1. Introduction

Aircraft (A/C), both in operation and in their end of life stage, are a potential source of both valuable parts and materials. Engines using e.g. nickel alloys, titanium and precious metal coatings, landing gear comprising titanium and high grade steel or structural parts made from aluminium alloys offer a good recovery potential.

More than half of all airliners ever produced are still in use. Moreover, a dramatic increase in air traffic is expected in the coming years. This may contribute to high-value material supply. This paper aims to quantify the worldwide material stock in the civilian aircraft fleet of airliners (narrow and widebody aircraft). To this end, the total number of aircraft that is available worldwide, and their mass in term of future (potential) recycling material stock has to be identified. Moreover, the figure of active aircraft has to be identified to predict aircraft retirement figures and mass potential for recycling in future.

Aircraft recycling is a field with numerous types of stakeholders. Stakeholders involved include, for example, not only aircraft (body and engine) producers and their suppliers, aircraft operators, dismantling and recycling companies; but also aircraft lessors, service organisations providing maintenance, repair and overhaul (MRO), parts traders, airport operators, and public regulatory organisations such as EASA. In the aircraft end of life phase, both aircraft safety regulations and waste-management rules and regulations apply, depending on the stage of aircraft decommissioning. As long as the aircraft remains “airworthy”, all repair and dismantling steps, including parts harvesting (see Figure 2), require certified staff and procedures, e.g., under EC Commission Regulation No. 2042/2003. Once airworthiness is lost, this renders the entire aircraft and its components scrap, so the material is available to the recycling cycle, with the materials value remaining.

2. Materials and Methods

As a basis for the calculations and forecasts, numerous sources for aircraft data were consolidated into one meta database including their figure, their regional allocation, assignment to airlines and their age. In order to acquire this information, we collected information from reference sites for aircraft, plane spotter websites, and websites for specific aircraft data. All these data are as of March 2015.

Based on 27,763 individual aircraft datasets, 21,028 aircraft can be classified with a full dataset (21,056 in total) as active aircraft and 6707 as in storage, scrapped, written off, or to be entered into service aircraft. Aircraft empty weight is stated, as well as the date of the first flight. Furthermore the data set contains the airline and the aircraft manufacturer, and additional model information. The forecast data were produced using the arithmetic mean composition data of aircraft engines, the mean number of engines per aircraft, and multiplying them by the total number of airliners. Aircraft models with known mass share regarding their structure were selected for a material forecast using identical calculations. The total aircraft fleet mass was calculated based on a mean airliner weight and the total number of airliners.

