Development of Concepts for a Climate-Neutral Chemical–Pharmaceutical Industry in 2045

Abstract

:1. Introduction

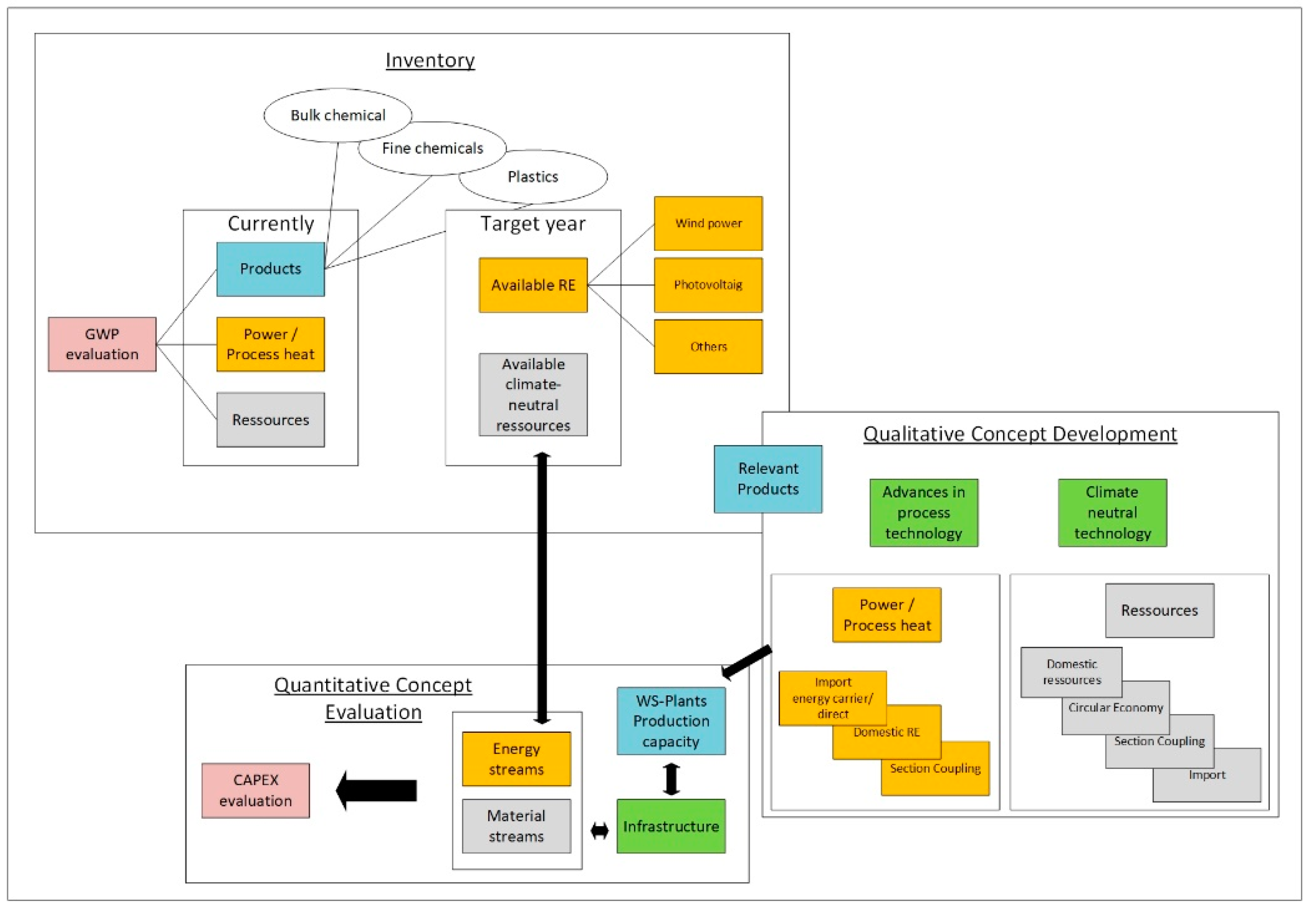

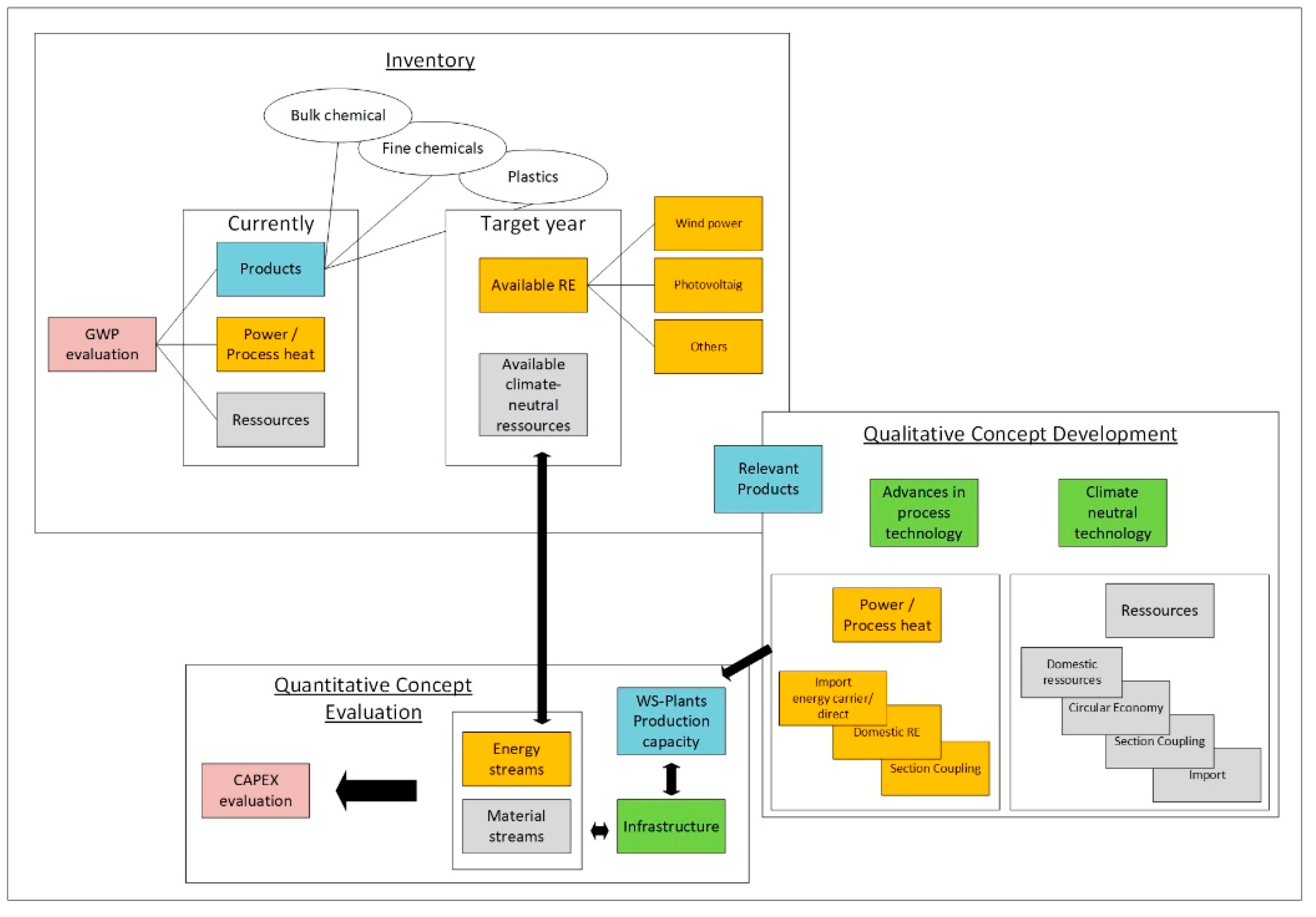

2. Methodology for the Development of Climate Neutrality Concepts

3. Overview of Existing Climate Neutrality Concepts

4. Alternative Climate Neutrality Concepts

5. Discussion

- To reduce GWP emissions in the German ChPI. energy demand has to be shifted towards renewable energies for both electrical power and process heat.

- Currently, half of the German ChPI-attributed GWP is based on fossil feedstock, such as oil and natural gas [15]. To replace these, alternative carbon sources have to be considered. As described, these are biomass, recycling and CCU, and all include section coupling within the industrial sector as a whole.

