Beyond Bitcoin: A Critical Look at Blockchain-Based Systems

Abstract

:1. Introduction

2. Current and Potential Applications

2.1. Smart Properties

2.1.1. Proof of Existence

2.1.2. Everledger

2.2. Smart Contracts

2.2.1. Namecoin

2.2.2. Ethereum

2.3. Decentralized Autonomous Organizations

2.3.1. Storj

2.3.2. ADePT

- Ethereum, in order to allow devices to understand contracts and capabilities (this is where blockchain technology comes into play);

- Telehash [37], a private messaging protocol used to share information among two or more devices;

- Bit Torrent [38] a file sharing protocol used to move data around also in case of discontinuous and unreliable connections.

2.4. Other Possible Application Fields

2.4.1. eScience

2.4.2. Healthcare

2.4.3. Financial Services

- In the scope of loans, usually banks along with credit scoring and rating firms assist in the issuance of mortgages, bonds, securities, etc. On the blockchain, anyone could check creditworthiness before issuing, trading and settling traditional debt instruments directly from peers.

- Blockchain cuts the settlement period on transactions from days to hours or minutes. The adoption of such tool in trading could reduce the post-trade processing such as settlement and reconciliation, which would eventually result in cost reduction.

- Each financial institution maintains its own ledgers for its assets (often product and/or region specific), which implies a multiplication of registers among parts. The reconciliation process of these ledgers is costly especially in the case of large banks, and software solutions often rely upon coding languages as awkward and primitive as Visual Basic for Applications (VBA). This results in human error, inefficiencies and therefore a decreased ability to manage risk. Creating databases among financial institutions resting upon a blockchain, could reduce these frictions.

- Smart contracts have the potential to automate existing logic in contracts which have multiple payment strands. As the majority of financial assets exist only in electronic form, many products could be governed by smart contracts.

- Compliance with regulation is costly, and a regulator enabled to view a transparent ledger shared by the financial services industry could drastically reduce the cost of Anti Money Laundering and fighting against terrorism financing.

3. Concepts and Technologies

3.1. Bitcoin Quick Overview

- keeps a copy of the ledger recording transfers related to digital coins/assets over time;

- performs a certain amount of publicly-verifiable computational work in order to have a chance to be rewarded in new mint coins plus some fees by the payers;

- checks the work performed by other participants in order to get more chances to be rewarded in the future.

- Miners collect transactions that are broadcast over the network, and use their computing power to try to generate a valid block of transactions. The generation is done through repeated invocation of a hash function on data which reference the specific transactions that a miner decided to include in its block, together with the previous valid block and its own Bitcoin address. (Since Bitcoin inception, the hash function has been implemented with a double call to the SHA-256 algorithm [48]. However, as the requirement of collision resistance is quickly hardening with the diffusion of Bitcoin and the introduction of the new hash standard SHA-3 [49], this could change in a near future.)

- When a miner succeeds in generating a block, meaning that the hash of its block data is smaller than a given difficulty threshold (aka target), then it broadcasts such block to the network.

- In case other miners see that the above block is valid, and see that it is the “longest extension” of the blockchain (i.e., the fork involving the highest amount of computational effort) that they are aware of, they move on and extend the blockchain from such block.

- The existence of the above block in the blockchain ratifies that the newly minted coins and the fees from the transactions included go to the public address that it provided. Only the miner having that address can redeem such coins and transaction fees, by using its corresponding private key.

- The difficulty level readapts to the total hashing power of the miners. This is done by updating the hash threshold value every 2016 blocks, so that so many blocks get generated in about two weeks (i.e., each new block is generated every 10 min on average).

- The reward in newly minted coins started at 50 coins in January 2009 and halves every 210,000 blocks, i.e., about every 4 years (see above).

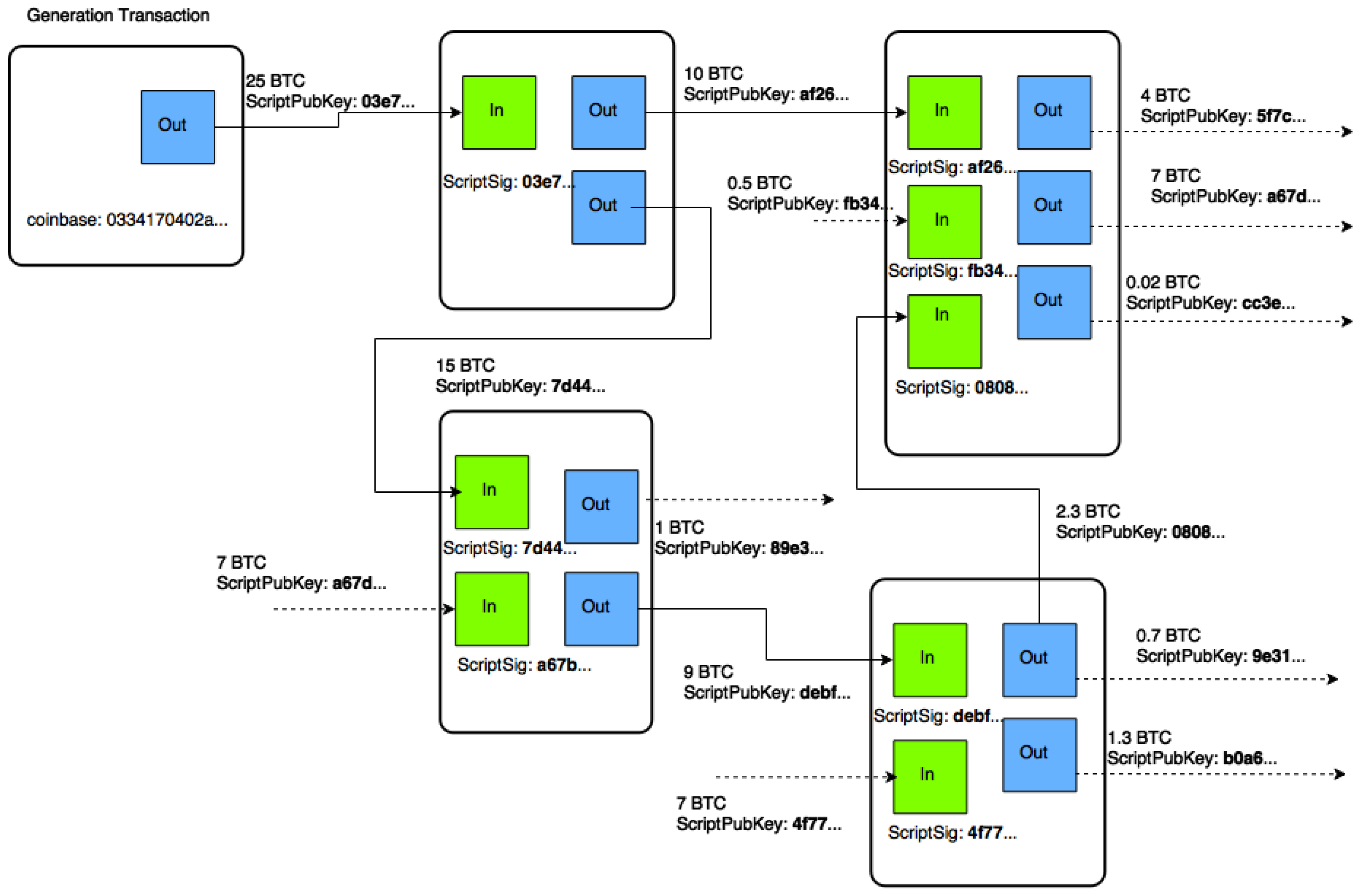

3.2. Transactions

3.2.1. Addressing

3.2.2. Transaction Inputs and Outputs

- -

- is the SHA-256 digest of a previous transaction . It is used to identify as the transaction used to get input I;

- -

- the input index i is a non negative integer which indicates the specific output in used as an input in the current transaction T;

- -

- the signing script SgnCode is a set of instructions and data provided by the transactor in order to satisfy the conditions placed in the pubkey script of output i in . In its simplest form, such script just applies the transactor signature on the SHA-256 digest of all the I/O fields of the current transaction, with the exclusion of SgnCode itself;

- -

- the output value v is the number of satoshis associated with O;

- -

- the pubkey script VrfCode is a set of instructions and data provided by the transactor that specifies the recipient(s) authorized to collect the value v in satoshi associated with O. The most used VrfCode returns true if matched with a signing script consisting in a signature of a (subsequent) transaction (see Section 3.2.3).

