The German Wine Market: A Comprehensive Strategic and Economic Analysis

Abstract

1. Introduction

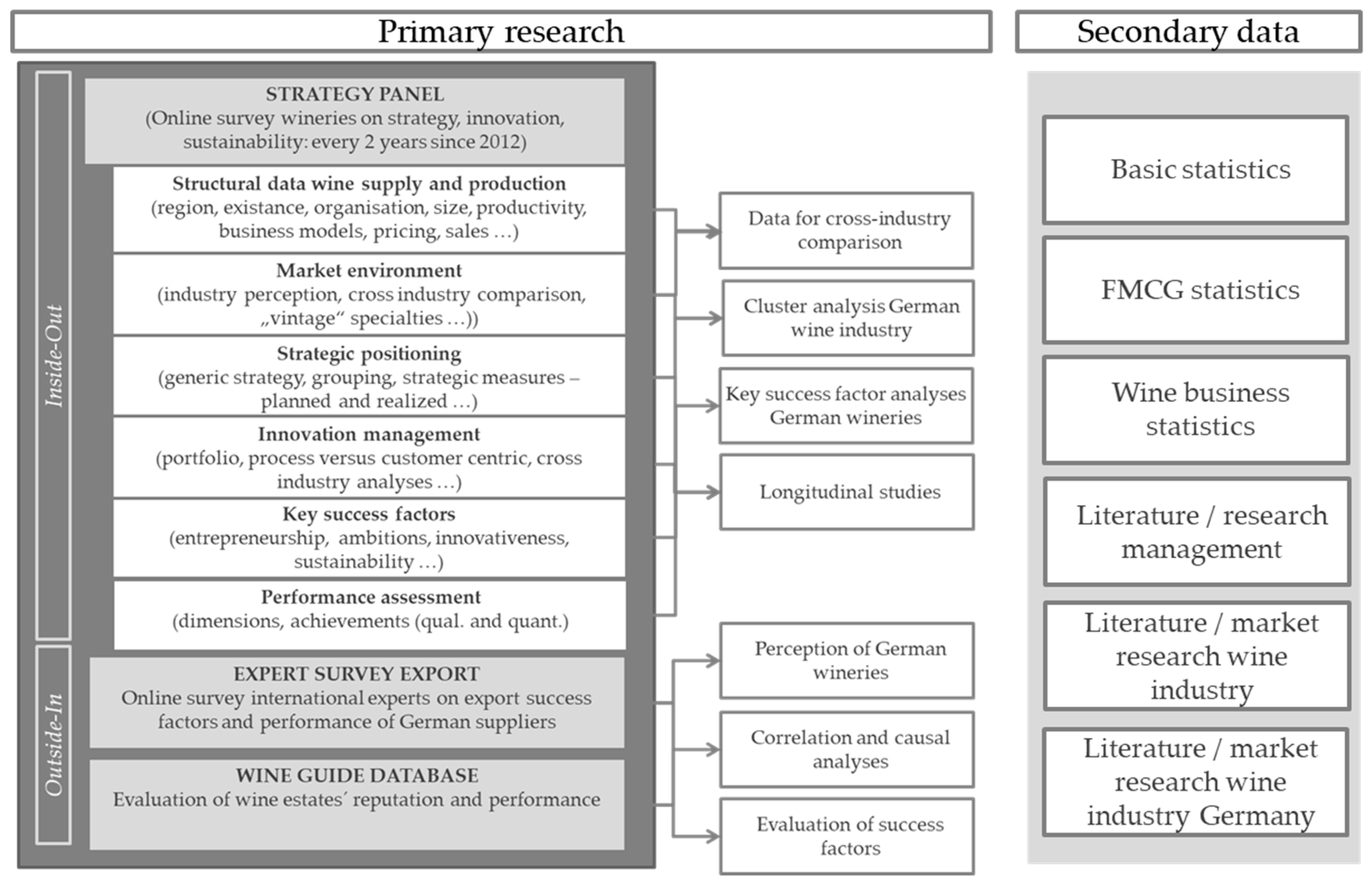

2. Materials and Methods

3. Economic and Strategic Market Analysis: The German Wine Market

3.1. Wine History and Relevance

3.2. The German Wine Supply Side

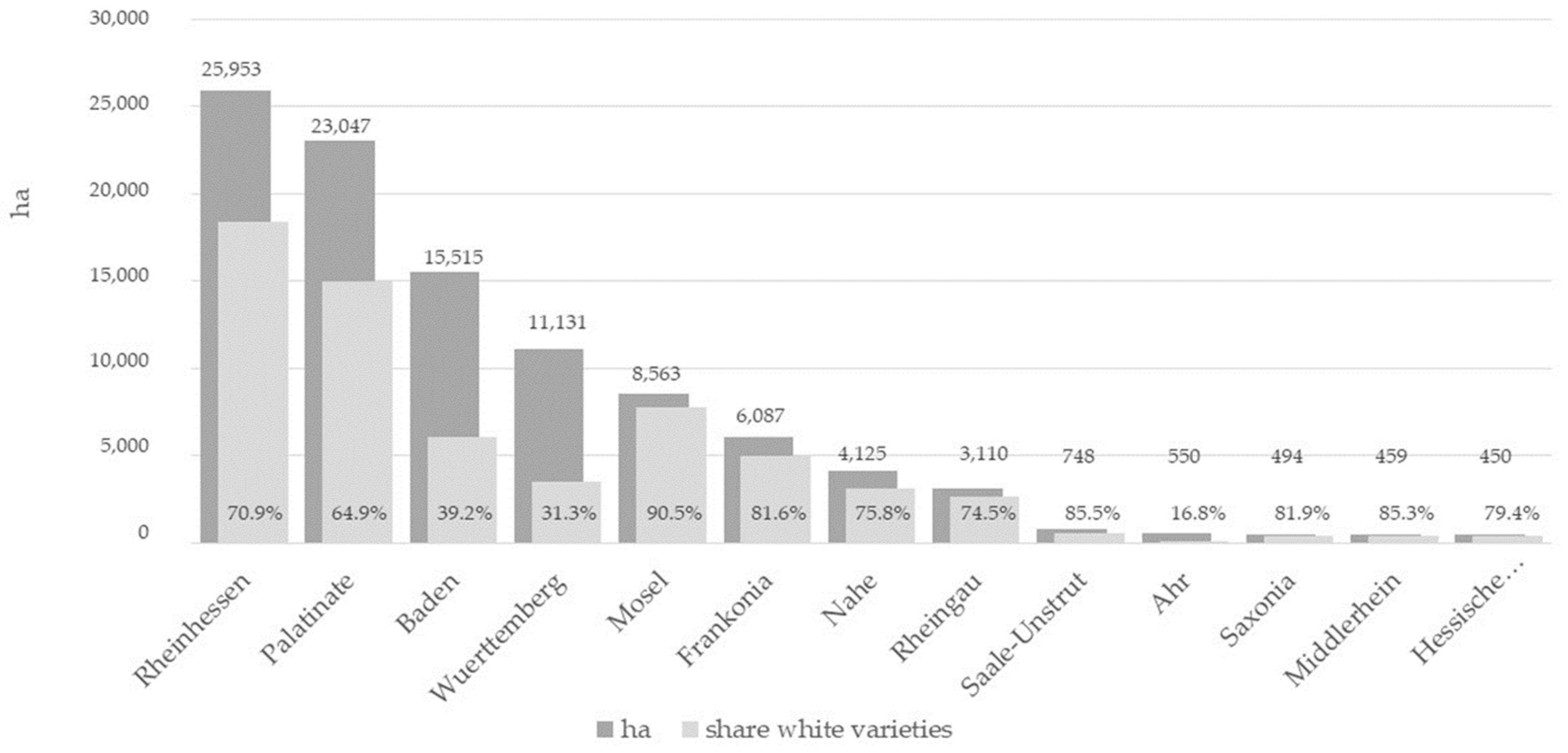

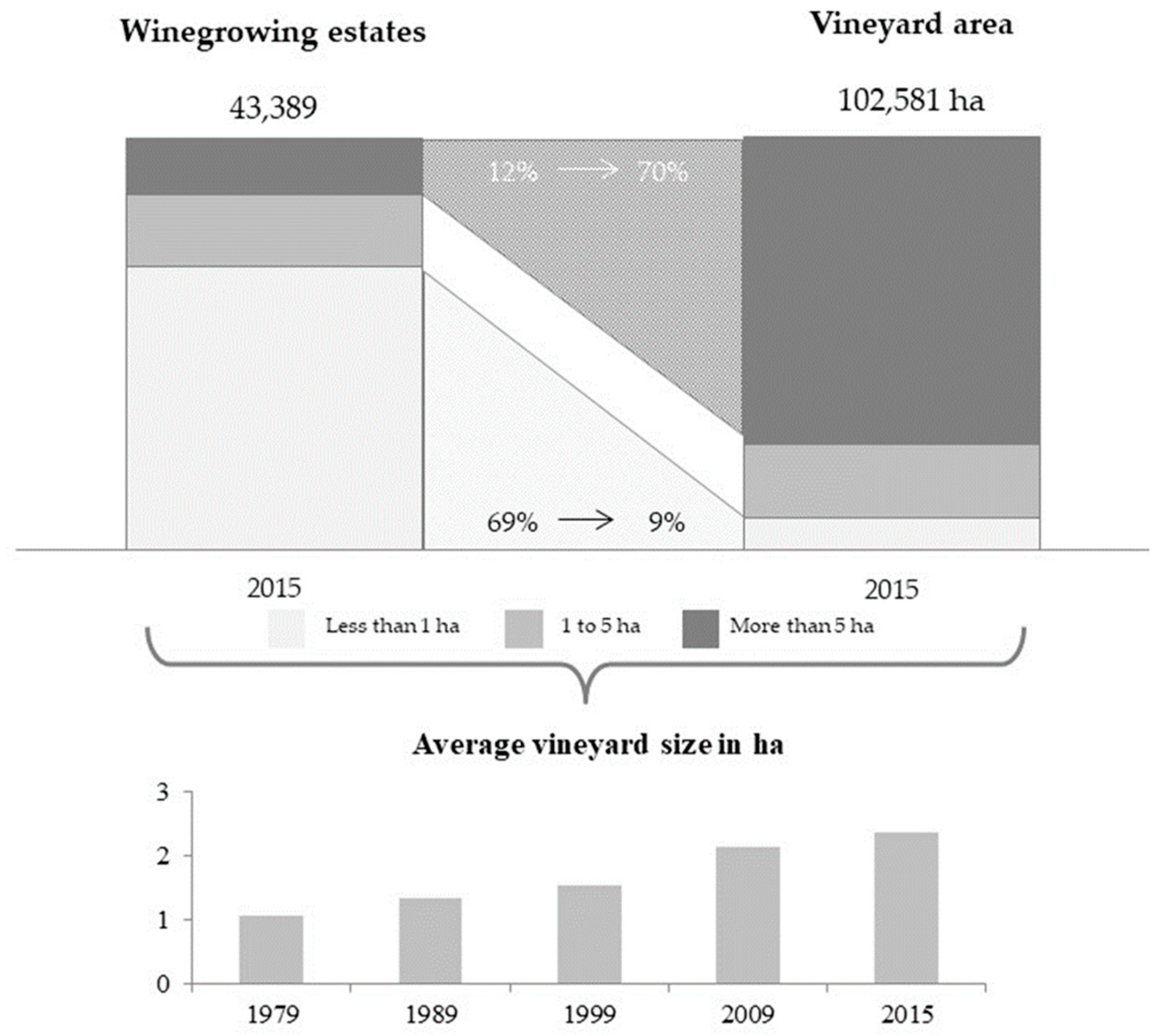

3.2.1. German Wine Production

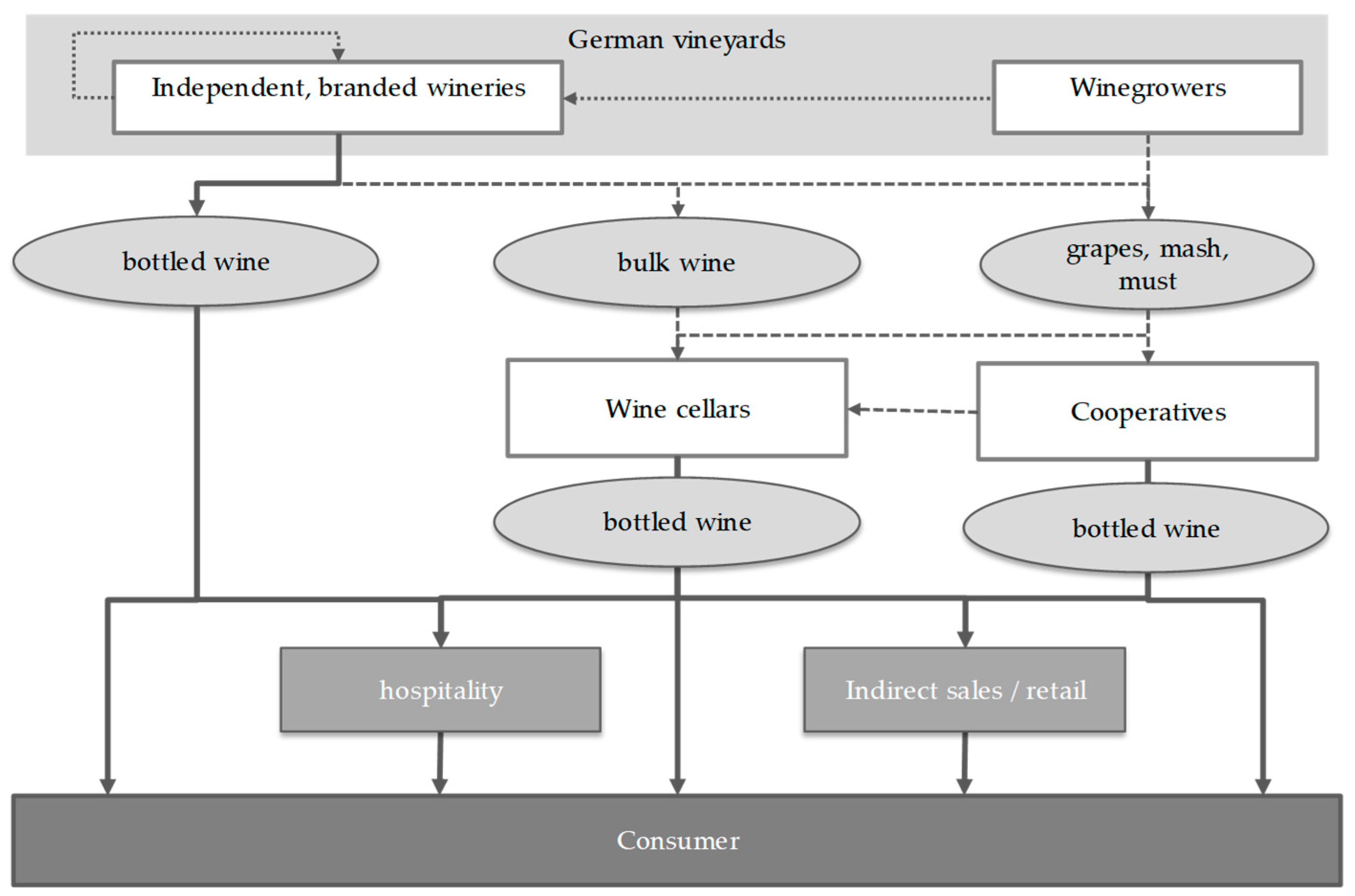

3.2.2. Supplier Typology

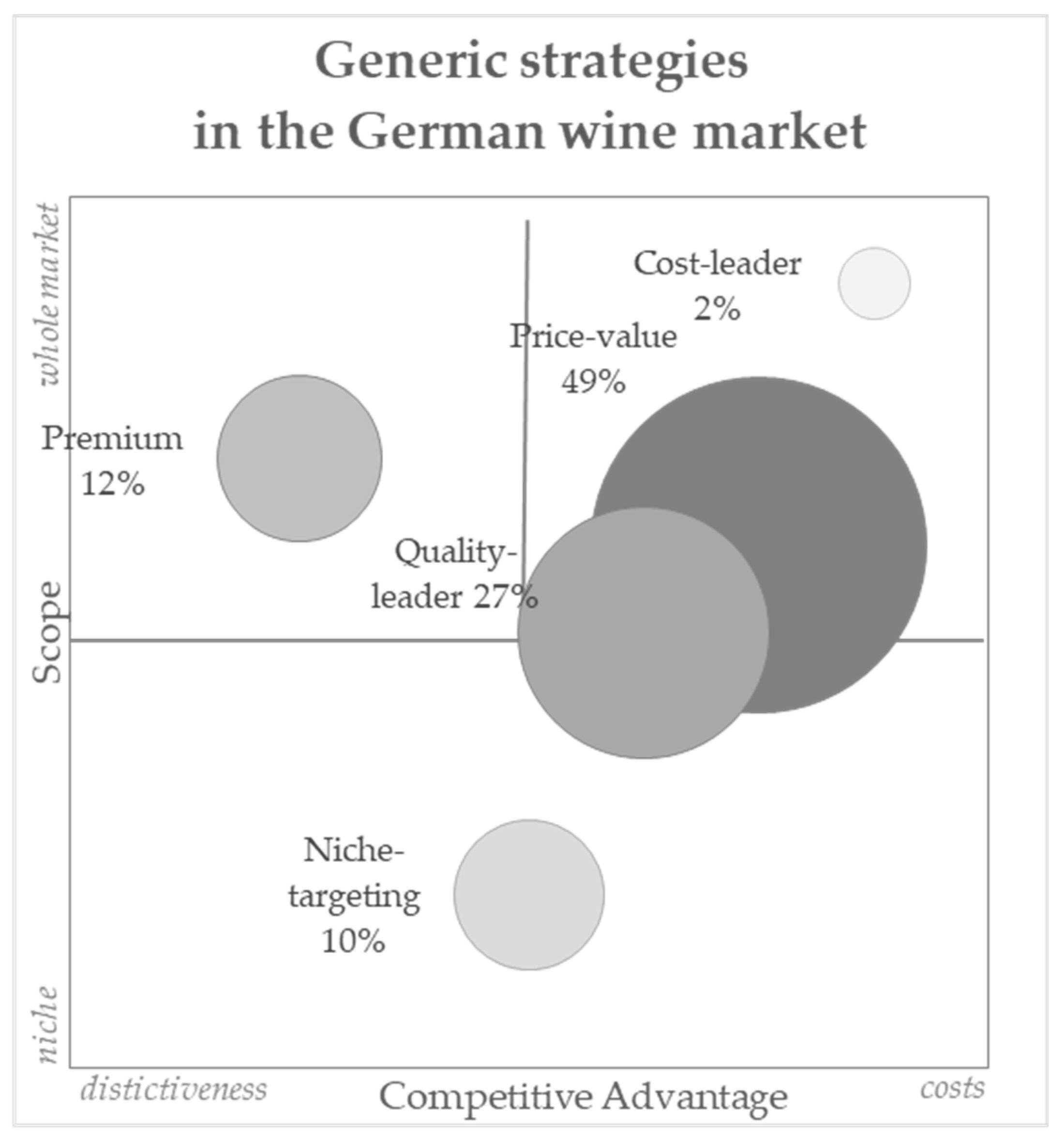

