Does Strategic Corporate Social Responsibility Drive Better Organizational Performance through Integration with a Public Sector Scorecard? Empirical Evidence in a Developing Country

Abstract

1. Introduction

2. Overview of Prior Research

2.1. The Association between Corporate Social Responsibility and Management

2.2. The Linkage between Corporate Social Responsibility and Organizational Performance

2.3. The Relationship between Corporate Social Responsibility Disclosure and Organizational Performance

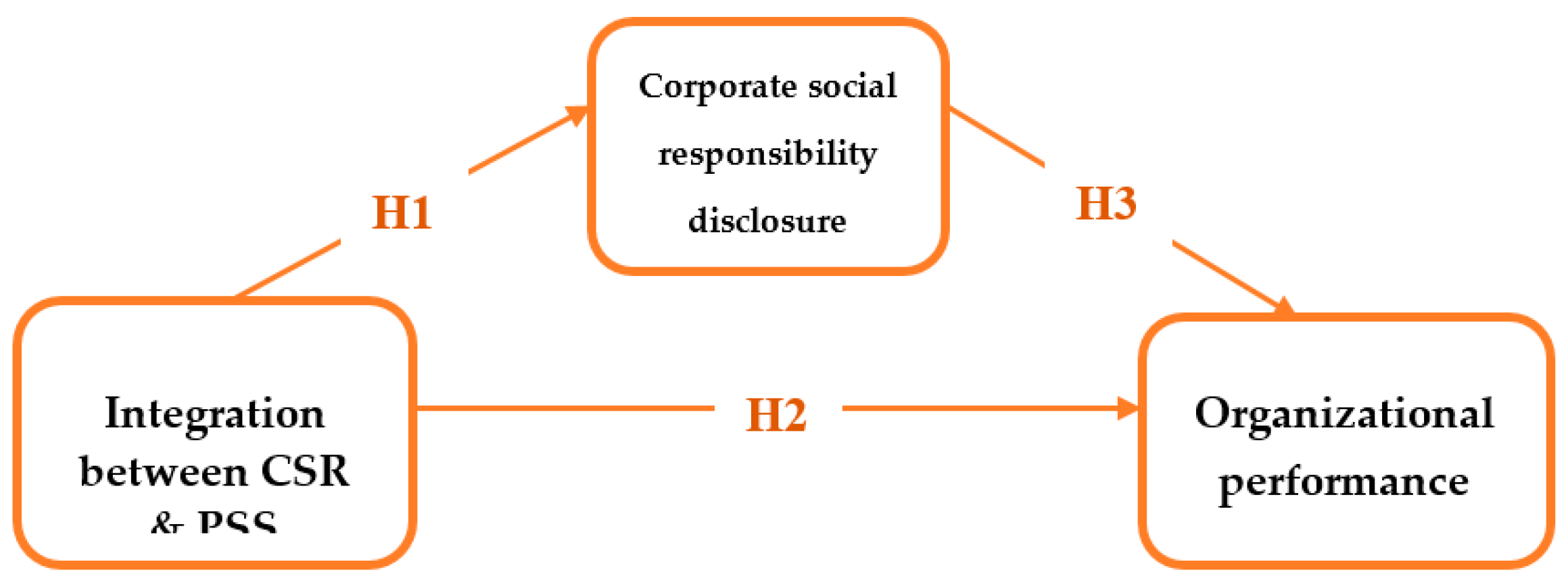

3. Theoretical Background and Hypothesis Development

3.1. Theoretical Background

3.1.1. Legitimacy Theory

3.1.2. Resource-Based Theory

3.1.3. Corporate Social Responsibility and CSR Disclosure

3.1.4. Public Sector Scorecard

3.1.5. Organizational Performance

3.2. Hypothesis Development

4. Methodology Design

4.1. Procedure and Item Generation

4.2. Data Analysis

4.3. Measures and the Questionnaire

4.3.1. The Integration between Corporate Social Responsibility and Public Sector Scorecard

4.3.2. Corporate Social Responsibility Disclosure

4.3.3. Organizational Performance

5. Result Analysis and Discussion

5.1. Demographic Characteristics

5.2. Assessment of Convergent Validity

5.3. Assessment of Discriminant Validity

5.4. Assessment of Overall Model Fit

5.5. Hypothesis Verification

5.5.1. Direct Effect

5.5.2. Indirect Effect

6. Concluding Remarks

6.1. Discussion and Implication

6.2. Limitations and Further Research

Author Contributions

Funding

Conflicts of Interest

References

- Saeed, M.M.; Arshad, F. Corporate social responsibility as a source of competitive advantage: The mediating role of social capital and reputational capital. J. Database Mark. Cust. Strat. Manag. 2012, 19, 219–232. [Google Scholar] [CrossRef]

- Mullerat, R. International Corporate Social Responsibility: The Role of Corporations in the Economic Order of the 21st Century; Wolters Kluwer: Alphen aan den Rijn, The Netherlands, 2010. [Google Scholar]

- Perry, P.; Towers, N. Conceptual framework development. Int. J. Phys. Distrib. Logist. Manag. 2013, 43, 478–501. [Google Scholar] [CrossRef]