3. Results and Discussion

3.1. Worldwide Aircraft Fleet

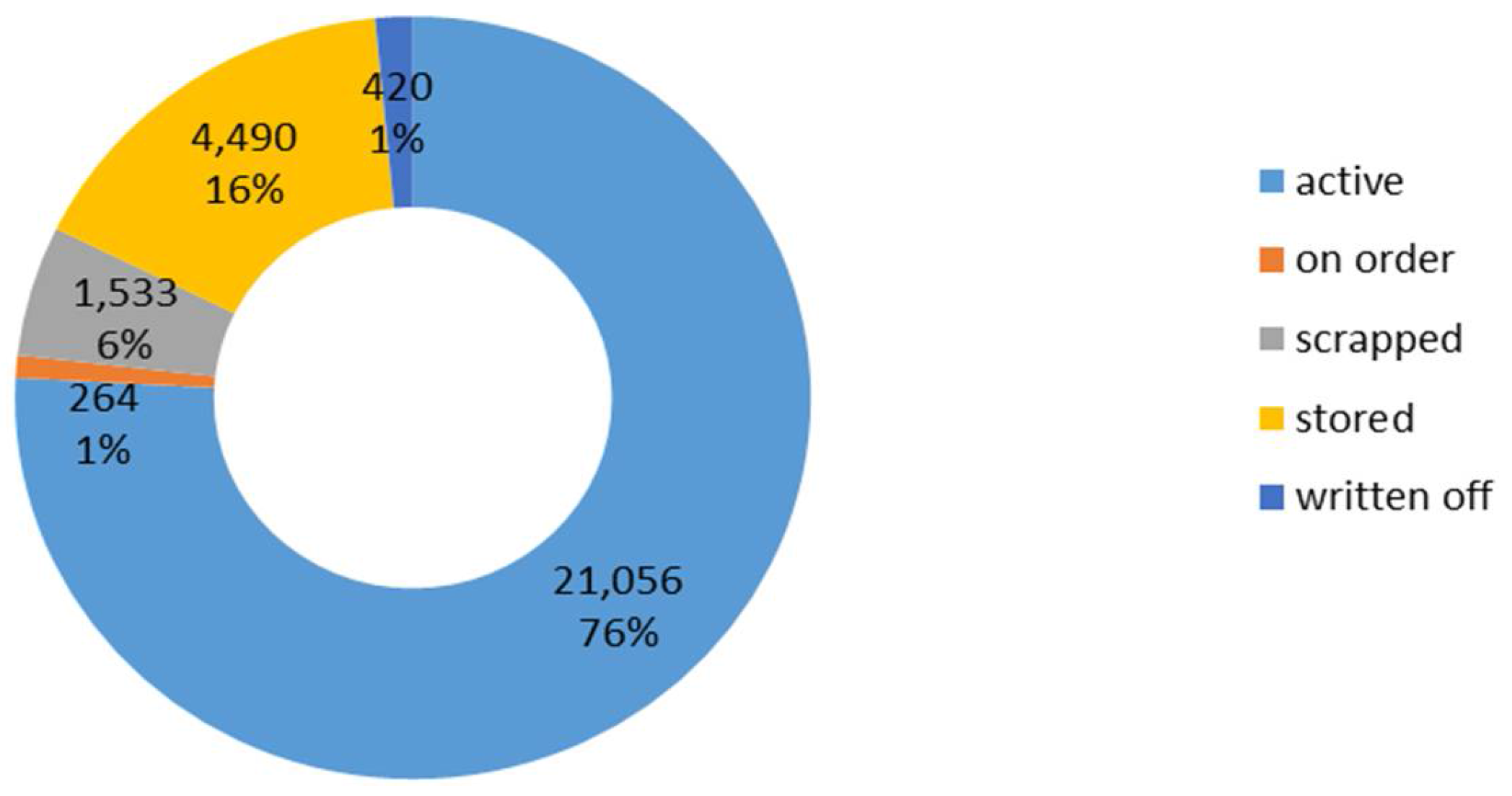

Figure 1 gives the worldwide air fleet status, extracted from a database covering a total of 27,763 commercial aircraft (narrow and wide body). Currently, about 25,546 aircraft are in use, but out of those, only 21,056 are actually in operation, and 4490 are stored. Storage mainly takes place in the United States, although aircraft