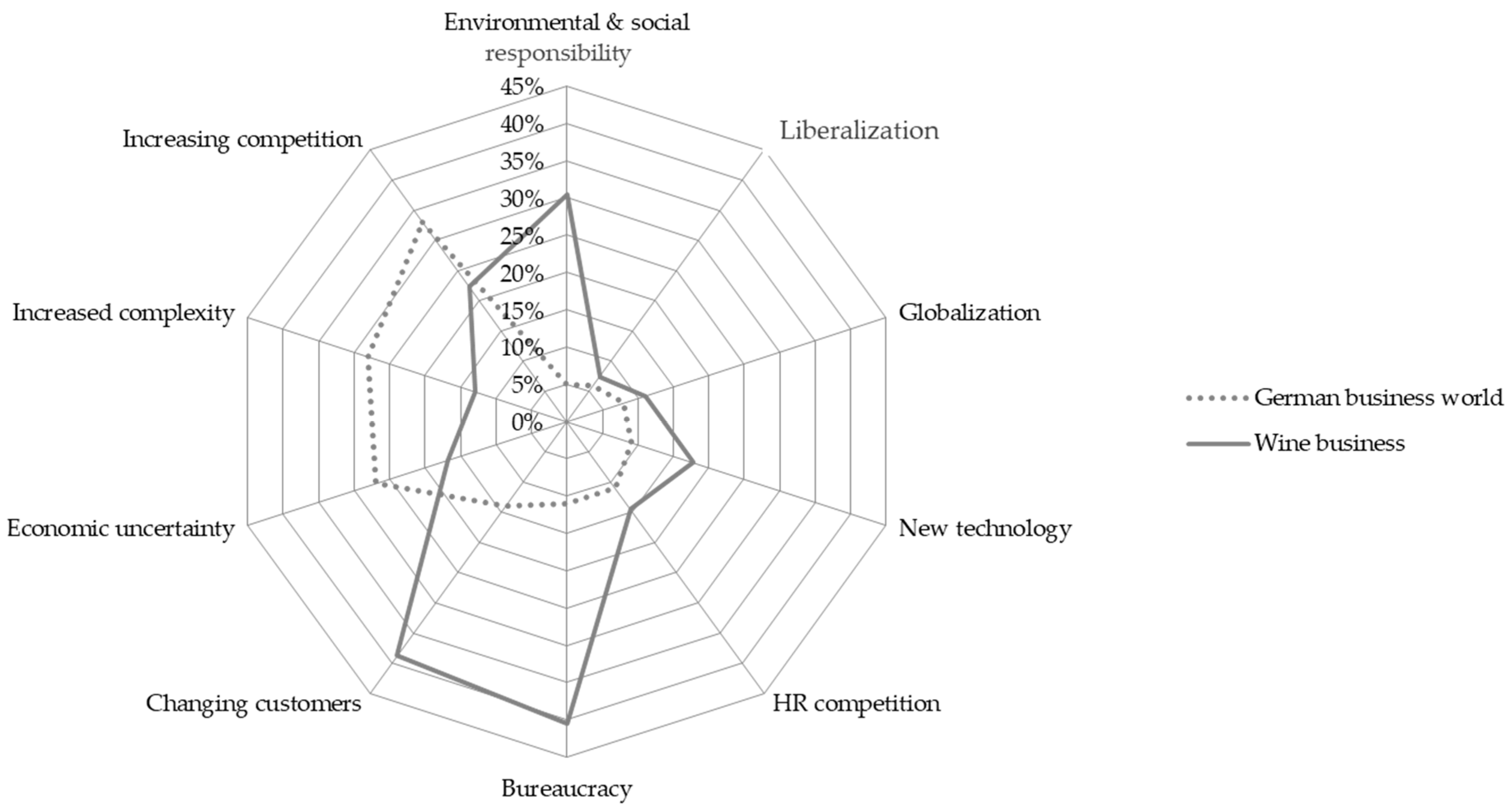

3.2.3. Strategic Positioning and Innovation Management

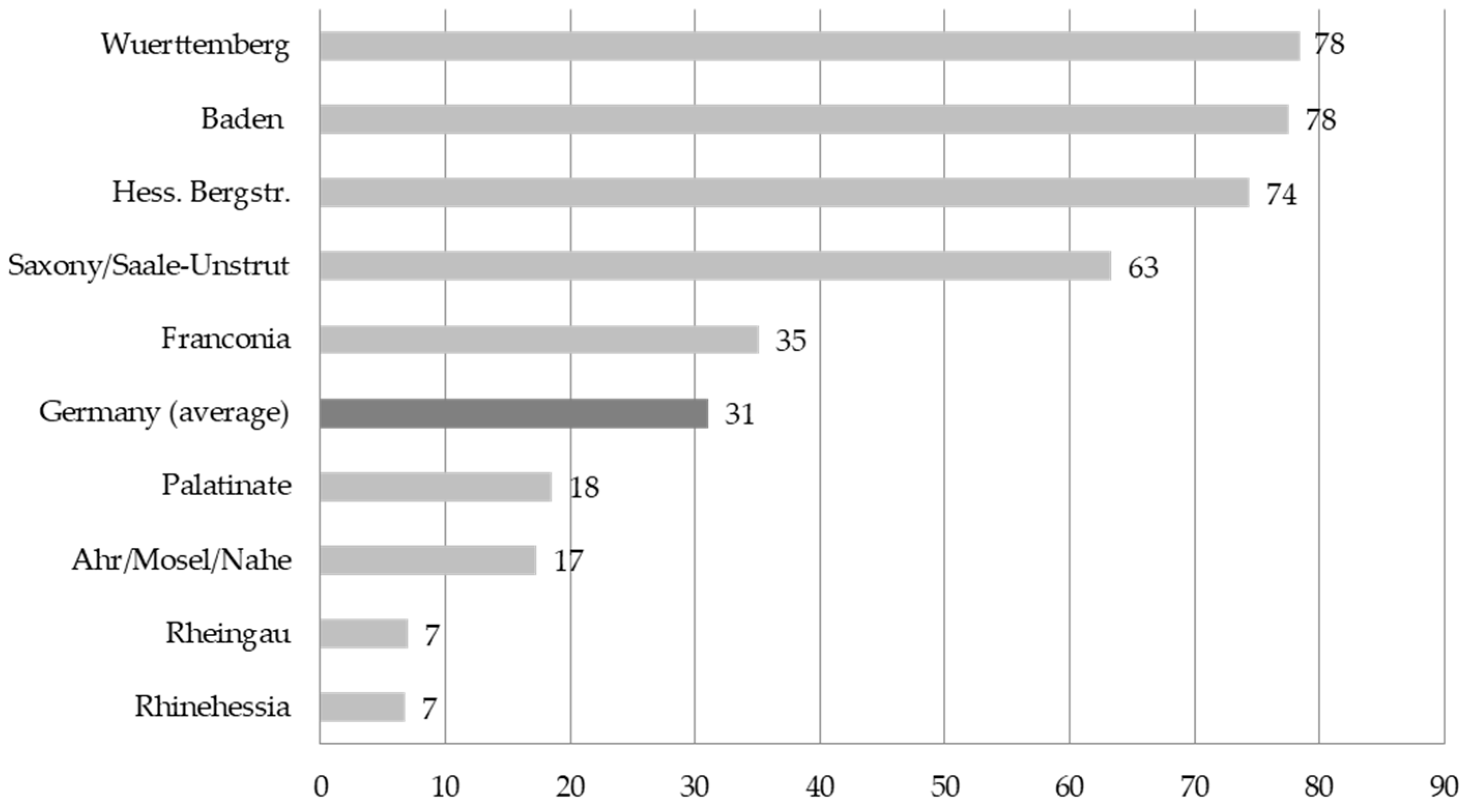

3.2.4. Environmental Perception

3.3. Demand Perspective: From Wine Consumption to Reaching Consumers

3.3.1. Wine as Product Category within Beverages

3.3.2. Consumer Preferences in Wine

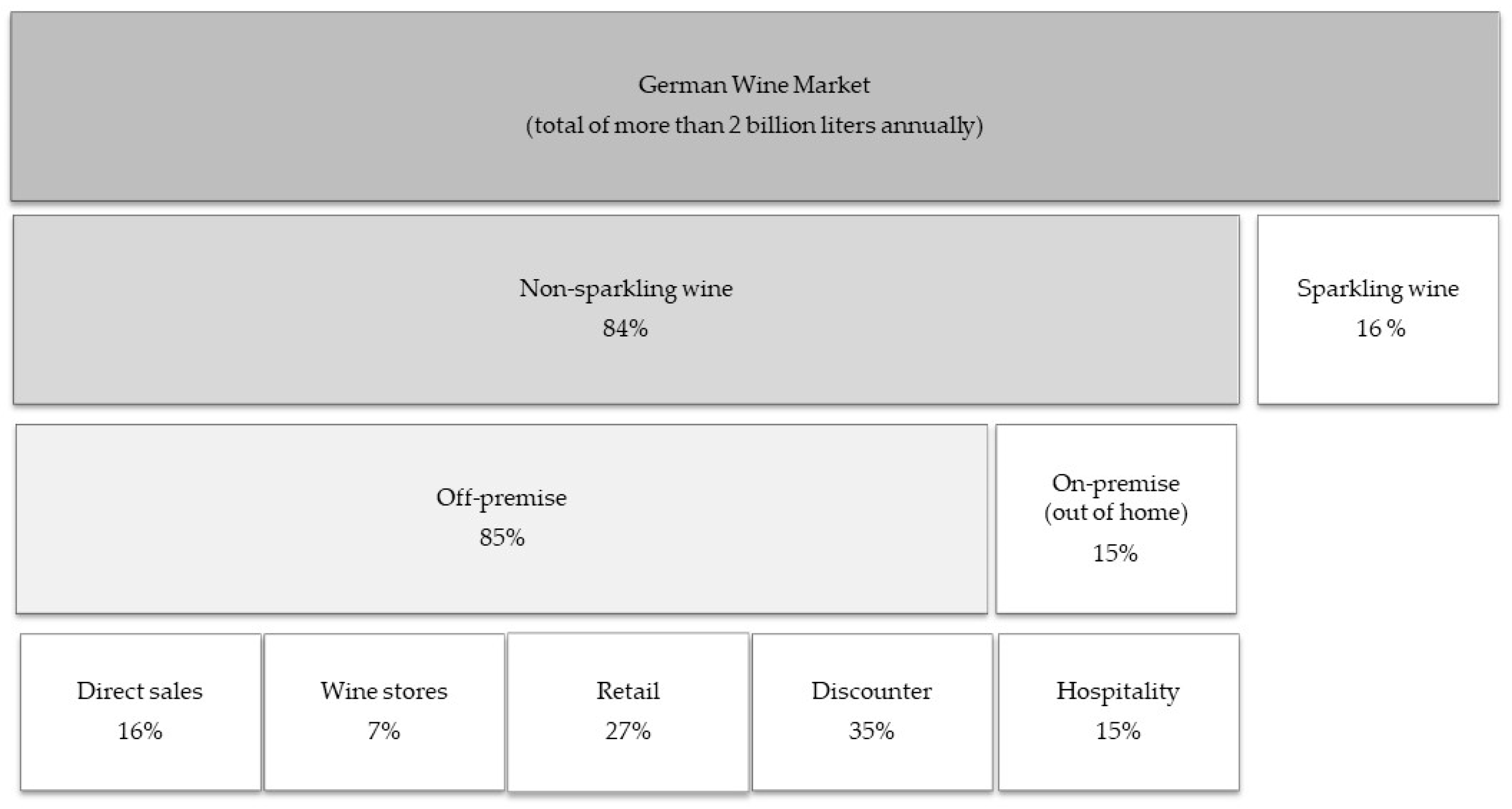

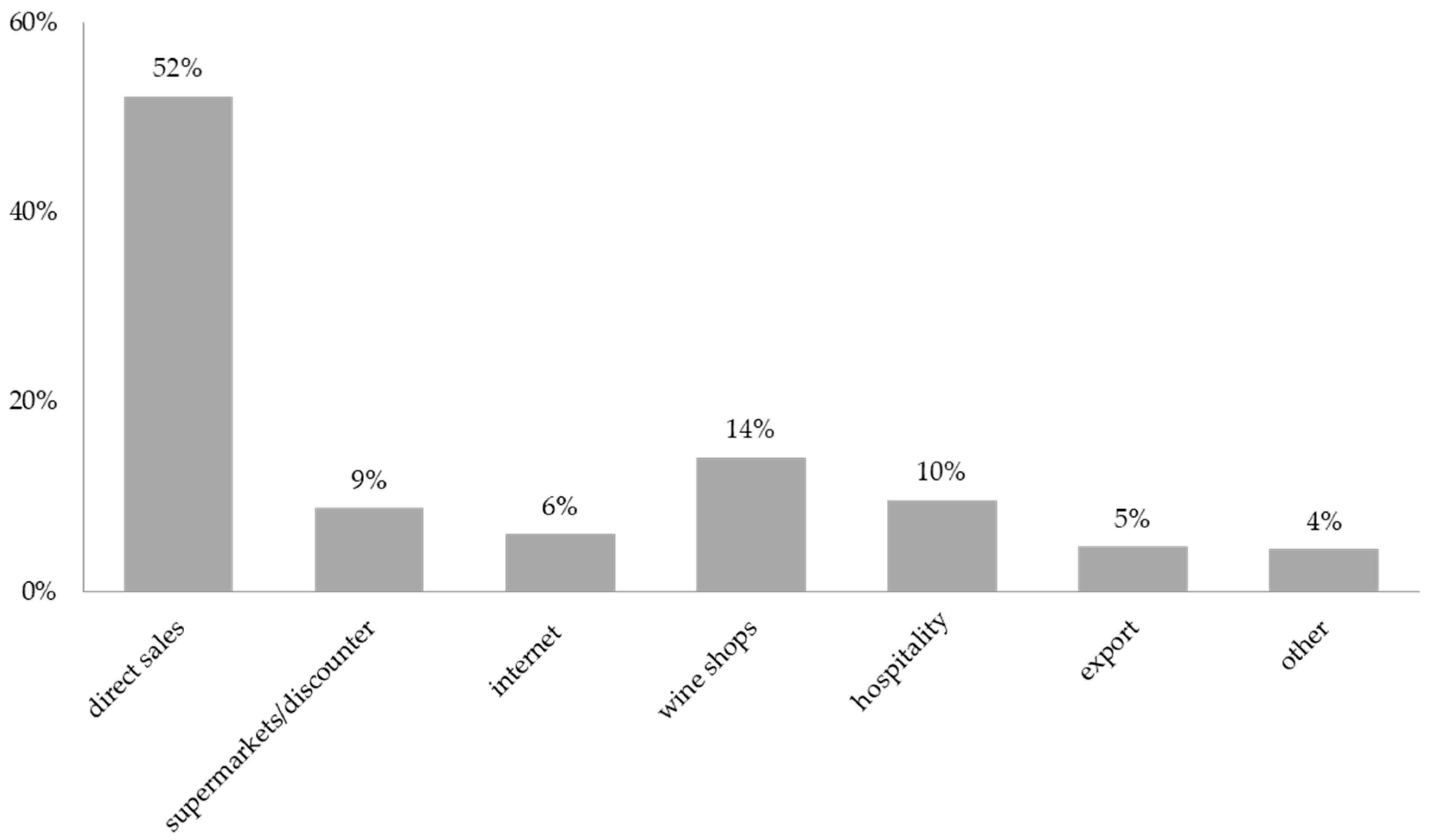

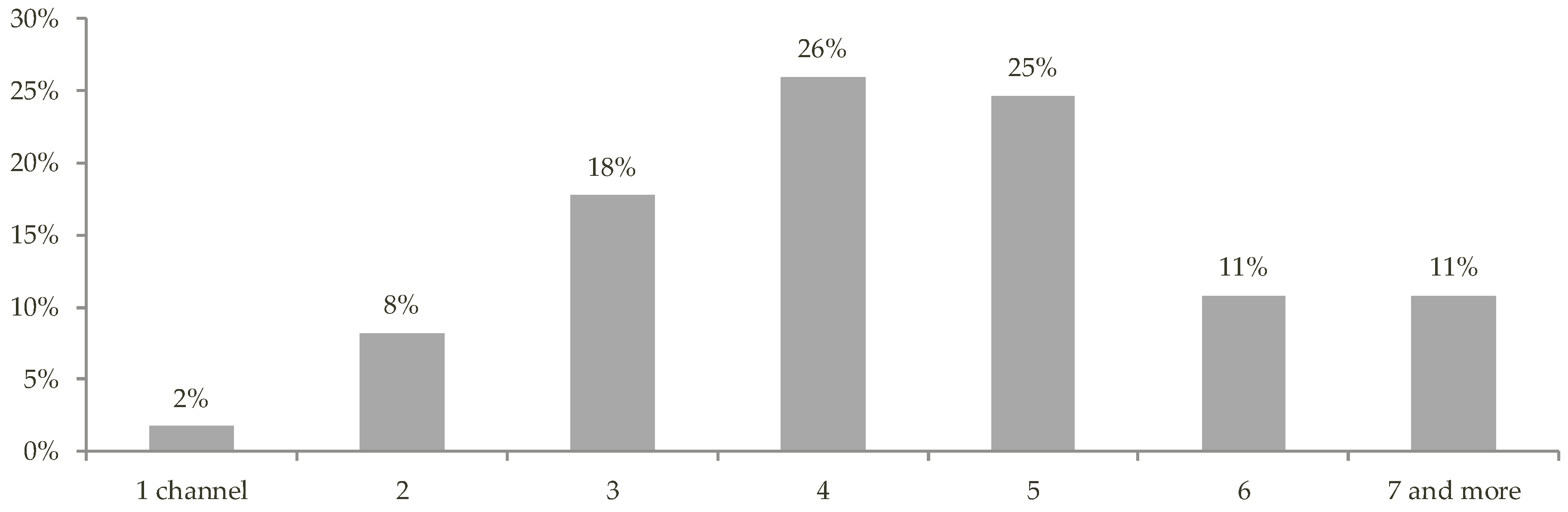

3.3.3. Reaching the Consumers: Distribution and Channel Perspectives

- (a)

- direct sales to consumers: all participants stated to actively serve their customers directly;

- (b)

- sales to restaurants being of relevance in importance in volume sold (exceeding perceived relevance by secondary market research), but also being a lever for brand communication;

- (c)

- specialized wine retail to serve for the distribution of more premium product ranges; and

- (d)

- online sales to grow and split the wine estate population [133].