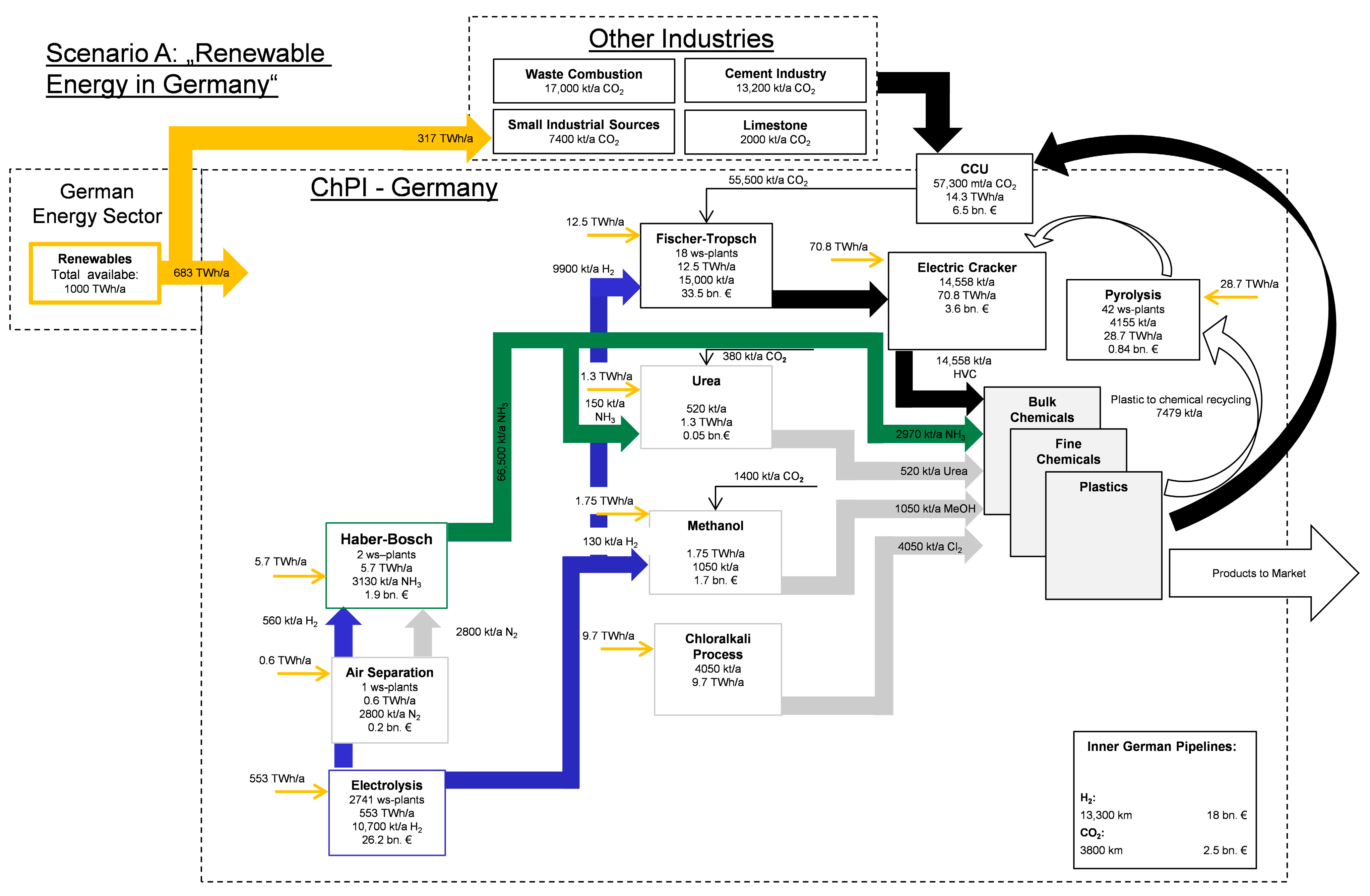

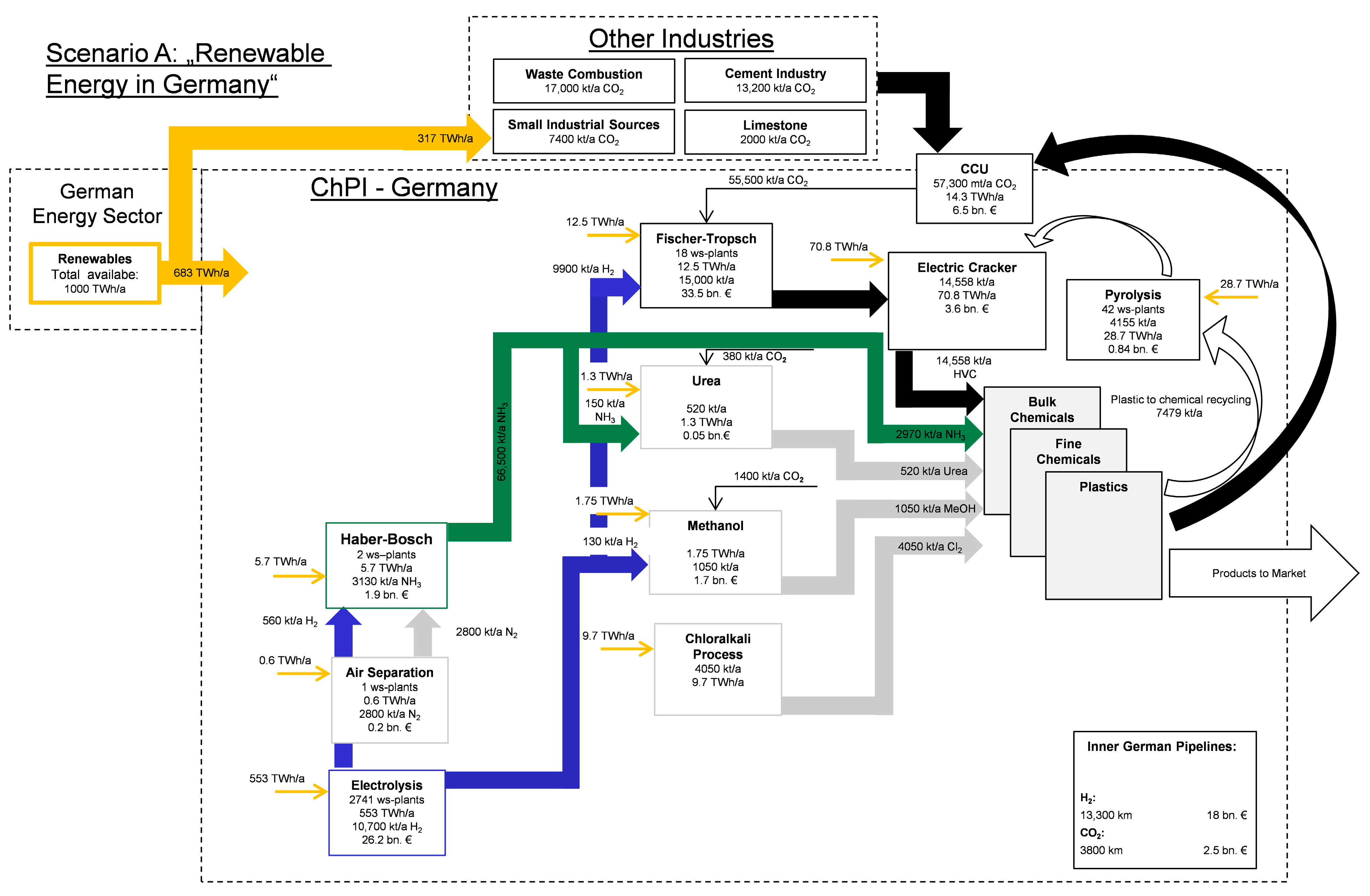

- CCU will have a primary role here, as some industries, such as the cement industry, will have process-related emissions, which will be impossible to eliminate. These can be bound within products of the ChPI and thus be valorized from harmful greenhouse gases to consumer goods. An estimated amount of 13.2 mt is annually available in Germany [37], as well as other sources. These include thermal waste disposal and other industrial processes. With section coupling, 39.2 mt of carbon capture can be made available to the ChPI with CCU [19,37].

- As well as feedstock towards non-fossil materials, such as carbon dioxide from CCU, CO2 will be required as a feedstock for ChPI and traded as such [23,24,49]. Section coupling will, therefore, become a major factor in running the economy. as trade with CO2 will develop naturally. Niche solutions for feedstock acquirement include the circular economy and will play a major role as a market for carbon dioxide from CCU and other sources evolves.