- Khan, S.N. Making sense of the black box: An empirical analysis investigating strategic cognition of CSR strategists in a transitional market. J. Clean. Prod. 2018, 196, 916–926. [Google Scholar] [CrossRef]

- Wahba, H.; Elsayed, K. The mediating effect of financial performance on the relationship between social responsibility and ownership structure. Futur. Bus. J. 2015, 1, 1–12. [Google Scholar] [CrossRef]

- Visser, W.; Matten, D.; Polh, M.; Tolhurst, N. The A to Z of corporate social responsibility: A Complete Reference Guide to Concepts, Codes and Organisations; John Wiley & Sons Ltd: West Sussex, UK, 2007. [Google Scholar]

- Visser, W. Corporate Social Responsibility in Developing Countries. In Corporate Social Responsibility in Developing Countries; Oxford University Press (OUP): Oxford, UK, 2009; pp. 473–479. [Google Scholar]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of Corporate Social Responsibility (CSR) Disclosure in Developed and Developing Countries: A Literature Review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- De Oliveira, J.A.P. Introduction: Corporate Citizenship in Latin America. J. Corp. Citizsh. 2006, 2006, 17–20. [Google Scholar] [CrossRef]

- Moon, J. Corporate Social Responsibility: A Very Short Introduction; Oxford University Press (OUP): Oxford, UK, 2014. [Google Scholar]

- Moullin, M. Improving and evaluating performance with the Public Sector Scorecard. Int. J. Prod. Perform. Manag. 2017, 66, 442–458. [Google Scholar] [CrossRef]

- Wang, Z.; Sarkis, J. Corporate social responsibility governance, outcomes, and financial performance. J. Clean. Prod. 2017, 162, 1607–1616. [Google Scholar] [CrossRef]

- Tilt, C. The Influence of External Pressure Groups on Corporate Social Disclosure. Account. Audit. Account. J. 1994, 7, 47–72. [Google Scholar] [CrossRef]

- Van Thanh, P.; Podruzsik, S. CSR in Developing Countries: Case Study in Vietnam. Management 2018, 13, 287–300. [Google Scholar] [CrossRef]

- Cook, L.; LaVan, H.; Žilić, I. An exploratory analysis of corporate social responsibility reporting in US pharmaceutical companies. J. Commun. Manag. 2018, 22, 197–211. [Google Scholar] [CrossRef]

- Adnan, S.M.; Hay, D.; Van Staden, C. The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. J. Clean. Prod. 2018, 198, 820–832. [Google Scholar] [CrossRef]

- Hu, W.; Ge, Y.; Dang, Q.; Huang, Y.; Hu, Y.; Ye, S.; Wang, S. Analysis of the Development Level of Geo-Economic Relations between China and Countries along the Belt and Road. Sustainability 2020, 12, 816. [Google Scholar] [CrossRef]

- Huang, X.; Watson, L. Corporate social responsibility research in accounting. J. Account. Lit. 2015, 34, 1–16. [Google Scholar] [CrossRef]

- Henri, J.-F.; Journeault, M. Eco-control: The influence of management control systems on environmental and economic performance. Account. Organ. Soc. 2010, 35, 63–80. [Google Scholar] [CrossRef]

- Gond, J.-P.; Grubnic, S.; Herzig, C.; Moon, J. Configuring management control systems: Theorizing the integration of strategy and sustainability. Manag. Account. Res. 2012, 23, 205–223. [Google Scholar] [CrossRef]

- Arjaliès, D.-L.; Mundy, J. The use of management control systems to manage CSR strategy: A levers of control perspective. Manag. Account. Res. 2013, 24, 284–300. [Google Scholar] [CrossRef]

- Sila, I.; Cek, K. The Impact of Environmental, Social and Governance Dimensions of Corporate Social Responsibility on Economic Performance: Australian Evidence. Procedia Comput. Sci. 2017, 120, 797–804. [Google Scholar] [CrossRef]

- Carroll, A.B.; Buchholtz, A.K. Business & Society: Ethics and Stakeholder Management, 5th ed.; Thomson Learning: Mason, OH, USA, 2003. [Google Scholar]

- Coldwell, D.A. Perceptions and expectations of corporate social responsibility: Theoretical issues and empirical findings. S. Afr. J. Bus. Manag. 2001, 32, 49–55. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Mishra, S.; Suar, D. Does Corporate Social Responsibility Influence Firm Performance of Indian Companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Crisóstomo, V.L.; Freire, F.D.S.; De Vasconcellos, F.C. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The Corporate Social-Financial Performance Relationship. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Gatsi, J.G.; Anipa, C.A.A.; Gadzo, S.G.; Ameyibor, J. Corporate social responsibility, risk factor and financial performance of listed firms in Ghana. J. Appl. Financ. Bank. 2016, 6, 21–38. [Google Scholar]

- Abdelmotaleb, M.; Saha, S.K. Corporate Social Responsibility, Public Service Motivation and Organizational Citizenship Behavior in the Public Sector. Int. J. Public Adm. 2018, 42, 929–939. [Google Scholar] [CrossRef]