3.3.4. Sparkling Wine—A Specific Segment in the German Wine Market

3.3.5. Market Volume, Growth, and Implications for Suppliers

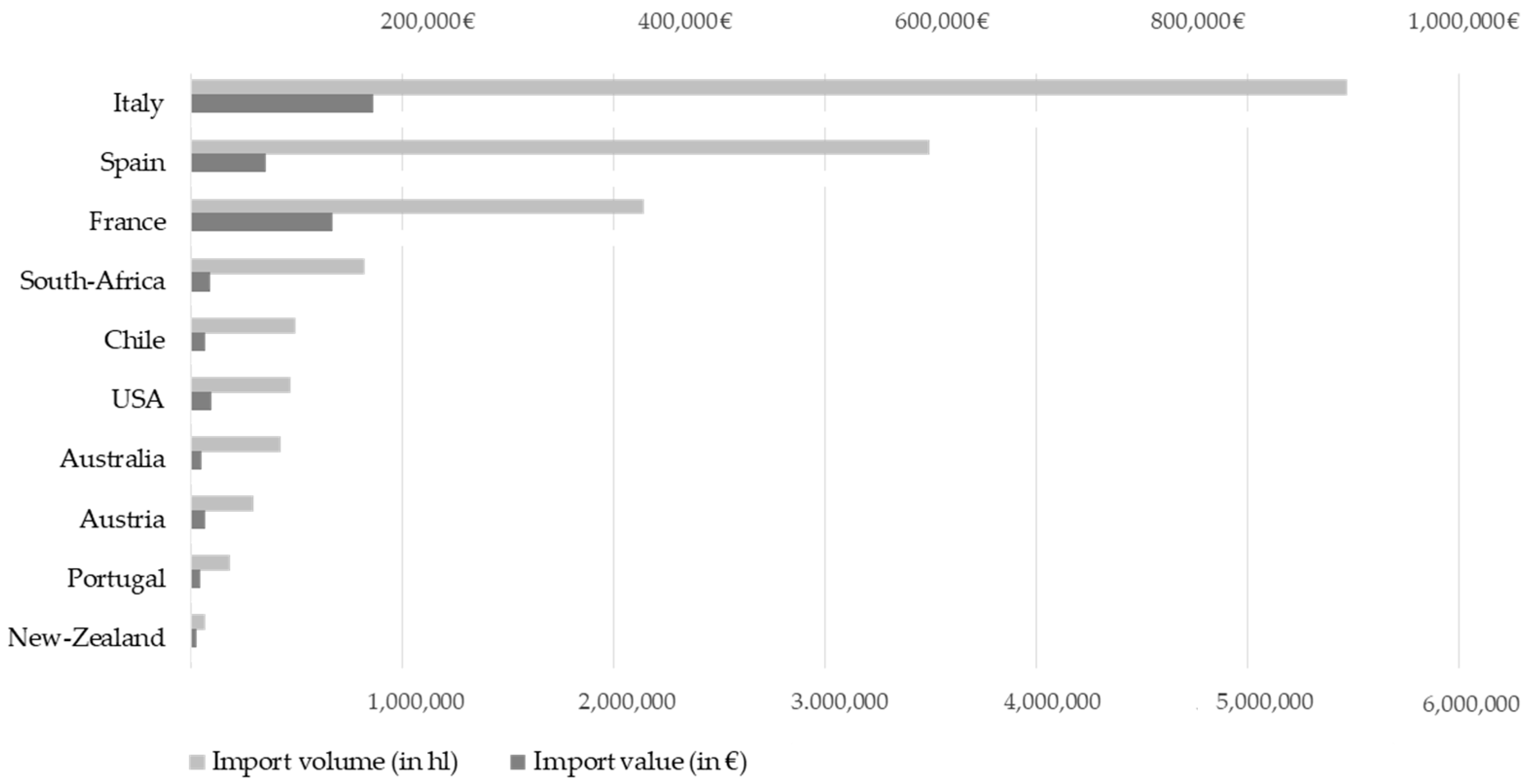

3.4. Import and Export Perspectives

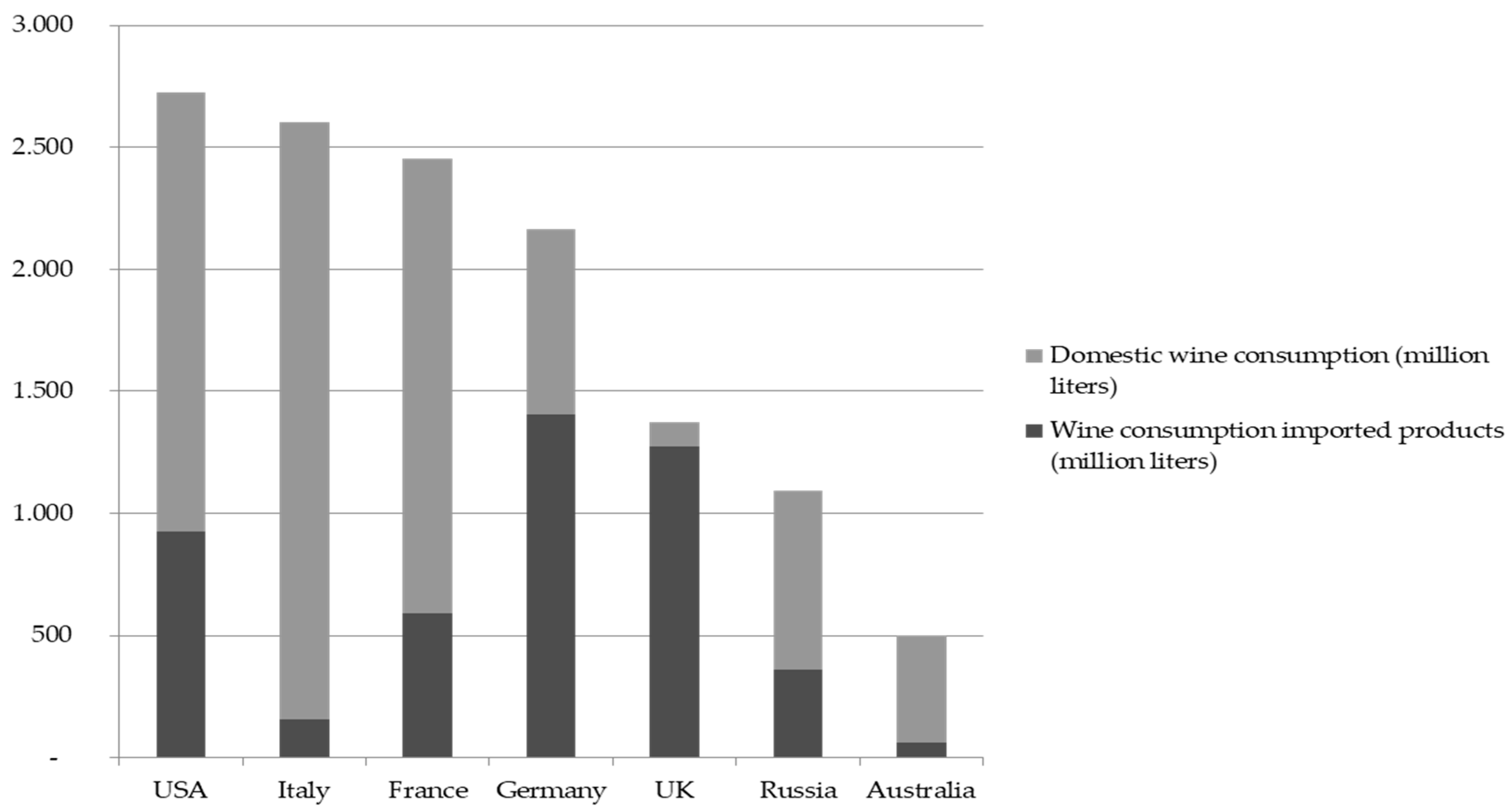

3.4.1. Germany as a Longstanding Wine Import Champion

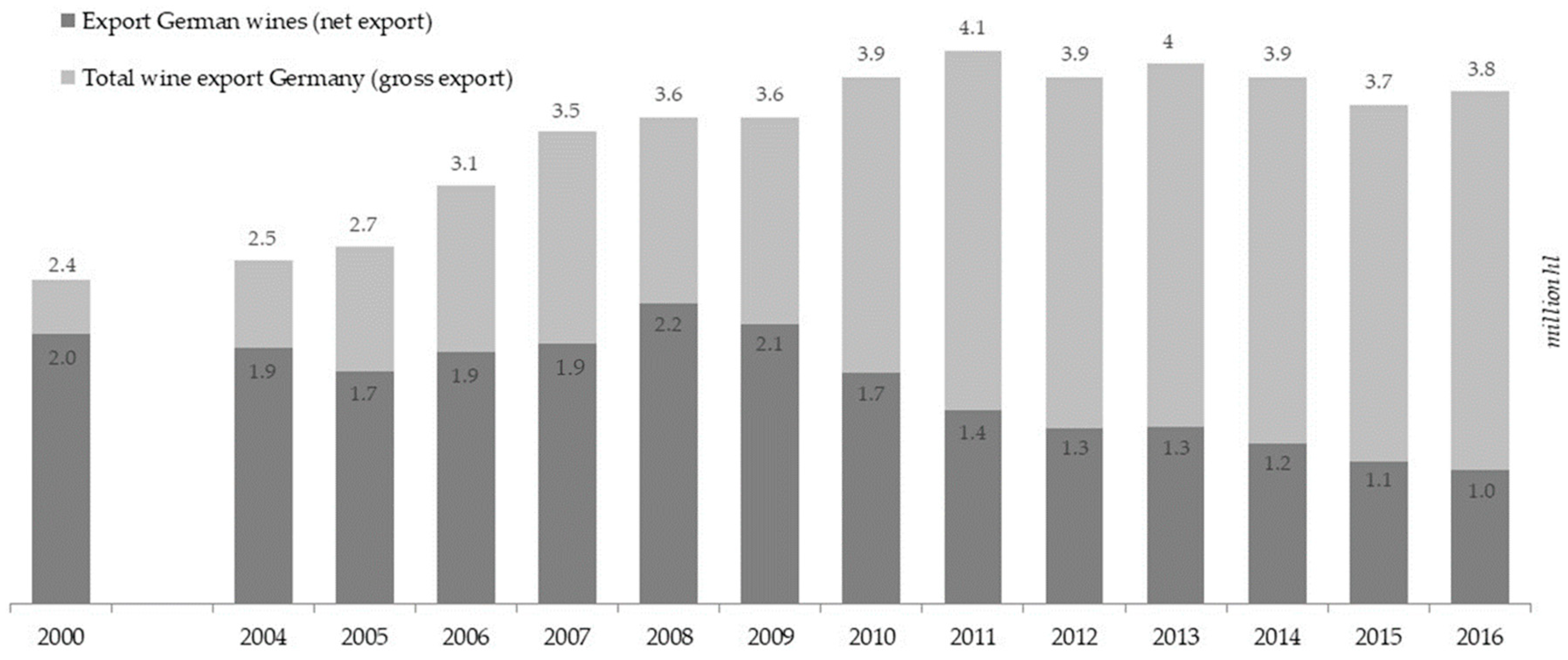

3.4.2. Export Performance

4. Discussion and Implications

Funding

Conflicts of Interest

References

- Rückrich, K. Daten zur Weltweinwirtschaft. Der Deutsche Weinbau 2018, 10, 1. [Google Scholar]

- OIV. World Vitiviniculture Situation 2016; OIV: Paris, France, 2016. [Google Scholar]

- Porter, M.E. Competitive Strategy: Techniques for Analyzing Industries and Competitors; Free Press: New York, NY, USA, 1980. [Google Scholar]

- Porter, M.E. What Is Strategy? Harvard Business Review; Harvard Business School Publishing: Boston, MA, USA, 1996; Volume 6, pp. 61–78. [Google Scholar]

- Besanko, D.; Dranove, D.; Shanley, M.; Schaefer, S. Economics of Strategy; John Wiley & Sons: Hobeken, NJ, USA, 2009. [Google Scholar]

- Burns, T.; Stalker, G. Mechanistic and organic systems. In Classics of Organization Theory; Harcourt College Publishers: Fort Worth, TX, USA, 1961; pp. 201–205. [Google Scholar]

- Chandler, A.D. Strategy and Structure: Chapters in the History of the Industrial Enterprise; MIT Press: Cambridge, MA, USA, 1990; Volume 120. [Google Scholar]

- Hannan, M.T.; Freeman, J. Structural inertia and organizational change. Am. Sociol. Rev. 1984, 49, 149–164. [Google Scholar] [CrossRef]

- Hoffmann, F. Organisation-Umwelt-Beziehungen in der Organisationsforschung. Klassische und neoklassische Organisationstheorien: Organisationstheoretische Ansätze, Munich; 1981; pp. 103–111. [Google Scholar]

- DeSarbo, W.S.; Grewal, R.; Wind, J. Who competes with whom? A demand-based perspective for identifying and representing asymmetric competition. Strat. Manag. J. 2006, 27, 101–129. [Google Scholar] [CrossRef]

- Miles, G.S.; Chales, C.; Sharfman, M.P. Industry variety and performance. Strat. Manag. J. 1993, 14, 163–177. [Google Scholar] [CrossRef]

- Miller, D. Configurations of strategy and structure: Towards a synthesis. Strat. Manag. J. 1986, 7, 233–249. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive strategy, structure and firm performance. Harv. Bus. Rev. 1998, 76, 77–90. [Google Scholar] [PubMed]

- Miller, D. The structural and environmental correlates of business strategy. Strat. Manag. J. 1987, 8, 55–76. [Google Scholar] [CrossRef]

- Orth, U.R.; Lockshin, L.; d’Hauteville, F. The global wine business as a research field. Int. J. Wine Bus. Res. 2007, 19, 5–13. [Google Scholar] [CrossRef]

- Ansoff, H.I. Corporate Strategy: An. Analytic Approach to Business Policy for Growth and Expansion; McGraw-Hill Companies: New York, NY, USA, 1965. [Google Scholar]

- Fiegenbaum, A.; Thomas, H. Strategic groups and performance: The US insurance industry, 1970–1984. Strat. Manag. J. 1990, 11, 197–215. [Google Scholar] [CrossRef]

- Pertusa-Ortega, E.M.; Molina-Azorín, J.F.; Claver-Cortés, E. Competitive strategy, structure; and firm performance. Manag. Decis. 2010, 48, 1282–1303. [Google Scholar] [CrossRef]

- Porter, M.E. Towards a dynamic theory of strategy. Strat. Manag. J. 1991, 12, 95–117. [Google Scholar] [CrossRef]

- Speed, R.J. Oh Mr Porter! A re-appraisal of competitive strategy. Mark. Intell. Plan. 1989, 7, 8–11. [Google Scholar] [CrossRef]

- Houben, G.; Lenie, K.; Vanhoof, K. A knowledge-based SWOT-analysis system as an instrument for strategic planning in small and medium sized enterprises. Dec. Support Syst. 1999, 26, 125–135. [Google Scholar] [CrossRef]

