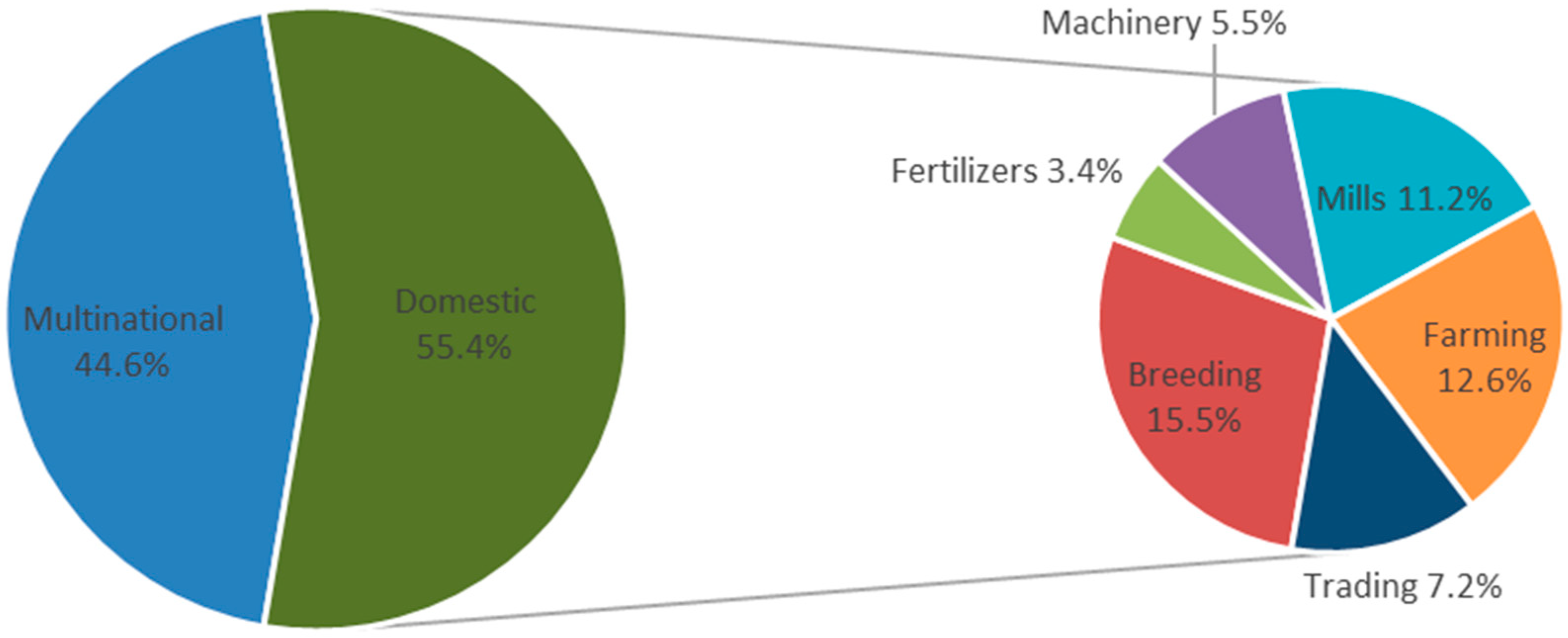

3.1. Plant Breeding

Sugarcane plant breeding in Brazil is, to a large extent, done by domestic companies that count on support from public agencies for research and development (R&D). Sugarcane varieties developed by the Interuniversity Network for the Development of the Sugar-Energy Sector (Ridesa), named with the acronym RB, are cultivated in more than 65% of the sugarcane area in Brazil [

22]. The other leading varieties are CTC (with 14% of the planted area), SP (with 13% of the planted area), IAC (with 2% of the planted area), CV (with 2% of the planted area) and others (with 4% of the planted area) (

Table 2). Ridesa has 10 universities, 79 research bases and different selection areas, the latter conducted in partnership with private companies that pay royalties to adopt the innovation developed by Ridesa. As the royalty paid to Ridesa is often lower than the amount paid to private plant breeders, Ridesa varieties tend to hold the largest share of the market.

