Data-Driven Investigation of Inflation Concerns Caused by COVID-19 Pandemic in the U.S.

Abstract

:1. Introduction

2. Materials and Methods

2.1. Materials

2.2. Methods

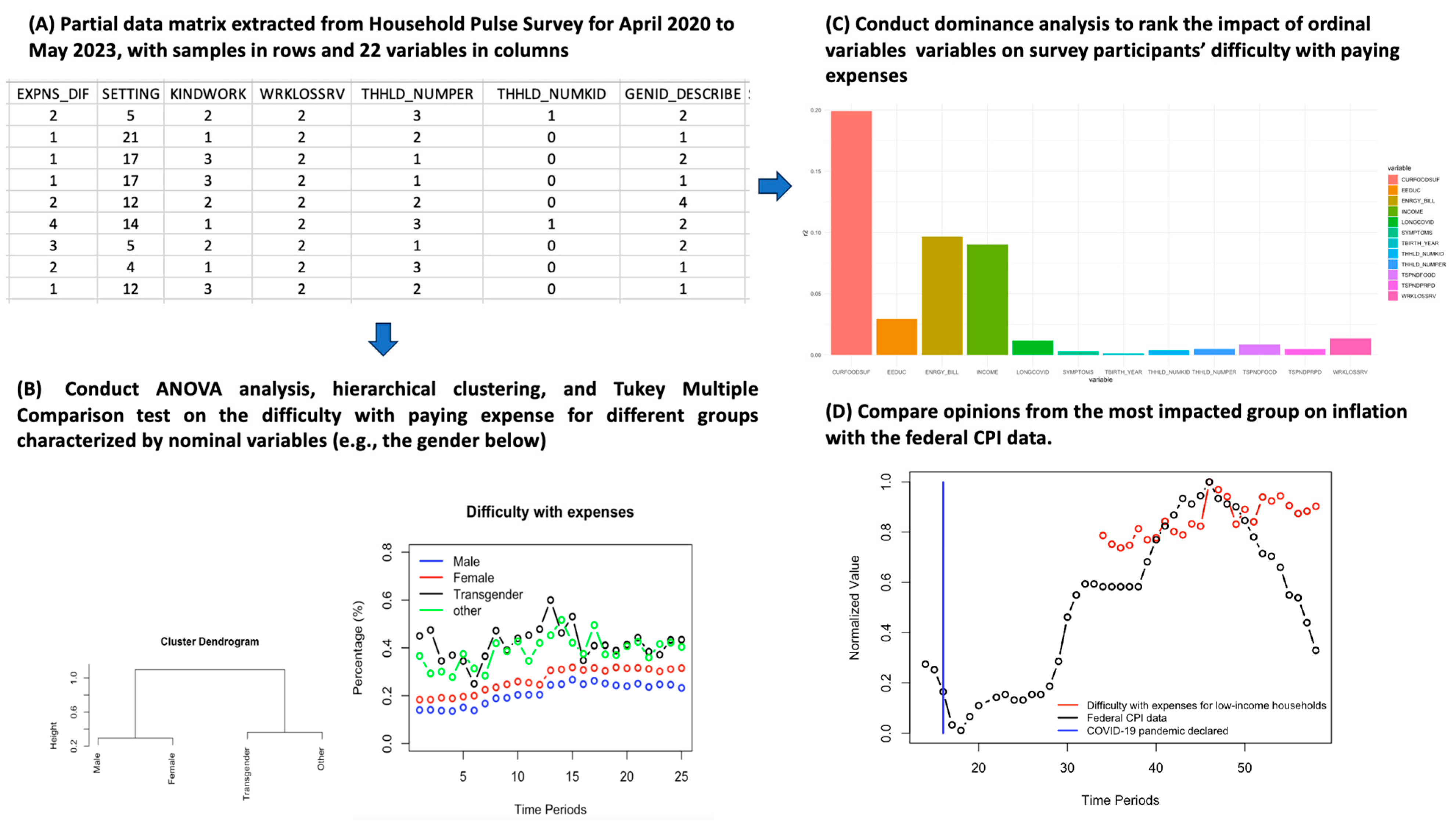

3. Results

3.1. Investigation of the Difficulty with Paying Expenses for Different Demographic and Socioeconomic Groups Characterized by Nominal Variables