- Panagiotou, G. Bringing SWOT into focus. Bus. Strat. Rev. 2003, 14, 8–10. [Google Scholar] [CrossRef]

- Grant, R.M. Contemporary Strategy Analysis: Text and Cases Edition; John Wiley & Sons: Hobeken, NJ, USA, 2016. [Google Scholar]

- Yinan, Q.; Xiande, Z.; Chwen, S. The Impact of Competitive Strategy and Supply Chain Strategy on Business Performance: The Role of Environmental Uncertainty. Dec. Sci. 2011, 42, 371–389. [Google Scholar]

- Hunger, J.D.; Wheelen, T.L. Essentials of Strategic Management; Pearson: London, UK, 2014. [Google Scholar]

- Wheelen, T.L.; Hunger, J.D. Concepts in Strategic Management and Business Policy; Pearson: London, UK, 2015. [Google Scholar]

- Gupta, A. Environment & PEST analysis: An approach to external business environment. Int. J. Mod. Soc. Sci. 2013, 2, 34–43. [Google Scholar]

- Menet, G. The importance of strategic management in international business: Expansion of the PESTEL method. Int. Bus. Glob. Econ. 2016, 35, 261–270. [Google Scholar]

- Clark, D.N. Strategic management tool usage: A comparative study. Strat. Chang. 1997, 6, 417–427. [Google Scholar] [CrossRef]

- Tassabehji, R.; Isherwood, A. Management use of strategic tools for innovating during turbulent times. Strat. Chang. 2014, 23, 63–80. [Google Scholar] [CrossRef]

- Gilinsky, A.; Santini, C.; Lazzeretti, L.; Eyler, R. Desperately seeking serendipity. Int. J. Wine Bus. Res. 2008, 20, 302–320. [Google Scholar] [CrossRef]

- Shamsuddoha, A.K.; Ali, M.Y. Mediated effects of export promotion programs on firm export performance. Asia Pac. J. Mark. Logist. 2006, 18, 93–110. [Google Scholar] [CrossRef]

- Storchmann, K. Germany, Austria and Switzerland. In Wine Globalization; Cambridge University Press: Cambridge, UK, 2018; p. 92. [Google Scholar]

- Gilles, K.-J.; König, M. Neuere Forschungen zum römischen Weinbau an Mosel und Rhein; Rheinisches Landesmuseum: Bonn, Germany, 1995. [Google Scholar]

- Standage, T. A History of the World in 6 Glasses; Walker & Co: New York, NY, USA, 2006. [Google Scholar]

- Butzer, P.; Kerner, M.; Oberschelp, W. Charlemagne and his Heritage. 1200 Years of Civilization and Science in Europe; Brepols Publisher: Turnhout, Belgium, 1997. [Google Scholar]

- Braun, K. Der Weinbau im Rheingau; Lüderitzsche Verlagshandlung: Berlin, Germany, 1869. [Google Scholar]

- Phillips, R. Die große Geschichte des Weins; Campus-Verlag: Francfurt, Germany, 2001. [Google Scholar]

- Trick, S. Der Deutsche Wein und die Globalisierung; Europäischer Hochschulverlag: Bremen, Germany, 2009; Volume Band 31. [Google Scholar]

- Frank, B. Die Diffusion von Rebsorten—Eine globale Betrachtung; Markgraf Publishers: Weikersheim, Germany, 2010; Volume 97. [Google Scholar]

- Umweltbundesamt. Struktur der Flächennutzung; Umweltbundesamt: Dessau-Roßlau, Germany, 2018. [Google Scholar]

- Wirtschaftlicher Vereinigung Zucker. Süßes aus der Erde; Wiesbadener Kurier, VRM: Mainz, Germany, 2017. [Google Scholar]

- BMELV. Land-, Forst- und Ernährungswirtschaft mit Fischerei und Wein- und Gartenbau; BMELV: Bonn, Germany, 2017. [Google Scholar]

- DBV. Situationsbericht 2011/12—Trends und Fakten zur Landwirtschaft; DBV: Berlin, Germany, 2012. [Google Scholar]

- DeStatis. Bruttoinlandsprodukt 2016 für Deutschland; DeStatis: Wiesbaden, Germany, 2017. [Google Scholar]

- Hensche, H.; Lorleberg, W. Volkswirtschaftliche Neubewertung des Gesamten Agrarsektors und Seiner Netzwerkstrukturen; Forschungsberichte des Fachbereichs Agrarwirtschaft: Soest, Germany, 2011. [Google Scholar]

- Brunner, K.-M. Essen, Trinken und Reisen im gesellschaftlichen Wandel - Potenziale für Weintourismus aus (wein-)soziologischer Perspektive. In Wein und Tourismus; Dreyer, A., Ed.; Erich Schmidt Verlag: München, Germany, 2011; Volume 11, pp. 37–47. [Google Scholar]

- Bundesbank, D. Deutschlands Reisebilanz. Wiesbadener Kurier, 30 June 2017. [Google Scholar]

- Faugère, C.; Bouzdine-Chameeva, T.; Durrieu, F.; Pesme, J.-O. The impact of tourism strategies and regional factors on wine tourism performance. In Proceedings of the 7th International Conference AWBR, St. Catherines, ON, Canada, 12–15 June 2013. [Google Scholar]

- Koch, J.; Martin, A.; Nash, R. Overview of perceptions of German wine tourism from the winery perspective. Int. J. Wine Bus. Res. 2013, 25, 50–74. [Google Scholar] [CrossRef]

- Orth, U.S.; Stöckl, A. Wein & Tourismus: Determinanten und Konsequenzen emotionaler Bindung zu Regionen und deren Marken. In Wein und Tourismus; Dreyer, A., Ed.; Erich Schmidt Verlag: Munich, Germany, 2011; Volume 11, pp. 49–60. [Google Scholar]

- Dreyer, A. Wein und Tourismus—Erfolg durch Synergien und Kooperationen; Erich Schmidt Verlag: Munich, Germany, 2011; Volume 11. [Google Scholar]

- Chang, S. Experience economy in hospitality and tourism: Gain and loss values for service and experience. Tour. Manag. 2018, 64, 55–63. [Google Scholar] [CrossRef]

- Bundesamt, S. Erste offizielle Ernteschätzung. In Weinwirtschaft; Meininger Verlag: Neustadt, Germany, 2018. [Google Scholar]

- DWI. Deutscher Wein Statistik 2017/2018; DWI: Mainz, Germany, 2018; pp. 1–40. [Google Scholar]

- Statista. Produktionsmenge von Wein. 2017. Available online: Statista.com/statistik/daten/studie (accessed on 20 November 2018).

- Loose, S.; Pabst, E. Current State of the German and International Wine Markets. Oceania 2018, 634, 1–9. [Google Scholar]

- Bogonos, M.; Engler, B.; Oberhofer, J.; Dressler, M.; Dabbert, S. Planting Rights Liberalization in the European Union: An Analysis of the Possible Effects on the Wine Sector in Rheinland-Pfalz, Germany. Ger. J. Agric. Econ. 2016, 65, 30–40. [Google Scholar]

- Deconinck, K.; Swinnen, J. The Economics of Planting Rights. LICOS Centre for Institutions and Economic Performance Discussion. 2013. Available online: https://ideas.repec.org/s/lic/licosd.html (accessed on 20 November 2018).

- Dpa. Mehr Weinanbau in Deutschland Möglich: Bundestag für mehr Fläche; Rhein Zeitung: Koblenz, Germany, 2015. [Google Scholar]

- Deutscher Bundestag. Drucksache 18/4656. V. 20.4.2015, Köln, Bundesanzeiger: 2015. Available online: http://dip21.bundestag.de/dip21/btd/18/046/1804656.pdf (accessed on 20 November 2018).

- Bindi, M.; Howden, M. Challenges and Opportunities for Cropping Systems in a Changing Climate. In Proceedings of the 4th International Crop Science Congress, Brisbane, Australia, 26 September–1 October 2004. [Google Scholar]

- DeGaetano, A.T.; Belcher, B.N. Spatial interpolation of daily maximum and minimum air temperature based on meteorological model analyses and independent observations. J. Appl. Meteorol. Climatol. 2007, 46, 1981–1992. [Google Scholar] [CrossRef]

- Hera, U.; Rötzer, T.; Zimmermann, L.; Schulz, C.; Maier, H.; Weber, H.; Kölling, C. Klima en détail. LWF aktuell 2012, 86, 34–37. [Google Scholar]

- Huglin, P. Nouveau mode d’évaluation des possibilités héliothermiques d’un milieu viticole. Comptes rendus des séances 1978. Available online: http://agris.fao.org/agris-search/search.do?recordID=US201301392531 (accessed on 20 November 2018).

- Johnson, G.L.; Daly, C.; Taylor, G.H.; Hanson, C.L. Spatial variability and interpolation of stochastic weather simulation model parameters. J. Appl. Meteorol. 2000, 39, 778–796. [Google Scholar] [CrossRef]

- Kovács, L.G.; Byers, P.L.; Kaps, M.L.; Saenz, J. Dormancy, cold hardiness, and spring frost hazard in Vitis amurensis hybrids under continental climatic conditions. Am. J. Enol. Viticul. 2003, 54, 8–14. [Google Scholar]

- Molitor, D.; Caffarra, A.; Sinigoj, P.; Pertot, I.; Hoffmann, L.; Junk, J. Late frost damage risk for viticulture under future climate conditions: A case study for the Luxembourgish winegrowing region. Aust. J. Grape Wine Res. 2014, 20, 160–168. [Google Scholar] [CrossRef]

- Statistisches Bundesamt. Bestockte Rebfläche 2005–2017; DWV: Bonn, Germany, 2018. [Google Scholar]

- Eurostat. 2017. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Vineyards_in_the_EU_-_statistics (accessed on 20 November 2018).

- Rückrich, K. Stand der Rebsortenzulassung. Der Deutsche Weinbau 2018, 16/17, 1. [Google Scholar]

- GfK. Weinmarkt Deutschland—Verbraucher-Analysen Jahr 2016; GfK: Nuremberg, Germany, 2017; not published. [Google Scholar]

- DWI. Öko-Weinbau in Deutschland Immer Beliebter; DWI: Mainz, Germany, 2018. [Google Scholar]

- Umweltbundesamt. Umwelt und Landwirtschaft 2018; Umweltbundesamt: Dessau, Germany, 2018. [Google Scholar]

- Cohen, E.; Goodman, S.; Remaud, H.; Lockshin, L. Building brand salience for commodity-based wine regions. Int. J. Wine Bus. Res. 2009, 21, 79–92. [Google Scholar]

- Thomas, L.C.; Painbéni, S.; Barton, H. Entrepreneurial marketing within the French wine industry. Int. J. Entrep. Behav. Res. 2013, 19, 238–260. [Google Scholar] [CrossRef]

- Van Leeuwen, C.; Seguin, G. The concept of terroir in viticulture. J. Wine Res. 2006, 17, 1–10. [Google Scholar] [CrossRef]

- RLP. Weinbau-bestockte Rebfläche; Statistisches Landesamt Rheinland-Pfalz: Mainz, Germany, 2010. [Google Scholar]

- BMELV. Ertragslage Obst-und Weinbau 2016; Abt, R., Ed.; BMELV: Bonn, Germany, 2016; pp. 92–131. [Google Scholar]

- Sellers-Rubio, R. Evaluating the economic performance of Spanish wineries. Int. J. Wine Bus. Res. 2010, 22, 73–84. [Google Scholar] [CrossRef]

- Mend, M. Wie steht´s mit dem Erfolg? Das Deutsche Weinmagazin 2009, 12/13, 26–28. [Google Scholar]

- Oberhofer, J. Agrarbericht 2012: Erfreuliche Entwicklung an der Mosel. Der Deutsche Weinbau 2013, 16, 14–19. [Google Scholar]

- Oberhofer, J. Agrarbericht—Erfreuliche Entwicklung. Der Deutsche Weinbau 2018, 16, 16–22. [Google Scholar]

- BMELV. Ertragslage Obst-und Weinbau 2012; BMELV: Bonn, Germany, 2012; pp. 90–123. [Google Scholar]

- SBA. Agrarstrukturerhebung 2010; Statistisches Bundesamt: Wiesbaden, Germany, 2011. [Google Scholar]

- BMELV. Ertragslage Obst-und Weinbau 2011; Abt, R., Ed.; BMELV: Bonn, Germany, 2011; pp. 86–119. [Google Scholar]

- DWI. Deutscher Wein Statistik 2016/2017; DWI: Mainz, Germany, 2017; pp. 1–40. [Google Scholar]

- Scheuermann, M. Die 50 größten Weingüter. In Drunkenmonday; 2012; Volume 2018, Available online: https://drunkenmonday.wordpress.com/2010/11/17/die-50-grosten-weinguter (accessed on 20 November 2018).

- Lambeck, M. Deutschlands größtes Weingut. Bild-Zeitung. Available online: www.bild.de/lifestyle/essen-trinken/edle-alkohole-weine/weinkolumne-kloster-eberbach-33914410 (accessed on 20 November 2018).

