1. Introduction

“Scotch whisky is more than a whisky. It is part of Scotland’s heritage and folklore. It is used as a medicine to cure many ills. As a toddy, it can dispel colds and 'flu. In porridge, it can drive out the freezing cold of Scotland’s winters. It lubricates the larynx and helps parties go with a swing.”

These are the words of Bill Walker MP in 1987, during the reading of the Scotch Whisky Bill in the UK Parliament [

1]. The emotive language of a representative from Scotland highlights more than the natural strength of feeling for a Scottish product that contributes £3.95 billion to the UK’s balance of trade [

2]. The industry was under attack from European Commission proposals for a standard Europe-wide definition of whiskey (the common spelling for the Irish and American category). The proposal threatened to undermine the labors of several decades to establish Scotch whisky (the common spelling for the Scotch and Canadian category) as the premier distilled spirit category, protected by law as to its geography and production process. That legal protection, defined in UK law since 1909, remains intact and was upheld by the European Commission in 1989. Its status was clarified further in ‘relevant market’ analysis in the 1997 merger of Guinness and Grand Metropolitan to form Diageo by the European Commission [

3], and the Federal Trade Commission [

4]. The UK Government recently detailed all current technical specifications of the Scotch whisky category, clarifying how the production method embodied in the Scotch Whisky Regulations 2009 differs from current production regulations in other whiskey-producing jurisdictions, including elsewhere in Europe [

5].

The Scotch whisky industry presents an interesting historical case study of industrial organization. The industry’s brands are of extremely long duration with many originating in the 1800s, and some, such as Johnnie Walker, J&B Rare and Chivas Regal sell globally. For business historians, the industry is an important example of Britain’s competitive advantage and one that internationalized many decades before the post-World War II era, largely under the leadership of Distillers Company Limited (DCL). As the large brands of Scotch whisky are blends of up to 40 different whiskies, firms have been bound by a multitude of co-operative agreements, swapping whiskies directly and through brokerage to meet their blending requirements. At the micro-level, such interplay between competition and collaboration is a classic empirical setting to test aspects of industrial economics, such as game theory and coopetition [

6]. From a macro-perspective, how the industry and the institutional environment has interacted through the long history, spanning world wars, Prohibition and other geopolitical events informs debates in regulation and co-evolution [

7].

In this article I explain how the industry has responded to the dynamics of consumption in the context of a highly idiosyncratic production process that incorporates mandatory stock maturation of at least three years as well as the location-specificity of distillation in Scotland. I have compiled a database of production, sales and stock information from the Scotch Whisky Association (SWA) database for the period 1969–2014 [

8], and an additional historic source that utilized UK government excise tax returns for the period 1945–1969 [

9]. In explaining and expanding on the industry’s evolution I have drawn on a selection of regulatory reports, including merger inquiry documents, all of which are available from the relevant agency websites. I have also sourced other archive material and related literature as indicated in the reference list below.

2. Theoretical Background

Alfred D Chandler’s post-World War II analysis of US multinational corporations [

10,

11], with its account of comparative industrial organization drawn from a multi-year, multi-jurisdictional study (known as the Harvard Program), continues to provide the academic foundation for contemporary case studies in the disciplinary areas of economic and business history and strategic management. For business historians such historically-informed analysis of firms and industries offers insights into the relationship between strategy, structure and performance [

12]. For strategic management, the closely aligned classic Structure-Conduct-Performance (SCP) paradigm that emerged from industrial economics [

13], was popularized by Michael Porter, whose Five Forces framework is a mainstay for business school students and management consultants [

14]. In this top-down analysis of strategic management a firm’s performance is governed essentially by the structural dynamics of the industry within which it operates, albeit with the definition of ‘industry’ defined flexibly to accommodate ‘strategic groups’ of firms that constitute close competitors [

15].

In the increasingly dynamic and international operating environment of the 1980s, scholars acknowledged shortcomings in the SCP paradigm. In seeking an alternative that placed the firm at the heart of the analysis, as opposed to the industry within which it operates, the Resource-Based View (RBV) emerged [

16]. With its academic foundation in the work of Edith Penrose [

17], RBV holds that performance is a function of a firm’s resources and capabilities, and how it uses them to generate competitive advantage [

18]. More recently a third paradigm has been proposed, to link SCP and RBV into a unifying framework [

19]; a tacit recognition that neither is satisfactory in its own right, and an acknowledgment of the over-riding importance of the institutional environment in shaping industrial organization and firm behavior [

20]. This is especially significant in industries subject to regulation, or in instances where firms’ strategies are conditioned by interaction with the institutional environment, for example as part of the mergers and acquisitions process.

In seeking to draw comparisons between US ‘managerial capitalism’ and UK ‘personal capitalism’, Chandler’s 1990 book,

Scale and Scope, highlighted UK entrepreneurship emanating in the Victorian era. British industrial fortunes prior to the World Wars were built on the consumer goods industry and four key firms, Lever Brothers, Imperial Tobacco, DCL and Guinness. Guinness acquired DCL in 1986 in what remains one of the most notorious and controversial mergers in UK corporate history for the accompanying illegal share support operation. In charting the success of UK industrial organizations the evolution of Scotch whisky, and in particular, DCL, featured prominently. Focusing on the product innovation of the Coffee still, that underpinned the larger scale production of Scotch whisky, Chandler’s analysis charted the support for the marketing and advertising initiatives of the brand owners as they pursued international growth. He highlighted the mergers and acquisitions of the inter-World Wars era that saw DCL emerge as the dominant producer and brand owner. DCL diversified subsequently into the manufacture of gin, industrial alcohol, and pharmaceuticals, the latter of which has its legacy in the thalidomide scandal, for which DCL became the UK’s licensed manufacturer [

21]. Weir’s subsequent account of the industry between 1877 and 1939 detailed the numerous attempts to refine and control the production process, exposing the nature of the relationships between firms locked together in a series of collaborative agreements, before many were incorporated under the DCL banner [

22].