The Sugarcane Technology Center (breeder of the CTC varieties) was created in 1969 by the group of Copersucar mills with a focus on conventional plant breeding and, recently, directed investments towards sugarcane transgenics. Since 2017, the company has already launched two transgenic varieties resistant to the sugarcane borer. The second wave of transgenics foresees the release of a weevil-resistant variety. The company expects to reach the end of the 2022/23 harvest with 50,000 hectares planted with transgenic sugarcane, out of a total of 8.13 million hectares planted with sugarcane across Brazil. Among CTC’s main shareholders are Copersucar, with 26% of the business, Raízen (a joint venture between Cosan and Shell), with a 20% share, and the equity branch of the National Bank for Economic and Social Development (BNDESPar), with 18.9%.

The only CTC competitor in the transgenic segment in Brazil is CanaVialis (breeder of the CV varieties). CanaVialis was created in 2003 by Brazilian scientists who took part in the sequencing of the sugarcane genome and had the Votorantim group as its main investor. The business caught the attention of Monsanto, which bought the company in 2008. Seven years later, the multinational decided to leave the sugarcane sector and ended the company’s activities in Brazil. As the CV varieties had a patent in the National Registry of Seeds and Seedlings (Renasen), Bayer (current owner of Monsanto) continues to receive royalties for the use of its varieties. Varieties of Brazilian groups still include SP from Copersucar and IAC developed by Instituto Agronomia de Campinas. An important Brazilian group that is no longer operational is Vignis, which developed VG varieties. Created in 2010, Vignis conducted the largest Cana Energia genetic improvement program in the world. In 2018, the Vignis Group had its request for judicial recovery accepted and left the market.

3.2. Fertilizers

Two types of companies operate in the fertilizer segment: those that produce raw materials and intermediate products (or simple fertilizers) and those that manufacture formulated fertilizers. Most of the raw material for fertilizers used in Brazil is imported by multinational companies. In the case of macronutrient phosphorus, potassium and nitrogen, respectively 44%, 95% and 75% of the total amount consumed in the country are imported [

13]. In Brazil, it is common for part of the fertilization of sugarcane plantations to be done with by-products from the sugarcane plants, such as vinasse and filter cake, which reduces the cost of fertilizers.

Fertilizer manufacturing in Brazil has strong participation of the multinational Yara, with national groups holding 29.8% of the market in 2021 (

Table 3). In 2018, the Canadian company Nutrien was created from the merger between Agrium and Potash and already appears to hold 10% of the Brazilian market. Following the example of multinationals in the agricultural trade, such as Archer Daniels Midland, Bunge, and Cargill, Louis Dreyfus reduced its investments in fertilizers due to poor growth prospects. At the same time, major players in the fertilizer industry (such as Yara) are buying up their competitors.

The Fertipar Group and Heringer are the Brazilian companies with the greatest participation in the manufacture of fertilizers in Brazil. The two companies produce basic fertilizers, NPK formulations and speciality fertilizers. Facing financial hardship for some years, Heringer (a publicly traded company with 56% domestic capital) filed for receivership in 2019 and lost an important part of the market with the closure of part of its factories. The rest of the Brazilian fertilizer market is served by regional domestic companies, such as Adubos Araguaia and Fertilizantes Tocantins.

3.3. Machinery

The segment of agricultural machinery used for sugarcane production mainly includes planters and seeders, sprayers, harvesters and transfers. In the case of planters and seeders, there is an important participation of Brazilian groups, with emphasis on the companies DMB Máquinas e Implementos Agrícolas Ltd., TMA Máquinas (from the Tracan Group) and Sollus Agrícola. Among multinationals, American John Deere has the largest market share. Mechanical planting represents about 52% of the planted area in the traditional sugarcane area in São Paulo and Paraná, compared to 48% of manual planting, mainly due to technical problems with the machines that still need to be solved by the industry as a way to optimize the distribution of stalks, reducing planting failures.

The market for sprayers and other implements is led by the Brazilian Jacto. The French Berthoud and the multinational giants Valtra, Case and John Deere still operate in the sprayer market. In the manufacture of other agricultural implements, the Brazilian companies Civemasa also stand out in the manufacture of a wide range of implements and Teston in the manufacture of transfers.