storage may be possible in Europe, e.g., in the Teruel site in Spain. Typically in Europe, due to a combination of unfavourable climatic conditions and high parking cost, a quick parting-out and teardown of aircraft is favourable [

1].

3.2. Mass and Value Distribution in Aircraft

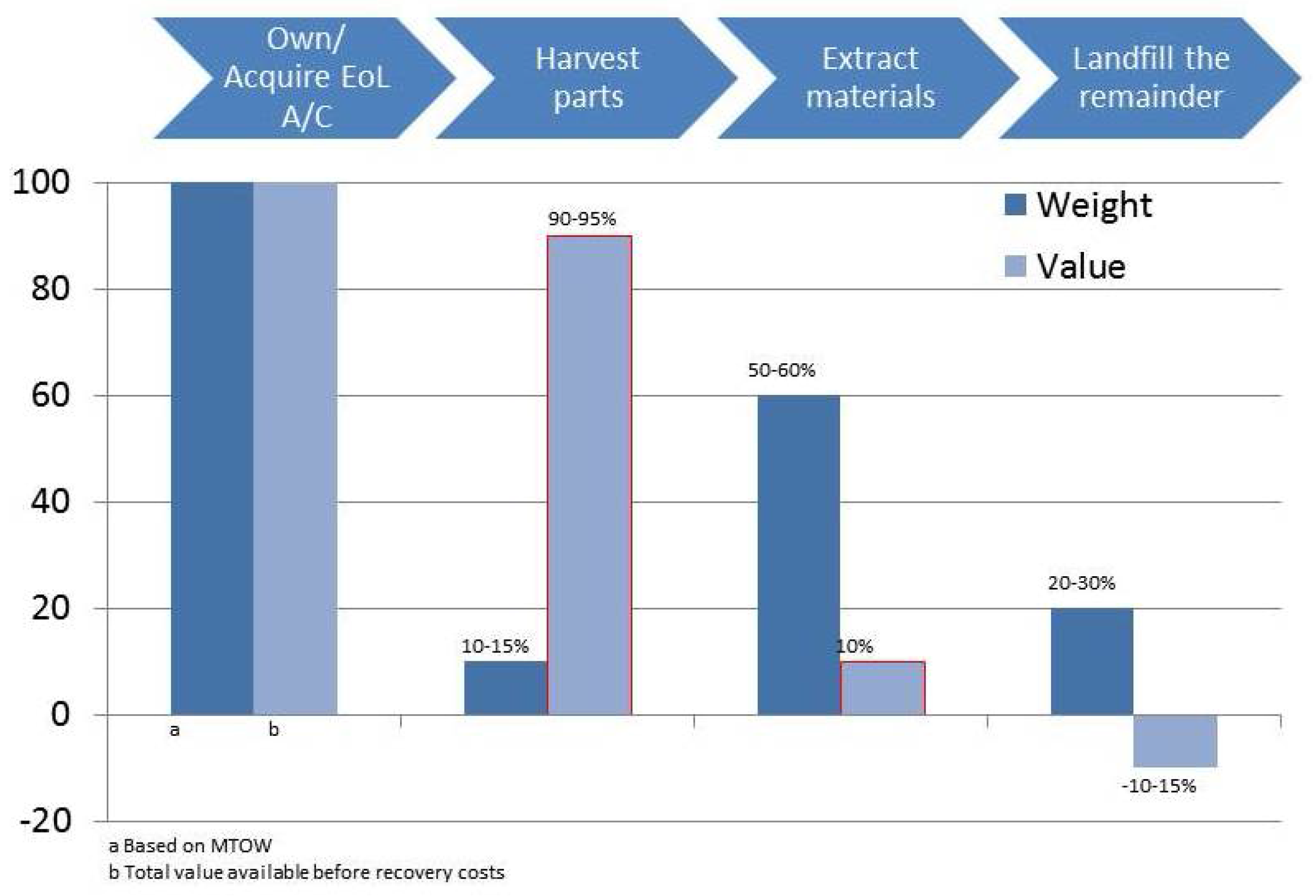

From a business perspective, material recovery from obsolete aircraft is second in importance to part re-use.

