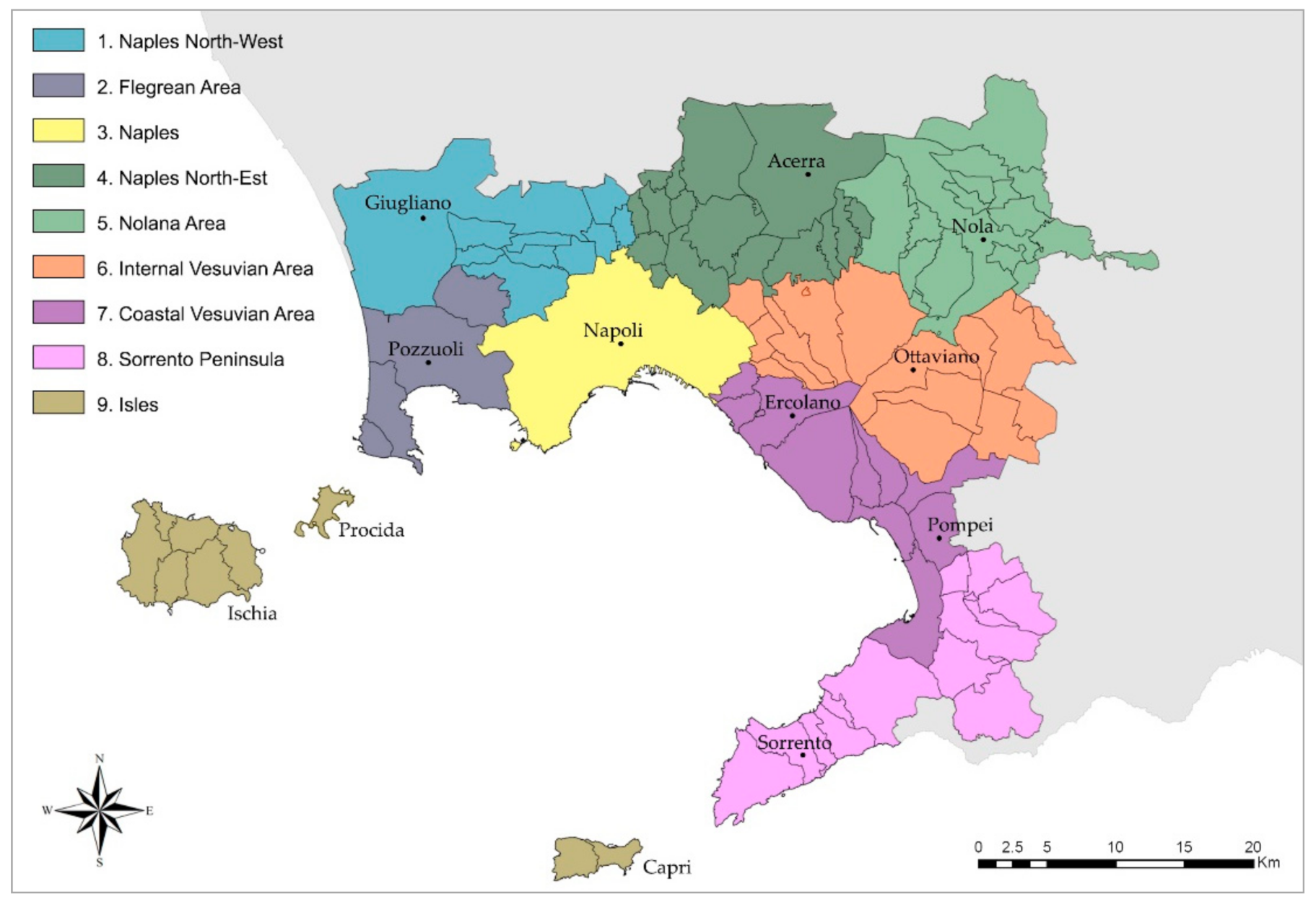

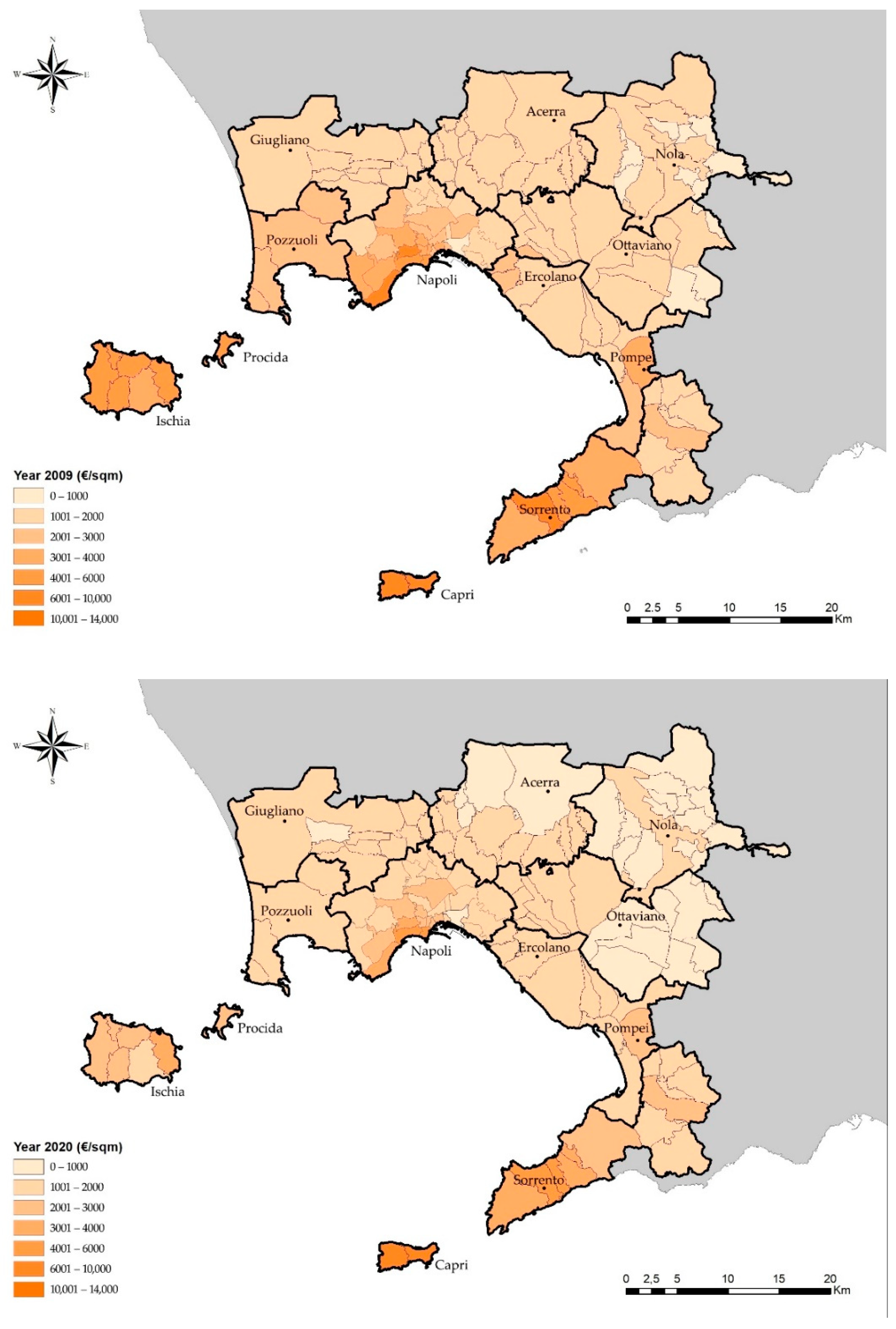

4.2. The Pre-COVID-19 Real Estate Market in the Metropolitan Area of Naples

5. Forecasts for the Post-COVID-19 Real Estate Market in Italy

5.1. Forecasts for Post-COVID-19 Buying, Selling and Rental Market

5.2. Forecasts for Tax Incentives and Changes in Housing Demand

6. The Real Estate Market in Italy in the Post-Lockdown Phase

6.1. Post-Lockdown Buying, Selling and Rental Market

6.2. Changes in Housing Demand, Incentives and New Research Technologies

7. Results of the Questionnaires

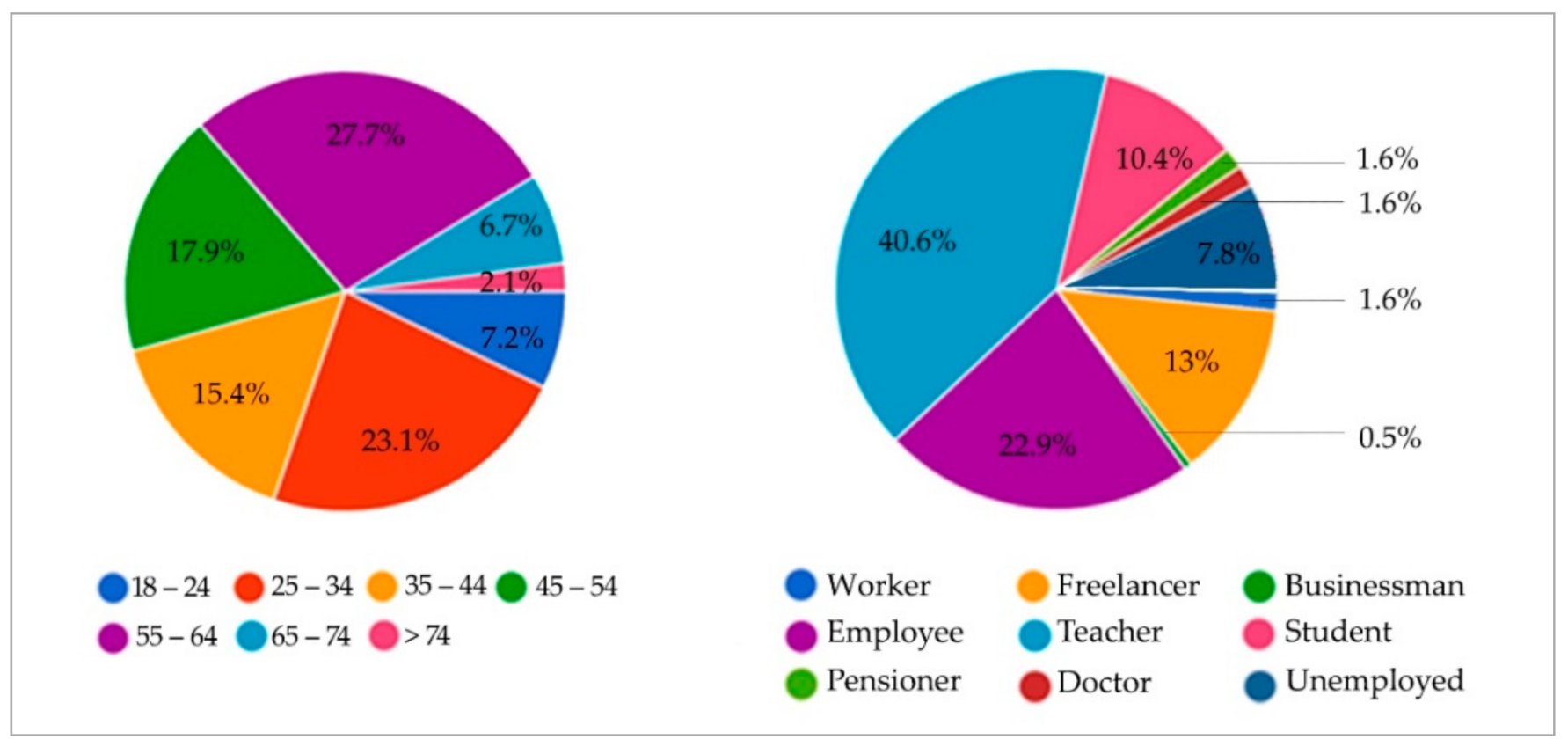

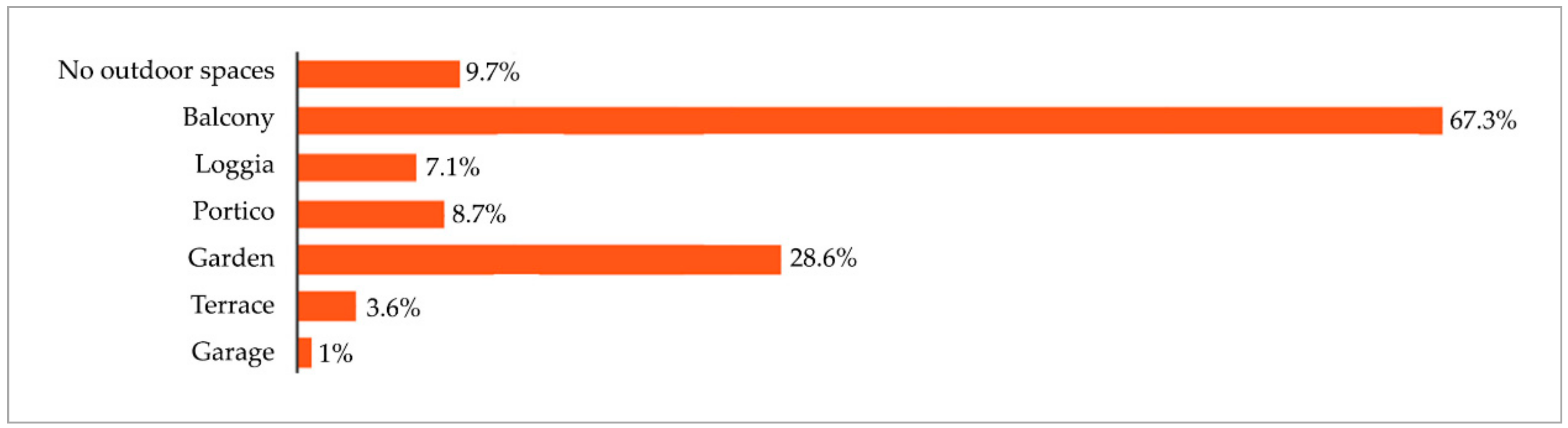

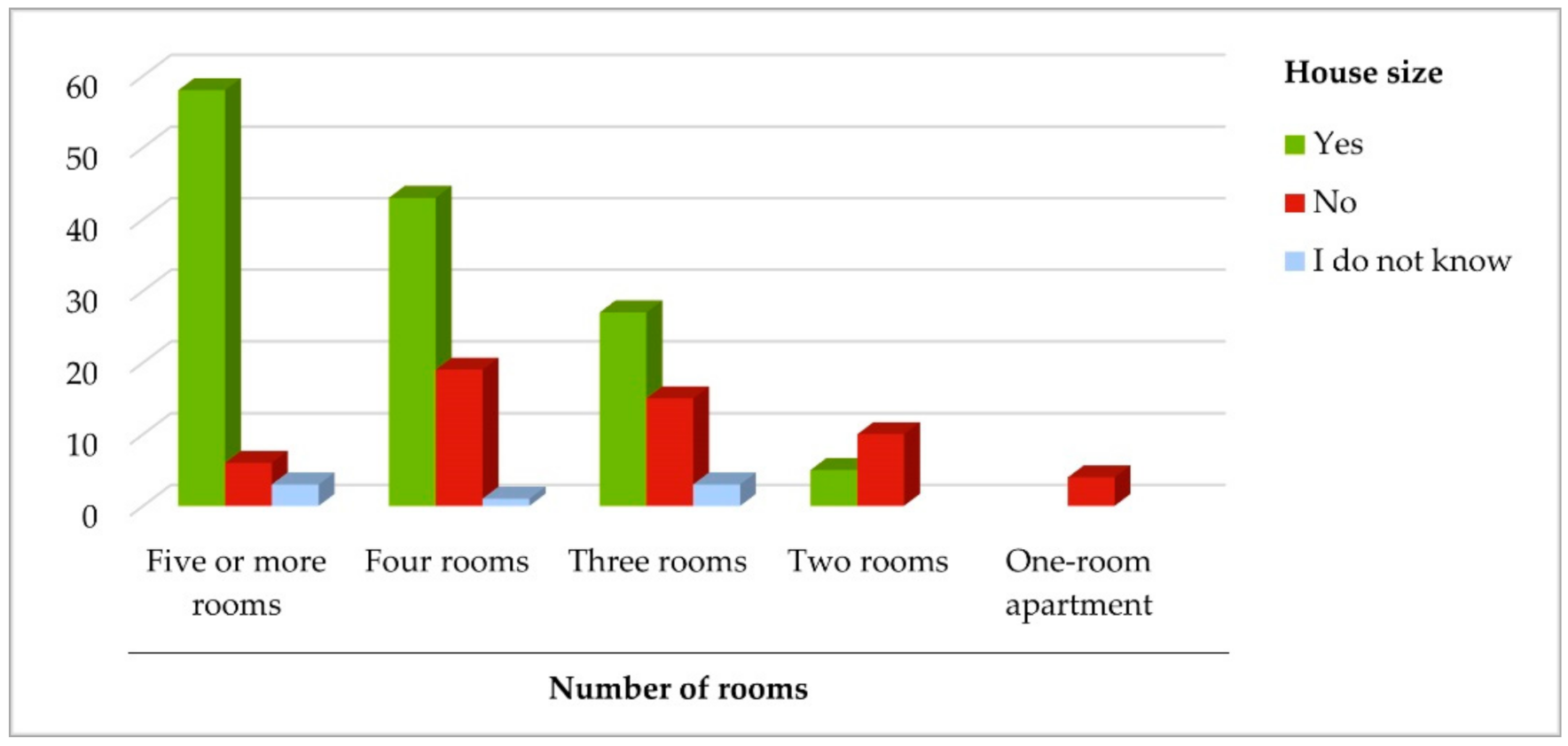

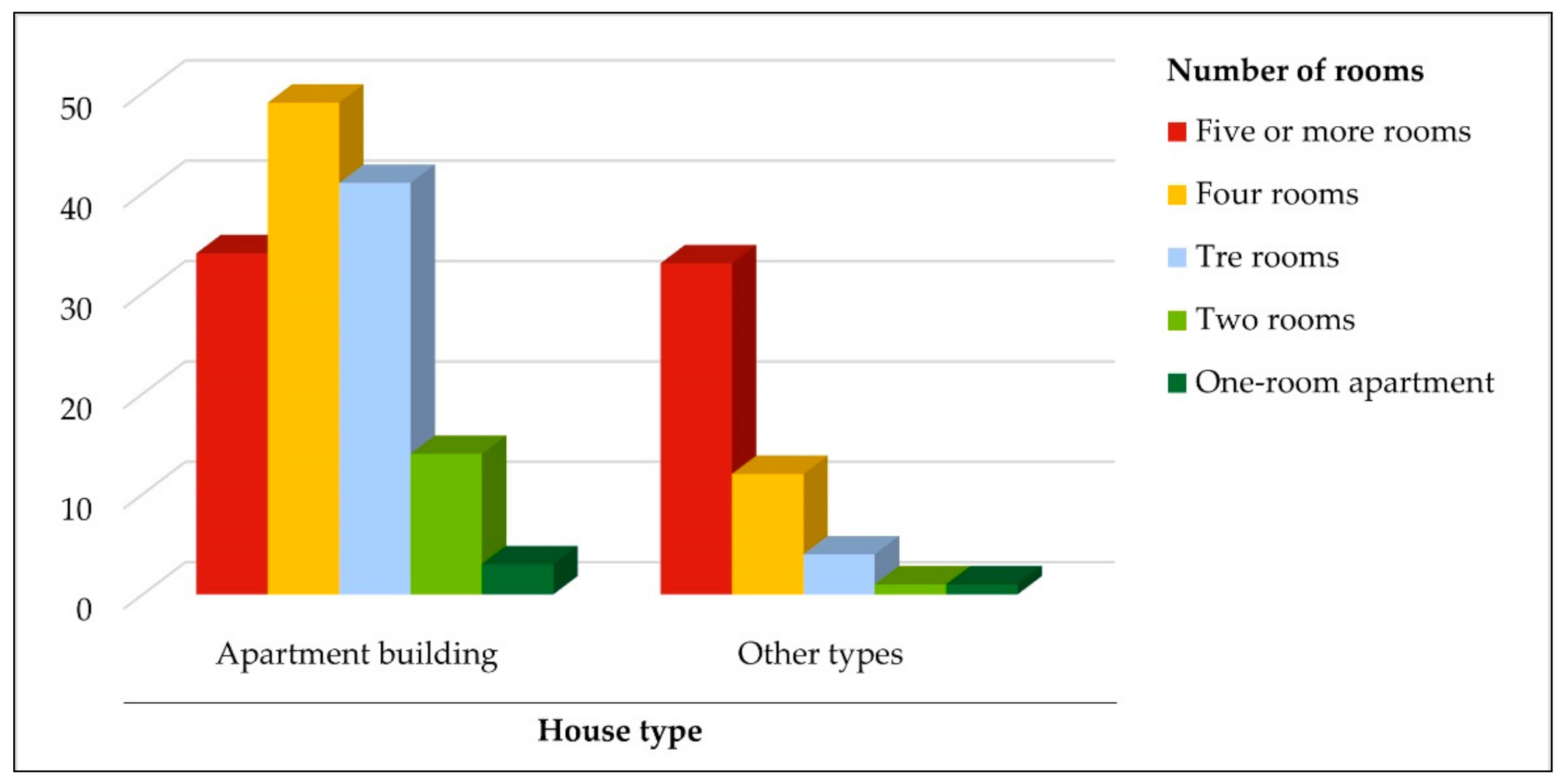

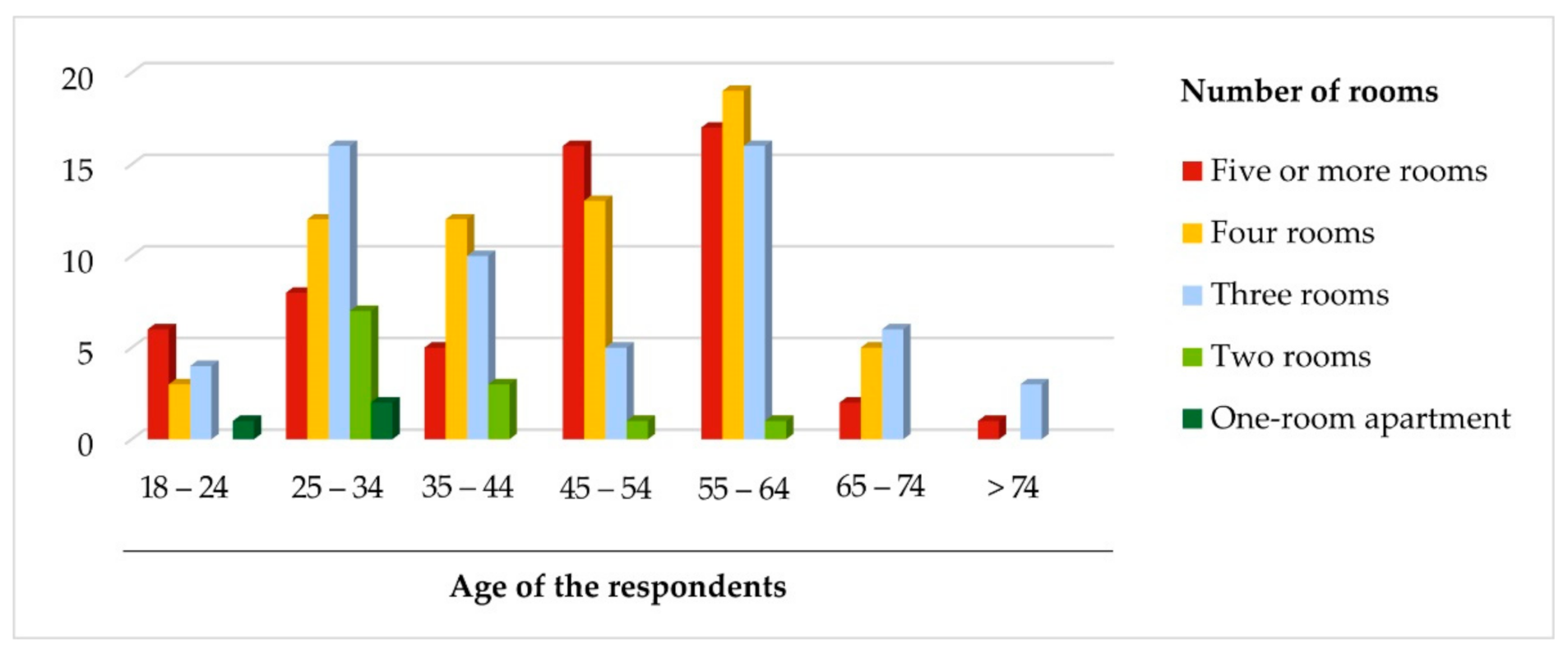

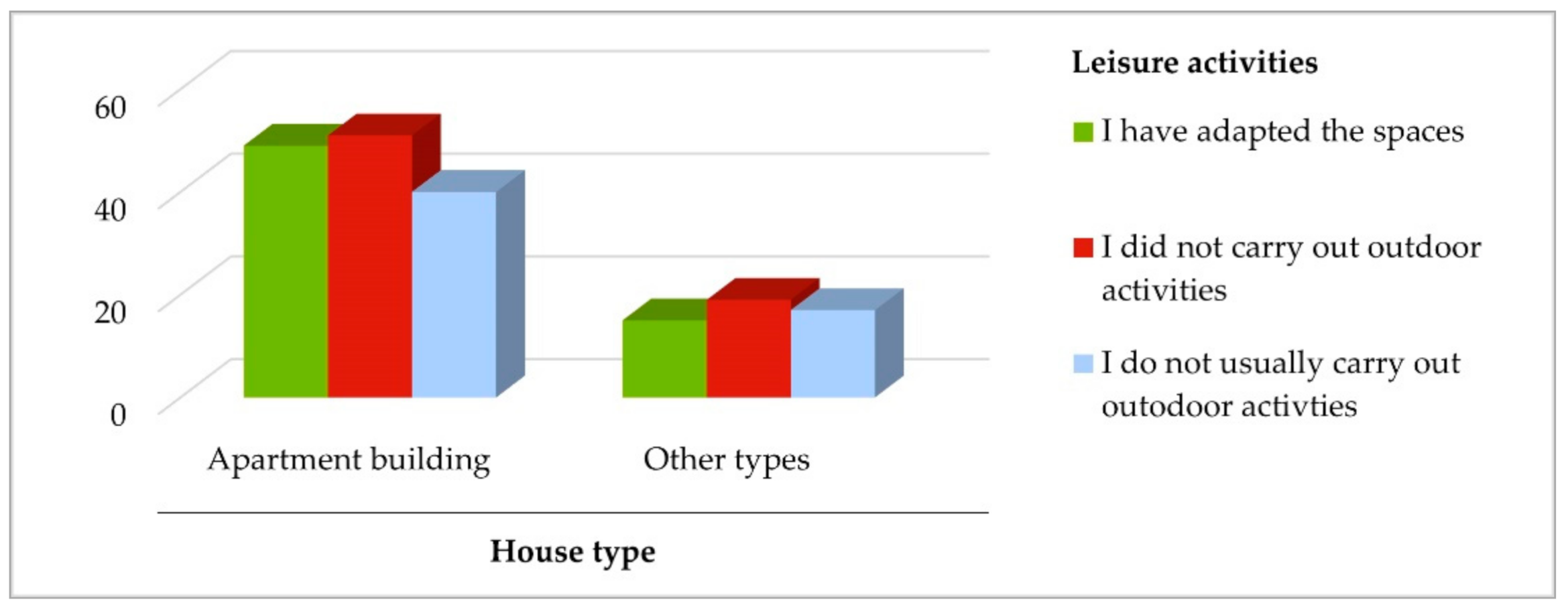

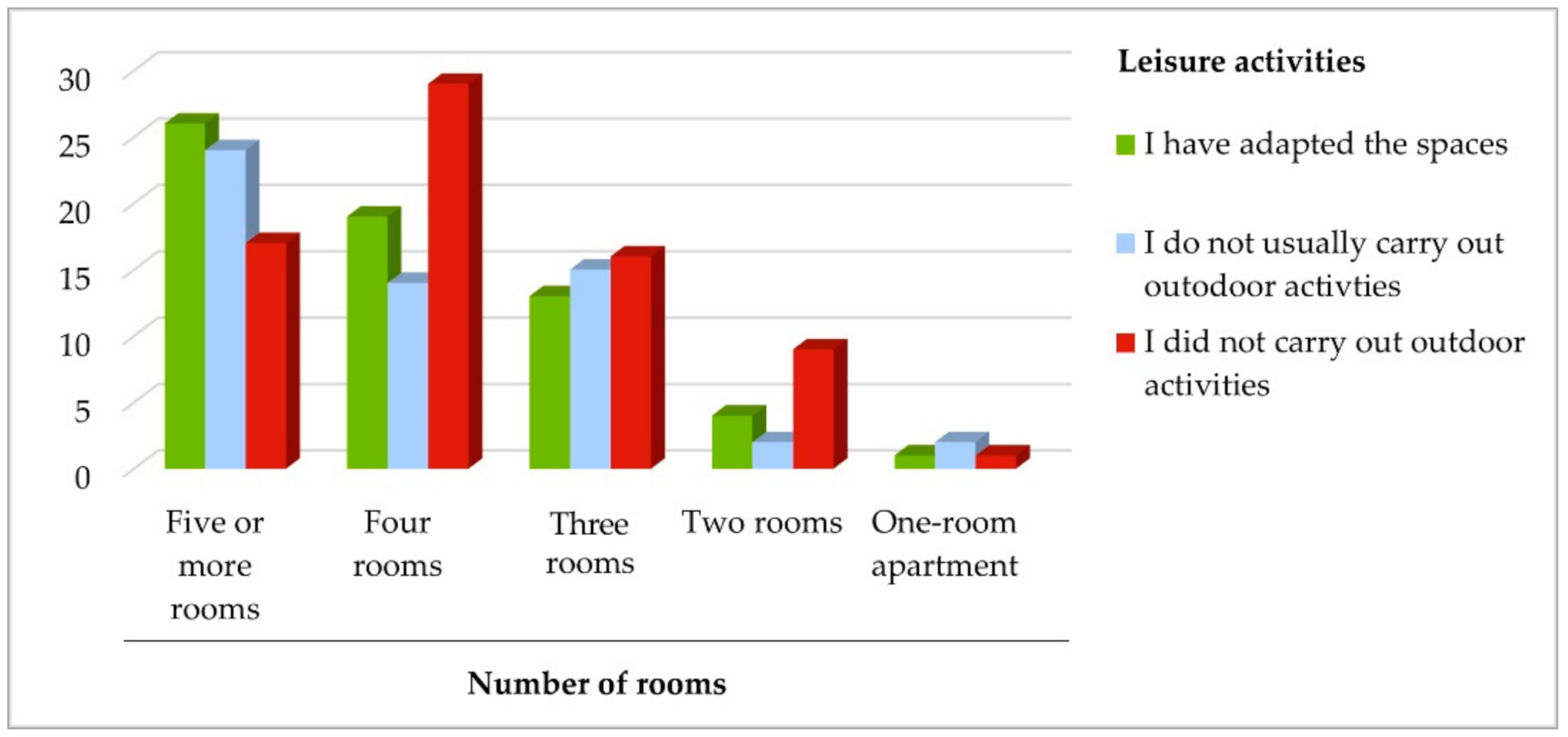

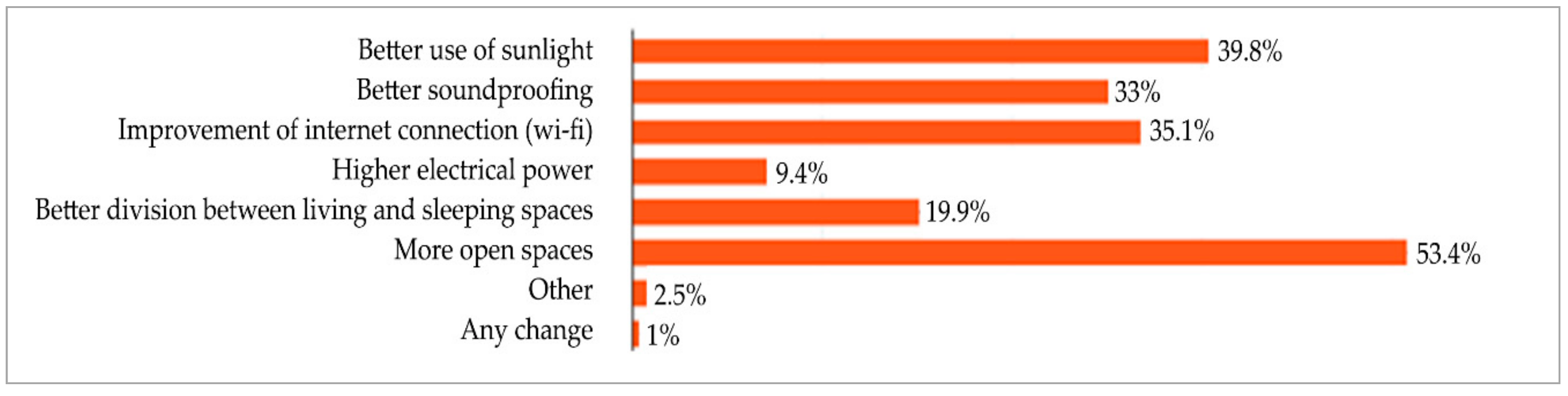

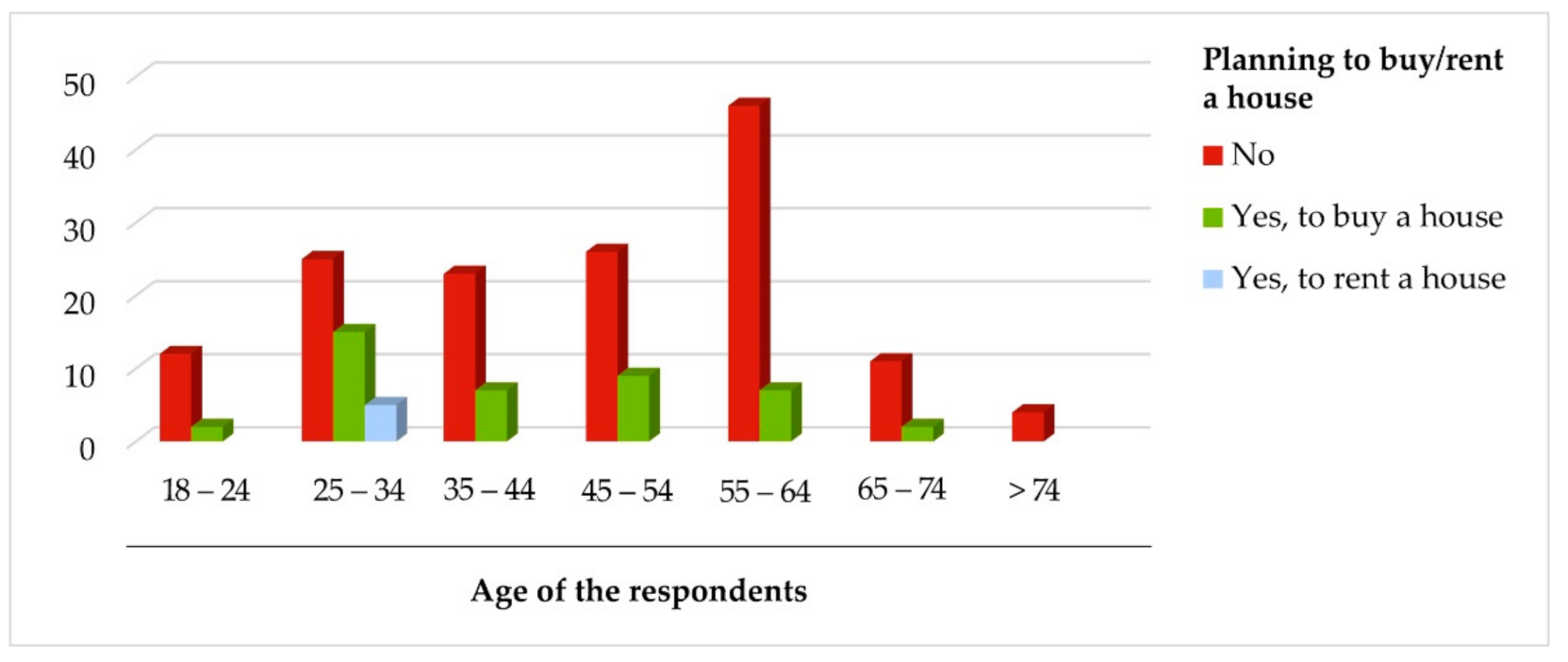

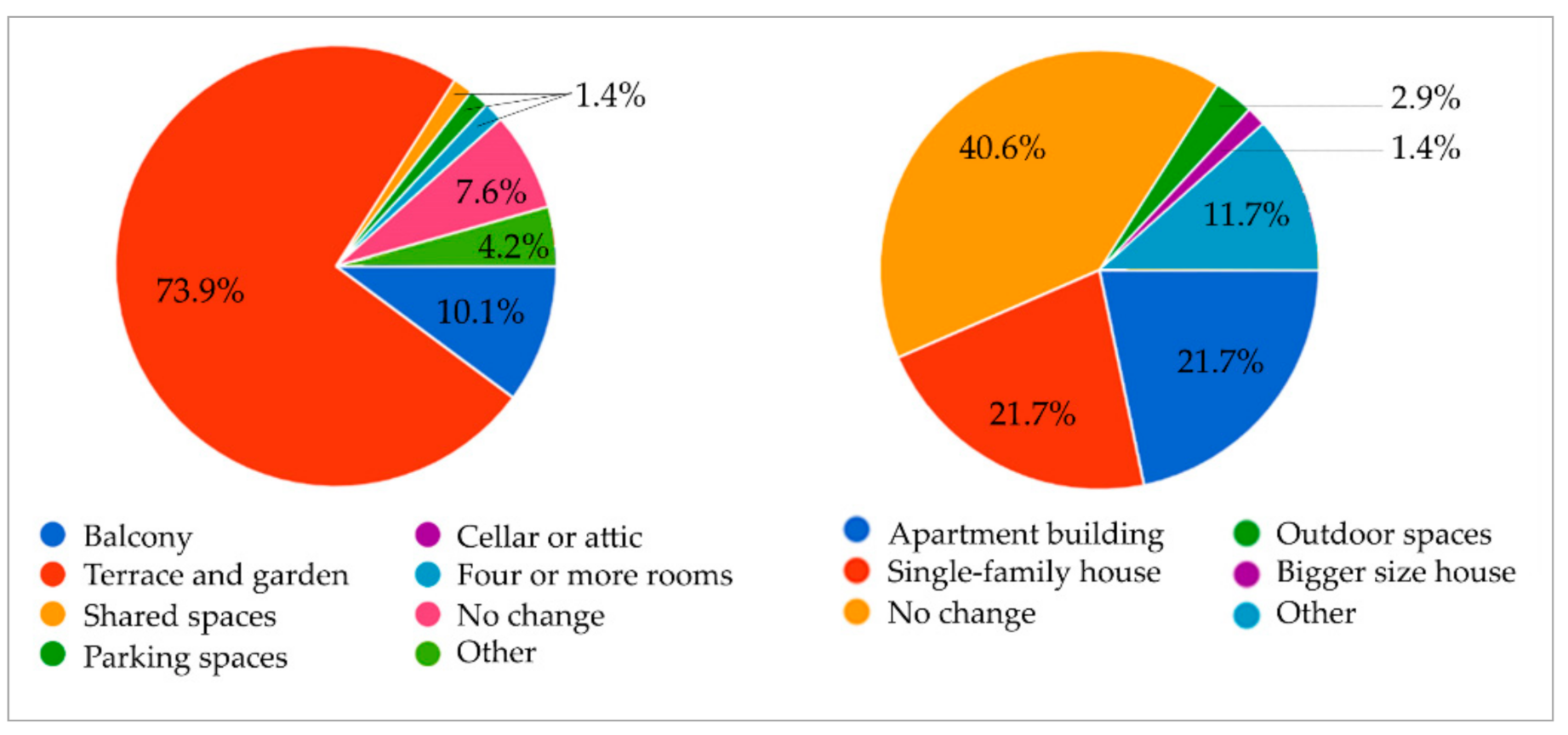

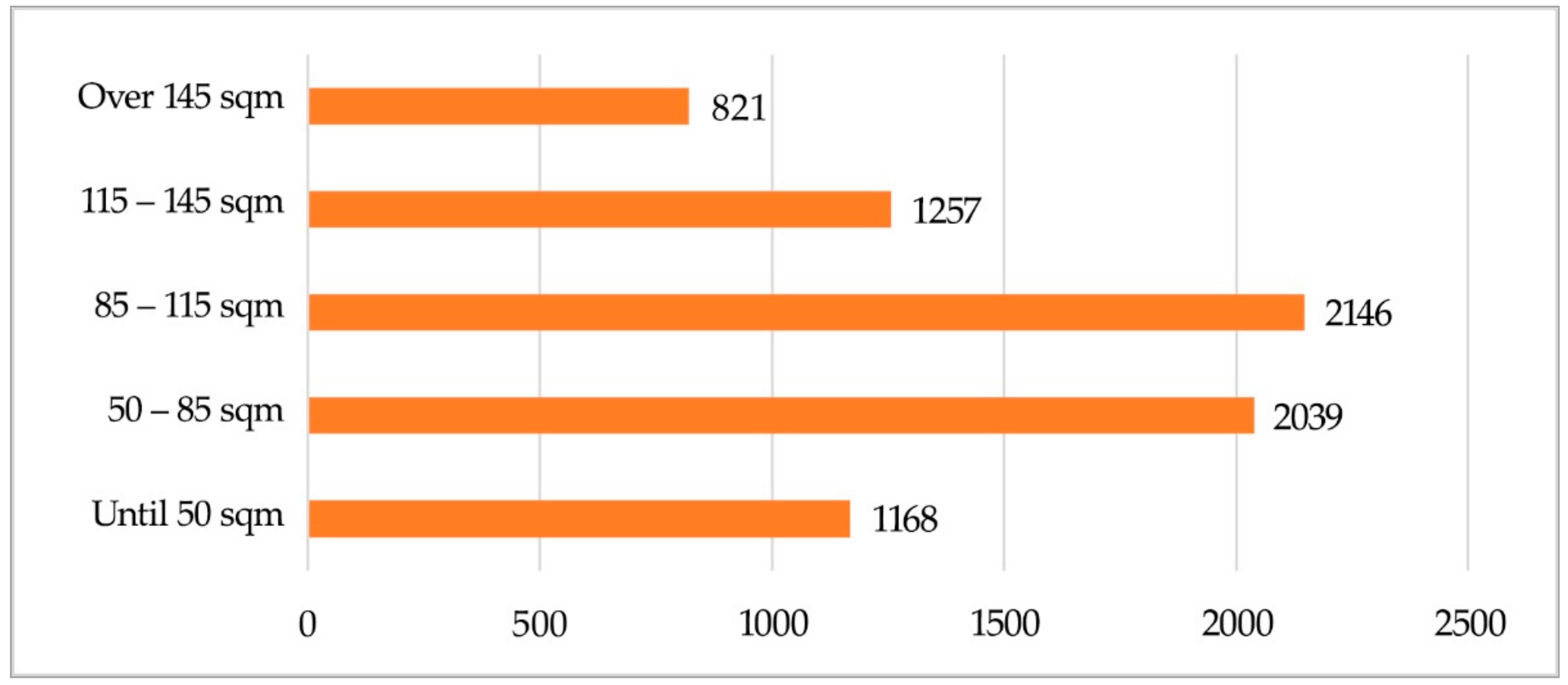

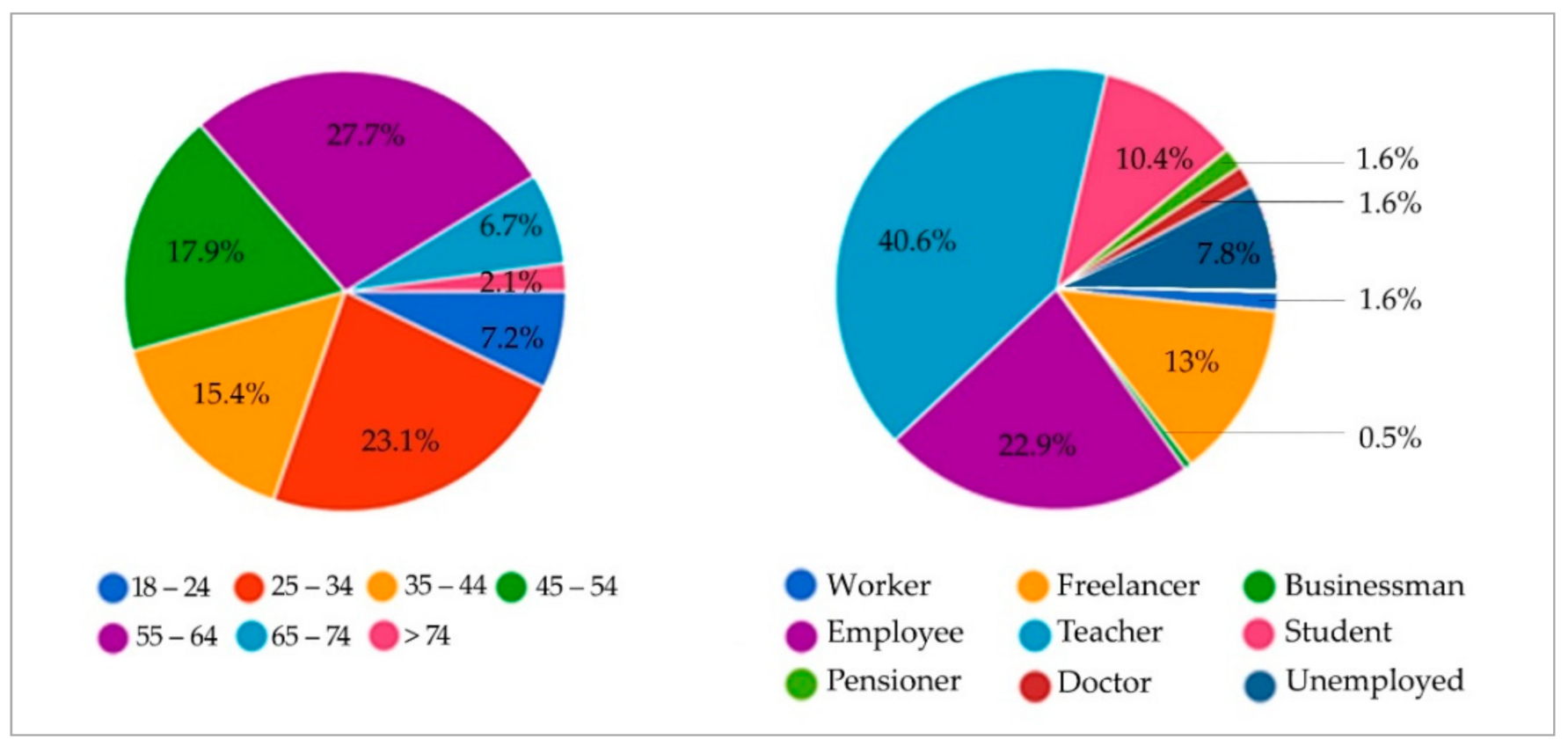

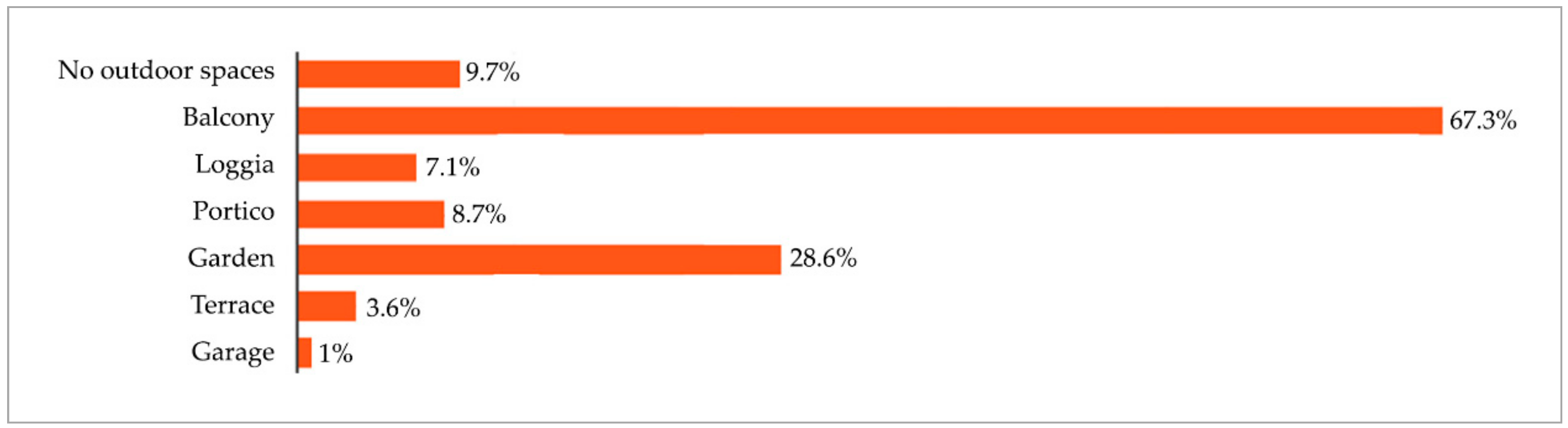