- Clarkson, P.; Overell, M.B.; Chapple, L. Environmental Reporting and its Relation to Corporate Environmental Performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Dabor, A.O.; Kaka, M.; Idogen, K. Corporate Social Responsibility and Financial Performance: A Two Least Regression Approach. Int. J. Soc. Sci. Educ. Stud. 2017, 4, 44–54. [Google Scholar] [CrossRef]

- Ahmed, M.N.; Zakaree, S.; Kolawole, O.O. Corporate Social Responsibility Disclosure and Financial Performance of Listed Manufacturing Firms in Nigeria. Res. J. Financ. Account. 2016, 7, 47–58. [Google Scholar]

- Bayoud, N.S.M.; Kavanagh, M.; Slaughter, G. An Empirical Study of the Relationship between Corporate Social Responsibility Disclosure and Organizational Performance: Evidence from Libya. Int. J. Manag. Mark. Res. 2012, 5, 69–82. [Google Scholar]

- Gallardo-Vázquez, D.; Méndez, M.J.B.; Pajuelo-Moreno, M.-L.; Sánchez-Meca, J. Corporate Social Responsibility Disclosure and Performance: A Meta-Analytic Approach. Sustainability 2019, 11, 1115. [Google Scholar] [CrossRef]

- Yahya, H.Y.; Ghodratollah, B. The effect of disclosure level of CSR on corporate financial performance in Tehran stock exchange. Int. J. Account. Res. 2014, 1, 43–51. [Google Scholar]

- Mittal, R.; Sinha, N.; Singh, A. An analysis of linkage between economic value added and corporate social responsibility. Manag. Decis. 2008, 46, 1437–1443. [Google Scholar] [CrossRef]

- Kimbro, M.B.; Melendy, S.R. Financial performance and voluntary environmental disclosures during the Asian Financial Crisis: The case of Hong Kong. Int. J. Bus. Perform. Manag. 2010, 12, 72. [Google Scholar] [CrossRef]

- Gray, R.; Javad, M.; Power, D.; Sinclair, C.D. Social and Environmental Disclosure and Corporate Characteristics: A Research Note and Extension. J. Bus. Financ. Account. 2001, 28, 327–356. [Google Scholar] [CrossRef]

- Castelló, I.; Lozano, J.M. Searching for New Forms of Legitimacy Through Corporate Responsibility Rhetoric. J. Bus. Ethics 2011, 100, 11–29. [Google Scholar] [CrossRef]

- Lim, S.; Wilmshurst, T.; Shimeld, S. Blowing in the Wind: Legitimacy Theory: An Environmental Incident and Disclosure; Research paper; University of Tasmania: Hobart, Australia, 2009. [Google Scholar]

- Deegan, C. Introduction. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Deegan, C.; Unerman, J. Finanical Accounting Theory; McGraw-Hill: Sydney, Australia, 2011. [Google Scholar]

- O’Donovan, G. Environmental disclosures in the annual report. Account. Audit. Account. J. 2002, 15, 344–371. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate Social Responsibility in Europe and the U.S.: Insights from Businesses’ Self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Adams, C.; Hill, W.-Y.; Roberts, C.B. Corporate Social Reporting Practices in Western Europe: Legitimating Corporate Behaviour. Br. Account. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Merkelsen, H. The double-edged sword of legitimacy in public relations. J. Commun. Manag. 2011, 15, 125–143. [Google Scholar] [CrossRef]

- Moir, L. What do we mean by corporate social responsibility? Corp. Gov. 2001, 1, 16–22. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Omran, M.; Ramdhony, D. Theoretical Perspectives on Corporate Social Responsibility Disclosure: A Critical Review. Int. J. Account. Financ. Rep. 2015, 5, 38. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268. [Google Scholar] [CrossRef]

- Kytle, B.; Hamilton, B.A.; Ruggie, J.G. Corporate Social Responsibility as Risk Management: A Model for Multinationals; Social Responsibility Initiative Working Paper: Cambridge, MA, USA, 2005. [Google Scholar]

- Oliver, C. Sustainable competitive advantage: Combining institutional and resource-based views. Strateg. Manag. J. 1997, 18, 697–713. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Gomez-Mejia, L.R.; Balkin, D.B. Management; McGraw-Hill: New York, NY, USA, 2002. [Google Scholar]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Surroca, J.; Tribo, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2009, 31, 463–490. [Google Scholar] [CrossRef]

- Orlitzky, M.; Siegel, D.S.; Waldman, D.A. Strategic Corporate Social Responsibility and Environmental Sustainability. Bus. Soc. 2011, 50, 6–27. [Google Scholar] [CrossRef]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation building and corporate strategy. Acad. Manag. J. 1990, 33, 233–258. [Google Scholar] [CrossRef]

- Priem, R.L.; Butler, J.E. Tautology in the Resource-Based View and the Implications of Externally Determined Resource Value: Further Comments. Acad. Manag. Rev. 2001, 26, 57–66. [Google Scholar] [CrossRef]

- European Commission. Promoting a European Framework for Corporate Social Responsibility; Office for Official Publications of the European Communities: Luxembourg, 2011. [Google Scholar]

