Sustainability Impact Assessment of Increased Plastic Recycling and Future Pathways of Plastic Waste Management in Sweden

Abstract

:1. Introduction

2. Plastic Waste Management and Policy Background

2.1. Plastic Waste Management and Policy in the EU

2.2. Plastic Waste Management and Policy in Sweden

3. Results and Discussion

3.1. Defining the Scenarios

Scenario A: Sweden fulfils all targets set by the EU

Scenario B: Sweden fulfils all targets set by the EU, with additional actions retaining plastic waste domestically for recycling and limited exports

Scenario C: Sweden fulfils all targets set by the EU, including a statutory ban on the incineration of recyclable plastic waste

3.2. Model Outputs

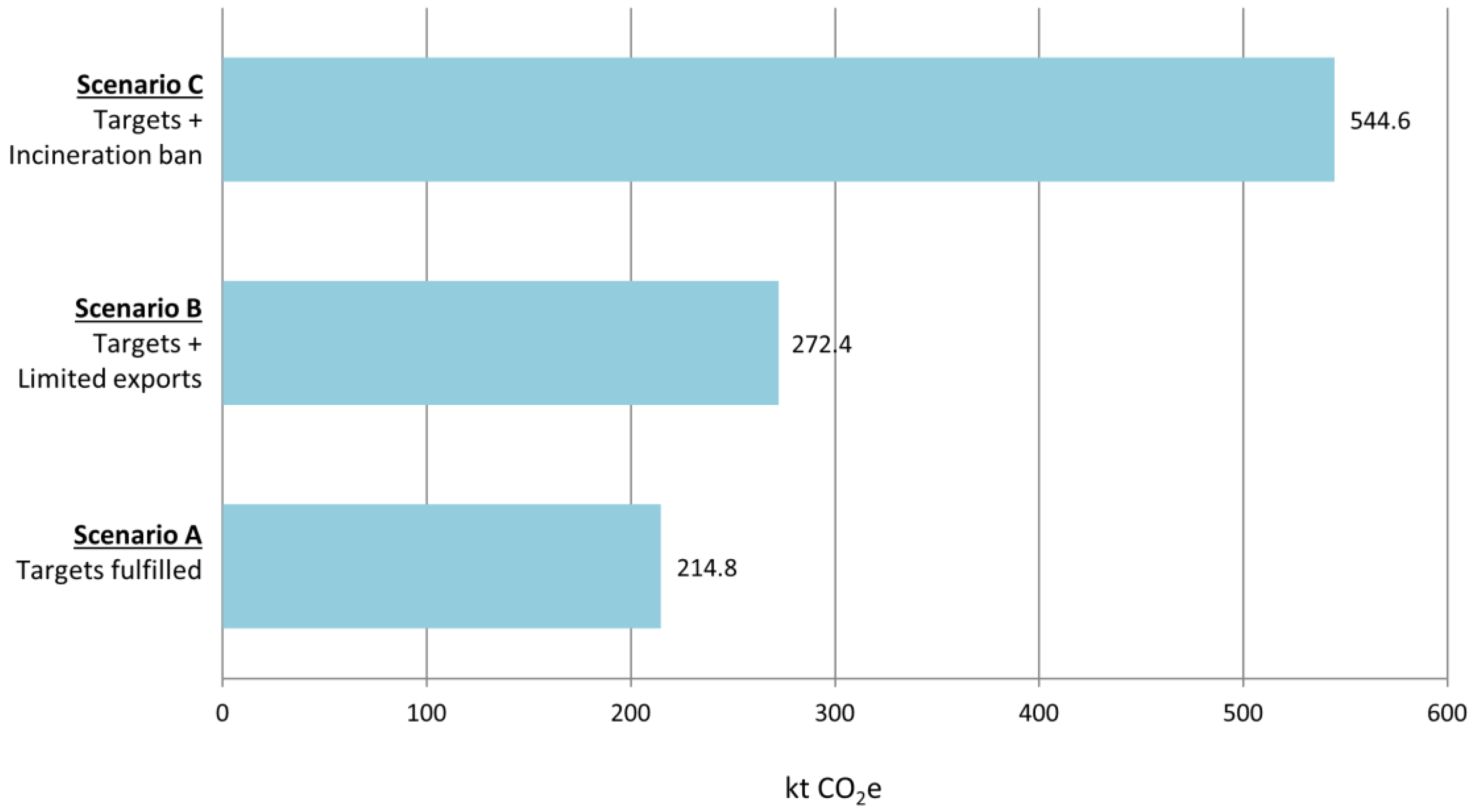

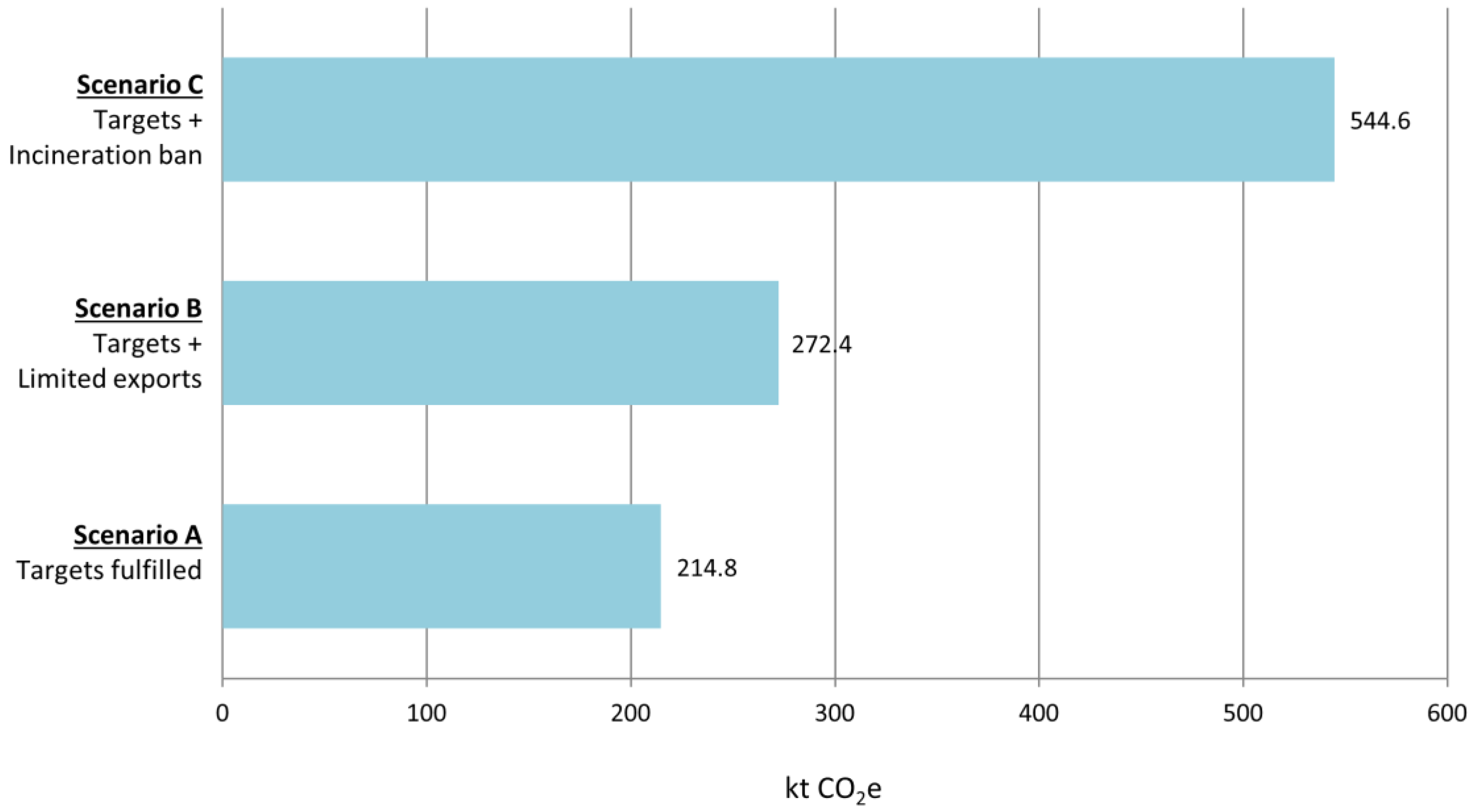

3.2.1. Environmental

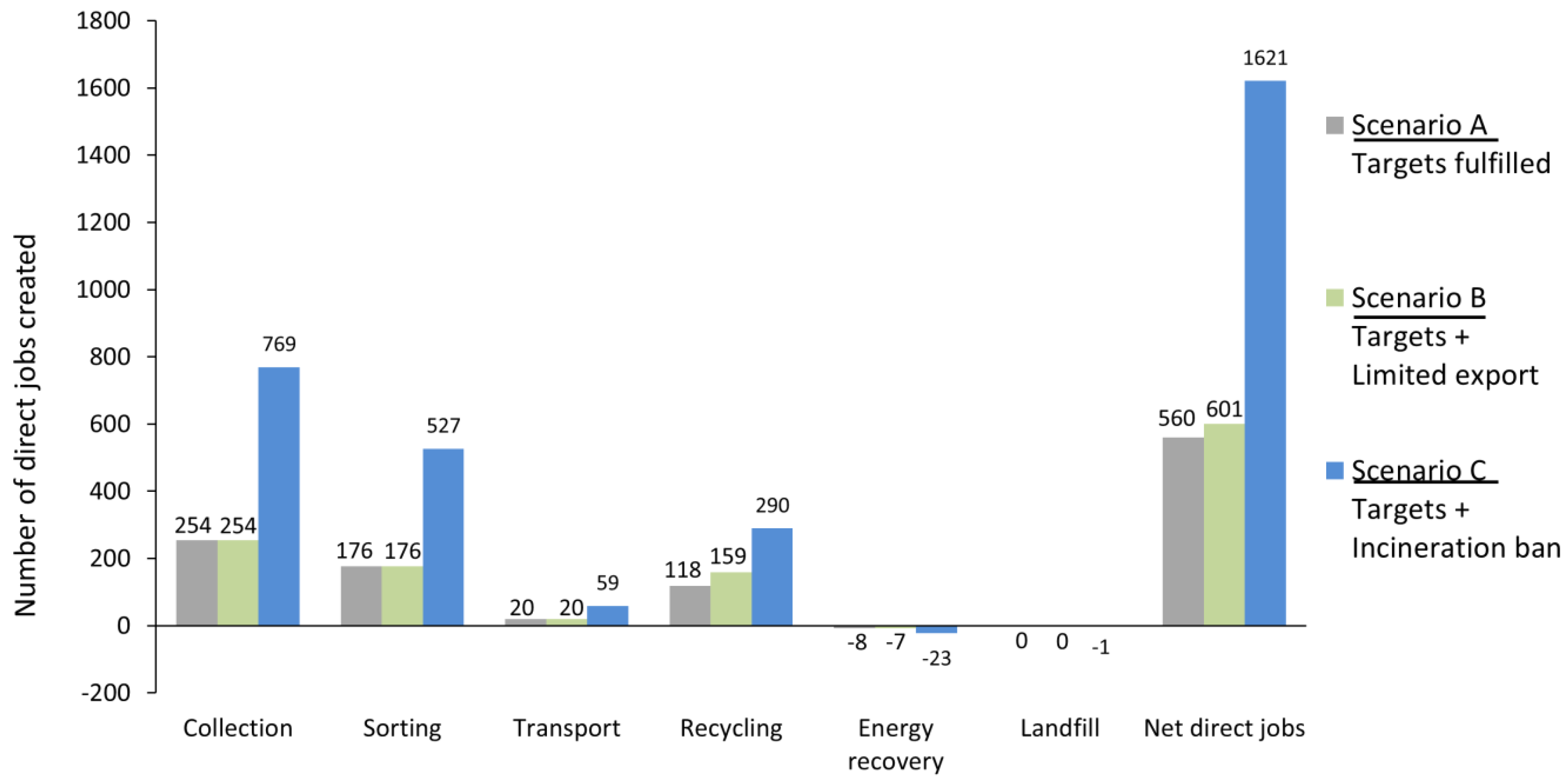

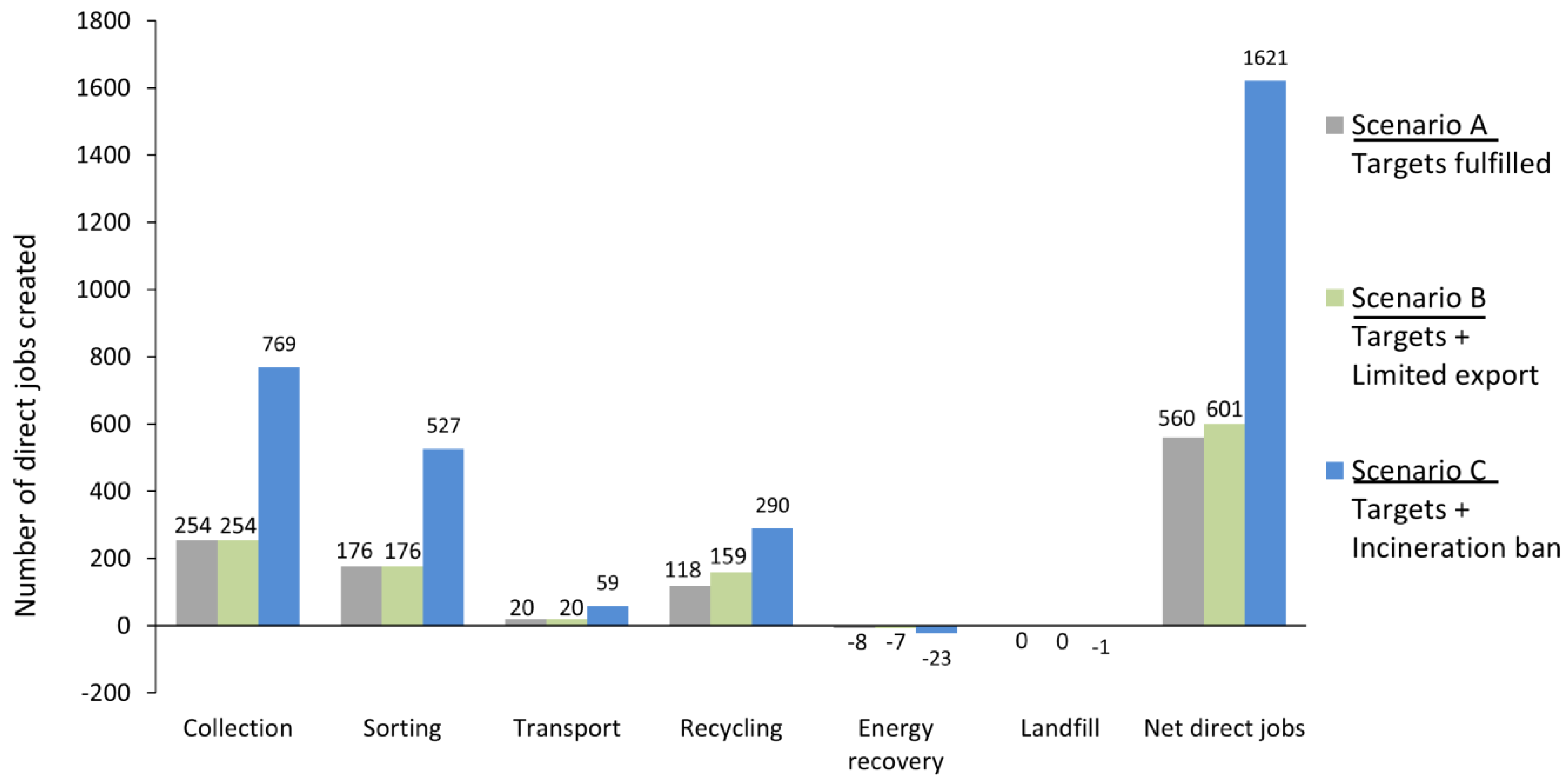