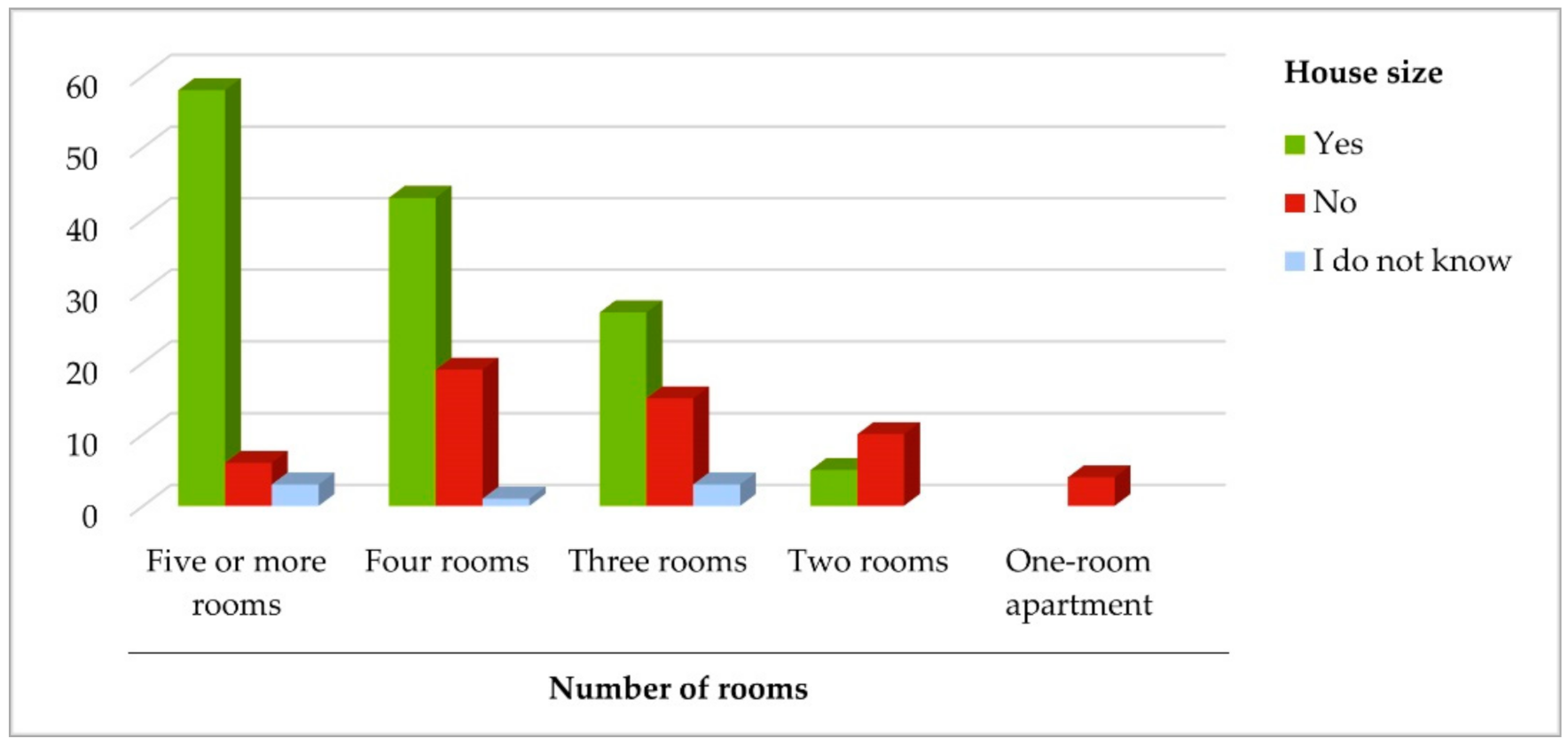

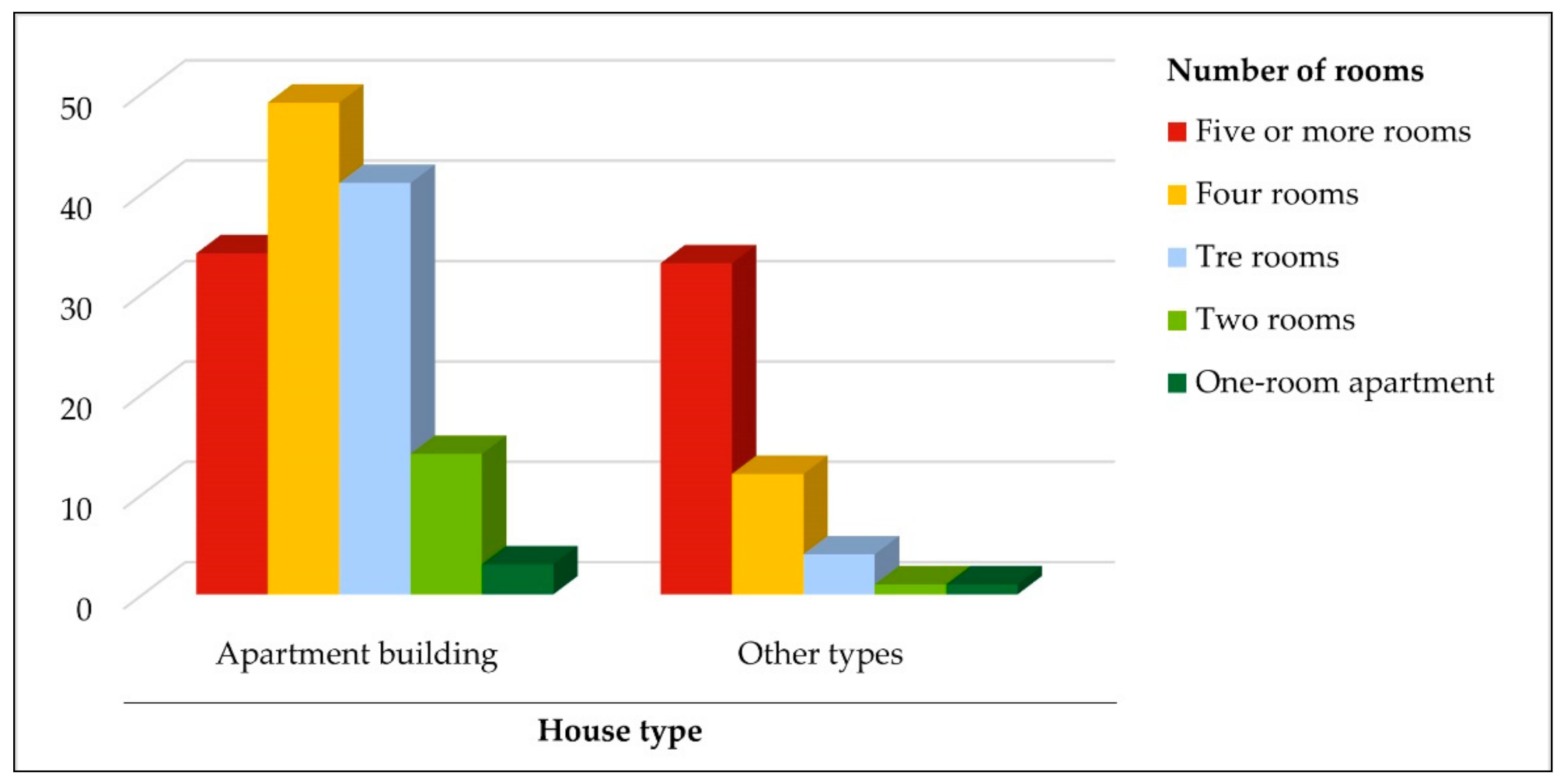

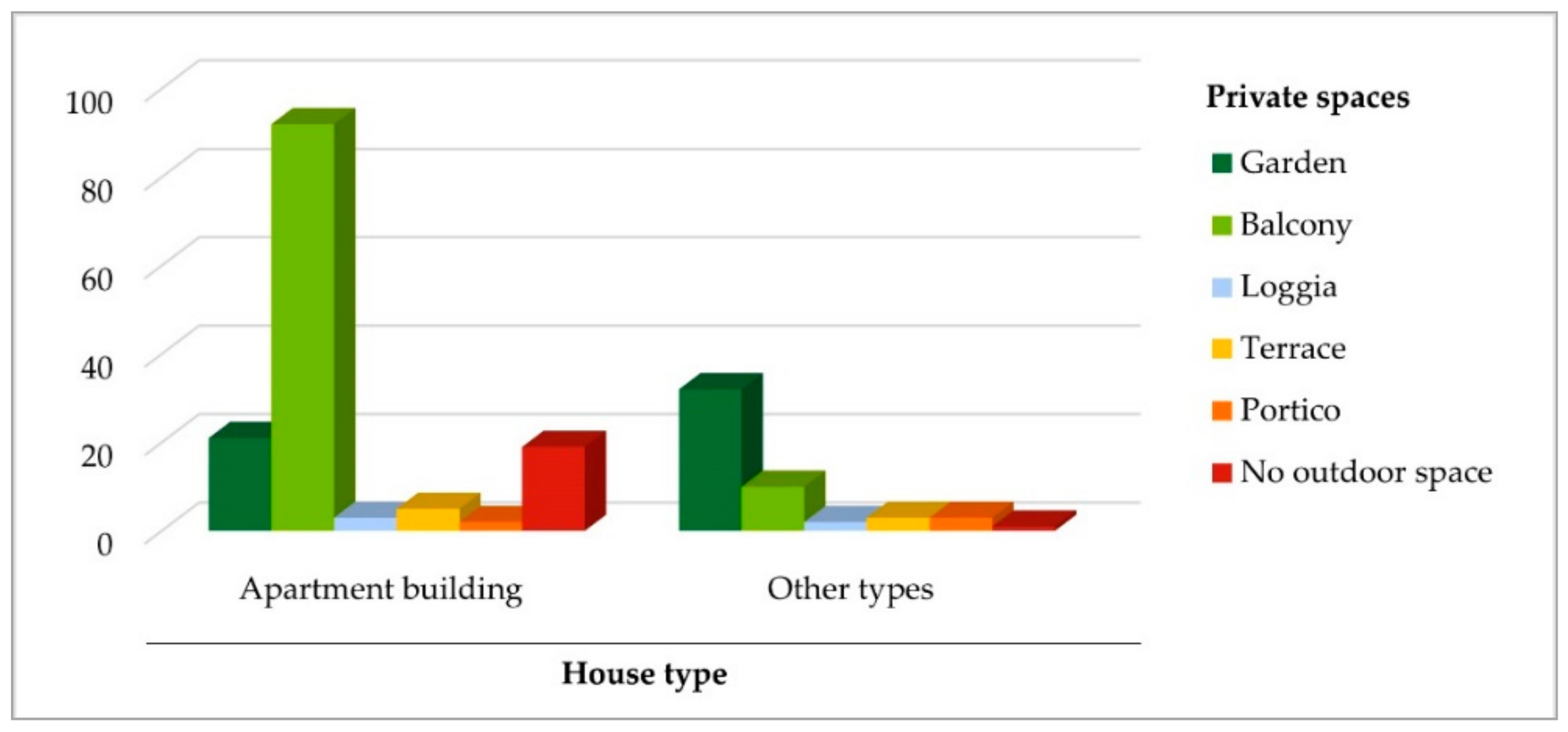

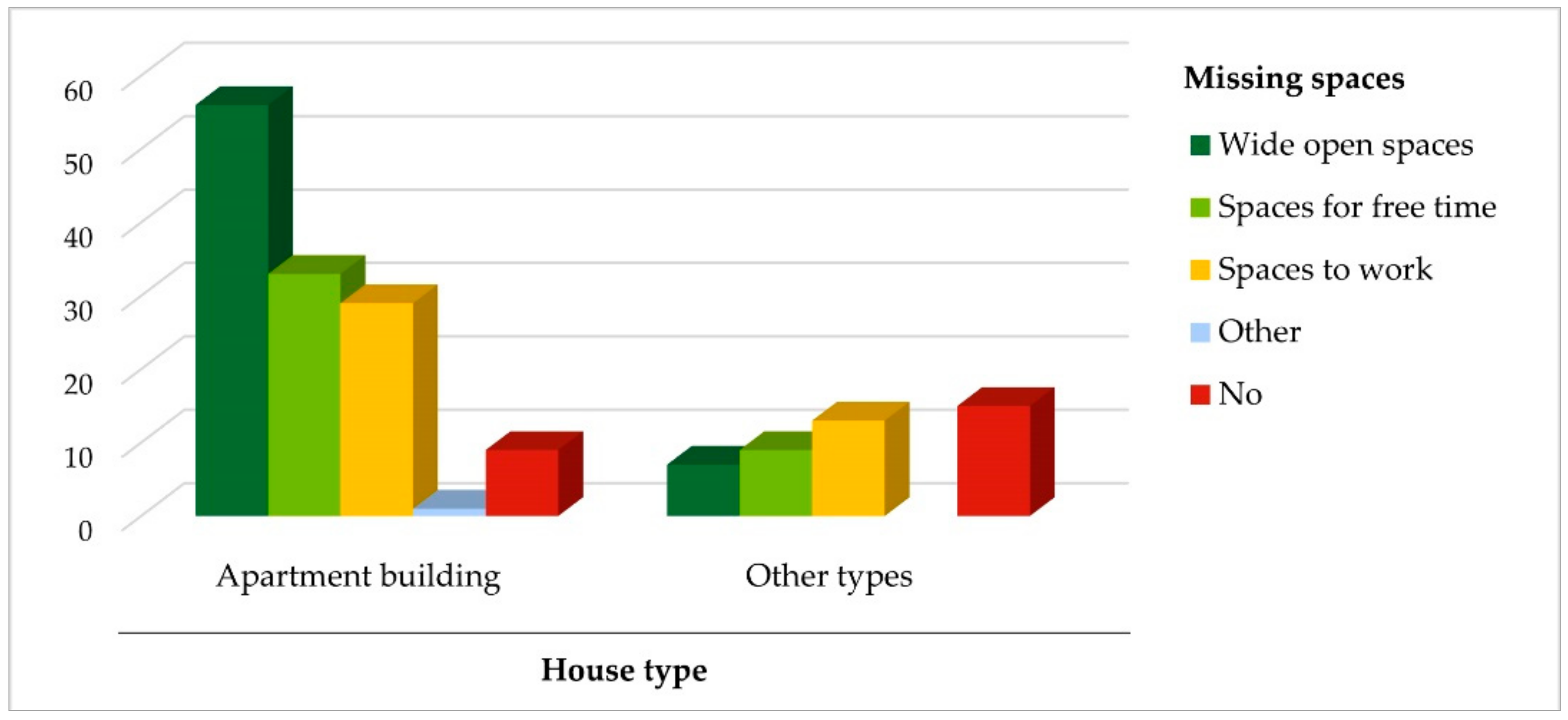

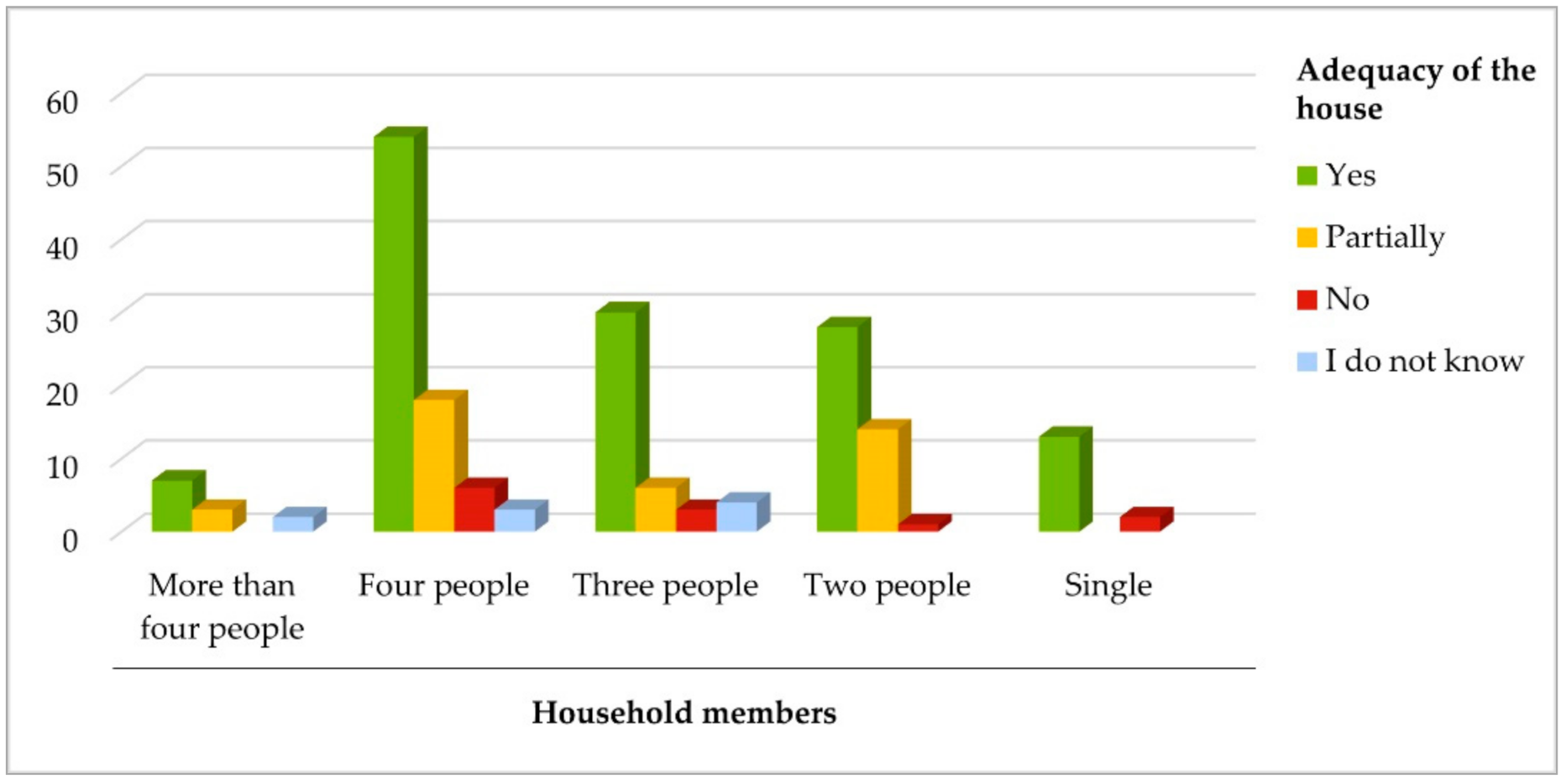

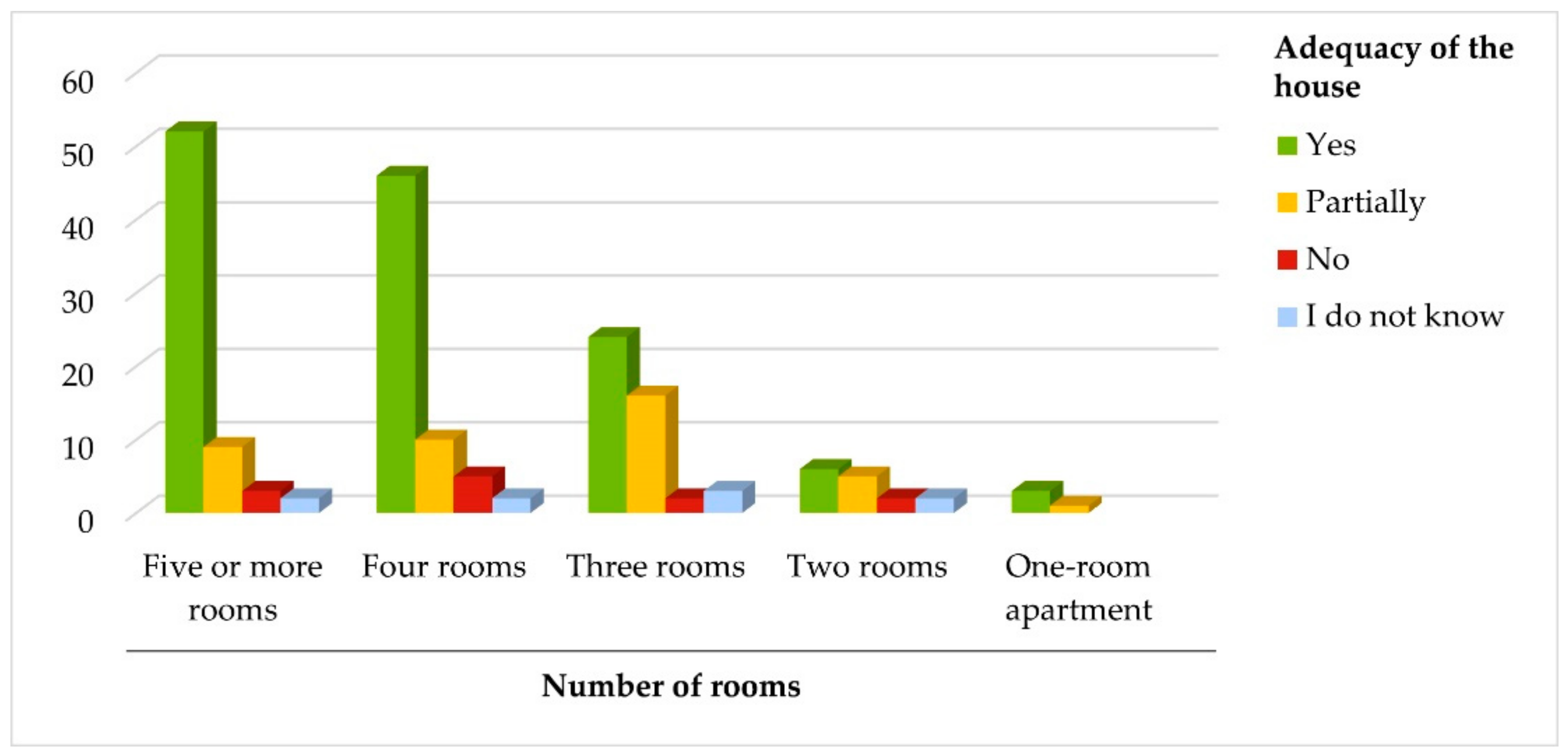

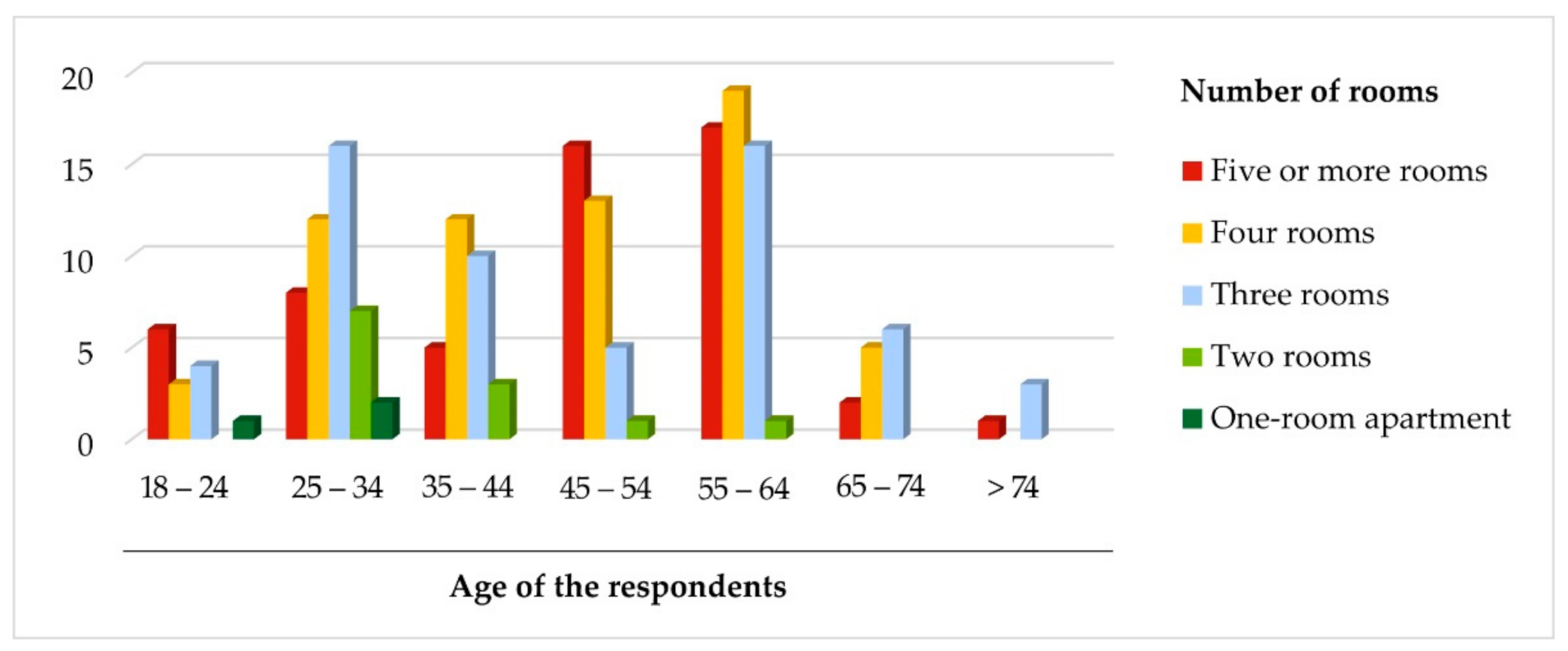

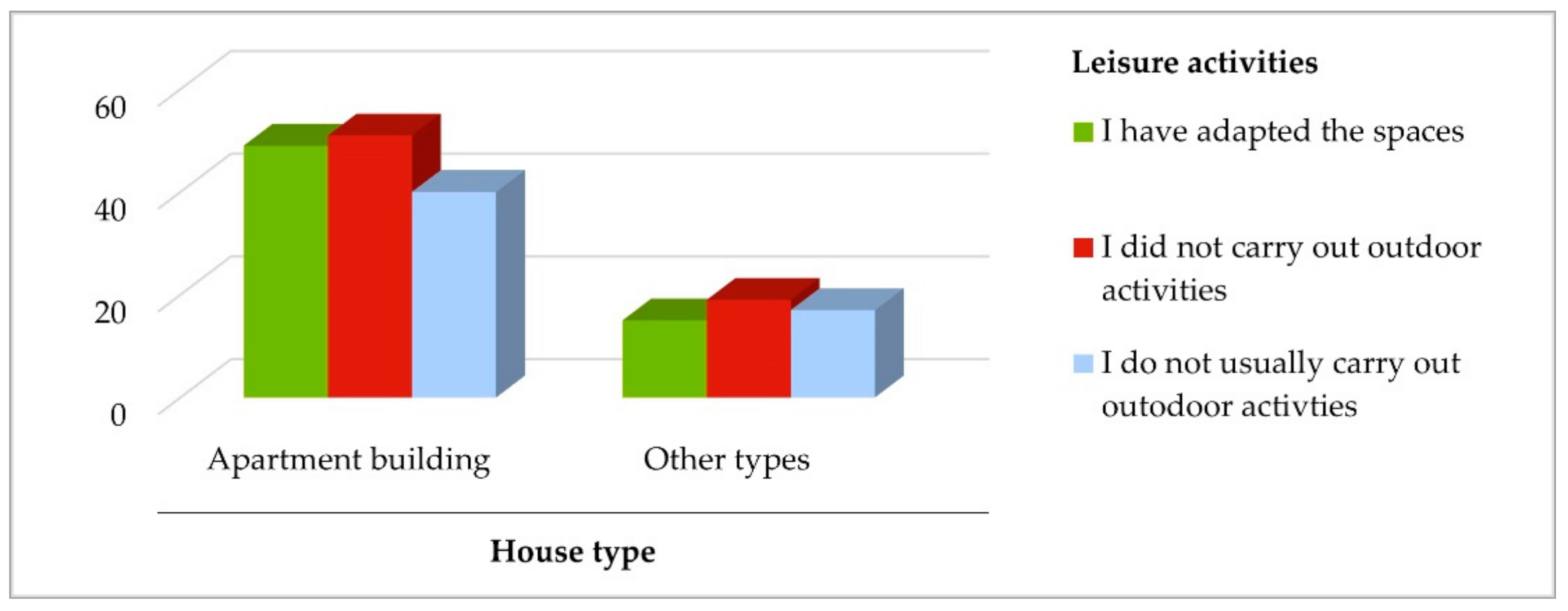

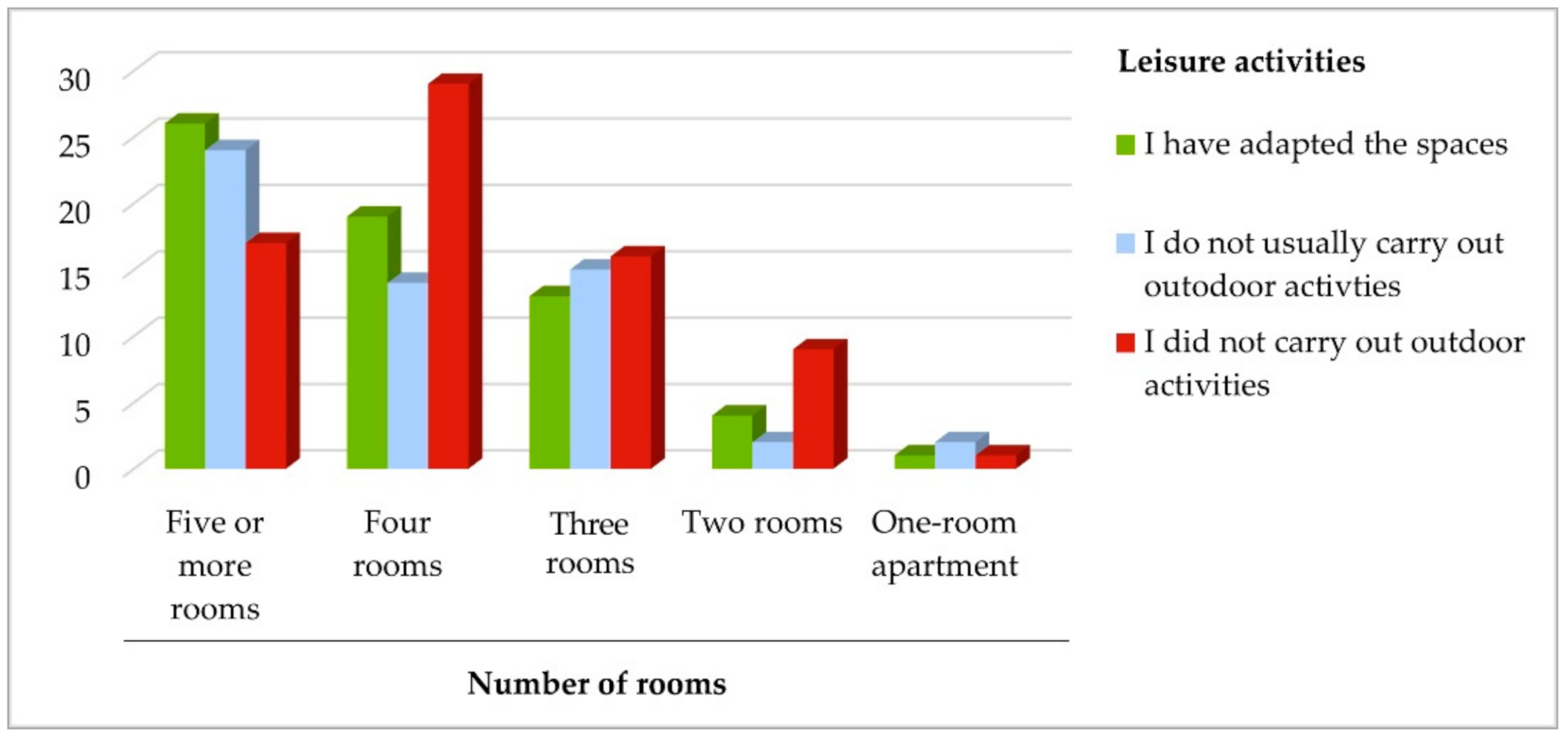

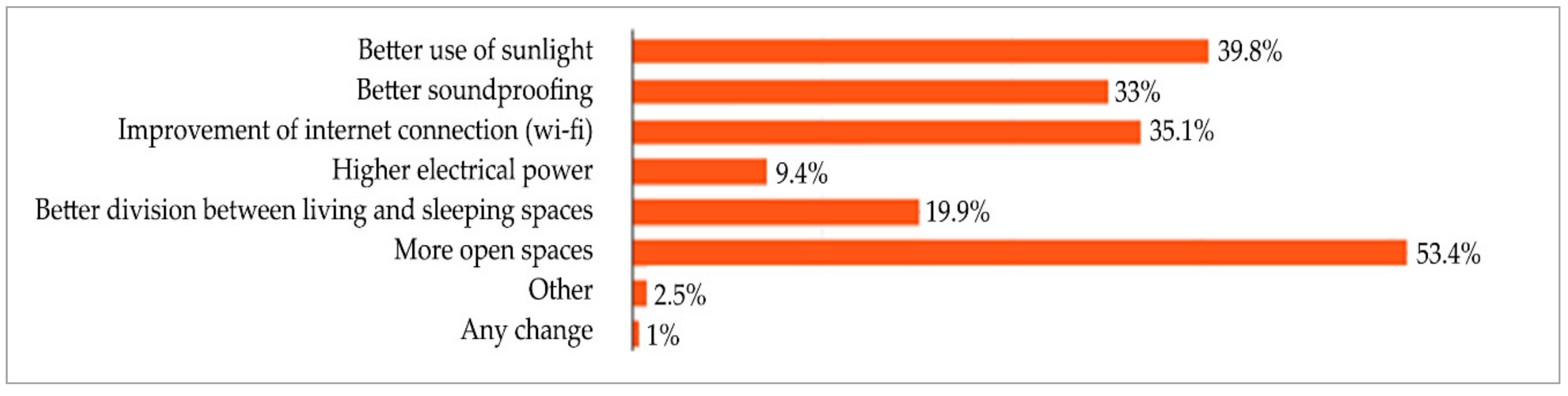

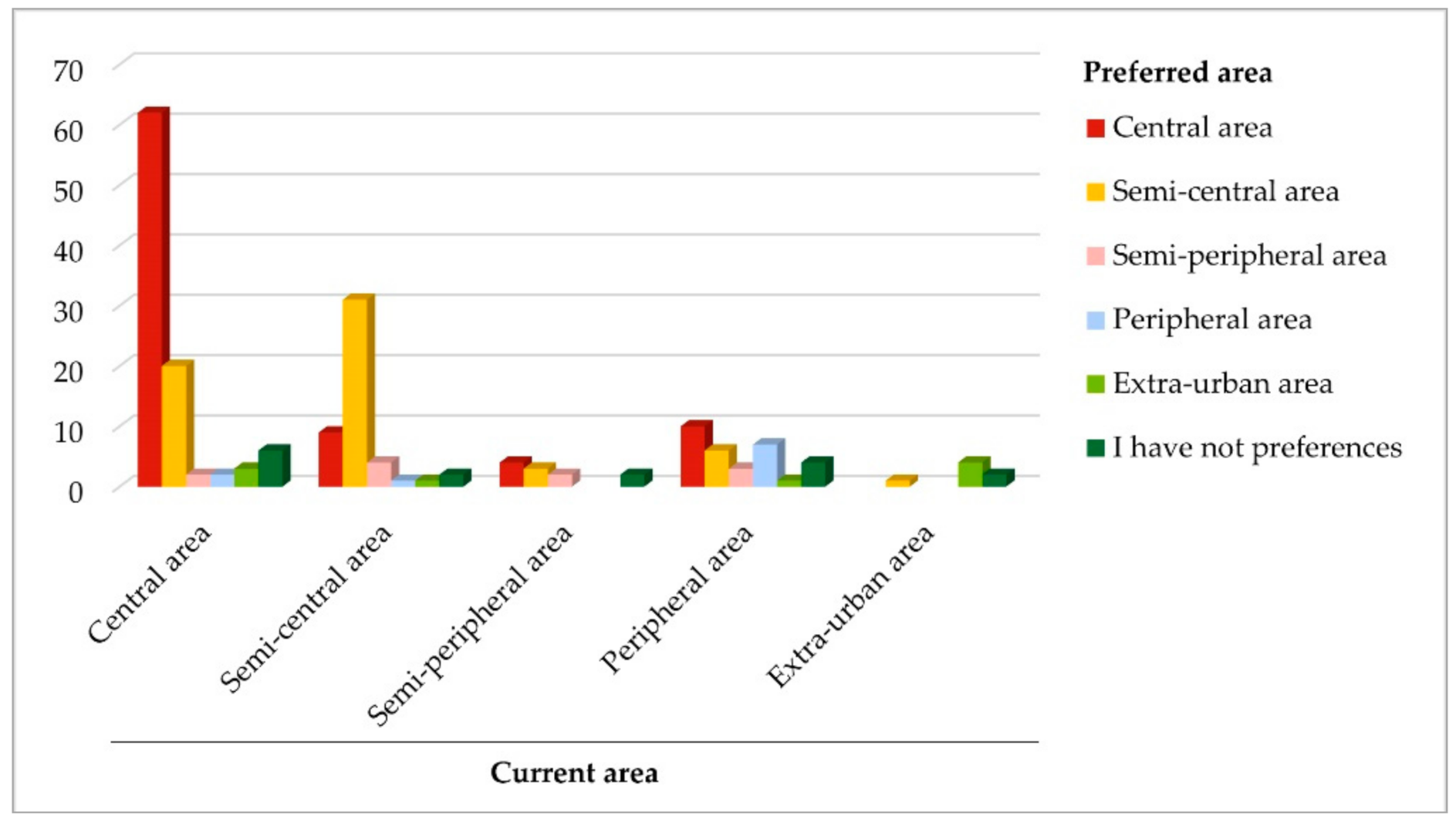

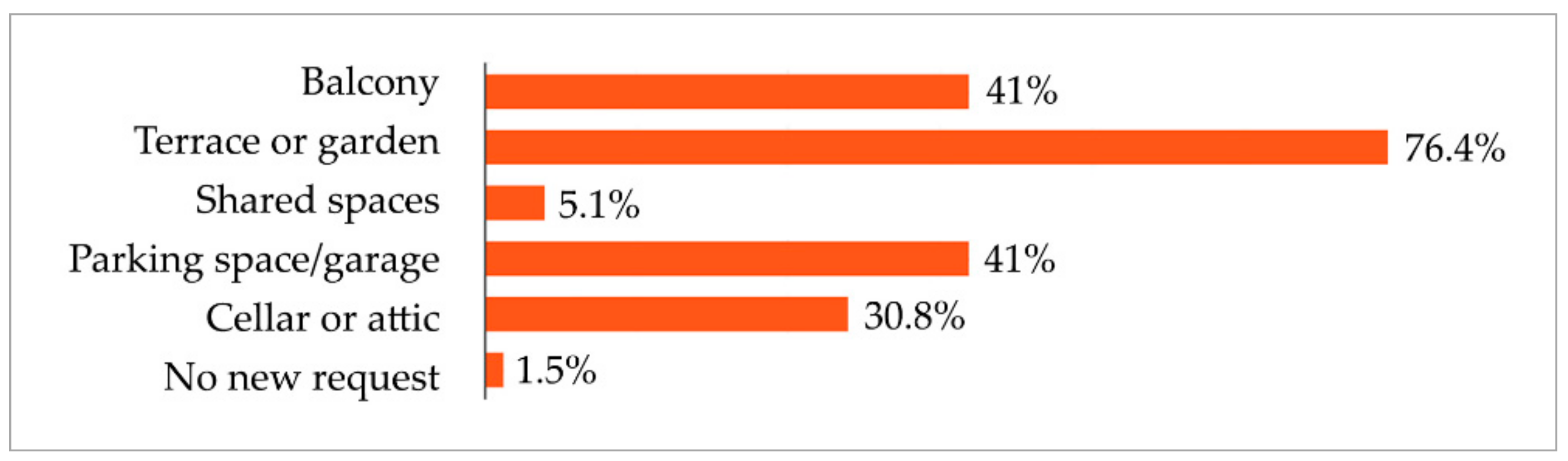

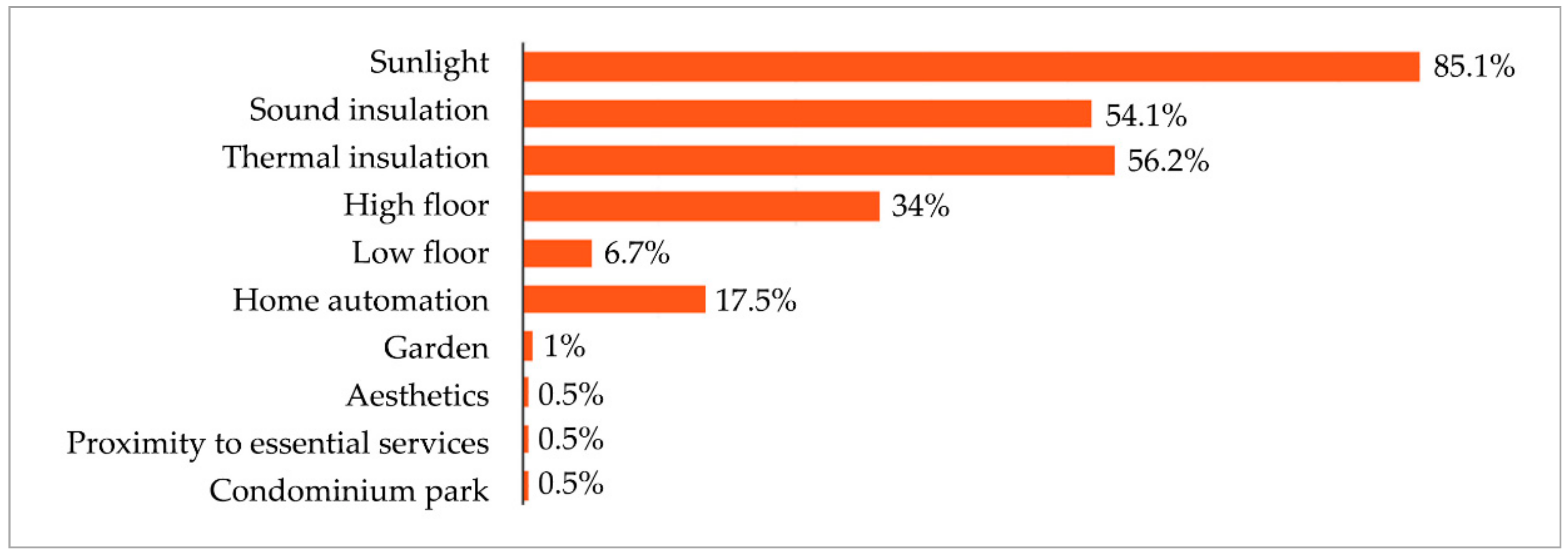

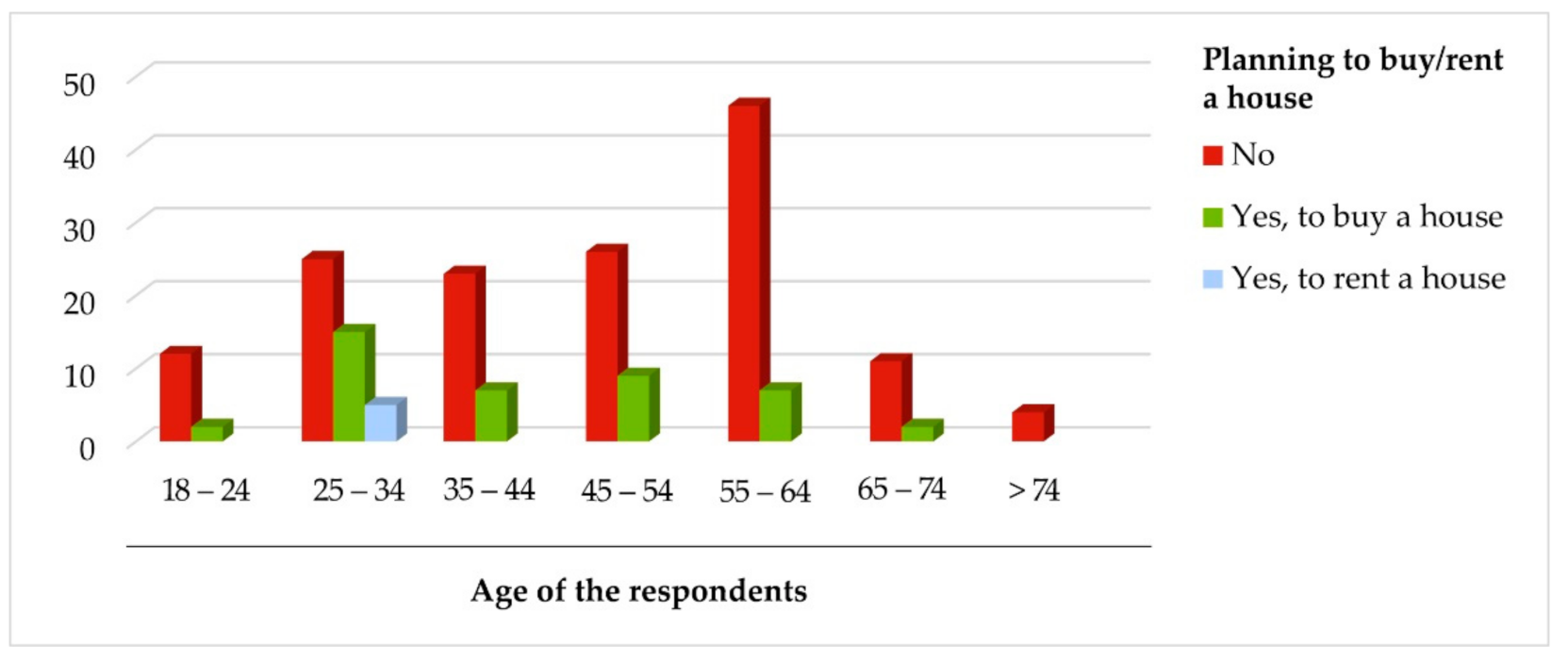

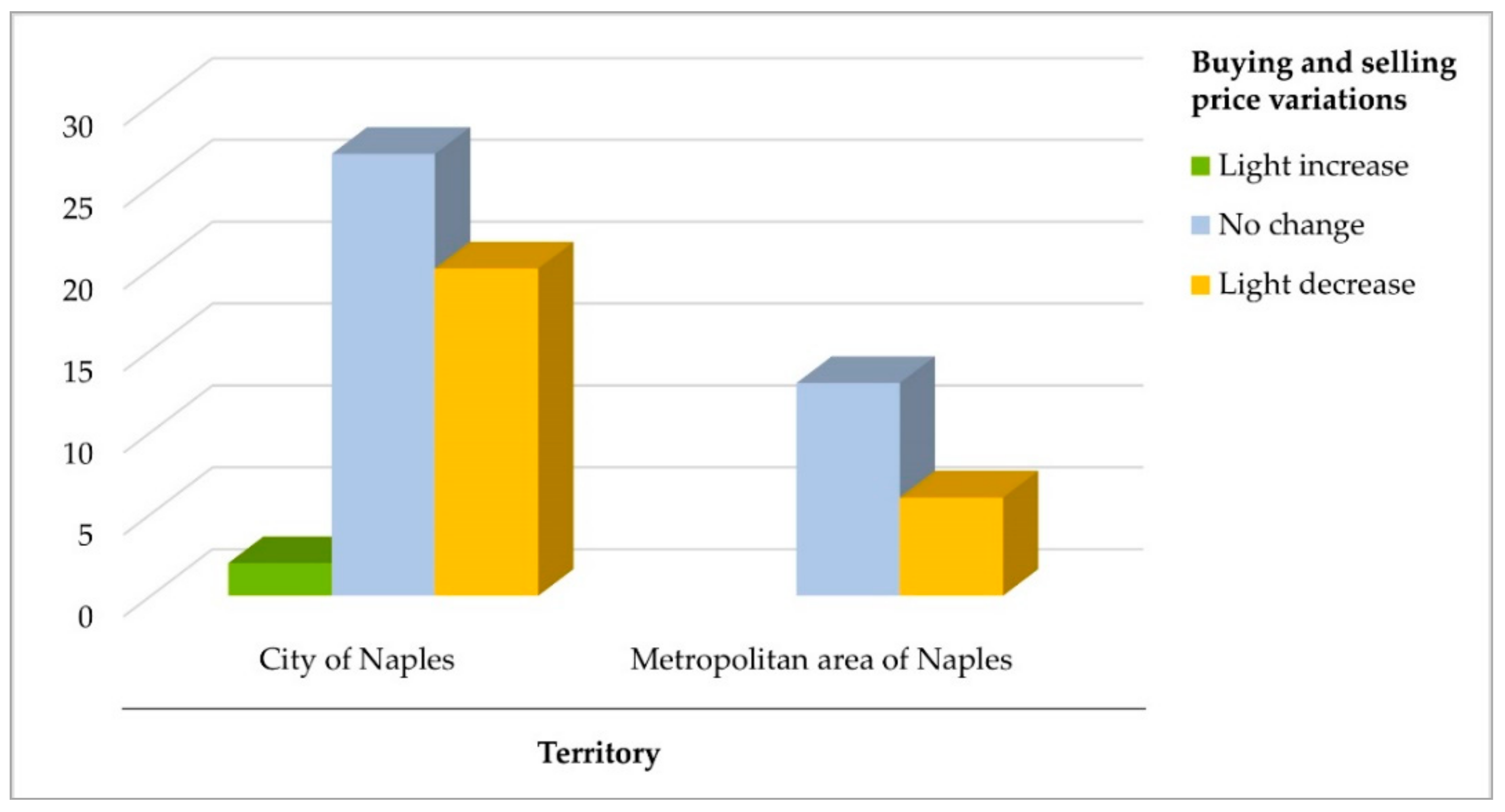

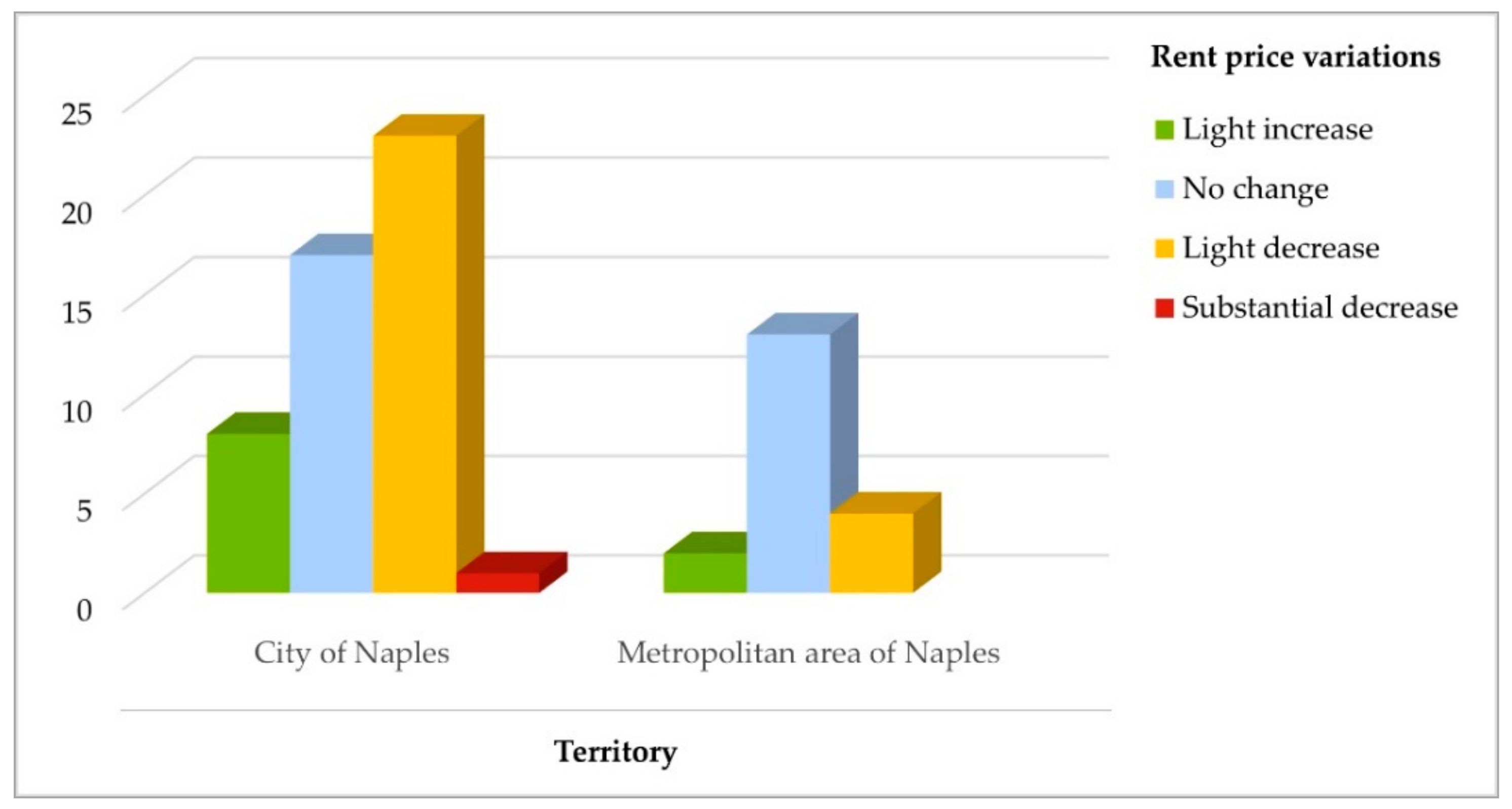

7.1. Results of the Community Questionnaire

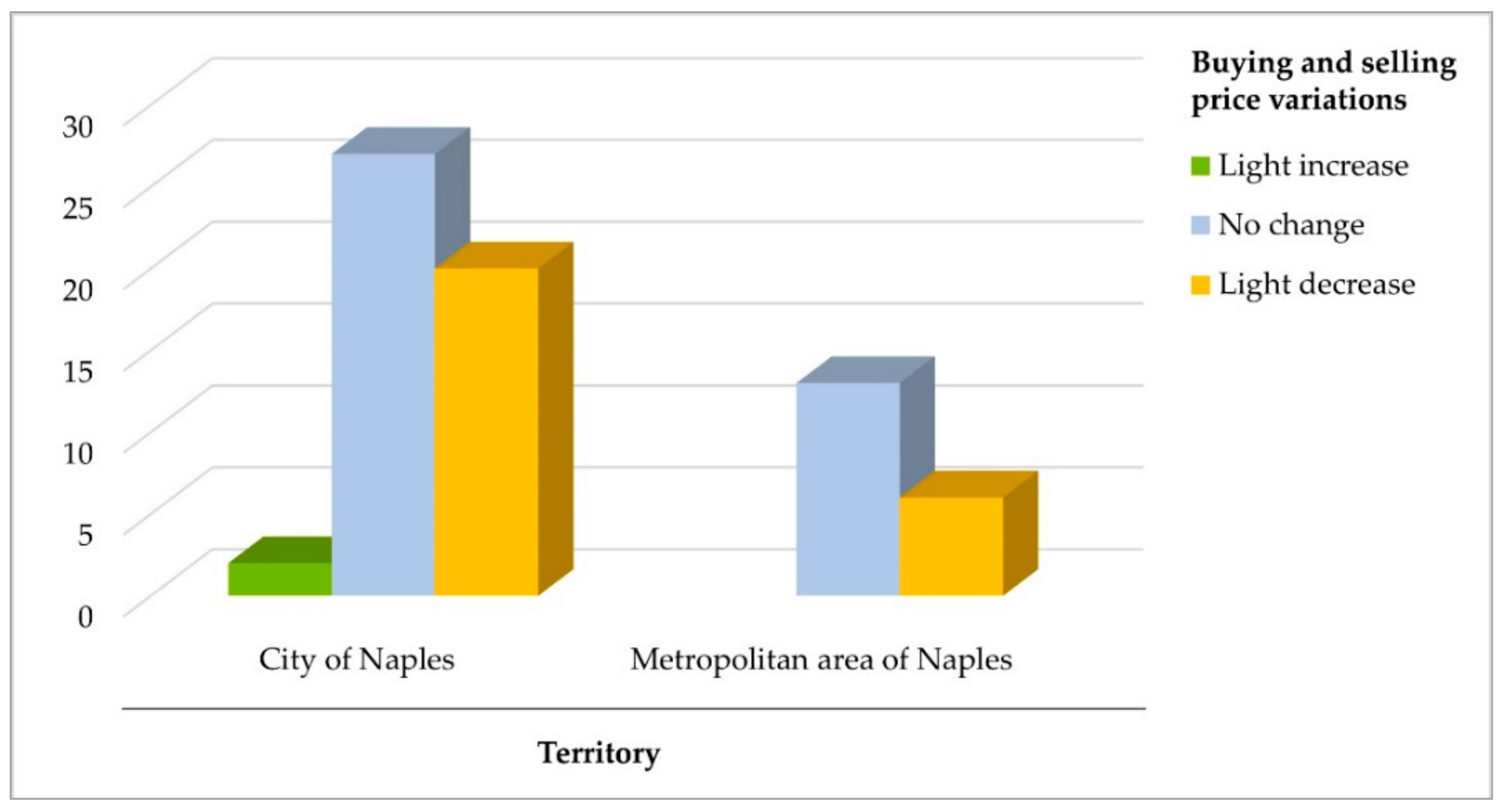

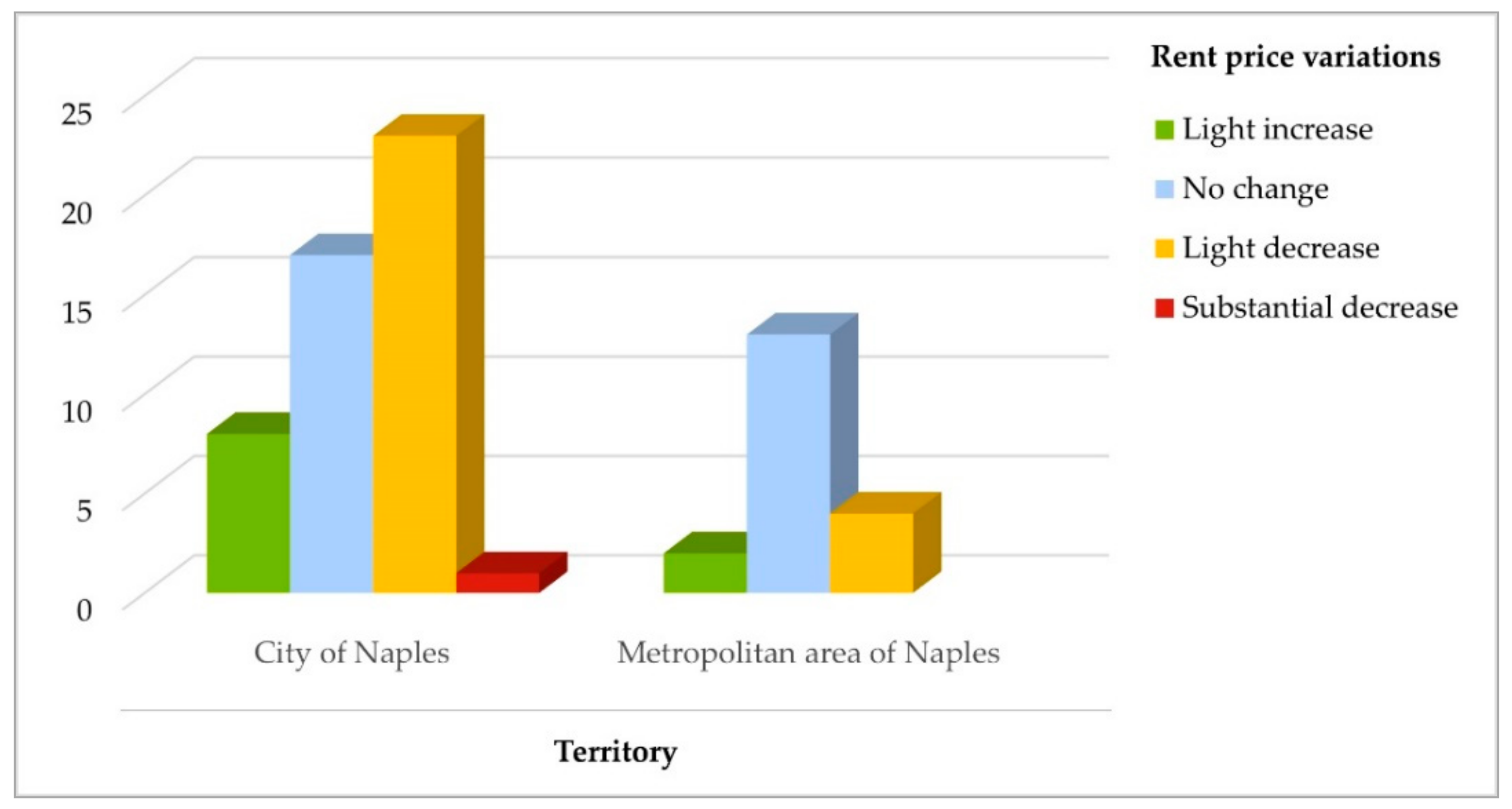

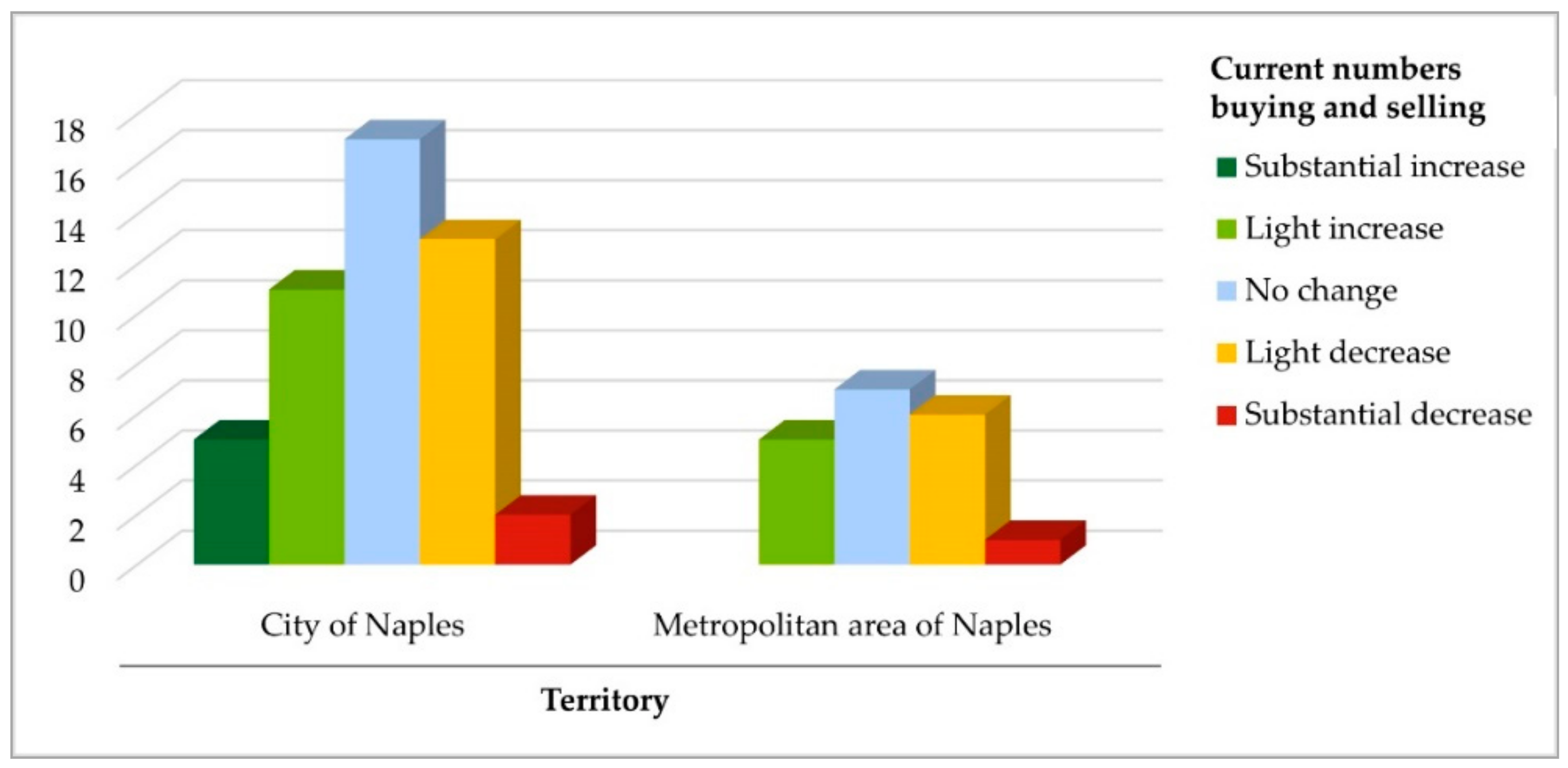

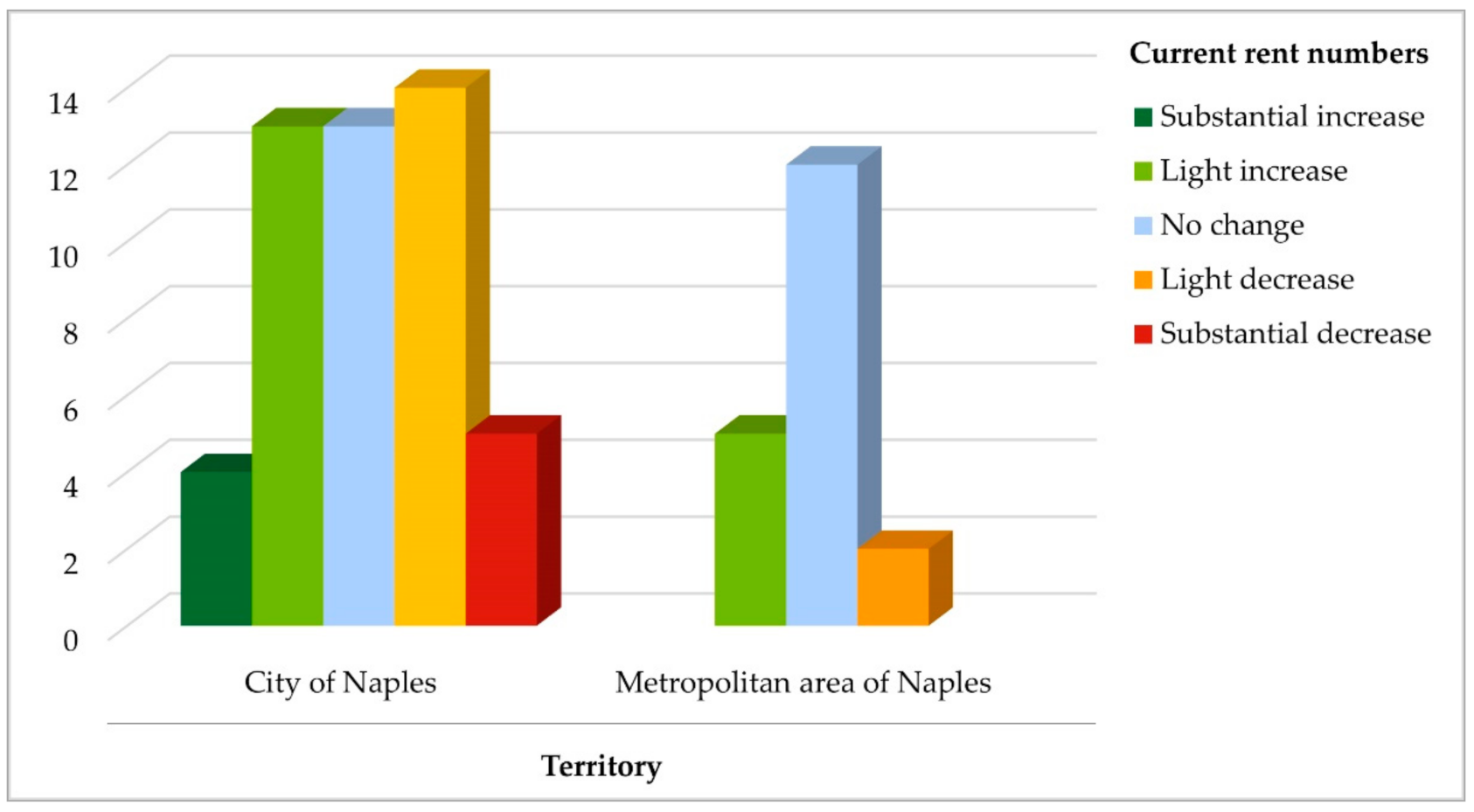

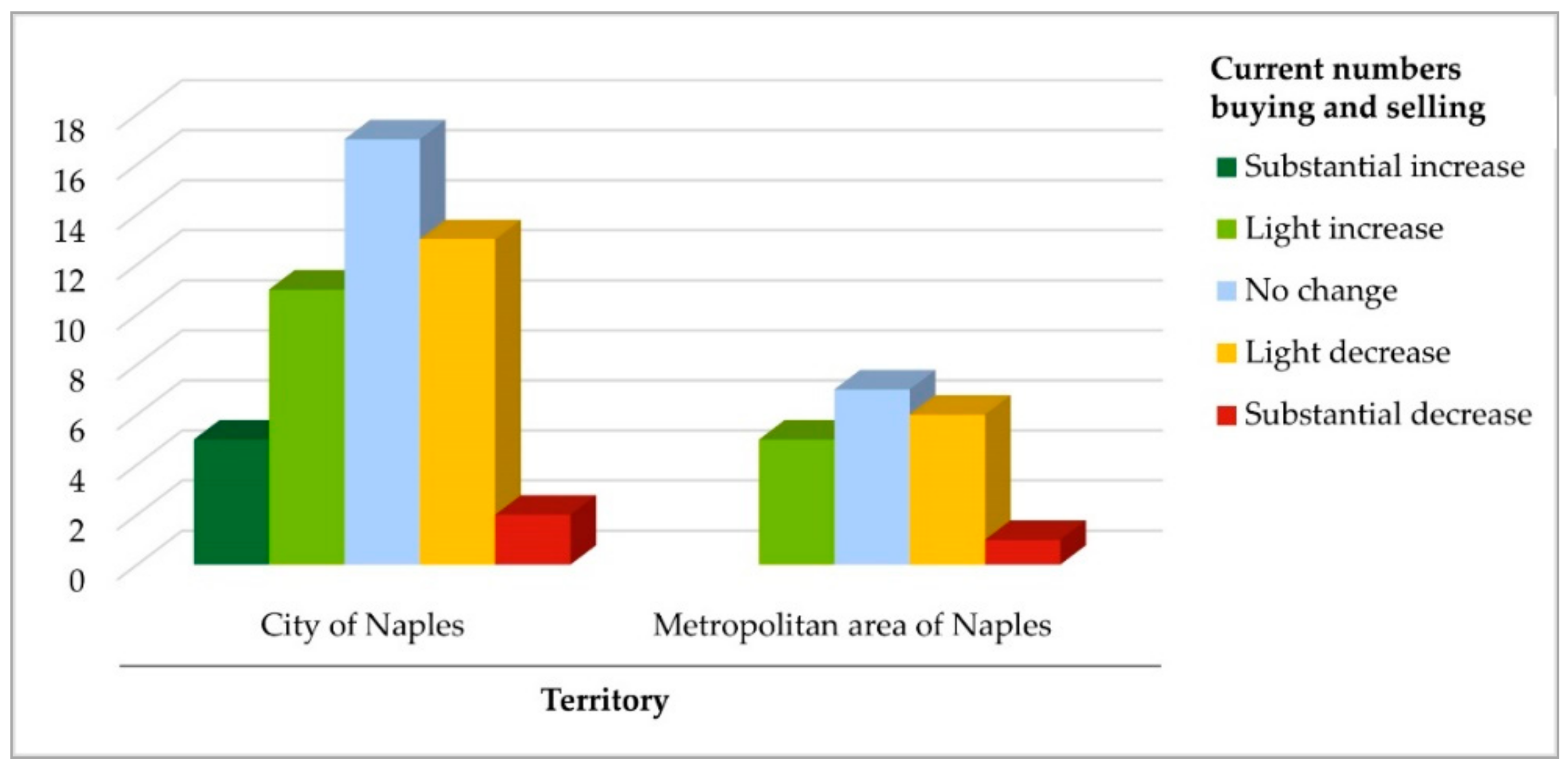

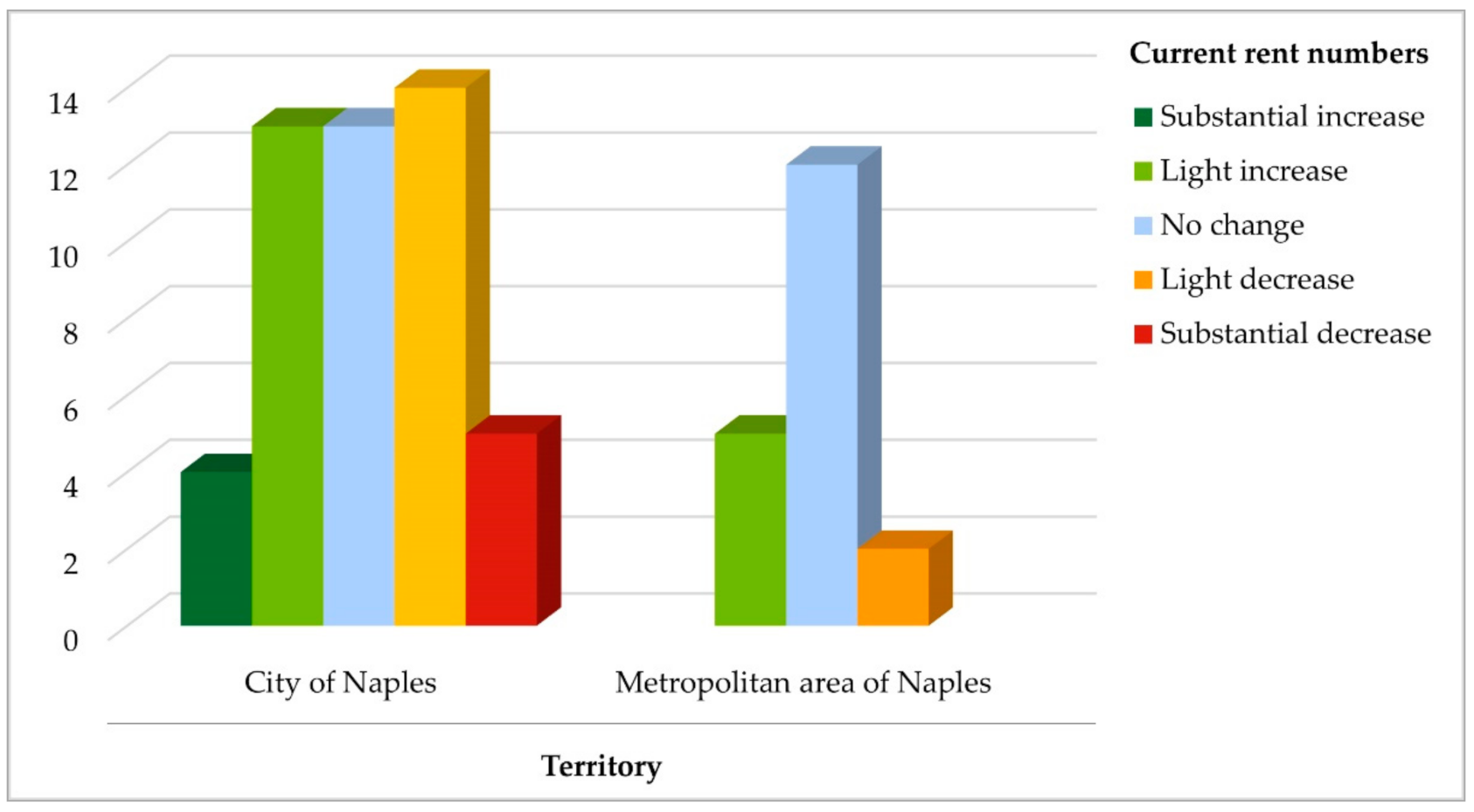

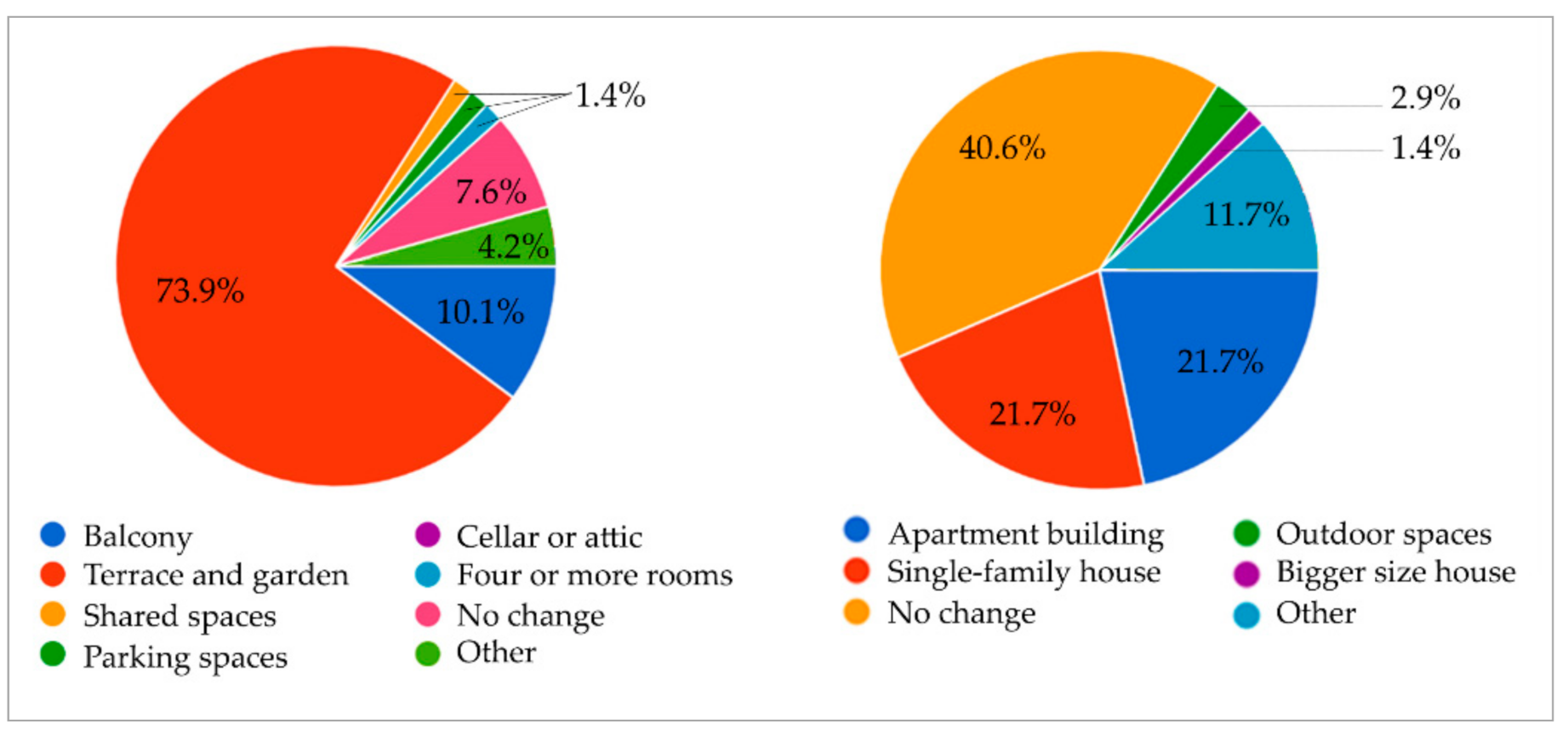

7.2. Results of the Questionnaire Distributed to the Real Estate Agents

8. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- World Health Organization. WHO Manifesto for a Healthy Recovery from COVID-19: Prescriptions and Actionables for a Healthy and Green Recovery; World Health Organization: Geneva, Switzerland, 2020. [Google Scholar]

- Tanrivermis, H. Possible impacts of COVID-19 outbreak on real estate sector and possible changes to adopt: A situation analysis and general assessment on Turkish perspective. J. Urban Manag. 2020, 9, 263–269. [Google Scholar] [CrossRef]

- Fusco Girard, L.; Nocca, F. Climate Change and Health Impacts in Urban Areas: Towards Hybrid Evaluation Tools for New Governance. Atmosphere 2020, 11, 1344. [Google Scholar] [CrossRef]

- Kholodilin, K.A. Housing Policies Worldwide during Coronavirus Crisis: Challenges and Solutions. Diw Focus 2020, 2. Available online: https://www.diw.de/de/diw_01.c.758176.de/publikationen/diw_focus/2020_0002/housing_policies_worldwide_during_coronavirus_crisis__challenges_and_solutions.html (accessed on 10 October 2020).

- Nicolaa, M.; Alsafib, Z.; Sohrabic, C.; Kerwand, A.; Al-Jabird, A.; Iosifidisc, C.; Aghae, M.; Aghaf, R. The socio-economic implications of the coronavirus pandemic (COVID-19): A review. Int. J. Surg. 2020, 78, 185–193. [Google Scholar] [CrossRef] [PubMed]