- Lii, Y.-S.; Lee, M. Doing Right Leads to Doing Well: When the Type of CSR and Reputation Interact to Affect Consumer Evaluations of the Firm. J. Bus. Ethics 2011, 105, 69–81. [Google Scholar] [CrossRef]

- Aguinis, H. Organizational responsibility: Doing good and doing well. In Handbook of Industrial and Organizational Psychology 3; Zedeck, S., Ed.; APA, American Psychological Association: Washington, DC, USA, 2011; pp. 855–879. [Google Scholar]

- Kim, E.E.K.; Kang, J.; Mattila, A.S. The impact of prevention versus promotion hope on CSR activities. Int. J. Hosp. Manag. 2012, 31, 43–51. [Google Scholar] [CrossRef]

- Wang, J.; Zhang, Y.; Goh, M. Moderating the Role of Firm Size in Sustainable Performance Improvement through Sustainable Supply Chain Management. Sustainability 2018, 10, 1654. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Said, R.; Zainuddin, Y.H.; Haron, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef]

- Moullin, M. Using the Public Sector Scorecard to measure and improve healthcare services. Nurs. Manag. 2009, 16, 26–31. [Google Scholar] [CrossRef]

- Pidd, M. Measuring the Performance of Public Services; Cambridge University Press (CUP): Cambridge, UK, 2012. [Google Scholar]

- McAdam, R.; Casey, C.; Hazlett, S.-A. Performance management in the UK public sector. Int. J. Public Sect. Manag. 2005, 18, 256–273. [Google Scholar] [CrossRef]

- Johnston, R.; Pongatichat, P. Managing the tension between performance measurement and strategy: Coping strategies. Int. J. Oper. Prod. Manag. 2008, 28, 941–967. [Google Scholar] [CrossRef]

- Al-Samman, E.; Al-Nashmi, M.M. Effect of corporate social responsibility on nonfinancial organizational performance: Evidence from Yemeni for-profit public and private enterprises. Soc. Responsib. J. 2016, 12, 247–262. [Google Scholar] [CrossRef]

- Talbot, C. Theories of Performance: Organizational and Service Improvement in the Public Domain; Oxford University Press: New York, NY, USA, 2010. [Google Scholar]

- Venkatraman, N.; Ramanujam, V. Measurement of Business Economic Performance: An Examination of Method Convergence. J. Manag. 1987, 13, 109–122. [Google Scholar] [CrossRef]

- Hancott, D.E. The Relationship between Transformational Leadership and Organizational Performance in the Largest Public Companies in Canada. Ph.D. Thesis, ProQuest database, UMI No. 3159704. Morrisville, NC, USA, 2005. [Google Scholar]

- Akanbi, P.A.; Ofoegbu, O.E. Impact of corporate social responsibility on bank performance in Nigeria. J. US China Public Adm. 2012, 9, 374–383. [Google Scholar]

- E Porter, M.; Van Der Linde, C. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Matousek, R.; Meyer, M.; Tzeremes, N.G. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental & social governance implementation and innovation performance. J. Bus. Res. 2019. [Google Scholar] [CrossRef]

- Zhu, Q.; Lowe, E.A.; Wei, Y.-A.; Barnes, D. Industrial Symbiosis in China: A Case Study of the Guitang Group. J. Ind. Ecol. 2008, 11, 31–42. [Google Scholar] [CrossRef]

- Rojas, R.R. A Review of Models for Measuring Organizational Effectiveness Among For-Profit and Nonprofit Organizations. Nonprofit Manag. Leadersh. 2000, 11, 97–104. [Google Scholar] [CrossRef]

- Osborne, S.P.; Radnor, Z.; Nasi, G. A New Theory for Public Service Management? Toward a (Public) Service-Dominant Approach. Am. Rev. Public Adm. 2012, 43, 135–158. [Google Scholar] [CrossRef]

- Maignan, I.; Ferrell, O.; Ferrell, L. A stakeholder model for implementing social responsibility in marketing. Eur. J. Mark. 2005, 39, 956–977. [Google Scholar] [CrossRef]

- Costa, C.; Lages, L.F.; Hortinha, P. The bright and dark side of CSR in export markets: Its impact on innovation and performance. Int. Bus. Rev. 2015, 24, 749–757. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Moullin, M. The design of an alternative balanced scorecard framework for public and voluntary organizations. Perspect. Perform. 2006, 5, 10–12. [Google Scholar]

- Goergen, M.; Chahine, S.; Wood, G.; Brewster, C. The relationship between public listing, context, multi-nationality and internal CSR. J. Corp. Financ. 2019, 57, 122–141. [Google Scholar] [CrossRef]

- Stahl, G.K.; Brewster, C.; Collings, D.; Hajro, A. Enhancing the role of human resource management in corporate sustainability and social responsibility: A multi-stakeholder, multidimensional approach to HRM. Hum. Resour. Manag. Rev. 2019, 100708, 100708. [Google Scholar] [CrossRef]

- Liu, X.; Zhang, C. Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 2017, 142, 1075–1084. [Google Scholar] [CrossRef]