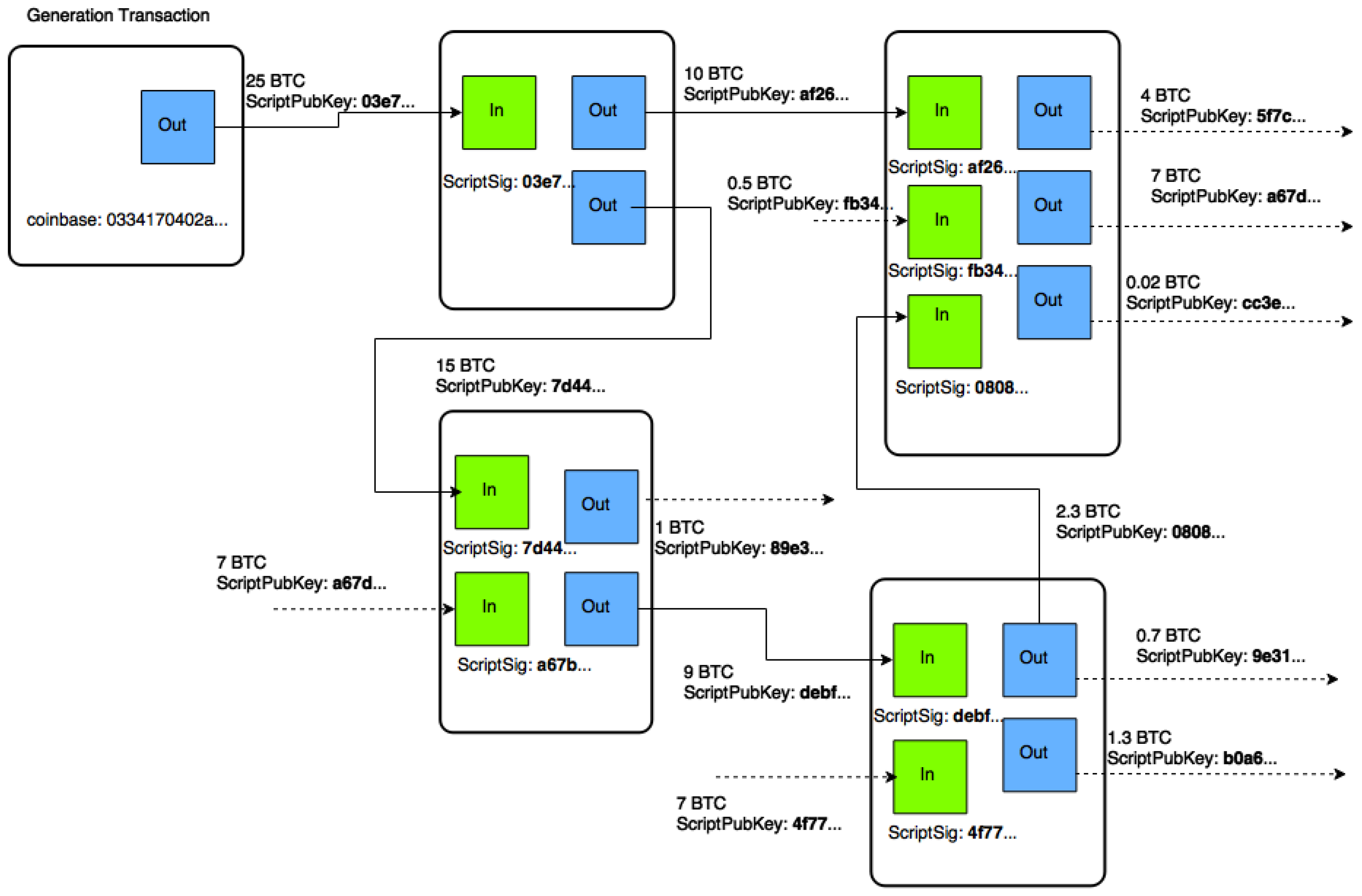

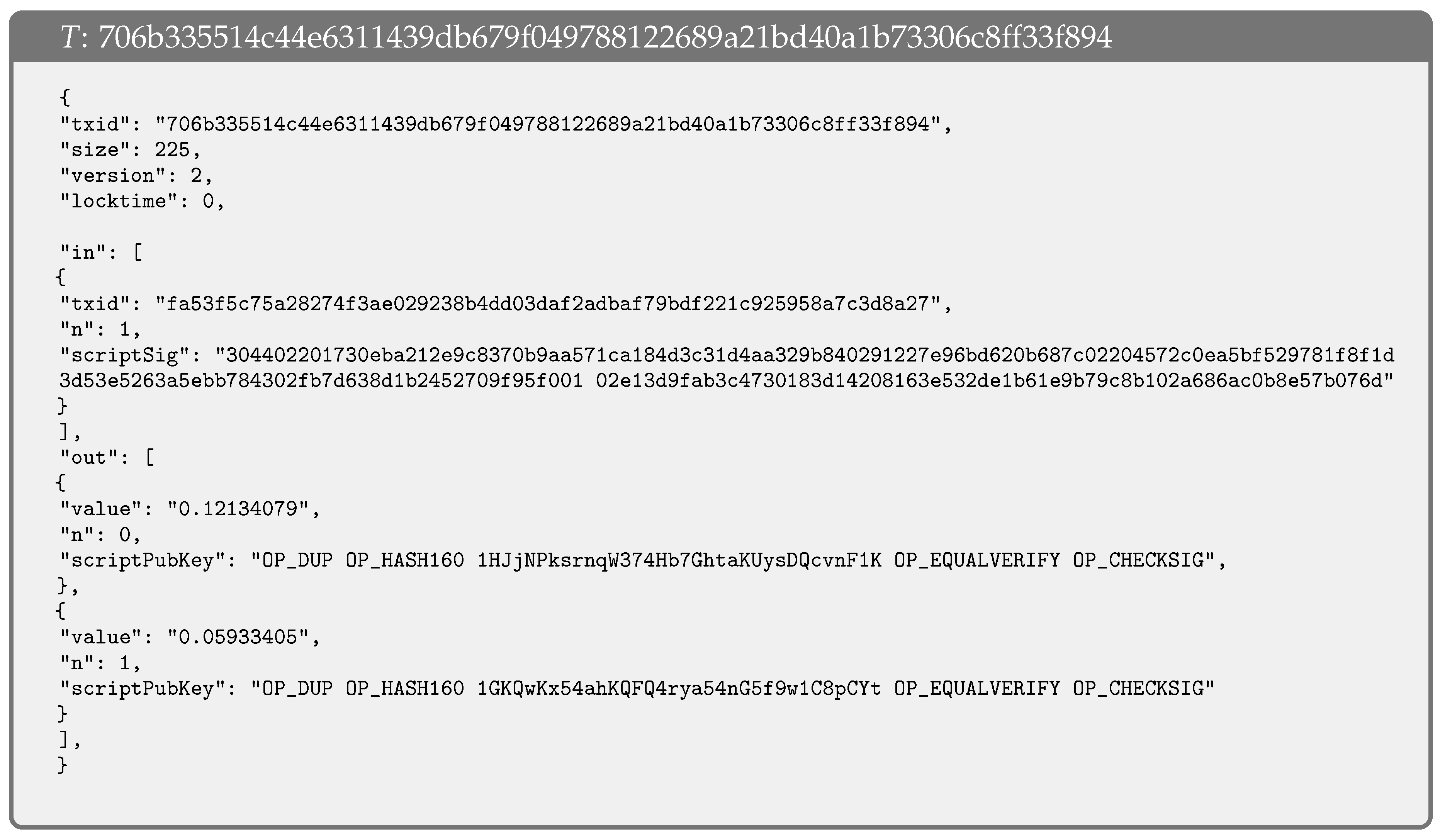

3.2.3. Transaction Processing

- the out section of T is created by instantiating the two value fields and by putting the addresses 1HJjNP... and 1GKQwK... after the OP_HASH160 instruction in their related scriptPubKey fields;

- the previous output (txid=fa53f5...,n=1) is indicated as the source of the input in the in section;

- P completes the encoding of T by writing in the scriptSig field its signature 304402... followed by a space and its public key 02e13d.... It can be worthwhile to notice that P’s signature is applied to all the in and out fields of T, with the only exception of scriptSig.