From this historic backdrop two related academic themes have emerged from subsequent analysis of the spirits industry; the role of brands in the internationalization process, and the relationship between the institutional environment and firms, in particular with regard to cross-border mergers and acquisitions strategies. In broad terms, the former, exemplified by the work of Da Silva Lopes [

23,

24], is a detailed account of individual firms’ resources and capabilities, and how this augmented international growth, in particular in the period 1960–2000. The theme of mergers and acquisitions has been investigated in the context of the spirits industry’s co-evolution with the changing regulatory environment [

25]. The significance of the coordinated Federal Trade Commission and European Commission investigation of the 1997 merger between the UK’s Grand Metropolitan and Guinness to form Diageo was a specific example in a commissioned policy review by prominent economist, and originator of the concept of coopetition in industrial economics, Barry Nalebuff [

26]. Naturally, the Scotch whisky industry and its firms feature in both lines of research, albeit the focus is either at the evolution of brands and brand portfolios or in the nature of the interaction with the international regulatory policy regime. My article returns to a more detailed, and contemporary account of the structure and organization of the Scotch whisky market and how the dynamics of production and consumption underpin industrial organization and performance, situating the analysis in the Structure-Conduct-Performance paradigm, albeit with an emphasis on the importance of interactions with the institutional environment.

3. The Production of Scotch Whisky

Although many countries produce whisk(e)y from assorted cereals, the legal designation of ‘Scotch whisky’ means that the whisky has been produced and matured in Scotland in oak casks for a minimum of three years, from distilleries located in the five designated regions labelled in

Figure 1. Some industry sources consider the islands, with the exception of Islay, as constituting a distinct sub-region (highlighted separately in

Figure 1). The SWA, however, categorizes them within the Highlands region. Since 2005, Scotch whisky has been defined into five distinct categories: Single Malt Scotch Whisky (distilled at a single distillery and must be bottled in Scotland), Single Grain Scotch Whisky (distilled at a single distillery), Blended Scotch Whisky (a blend of one or more Single Malt Scotch whiskies with one or more Single Grain Scotch whiskies), Blended Malt Scotch Whisky (a blend of Single Malt Scotch whiskies which have been distilled at more than one distillery) and Blended Grain Scotch Whisky (a blend of Single Grain Scotch whiskies which have been distilled at more than one distillery) [

27].

There are currently 115 operational distilleries the majority of which are small, malt whisky distilleries with a concentration around the river Spey. There are also seven large grain distilleries located mainly in the Lowland region near to Glasgow and Edinburgh. On the basis of 2014 production, the average output per grain distillery is 46 million liters of pure alcohol (mlpa), and that per malt distillery is 2.6 mlpa.

Malt whisky is made exclusively from malted barley by the pot still method, a batch process that is comprised of the four main stages of malting, mashing, fermenting and distilling. Distillation in large copper pot stills is usually performed at least twice, and in some cases three times, to convert the low alcohol yeast-fermented liquid ‘wash’ into an acceptable quality distillate for maturation in oak casks for at least three years, although some malt whiskies are left in casks to mature for periods of more than 18 years. The malt whisky production process is intermittent with the still being recharged every time a distillation is completed [

5,

28].

Malt whiskies differ considerably in flavor depending on the distillery from which they are produced. The geography, climatic conditions and the nature of the soil from which the water is drawn for production are just some of the many factors that affect the characteristics of a malt whisky. Lowland malts are the lightest in flavor and Islay malts are heavier and noted for their smokiness and peaty flavor. Half of all distilleries are in Speyside, this being the home of some of the best known malts such as Glenfiddich.