In the case of harvesters, the market is completely controlled by the three giant multinationals in the sector (

Table 4). CNH leads domestic sales of sugarcane harvesters with 348 units sold in Brazil in 2021, closely followed by John Deere with 290 units. AGCO traditionally has a smaller share of this market, having sold seven sugarcane harvesters in 2021 [

24]. Santal Equipamentos S.A. was one of the Brazilian pioneers in the mechanization of sugarcane harvesting but was sold to the transnational AGCO in 2012. In 2020, the Brazilian Jacto launched the Hover 500 cane harvester, but sales data are not yet available.

In addition to agricultural machinery, there is the industrial equipment segment. The base industry has generalist equipment for sugarcane milling and specific equipment for the production of sugar, ethanol and energy. The main industrial equipment common to all processes is the mill or diffuser. Through mills or diffusers, the raw material responsible for the production of sugar, ethanol and bioenergy is removed from sugarcane.

Brazilian groups hold the largest share of the basic equipment market for the sugar-energy industry. However, Brazilian companies operating in this segment generally establish partnerships or joint ventures with multinational groups for the development or importation of technologies. For example, Dedini S/A Indústrias de Base is a company with a family structure and Brazilian capital that supplies equipment from the reception, preparation, extraction and treatment of the broth to the production of sugar and ethanol. With financial difficulties since the end of 2008, in 2019 Dedini signed a technology agreement with the Indian PRAJ Industries that will manage technology licensing and supply key equipment. Zanini Renk was born as a joint venture between the companies Zanini and Renk AG, from Germany. Since 1983, Renk AG has maintained a technology transfer contract with Zanini Renk, ensuring the same technological conception developed in the gearboxes designed in Germany. The Brazilian company Sermasa Equipamentos Industriais Ltd.a. started its activities in 2006 and established important partnerships with multinational companies that own technologies and also supply complementary components of the systems, enabling it to manufacture and assemble complete plants for the sugar and ethanol sector. Founded in 1989, the Brazilian RG Sertal stands out among suppliers of services and products for the sugar and ethanol industry.

3.4. Sugarcane Processing (Industrial Plants/Mills)

Brazil has 234 plants that produce both ethanol and sugar and 178 distilleries that produce ethanol, summing up to 412 agro-industrial units (mills). In addition to ethanol and sugar, all industries in the sugar-energy sector produce energy and around 30% of the agro-industrial units also co-generate energy from sugarcane bagasse, selling the surplus electricity produced. The industries of the Center-South region concentrate more than 90% of the national production of 642.7 million tons processed annually [

18].

The Copersucar S/A group processed 85 million tons of sugarcane in 2019, the highest volume in the country. The Company has exclusivity in the sale of sugar and ethanol produced by 34 partner mills belonging to 20 different economic groups (

Table 5). The group’s largest producer is Zilor, which processes 10.6 million tons of sugarcane annually, followed by Viracool with 10 million tons per year. Copersucar and its partner mills are autonomous companies and conduct their corporate policies independently.

The second largest sugar mill group in the country is Raízen, a 50:50 joint venture between Cosan S/A and Royal Dutch Shell. The partnership provides for the production of ethanol by Cosan’s plants and distribution at Shell service stations. Raízen annually processes 73 million tons of sugarcane and, considered individually, is the largest segment company operating in Brazil [

28]. Although known for producing ethanol, Raízen is also a major sugar producer. In 2019, the joint venture acquired NovAmérica’s agricultural operations at the Caarapó (MS) unit, expanding its production capacity.

Among essentially Brazilian companies, the São Martinho Group leads the ranking of sugarcane processing and profitability in the activity. The São Martinho Group led the ranking Value in net income with a positive R

$ 288.3 million in the 2014 fiscal year. In second place came Usina Colombo and, in third place, was the Santa Terezinha Participações Group. Usina Ipiranga ranked fourth. Following, they complete the list of 10 sugar-energy groups with positive net profit: Usina da Pedra; Batatais plant; Balbo Group; Adecoagro Brazil; Usina São João and the Zilor Group [

29].