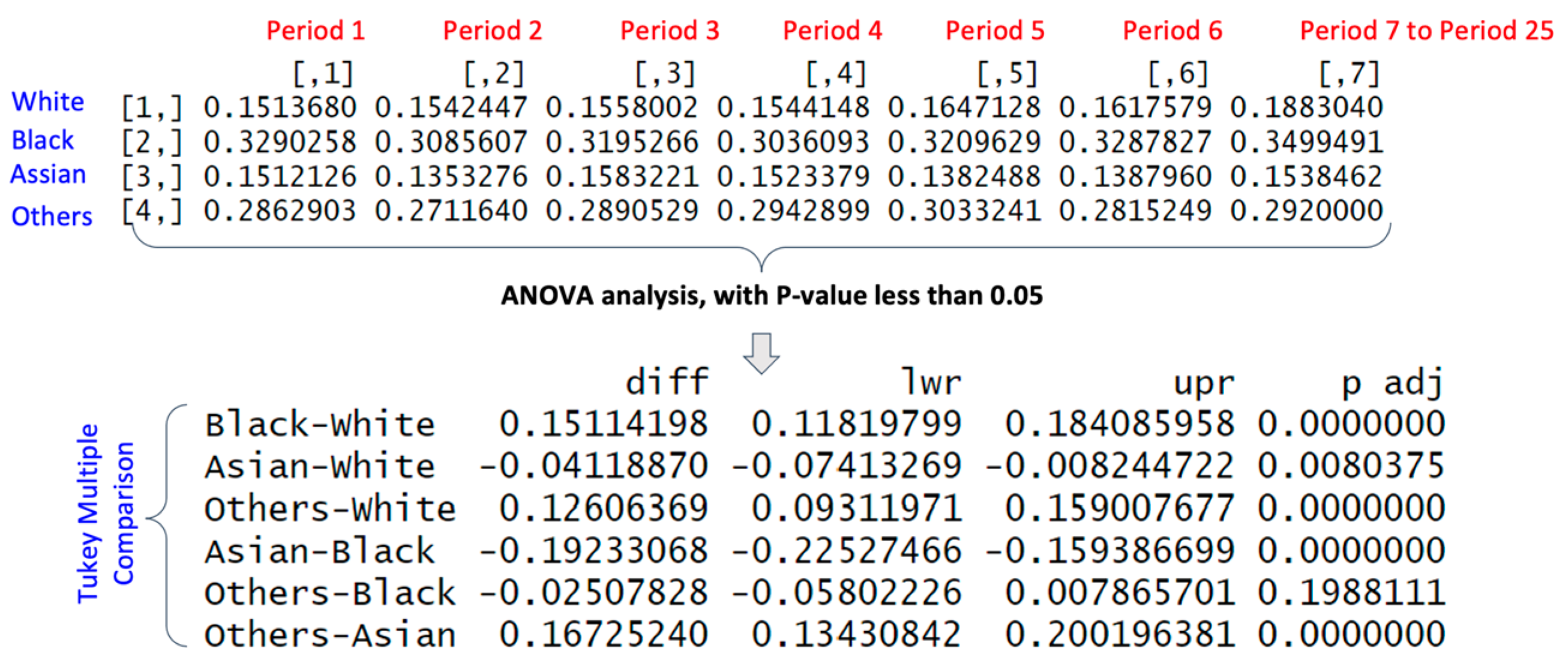

3.1.1. Difficulty with Paying Expenses for Different Races

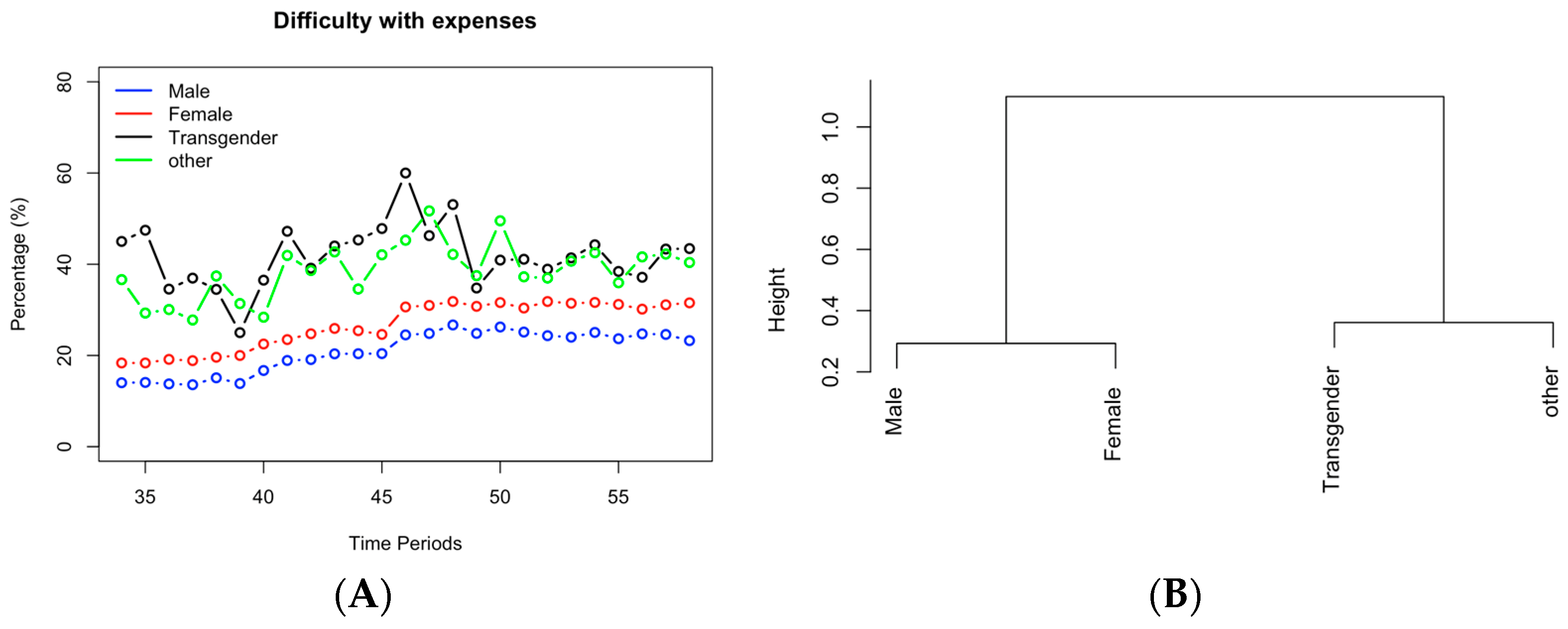

3.1.2. Difficulty with Paying Expenses for Different Genders

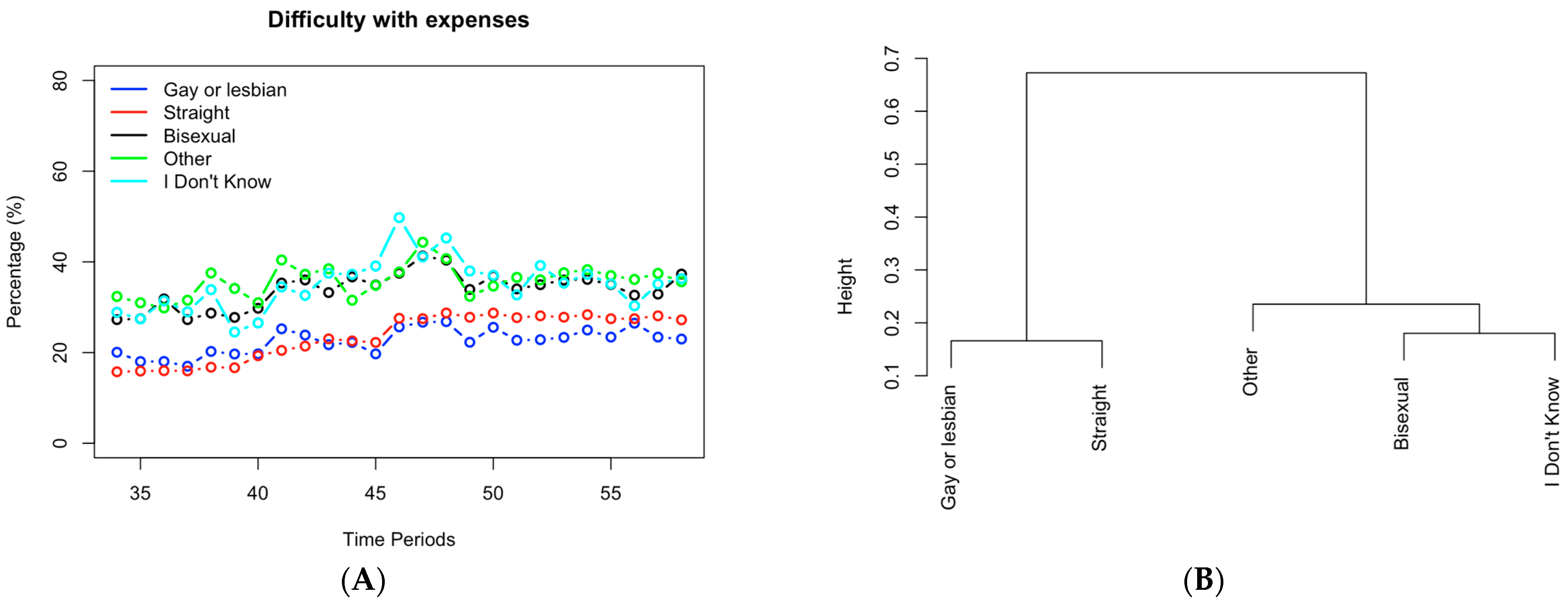

3.1.3. Difficulty with Paying Expenses for Different Sexual Orientations

3.1.4. Difficulty with Paying Expenses for Different Marital Statuses

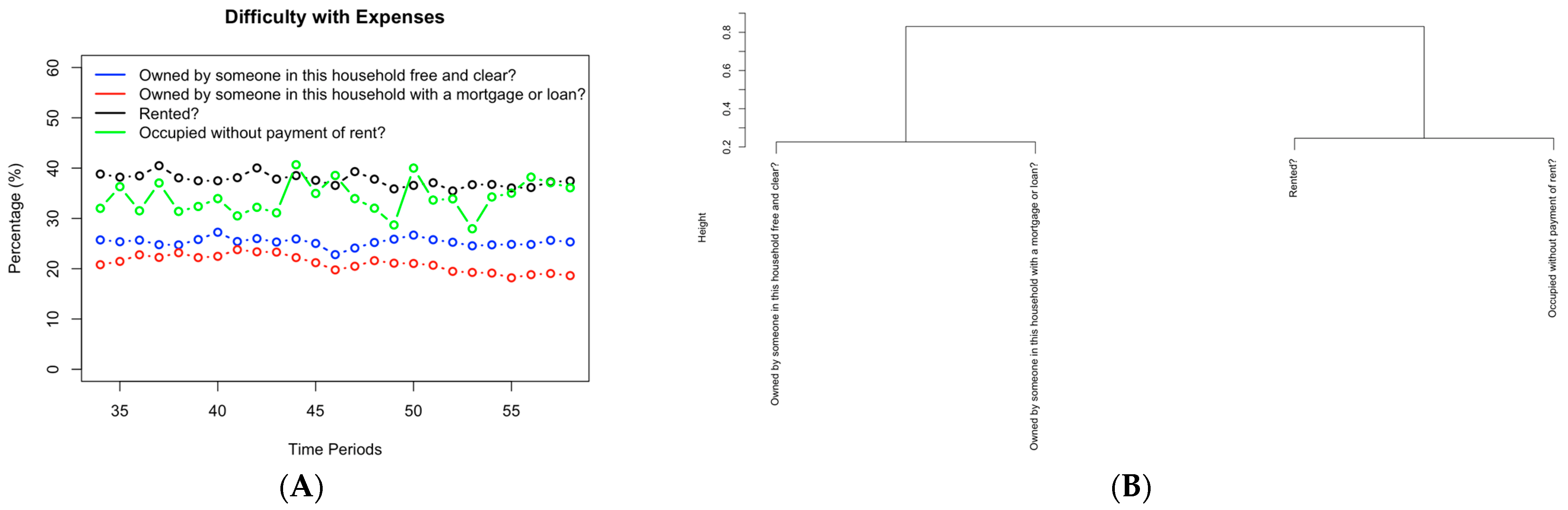

3.1.5. Difficulty with Paying Expenses for Different Property Statuses