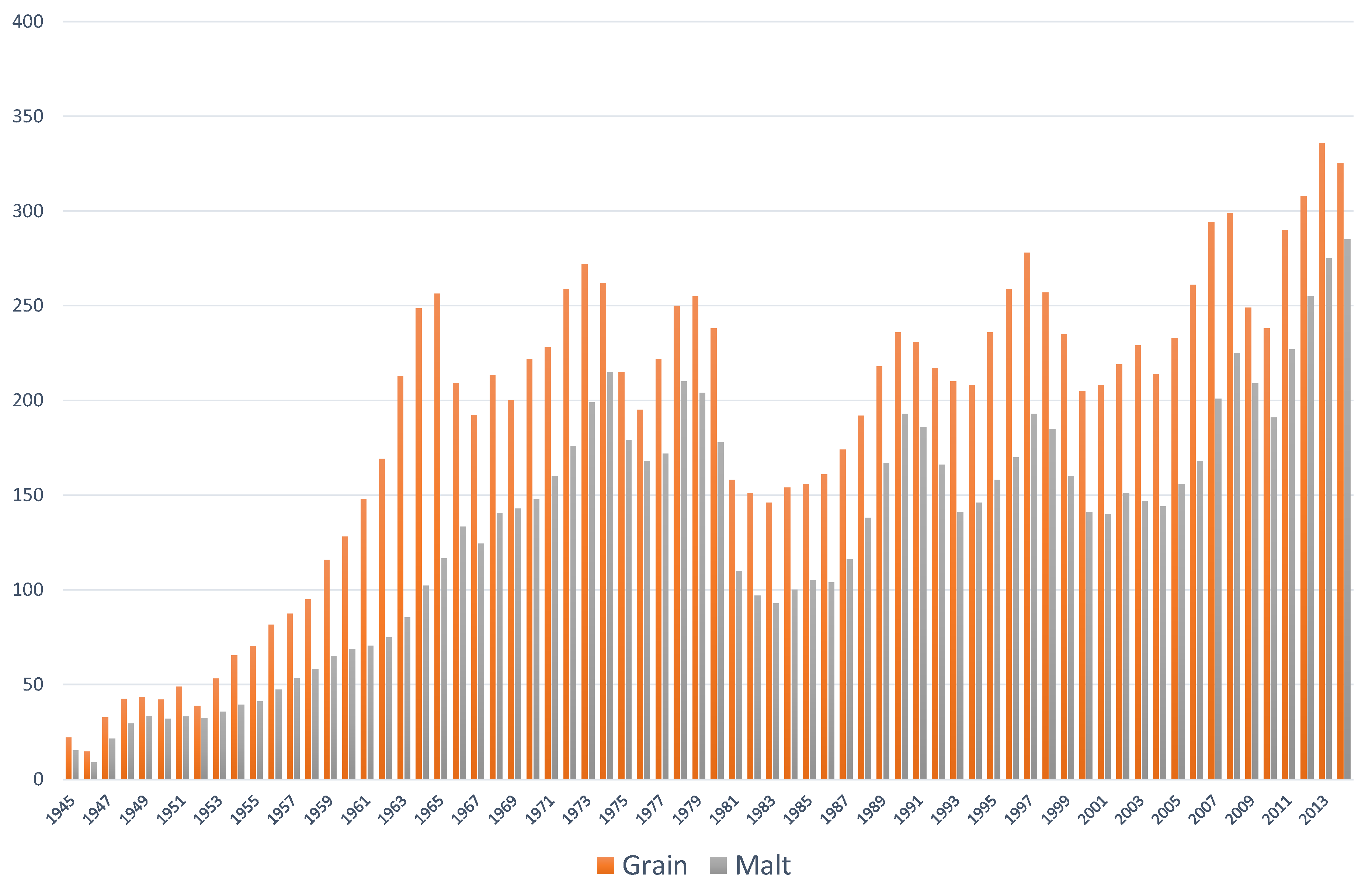

The grain distilleries are located primarily, and as a function of history, in the Lowland region that is home to the major metropolitan areas of Edinburgh and Glasgow. Grain whisky is made from a mixture of malted barley, wheat or maize and is produced in a continuous distillation process from much larger distilleries employing a Patent or Coffey still, named after Irishman Aeneas Coffee’s 1831 invention. Consequently, there are considerably fewer grain distilleries than there are malt distilleries due to the much larger capital commitment and not all major brand owners have historically owned their own grain distilleries. Grain whisky production volumes are greater than that of malt whisky reflecting the fact that blended Scotch whisky brands are typically 60% grain spirit mixed with 40% malt spirit. As

Figure 2 shows, the production of both grain and malt whisky tends to fluctuate and adjust to changing demand although not always in a synchronized manner, as discussed in

Section 5 below.

The process of blending malt and grain whisky has been the most important factor in the growth and internationalization of Scotch whisky. Blending companies and brand owners obtain new whisky as ‘new fillings’ (the name reflecting the fact that buyers supplied their own casks) either by purchasing it or exchanging it for the output of their own distilleries. Such trading in the new fillings market was normal practice for all but Distillers Company Limited (DCL), acquired by Guinness in 1986, which had been entirely self-sufficient with respect to both grain and malt distillery ownership to produce its blend brands since the mid-1920s. Once the whiskies have matured in cask for sufficient time they are mixed in a blending vat with water added to reduce the alcohol content. The resulting blend is usually returned to cask for an additional few weeks or months before bottling.

4. Consumption of Scotch Whisky

Although recorded in UK Exchequer accounts as far back as 1494, the Scotch whisky market in a form recognizable as such today is usually anchored in the early 1800s. The harsh and fiery liquor associated with the illicit Pot or copper stills of the Scottish Highlands was bought in cask by grocers and wine merchants who ‘vatted’ (mixed in large tanks) the whisky to iron out inconsistencies and make the product more appealing to clients in the metropolitan areas of Glasgow and Edinburgh. Foremost among these merchants were John Walker, George Ballantine, the Chivas brothers, and John Dewar. Following the introduction of the Coffey still, the industrialization of whisky production from larger grain distilleries became possible. By 1860, whisky broker Andrew Usher & Co started the blending of grain and malt whisky spirits to create a smoother and lighter tasting Scotch that met with favor in England, subsequently paving the way for the internationalization of Scotch whisky [

29]. Annual production of whisky rose rapidly to almost 90 mlpa by the end of the 19th century.

The Scotch whisky market internationalized before many other organized industrial categories. Incentivized as much by declining per capita consumption of spirits in Victorian Britain as the competitive opportunity presented by the Phylloxera plague that started in the 1860s, and which devastated the French vineyards, Scotch whisky gradually displaced French brandy in the international market. Entrepreneurial brand owners with relatives in Britain’s colonies established their own networks of agents to handle international trade. By 1914, for example, John Dewar & Sons Limited had branch offices in New York, Calcutta, Sydney, Melbourne and Johannesburg to complement the first branch office opened in London in 1891 [

30]. For the industry in aggregate, exports accounted for almost 30% of total sales, with a fairly even distribution across North America, Europe, and Australasia, as brand owners, including Buchanan’s, Walker’s, DCL and Bell’s cemented an export future, adding to maturing stock positions and investing in efficient equipment, such as bottling plants.

Emerging almost in parallel with this early successful internationalization was the Temperance movement, rearing its head in the legislative changes of the Lloyd George government of 1907/08 in the UK, and the Women’s Christian Temperance Union that culminated in the legislation that enacted Prohibition in the US in the 1920 to 1933 period [