Characteristically, in addition to public credits, the largest Brazilian groups constituted as S/A go public and raise funds for investments either via debentures or the sale of shares. As an example, Ipiranga Agroindustrial S/A raised BRL 200 million in 2019 with debentures. Therefore, it is likely that many of these companies have creditors in other countries, although they remain companies with the national capital.

However, the segment has also attracted multinational groups. Bunge, which already operated in the market with plants and distilleries, 2019 set up a 50:50 joint venture with BP British Petroleum that resulted in the creation of BP Bunge Bioenergia. The joint venture has a total of 11 mills with 32 million tonnes of combined crushing capacity per year. In addition to sugar and ethanol, the company also co-generates electricity.

The Atvos Agroindustrial group, which grinds 27 million tons per year, is changing from Brazilian controllers to US ones. The American fund Lone Star may be the new controller of Atvos Agroindustrial, the sugar and ethanol company of the Odebrecht group that filed for bankruptcy in 2019.

Tereos Açúcar & Energia Brasil, one of the leaders in the Brazilian sugar-energy sector, processed 18.8 million tons of sugarcane in its seven units during the 2019/2020 harvest, an increase of 7.5% compared to the previous harvest. Tereos Brasil is part of the Tereos Internacional Group, a global company of French origin that transforms sugarcane, cereals and tubers into sugar, starch, ethanol and alcohol. The plants of the Tereos Brasil group are Andrade, Cruz Alta, São José, Severínia, Mandu, Tanabi and Usina Vertente (in the latter with 50% control in partnership with the Humus Group).

Among the multinationals, the Indian group Shree Renuka Sugars Ltd. completed 2010 the acquisition of 59.4% of Equipav Açúcar e Álcool, creating Renuka do Brasil S/A with the capacity to process 10.5 million tons/year of sugarcane. Also in 2010, the Indian group acquired 100% of Renuka Vale do Ivaí with the capacity to process 3.1 million tons/per year. As a result, the Indian multinational now can process 13.6 million tons per year. Another multinational in the segment is Glencore which, through Glencane, can process 4.9 million tons annually. In 2018, Cargill acquired 100% control of Cevasa, a sugar and ethanol unit with a capacity to grind 2.3 million tons per year that it had in partnership with Canagril, although it intends to invest more in the production of ethanol from corn, with SJC Bioenergy. In 2016, Archer-Daniels-Midland (ADM) sold the Cabreira Energética plant, its sole sugar-energy operation in Brazil. The unit came to be controlled by Companhia Mineira de Açúcar e Álcool. The plant has a crushing capacity of 1.5 million tons of sugarcane per harvest, in addition to being able to produce up to 1.2 million litres of ethanol daily.

3.6. Trading

Ethanol and sugar trading groups were created to increase the bargaining power of producers vis-à-vis distributors [

31]. The main Brazilian trading groups are Coopersucar, Bioagência, CPA and SCA (

Table 7).

Copersucar markets ethanol directly or through Eco-Energy for the case of the the United States market (Copersucar controls 100% of Eco-Energy). Sugar is sold through Alvean, a 50:50 joint venture formed by Copersucar and Cargill. In addition to marketing the production of its partner plants on an exclusive basis, Copersucar markets the sugar and ethanol production of approximately 50 non-partner production units on a non-exclusive basis. In total, Copersucar S.A. trades 2.4 million tons of sugar and 4.8 billion litres of ethanol per year.

The leader in the ethanol segment is the multinational Raízen, with 16.5 billion litres sold annually. The Brazilian sugar market is controlled by four large groups (Biosev, Alvean, Wilmar and Sucden) which together hold around 75% of the traded volume. For the first time in recent years, in 2019, Biosev (controlled by Louis Dreyfus) took the market lead followed by Alvean, Wilmar and Sucden. In addition to trading sugar, Louis Dreyfus controls production at the Santa Elisa, Jardest, Vale do Rosário, Morro Agudo and Continental mills. Singapore-based agribusiness giant Wilmar International increased its stake in 2018 by acquiring sugar trading operations in Brazil from Bunge.

{kind=link}

{kind=link}