3.2.2. Social

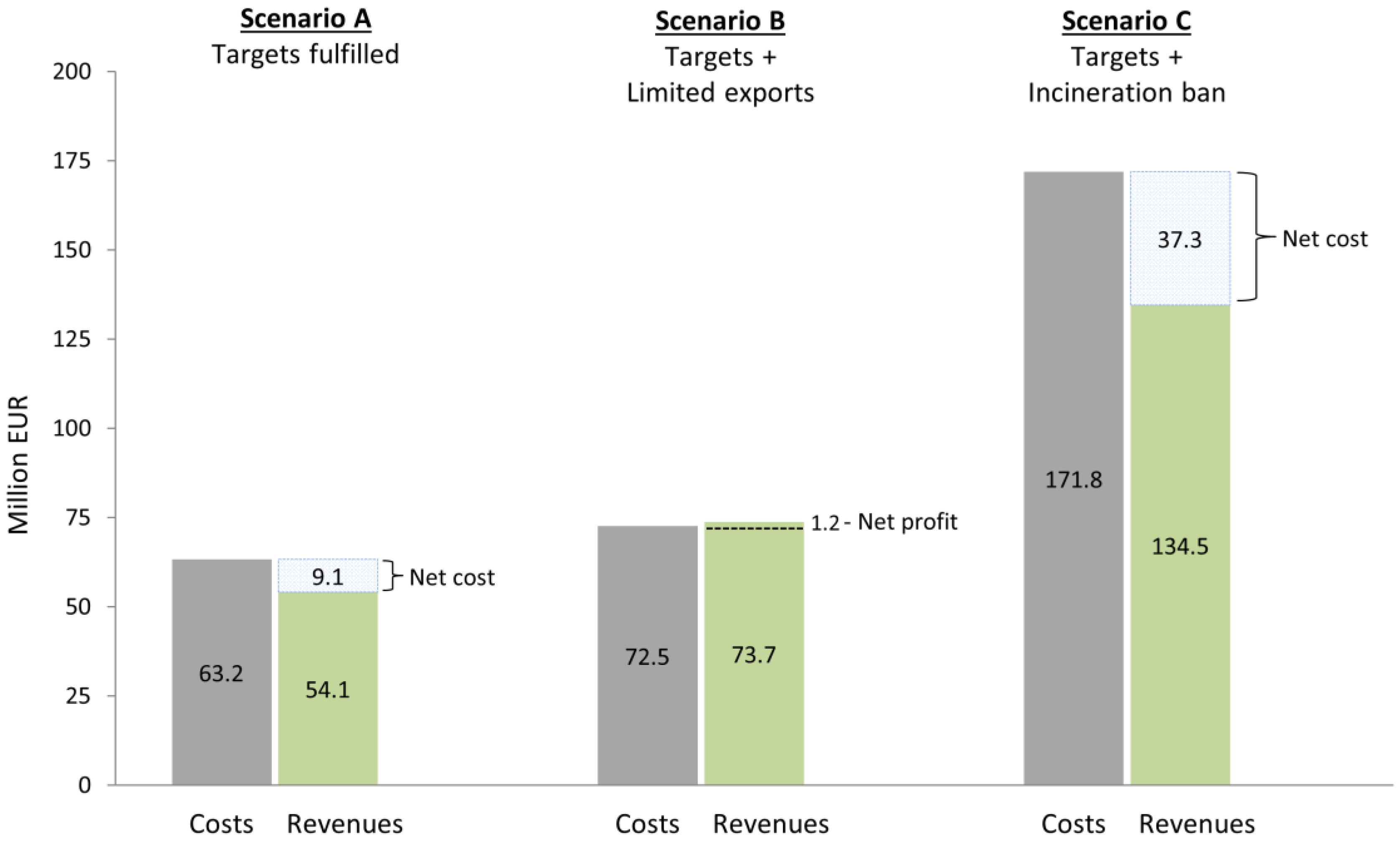

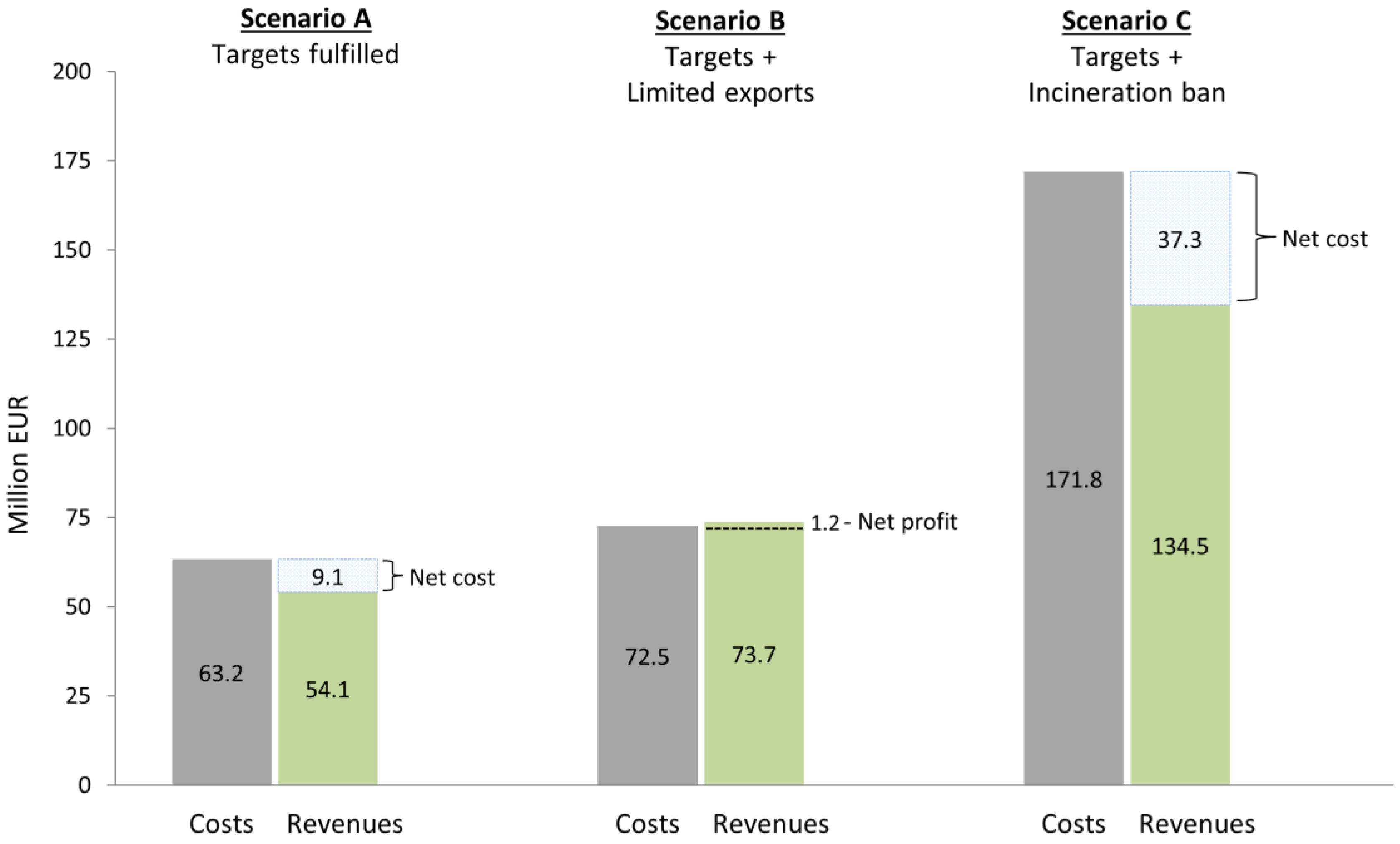

3.2.3. Economic

3.3. Analysis of Findings

4. Method

4.1. The Model

4.2. Limitations of the Model

4.3. Model Baseline Assumptions and Calculations

4.3.1. Plastic Waste Generation by Waste Stream

4.3.2. Plastic Waste Collection Mode Differentiation

4.3.3. Plastic Waste Treatment by Waste Stream

4.3.4. Plastic Waste Imports and Exports

4.3.5. Projections of Future Plastic Waste Generation

4.4. Data Collection

5. Conclusions and Future Research

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Hopewell, J.; Dvorak, R.; Kosior, E. Plastics recycling: Challenges and opportunities. Philos. Trans. R. Soc. B Biol. Sci. 2009, 364, 2115–2126. [Google Scholar] [CrossRef] [PubMed]