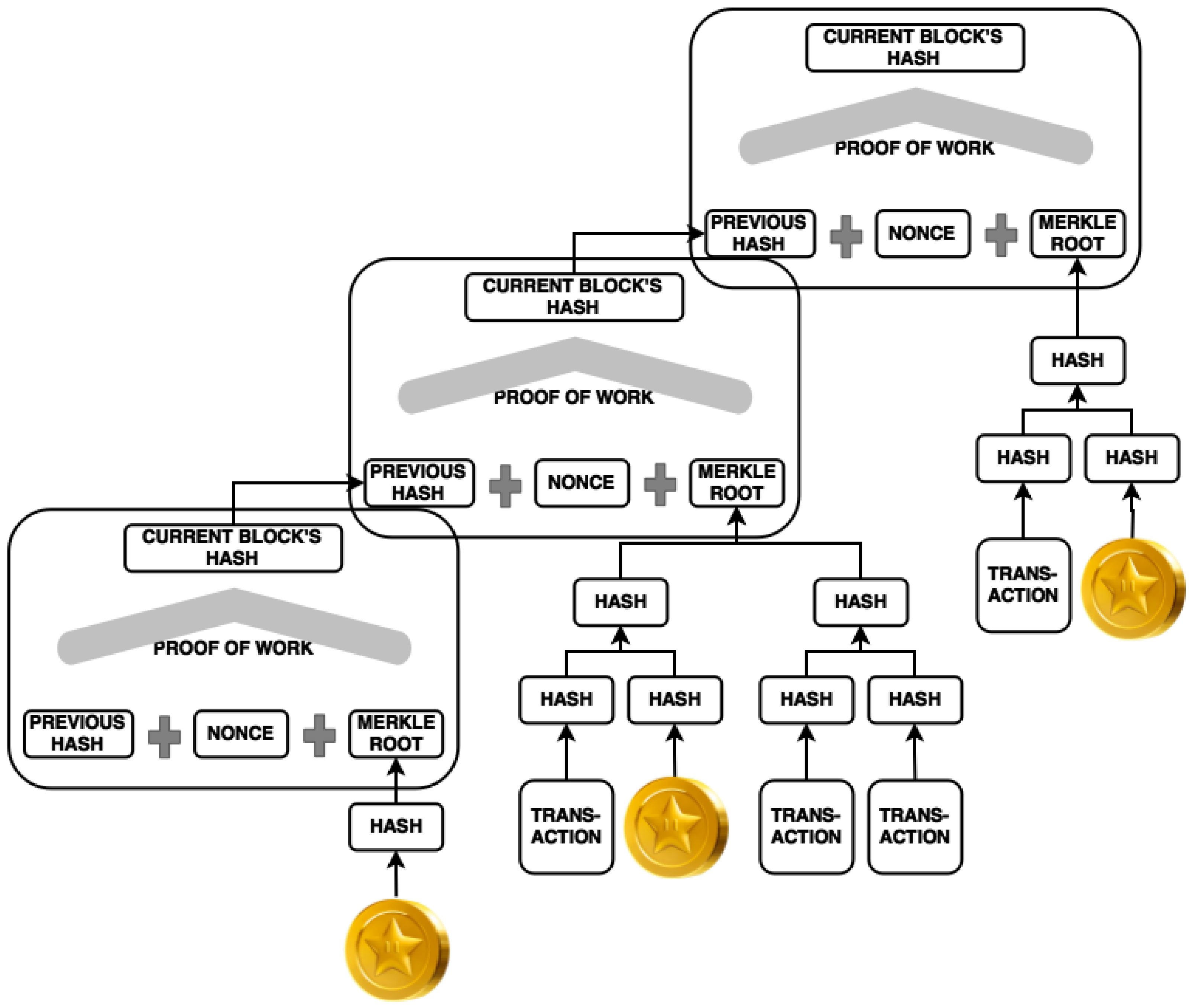

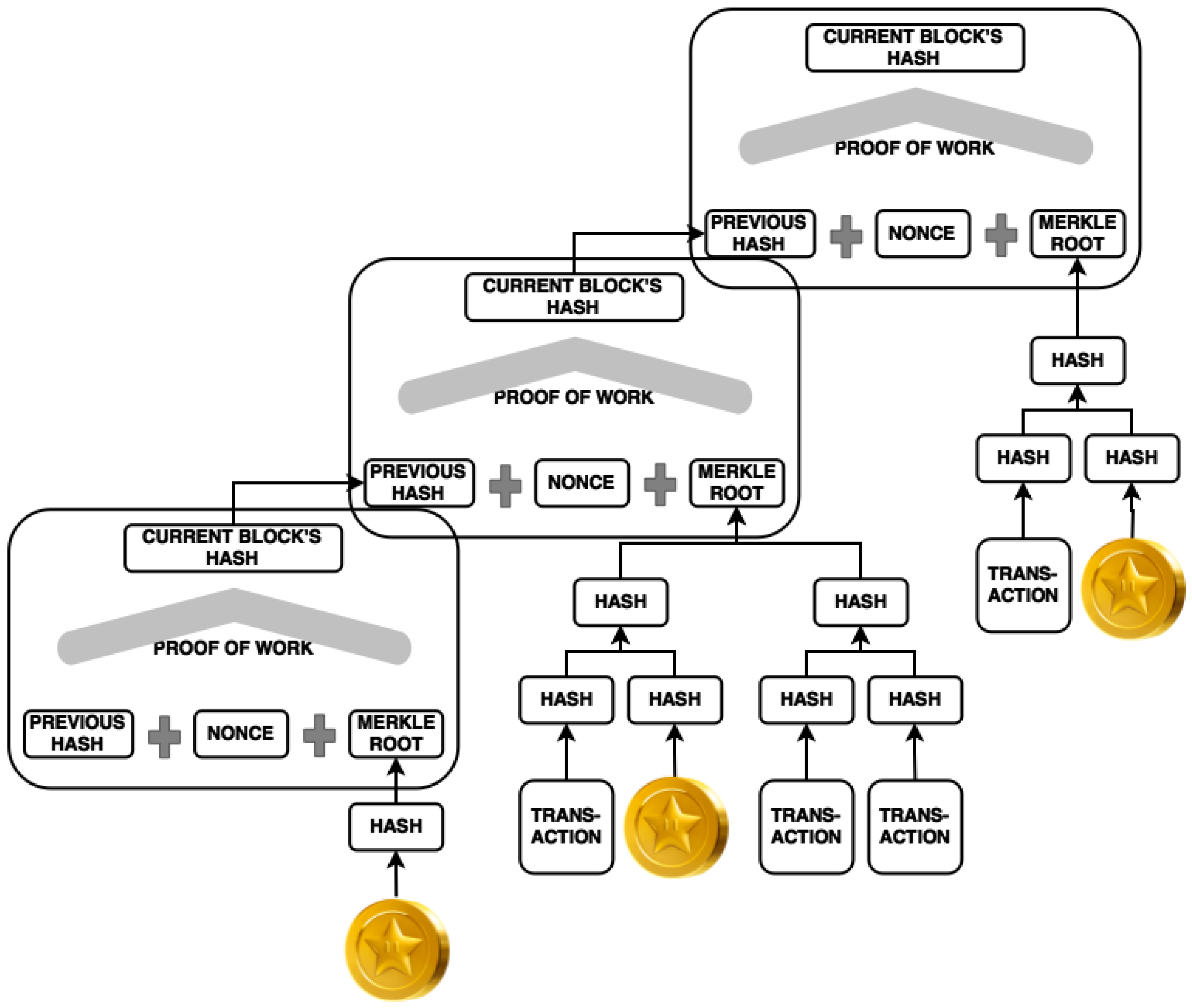

3.3. The Blockchain Technology

- Collecting incoming transactions into new blocks;

- Mining of new blocks;

- Blockchain updating.