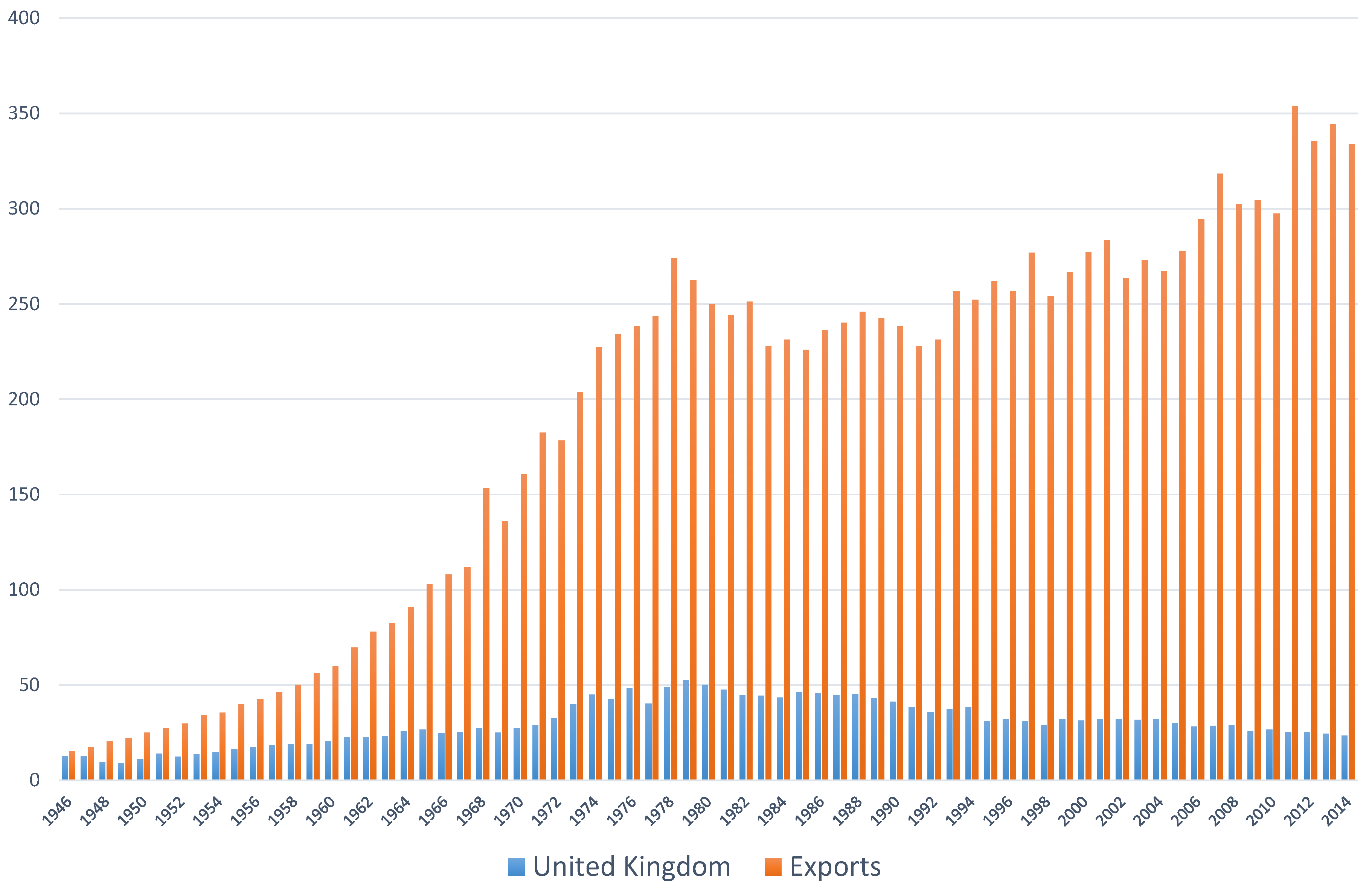

24]. However, assaults on the industry’s fortunes as a result of war, the spread of anti-drink legislation and tariff protection that was apparent in the inter-War era, failed to dent the industry’s longevity as its post-World War II trajectory in

Figure 3 shows. Weir estimates that annual sales of Scotch were approximately 90 mlpa just prior to World War I, of which 28% was attributable to exports. By 1932, consumption had fallen to 35 mlpa, before recovering to 48 mlpa in 1938. This level was surpassed in 1953, when the industry resumed full operation after World War II.

Having managed Prohibition with the benefit of ‘controlled bootlegging’ through the industry-regulated scheduled area initiative (under the radar of the US and UK authorities, who Weir suggests may have purposefully turned a blind eye), exports declined less than 3% between 1920 and 1932. Following the repeal of Prohibition, the UK government played an important role in negotiating reduced import tariffs to the US. By 1938 export volume outstripped domestic UK sales, with the US accounting for over 60% of the export total. Exports then delivered rapid and sustained growth in the 1950s and 1960s as the world’s major economies recovered from the war years and emerging markets industrialized.

It is clear from

Table 1 below that Scotch whisky is truly global in reach. Although France is the largest market for Scotch whisky shipments, the US is the key driver of industry profitability, as it accounts for 19% of the industry’s total export value of £3.95 billion, compared to France’s 11%. The difference in export value to these two markets is accounted for by the significance of lower-value bulk blend Scotch shipments to France, compared to higher-value bottled blended Scotch shipments to the US. Shipments of higher-value bottled single malt Scotch to both countries are similar, and neither country is important in the bulk malt export trade, according to the latest data available from the SWA. Industry leader, Diageo, elaborates this relative importance of the US on the firm’s website “

North America accounts for about a third of our net sales and around 45% of operating profit and is the largest market for premium drinks in the world”. The 1997 merger of Grand Metropolitan and Guinness that created Diageo, highlighted the firms’ collective dominance of the premium blended Scotch market, defined for anti-trust purposes around the brands Johnnie Walker Red Label, J&B Rare and Dewar’s (the latter of which was sold to comply with the directions of the Federal Trade Commission [

31]).

The emerging markets have played a significant, albeit volatile role in the progress of the industry for several decades. Venezuela, for example, illustrates not just the volatility of emerging market growth, but the impact on Scotch whisky sales from the economic cycle, foreign exchange rates, changing excise tax regimes and wider socio-economic factors. Venezuela experienced explosive growth in Scotch whisky demand in the 1970s during the oil boom. However, the import restrictions and 80% excise duty rate that followed the hyperinflationary bust of the 1980s quickly reversed this trend. As the economic situation improved in the late 1980s a new surge in Scotch whisky demand culminated in sales of more than 9 mlpa by 1993, before almost halving again by 1995. This pattern of boom and bust has been repeated again through the 2000s as shown.

5. The Stock Cycle and Competitive Behavior

It is immediately apparent from the economics of production and the history of export growth that industry profitability is highly dependent on the accuracy of forecasting future demand, and matching production accordingly. The industry’s record of achieving this through the course of history is poor, with observable patterns of over-production in an environment of positive demand growth and under-production when the outlook becomes less favorable. This was particularly apparent in the 1970s and 1980s, giving rise to what was referred to at the time as the stock or whisky cycle.