- Another GWP-reducing action is the expansion of the circular economy, as this saves energy, as well as material resources. This is supported by rising digitalization [53]. This is not only applicable to metals and carbon, but also to biologicals [54]. The development of urban mining projects, as shown by the University of Clausthal, is important to close gaps in resource procurement and increase the efficiency in which we use our environment [55].

- The pharmaceutical industry currently consumes 16 TWh of energy and emits 3 Mt CO2eq annually. The biggest factors are WFI consumption for CIP/SIP in the production of biologics. There is potential for GWP reduction through the introduction of continuous processes and the valorization of residual materials in the production of natural products [56,57,58]. Problem analyses and solutions such as these in the pharmaceutical industry are not always transferable to other industries. Companies and industries must, therefore, consider individual solutions for their specific GWP sources. This will lead to the easiest sources to eliminate being tackled first. This freedom of action will ensure that the most efficient GWP reduction is achieved.

- The problem becomes rewarding efforts to reduce GWP and penalizing emissions. Setting a political framework for this is feasible within a country with the help of CO2 certificates. In this way, climate protection can become a business decision. However, this will be difficult in international competition and trade without a superordinate body or international regulations. How this can be implemented on an international scale remains an open question.

- Moving towards renewable electrical power generation requires consent within the populous to make the transition from traditional energy generation as efficient as possible. This includes the construction of power lines and wind turbines [26]. This is invoking a debate on land use, as RE production has proven to be more space-inefficient than traditional fossil energy generation. This predicament between preserving nature as is and developing more areas for RE is still subject to ongoing debates not only in Germany. Importing power via ammonia could be a solution to this problem.

- To guarantee a stable power supply, long- and short-term energy storage and supply is needed. The electrification of the ChPI can help net stability by buying power during high production [22].

- Even with the high aims of current policies, Germany will remain a net energy importer as it has been in the past. Germany recently intended to import LNG, and long-term contracts with places such as Qatar have been negotiated. German industry is investing at least EUR 1 bn in harbour terminal buildings for at least the next 5 years. Qatar is investing about USD 30 bn in upgrading the amounts of gas [59,60,61].