- Plastics Europe. Plastics—The Facts 2016. An Analysis of European Plastics Production, Demand and Waste Data; Plastics Europe—Association of Plastics Manufacturers: Brussels, Belgium, 2017. [Google Scholar]

- World Economic Forum. The New Plastics Economy: Rethinking the Future of Plastics; Industry Agenda REF 080116; World Economic Forum: Geneva, Switzerland, 2016. [Google Scholar]

- Palm, E.; Svensson Myrin, E. Mapping the Plastics System and Its Sustainability Challenges; Lund University: Lund, Sweden, 2018. [Google Scholar]

- UNEP (United Nations Environment Programme). Plastic Debris in the Ocean. In UNEP Yearbook 2014—Emerging Issues in Our Global Environment; United Nations Environment Programme: Nairobi, Kenya, 2014. [Google Scholar]

- Li, W.C.; Tse, H.F.; Fok, L. Plastic waste in the marine environment: A review of sources, occurrence and effects. Sci. Total Environ. 2016, 566, 333–349. [Google Scholar] [CrossRef] [PubMed]

- Eriksen, M.; Lebreton, L.C.; Carson, H.S.; Thiel, M.; Moore, C.J.; Borerro, J.C.; Galgani, F.; Ryan, P.G.; Reisser, J. Plastic pollution in the world’s oceans: More than 5 trillion plastic pieces weighing over 250,000 tons afloat at sea. PLoS ONE 2014, 9, e111913. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Milios, L.; Holm Christensen, L.; McKinnon, D.; Christensen, C.; Rasch, M.K.; Hallstrøm Eriksen, M. Plastic recycling in the Nordics: A value chain market analysis. Waste Manag. 2018, 76, 180–189. [Google Scholar] [CrossRef] [PubMed]

- European Commission. A European Strategy for Plastics in a Circular Economy; COM(2018) 28 Final; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Skog, K. EU Has to Step Up in Fight against Plastic Waste. Available online: https://www.regeringen.se/debattartiklar/2018/03/eu-has-to-step-up-in-fight-against-plastic-waste/ (accessed on 21 May 2018).

- Mickwitz, P. A Framework for Evaluating Environmental Policy Instruments—Context and Key Concepts. Evaluation 2003, 9, 415–436. [Google Scholar] [CrossRef]

- Lazarevic, D.; Aoustin, E.; Buclet, N.; Brandt, N. Plastic waste management in the context of a European recycling society: Comparing results and uncertainties in a life cycle perspective. Res. Conserv. Recycl. 2010, 55, 246–259. [Google Scholar] [CrossRef]

- Astrup, T.; Fruergaard, T.; Christensen, T.H. Recycling of plastic: Accounting of greenhouse gases and global warming contributions. Waste Manag. Res. 2009, 27, 763–772. [Google Scholar] [CrossRef] [PubMed]

- Eriksson, O.; Carlsson Reich, M.; Frostell, B.; Björklund, A.; Assefa, G.; Sundqvist, J.O.; Granath, J.; Baky, A.; Thyselius, L. Municipal solid waste management from a systems perspective. J. Clean. Prod. 2005, 13, 241–252. [Google Scholar] [CrossRef] [Green Version]