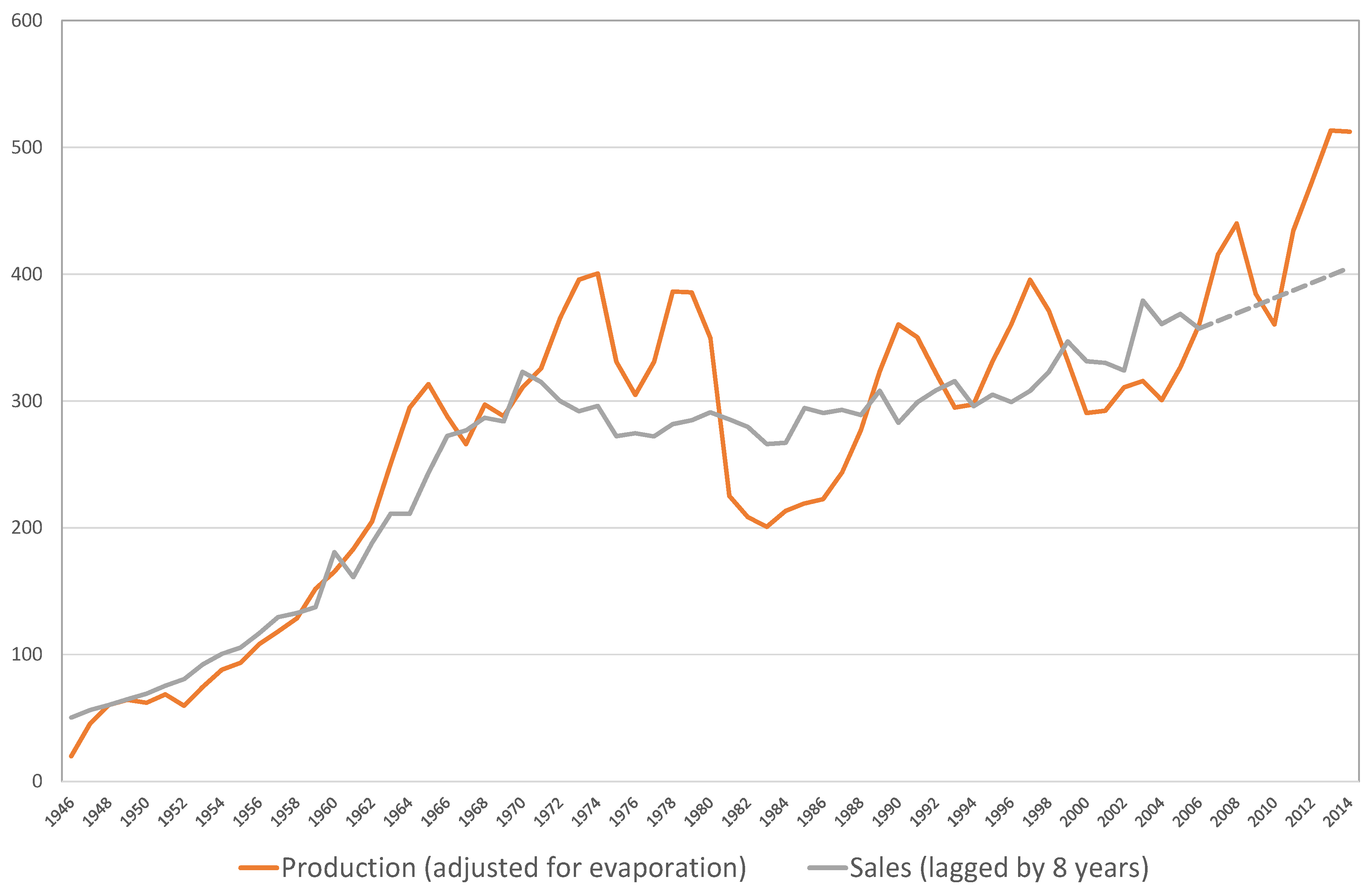

Figure 4 illustrates the relationship between actual production and future sales. Scotch whisky produced today will, on average, be consumed in eight years’ time even though it must only mature for three years to be legally sold as Scotch whisky. Although many leading blends, such as Johnnie Walker Red Label, J&B Rare and The Famous Grouse, do not carry age statements, others do. For example, in 1994, UK market leader, Bell’s was relaunched by brand owner, Guinness, as an eight-year-old blend, to signal a premium image. At the time there was a surplus of mature whisky. However, in 2008 with mature whisky in short supply, the age statement was dropped and the blend was revamped, the assumption being that it contains less mature stock [

32]. In contrast, notwithstanding the evident constraint, the age statement remains integral to the premium status of brands such as Johnnie Walker Black Label and Chivas Regal (12 year-old blends), and well-known single malt brands such as The Macallan are typically at least 10 years old. Conversely value products, in particular those sold as supermarket own label blends, may contain Scotch whisky of no more than five years-old. The weighted average age of malt and grain stocks in 2014 was an estimated 4.9 years for all whisky and 7.9 years for whisky older than three years. This compares with an estimated 5.1 years for all whisky and 7.5 years for whisky older than three years in 2000. Consequently, in aggregate, eight years is an appropriate average maturity to use in calculations.

To account for the fact that the whisky evaporates every year it is maturing in cask, today’s production volume is adjusted downwards by 16%. This is referred to as the ‘angel’s share’. Up to 5% can be lost in the first year before settling to closer to 2% per annum, although this varies depending on climatic conditions and types of whiskies and casks used for maturation [

33]. The UK Government uses a working average of 2% evaporation per annum per cask [

5], and this has therefore been applied to the average maturity of eight years. The dotted line on the chart is not an official sales forecast, but follows the trend of actual sales recorded in the last ten years, where sales increased on average at approximately 6 mlpa per annum. It represents sales that will occur in the eight years after 2014 from whisky produced in the period 2006 to 2014. When the production line sits above the lagged sales line the industry is over-producing, and in reverse, the industry is under-producing. The long period of over-production in the 1970s gave rise to what was called the ‘whisky loch’.

The Scotch whisky industry therefore has to forecast accurately what will be consumed on average in eight years’ time when planning production today. Forecasting sales so far ahead is by no means an easy task, more so as that planning needs to be done on a distillery by distillery basis. This has become particularly apparent recently, with the (re)emergence of the single malt category as a growth driver in its own right. According to SWA data, the single malt category, which comprised less than 5 mlpa in 1977, now accounts for some 29 mlpa, representing 9% market share of all Scotch whisky shipments. Responding to this growth dynamic has created problems for market leaders, if not the industry as a whole. In a controversial move in 2003, subsequently accepted in an industry-wide agreement on category definitions, Diageo opted to vat different malts from elsewhere in Speyside as it had insufficient stocks, and could not produce sufficient quantities in the future, for its popular Cardhu 12-year-old single malt [

34].