Figure 2 provides a mass and value estimation of the end of life aircraft. About ninety percent of the total end of life aircraft value is generated from parts harvesting and re-use according to air safety regulations. These operations are highly regulated, and open only to certified companies. The materials value share of the aircraft (not taking the re-use components into account) only amounts to 10% of the aircraft, and thus is in the same range as the disposal cost for hazardous materials and components. The material value of the structure (scrap value) is in the same order of magnitude as the typical cost of ferry flights from Europe to the US (approx. 50,000–100,000 Euro) [

1].

The composition of aircraft structures can be seen in

Table 1. In recent years, the use of carbon fibre reinforced and other composites has been intensified, but the aircraft to be retired in the coming years will still mainly contain aluminium and other metals as their main constituent. Main aircraft elements are structure (body with approx. 20% of the total aircraft mass, plus wings, fin and elevator covering approx. 28%), engines (15%), landing gear (9%) and other components (28%) [

3].

Table 1 gives the structure composition (without engines, auxiliary power unit, landing gear and some avionic equipment).

3.3. Aircraft Structure

Aluminium (7075, 6061, 6063, 2024, 5052 alloys) is the dominant material for aircraft structures, skin, wings, fin and elevator and also some electrical components [

5]. Recycling trials have shown the feasibility of high-value alloy material recovery, although quality standards for material application in primary aircraft structures have not been reached [

6]. Other prevalent alloys of the structure are titanium and steel.

3.4. Aircraft Engines

The physical and chemical stresses in the aircraft engine require the use of high-value materials such as nickel, cobalt, and rhenium “super alloys” for their high strengths at high temperatures. Moreover, titanium alloys, as well as tungsten, gold and platinum coatings, may be applied.

92% of all the aircraft placed into service are equipped with two engines, 7% with four engines, and 1% with three engines [

7], not covering the auxiliary power unit (APU). With a medium mass of the engines being about 3 metric tons, based on the total fleet size of 21,056 the engine mass sum of 168,000 metric tons can be calculated, mainly formed by titanium and nickel alloys, and other high-value materials.

An aircraft engine contains several metals and alloys that could be recycled not only due to ecological reasons but also to economic reasons.

Table 2 gives the amount of the range of metals [

8] and

Table 3 a mass forecast on a global perspective for active and stored engine material in aircraft based on an average number of 2.1 engines per aircraft. This figure was derived from an investigation into the ten airlines in Europe and Northern America with the highest turnover (2013). The population of aircraft for this investigation was 7246 [

1].

Using the mentioned figure of 25,546 aircraft being used actively or stored as a basis, and assuming the above-mentioned average engine number of 2.1 engines per aircraft, it can be calculated that there is a potential of an overall number of 53,646 engines.

Focusing on the number of 4490 stored aircrafts currently available, it could be assumed that out of this total figure of 53,646 engines, approximately 9429 engines might be available for recycling at short notice.

3.5. Aircraft Interior and Other Materials

From a materials availability point of view, during the use phase, the maintenance and overhaul steps, especially, of the engines are relevant, but what is even more important may be the cabin interior replacement, which happens every five to ten years, and with each leasing status change. Taking into account an airliner life span of about 26 years [

9], each aircraft might produce a minimum of about three to four obsolete cabin interiors during its use phase.

The interior mass of a typical B737 is about 5 metric tons, whereas the larger B747 carries about double this mass. The high share of composites renders the interior mainly non-recyclable as of today. The same is basically true for the glass fibre insulation material attached to the structure, which in case of production before 1995 is regarded to be potentially carcinogenic.