3.3.1. Collecting New Transactions into Blocks

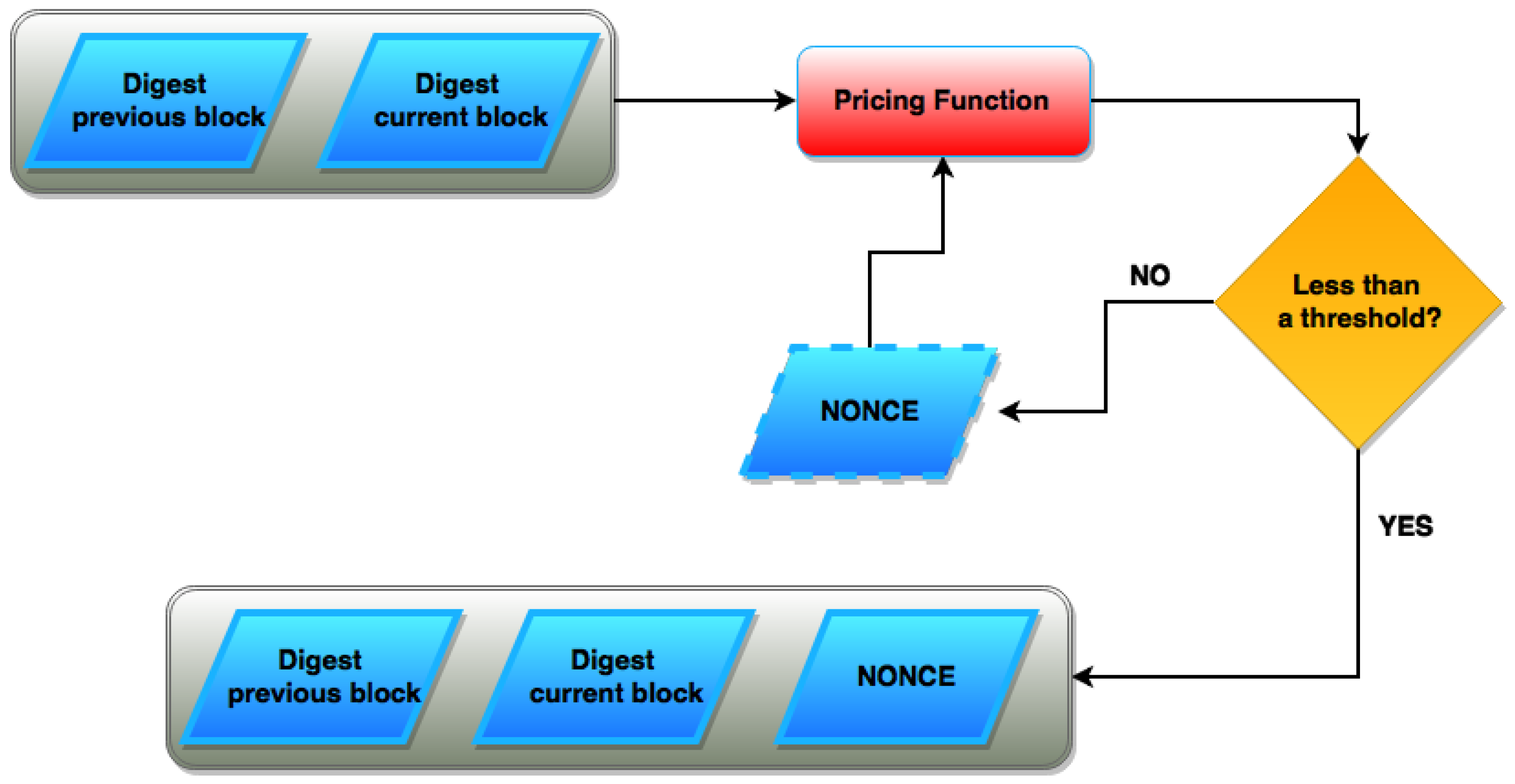

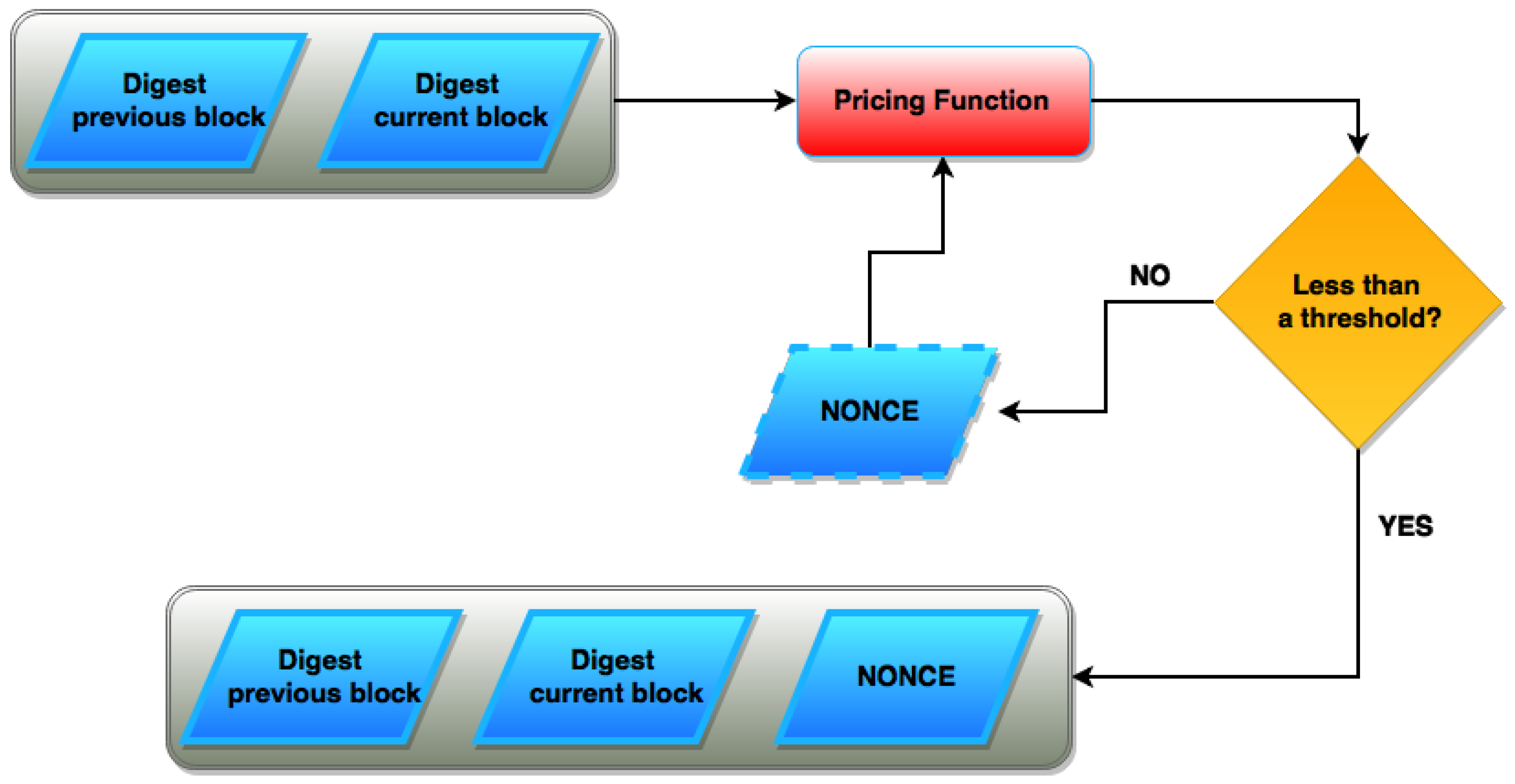

3.3.2. Mining of New Blocks

- the fastest sequential algorithm for computing requires an amount of memory roughly proportional to the number of operations to be performed;

- it is impossible for a parallel algorithm to asymptotically achieve a significantly lower cost in terms of both cost and time than the fastest sequential algorithm.