- Mieding, N. Der Dino unter den Winzern. Rheinzeitung, 12 March 2016. [Google Scholar]

- Atkin, T.; Gilinsky, A.; Newton, S.K. Sustainability in the Wine Industry: Altering the Competitive Landscape? In Proceedings of the 6th AWBR International Conference, Bordeaux, France, 9–10 June 2011. [Google Scholar]

- Algner, M.; Fritsch, A.; Reichel, R. Winzergenossenschaften im Wettbewerb. ZfgG 2007, 57, 167–177. [Google Scholar] [CrossRef]

- DRV. Deutsche Winzergenossenschaften. Available online: https://www.raiffeisen.de/wein (accessed on 20 November 2018).

- Grosskopf, W.M.; Hans, H.; Ringle, G. Unsere Genossenschaften-Idee, Auftrag, Leistungen; Deutscher Genossenschaftsverlag: Wiesbaden, Germany, 2009. [Google Scholar]

- DRV. Weinwirtschaftsjahr-Auszüge; Deutscher Raiffeisenverband: Berlin, Germany, 2012. [Google Scholar]

- Dpa. “Jeder macht, was er kann”—Wenn Winzer sich zusammenschließen. Merkur.de. Available online: www.merkur.de/wirtschaft/wenn-winzer-sich-zusammenschliessen-zr-10219953 (accessed on 20 November 2018).

- Anonymous. Moselland eG feiert “50 Jahre eine starke Gemeinschaft” Eifel Zeitung. Available online: www.eifelzeitung.de/region/bernkastel-wittlich/moselland-eg-feiert-50-jahre-eine-starke-gemeinschaft-177438 (accessed on 20 November 2018).

- Gerke, C. Rückkehr an die Spitze. Weinwirtschaft 2018, 4, 146–152. [Google Scholar]

- Kolb, S. Winzergenossenschaften auf dem Weg in die Zukunft; Deutscher Raiffeisenverband: FES, Kirrweiler, 2012. [Google Scholar]

- Gerke, C. Größe gesucht. Weinwirtschaft 2012, 4, 122–125. [Google Scholar]

- BVW. Wer Sind Wir und Was Tun Wir? Available online: www.ihk-trier.de (accessed on 20 November 2018).

- Pilz, H. Es rauscht im Karton. Weinwirtschaft 2018, 4, 142–146. [Google Scholar]

- Schallenberger, F. Weinbau. Made in Germany. Der deutsche Weinmarkt im Blickfeld; LBBW: Mainz, Germany, 2009; pp. 1–36. [Google Scholar]

- Fiegenbaum, A.; Thomas, H. Strategic groups as reference groups: Theory, modeling and empirical examination of industry and competitive strategy. Strat. Manag. J. 1995, 16, 461–476. [Google Scholar] [CrossRef]

- Fiegenbaum, A. Strategic Groups and Performance: The US Insurance Industry; University of Michigan, School of Business Administration: Ann Arbor, MI, USA, 1987. [Google Scholar]

- Ward, P.T.B.; Deborah, J.; Leong, G.K. Configurations of manufacturing strategy, business strategy, environment and structure. J. Manag. 1996, 22, 597–626. [Google Scholar] [CrossRef]

- Ward, P.T.D. Rebecca, Manufacturing strategy in context: Environment, competitive strategy and manufacturing strategy. J. Oper. Manag. 2000, 18, 123–138. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Porter, M.E. From competitive advantage to corporate strategy. McKinsey Q. 1988, 2, 35–66. [Google Scholar]

- Porter, M.E. What is strategy? In Strategy for business: A Reader; Mazzucato, M., Ed.; Sage: New York, NY, USA, 2002. [Google Scholar]

- Campbell-Hunt, C. What have we learned about generic competitive strategy? A meta-analysis. Strat. Manag. J. 2000, 21, 127–154. [Google Scholar] [CrossRef]

- Porter, M.E. Location, Competition, and Economic Development: Local Clusters in a Global Economy. Econ. Dev. Q. 2000, 14, 15–34. [Google Scholar] [CrossRef]

- Dressler, M. Strategic grouping in a fragmented market: SMEs’ strive for legitimacy. Int. J. Entrep. Small Bus. 2017, 32, 229–253. [Google Scholar] [CrossRef]

- Santini, C.; Cavicchi, A.; Gilinsky, A.; Newton, S.; Rabino, S. Niche Strategy and Resources: Dilemmas and open questions, an exploratory study. In Proceedings of the 8th International Conference, Academy of Wine Business Research, Geisenheim, Germany, 28–30 June 2014. [Google Scholar]

- Freter, H. Markt-und Kundensegmentierung, 2nd ed.; Kohlhammer: Stuttgart, Germany, 2008. [Google Scholar]

- Touzard, J.-M. Innovation Systems and Regional Vineyards. ISDA: Montpellier, France, 2010; pp. 1–13. [Google Scholar]

- Gray, A.; Boehlje, M.; Amanor-Boadu, V.; Fulton, J. Agricultural innovation and new ventures: Assessing the commercial potential. Am. J. Agric. Econ. 2004, 86, 1322–1329. [Google Scholar] [CrossRef]

- Kumar, N. Marketing as Strategy; HBS Press: Boston, MA, USA, 2004. [Google Scholar]

- Kotler, P. The Prosumer Movement: A new challenge for marketers. Adv. Consum. Res. 1986, 13, 510–513. [Google Scholar]

- Bloemer, J.; Ruyter, K.D. Customer Loyalty in High and Low Involvement Service Settings: The Moderating Impact of Positive Emotions. J. Mark. Manag. 1999, 15, 315–330. [Google Scholar] [CrossRef]

- Carù, A.; Cova, B. Revisiting Consumption Experience a More Humble but Complete View of the Concept. Mark. Theory 2003, 3, 267–286. [Google Scholar] [CrossRef]

- Ravald, A.G.; Grönroos, C. The value concept and relationship marketing. Eur. J. Mark. 1996, 30, 19–30. [Google Scholar] [CrossRef]

- Dess, G.G.; Davis, P.S. Porter’s (1980) Generic Strategies as Determinants of Strategic Group Membership and Organizational Performance. Acad. Manag. J. 1984, 27, 467–488. [Google Scholar]

- Göbel, R. Marketingstrategische Ausrichtung und Veränderungsfähigkeit als Ursache des wirtschaftlichen Erfolges analysiert am Beispiel direktvermarktender Weingüter. Geisenheimer Berichte 2003, 49, 1–163. [Google Scholar]

- BÖLN. Höhere Preise fördern die Nachfrage. Das Deutsche Weinmagazin, 2 July 2018. [Google Scholar]

- Dressler, M. Ökologischer Weinbau: Positionierungsanalysen. Der Deutsche Weinbau 2013, 5, 16–18. [Google Scholar]

- Siebold, H. Ökoweingut Findet Einen Potenten Retter. Available online: www.stuttgarter-zeitung.de/inhalt.kaiserstuhl-oekoweingut-findet-einen-potenten-retter.489584de-5f25-4a1f-8c88-b5600556fff7.html (accessed on 20 Novermber 2018).

- Dressler, M. Umweltadaption durch Innovation—Strategische Maßnahmen bei Umweltveränderungen am Beispiel Weinbau. zfO 2018, 87, 24–32. [Google Scholar]

- Zahra, S.A.; George, G. Absorptive capacity: A review, reconceptualization, and extension. Acad. Manag. Rev. 2002, 27, 185–203. [Google Scholar] [CrossRef]

- Hamilton, B.H.; Nickerson, J.A. Correcting for endogeneity in strategic management research. Strat. Organ. 2003, 1, 51–78. [Google Scholar] [CrossRef]

- BCG. Organisation 2015—Designed to Win; The Boston Consulting Group: Boston, MA, USA, 2009. [Google Scholar]

- Schwiddessen, J. Da muss man schon was tun. Wiesbadener Kurier, 13 October 2018. [Google Scholar]

- Dressler, M. Vertriebsmanagement—Multikanaler und moderner Vertrieb. In Deutsches Weinbaujahrbuch 2016; Schultz, H.-R., Stoll, M., Eds.; Ulmer: Stuttgart, Germany, 2016; Volume 67, pp. 69–77. [Google Scholar]

- Malheiro, A.C.; Santos, J.A.; Pinto, J.G.; Jones, G.V. European Viticulture Geography in a changing climate. OIV Bull. 2012, 85, 15–22. [Google Scholar]

- Nielsen. Handel, Verbraucher, Werbung—Deutschland 2011; The Nielsen Company: New York, NY, USA, 2012. [Google Scholar]

- DWI. Deutscher Wein Statistik 2012/2013; DWI: Mainz, Germany, 2012; pp. 1–36. [Google Scholar]

- Ipsos. Europäer und Biowein. Available online: http://www.marktmeinungmensch.de/studien/ipsos-studie-weinkonsum-und-bio-wein-in-deutschland (accessed on 20 November 2018).

- Pabst, A.; Kraus, L.; Matos, E.G.D.; Piontek, D. Substanzkonsum und substanzbezogene Störungen in Deutschland im Jahr 2012. Sucht 2013, 59, 321–331. [Google Scholar] [CrossRef]

- Aizenman, J.; Brooks, E. Globalization and Taste Convergence: The Cases of Wine and Beer. Rev. Int. Econ. 2008, 16, 217–233. [Google Scholar] [CrossRef]

- MDS. VerbraucherAnalyse. Available online: www.verbraucheranalyse.de/fakten/studie (accessed on 20 November 2018).

- OIV. World Vitiviniculture Situation 2012; OIV: Paris, France, 2012. [Google Scholar]

- Markgraf, H. Die Deutschen lieben Sekt. 2012. AHGZ. Available online: https://www.ahgz.de/zulieferer/die-deutschen-lieben-sekt (accessed on 20 November 2018).

- Anderson, K.; Nelgen, S. Global Wine Markets 1961–2009: A Statistical Compendium; University of Adelaide Press: Adelaide, Australia, 2011. [Google Scholar]

- OIV. World Vitiviniculture Situation 2013; OIV: Paris, France, 2013. [Google Scholar]

- Wiesgen-Pick, A. Daten aus der Alkoholwirtschaft 2016; Bundesverband der Deutschen Spirituosen-Industrie und -Importeure e. V. (BSI): Bonn, Germany, 2016. [Google Scholar]

- WHO. Alkoholkonsum in Europa; Dpa, Ed.; Verlagsgruppe Rhein-Main: Wiesbadener Kurier, Germany, 2018; p. 8. [Google Scholar]

- Statista. Pro-Kopf-Verbrauch von Bier, Wein, Schaumwein und Spirituosen in Deutschland. Available online: Statista.com/statistik/daten/studie (accessed on 20 November 2018).

- Handelsblatt, Markt für Spirituosen—Werbeausgaben der Branche. Grafik, H., Ed. HB. Available online: https://www.handelsblatt.com/infografiken/grafik/ (accessed on 20 September 2018).

- Nielsen. Entwicklung der Werbeausgaben für Wein 2000–2017; Statista: Hamburg, Germany, 2018. [Google Scholar]

- Nielsen. Consumers Deutschland; Nielsen: Hamburg, Germany, 2017. [Google Scholar]

- Haupt, D. Weinwirtschaftsbericht; MWVLW Rheinland Pfalz: Mainz, Germany, 2010. [Google Scholar]

- DWI. Deutscher Wein Statistik 2010/2011; DWI: Mainz, Germany, 2011; pp. 1–36. [Google Scholar]

- Szolnoki, G.; Hoffmann, D. Neue Weinkunden-Segmentierung in Deutschland. In Proceedings of the 37th World Congress of Vine and Wine and 12th General Assembly of the OIV, EDP Sciences, Mendoze, Argentina, 9–14 November 2014; p. 07002. [Google Scholar]

- Szolnoki, G.; Hoffman, D. Neue Weinkundensegmentierung in Deutschland; Hochschule Geisenheim: Geisenheim, Germany, 2014; Volume 73. [Google Scholar]

- Mannheim, U.O. Studie zum Konsum von Wein. Available online: www.natuerlichkork.de (accessed on 20 November 2018).

- Nielsen. Deutsche geben Milliarden für alkoholische Getränke aus. Available online: https://www.proplanta.de/Agrar-Nachrichten/Verbraucher: Düsseldorf (accessed on 20 November 2018).