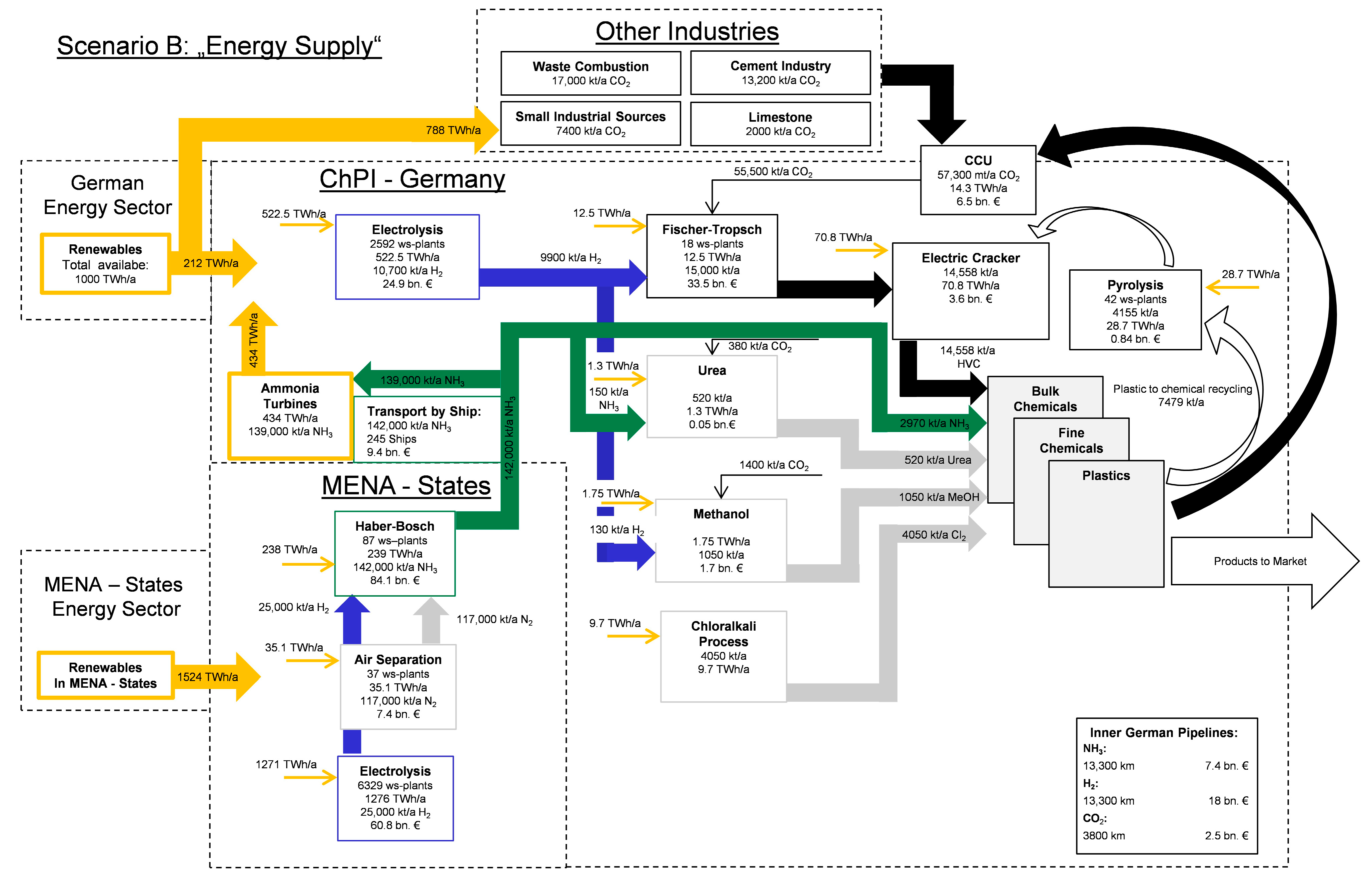

- A candidate for energy importation is ammonia, as its production is well understood by the ChPI. The substitution of hydrogen provided by natural gas with electrolysis is a minor one. Electrolysis has been subject to research and development for decades and is projected to become more cost-effective in the near future [31]. The transportation costs are lower than those of alternative green fuels [62]. Additionally, ammonia can be converted to electrical power as well as process heat [40,63,64,65]. This can also help to manage electrical power supply during fluctuations in wind and solar power.

- Producing ammonia in favourably located states from renewable sources can circumvent energy scarcity within Germany and keep the German ChPI supplied with hydrogen. Thus, the migration of oil and gas-based industry can be avoided.

- As the requirements of site factors are having access to renewable-energy-suitable areas, the list of possible countries is plentiful [66]. This can be used to diversify sources of green ammonia to avoid being affected by political conflict and other local factors. This would stabilize energy availability and grant a greater degree of independence. Recent efforts towards the importation of ammonia and hydrogen have been made by the German government, and they will have to continue to move towards a climate-neutral ChPI [67,68,69].

- As this technology develops and is being applied by other countries, the cost of ammonia plants will decrease and the efficiency of ammonia technology will increase. Ammonia-fired turbines, as well as co-fired ammonia methane, are currently under development and improvement by Mitsubishi and are projected to be commercial by 2025 [70]. The efficiency of power to ammonia to power was calculated to be between 31 and 39% [71]. This is of interest for further research.