- Given and , it is moderately hard to find ;

- for any , it is easy to compute ;

- is not amenable to amortization: for any finite set of input values and corresponding threshold values , the cost of finding with on the whole set is comparable to the total cost of finding from scratch for each ;

3.3.3. Blockchain Updating

- The majority decision mechanism described above is not mandatory, and the choice of the block to be referenced in the chain is actually left to each single miner. A miner M is just encouraged to adhere to the mechanism, on the basis of the fact that the longer is the chain linked to M’s new mined block , the higher are the chances that M gets a reward for the mining activity spent on . This design was presumably chosen in [7] because it is really difficult to guarantee and ascertain the correctness of peers local processing, but—as we are going to discuss shortly—it is the root cause of the double-spending threat.

- The “longest chain” is not actually unique. Indeed, it may be the case that the same mining effort corresponds to two or more chains that differs for some block and/or the block order. Thus, also assuming that all the miners follow the majority decision mechanism, branches are possible.

- Each branch must be internally consistent and can never include two conflicting transactions; however, branches do not need to be consistent with one another, and one branch can include a transaction which contradicts a transaction in another branch.

- The blocks that will be incorporated in the blockchain are determined by the upshot of a sequence of mining activities and, ultimately, by the relative fitness of all miners working at that section of the blockchain. As we will detail in Section 4, at least in the case of Bitcoin, this has given rise to a rude mining-hardware race which undermines the confidence of users in the cryptocurrency and its stability on the market.