- Research, S. Weinatlas Deutschland; Splendid Research: Hamburg, Germany, 2018. [Google Scholar]

- Hoffmann, D.; Szolnoki, G. Der Premiummarkt für Weine in Deutschland; MULEWF Rheinland Pfalz: Mainz, Germany, 2011; pp. 1–83. [Google Scholar]

- Haupt, D. Weissweinstudie—Repräsentative Verbraucheruntersuchung; MWVLW Rheinland Pfalz: Mainz, Germany, 2006; pp. 1–120. [Google Scholar]

- GfK. Verbraucher-Analysen Wein 2017; Gesellschaft für Konsumforschung: Nuremberg, Germany, 2018. [Google Scholar]

- Hoffmann, D. Stabiler Markt. Weinwirtschaft 2010, 5, 167–168. [Google Scholar]

- Dressler, M. Reputationsmanagement und Einfluss auf die Preisdurchsetzung—Empirische Einsichten. In Deutsches Weinbaujahrbuch 2017; Schultz, H.-R., Stoll, M., Eds.; Ulmer: Stuttgart, Germany, 2017; Volume 68, pp. 118–124. [Google Scholar]

- Fleuchaus, R.; Arnold, R.C. Weinmarketing: Kundenwünsche Erforschen, Zielgruppen Identifizieren, Innovative Produkte Entwickeln; Gabler Verlag: Wiesbaden, Germany, 2010. [Google Scholar]

- Dressler, M. Strategic winery reputation management—Exploring German wine guides. Int. J. Wine Bus. Res. 2016, 28, 4–21. [Google Scholar] [CrossRef]

- DWI. Deutsche Weine aus Sicht der Konsumenten; DWI: Mainz, Germany, 2013. [Google Scholar]

- Riviezzo, A.; De Nisco, A.; Garofano, A. Understanding wine purchase and consumption behaviour: A market segmentation approach. In Proceedings of the 6th AWBR International Conference, Bordeaux, Germany, 9–10 June 2011. [Google Scholar]

- Arnold, R.; Fleuchaus, R. Ein Überblick zu Segmentierungsansätzen im Weinmarketing. In Weinmarketing: Kundenwünsche Erforschen, Zielgruppen Identifizieren, Innovative Produkte Entwickeln; Fleuchaus, R.A., Ed.; Gabler Verlag: Wiesbaden, Germany, 2010; pp. 119–144. [Google Scholar]

- Olsen, J.; Newton, S.K. Millenial Wine Consumer Dining Preferences Segmented by Restaurant Type—An Exloratory Study. In Proceedings of the 6th AWBR International Conference, Bordeaux, Germany, 9–10 June 2011; pp. 1–12. [Google Scholar]

- Corsi, A.M.; Lockshin, L.; Mueller, S. Competition between and competition within: The strategic positioning of competing countries in key export markets. In Proceedings of the 6th International Conference, AWBR, Bordeaux, France, 9–10 June 2011. [Google Scholar]

- Reule, M. Zielgruppen für deutsche Weine 2013; Weinmarkt, A.T.I.D., Ed.; DWI: Dresden, Germany, 2014. [Google Scholar]

- Sociodimensions. Deutsche Weine aus Sicht der Konsumenten; DWI: Mainz, Germany, 2013. [Google Scholar]

- Schipperges, M. Verbraucher offen für neue Entdeckungen. Das deutsche Weinmagazin 2013, 17/18, 58–63. [Google Scholar]

- DWI. Die Wahrnehmung deutscher Weine aus Sicht der Konsumenten. Available online: https://www.lwg.bayern.de/mam/cms06/weinbau/dateien/14_wbt_20140220-fränkische-weinwirtschaftstage-image-zielgruppen.pdf (accessed on 20 November 2018).

- Wiesgen-Pick, A. Pro-Kopf-Verbrauch der verschiedenen alkoholhaltigen Getränke nach Bundesländern 2015; Bundesverband der Deutschen Spirituosen-Industrie und -Importeure e. V. (BSI): Bonn, Germany, 2016. [Google Scholar]

- Dünnebacke, T. Steigende Lust auf deutsche Weine. Lebensmittelpraxis. Available online: https://lebensmittelpraxis.de /sortiment/11401-wein-und-sekt-steigende-lust-auf-deutsche-weine (accessed on 20 November 2018).

- Nestlé. So is(s)t Deutschland—Ein Spiegel der Gesellschaft; Nestlé Deutschland AG: Frankfurt Main, Germany, 2011. [Google Scholar]

- Nielsen. Deutsche gehen seltener einkaufen dpa, Ed. Available online: stuttgarter-nachrichten.de (accessed on 20 November 2018).

- Haucap, J.; Heimeshoff, U.; Klein, G.J.; Rickert, D.; Wey, C. Wettbewerbsprobleme im Lebensmitteleinzelhandel; Düsseldorfer Institut für Wettbewerbsökonomie: Düsseldorf, Germany, 2013. [Google Scholar]

- Cohen, E.; D’Hauteville, F.; Goodwill, S.; Lockshin, L.; Sirieix, L. A cross-cultural comparison of choice criteria for wine in restaurants. In Proceedings of the 4th International Conference of AWBR, Siena, Italy, 17–19 July 2008; pp. 1–18. [Google Scholar]

- Statista. Umsatz mit Wein in Deutschland nach Vertriebsformen in den Jahren 2008 bis 2014 (in Mrd. Euro). 2015. Available online: Statista.com/statistik/daten/studie (accessed on 20 November 2018).

- Engelhard, W. Konsumhype geht an Wein vorbei. Markt+Wein 2017, 3, 78–82. [Google Scholar]

- Rabobank. The Incredible Bulk; Rabobank: Utrecht, The Netherlands, 2012. [Google Scholar]

- Engelhard, W. Harddiscounter: Verloren Und Trotzdem Gewonnen. Wein+Markt 2011, 16–17. [Google Scholar]

- Engelhard, W. Wieder weniger Weinkunden. Wein+Markt 2011, 14–15. [Google Scholar]

- Engelhard, W. Erneuter Absatzknick. Wein+Markt 2011, 18–19. [Google Scholar]

- Engelhard, W. Rückschlag. Markt+Wein 2017, 3, 72–75. [Google Scholar]

- Engelhard, W. Ernüchterung. Markt+Wein 2017, 3, 76–77. [Google Scholar]

- DWI. Trend zum Weinkauf in Supermärkten hält an. Available online: https://www.deutscheweine.de/presse/pressemeldungen/details/news/detail/News/trend-zum-weinkauf-in-supermaerkten-haelt-an/ (accessed on 20 November 2018).

- OC&C. Erwartete Konsumentenreaktion auf Preiserhöhung je Land. 2011/2012; OC&C Strategy Consultants: Hamburg, Germany, 2012. [Google Scholar]

- OC&C. Messers Schneide—Die Preisstrategie als wesentlicher Erfolg des Geschäftsmodells; OC&C Strategy Consultants: Hamburg, Germany, 2013. [Google Scholar]

- COGEA. Study on the Competitiveness of European Wines; European Commission: Luxembourg, 2014; pp. 1–146. [Google Scholar]

- Hoffmann, D.; Szolnoki, G. Consumer segmentation based on usage of sales channels in the German wine market. Int. J. Wine Bus. Res. 2014, 26, 27–44. [Google Scholar]

- Ghvanidze, S.T.L.; Fleuchaus, R. Die Bedeutung des Wein Herkunftslandes für die Wahrnehmung der Konsumenten—Eine Kausalanalyse. IL Jahrestagung: Oppenheim, Germany, 2011; pp. 73–76. [Google Scholar]

- Szolnoki, G.; Heußler, N.; Bleich, S. Analysis of prices and geografical origins as quality indicators. Le Bulletin de l´OIV 2009, 82, 411–420. [Google Scholar]

- Hall, C.M.M.R. Wine Marketing; Butterworth-Heinemann: Oxford, UK, 2010. [Google Scholar]

- Kern, M.; Müller, S. Sensorische Konsumentenforschung für modernes Weinmarketing. Weinmarketing: Kundenwünsche erforschen, Zielgruppen identifizieren, innovative Produkte entwickeln; Fleuchaus, R., Arnold, R., Eds.; Gabler Verlag: Wiesbaden, Germany, 2010; pp. 75–118. [Google Scholar]

- Orth, U. Weinkonsumentenverhalten—Der aktuelle Stand der Forschung und Ausblick. In Weinmarketing; Fleuchaus, R., Arnold, R., Eds.; Gabler Verlag: Wiesbaden, Germany, 2010; pp. 5–33. [Google Scholar]

- Castriota, S.; Curzi, D.; Delmastro, M. Tasters’ Bias in Wine Guides’ Quality Evaluations. Appl. Econ. Lett. 2013, 20, 1174–1177. [Google Scholar] [CrossRef]

- Gokcekus, O.; Nottebaum, D. The Buyer’s Dilemma—Whose Rating Should a Wine Drinker Pay Attention to? Am. Assoc. Wine Econ. Work. Pap. 2011, 91, 1–12. [Google Scholar]

- Karpik, L. Valuing the Unique: The Economics of Singularities; Princeton University Press: Princeton, NJ, USA, 2010. [Google Scholar]

- Akerlof, G.A. The Market for “Lemons”: Quality Uncertainty and the Market Mechanisms. Q. J. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Bagwell, K.; Riordan, M.H. High and Declining Prices Signal Product Quality. Am. Econ. Rev. 1991, 81, 224–239. [Google Scholar]

- Castriota, S.; Delmastro, M. The economics of collective reputation: Minimum quality standards, vertical differentiation and optimal group size. AAWE 2009. working paper 50. [Google Scholar]

- Andersson, F. Pooling Reputation. Int. J. Ind. Organ. 2002, 20, 715–730. [Google Scholar] [CrossRef]

- Ling, B.-H.; Lockshin, L. Components of wine prices for Australian wine: How winery reputation, wine quality, region, vintage, and winery size contribute to the price of varietal wines. Australas. Mark. J. (AMJ) 2003, 11, 19–32. [Google Scholar] [CrossRef]

- Lachmann, U.; Arnold, R. Wie funktioniert Weinkommunikation? ... Und wie nicht? Weinmarketing: Kundenwünsche Erforschen, Zielgruppen Identifizieren, Innovative Produkte Entwickeln; Fleuchaus, R., Arnold, R., Eds.; Gabler Verlag: München, Germany, 2011. [Google Scholar]

- Schneider, C. Präferenzbildung bei Qualitätsunsicherheit: Das Beispiel Wein; Duncker&Humblodt: Schriften zum Marketing, Berlin, Germany, 1997. [Google Scholar]

- Häusel, H.G. Brain View: Warum Kunden Kaufen; Rudolf Haufe Verlag: München, Germany, 2008. [Google Scholar]

- Ashenfelter, O. Predicting the Quality and Prices of Bordeaux Wine. Econ. J. 2008, 118, 174–184. [Google Scholar] [CrossRef]

- Gergaud, O.; Livat, F. How Do Customers Use Signals to Assess Quality? Am. Assoc. Wine Econ. Work. Pap. 2007, 3, 1–22. [Google Scholar]

- Schiefer, J.; Fischer, C. The Gap between Wine Experts Ratings and Consumer Preferences: Measures, Determinants and Marketing Implictaions. Int. J. Wine Bus. Res. 2008, 20, 335–351. [Google Scholar] [CrossRef]

- Charters, S.; Pettigrew, S. Is Wine Consumption an Aesthetic Experience? J. Wine Res. 2005, 16, 121–136. [Google Scholar] [CrossRef]

- Olsen, J.; Newton, S.K. Millenial Wine Consumer Dining Preferences Segmented by Restaurant Type. In Proceedings of the 6th International Conference, AWBR, Bordeaux, France, 9–10 June 2011. [Google Scholar]

- Winfree, J.A.; McCluskey, J.J. Collective Reputation and Quality. Am. J. Agric. Econ. 2005, 87, 206–213. [Google Scholar] [CrossRef]

- Kirmani, A.; Rao, A.R. No pain, no gain: A critical review of the literature on signaling unobservable product quality. J. Mark. 2000, 64, 66–79. [Google Scholar] [CrossRef]

- Landon, S.; Smith, C.E. Quality expectations, reputation, and price. South. Econ. J. 1998, 64, 628–647. [Google Scholar] [CrossRef]

- Shapiro, C. Premiums for high quality products as returns to reputations. Q. J. Econ. 1983, 659–679. [Google Scholar] [CrossRef]

- Cavusgil, S.T.; Hult, G.T.M.; Kiyak, T.; Deligonul, S.; Lagerström, K. What Drives Performance in Globally Focused Marketing Organizations? A Three-Country Study. J. Int. Mark. 2007, 15, 58–85. [Google Scholar]

- Castriota, S.; Delmastro, M. Individual and Collective Reputation: Lessons from the Wine Market. L’industria 2010, 31, 149–172. [Google Scholar] [CrossRef][Green Version]

- Schrader, C. Reputation und Kaufverhalten: Eine empirische Analyse am Beispiel der Vermarktung deutscher Weine in Großbritannien; Universität Hamburg: Hamburg, Germany, 2008. [Google Scholar]

- Benfratello, L.; Piacenza, M.; Sacchetto, S. Taste or reputation: What drives market prices in the wine industry? Appl. Econ. 2009, 41, 2197–2209. [Google Scholar] [CrossRef]

- Jung, C.H.D. Strategic groups in Spezialized Wine Retail in Germany. In Proceedings of the 6th International Conference of the Association of Wine Business Research, Bordeaux, France, 9–10 June 2011. [Google Scholar]

- DWI. Weineinkauf privater Haushalte in Deutschland im Handel—4. Quartal 2013; DWI: Mainz, Germany, 2014; pp. 1–36. [Google Scholar]

- DWI. Deutscher Wein Statistik 2015/2016; DWI: Mainz, Germany, 2015; pp. 1–39. [Google Scholar]

- Pekel. Tourismus: Gäste und Übernachtungen im Reiseverkehrm, Beherbergungskapazität—Vorläufige Ergebnisse; Statistisches Landesamt Sachsen-Anhalt: Halle, Germany, 2013. [Google Scholar]

- Dressler, M. Innovative Weinwelt: Der “aktive Kunde”. Der Deutsche Weinbau 2012, 6, 16–18. [Google Scholar]

- DWI. Weinmarkt 2010; DWI: Mainz, Germany, 2011. [Google Scholar]

- MarketLine. Wine Industry Profile: Germany; MarketLine: London, UK, 2012; pp. 1–32. [Google Scholar]

- Dressler, M. Innovation focus and capacity challenge of small entrepreneurs—Looking at German wineries. In Proceedings of the International Conference on Innovation & Trend in Wine Management, Dijon, France, 22 June 2012. [Google Scholar]

- Ernest-Hahn, S. Wein in der Gastronomie; Matthaes: Stuttgart, Germany, 2005. [Google Scholar]

- Dressler, M. Perfekter Absatz—Kunden und struktureller Wandel fordern professionellen Vertrieb. Das Deutsche Weinmagazin 2015, 20, 17–19. [Google Scholar]

- Hoffmann, D. Der deutsche Weinmarkt 2009. Das Deutsche Weinmagazin 2010, 5/6, 56–58. [Google Scholar]

- Heilig, A.T.B.; Tschernavskij, A. Studie zeigt großes Potential im Online-Handel! Das deutsche Weinmagazin 2012, 15, 24–27. [Google Scholar]

- Nitt-Drießelmann, D. Einzelhandel im Wandel; Hamburgisches Weltwirtschafts Institut: Hamburg, Germany, 2013. [Google Scholar]

- GfK. Weinmarkt Deutschland—Verbraucher-Analysen Jahr 2015; Gesellschaft für Konsumforschung: Nuremberg, Germany, 2016; in press. [Google Scholar]

- GfK. Online-Weinkäufer legen Wert auf Qualität; Gesellschaft für Konsumforschung: Nuremberg, Germany, 2015; in press. [Google Scholar]

- Pilz, H. Ungewisse Zukunft. Weinwirtschaft 2018, 21, 26–29. [Google Scholar]

- Mangelsdorf, F. Rotkäppchen-Mumm legt weiter zu und investiert. Märkische Oberzeitung, 28 October 2012. [Google Scholar]

- GfK. Weinmarkt Deutschland—Verbraucher-Analysen Jahr 2014, Konsumforschung, G.F., Ed.; 2015; unpublished.