- Zink, T.; Geyer, R. Circular Economy Rebound. J. Ind. Ecol. 2017, 21, 593–602. [Google Scholar] [CrossRef]

- Arena, U.; Mastellone, M.L.; Perugini, F. Life Cycle assessment of a plastic packaging recycling system. Int. J. LCA 2003, 8, 92–98. [Google Scholar] [CrossRef]

- Carlsson Reich, M. Economic assessment of municipal waste management systems—Case studies using a combination of life cycle assessment (LCA) and life cycle costing (LCC). J. Clean. Prod. 2005, 13, 253–263. [Google Scholar] [CrossRef]

- Da Cruz, N.F.; Ferreira, S.; Cabral, M.; Simões, P.; Marques, R.C. Packaging waste recycling in Europe: Is the industry paying for it? Waste Manag. 2014, 34, 298–308. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Hestin, M.; Faninger, T.; Milios, L. Increased EU Plastics Recycling Targets: Environmental, Economic and Social Impact Assessment; BIO by Deloitte for Plastic Recyclers Europe: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. Closing the Loop—An EU Action Plan for the Circular Economy; COM(2015) 614 Final; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. Proposal for a Directive of the European Parliament and of the Council Amending Directive 94/62/EC on Packaging and Packaging Waste; COM(2015) 596 Final; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. Circular Economy: New Rules will Make EU the Global Front-Runner in Waste Management and Recycling. Available online: http://europa.eu/rapid/press-release_IP-18-3846_en.htm (accessed on 23 May 2018).

- Wilts, H.; von Gries, N. Municipal Solid Waste Management Capacities in Europe; ETC/SCP Working Paper No. 8/2014; European Topic Centre on Sustainable Consumption and Production: Copenhagen, Denmark, 2014. [Google Scholar]

- Corvellec, H.; Zapata Campos, M.J.; Zapata, P. Infrastructures, lock-in, and sustainable urban development: The case of waste incineration in the Göteborg Metropolitan Area. J. Clean. Prod. 2013, 50, 32–39. [Google Scholar] [CrossRef]

- Hennlock, M.; zu Castell-Rüdenhausen, M.; Wahlström, M.; Kjær, B.; Milios, L.; Vea, E.; Watson, D.; Hanssen, O.J.; Fråne, A.; Stenmarck, Å.; et al. Economic Policy Instruments for Plastic Waste—A Review with Nordic Perspectives; TemaNord 2014:569; Nordic Council of Ministers: Copenhagen, Denmark, 2015. [Google Scholar]

- Swedish Environmental Protection Agency. From Waste Management to Resource Efficiency—Sweden’s Waste Plan 2012–2017; Report 6560; Swedish Environmental Protection Agency: Stockholm, Sweden, 2012. [Google Scholar]

- Swedish Environmental Protection Agency. Together We Will Gain from a Non-Toxic, Resource Efficient Society—The Swedish Waste Prevention Programme for 2014 to 2017; Report 6654; Swedish Environmental Protection Agency: Stockholm, Sweden, 2015. [Google Scholar]

- Sveriges Riksdag. Förordning (2014:1073) om Producentansvar för Förpackningar. Available online: https://www.riksdagen.se/sv/dokument-lagar/dokument/svensk-forfattningssamling/forordning-20141073-om-producentansvar-for_sfs-2014-1073 (accessed on 24 May 2018).

- Sveriges Riksdag. Avfallsförordning (2011:927). Available online: https://www.riksdagen.se/sv/dokument-lagar/dokument/svensk-forfattningssamling/avfallsforordning-2011927_sfs-2011-927 (accessed on 24 May 2018).

- Fråne, A.; Stenmarck, Å.; Gislason, S.; Lyng, K.A.; Løkke, S.; zu Castell-Rüdenhausen, M.; Wahlström, M. Collection & Recycling of Plastic Waste: Improvements in Existing Collection and Recycling Systems in the Nordic Countries; TemaNord 2014:543; Nordic Council of Ministers: Copenhagen, Denmark, 2014. [Google Scholar]

- Avfall Sverige. Svensk Avfallshantering 2017; Avfall Sverige: Malmö, Sweden, 2017. [Google Scholar]

- Returpack. Customers & Partners. Available online: https://pantamera.nu/om-oss/returpack-in-english/customers-partners/ (accessed on 27 April 2018).

- Returpack. About Returpack. Available online: https://pantamera.nu/om-oss/returpack-in-english/about-returpack/ (accessed on 27 April 2018).

- Fråne, A.; Stenmarck, Å.; Sörme, L.; Carlsson, A.; Jensen, C. Kartläggning av Plastavfalls-Strömmar i Sverige; SMED Report No 108/2012; Swedish Meteorological and Hydrological Institute: Norrköping, Sweden, 2012. [Google Scholar]

- Avfall Sverige. Svensk Avfallshantering 2015; Avfall Sverige: Malmö, Sweden, 2015. [Google Scholar]

- EEA. More from Less—Material Resource Efficiency in Europe. Country Profile: Sweden; European Environment Agency: Copenhagen, Denmark, 2016. [Google Scholar]

- Bauer, J. State of Agricultural Plastics management in Europe. Presented at the TPSA Pesticide Stewardship Conference, Boise, ID, USA, 7–9 February 2012. [Google Scholar]

- Olofsson, J. Materialåtervinning av Förpackningar och Tidningar—Kartläggning och Klimatnyttoanalys Baserat på två Fallstudier. Master’s Thesis, LTH, Lund University, Lund, Sweden, June 2014. [Google Scholar]

- Ruther, C.; (CFO, Swerec AB, Lanna, Sweden). Personal communication, 20 April 2018.