- Forker, J.J. Corporate Governance and Disclosure Quality. Account. Bus. Res. 1992, 22, 111–124. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L. Corporate Social Responsibility and Resource-Based Perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- McGahan, A.M.; Porter, M.E. HOW MUCH DOES INDUSTRY MATTER, REALLY? Strateg. Manag. J. 1997, 18, 15–30. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. Are firms with different CSR profiles equally innovative? Empirical analysis with survey data. Eur. Manag. J. 2013, 31, 642–654. [Google Scholar] [CrossRef]

- Aras, G.; Aybars, A.; Kutlu, O.; Aybars, A. Managing corporate performance. Int. J. Prod. Perform. Manag. 2010, 59, 229–254. [Google Scholar] [CrossRef]

- Hillman, A.; Keim, G. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Oeyono, J.; Samy, M.; Bampton, R. An examination of corporate social responsibility and financial performance. J. Glob. Responsib. 2011, 2, 100–112. [Google Scholar] [CrossRef]

- Gorski, H. Leadership and Corporate Social Responsibility. In Proceedings of the International Conference Knowledge Based Organization, Warsaw, Poland, 12 June 2017; Volume 23, pp. 372–377. [Google Scholar] [CrossRef]

- Asrar-Ul-Haq, M.; Kuchinke, K.P.; Iqbal, A. The relationship between corporate social responsibility, job satisfaction, and organizational commitment: Case of Pakistani higher education. J. Clean. Prod. 2017, 142, 2352–2363. [Google Scholar] [CrossRef]

- Suganthi, L. Examining the relationship between corporate social responsibility, performance, employees’ pro-environmental behavior at work with green practices as mediator. J. Clean. Prod. 2019, 232, 739–750. [Google Scholar] [CrossRef]

- Lindgreen, A.; Swaen, V.; Johnston, W. The Supporting Function of Marketing in Corporate Social Responsibility. Corp. Reput. Rev. 2009, 12, 120–139. [Google Scholar] [CrossRef]

- Humphrey, J.; Lee, D.D.; Shen, Y. The independent effects of environmental, social and governance initiatives on the performance of UK firms. Aust. J. Manag. 2012, 37, 135–151. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C.B. Corporate Social Responsibility, Customer Satisfaction, and Market Value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Vurro, C.; Perrini, F. Making the most of corporate social responsibility reporting: Disclosure structure and its impact on performance. Corp. Gov. Int. J. Bus. Soc. 2011, 11, 459–474. [Google Scholar] [CrossRef]

- Waddock, S.; Bodwell, C. Managing Responsibility: What Can Be Learned from the Quality Movement? Calif. Manag. Rev. 2004, 47, 25–37. [Google Scholar] [CrossRef]

- Yusoff, H.; Mohamad, S.S.; Darus, F. The Influence of CSR Disclosure Structure on Corporate Financial Performance: Evidence from Stakeholders’ Perspectives. Procedia Econ. Financ. 2013, 7, 213–220. [Google Scholar] [CrossRef]

- Choongo, P. A Longitudinal Study of the Impact of Corporate Social Responsibility on Firm Performance in SMEs in Zambia. Sustainability 2017, 9, 1300. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Bernard, H.R. Social Research Methods: Qualitative and Quantitative Approaches; Sage: Thousand Oaks, CA, USA, 2000. [Google Scholar]

- Dunn, T.J.; Baguley, T.; Brunsden, V.; Baguley, T. From alpha to omega: A practical solution to the pervasive problem of internal consistency estimation. Br. J. Psychol. 2013, 105, 399–412. [Google Scholar] [CrossRef] [PubMed]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a Silver Bullet. J. Mark. Theory Pr. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis with Readings, 7th ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 2010. [Google Scholar]

- Hinkin, T.R. A review of scale development practices in the study of organizations. J. Manag. 1995, 21, 967–988. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Tatham, R.L.; Black, W.C. Multivariate Data Analysis; Prentice Hall: London, UK, 1998. [Google Scholar]

- Vinodh, S.; Joy, D. Structural Equation Modelling of lean manufacturing practices. Int. J. Prod. Res. 2012, 50, 1598–1607. [Google Scholar] [CrossRef]

- Moon, J.-W.; Kim, Y.-G. Extending the TAM for a World-Wide-Web context. Inf. Manag. 2001, 38, 217–230. [Google Scholar] [CrossRef]

- Petkoski, D.; Nigel, T. (Eds.) Public Policy for Corporate Social Responsibility. WBI Series on Corporate Responsibility, July 7–25 2003; World Bank Institute: Washington, DC, USA, 2003. [Google Scholar]

- Mansi, M.; Pandey, R.; Ghauri, E. CSR focus in the mission and vision statements of public sector enterprises: Evidence from India. Manag. Audit. J. 2017, 32, 356–377. [Google Scholar] [CrossRef]

- Townsend, W. Innovation and the perception of risk in the public sector. Int. J. Organ. Innov. 2013, 5, 21–34. [Google Scholar]

- Khan, A.R.; Khandaker, S. Public and Private Organizations: How Different or Similar are They. J. Sib. Fed. Univ. Humanit. Soc. Sci. 2016, 9, 2873–2885. [Google Scholar] [CrossRef]