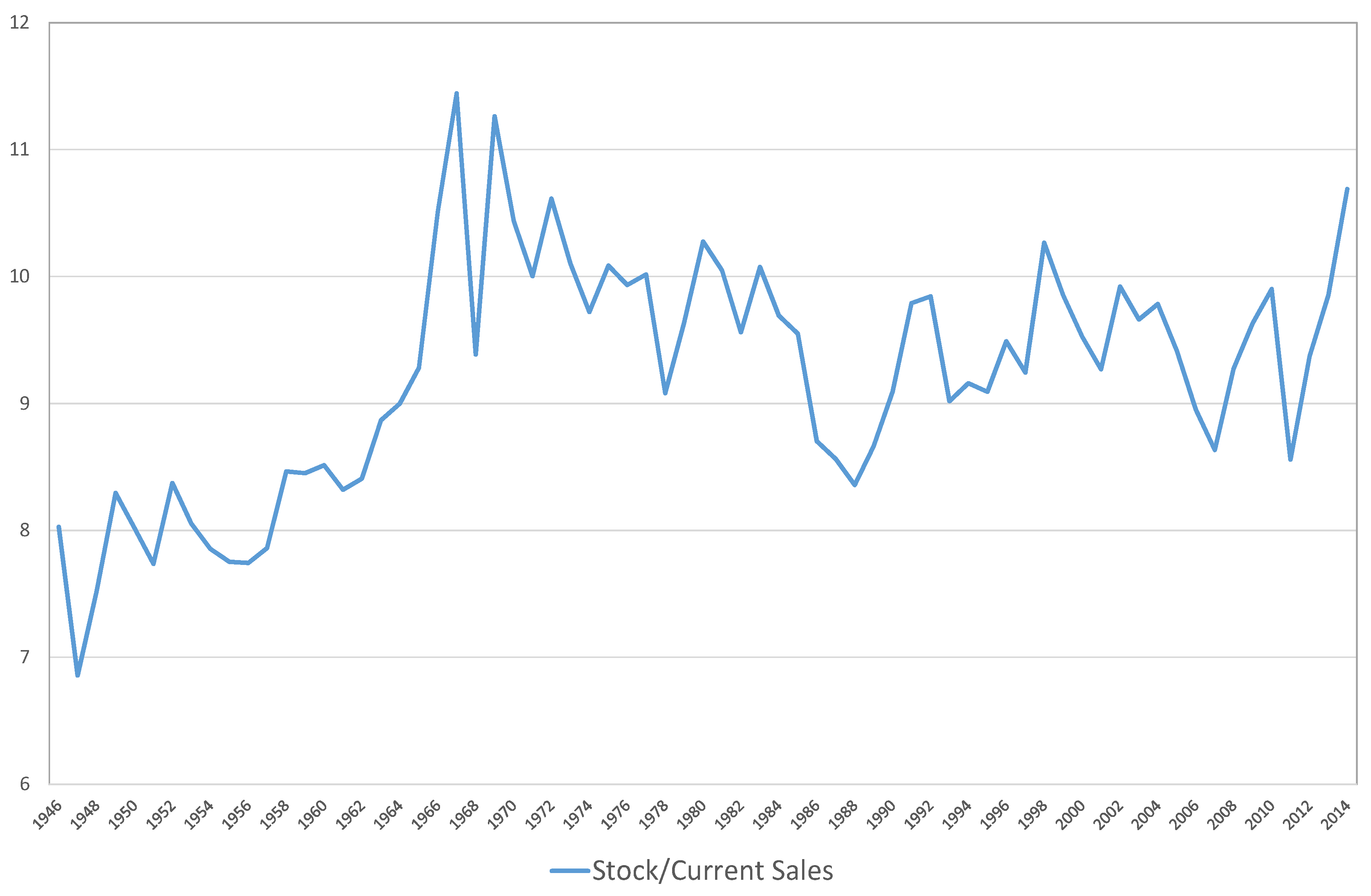

Rationally, for a product that benefits from additional maturation in both taste characteristics and the optionality of an aged stock profile (the opportunity to add premium and deluxe brands), production should adjust in a controlled and gradual manner. As is clear from

Figure 4 above, the production profile of the industry is characterized by sharp cuts followed by equally sharp reversals. The reason this occurs is explained by

Figure 5, where deviations from an ideal stock to

current sales ratio of around 9.5 years (reflecting the average 8-year old product, and allowing for evaporation) is the catalyst for these sharp changes in production. The difficulty of managing production and stock levels is amplified if there is a concurrent rise in the cost of carry (the financing of stock in warehouse); smaller producers quickly come under pressure to both cut back production and liquidate stock. This has a knock-on effect throughout the industry in terms of the overall pricing environment.

Industry consolidation in order to rationalize production and manage stock levels is an obvious strategy for managing the whisky cycle. Throughout the industry’s history the more numerous and smaller malt distilleries have gone through repeated cycles of closing down completely, being mothballed for extended periods, and being re-opened by new entrants to the industry. Acquiring a divested or mothballed malt distillery has been the only realistic way for small scale entry into the industry. In contrast, the ownership of grain distillation capacity has followed a somewhat different path, reflecting its much larger scale and the production dynamics outlined above. Grain distillation offers the potential to divert productive capacity to the manufacture of vodka, gin and industrial alcohol.

From the inception of the market for blended Scotch whisky, DCL, formed in 1877 from the amalgamation of six distilleries, dominated the production of grain spirit, and from that position sought to control the wider whisky market [

22]. During the 1880s, when Scotch whisky sales declined sharply, DCL’s initiatives to match production more closely to future demand were credited for restoring the industry’s fortunes. However, DCL’s attempts to fix prices to blenders was not met with universal accord. A group of Edinburgh merchants and blenders established their own unique co-operative, the North British Distillery Limited (NB) in 1885, with the objective of securing a dedicated supply of grain that was both consistent and at a price their owners considered acceptable to meet their individual brand and blending commitments [

29]. The co-operative remained intact with a unique shareholding structure until 1993, when two shareholders, Grand Metropolitan and the Edringtongroup bought out the other shareholders.

For much of the 1900s, and notwithstanding the early acrimony, DCL and NB worked together co-operatively for the good of the industry when needed, for example during Prohibition. Some of their co-operative agreements would almost certainly breach today’s anti-trust legislation at the level of cartelization and collective dominance, although they served a crucial role in stabilizing and managing the industry production and stock cycle. DCL not only controlled all grain capacity with the exception of NB but also owned several malt distilleries. However, it remained dependent on the large blending houses, Buchanan, Dewar’s and John Walker, for mature stocks as well as access to markets. In 1925 the ‘Big Amalgamation’ occurred, with DCL absorbing the three blending houses, to create a forward-integrated, totally self-sufficient owner of leading Scotch whisky brands. From this leadership position, and aligned to the inherent stability within the NB co-operative, the inter-War Prohibition era and post-World War II transition to rapid export growth were managed with a demonstrable balance in production and stock levels.

By the time the late 1970s slowdown in consumption materialized, the industry was already over-supplied with stock. In terms of strategic behavior, the industry’s fortunes were increasingly impacted by new grain distillation capacity that was added in the 1960s, under the controlof the private firm William Grant & Sons (Girvan distillery opened in 1963 and expanded in 1975) and Invergordon Distillers (North Highlands, opened in 1960 and expanded in 1978). The latter firm was acquired in 1993 by the then US-owned Whyte & Mackay. These two firms were cited widely as responsible for disrupting the industry consensus on stock management and long-term brand building that re-emerged in the early 1990s [

35].