3.6. Total Availability of Aircraft

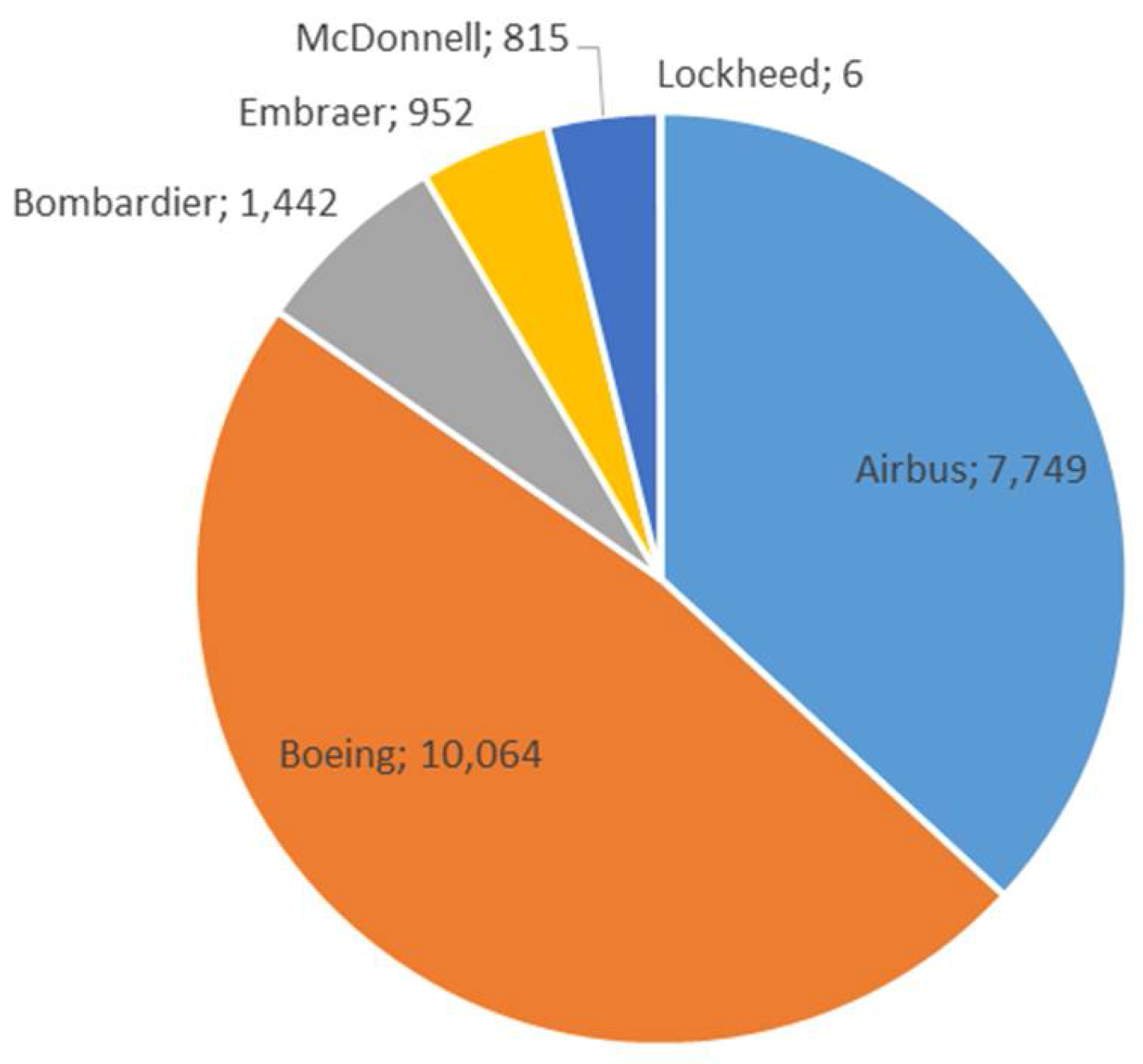

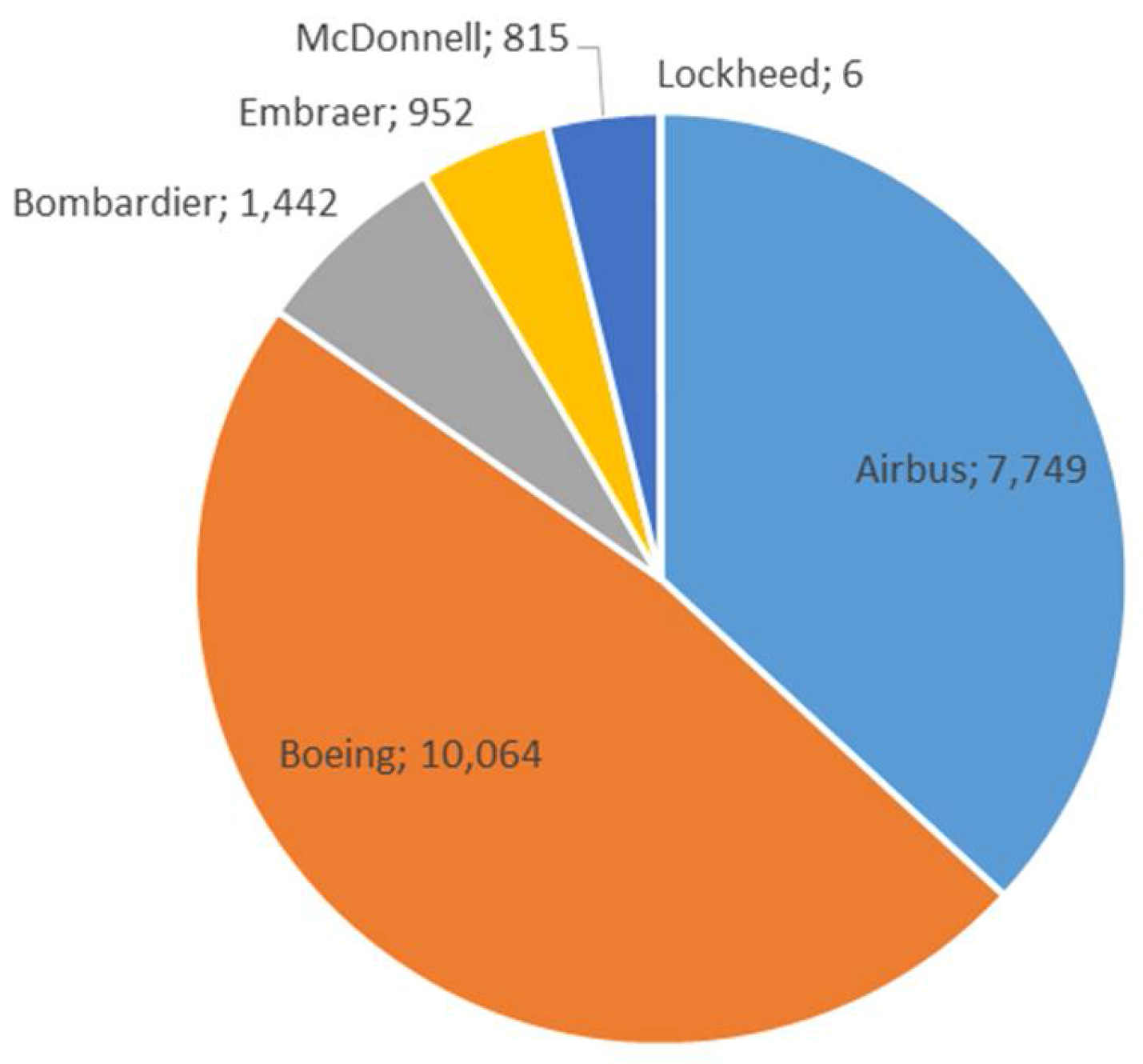

As

Figure 3 shows, there are currently 21,028 commercial narrow- and wide-body aircraft (with a full dataset) in use on a worldwide level, with Boeing as the most important manufacturer.

Consequently, about 1,283,985 tons of aircraft (structural) material is in use as of today. This calculation is based on an average aircraft mass of 61.06 metric tons. With an estimated aluminium share of 70% (

Table 1), the total aluminium stock amounts to 898,789 metric tons.