- Allen-Coghlan, M.; McQuinn, K.M. The Potential Impact of Covid-19 on the Irish Housing Sector. Int. J. Hous. Mark. Anal. 2020, in press. Available online: https://www.emerald.com/insight/conten (accessed on 10 October 2020).

- Sharifi, A.; Khavarian-Garmsir, A.R. The COVID-19 pandemic: Impacts on cities and major lessons for urban planning, design, and management. Sci. Total Environ. 2020, 749, 142391. [Google Scholar] [CrossRef] [PubMed]

- Bauman, Z. Modernità Liquida, 23rd ed.; Laterza: Roma-Bari, Italy, 2008. [Google Scholar]

- Dezza, P. Il Real Estate Chiede Misure anti Covid; IlSole24Ore: Milan, Italy, 1 May 2020. [Google Scholar]

- Santilli, G. Dal Covid la Città Arcipelago: Più Verde, più aria, Orari Liberi; IlSole24Ore: Milan, Italy, 24 September 2020. [Google Scholar]

- De Toro, P.; Gallo, R.; Gerundo, R.; Iodice, S.; Nocca, F. Standards perequation: New perspectives for the realization of services for the city. Sustain. Mediterr. Constr. 2020, 12, 125–131. [Google Scholar]

- González Pérez, J.M.; Piñeira Mantiñán, M.J. The unequal city in Palma (Majorca): Geography of confinement during the COVID-19 pandemic. Boletín Asoc. Geógrafos Españoles 2020. [Google Scholar] [CrossRef]

- Checa, J.; Martín, J.; López, J.; Nello, O. Los que no pueden quedarse en casa: Movilidad urbana y vulnerabilidad territorial en el área metropolitana de Barcelona durante la pandemia COVID-19. Boletín Asoc. De Geógrafos Españoles 2020. [Google Scholar] [CrossRef]

- Coronavirus: An Architect on How the Pandemic Could Change Our Homes Forever. Available online: https://theconversation.com/coronavirus-an-architect-on-how-the-pandemic-could-change-our-homes-forever-138649 (accessed on 15 January 2021).

- JLL Research & Strategy. COVID-19: Global Real Estate Implications, Paper II; Global Research: Hillsborough, UK, 20 April 2020; Available online: https://www.jll.it/it/tendenze-e-ricerca/research/covid-19-global-real-estate-implications (accessed on 13 November 2020).

- PricewaterhouseCoopers Advisory SpA (PwC). Impatti del COVID-19 sul Real Estate: Come Rispondere Rapidamente; London, UK, 2020; Available online: https://www.pwc.com/it/it/publications/assets/docs/PwC-Italia-Real-Estate-impatti-del-covid-19-Checkup.pdf (accessed on 13 November 2020).