- Niven, P.R. Balanced Scorecard Step-by-Step for Government and Non-Profit Agencies; John Wiley and Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Ellis, J. The Case for an Outcomes Focus; Charities Evaluation Services: London, UK, 2009. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horizons 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Schwartz, M.S.; Carroll, A.B. Corporate Social Responsibility: A Three-Domain Approach. Bus. Ethics Q. 2003, 13, 503–530. [Google Scholar] [CrossRef]

- Rettab, B.; Ben Brik, A.; Mellahi, K. A Study of Management Perceptions of the Impact of Corporate Social Responsibility on Organisational Performance in Emerging Economies: The Case of Dubai. J. Bus. Ethics 2008, 89, 371–390. [Google Scholar] [CrossRef]

- Al-Salem, A.; Speece, M. Women in leadership in Kuwait: A research agenda. Gend. Manag. Int. J. 2017, 32, 141–162. [Google Scholar] [CrossRef]

- Avina, J. The Evolution of Corporate Social Responsibility (CSR) in the Arab Spring. Middle East J. 2013, 67, 76–91. [Google Scholar] [CrossRef]

- Hodges, J. Cracking the walls of leadership: Women in Saudi Arabia. Gend. Manag. Int. J. 2017, 32, 34–46. [Google Scholar] [CrossRef]

- Sidani, Y. Ibn Khaldun of North Africa: An AD 1377 theory of leadership. J. Manag. Hist. 2008, 14, 73–86. [Google Scholar] [CrossRef]

- Asemah, E.; Okpanachi, R.; Olumuji, E. Universities and Corporate Social Responsibility Performance: An Implosion of the Reality. Afr. Res. Rev. 2013, 7, 195. [Google Scholar] [CrossRef]

- Engert, S.; Baumgartner, R.J. Corporate sustainability strategy – bridging the gap between formulation and implementation. J. Clean. Prod. 2016, 113, 822–834. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Manag. Sustain. Bus. 2018, 89, 323–346. [Google Scholar] [CrossRef]

- Heslin, P.A.; Vandewalle, D.; Latham, G.P. Keen to help? Managers’ implicit person theories and their subsequent employee coaching. Pers. Psychol. 2006, 59, 871–902. [Google Scholar] [CrossRef]

- Ehsan, S.; Nazir, M.S.; Nurunnabi, M.; Khan, Q.R.; Tahir, S.; Ahmed, I. A Multimethod Approach to Assess and Measure Corporate Social Responsibility Disclosure and Practices in a Developing Economy. Sustainability 2018, 10, 2955. [Google Scholar] [CrossRef]

- Guthrie, J.; Parker, L.D. Corporate Social Reporting: A Rebuttal of Legitimacy Theory. Account. Bus. Res. 1989, 19, 343–352. [Google Scholar] [CrossRef]

- Hamid, F.Z.; Atan, R. Corporate social responsibility by the Malaysian Telecommunication firms. Int. J. Bus. Soc. Sci. 2011, 2, 1–11. [Google Scholar]

- Wiklund, J.; Shepherd, D. Entrepreneurial orientation and small business performance: A configurational approach. J. Bus. Ventur. 2005, 20, 71–91. [Google Scholar] [CrossRef]

- Helm, S.T.; Andersson, F.O. Beyond taxonomy. Nonprofit Manag. Leadersh. 2010, 20, 259–276. [Google Scholar] [CrossRef]

- Chang, H.-T.; Chi, N.-W. Human resource managers’ role consistency and HR performance indicators: The moderating effect of interpersonal trust in Taiwan. Int. J. Hum. Resour. Manag. 2007, 18, 665–683. [Google Scholar] [CrossRef]

- Calantone, R.J.; Cavusgil, S.T.; Zhao, Y. Learning orientation, firm innovation capability, and firm performance. Ind. Mark. Manag. 2002, 31, 515–524. [Google Scholar] [CrossRef]

- Andersson, L.; Jackson, S.E.; Russell, S.V. Greening organizational behavior: An introduction to the special issue. J. Organ. Behav. 2013, 34, 151–155. [Google Scholar] [CrossRef]

- Junior, F.H.; Gabriel, M.L.D.S.; Gallardo-Vázquez, D.A. Triple bottom line and sustainable performance measurement in industrial companies. Revista de Gestão 2018, 25, 413–429. [Google Scholar] [CrossRef]

- De La Cuesta-González, M.; Rodríguez, D.M.; Fernández-Izquierdo, M. Ángeles Analysis of Social Performance in the Spanish Financial Industry Through Public Data. A Proposal. J. Bus. Ethics 2006, 69, 289–304. [Google Scholar] [CrossRef]

- Cornforth, C. Nonprofit Governance Research: The Need for Innovative Perspectives and Approaches. In Nonprofit Governance, Innovative Perspectives and Approaches; Cornforth, C., Brown, W.A., Eds.; Routledge: Abingdon, UK, 2014; pp. 1–14. [Google Scholar]

- Hambrick, D.C.; Werder, A.V.; Zajac, E.J. New Directions in Corporate Governance Research. Organ. Sci. 2008, 19, 381–385. [Google Scholar] [CrossRef]

- Chan, M.C.; Watson, J.; Woodliff, D. Corporate Governance Quality and CSR Disclosures. J. Bus. Ethics 2013, 125, 59–73. [Google Scholar] [CrossRef]