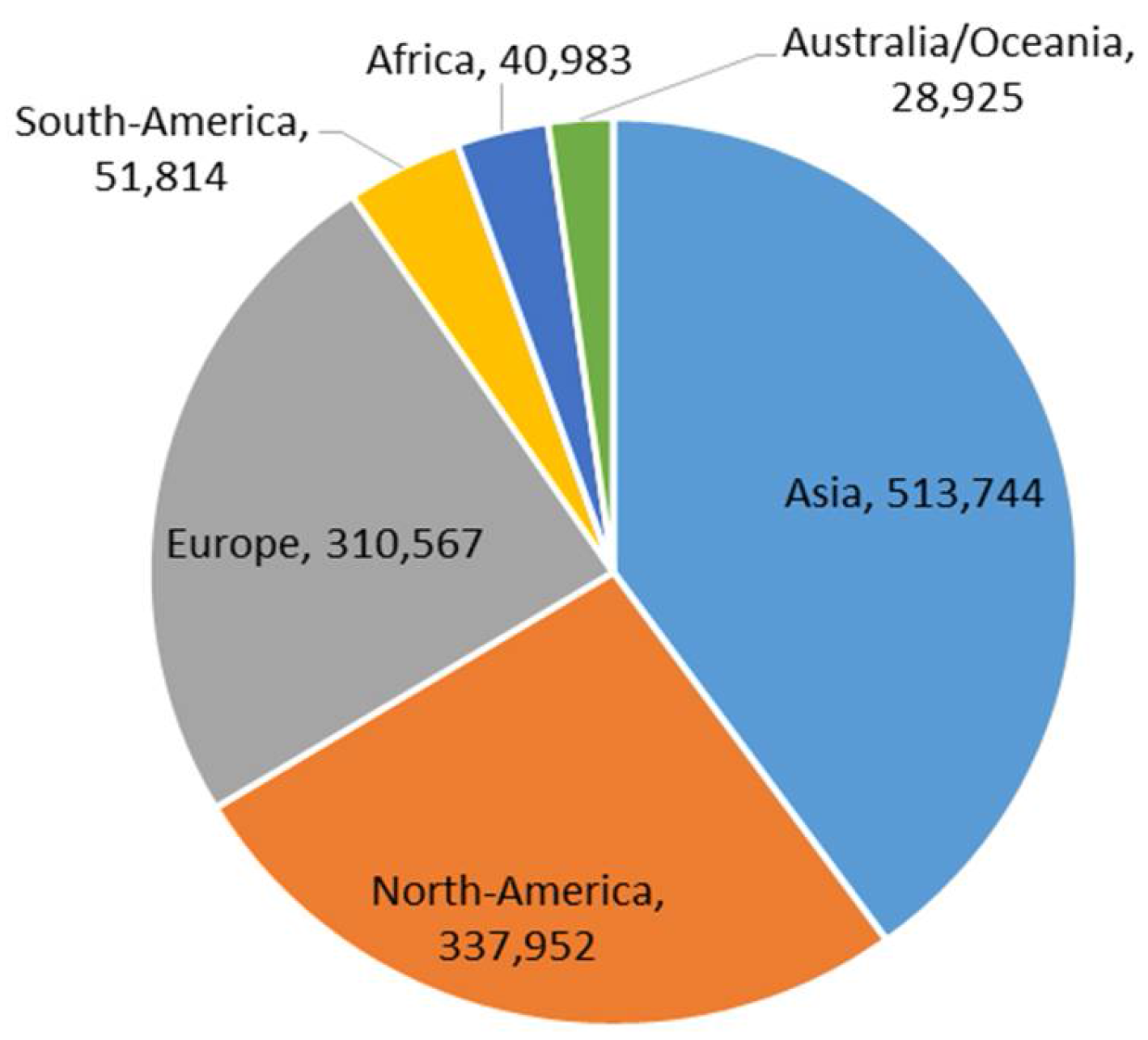

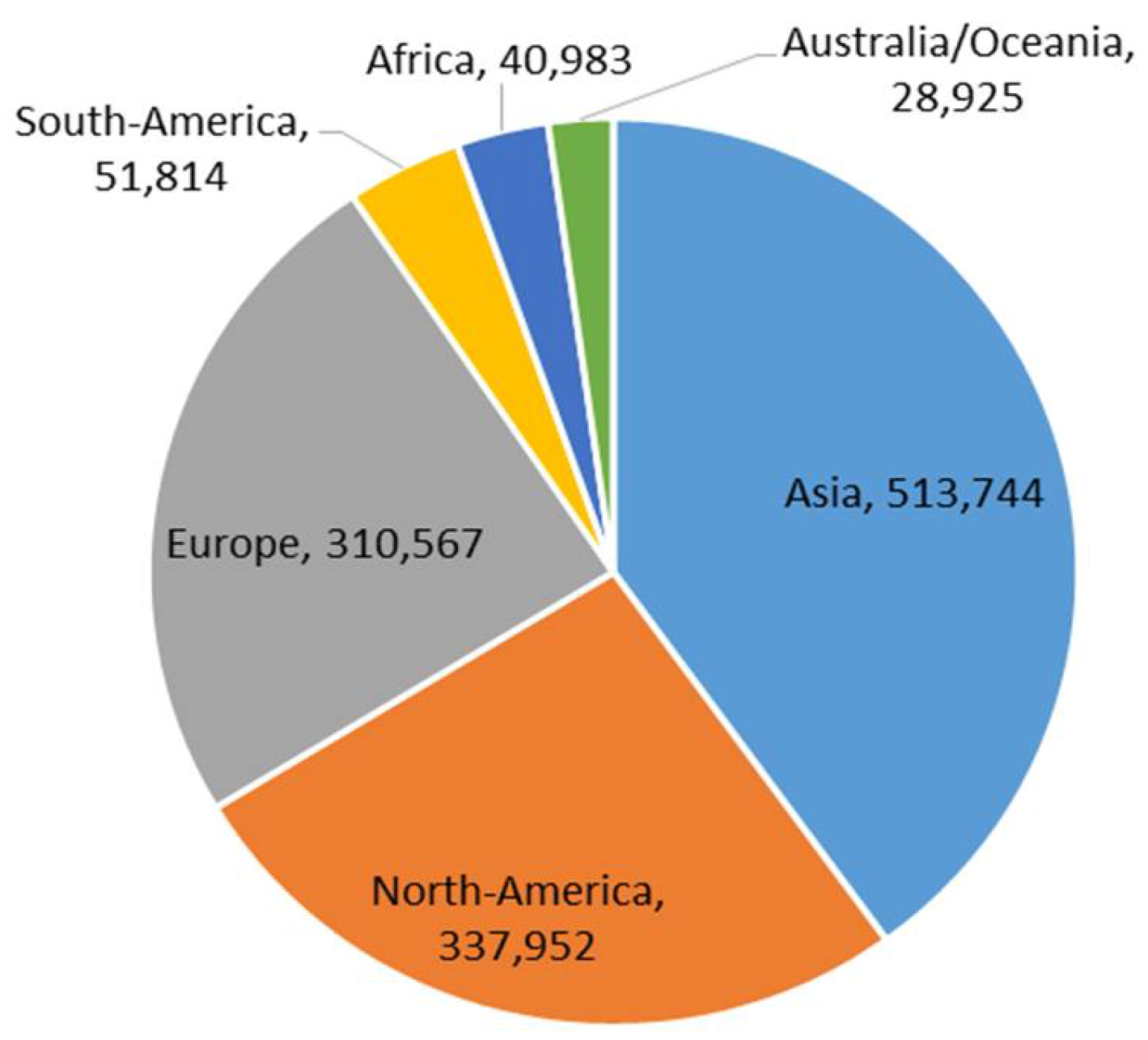

Figure 4 illustrates the share of the aircraft by continent, indicating the high importance of the Asian region and an equal share of about 25% each for Europe and North America.