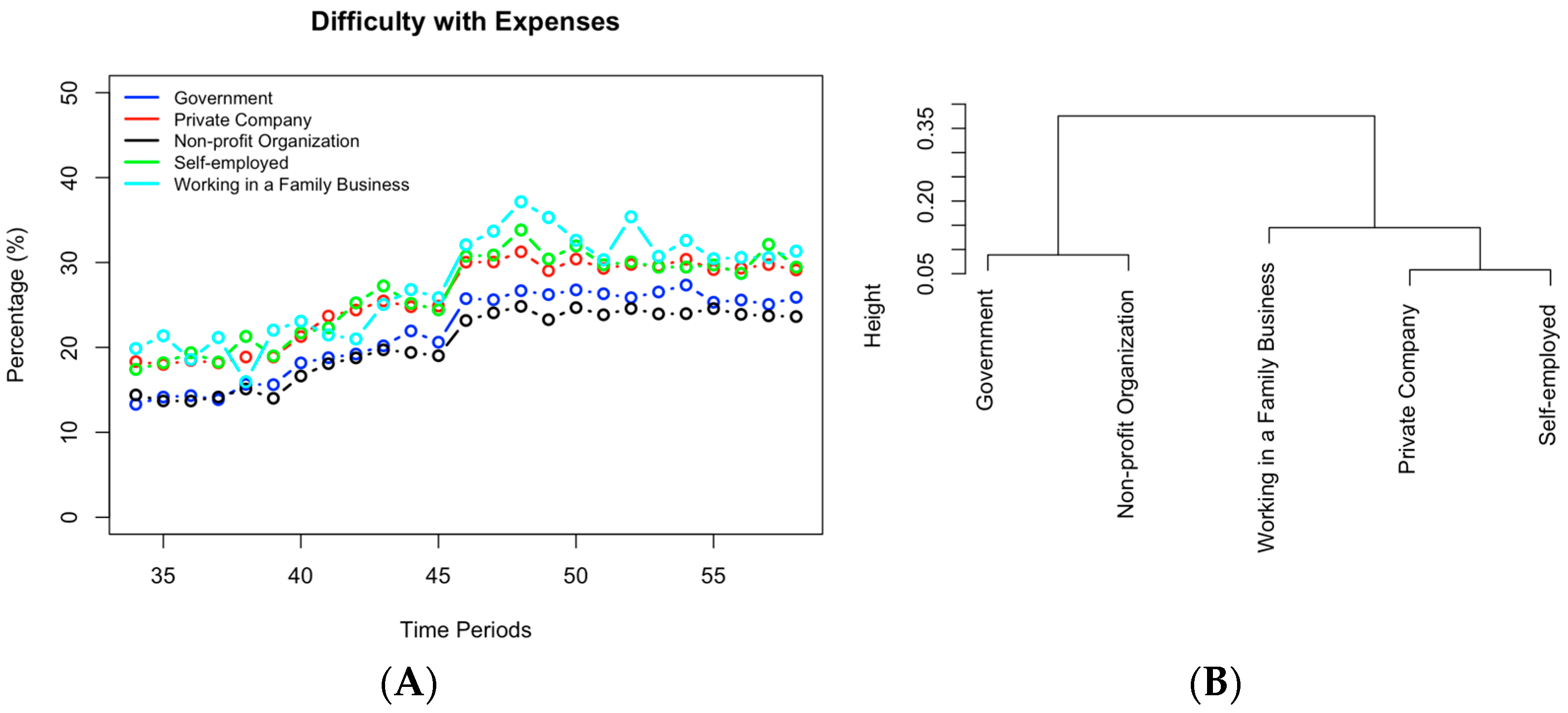

3.1.6. Difficulty with Paying Expenses for Different Sectors of Employment Clusters

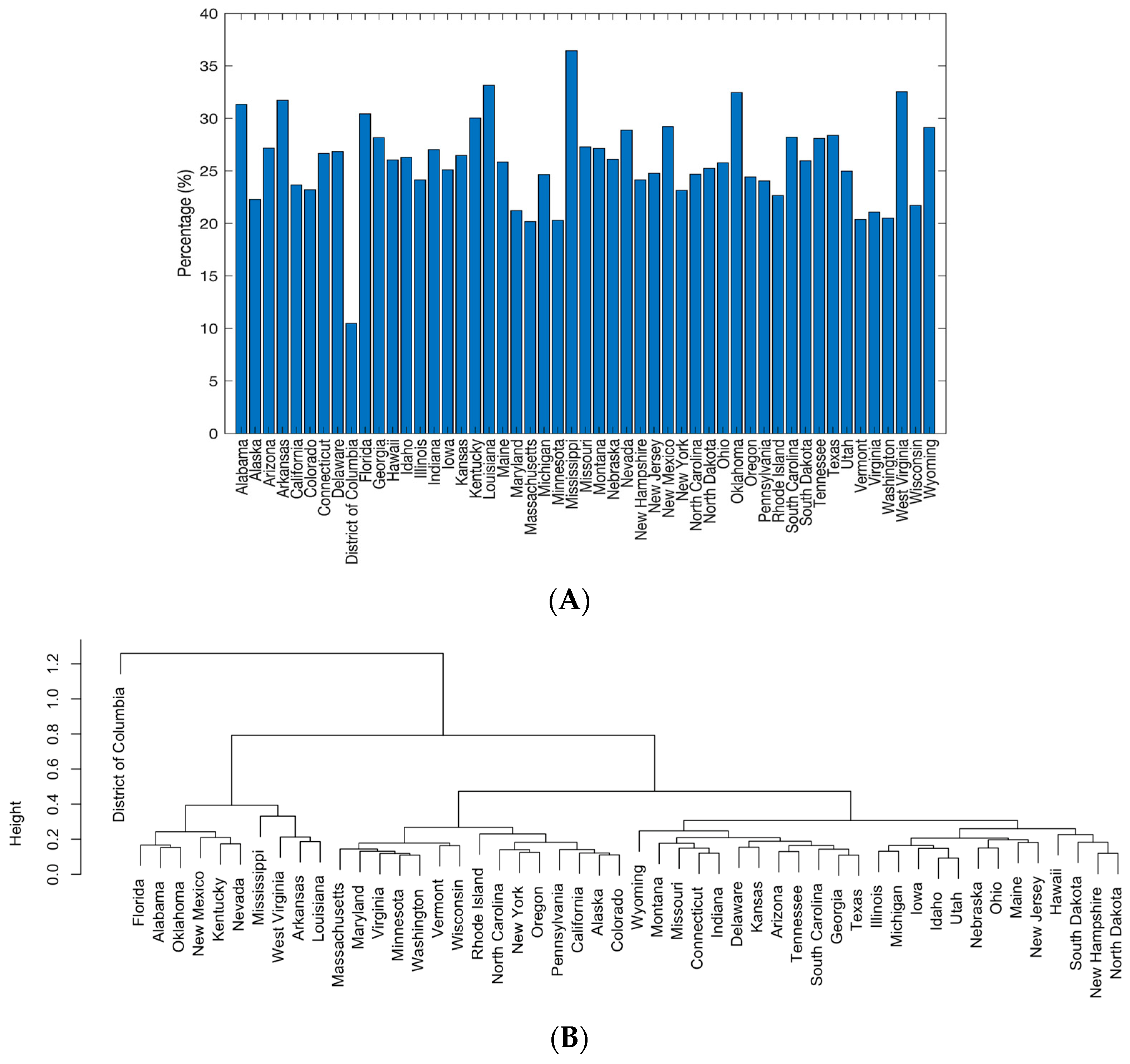

3.1.7. Difficulty with Paying Expenses for People from Different States (Locations)

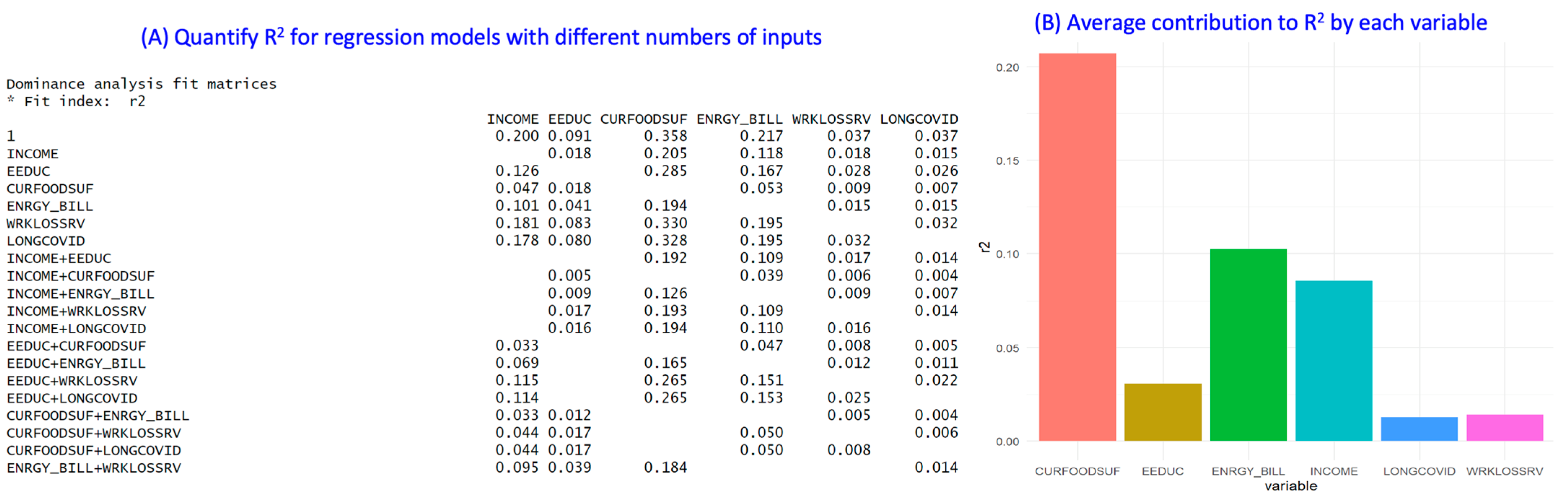

3.2. Investigation of Quantitative Factors Influencing People’s Opinions on Difficulty with the Expense

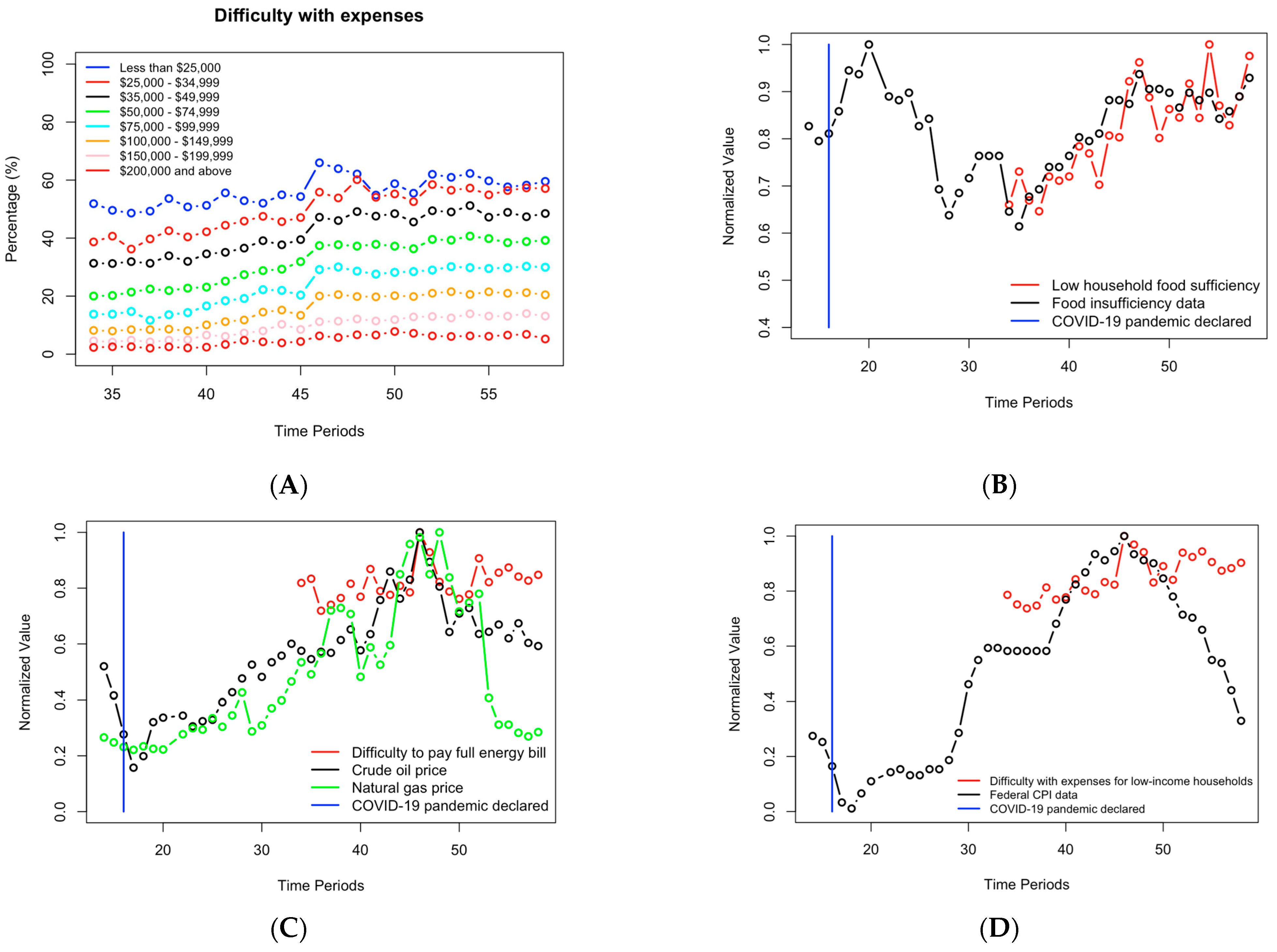

3.3. Comparison of People’s Opinions on Difficulty with Expense to Economic Data

4. Discussion

4.1. Investigation of Disparities among Nominal Demographic and Socioeconomic Groups on Their Difficulty with Paying Expenses during the COVID-19 Pandemic

4.2. Identification of Important Ordinal Demographic and Socioeconomic Factors Influencing Expense Difficulty during the COVID-19 Pandemic

4.3. The Disparities between People’s Opinion on Economic Hardship and Economic Data

4.4. Practical Implications of the Findings

4.5. Limitation and Future Work

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Wahdat, A.Z. Economic Impact Payments and Household Food Insufficiency during COVID-19: The Case of Late Recipients. Econ. Disasters Clim. Chang. 2022, 6, 451–469. [Google Scholar] [CrossRef]

- Rokhsari, A.; Doodman, N.; Tanha, H. Effects of Coronavirus Pandemic on U.S Economy: D-Vine Regression Copula Approach. Sci. Iran. 2022. [Google Scholar] [CrossRef]