The well-documented ‘merger wave’ of the 1980s, where the large multinational spirits firms emerged from the UK’s former brewers—Allied-Lyons (acquired Hiram Walker in 1986), Grand Metropolitan (acquired Heublein in 1987) and Guinness (acquired Bell’s in 1985 and DCL in 1986) [

23]—was heralded as the solution to the wide swings in production and stock liquidation of the 1970s and early 1980s. Of themselves, they did not rationalize and consolidate grain whisky production, and this is also true for the later mergers, Diageo and Pernod Ricard’s joint acquisition of Seagram (2000), and Pernod Ricard’s acquisition of Allied Domecq (2005). The principle objective of these mergers was the optimization of an international distribution capability around a portfolio of leading spirits brands [

25].

6. Discussion and Conclusions

Periods of significant under-production and over-production have characterized the Scotch whisky industry since the 1970s. In many ways this mirrors the early days prior to the emergence of blending and internationalization in the Victorian era, where cycles of boom and bust were the norm, exemplified most catastrophically by the collapse of Pattisons in 1898, and with it, a large proportion of the independent malt whisky sector [

9]. It was from this era that DCL emerged as the increasingly dominant force in the Scotch whisky industry, initially in terms of controlling the grain market, but by the late 1920s, as an integrated grain and malt distiller with ownership of a portfolio of leading blend brands [

30]. Both Weir and Gardiner recount significant periods where, for the greater good of the growth and stability of the industry, the arch-rivalry between DCL and NB was set aside, with formal agreements and collaboration that extended to the fixing of prices and volumes of whisky released to the market. So, for example, as the industry struggled in the aftermath of the introduction of Prohibition, the two rivals agreed to cut production through a quota system in the ratio four-fifths DCL to one-fifth NB. The quota system was effective in that grain whisky prices remained unchanged between 1925 and 1935 despite a large drop in maize prices. The fact that the industry managed to balance production and stock levels to match demand in the 1950s and 1960s owed as much to rapid export growth as the relatively consolidated ownership of grain production and the influence of DCL and NB that continued through this period. The period of relative harmony ended in the 1970s.