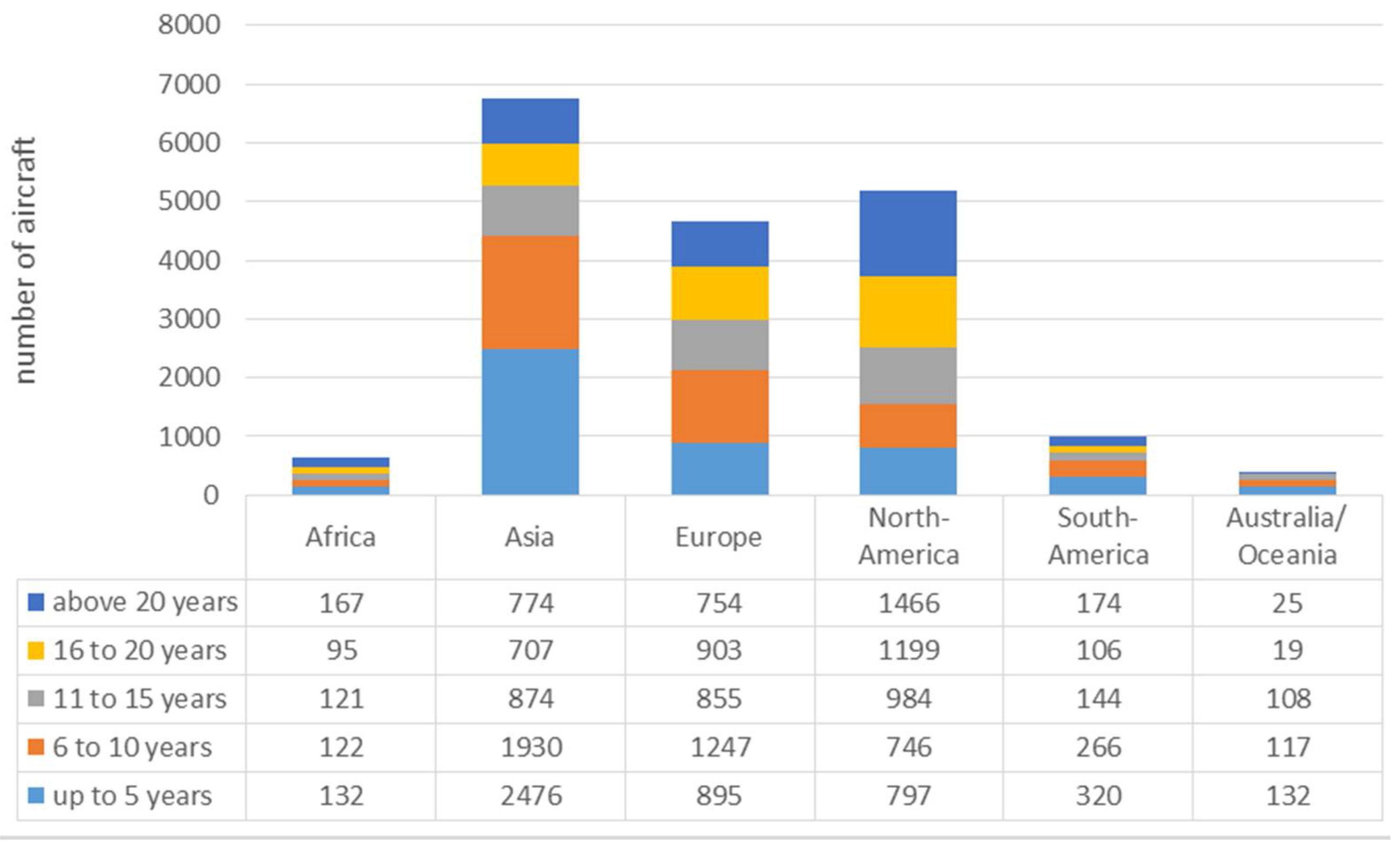

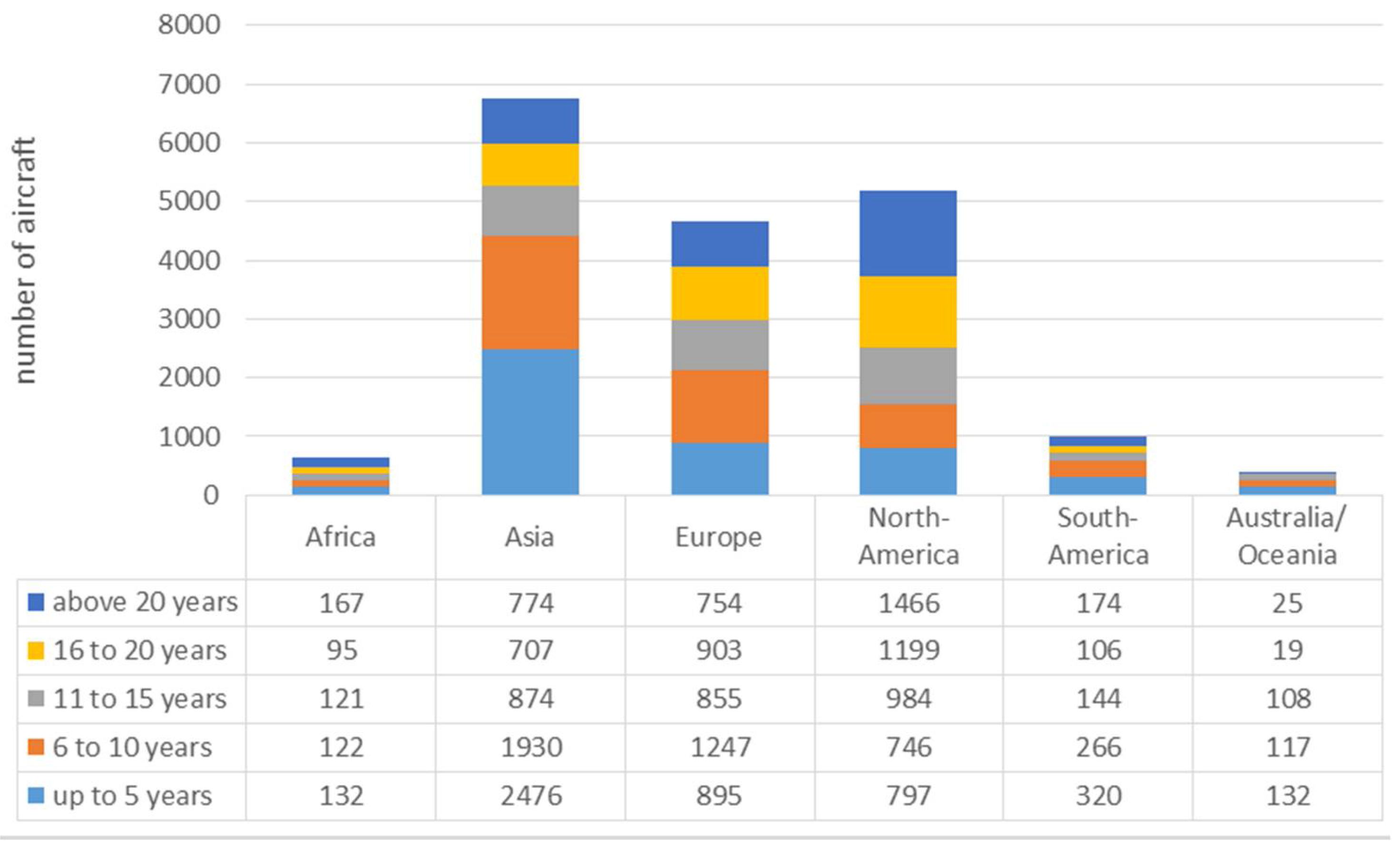

Regarding the time line of future availability, the fleet age has to be taken into account.

Figure 5 shows the high number of older aircraft (20 years plus) in North America, which is about the same range as the sum of the older European and Asian aircraft. In total, about 22% of today’s operating aircraft will reach their end of life phase in 10 or less years. These aircraft can be expected to retire in the coming years, amounting to 3360 aircraft or 205,162 metric tons of structural materials.

For decommissioning and recycling of retired aircraft specific regional recycling options are available: In North America, long-term aircraft parking and aircraft recycling has been a business for decades. Starting with military aircraft, operations were soon extended to the civilian fleet, providing great experience and numerous sites, so still today, European aircraft are transferred for end of life operations to the US by ferry flights [

10]. In Europe, one dedicated aircraft recycling site for the civilian airfleet is operated in Tarbes (France), partnering with an international waste management company, and with a parking space in Spain. Moreover, mobile solutions for dismantling are offered in Europe and worldwide, whereas it seems that on other continents mainly long-term parking for obsolete aircraft has the highest relevance.

Based on the data available it is possible to draw a scenario of the potential material composition of active aircraft. This leads to a model-specific forecast of the “flying stock” to forecast the masses divided in aluminium, steel, titanium, composites and other materials for the Boeing patterns 747, 757, 767, 777, 787 and the A300 model. The specific results for the different materials can be seen in

Table 4.

To maintain the high material properties of the aircraft metal scrap, which is mainly aluminium, identification and separation of the alloys used is of primary importance. To this end, handheld x-ray fluorescence technology is currently used. Future developments may also provide laser-induced plasma breakdown spectroscopy (LIBS) for stationary or mobile (handheld) identification and sorting. These sorting processes will not only yield general-purpose cast aluminium alloys, but the recycled aluminium alloy will qualify for aircraft use, but outside the primary or secondary structure only [