- Garner, T.; Safir, A.; Schild, J. Changes in consumer behaviors and financial well-being during the coronavirus pandemic: Results from the U.S. Household Pulse Survey. Mon. Lab. Rev. 2020, 143, 1. [Google Scholar] [CrossRef]

- Armantier, O.; Koşar, G.; Pomerantz, R.; Skandalis, D.; Smith, K.; Topa, G.; van der Klaauw, W. How economic crises affect inflation beliefs: Evidence from the COVID-19 pandemic. J. Econ. Behav. Organ. 2021, 189, 443–469. [Google Scholar] [CrossRef]

- Banerjee, R.N.; Mehrotra, A.; Zampolli, F. Inflation at risk from COVID-19; Bank for International Settlements: Basel, Switzerland, 2020. [Google Scholar]

- Santacreu, A.M.; LaBelle, J. Global Supply Chain Disruptions and Inflation during the COVID-19 Pandemic. Fed. Reserve Bank St. Louis Rev. 2022, 104, 78–91. [Google Scholar] [CrossRef]

- Li, C. Inflation in the US during COVID-19 Crisis: Cause, Current Status, and Moving Forward. In Proceedings of the 2021 3rd International Conference on Economic Management and Cultural Industry (ICEMCI 2021), Guangzhou, China, 22–24 October 2021; pp. 2346–2354. [Google Scholar]

- Enriquez, D.; Goldstein, A. COVID-19′s Socioeconomic Impact on Low-Income Benefit Recipients: Early Evidence from Tracking Surveys. Socius Sociol. Res. Dyn. World 2020, 6, 2378023120970794. [Google Scholar] [CrossRef]

- Park, J.; Kim, S. Child Tax Credit, Spending Patterns, and Mental Health: Mediation Analyses of Data from the U.S. Census Bureau’s Household Pulse Survey during COVID-19. Int. J. Environ. Res. Public Health 2023, 20, 4425. [Google Scholar] [CrossRef]

- Louie, P.; Wu, C.; Shahidi, F.V.; Siddiqi, A. Inflation hardship, gender, and mental health. SSM Popul. Health 2023, 23, 101452. [Google Scholar] [CrossRef]

- Donnelly, R.; Farina, M.P. How do state policies shape experiences of household income shocks and mental health during the COVID-19 pandemic? Soc. Sci. Med. 2021, 269, 113557. [Google Scholar] [CrossRef]

- Cleaveland, C.L.; Frankenfeld, C.L. Household Financial Hardship Factors Are Strongly Associated with Poorer Latino Mental Health During COVID-19. J. Racial Ethn. Health Disparities 2022, 10, 1823–1836. [Google Scholar] [CrossRef]

- Wu, M.; Yu, E.; Kodali, A.; Wang, K.; Chen, R.; Song, K.; Wang, V.; Li, S.; Zhong, A.; Liu, D.; et al. Investigating the Economic Impacts of COVID-19 on the Mental Health of Different Demographics. J. Stud. Res. 2021, 10. [Google Scholar] [CrossRef]

- Chen, J.; Chen, A.; Shi, Y.; Chen, K.; Zhao, K.H.; Xu, M.; He, R.; Huang, Z. A Systematic Investigation of American Vaccination Preference via Historical Data. Processes 2022, 10, 1665. [Google Scholar] [CrossRef]

- Abu Farha, R.K.; Alzoubi, K.H.; Khabour, O.F.; Alfaqih, M.A. Exploring perception and hesitancy toward COVID-19 vaccine: A study from Jordan. Hum. Vaccines Immunother. 2021, 17, 2415–2420. [Google Scholar] [CrossRef]

- Kreps, S.; Dasgupta, N.; Brownstein, J.S.; Hswen, Y.; Kriner, D.L. Public attitudes toward COVID-19 vaccination: The role of vaccine attributes, incentives, and misinformation. NPJ Vaccines 2021, 6, 73. [Google Scholar] [CrossRef]

- Determann, D.; Korfage, I.J.; Lambooij, M.S.; Bliemer, M.; Richardus, J.H.; Steyerberg, E.W.; de Bekker-Grob, E.W. Acceptance of vaccinations in pandemic outbreaks: A discrete choice experiment. PLoS ONE 2014, 9, e102505. [Google Scholar] [CrossRef]

- Kreps, S.E.; Goldfarb, J.L.; Brownstein, J.S.; Kriner, D.L. The relationship between US adults’ misconceptions about COVID-19 vaccines and vaccination preferences. Vaccines 2021, 9, 901. [Google Scholar] [CrossRef]

- Alderman, H.; Gilligan, D.O.; Hidrobo, M.; Leight, J.; Ramani, G.V.; Taffesse, A.S.; Tambet, H. Impact Evaluation of the Strengthen PSNP4 Institutions and Resilience (SPIR) Development Food Security Activity (DFSA): Endline Report; International Food Policy Research Institute: Washington, DC, USA, 2021. [Google Scholar]

- Porter, C.; Hittmeyer, A.; Favara, M.; Scott, D.; Sánchez, A. The evolution of young people’s mental health during COVID-19 and the role of food insecurity: Evidence from a four low-and-middle-income-country cohort study. Public Health Pract. 2022, 3, 100232. [Google Scholar] [CrossRef]

- Huato, J.; Chavez, A. Household Income, Pandemic-Related Income Loss, and the Probability of Anxiety and Depression. East. Econ. J. 2021, 47, 546–570. [Google Scholar] [CrossRef] [PubMed]

- Keke, Y.; Dida, S.; Sugiyana, D.; Suryana, A. Determining the influence of Consumer Behaviour in using Co-Branded Card during Pandemic-COVID19. Rev. Int. Geogr. Educ. Online 2021, 11. [Google Scholar] [CrossRef]

- Braholli, A. An Investigation of Consumer Behavior in Online Trade during the COVID-19 Pandemic: A Case Study. Qual. Access Success 2022, 23, 45–58. [Google Scholar] [CrossRef]

- Wu, C.; Louie, P.; Bierman, A.; Schieman, S. Assessment of Sociodemographics and Inflation-Related Stress in the US. JAMA Netw. Open 2023, 6, e2313431. [Google Scholar] [CrossRef] [PubMed]

- Morales, D.X.; Morales, S.A.; Beltran, T.F. Racial/Ethnic Disparities in Household Food Insecurity during the COVID-19 Pandemic: A Nationally Representative Study. J. Racial Ethn. Health Disparities 2021, 8, 1300–1314. [Google Scholar] [CrossRef] [PubMed]