4. Computational Aspects

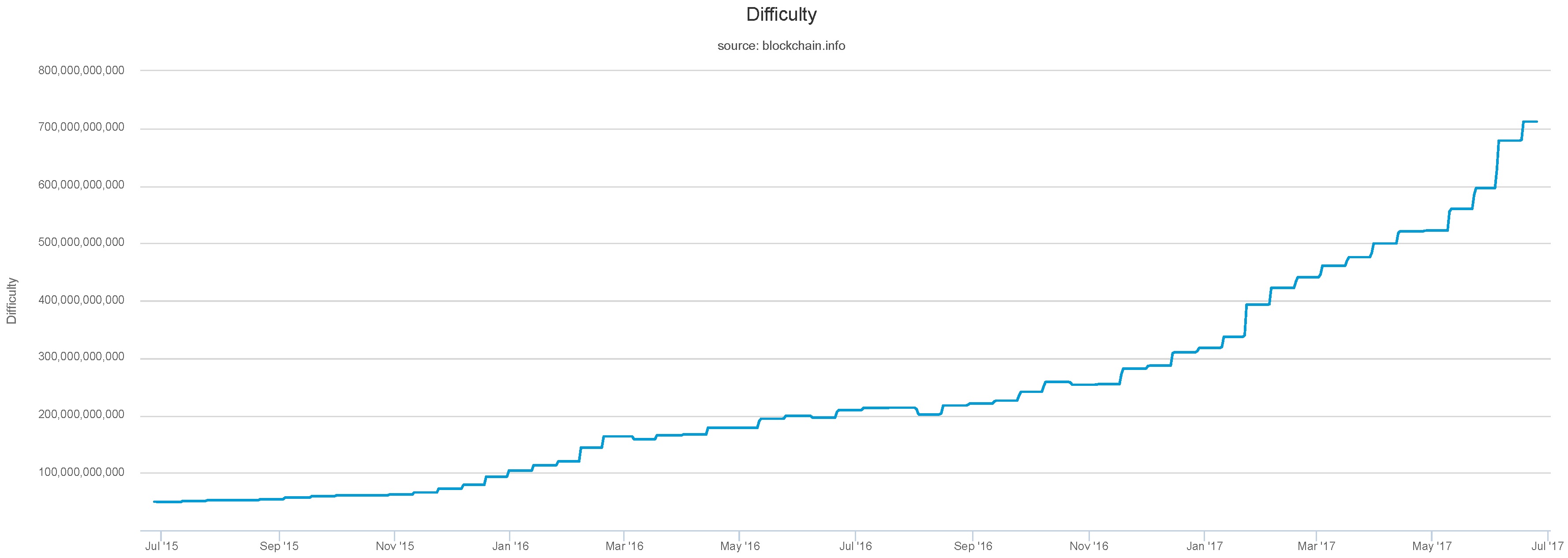

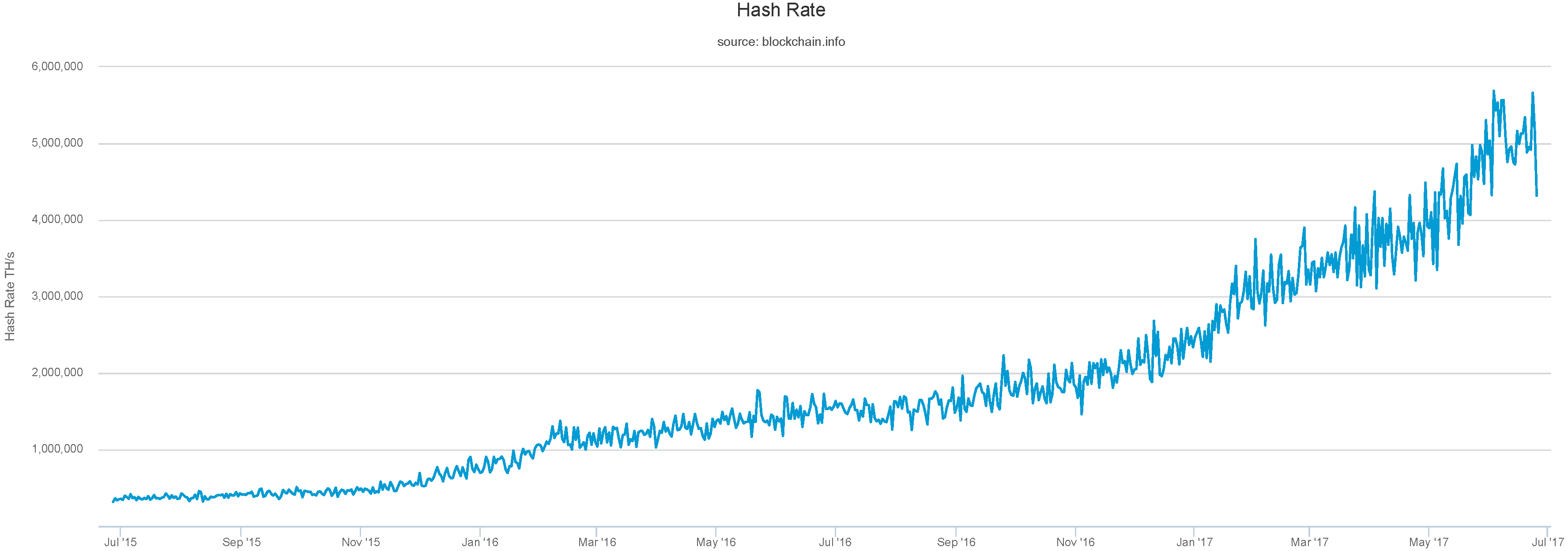

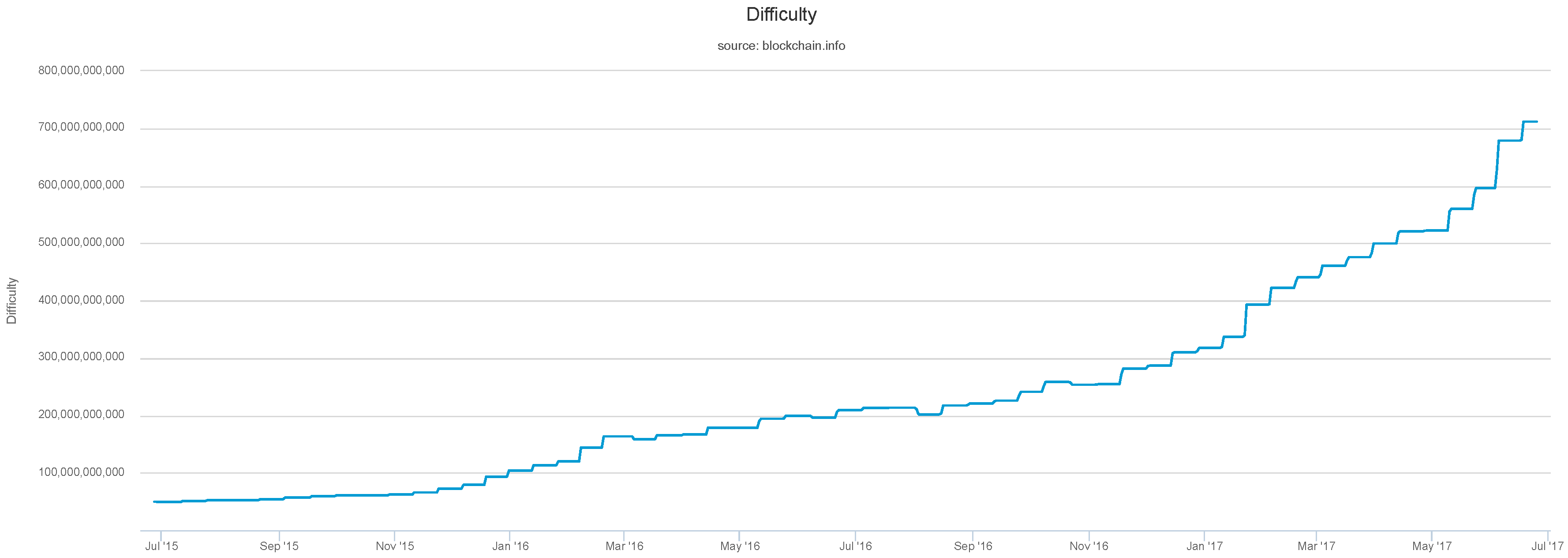

4.1. Difficulty and Performance in Bitcoin

- The growth in number of competitors to the race, due to the diffusion of currency and to the prize offered.

- The growth in performance of the single computational resource, due to the usage of better hardware.

- The sentiment of investors in mining pools.

4.2. Making It Useful

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Wikipedia. DigiCash. Available online: https://en.wikipedia.org/wiki/DigiCash (accessed on 13 June 2017).

- Wikipedia. E-gold. Available online: https://en.wikipedia.org/wiki/E-gold (accessed on 13 June 2017).

- eDINAR. Available online: https://www.e-dinar.com (accessed on 13 June 2017).

- Wikipedia. Liberty Reserve. Available online: https://en.wikipedia.org/wiki/Liberty_Reserve (accessed on 13 June 2017).

- Condon, S. Judge Spares E-Gold Directors Jail Time. Available online: http://www.cnet.com/news/judge-spares-e-gold-directors-jail-time/ (accessed on 28 August 2017).

- Cloherty, J. ’Black Market Bank’ Accused of Laundering $ 6B in Criminal Proceeds. Available online: http://abcnews.go.com/US/black-market-bank-accused-laundering-6b-criminal-proceeds/story?id=19275887 (accessed on 28 August 2017).

- Nakamoto, S. Bitcoin: A Peer to Peer Electronic Cash System. 2008. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 28 August 2017).

- Dai, W. B-Money Proposal. 1998. Available online: http://www.weidai.com/bmoney.txt (accessed on 28 August 2017).

- CryptoCurrency Market Capitalizations. Available online: http://coinmarketcap.com/ (accessed on 11 August 2017).

- MAPofCOINS. Available online: http://mapofcoins.com/ (accessed on 13 July 2017).

- Szabo, N. Formalizing and Securing Relationships on Public Networks. 1997. Available online: http://journals.uic.edu/ojs/index.php/fm/article/view/548/469 (accessed on 11 August 2017).

- Buterin, V. DAOs, DACs, DAs and More: An Incomplete Terminology Guide, 2014. Available online: https://blog.ethereum.org/2014/05/06/daos-dacs-das-and-more-an-incomplete-terminology-guide/ (accessed on 20 July 2017).

- Bitcoin Wiki. Smart Property. Available online: https://en.bitcoin.it/wiki/Smart_Property (accessed on 27 July 2017).

- Bitcoin Wiki. Colored Coins. Available online: https://en.bitcoin.it/wiki/Colored_Coins (accessed on 27 July 2017).

- Umeh, J. Blockchain Double Bubble or Double Trouble? ITNOW 2016, 58, 58–61. [Google Scholar] [CrossRef]

- Proof of Existence. Available online: http://www.proofofexistence.com/ (accessed on 13 June 2017).

- Everledger. Available online: https://www.everledger.io/ (accessed on 18 July 2017).

- Official Kimberley Process. Available online: https://www.kimberleyprocess.com (accessed on 18 July 2017).

- Wright, A.; De Filippi, P. Decentralized Blockchain Technology and the Rise of Lex Cryptographia, 2015. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2580664 (accessed on 3 July 2017).

- Swan, M. Blockchain: Blueprint for a New Economy; O’Reilly Media, Inc.: California, CA, USA, 2015. [Google Scholar]

- Delmolino, K.; Arnett, M.; Kosba, A. A Programmer’s Guide to Ethereum and Serpent, 2015. Available online: https://mc2-umd.github.io/ethereumlab/docs/serpent_tutorial.pdf (accessed on 28 August 2017).

- Solidity Documentation. Available online: https://solidity.readthedocs.io/en/develop/ (accessed on 8 June 2017).

- ICANN (Internet Corporation for Assigned Names and Numbers). Available online: https://www.icann.org/ (accessed on 14 July 2017).

- Ramaswamy, V.S.; Namakumari, S. Marketing Management: Global Perspective, Indian Context; McGraw Hill Education (India) P. Ltd.: New Delhi, India, 2013. [Google Scholar]

- Namecoin. Available online: https://namecoin.org/ (accessed on 14 June 2017).

- Buterin, V. Ethereum White Paper, 2014. Available online: https://github.com/ethereum/wiki/wiki/White-Paper#ethereum (accessed on 3 July 2017).

- Frontier Documentation. Available online: https://ethereum.gitbooks.io/frontier-guide/content/index.html (accessed on 20 July 2017).

- A Call for a Temporary Moratorium on “The DAO”. Available online: https://docs.google.com/document/d/10kTyCmGPhvZy94F7VWyS-dQ4lsBacR2dUgGTtV98C40 (accessed on 20 July 2017).

- The DAO, The Hack, The Soft Fork and The Hard Fork. Available online: https://www.cryptocompare.com/coins/guides/the-dao-the-hack-the-soft-fork-and-the-hard-fork/ (accessed on 20 July 2017).

- The Explorer for the Ethereum blockchain. Available online: https://etherchain.org/ (accessed on 20 July 2017).

- The Ethereum Block Explorer. Available online: https://etherscan.io/ (accessed on 20 July 2017).

- Ethereum Classic Block Explorer. Available online: http://gastraker.io (accessed on 20 July 2017).

- ETC E CHAIN. Available online: https://etcchain.com/explorer (accessed on 20 July 2017).

- Enterprise Ethereum Alliance. Available online: https://entethalliance.org/ (accessed on 20 July 2017).

- Storj Whitepaper, 2016. Available online: https://storj.io/storj.pdf (accessed on 28 August 2017).

- Pureswaran, V.; Brody, P. Device democracy, Saving the future of the Internet of Things, 2015. Available online: http://www-935.ibm.com/services/multimedia/GBE03620USEN.pdf (accessed on 28 August 2017).