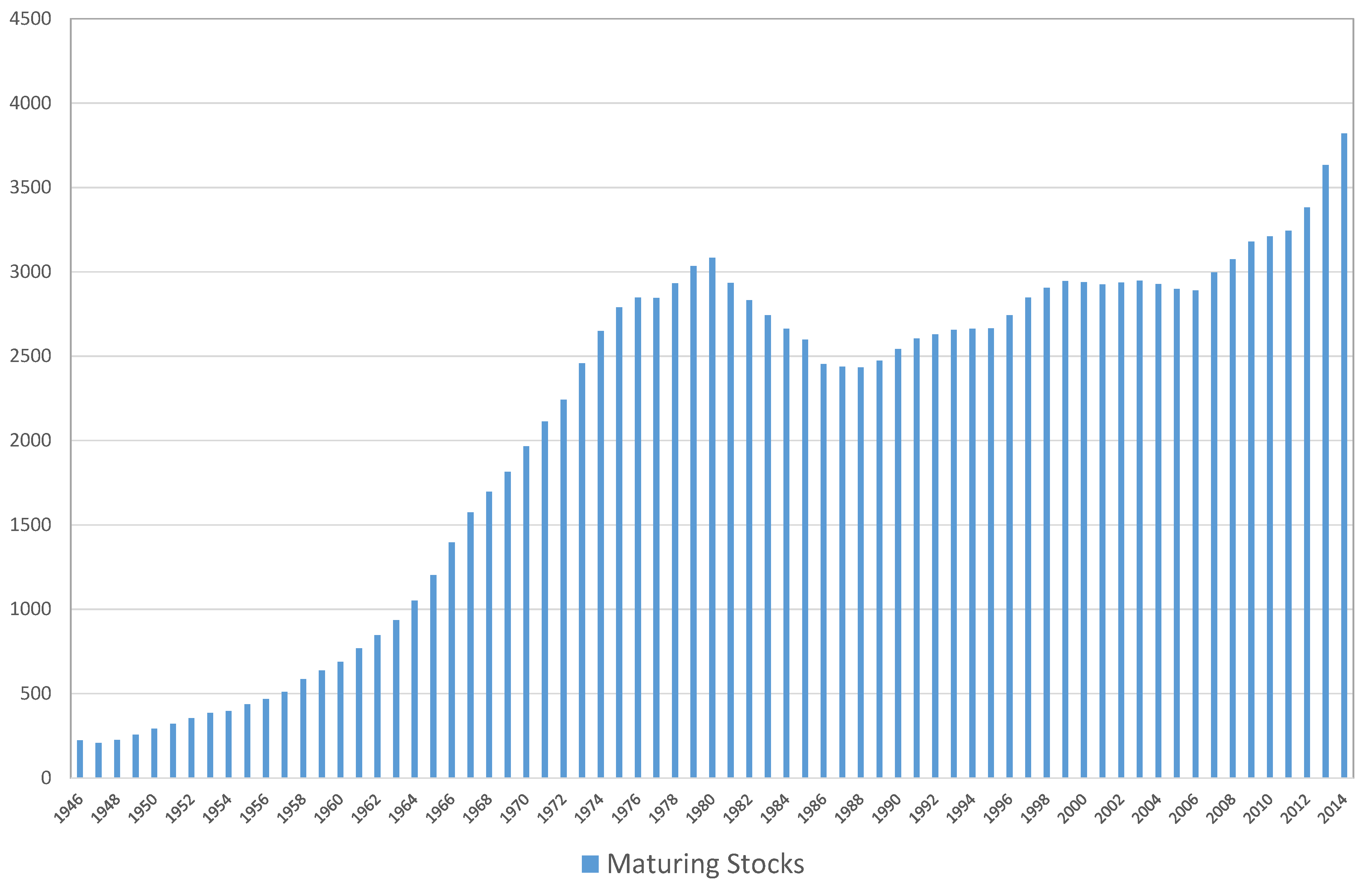

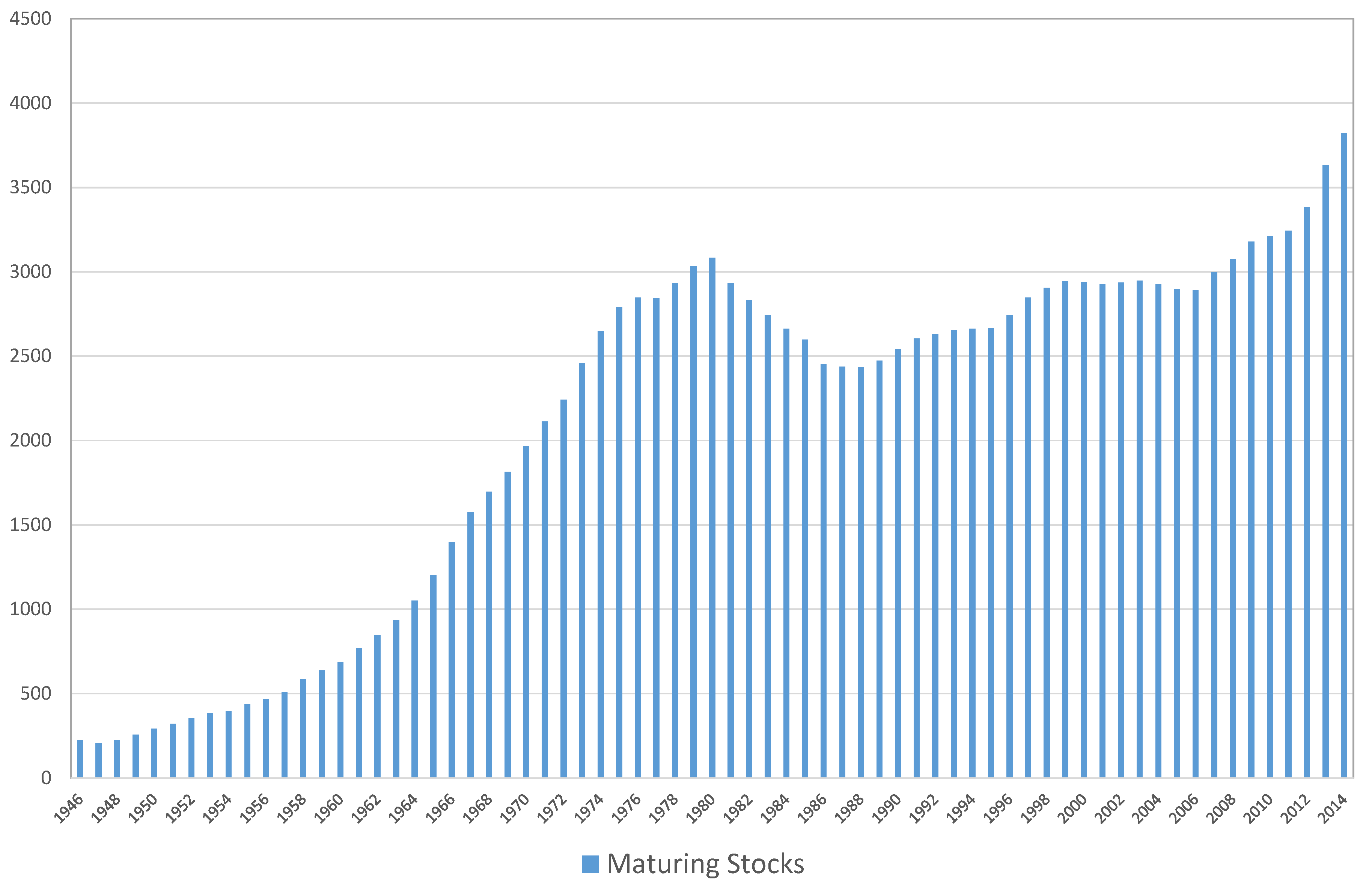

Following a period of growth in the 2000s, fueled largely by emerging markets such as India and Brazil, sales have declined from the peak level in 2011. After a temporary dip in the immediate aftermath of the Financial Crisis of 2007/8, production has continued to rise, reaching record levels in 2014. The current stock to sales ratio is approaching the critical high seen in the 1970s, and maturing stocks, as shown in

Figure 6 below, are also at record levels. Firms with limited financial resources may be forced once again by circumstance to take drastic action to cut production, thereby undermining rational longer-term strategic planning. This has likely been tempered by the environment of unusually low interest rates that have continued after the Financial Crisis. Lower interest rates reduce the likelihood of financial distress and the pressure to increase cash flow by liquidating stock. However, if central banks start to raise interest rates and/or commercial banks started to tighten lending criteria and reduced their willingness to lend, it is highly likely that a new cycle of rapidly declining production and a round of stock liquidation will occur.

The article has established that forecasting future demand and matching production accordingly is especially problematic for an industry that has such a long product cycle. This transcends an ability to forecast through the normal vagaries of the economic and business cycle, albeit on a global basis. From an industrial organization perspective this raises interesting pointers for future research to illuminate fully the optimal way to manage the stock cycle. Prior to 1925, the industry displayed higher specialization, with highly consolidated ownership and control of grain distillation capacity, disparate ownership of malt whisky distillation, and with a small number of dedicated blenders and brand owners. Although the collaborative agreements characterized by the production and price-fixing between DCL and NB, described above, would likely fall foul of current anti-trust legislation, it is tempting to speculate that greater horizontal integration might be possible in lieu of a separation of vertically-integrated assets. The ‘merger wave’ from the mid-1990s to mid-2000s, has been motivated by the rationalization of the international distribution networks and spirits brand portfolios of the former Allied Domecq, Grand Metropolitan, Guinness and J Seagram operations into two global leaders, Diageo and Pernod Ricard. These two firms, both formed under the auspices of internationally coordinated merger policy, are vertically-integrated, marketing-led firms. They own the distilleries, marketing networks and the brands.

However, industrial architecture is not set in stone; alternative arrangements can, and do, emerge as a function of technological, regulatory or other institutional change. An alternative organizational structure is seen in Champagne, an industry with a similarly protected status in terms of production and geography. French law has made it difficult for Champagne brand owners to acquire their own vineyards and become vertically-integrated. The small and numerous growers retain the option of working as part of an industry cooperative that also produces its own competing (with the well-known Champagne houses) brands [

36]. Although Scotch whisky’s integration wrests at the marketing and production of brands, as opposed to the retail sellers of those products, it is of interest that similar disaggregation of the supply chain, followed by consolidation and rationalization at either end, has occurred in the brewing industry under the auspices of anti-trust policy [

37,

38]. Whether this is possible, or indeed desirable is worthy of additional inquiry.

Secondly, the role of a marketing, as opposed to production focus in the industry is an important feature of the post-1980s era of brand-based consolidation. The industry might well have been hopeful that a new phase of leadership had emerged in the 1990s when Guinness, as the owner of DCL, established Bell’s as an eight-year-old blend. Yet Diageo’s more recent decision to reverse course on Bell’s, following shortly after its decision to alter the formulation of Cardhu to support volume sales, rather than increase its price, raises as many questions about the nature of industry leadership as the possible fragmentation of the industry into more discrete strategic groups, as an entirely new category (that of ‘pure malt’) has emerged.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}