- Neymotin, F.; Forgey, F. Government Stimulus and Mortgage Payments during COVID-19: Evidence from the US Census Household Pulse Survey. J. Hous. Res. 2023, 32, 66–80. [Google Scholar] [CrossRef]

- Madgavkar, A.; White, O.; Krishnan, M.; Mahajan, D.; Azcue, X. COVID-19 and Gender Equality: Countering the Regressive Effects; McKinsey Global Institute: Washington, DC, USA, 2020. [Google Scholar]

- Fox, J.; Bartholomae, S. Household finances, financial planning, and COVID-19. Financ. Plan. Rev. 2020, 3, e1103. [Google Scholar] [CrossRef]

- Higgins, M. Investors Can Temper Their Inflation Fears: Post-COVID Inflation is Unlikely to Resemble the Great Inflation of 1968 to 1982. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Klesta, M. Inflation Adds Burden to Households Already Struggling to Cope with Lingering Effects of the Pandemic, and the Tight Job Market Challenges Hiring and Retention in Some Sectors: Findings From the Community Issues Survey 2022. 2022. Available online: https://www.clevelandfed.org/publications/community-issues-and-insights/ii-20220519-community-issues-and-insights-survey-results (accessed on 1 June 2023).

- Carpenter, C.S.; Lee, M.J.; Nettuno, L. Economic outcomes for transgender people and other gender minorities in the United States: First estimates from a nationally representative sample. South. Econ. J. 2022, 89, 280–304. [Google Scholar] [CrossRef]

- Barnes, M.; Bauer, L.; Edelberg, W. 11 Facts on the Economic Recovery from the COVID-19 Pandemic; Hamilton Project Economic; Brookings: Washington, DC, USA, 2021. [Google Scholar]

- CBPP. Robust COVID Relief Achieved Historic Gains against Poverty and Hardship, Bolstered Economy. 2022. Available online: www.cbpp.org (accessed on 1 June 2023).

- Reinsdorf, M. COVID-19 and the CPI: Is Inflation Underestimated? SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Gelman, A. Analysis of variance—Why it is more important than ever. Ann. Statist. 2005, 33, 1–53. [Google Scholar] [CrossRef]

- McHugh, M.L. Multiple comparison analysis testing in ANOVA. Biochem. Med. 2011, 21, 203–209. [Google Scholar] [CrossRef]

- Simkus, J. ANOVA (Analysis Of Variance): Definition, Types, and Examples; Simply Scholar Ltd.: London, UK, 2022. [Google Scholar]

- Zwanenburg, G.; Hoefsloot, H.C.; Westerhuis, J.A.; Jansen, J.J.; Smilde, A.K. ANOVA-principal component analysis and ANOVA-simultaneous component analysis: A comparison. J. Chemom. 2011, 25, 561–567. [Google Scholar] [CrossRef]

- Minitab. What Is Tukey’s Method for Multiple Comparisons? Minitab LLC: State College, PA, USA, 2022. [Google Scholar]

- Hsu, J.C.; Peruggia, M. Graphical Representations of Tukey’s Multiple Comparison Method. J. Comput. Graph. Stat. 1994, 3, 143–161. [Google Scholar] [CrossRef]

- Azen, R.; Budescu, D.V. The dominance analysis approach for comparing predictors in multiple regression. Psychol. Methods 2003, 8, 129–148. [Google Scholar] [CrossRef] [PubMed]

- Budescu, D.V. Dominance analysis: A new approach to the problem of relative importance of predictors in multiple regression. Psychol. Bull. 1993, 114, 542–551. [Google Scholar] [CrossRef]

- Friedman, C. Financial hardship experienced by people with disabilities during the COVID-19 pandemic. Disabil. Health J. 2022, 15, 101359. [Google Scholar] [CrossRef] [PubMed]

- Kim, Y.; Murphy, J. Mental Health, Food Insecurity, and Economic Hardship among College Students during the COVID-19 Pandemic. Health Soc. Work. 2023, 48, 124–132. [Google Scholar] [CrossRef]

- Sultana, M.S.; Khan, A.H.; Hossain, S.; Islam, T.; Hasan, M.T.; Ahmed, H.U.; Li, Z.; Khan, J.A.M. The Association between Financial Hardship and Mental Health Difficulties among Adult Wage Earners during the COVID-19 Pandemic in Bangladesh: Findings from a Cross-Sectional Analysis. Front. Psychiatry 2021, 12, 635884. [Google Scholar] [CrossRef]

- Gonzalez, M.R.; Brown, S.A.; Pelham, W.E.; Bodison, S.C.; McCabe, C.; Baker, F.C.; Baskin-Sommers, A.; Dick, A.S.; Dowling, G.J.; Gebreselassie, S.; et al. Family Well-Being during the COVID-19 Pandemic: The Risks of Financial Insecurity and Coping. J. Res. Adolesc. 2023, 33, 43–58. [Google Scholar] [CrossRef]

- Kim, B.; Kim, D.H.; Jang, S.-Y.; Shin, J.; Lee, S.G.; Kim, T.H. Family economic hardship and adolescent mental health during the COVID-19 pandemic. Front. Public Health 2022, 10, 904985. [Google Scholar] [CrossRef]

- Sujan, M.H.; Tasnim, R.; Islam, S.; Ferdous, M.; Haghighathoseini, A.; Koly, K.N.; Pardhan, S. Financial hardship and mental health conditions in people with underlying health conditions during the COVID-19 pandemic in Bangladesh. Heliyon 2022, 8, e10499. [Google Scholar] [CrossRef]

- Trógolo, M.A.; Moretti, L.S.; Medrano, L.A. A nationwide cross-sectional study of workers’ mental health during the COVID-19 pandemic: Impact of changes in working conditions, financial hardships, psychological detachment from work and work-family interface. BMC Psychol. 2022, 10, 73. [Google Scholar] [CrossRef]

- Kim, C.E.; Kim, H.H.-S. Economic precarity and mental health during the COVID-19 pandemic: Findings from the census household pulse survey (2020–2021). Sociol. Spectr. 2022, 42, 195–216. [Google Scholar] [CrossRef]

- Kim, D. Financial hardship and social assistance as determinants of mental health and food and housing insecurity during the COVID-19 pandemic in the United States. SSM Popul. Health 2021, 16, 100862. [Google Scholar] [CrossRef] [PubMed]

- Yao, H.; Wang, J.; Liu, W. Lockdown Policies, Economic Support, and Mental Health: Evidence From the COVID-19 Pandemic in United States. Front. Public Health 2022, 10, 857444. [Google Scholar] [CrossRef] [PubMed]

- Newswire, P.R. The Pandemics within the Pandemic; Parker-University: Dallas, TX, USA, 2020. [Google Scholar]

- United States Census Bureau. Household Pulse Survey: Measuring Social and Economic Impacts during the Coronavirus Pandemic; United States Census Bureau: Suitland, MD, USA, 2021. Available online: https://www.census.gov/programs-surveys/household-pulse-survey.html (accessed on 1 June 2023).