- Telehash. Available online: http://telehash.org/ (accessed on 20 July 2017).

- BitTorrent. Available online: http://www.bittorrent.com/ (accessed on 27 July 2017).

- Morabito, V. Business Innovation Through Blockchain: The B3 Perspective; Springer International Publishing: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Carlisle, B.G. Proof of Prespecified Endpoints in Medical Research with the Bitcoin Blockchain. Available online: https://www.bgcarlisle.com/blog/2014/08/25/proof-of-prespecified-endpoints-in-medical-research-with-the-bitcoin-blockchain/ (accessed on 20 July 2017).

- Nichol, P.B. Blockchain Applications for Healthcare. Available online: http://www.cio.com/article/3042603/innovation/blockchain-applications-for-healthcare.html (accessed on 20 July 2017).

- Walch, A. The bitcoin blockchain as financial market infrastructure: A consideration of operational risk. N. Y. Univ. J. Legis. Public Policy 2015, 18, 837. [Google Scholar]

- Tapscott, A.; Tapscott, D. How Will Blockchain Change Banking? How Won’t It? Available online: https://www.americanbanker.com/opinion/how-will-blockchain-change-banking-how-i-wont-i-it (accessed on 24 July 2017).

- Brennan, C.; Lunn, W. Blockchain: The Trust Disrupter; Credit Suisse Securities (Europe) Ltd.: London, UK, 2016. [Google Scholar]

- Ripple. Available online: https://ripple.com/ (accessed on 24 July 2017).

- Crosman, P. Ripple vs. Swift Rivalry Heats Up; Banking May Be Ultimate Winner. Available online: https://www.paymentssource.com/news/ripple-vs-swift-rivalry-heats-up-banking-may-be-ultimate-winner (accessed on 24 July 2017).

- Tschorsch, F.; Scheuermann, B. Bitcoin and beyond: A technical survey on decentralized digital currencies. IEEE Commun. Surv. Tutor. 2016, 18, 2084–2123. [Google Scholar] [CrossRef]

- Gutierrez, C.M.; Gallagher, P. (Eds.) Secure Hash Standard; Federal Information Processing Standards Publication; National Institute of Standards and Technology: Gaithersburg, MD, USA, 2008; Volumes 180–183.

- Pritzker, P.; May, W. (Eds.) SHA-3 Standard: Permutation-Based Hash and Extendable-Output Functions; Federal Information Processing Standards Publication; National Institute of Standards and Technology: Gaithersburg, MD, USA, 2015; Volume 202.

- Bitcoin.info Explorer. Available online: https://blockchain.info (accessed on 23 July 2017).

- Bitcoin Block Explorer. Available online: https://blockexplorer.com/ (accessed on 13 July 2017).

- Bitcoin Network Graphs by bitcoin.org. Available online: http://bitcoin.sipa.be/ (accessed on 13 July 2017).

- Bitcoin Wiki.Script. Available online: https://en.bitcoin.it/wiki/Script (accessed on 21 July 2017).

- Cooper, D.; Santesson, S.; Farrell, S.; Boeyen, S.; Housley, R.; Polk, W. Internet X.509 Public Key Infrastructure Certificate and Certificate Revocation List (CRL) Profile. 2008. Available online: http://tools.ietf.org/html/rfc5280 (accessed on 28 August 2017).

- Johnson, D.; Menezes, A.; Vanstone, S. The elliptic curve digital signature algorithm (ECDSA). Int. J. Inf. Secur. 2001, 1, 36–63. [Google Scholar] [CrossRef]

- Dobbertin, H.; Bosselaers, A.; Preneel, B. RIPEMD-160: A strengthened version of RIPEMD. In Fast Software Encryption; Springer: Berlin/Heidelberg, Germany, 1996; pp. 71–82. [Google Scholar]

- Bitcoin Developer Guide. Available online: https://bitcoin.org/en/developer-guide (accessed on 14 July 2017).

- Menezes, A.J.; Van Oorschot, P.C.; Vanstone, S.A. Handbook of Applied Cryptography; CRC Press: Boca Raton, FL, USA, 2010. [Google Scholar]

- Bos, J.W.; Halderman, J.A.; Heninger, N.; Moore, J.; Naehrig, M.; Wustrow, E. Elliptic curve cryptography in practice. In Proceedings of the International Conference on Financial Cryptography and Data Security, Christ Church, Barbados, 3–7 March 2014; Springer: Berlin/Heidelberg, Germany, 2014; pp. 157–175. [Google Scholar]

- Ron, D.; Shamir, A. Quantitative analysis of the full bitcoin transaction graph. In Proceedings of the International Conference on Financial Cryptography and Data Security, Okinawa, Japan, 1–5 April 2013; Springer: Berlin/Heidelberg, Germany, 2013; pp. 6–24. [Google Scholar]

- Fleder, M.; Kester, M.S.; Pillai, S. Bitcoin transaction graph analysis. arXiv, 2015; arXiv:arXiv:1502.01657. [Google Scholar]

- Garay, J.; Kiayias, A.; Leonardos, N. The bitcoin backbone protocol: Analysis and applications. In Proceedings of the Annual International Conference on the Theory and Applications of Cryptographic Techniques, Sofia, Bulgaria, 26–30 April 2015; Springer: Berlin/Heidelberg, Germany, 2015; pp. 281–310. [Google Scholar]

- Tor project. Overview. Available online: https://www.torproject.org/about/overview.html.en (accessed on 14 July 2017).

- Wikipedia. Forth Programming Language. Available online: https://en.wikipedia.org/wiki/Forth_(programming_language) (accessed on 17 July 2017).

- Bitcoin Wiki. Contract. Available online: https://en.bitcoin.it/wiki/Contract (accessed on 21 July 2017).

- Wood, G. Ethereum: A Secure Decentralized Generalized Transaction Ledger, 2016. Available online: https://ethereum.github.io/yellowpaper/paper.pdf (accessed on 28 August 2017).

- Bitcoin Wiki. Block Size Limit Controversy. Available online: https://en.bitcoin.it/wiki/Block_size_limit_controversy (accessed on 21 July 2017).

- StephenM347. Bitcoin@Stack Exchange. What’s the Purpose of a Maximum Block Size? Available online: http://bitcoin.stackexchange.com/questions/37292/whats-the-purpose-of-a-maximum-block-size/37303#37303 (accessed on 14 July 2017).

- Merkle, R.C. A digital signature based on a conventional encryption function. In Advances in Cryptology—CRYPTO’87; Springer: Berlin/Heidelberg, Germany, 1988; pp. 369–378. [Google Scholar]

- Bitcoin Wiki. Block Hashing Algorithm. Available online: https://en.bitcoin.it/wiki/Block_hashing_algorithm (accessed on 27 July 2017).

- Shirrif, K. Bitcoin Mining the Hard Way: The Algorithms, Protocols, and Bytes. Available online: http://www.righto.com/2014/02/bitcoin-mining-hard-way-algorithms.html (accessed on 11 August 2018).

- Jakobsson, M.; Juels, A. Proofs of Work and Bread Pudding Protocols. In Proceedings of the IFIP TC6/TC11 Joint Working Conference on Secure Information Networks: Communications and Multimedia Security, Deventer, The Netherlands, 20–21 September 1999; pp. 258–272. [Google Scholar]

- Dwork, C.; Naor, M. Pricing via processing or combatting junk mail. In Advances in Cryptology—CRYPTO’92; Springer: Berlin/Heidelberg, Germany, 1993; pp. 139–147. [Google Scholar]

- Rogaway, P. Nonce-Based Symmetric Encryption. In Fast Software Encryption; Roy, B., Meier, W., Eds.; Lecture Notes in Computer Science; Springer: Berlin/Heidelberg, Germany, 2004; Volume 3017, pp. 348–358. [Google Scholar]

- Rosenfeld, M. Analysis of Hashrate-Based Double Spending. 2014. Available online: http://arxiv.org/abs/1402.2009v1 (accessed on 28 August 2017).