- Jackson, D.K.; Holland, T.P. Measuring the Effectiveness of Nonprofit Boards. Nonprofit Volunt. Sect. Q. 1998, 27, 159–182. [Google Scholar] [CrossRef]

- Hundleby, J.D.; Nunnally, J. Psychometric Theory. Am. Educ. Res. J. 1968, 5, 431. [Google Scholar] [CrossRef]

- Malhotra, N.K. Marketing Research, 4th ed.; Pearson Education: Singapore, 2002. [Google Scholar]

- Anderson, J.C.; Gerbing, D.W. Structural Equation Modeling in Practice: A Review and Recommended Two-Step Approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Suh, B.; Han, I. Effect of trust on customer acceptance of Internet banking. Electron. Commer. Res. Appl. 2002, 1, 247–263. [Google Scholar] [CrossRef]

- Raykov, T. Estimation of Composite Reliability for Congeneric Measures. Appl. Psychol. Meas. 1997, 21, 173–184. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Dijkstra, T.K.; Sarstedt, M.; Ringle, C.M.; Diamantopoulos, A.; Straub, D.W.; Ketchen, D.J.; Hair, J.F.; Hult, G.T.M.; Calantone, R.J. Common beliefs and reality about partialleast squares: Comments on Rönkkö & Evermann (2013). Organ. Res. Methods 2014, 17, 182–209. [Google Scholar]

- Segars, A.H.; Grover, V. Re-Examining Perceived Ease of Use and Usefulness: A Confirmatory Factor Analysis. MIS Q. 1993, 17, 517. [Google Scholar] [CrossRef]

- Motawa, I.; Oladokun, M. Structural equation modelling of energy consumption in buildings. Int. J. Energy Sect. Manag. 2015, 9, 435–450. [Google Scholar] [CrossRef]

- Coffie, W.; Aboagye-Otchere, F.; Musah, A. Corporate social responsibility disclosures (CSRD), corporate governance and the degree of multinational activities. J. Account. Emerg. Econ. 2018, 8, 106–123. [Google Scholar] [CrossRef]

- Fifka, M.S. Corporate Responsibility Reporting and its Determinants in Comparative Perspective—A Review of the Empirical Literature and a Meta-analysis. Bus. Strat. Environ. 2011, 22, 1–35. [Google Scholar] [CrossRef]

- Bayoud, N.S.M. Corporate Social Responsibility Disclosure and Organisational Performance: The Case of Libya, a Mixed Methods Study. Ph.D. Thesis, University of Southern Queensland, Toowoomba, Australia, 2012. [Google Scholar]

- Machdar, N.M. Corporate Social Responsibility Disclosure Mediates the Relationship between Corporate Governance and Corporate Financial Performance in Indonesia. Acad. Account. Financ. Stud. J. 2019, 23, 1–14. [Google Scholar]

- Kellett, P. Securing High Levels of Business Compliance with Environmental Laws: What Works and What to Avoid. J. Environ. Law 2019. [Google Scholar] [CrossRef]

- Stone-Romero, E.F. Implications of Research Design Options for the Validity of Inferences Derived from Organizational Research; The Sage Handbook of Organizational Research Methods, Sage: Thousand Oaks, CA, USA, 2009; pp. 302–327. [Google Scholar]

{kind=link}

| Model Construct | Items | Factor Loadings Ranges | AVE | Cronbach’s Alpha | Composite Reliability | Discriminant Validity | Source |

|---|---|---|---|---|---|---|---|

| Integration Between Csr and Pss | |||||||

| Key performance outcome | 4 | 0.748–0.854 | 0.614 | 0.861 | 0.864 | Yes | [123,124] |

| Financial | 2 | 0.839–0.854 | 0.719 | 0.835 | 0.837 | Yes | |

| Service delivery | 4 | 0.722–0.805 | 0.595 | 0.852 | 0.854 | Yes | |

| People, partnerships and resources | 3 | 0.823–0.858 | 0.698 | 0.871 | 0.874 | Yes | |

| Service user/stakeholder | 3 | 0.817–0.877 | 0.714 | 0.882 | 0.882 | Yes | [123,124,125] |

| Leadership | 3 | 0.806–0.889 | 0.710 | 0.878 | 0.880 | Yes | [130] |

| Innovation and Learning | 3 | 0.826–0.888 | 0.734 | 0.892 | 0.892 | Yes | [26,125,134] |

| Corporate Social Responsibility Disclosures | |||||||

| Community Welfare | 3 | 0.795–0.888 | 0.696 | 0.872 | 0.873 | Yes | [33,40,135,136,137] |

| Contribution to Education | 2 | 0.832–0.910 | 0.759 | 0.862 | 0.863 | Yes | [135] |

| Environmental and Energy Importance | 3 | 0.814–0.874 | 0.723 | 0.884 | 0.887 | Yes | |

| Services, Customers and Stakeholders | 3 | 0.832–0.883 | 0.745 | 0.893 | 0.898 | Yes | |