- Crude Oil Brent US Dollars per Barrel. Available online: https://countryeconomy.com/ (accessed on 1 June 2023).

- US Natural Gas Residential Price. Available online: https://ycharts.com/ (accessed on 1 June 2023).

- United States Census Bureau. Food Scarcity Percentage of Adults in Households Where There Was Either Sometimes or Often Not Enough to Eat in the Last 7 Days; United States Census Bureau: Suitland, MD, USA, 2021. Available online: https://www.census.gov/data-tools/demo/hhp/#/?periodSelector=14 (accessed on 1 June 2023).

- Ran, X.; Xi, Y.; Lu, Y.; Wang, X.; Lu, Z. Comprehensive survey on hierarchical clustering algorithms and the recent developments. Artif. Intell. Rev. 2022, 56, 8219–8264. [Google Scholar] [CrossRef]

- Heslin, K.C.; Hall, J.E. Sexual Orientation Disparities in Risk Factors for Adverse COVID-19–Related Outcomes, by Race/Ethnicity—Behavioral Risk Factor Surveillance System, United States, 2017–2019. MMWR. Morb. Mortal. Wkly. Rep. 2021, 70, 149–154. [Google Scholar] [CrossRef]

- Kudoh, R.; Komiya, K.; Shinohara, A.; Kageyama, T.; Hiramatsu, K.; Kadota, J.-I. Marital status and post-COVID-19 conditions. Respir. Investig. 2023, 61, 181–185. [Google Scholar] [CrossRef]

- Seiler, P. Weighting bias and inflation in the time of COVID-19: Evidence from Swiss transaction data. Swiss J. Econ. Stat. 2020, 156, 13. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Abbreviation | Meanings of Abbreviations |

|---|---|

| CURFOODSUF | Food sufficiency in the household over the past week: (1) Sufficient supply of desired food types, (2) Adequate supply, though not always preferred food types, (3) Occasional insufficient food, (4) Frequent food shortages |

| EEDUC | Level of education achieved: (1) Below high school, (2) Partial high school, (3) High school diploma, (4) Some college (without degree or ongoing), (5) Associate’s degree (e.g., AA, AS), (6) Bachelor’s degree, (7) Advanced degree |

| ENRGY_BILL | Challenges in paying the entire energy bill: (1) Almost every month; (2) Some months; (3) 1 or 2 months; (4) Never. |

| TBIRTH_YEAR | Birth year: Individuals born prior to 2005. |

| EXPNS_DIF | Difficulty with paying expenses: (1) Not challenging, (2) Slightly challenging, (3) Moderately challenging, (4) Highly challenging. |

| SYMPTOMS | Severity of COVID-19 symptoms at their worst: (1) No symptoms, (2) Mild symptoms, (3) Moderate symptoms, (4) Severe symptoms. |

| INCOME | Household income (pre-tax): (1) Less than $25,000; (2) $25,000–$34,999; (3) $35,000–$49,999; (4) $50,000–$74,999; (5) $75,000–$99,999; (6) $100,000–$149,999; (7) $150,000–$199,999; (8) $200,000 or more. |

| LONGCOVID | Prolonged COVID-19 or coronavirus symptoms (lasting 3 months or more): (1) Yes, (2) No |

| THHLD_NUMKID | Total count of individuals under the age of 18 in the household: (0–40) number of individuals under 18 (whole number) |

| TSPN FOOD | Amount spent on food and groceries by the household: $0-$900 |

| TSPN PRPD | Expenditure on ready-made meals by the household: $0-$500 |

| THHLD_NUMPER | Total count of individuals in the household: (1–40) number of individuals (whole number) |

| WRKLOSSRV | “Recent job loss in the household: (1) Yes, (2) No |

| PERIOD | The survey’s time period index |

| MS | Current marital status: (1) Married; (2) Widowed; (3) Divorced; (4) Separated; (5) Single (Never married) |

| GENID_DESCRIBE | Present gender identity: (1) Male, (2) Female, (3) Transgender, (4) Other |

| RRACE | Race: (1) White, (2) Black, (3) Asian, (4) Other races |

| SEXUAL_ORIENTATION | Sexual orientation: (1) Gay or lesbian, (2) Straight, (3) Bisexual, (4)Other, (5) I don’t know |

| KINDWORK | Employment sector: (1) Government, (2) Private company, (3) Non-profit organization (including tax-exempt and charitable organizations), (4) Self-employed, (5) Family business |

| TENURE | Housing status: (1) Owned outright by you or a household member? (2) Owned with a mortgage or loan (including home equity loans) by you or a household member? (3) Rented? (4) Occupied without rent payment? |

| EST_ST | Survey participants’ state of residence |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, C.; Tang, J.; Jiang, E.; Chen, W.; Guo, A.; Huang, Z. Data-Driven Investigation of Inflation Concerns Caused by COVID-19 Pandemic in the U.S. Processes 2023, 11, 3217. https://doi.org/10.3390/pr11113217

Zhang C, Tang J, Jiang E, Chen W, Guo A, Huang Z. Data-Driven Investigation of Inflation Concerns Caused by COVID-19 Pandemic in the U.S. Processes. 2023; 11(11):3217. https://doi.org/10.3390/pr11113217

Chicago/Turabian StyleZhang, Cheng, Joanna Tang, Ethan Jiang, Willa Chen, Anthony Guo, and Zuyi Huang. 2023. "Data-Driven Investigation of Inflation Concerns Caused by COVID-19 Pandemic in the U.S." Processes 11, no. 11: 3217. https://doi.org/10.3390/pr11113217

APA StyleZhang, C., Tang, J., Jiang, E., Chen, W., Guo, A., & Huang, Z. (2023). Data-Driven Investigation of Inflation Concerns Caused by COVID-19 Pandemic in the U.S. Processes, 11(11), 3217. https://doi.org/10.3390/pr11113217