- FTI AB. Plastkretsen Investerar i Sorteringsanläggning. Available online: http://www.ftiab.se/2351.html (accessed on 23 April 2018).

- Duinker, P.N.; Greig, L.A. Scenario analysis in environmental impact assessment: Improving explorations of the future. Environ. Impact Assess. Rev. 2007, 27, 206–219. [Google Scholar] [CrossRef]

- Schoemaker, P.J. Scenario planning: A tool for strategic thinking. Sloan Manag. Rev. 1995, 36, 25–40. [Google Scholar]

- European Commission. Proposal for a Directive of the European Parliament and of the Council Amending Directive 2008/98/EC on Waste; COM(2015) 595 Final; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Svepretur. Målsättning. Available online: http://svepretur.se/om-svepretur/ (accessed on 21 March 2018).

- ISWA. China’s Ban on Recyclables: Beyond the Obvious…. Available online: https://www.iswa.org/home/news/news-detail/article/chinas-ban-on-recyclables-beyond-the-obvious/109/ (accessed on 2 May 2018).

- UN (United Nations). Comtrade Database. Available online: https://comtrade.un.org/ (accessed on 19 January 2017).

- Government of Sweden. New Climate Decision to Reduce Industry and Transport Emissions. Available online: https://www.government.se/press-releases/2017/12/new-climate-decision-to-reduce-industry-and-transport-emissions/ (accessed on 23 May 2018).

- Harris, S.; Ljungkvist, H. Strategy Paper of Malmö towards a Post-Carbon City; IVL Swedish Environmental Research Institute: Gothenburg, Sweden, 2016. [Google Scholar]

- Statistics Sweden. Population by Region, Marital Status, Age and Sex. Year 1968–2017. Available online: http://www.statistikdatabasen.scb.se/pxweb/en/ssd/?rxid=86abd797-7854-4564-9150-c9b06ae3ab07 (accessed on 31 May 2018).

- Statistics Sweden. Gross Regional Domestic Product (GRDP), (ESA2010) by Region (LAU2). Year 2012–2015. Available online: http://www.statistikdatabasen.scb.se/pxweb/en/ssd/?rxid=86abd797-7854-4564-9150-c9b06ae3ab07 (accessed on 31 May 2018).

- Friends of the Earth. More Jobs, Less Waste—Potential for Job Creation through Higher Rates of Recycling in the UK and the EU; Fiends of the Earth: London, UK, 2010. [Google Scholar]

- SUEZ Environment. Driving Green Growth—The Role of the Waste Management Industry and the Circular Economy; SUEZ Environment UK: Maidenhead, UK, 2011. [Google Scholar]

- Finnveden, G.; Björklund, A.; Carlsson Reich, M.; Eriksson, O.; Sörbom, A. Flexible and robust strategies for waste management in Sweden. Waste Manag. 2007, 27, S1–S8. [Google Scholar] [CrossRef] [PubMed]

- EEA. Managing Municipal Solid Waste—A Review of Achievements in 32 European Countries; Report No 2/2013; European Environment Agency: Copenhagen, Denmark, 2013. [Google Scholar]

- Cramer, J. Key Drivers for High-Grade Recycling under Constrained Conditions. Recycling 2018, 3, 16. [Google Scholar] [CrossRef]

- Corvellec, H.; Bramryd, T. The multiple market-exposure of waste management companies: A case study of two Swedish municipally owned companies. Waste Manag. 2012, 32, 1722–1727. [Google Scholar] [CrossRef] [PubMed]

- Marques, R.C.; Simões, P.; Pinto, F.S. Tariff regulation in the waste sector: An unavoidable future. Waste Manag. 2018, 78, 292–300. [Google Scholar] [CrossRef]

- Eurostat. EU Trade Since 1988 by CN8 (DS-016890). Available online: http://ec.europa.eu/eurostat/web/international-trade-in-goods/data/database (accessed on 19 January 2017).

- National Institute of Economic Research. Miljö, Ekonomi och Politik 2016; Konjunkturinstitutet: Stockholm, Sweden, 2016; ISBN 978-91-86315-76-4. [Google Scholar]

- Fråne, A.; Hulten, J.; Sundqvist, J.O; Viklund, L. Framtida Avfallsmängder och Avfallsbehandlingskapacitet; SMED Report 2017:1; Swedish Meteorological and Hydrological Institute: Norrköping, Sweden, 2017. [Google Scholar]

- Eurostat. Generation of Waste by Waste Category, Hazardousness and NACE Rev. 2 Activity (env_wasgen). Available online: http://ec.europa.eu/eurostat/web/environment/waste/database (accessed on 16 April 2018).

- Eurostat. Packaging Waste by Waste Operations and Waste Flow (env_waspac). Available online: http://ec.europa.eu/eurostat/web/environment/waste/database (accessed on 16 April 2018).

- Eurostat. Municipal Waste by Waste Operations (env_wasmun). Available online: http://ec.europa.eu/eurostat/web/environment/waste/database (accessed on 16 April 2018).

- Statistics Sweden. Generated Waste by Economic Activity NACE Rev. 2 and Households and by Waste Category. Every Second Year 2010–2014. Available online: http://www.statistikdatabasen.scb.se/pxweb/en/ssd/?rxid=86abd797-7854-4564-9150-c9b06ae3ab07 (accessed on 16 April 2018).