- Engel & Völkers. Report sul Mercato Immobiliare Post COVID-19; Engel & Völkers Padova: Padova, Italy, 2020; Available online: https://www.engelvoelkers.com/it-it/padova/blog/report-sul-mercato-immobiliare-post-covid-19/ (accessed on 20 November 2020).

- Pickford, J. Coronavirus Fears Hit UK Property Market as Viewings Dry Up; Financial Times: London, UK, 17 March 2020; Available online: https://www.ft.com/content/e30ccb84-6799-11ea-800d-da70cff6e4d3 (accessed on 13 November 2020).

- Scenari Immobiliari. FUTU.RE Report, COVID-19 e l’impatto sul Mondo dei Servizi Immobiliari. June 2020. Available online: https://www.scenari-immobiliari.it/shop/futu-re-covid-19-elimpatto-sul-mondo-dei-servizi-immobiliari/ (accessed on 13 November 2020).

- Dezza, P. La Rigenerazione Urbana Potrà Essere il Motore Della Ripresa Post Covid-19; IlSole24Ore: Milan, Italy, 23 September 2020. [Google Scholar]

- Italian Federation of Professional Real Estate Agents (FIAIP). Osservatorio Immobiliare Nazionale Settore Urbano 2019; Italian Federation of Professional Real Estate Agents: Rome, Italy, 2019; Available online: https://ilmercatoimmobiliare.altervista.org/osservatorio-immobiliare-nazionale-settore-urbano-tra-crescita-nel-2019-e-le-conseguenze-dellemergenza-coronavirus/ (accessed on 13 November 2020).

- Real Estate Market Observatory (OMI). Rapporto Immobiliare 2019, il Settore Residenziale; Services Division, Estimation Services Central Management and Real Estate Market Observatory: Rome, Italy, 2019. Available online: https://www.agenziaentrate.gov.it/portale/documents/20143/263076/rapporto+immobiliare2019+ri_RI2019_Residenziale_20190523.pdf/a175f856-2363-dda7-da64-b1c0e544eb12 (accessed on 20 November 2020).

- Il Mercato delle Locazioni Residenziali—Continuano a Crescere i Canoni in Tutte le Grandi Città. Available online: https://www.aspesi-associazione.it/news.asp?idn=35727 (accessed on 20 November 2020).

- Locazione Come Scelta Abitativa in Forte Aumento. Available online: https://news.tecnocasagroup.it/ufficio-stampa/comunicati-stampa/mercato-nazionale-e-attualita/analisi-socio-demografica-locazioni-iisem2019/ (accessed on 5 October 2020).