| Workforce | 3 | 0.802–0.889 | 0.713 | 0.877 | 0.881 | Yes | |

| Organizational Performance | |||||||

| Economic performance | 4 | 0.707–0.821 | 0.622 | 0.866 | 0.868 | Yes | [139] |

| Environment performance | 3 | 0.790–0.835 | 0.669 | 0.858 | 0.858 | Yes | [125,143,134,144] |

| Human performance | 5 | 0.705–0.804 | 0.562 | 0.864 | 0.865 | Yes | [141] |

| Governance performance | 4 | 0.709–0.861 | 0.607 | 0.859 | 0.860 | Yes | [148] |

| HP | EP | KPO | GP | SD | SCS | IL | SUS | EEI | WORK | LEAD | CW | PPR | ENP | CE | FINA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HP | 1 | |||||||||||||||

| EP | 0.034 | 1 | ||||||||||||||

| KPO | 0.243 | 0.090 | 1 | |||||||||||||

| GP | 0.128 | 0.171 | 0.093 | 1 | ||||||||||||

| SD | 0.061 | 0.065 | 0.064 | 0.186 | 1 | |||||||||||

| SCS | 0.097 | 0.071 | 0.073 | −0.005 | 0.012 | 1 | ||||||||||

| IL | 0.146 | −0.010 | 0.040 | 0.076 | 0.133 | 0.065 | 1 | |||||||||

| SUS | 0.014 | −0.026 | 0.156 | −0.011 | 0.037 | 0.078 | 0.025 | 1 | ||||||||

| EEI | 0.318 | 0.145 | 0.121 | 0.108 | 0.037 | 0.150 | 0.078 | −0.001 | 1 | |||||||

| WORK | 0.146 | 0.191 | 0.112 | 0.047 | 0.030 | 0.228 | 0.124 | 0.107 | 0.013 | 1 | ||||||

| LEAD | −0.023 | −0.017 | 0.044 | 0.006 | 0.172 | 0.027 | 0.213 | 0.160 | 0.037 | 0.100 | 1 | |||||

| CW | 0.123 | 0.051 | 0.106 | 0.070 | 0.063 | 0.136 | −0.024 | 0.035 | 0.209 | 0.110 | 0.143 | 1 | ||||

| PPR | 0.158 | 0.038 | 0.099 | 0.008 | 0.229 | 0.016 | 0.174 | −0.160 | 0.056 | 0.123 | 0.168 | 0.074 | 1 | |||

| ENP | 0.121 | 0.212 | 0.131 | 0.147 | 0.049 | 0.043 | 0.065 | 0.062 | 0.067 | −0.043 | 0.004 | 0.089 | 0.003 | 1 | ||

| CE | 0.062 | 0.019 | 0.119 | 0.071 | 0.027 | 0.095 | 0.072 | 0.066 | 0.159 | 0.126 | 0.054 | 0.233 | −0.017 | 0.067 | 1 | |

| FINA | 0.231 | 0.035 | 0.195 | 0.074 | −0.023 | 0.047 | 0.000 | 0.194 | 0.036 | 0.190 | −0.071 | 0.077 | 0.008 | 0.024 | 0.017 | 1 |

| The Goodness of Fit Measures | CMIN/DF | GFI | CFI | TLI | RMSEA |

|---|---|---|---|---|---|

| Recommended value | ≤3 | ≥0.9 | ≥0.9 | ≥0.9 | ≤0.08 |

| Measurement Model | 1.810 | 0.903 | 0.953 | 0.964 | 0.033 |

| Structural Model | 1.946 | 0.887 | 0.940 | 0.937 | 0.036 |

| Hypothesis | Relationship | Estimate | S.E. | C.R. | P | Inference | ||

|---|---|---|---|---|---|---|---|---|

| Hypothesis 1 (H1) | CSRD | ← | ICP | 0.544 | 0.137 | 3.960 | 0.000 | Supported |

| Hypothesis 2 (H2) | OP | ← | ICP | 0.291 | 0.117 | 2.482 | 0.013 | Supported |

| Hypothesis 3 (H3) | OP | ← | CSRD | 0.272 | 0.112 | 2.427 | 0.015 | Supported |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huy, P.Q.; Phuc, V.K. Does Strategic Corporate Social Responsibility Drive Better Organizational Performance through Integration with a Public Sector Scorecard? Empirical Evidence in a Developing Country. Processes 2020, 8, 596. https://doi.org/10.3390/pr8050596

Huy PQ, Phuc VK. Does Strategic Corporate Social Responsibility Drive Better Organizational Performance through Integration with a Public Sector Scorecard? Empirical Evidence in a Developing Country. Processes. 2020; 8(5):596. https://doi.org/10.3390/pr8050596

Chicago/Turabian StyleHuy, Pham Quang, and Vu Kien Phuc. 2020. "Does Strategic Corporate Social Responsibility Drive Better Organizational Performance through Integration with a Public Sector Scorecard? Empirical Evidence in a Developing Country" Processes 8, no. 5: 596. https://doi.org/10.3390/pr8050596

APA StyleHuy, P. Q., & Phuc, V. K. (2020). Does Strategic Corporate Social Responsibility Drive Better Organizational Performance through Integration with a Public Sector Scorecard? Empirical Evidence in a Developing Country. Processes, 8(5), 596. https://doi.org/10.3390/pr8050596