- Statistics Sweden. Total Amount of Packaging Put on the Market and Recycled Broken down by Type of Packaging. Year 2012–2016. Available online: http://www.statistikdatabasen.scb.se/pxweb/en/ssd/?rxid=86abd797-7854-4564-9150-c9b06ae3ab07 (accessed on 16 April 2018).

- Swedish Environmental Protection Agency. Att Styra Mot en Effektivare Avfallshantering—En Utvärdering av den Nationella Avfallsplanen och det Avfallsförebyggande Programmet; Report 6744; Swedish Environmental Protection Agency: Stockholm, Sweden, 2017. [Google Scholar]

- Government of Sweden. The Goal Is a Fossil-Free Sweden. Available online: https://www.government.se/information-material/2015/11/the-goal-is-a-fossil-free-sweden/ (accessed on 23 May 2018).

{kind=link}

{kind=link}

{kind=link}

| Target | 2030 | Source |

|---|---|---|

| Packaging recycling | 55% | COM (2015) 596 final, target for plastic packaging [21]. |

| Waste Electrical and Electronic Equipment (WEEE) recycling | 50% | Directive 2012/19/EU, weighted average of the different targets by WEEE categories. The rate presented here represents the share of plastics in WEEE that needs to be recycled for reaching the overall target in the Directive. For calculation method, refer to the PRE report [19]. In the PRE report this rate is calculated at 45% for 2020, but in this contribution we assume progression of the target to 50% by 2030. |

| End of Life Vehicles (ELV) recycling | 30% | Directive 2000/53/EC, based on plastic content in ELV. The rate presented here represents the share of plastics in ELV that needs to be recycled for reaching the overall target in the Directive. For the calculation method refer to the PRE report [19]. |

| Building & Construction plastic recycling | 30% | No target, legal or voluntary, was found for this waste stream, and therefore we assume a 30% target in line with other waste streams (e.g., ELV and Agri.), as a measure of good practice and ambition within the construction sector. |

| Agricultural plastic recycling | 30% | Voluntary industry target, set at sectoral level by Swepretur—an industry association for manufacturers, importers and retailers of silage film, plastic bags and horticultural foil [44]. |

| Other plastic waste recycling | 7% | Plastic content in municipal solid waste (except packaging waste) that needs to be recycled for achieving the revised municipal waste target of 60% by 2030 (COM(2015) 595 final) [43]. For the calculation method refer to the PRE report [19]. |

| Environmental Impact (GHG Emmisions) | Economic Impact (Costs) | Social Impact (Number of Jobs) | Sustainability Assessment | ||||

|---|---|---|---|---|---|---|---|

| Quant. | Qual. | Quant. | Qual. | Quant. | Qual. | ||

| Scenario A | −214.8 kt CO2e | + | 9.1 mEUR | − | 560 jobs | + | 0/+ |

| Scenario B | −272.4 kt CO2e | + | −1.2 mEUR | + | 601 jobs | + | + |

| Scenario C | −544.6 kt CO2e | ++ | 37.3 mEUR | −− | 1621 jobs | ++ | +/++ |

| Ref. Year 2010 | Packaging | WEEE | ELV | B&C | Agricultural | Other | TOTAL |

|---|---|---|---|---|---|---|---|

| Post-consumer plastic waste (tonnes) | 299,000 | 34,000 | 18,000 | 43,000 | 18,000 | 81,000 | 493,000 |

| Proportion of post- consumer plastic waste | 61% | 7% | 4% | 9% | 4% | 16% | 100% |

| Ref. 2010 | Collection for Recycling Rate | Incineration Rate | Landfilling Rate |

|---|---|---|---|

| Packaging | 37% | 63% | 0% |

| WEEE | 43% | 44% | 13% |

| ELV | 0% | 67% | 33% |

| B&C | 0% | 100% | 0% |

| Agricultural | 89% | 11% | 0% |

| Others | 4% | 96% | 0% |

| Total | 29.13% | 68.75% | 2.12% |

| Packaging | WEEE | ELV | B&C | Agricultural | Other | TOTAL | |

|---|---|---|---|---|---|---|---|

| Post-consumer plastic waste (2010) (tonnes) | 299,000 | 34,000 | 18,000 | 43,000 | 18,000 | 81,000 | 493,000 |

| Annual growth (%) | 2.4% | 2.5% | 2.5% | 2.6% | 1.0% | 2.4% | - |

| Post-consumer plastic waste (2030) (tonnes) | 480,474 | 55,713 | 29,495 | 71,848 | 21,963 | 130,162 | 789,656 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Milios, L.; Esmailzadeh Davani, A.; Yu, Y. Sustainability Impact Assessment of Increased Plastic Recycling and Future Pathways of Plastic Waste Management in Sweden. Recycling 2018, 3, 33. https://doi.org/10.3390/recycling3030033

Milios L, Esmailzadeh Davani A, Yu Y. Sustainability Impact Assessment of Increased Plastic Recycling and Future Pathways of Plastic Waste Management in Sweden. Recycling. 2018; 3(3):33. https://doi.org/10.3390/recycling3030033

Chicago/Turabian StyleMilios, Leonidas, Aida Esmailzadeh Davani, and Yi Yu. 2018. "Sustainability Impact Assessment of Increased Plastic Recycling and Future Pathways of Plastic Waste Management in Sweden" Recycling 3, no. 3: 33. https://doi.org/10.3390/recycling3030033

APA StyleMilios, L., Esmailzadeh Davani, A., & Yu, Y. (2018). Sustainability Impact Assessment of Increased Plastic Recycling and Future Pathways of Plastic Waste Management in Sweden. Recycling, 3(3), 33. https://doi.org/10.3390/recycling3030033