- Statistisches Bundesamt. Vorausberechneter Bevolkerungsstand; Statistisches Bundesamt: Wiesbaden, Germany, 2017. [Google Scholar]

- Nestlé Deutschland AG. Nestlé Studie 2009: Ernährung in Deutschland 2008—Kurzfassung; Nestlé Deutschland AG: Frankfurt, Germany, 2009. [Google Scholar]

- Göbel, R. Praktische Unternehmensführung—Planung, Controlling und Organisatin in Unternehmen der Weinbranche; DLG Verlag: Frankfurt, Germany, 2005. [Google Scholar]

- DWI. Neues Marketing für neue Konsumenten; DWI: Mainz, Germany, 2003. [Google Scholar]

- Römmelt, W. Schwierige Imagebildung trotz Wachstum. Weinwirtschaft 2012, 20, 31–35. [Google Scholar]

- Schön, W. Regionalität ist unsere Stärke. Weinwirtschaft 2018, 9, 26–27. [Google Scholar]

- Cusson, A. Trends und Perspektiven des weltweiten Wein-und Spirituosenmarktes bis 2014; Vinexpo-Sopexa: Bordeaux, France, 2011. [Google Scholar]

- WeinWir, H.I. Weinimport auf Rekordniveau. Weinwirtschaft 2012, 20, 9. [Google Scholar]

- Rückrich, K. Entwicklung der Stillweinimporte. Der Deutsche Weinbau 2012, 22, 9. [Google Scholar]

- Pilz, H. Weinimport auf Rekordniveau. Weinwirtschaft 2012, 20, 9. [Google Scholar]

- Mathäß, J. Globalisierung im Glas. Rheinpfalz am Sonntag, 30 September 2018; 6. [Google Scholar]

- Unione Italiana Vini. Import. Wine by numbers, 5. 2017. Available online: http://www.uiv.it/corriere/english-version/ (accessed on 20 November 2018).

- Rückrich, K. Weinaußenhandel in der Europäischen Union—Weinimporte im Fokus. Der Deutsche Weinbau 2018, 12, 12. [Google Scholar]

- Pilz, H. Von Einäugigen und Blinden. Weinwirtschaft 2012, 20, 46–51. [Google Scholar]

- Scheuermann, M. Deutschland als Weindrehscheibe Europas. The Drink Tank 2012, 4, 1–3. [Google Scholar]

- Dressler, M. Wein: Globale Chancen für deutsche Anbieter. Der Deutsche Weinbau 2014, 10, 18. [Google Scholar]

- Rheinschmidt, K. Abwärtstrend scheint gestoppt. Das Deutsche Weinmagazin 2018, 20, 32–34. [Google Scholar]

- Dressler, M. Vertriebsstrategien angepasst an sich änderndes Verbraucherverhalten und schwankende Erntemengen. In Pfälzer Weinbautage 2015; DLR Rheinpfalz: Neustadt, Germany, 2015. [Google Scholar]

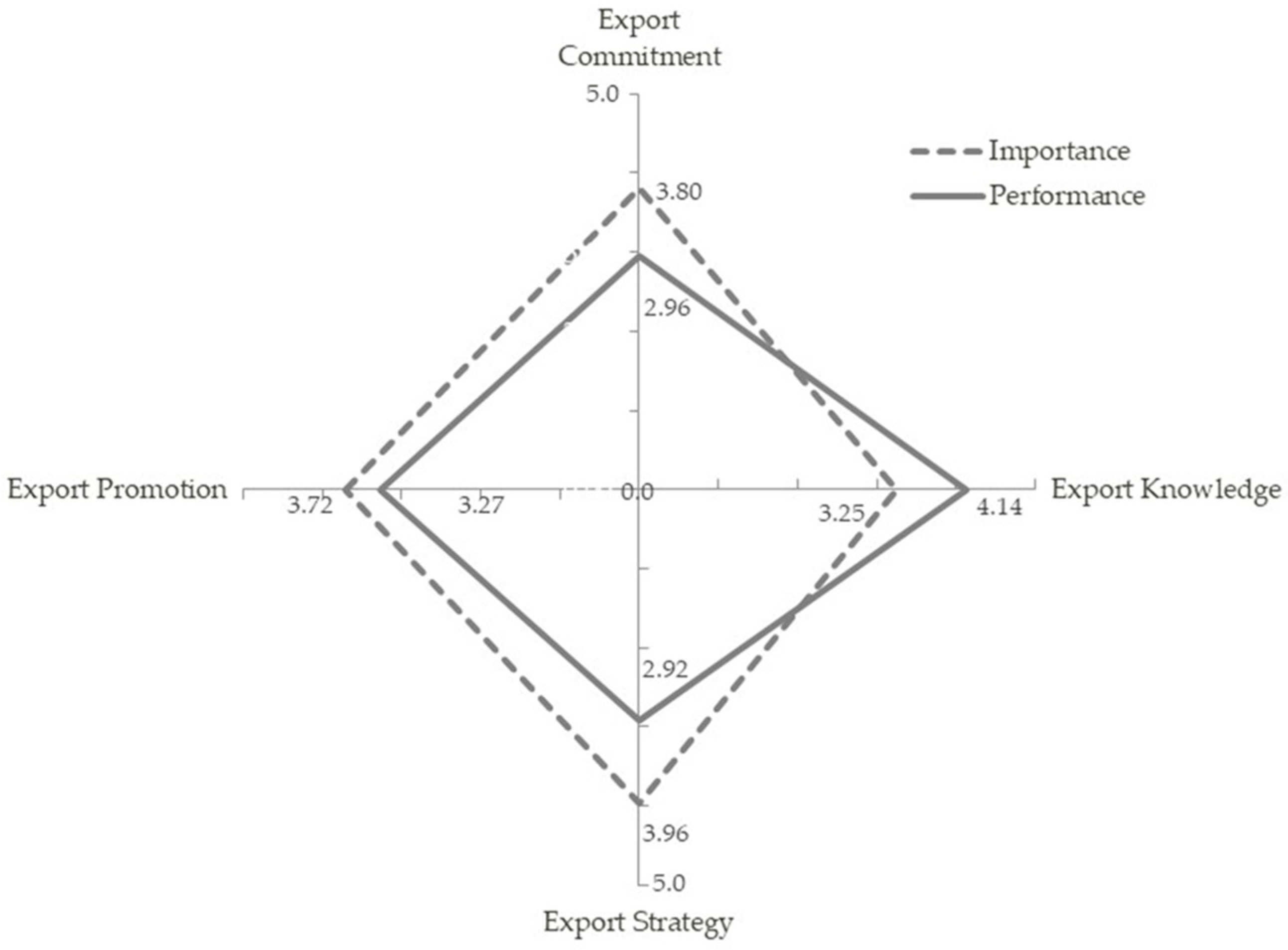

- Dressler, M. Erfolgsfaktoren im Weinexport und Leistungswahrnehmung deutscher Anbieter. In Deutsches Weinbaujahrbuch 2015; Schultz, H.-R., Stoll, M., Eds.; Ulmer: Stuttgart, Germany, 2015; Volume 66, pp. 146–158. [Google Scholar]

- Hofstede, G. Cultural constraints in management theories. Acad. Manag. Exec. 1993, 7, 81–94. [Google Scholar] [CrossRef]

- Kreiser, P.M.; Marino, L.D.; Dickson, P.; Weaver, K.M. Cultural influences on entrepreneurial orientation: The impact of national culture on risk taking and proactiveness in SMEs. Entrep. Theory Pract. 2010, 34, 959–983. [Google Scholar] [CrossRef]

- Pagell, M.; Katz, J.P.; Sheu, C. The importance of national culture in operations management research. Int. J. Oper. Prod. Manag. 2005, 25, 371–394. [Google Scholar] [CrossRef]

- Wursten, H.; Fadrhonc, T. International Marketing and Culture. ITIM International. 2012. Available online: http://www.academia.edu/22416733/International_marketing_and_Culture (accessed on 20 November 2018).

- Dressler, M. Managing Export Success–An empirical Picture of German Wineries’ Performance. In BIO Web of Conferences; France, 2001; EDP Sciences: Les Ulis, France, 2015; p. 03001. [Google Scholar]

- Agri, D. Wine CMO: Submission of Financial Table of the National Support Programme; Commission Regulation EC 555/2008; European Commission: Belgium, Brussels, 2017. [Google Scholar]

- Dressler, M. Wahrnehmung der Exportaktivitäten von deutschem Wein—Die “Sicht von außen”. In Pfälzer Weinbautage 2016; Rheinpfalz, D., Ed.; DLR Rheinpfalz: Neustadt, Germany, 2016. [Google Scholar]

- Dressler, M. Strategic profiling and the value of wine & tourism initiatives: Exploring strategic grouping of German wineries. Int. J. Wine Bus. Res. 2017, 29, 484–502. [Google Scholar]

- Degravel, D. Strategy-As-Practice to Reconcile Small Businesses’ Strategies and RBV? J. Manag. Policy Pract. 2012, 13, 46–66. [Google Scholar]

- Porter, M.E. How Competitive Forces Shape Strategy. Harvard Businesss Review. Harvard Business School Publishing: Boston, MA, USA, 1979; pp. 137–145. [Google Scholar]

- Miles, R.E.S.; Snow, C.C.; Meyer, A.D.; Coleman, H.J. Organizational Strategy, Structure, and Process. Acad. Manag. Rev. 1978, 3, 546–562. [Google Scholar] [CrossRef]

- Hoffman, D. Struktur und Entwicklung des Weinmarktes in Deutschland. In Weinbaujahrbuch 2014; Schultz, H.-R., Stoll, M., Eds.; Ulmer: Stuttgart, Germany, 2013; Volume 65, pp. 242–245. [Google Scholar]

- Schnabl, A.; Lappöhn, S.; Pohl, A. Ökonomische Bedeutung der Weinwirtschaft für Österreich; IHS: Vienna, Austria, 2016. [Google Scholar]

- Kim, W.C.; Mauborgne, R.A. Blue Ocean Strategy: How to Create Uncontested Market Space and Make the Competition Irrelevant; Harvard Business Review Press: Boston, MA, USA, 2014. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | 1900 | 1938 | 1980 | 2018 |

|---|---|---|---|---|

| Cooperatives | 113 | 493 | 342 | 164 |

| Membership | 1000 | 29,000 | 67,000 | 49,000 |

| Consumption by Category | 2002 | 2016 | 16 vs. 02 |

|---|---|---|---|

| Spirits | 5.9 | 5.4 | 92% |

| Sparkling wine | 3.9 | 3.7 | 95% |

| Wine | 20.3 | 20.6 | 101% |

| Beer | 121.9 | 104.0 | 85% |

| Total | 152.0 | 133.7 | 88% |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dressler, M. The German Wine Market: A Comprehensive Strategic and Economic Analysis. Beverages 2018, 4, 92. https://doi.org/10.3390/beverages4040092

Dressler M. The German Wine Market: A Comprehensive Strategic and Economic Analysis. Beverages. 2018; 4(4):92. https://doi.org/10.3390/beverages4040092

Chicago/Turabian StyleDressler, Marc. 2018. "The German Wine Market: A Comprehensive Strategic and Economic Analysis" Beverages 4, no. 4: 92. https://doi.org/10.3390/beverages4040092

APA StyleDressler, M. (2018). The German Wine Market: A Comprehensive Strategic and Economic Analysis. Beverages, 4(4), 92. https://doi.org/10.3390/beverages4040092