6]. Besides separation at the source, few technical options for removal of alloying elements in secondary aluminium processing are available, due to the chemical properties of aluminium [

11]. Thus, a cascade in material use can be observed [

12], which might also be caused by economic constraints such as specific alloy batches being too small to be treated economically. In the case of aircraft recycling, currently, the combination of identification methods is improving for alloy sorting, and the increase in scrap availability is favorable for closing high-value material cycles, along with the associated environmental benefits [

11,

12].

4. Conclusions

Currently, about 21,000 aircraft (airliner) are in use worldwide, and approximately 4500 aircraft are stored, but may return into use. Aircraft structural materials cover about 48% of the total aircraft mass, the mass share of engines lies at 15%.

With a mean mass of about 60 metric tons per aircraft, the total flying metal stock in aircraft structures amounts to almost 1.3 million metric tons, plus about 170,000 metric tons of engine material. The most prevalent single materials are aluminium (about 0.9 million metric tons) from the structure and 7500 metric tons from the engines. The engines are much more important as a stock of super alloys, with a potential of 66,000 metric tons of titanium and 35,500 metric tons of nickel alloys in the entire fleet.

In the coming decade, a minimum of more than 200,000 metric tons of structural material can expected to become obsolete out of this stock. For the metal alloys, current improvement of alloy identification and sorting techniques along with the increase of scrap availability are favorable for closing high value material cycles. Composites will become an end of life issue only from the medium-term perspective, as the current fleet of older aircraft only carries a one-digit mass percentage portion of composites.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}