- Statistical Office of the European Union (Eurostat). Housing Price Statistics: Newsrelease Euroindicators; European Commission: Brussels, Belgium, 2020; Available online: https://ec.europa.eu/eurostat/documents/portlet_file_entry/2995521/2-08042020-AP-EN.pdf/d624aabc-eca8-029c-868b-f80efec5b89a (accessed on 7 October 2020).

- Italian National Institute for Environmental Protection and Research (ISPRA). XIII Rapporto Qualità Dell’ambiente Urbano, 2017 ed.; Rome, Italy, 2017. Available online: https://www.isprambiente.gov.it/it/pubblicazioni/stato-dellambiente/xiii-rapporto-qualita-dell2019ambiente-urbano-edizione-2017 (accessed on 7 October 2020).

- Department for Regional Affairs and Autonomies (DARA). I Dossier Delle Città Metropolitane. Città Metropolitana di Napoli, 1st ed.; Naples, Italy, 2017; Available online: http://www.affariregionali.it/comunicazione/dossier-e-normativa/i-dossier-delle-citt%C3%A0-metropolitane/ (accessed on 12 October 2020).

- Metropolitan City of Naples. Piano Strategico della Città Metropolitana di Napoli. Available online: https://www.cittametropolitana.na.it/strategie (accessed on 12 October 2020).

- Italian National Institute of Statistic (ISTAT). Il Benessere Equo e Sostenibile in Italia. BES Report 2015; Italian National Institute of Statistic: Rome, Italy, 2015. [Google Scholar]

- Italian National Institute of Statistic (ISTAT). Il Benessere Equo e Sostenibile in Italia. BES Report 2019; Italian National Institute of Statistic: Rome, Italy, 2019. [Google Scholar]

- Fusco Girard, L.; Cerreta, M.; De Toro, P.; Nocca, F.; Poli, G.; Buglione, F.; Regalbuto, S.; Muccio, E.; Romano, F. L’Economia Circolare Nella Rigenerazione Delle Risorse Ambientali, Culturali e Paesaggistiche Delle Città Metropolitane portuali: Sfide, Strategie, Modelli di Valutazione; PRIN 2015 Research Report, University of Naples Federico II, Naples, Italy. Unpublished work. 2020. [Google Scholar]

- Italian Federation of Business Agents Mediators (FIMAA) of Naples. Quotazioni Metroquadro Napoli e Provincia; Real Estate Agents: Naples, Italy, 2019. [Google Scholar]

- Italian National Institute of Statistic (ISTAT). Edifici per Stato d’uso, in Censimento ISTAT; Italian National Institute of Statistic: Rome, Italy, 2011. [Google Scholar]

- Andamento dei Prezzi Degli Immobili Nella Provincia di Napoli. Available online: https://www.immobiliare.it/mercato-immobiliare/campania/napoli-provincia/ (accessed on 12 October 2020).

- De Falco, V. Nell’anno della pandemia da Covid-19 Fimaa resta la bussola del consumatore. In Quotazioni Metroquadro Napoli e Provincia; Real Estate Agents: Naples, Italy, November 2020. [Google Scholar]

- Osservatorio Immobiliare Nella Città Metropolitana di Napoli, Quotazioni Immobiliari e News sul Mercato Immobiliare Nella Città Metropolitana di Napoli. Available online: https://www.mercato-immobiliare.info/campania/napoli.html (accessed on 12 October 2020).

- Italian Federation of Business Agents Mediators (FIMAA) of Naples. Quotazioni Metroquadro Napoli e Provincia; Real Estate Agents: Naples, Italy, 2020. [Google Scholar]

- Naples Real Estate Exchange. Official Catalog; Chamber of Commerce, Industry, Crafts and Agriculture: Naples, Italy, 2009–2018. [Google Scholar]

- Jenks, G.F. The data model concept in statistical mapping. Int. Yearb. Cartogr. 1967, 7, 186–190. [Google Scholar]

- Mercato immobiliare, Tecnocasa: Nel 2019 compravendite in calo del 2.4% a Napoli. Available online: https://www.ildenaro.it/mercato-immobiliare-tecnocasa-nel-2019-compravendite-in-calo-del-24-a-napoli/ (accessed on 12 October 2020).

- Mercato immobiliare Napoli, II Semestre 2019. Available online: https://news.tecnocasagroup.it/ufficio-stampa/comunicati-stampa/mercato-immobiliare-locale/mercato-immobiliare-napoli-ii-semestre-2019/ (accessed on 12 October 2020).

- Osservatorio Immobiliare, per Nomisma Segnali di Ripresa dal 2022. Available online: https://www.idealista.it/news/immobiliare/residenziale/2020/11/25/151868-osservatorio-immobiliare-per-nomisma-segnali-di-ripresa-dal-2022 (accessed on 20 October 2020).

- Istat: Marcata Contrazione del Pil nel 2020, Ripresa Parziale nel 2021. Available online: https://www.ansa.it/sito/notizie/economia/2020/06/08/istat-marcata-contrazione-del-pil-nel-2020-ripresa-parziale-nel-2021_752c65ee-1e62-4426-9f51-4ae57cda4db6.html (accessed on 20 October 2020).

- Lovera, A. Sarà il Residenziale il Primo a Ripartire Nella Fase Post Covid; IlSole24Ore: Milan, Italy, 29 June 2020. [Google Scholar]

- Mercato Immobiliare Colpito, ma non Affondato. Available online: https://www.scenari-immobiliari.it/2020/05/13/mercato-immobiliare-colpito-ma-non-affondato/ (accessed on 20 October 2020).

- Real Estate Market Observatory (OMI). Rapporto Immobiliare 2020, il Settore Residenziale; Services Division, Estimation Services Central Management and Real Estate Market Observatory: Rome, Italy, 2020. Available online: https://www.agenziaentrate.gov.it/portale/web/guest/schede/fabbricatiterreni/omi/pubblicazioni/rapporti-immobiliari-residenziali (accessed on 20 October 2020).

- Marchesini, E. Per il Real Estate Rimbalzo nel 2021. Case, Prezzi In Calo; IlSole24Ore: Milan, Italy, 7 September 2020. [Google Scholar]

- Gabetti&Patrigest. Real Estate. I Trend Post Covid Settore per Settore; Gabetti Property Solutions: Milan, Italy, 2020; Available online: http://www.gabettigroup.com/it-it/ufficio-studi/dettaglio-tutti-i-report/artmid/1106/articleid/1001/real-estate-i-trend-post-covid-settore-per-settore-2020 (accessed on 13 October 2020).

- Mercato Immobiliare Dopo il Covid, le Previsioni dal 2020 al 2025. Available online: https://www.idealista.it/news/finanza/investimenti/2020/06/23/147090-mercato-immobiliare-dopo-il-covid-le-previsioni-dal-2020-al-2025 (accessed on 20 October 2020).

- Valutare Nell’incertezza. Un Modello Previsivo 2020–2025. Available online: https://www.scenari-immobiliari.it/2020/04/30/valutare-nellincertezza-un-modello-previsivo-2020-2025/ (accessed on 20 October 2020).

- Santilli, G. L’Ance Scommette sul Bazooka: Vale 6 Miliardi di Lavori; IlSole24Ore: Milan, Italy, 8 May 2020. [Google Scholar]

- Mobili, M. Superbonus 110%, le Regole Finali; IlSole24Ore: Milan, Italy, 4 July 2020. [Google Scholar]

- Santilli, G. Ecobonus 110%, Corsa al via. Cosa si può Fare e Come; IlSole24Ore: Milan, Italy, 15 May 2020. [Google Scholar]

- Italian Federation of Professional Real Estate Agents (FIAIP). “Sorpresa, l’immobiliare Regge. Richieste di Prima Casa a +15%”; LaStampa: Turin, Italy, 18 June 2020; p. 17. [Google Scholar]

- Dezza, P. Real Estate, la Rivoluzione Verde Prende Forma; IlSole24Ore: Milan, Italy, 15 May 2020. [Google Scholar]

- Degli Innocenti, N. Knight Frank Rivoluziona le Previsioni: Vienna e Lisbona Vincono sul Covid; IlSole24Ore: Milan, Italy, 6 May 2020. [Google Scholar]

- Covid e Mercato Immobiliare, le Previsioni di Nuveen Real Estate per l’Europa. Available online: https://www.idealista.it/news/finanza/investimenti/2020/05/11/140236-covid-e-mercato-immobiliare-le-previsioni-di-nuveen-real-estate-per-leuropa (accessed on 26 October 2020).

- Real Estate Market Observatory (OMI). Residenziale. Statistiche I trimestre 2020; Services Division, Estimation Services Central Management and Real Estate Market Observatory: Rome, Italy, 2020. Available online: https://www.agenziaentrate.gov.it/portale/documents/20143/262485/StatisticheOMI_RES_1_2020_20200605.pdf/3af07746-906c-45af-5853-da521605de03 (accessed on 9 November 2020).

- Gabetti. Residential Snapshot Q1 2020; Gabetti Property Solutions: Milan, Italy, 2020; Available online: http://www.gabettigroup.com/it-it/ufficio-studi/dettaglio-tutti-i-report/artmid/1106/articleid/996/residential-snapshot-q1-2020 (accessed on 9 November 2020).

- Italian National Institute of Statistic (ISTAT). Prezzi Delle Abitazioni. II Trimestre 2020; Italian National Institute of Statistic: Rome, Italy, 2020; Available online: https://www.istat.it/it/files//2020/09/CS-abitazioni-Q22020.pdf (accessed on 10 November 2020).

- Il Mattone Batte il Virus, Nonostante il clima Economico Negativo. Available online: https://www.aspesi-associazione.it/news.asp?idn=35781 (accessed on 12 November 2020).

- Mercato Immobiliare Italiano Post Covid-19: La voglia di Acquistare casa non Viene Meno. Available online: https://www.lavoripubblici.it/news/2020/07/STIME-E-IMMOBILI/24048/Mercato-immobiliare-italiano-post-Covid-19-La-voglia-di-acquistare-casa-non-viene-meno (accessed on 12 November 2020).

- Gli Effetti del Lockdown si Fanno Sentire. Available online: https://news.tecnocasagroup.it/ufficio-stampa/comunicati-stampa/mercato-nazionale-e-attualita/compravendite-residenziali-primo-trimestre-2020/ (accessed on 12 November 2020).

- Cavestri, L. Università, la Partenza Incerta fa Tremare il Mercato Degli Affitti; IlSole24Ore: Milan, Italy, 30 August 2020. [Google Scholar]

- Lovera, A. Affitti per Studenti, il 43% dei Proprietari Pronto allo Sconto; IlSole24Ore: Milan, Italy, 14 September 2020. [Google Scholar]

- Dezza, P. Affitti Brevi Torna l’incubo Covid; IlSole24Ore: Milan, Italy, 24 September 2020. [Google Scholar]

- Prezzi e Locazioni Immobiliari, Cosa è Cambiato con il Covid. Available online: https://www.idealista.it/news/immobiliare/residenziale/2020/07/27/149791-prezzi-e-locazioni-immobiliari-cosa-e-cambiato-con-il-covid (accessed on 12 November 2020).

- Deganello, S. Ecco la Casa Ibrida, Pronta a Tutti gli usi; IlSole24Ore: Milan, Italy, 17 May 2020. [Google Scholar]

- LaRepubblicaEconomia. Lockdown, Caccia alla casa Vacanze. I prezzi Vantaggiosi Spingono le Vendite; LaRepubblica: Rome, Italy, 28 December 2020. [Google Scholar]

- Leone, C. L’impatto della pandemia da Covid-19 nel mercato del credito alle famiglie. In Quotazioni Metroquadro Napoli e Provincia; Real Estate Agents: Naples, Italy, November 2020. [Google Scholar]

- Italian Association of Real Estate Development and Property Companies (ASPESI). Nota Mensile n. 2–Maggio 2020. Available online: http://www.aspesi-associazione.it/public/files/2020/Centro-Studi-FIAIP-nota-congiunturale_-maggio-2020.pdf (accessed on 16 November 2020).

- Santilli, G. Superbonus 110%, gli Interventi Crescono con più Proprietari; IlSole24Ore: Milan, Italy, 8 May 2020. [Google Scholar]

- IlSole24Ore. L’immobiliare ai Tempi del Covid. Così Tempocasa ce l’ha Fatta; IlSole24Ore: Milan, Italy, 30 August 2020. [Google Scholar]

- Lovera, A. Il proptech non si Ferma Neanche con il Covid; IlSole24Ore: Milan, Italy, 4 May 2020. [Google Scholar]

- Marrazzo, D. Un po’ Palcoscenico, Palestra e Altare: Quanta Nuova vita c’è su Tetti e Terrazzi; IlSole24Ore: Milan, Italy, 31 August 2020. [Google Scholar]

- Pike, J. The Future of Sustainable real Estate Investments in a Post-COVID-19 World. J. Eur. Real Estate Res. 2020, in press. Available online: https://www.researchgate.net/publication/343291835_The_future_of_sustainable_real_estate_investments_in_a_post-COVID-19_world (accessed on 19 November 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

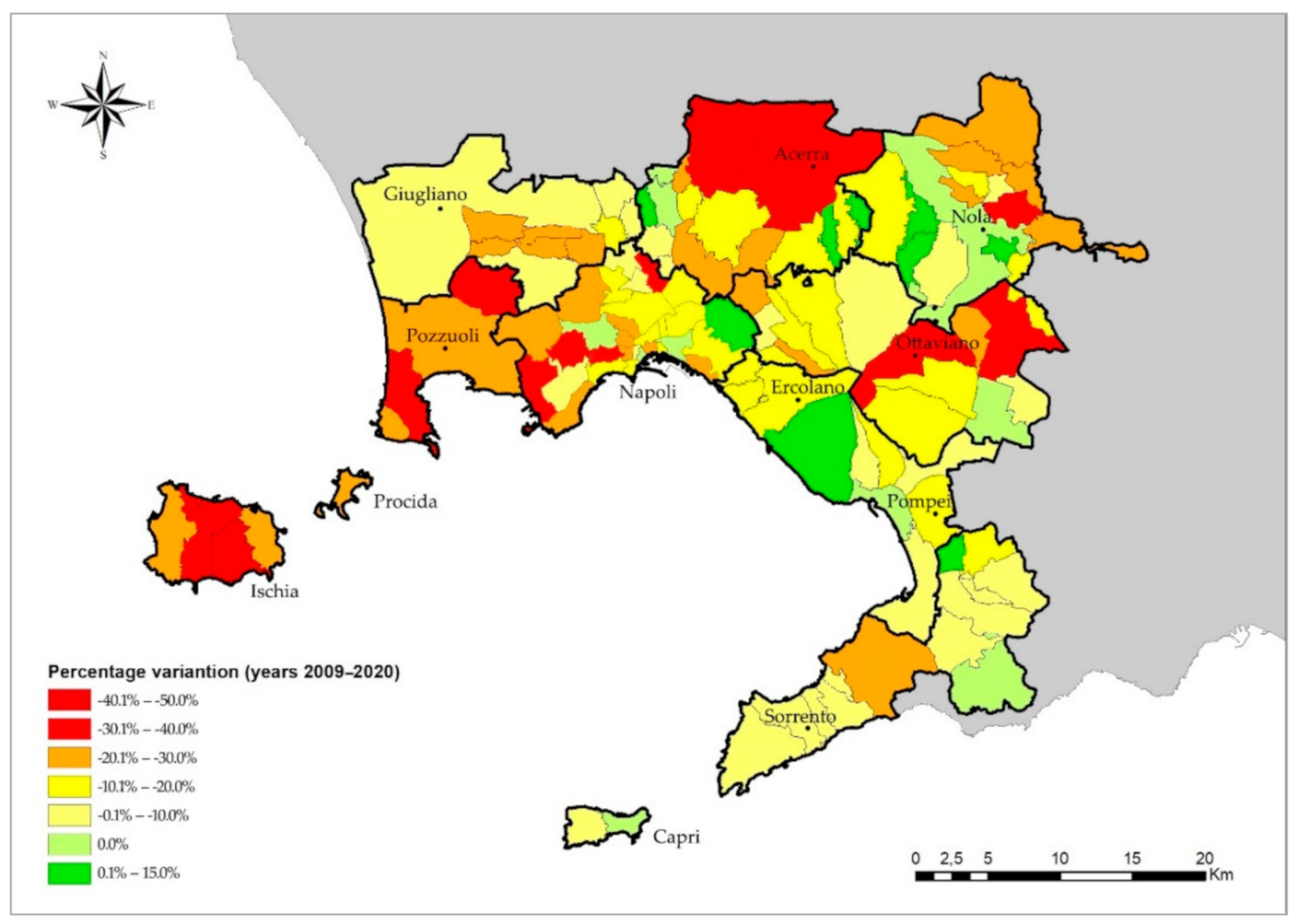

| Macro-Areas | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | Variation 2009–2020 (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Area 1 | 1530 | 1490 | 1580 | 1577 | 1461 | 1426 | 1332 | 1208 | 1191 | 1193 | 1203 | 1163 | −23.97 |

| Area 2 | 2710 | 2720 | 2628 | 2393 | 2230 | 2070 | 1935 | 1883 | 1825 | 1825 | 1660 | 1633 | −39.76 |

| Area 3 | 2924 | 3045 | 3056 | 2828 | 2731 | 2604 | 2535 | 2450 | 2381 | 2366 | 2145 | 2082 | −29.01 |

| Area 4 | 1426 | 1504 | 1508 | 1488 | 1425 | 1377 | 1353 | 1276 | 1271 | 1259 | 1153 | 1134 | −20.51 |

| Area 5 | 1089 | 1125 | 1149 | 1090 | 1053 | 1016 | 1017 | 979 | 911 | 911 | 963 | 851 | −21.86 |

| Area 6 | 1494 | 1500 | 1865 | 1421 | 1344 | 1276 | 1264 | 1274 | 1231 | 1245 | 1179 | 1087 | −27.22 |

| Area 7 | 2049 | 2029 | 1925 | 1862 | 1840 | 1743 | 1701 | 1679 | 1622 | 1605 | 1665 | 1670 | −18.50 |

| Area 8 | 3031 | 2962 | 2754 | 2633 | 2812 | 2717 | 2608 | 2505 | 2532 | 2520 | 2552 | 2535 | −16.35 |

| Area 9 | 5260 | 4958 | 4630 | 4388 | 5072 | 4873 | 4473 | 4320 | 4122 | 4101 | 3941 | 3769 | −28.34 |

| Metropolitan area | 2134 | 2111 | 2107 | 1961 | 2002 | 1921 | 1840 | 1775 | 1729 | 1724 | 1690 | 1628 | −23.73 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

De Toro, P.; Nocca, F.; Buglione, F. Real Estate Market Responses to the COVID-19 Crisis: Which Prospects for the Metropolitan Area of Naples (Italy)? Urban Sci. 2021, 5, 23. https://doi.org/10.3390/urbansci5010023

De Toro P, Nocca F, Buglione F. Real Estate Market Responses to the COVID-19 Crisis: Which Prospects for the Metropolitan Area of Naples (Italy)? Urban Science. 2021; 5(1):23. https://doi.org/10.3390/urbansci5010023

Chicago/Turabian StyleDe Toro, Pasquale, Francesca Nocca, and Francesca Buglione. 2021. "Real Estate Market Responses to the COVID-19 Crisis: Which Prospects for the Metropolitan Area of Naples (Italy)?" Urban Science 5, no. 1: 23. https://doi.org/10.3390/urbansci5010023

APA StyleDe Toro, P., Nocca, F., & Buglione, F. (2021). Real Estate Market Responses to the COVID-19 Crisis: Which Prospects for the Metropolitan Area of Naples (Italy)? Urban Science, 5(1), 23. https://doi.org/10.3390/urbansci5010023