- Litecoin. Available online: https://litecoin.org/ (accessed on 20 July 2017).

- Percival, C. Stronger Key Derivation via Sequential Memory-Hard Functions, 2009. Available online: http://www.bsdcan.org/2009/schedule/attachments/87_scrypt.pdf (accessed on 28 August 2017).

- Rivest, R. The MD5 Message-Digest Algorithm. 1992. Available online: http://tools.ietf.org/html/rfc1321 (accessed on 28 August 2017).

- Daley, W.M.; Kammer, R.G. (Eds.) Data Encryption Standard (DES); Federal Information Processing Standards Publication; National Institute of Standards and Technology: Gaithersburg, MD, USA, 1999; Volume 46–3.

- King, S.; Nadal, S. Ppcoin: Peer-to-Peer Crypto-Currency with Proof-of-Stake, 2012. Available online: https://peercoin.net/assets/paper/peercoin-paper.pdf (accessed on 28 August 2017).

- Larimer, D. Transactions as Proof-of-Stake, 2013. Available online: https://steemit.com/bitshares/@testz/bitshares-history-transactions-as-proof-of-stake-tapos (accessed on 3 July 2017).

- Larimer, D. Delegated Proof-of-Stake (DPoS), 2014. Available online: http://docs.bitshares.eu/bitshares/dpos.html (accessed on 28 August 2017).

- Takura, A.; Ono, S.; Naito, S. A secure and trusted time stamping authority. In Proceedings of the IEEE IWS 99 Internet Workshop, Osaka, Japan, 18–20 February 1999; pp. 88–93. [Google Scholar]

- Bentov, I.; Lee, C.; Mizrahi, A.; Rosenfeld, M. Proof of Activity: Extending Bitcoin’s Proof of Work via Proof of Stake. SIGMETRICS Perform. Eval. Rev. 2014, 42, 34–37. [Google Scholar] [CrossRef]

- Wuille, P.; Bitcoin@Stack Exchange. What Does the Term “Longest Chain” Mean? Available online: http://bitcoin.stackexchange.com/questions/5540/what-does-the-term-longest-chain-mean/5542#5542 (accessed on 14 July 2017).

- Kolden, J.; Bitcoin@Stack Exchange. What Are Bitcoin “Confirmations”? Available online: http://bitcoin.stackexchange.com/questions/146/what-are-bitcoin-confirmations/160#160 (accessed on 14 July 2017).

- Kopetz, H. Real-Time Systems: Design Principles for Distributed Embedded Applications; Springer: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Laccetti, G.; Schmid, G. Brute force attacks on hash functions. J. Discret. Math. Sci. Cryptogr. 2007, 10, 439–460. [Google Scholar] [CrossRef]

- Bitcoin Wiki. Non-Specialized Hardware Comparison. Available online: https://en.bitcoin.it/wiki/Non-specialized_hardware_comparison (accessed on 15 June 2017).

- Bitcoin Wiki: Mining Hardware Comparison. Available online: https://en.bitcoin.it/wiki/Mining_ hardware_comparison (accessed on 15 June 2017).

- McCook, H. An Order-of-Magnitude Estimate of the Relative Sustainability of the Bitcoin Network, 2015. Available online: https://www.academia.edu/7666373 (accessed on 28 August 2017).

- King, S. Primecoin: Cryptocurrency with Prime Number Proof-of-Work, 2013. Available online: http://primecoin.io/bin/primecoin-paper.pdf (accessed on 28 August 2017).

- The University of Tennessee. Finding Primes and Proving Primality. Available online: http://primes.utm.edu/prove/merged.html (accessed on 10 August 2017).

- Lifchitz, H. Generalization of Euler-Lagrange Theorem. Available online: http://www.primenumbers.net/Henri/us/NouvTh1us.htm (accessed on 10 August 2017).

- CureCoin. What Is CureCoin? Available online: https://curecoin.net/knowledge-base/about-curecoin/what-is-curecoin/ (accessed on 27 July 2017).

- Gridcoin Wiki. Available online: http://wiki.gridcoin.us/Main_Page (accessed on 27 July 2017).

- Common Vulnerabilities and Exposuresdatabase. Available online: https://cve.mitre.org/cve/cve.html (accessed on 27 July 2017).

- Wikipedia. History of Bitcoin. Available online: https://en.wikipedia.org/wiki/History_of_Bitcoin (accessed on 14 July 2017).

- Top 500 Supercomputing Sites. Available online: www.top500.org (accessed on 30 July 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Symbol [Section(s)] | Meaning [Section(s)] | Symbol [Section(s)] | Meaning [Section(s)] |

|---|---|---|---|

| T [3.2.2] | Transaction [3.1,3.2] | M [3.3.1] | Miner [3.1] |

| I [3.2.2] | Transaction input [3.2.2] | R [3.2.3] | Recipient (payee in cryptocurrency) [3.2] |

| O [3.2.2] | Transaction output [3.2.2] | P [3.2] | Transactor (payer in cryptocurrency) [3.2] |

| B [3.3.1] | Transaction block [3.3] | N [3.3.2] | Solution of mining (nonce) [3.3.2] |

| H [3.3.1] | Block header [3.3.1] | [3.3.2] | Difficulty of mining (threshold, aka target in Bitcoin) [3.3.2] |

| D [3.3.1] | Digest [3.2.1] | [3.3.2] | Pseudo-random function [3.3.2] |

| [3.3.2] | Root hash (aka root digest) [3.3.2] | [3.3.2] | Pricing function [3.3.2] |

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Step 6 | Step 7 | ||

|---|---|---|---|---|---|---|---|---|

| Processed inst/data | <sig> | <pubkey> | OP_DUP | OP_HASH160 | <pubKeyHash> | OP_EQUALVERIFY | OP_CHECKSIG | |

| Stack content | <pubKeyHash> | |||||||

| <pubkey> | <pubKeyHash> | <pubKeyHash> | ||||||

| <pubkey> | <pubkey> | <pubkey> | <pubkey> | <pubkey> | <pubkey> | |||

| <sig> | <sig> | <sig> | <sig> | <sig> | <sig> | <sig> | True |

| Technology | Device | Mhash/s | W | $ | Mhash/s/$ | Mhash/J |

|---|---|---|---|---|---|---|

| CPU-Intel | Core i7 3930k | 66.6 | 130 | 670 | 0.10 | 0.51 |

| CPU-AMD | 4x Opteron 6174 | 115 | 320 | 220 | 0.52 | 0.36 |

| Coprocessor Intel | Xeon Phi 5100 | 140 | 225 | 4000 | 0.03 | 0.62 |

| GPU-Nvidia | Tesla S2070 | 749.23 | 900 | 3000 | 0.25 | 0.83 |

| GPU-AMD (ATI) | 5870x6 | 2568 | 1200 | 300 | 8.56 | 2.14 |

| FPGA | Butterflylabs Mini Rig | 25,200 | 1250 | 15,295 | 1.64 | 20.16 |

| ASIC | AntMiner S9 | 14,000,000 | 1375 | 2400 | 5833 | 10,182 |

| ASIC | Spondooliestech SP35 Yukon | 5,500,000 | 3650 | 2235 | 2460 | 1506 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Romano, D.; Schmid, G. Beyond Bitcoin: A Critical Look at Blockchain-Based Systems. Cryptography 2017, 1, 15. https://doi.org/10.3390/cryptography1020015

Romano D, Schmid G. Beyond Bitcoin: A Critical Look at Blockchain-Based Systems. Cryptography. 2017; 1(2):15. https://doi.org/10.3390/cryptography1020015

Chicago/Turabian StyleRomano, Diego, and Giovanni Schmid. 2017. "Beyond Bitcoin: A Critical Look at Blockchain-Based Systems" Cryptography 1, no. 2: 15. https://doi.org/10.3390/cryptography1020015

APA StyleRomano, D., & Schmid, G. (2017). Beyond Bitcoin: A Critical Look at Blockchain-Based Systems. Cryptography, 1(2), 15. https://doi.org/10.3390/cryptography1020015