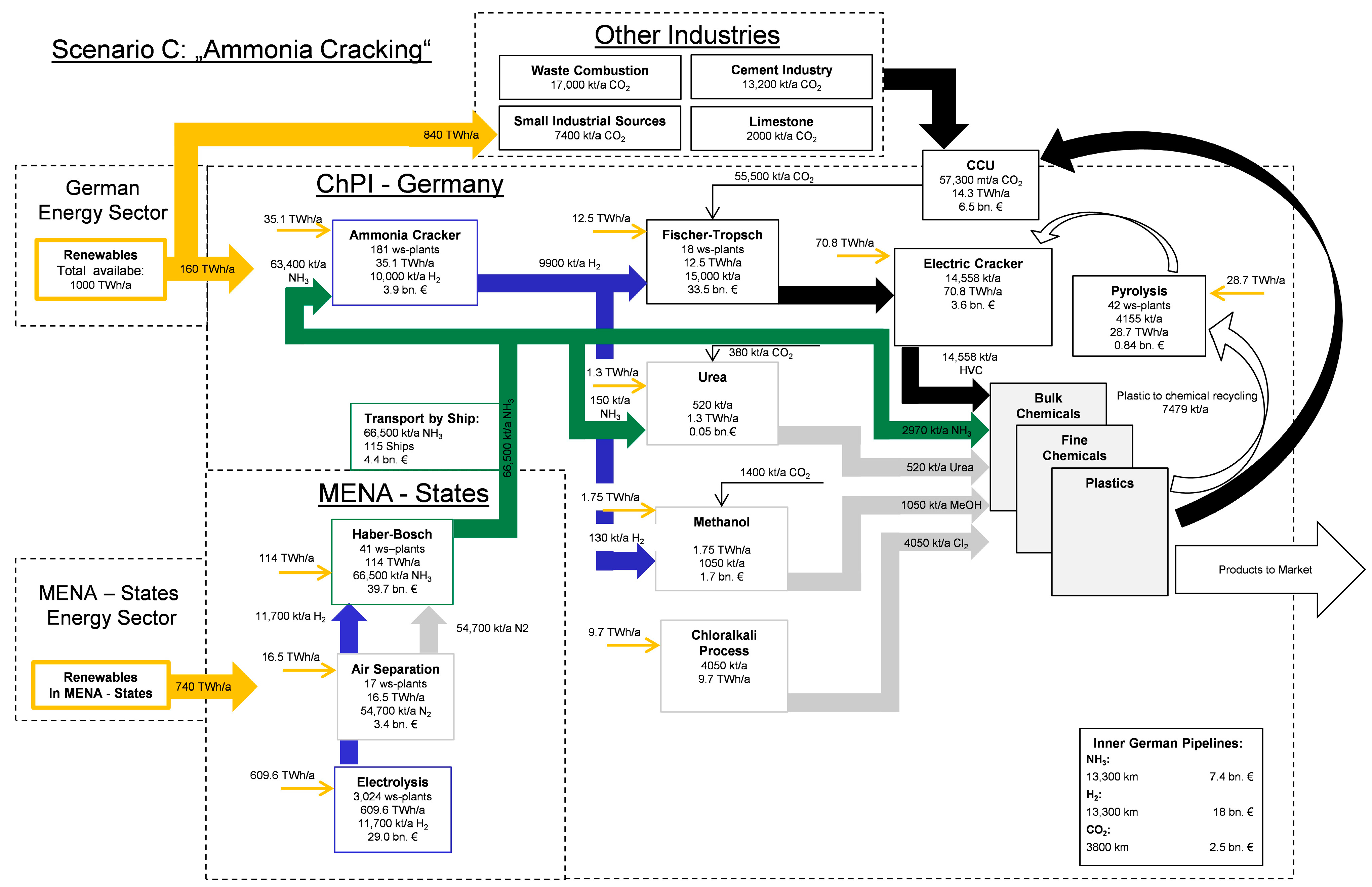

- It has been found that ammonia can be cracked into hydrogen at a relatively low cost. To move towards a ChPI without Scope 3 emissions, CO2 and hydrogen have to be used as a feedstock for the traditional petrochemical industry. Furthermore, ammonia crackers are already commercially available [72,73] and under further study [74]. With further study, this technology can make a great impact towards climate neutrality.

- Nevertheless, to implement this strategy, steps have to be taken today: a framework for an ammonia-based ChPI needs to be developed. This includes ammonia infrastructure a national and international pipeline grid, as well as international shipping. Further development of ammonia-based technology and commercial availability is needed. In any case, the expansion of RE is not circumventable within Germany or internationally.

- Inventory of current production and availability of future resources;

- Qualitative concept development with climate-neutral technologies;

- Quantitative concept evaluation of energy and material streams and, finally, costs.

- The use of non-fossil energy sources (in this study, NH3 and H2) and renewable energies (photovoltaic or wind);

- Avoidance of fossil carbon as a feedstock for the synthesis of goods;

- Sector coupling and use of CCU;

- Application of the economy-of-scale principle where possible.

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| CAPEX | Capital expenditure |

| CCU | Carbon capture and utilization |

| ChPI | Chemical–pharmaceutical industry |

| GWP | Global warming potential |

| MENA | Middle East and Northern Africa |

| OPEX | Operational expenditure |

| PAT | Process analytical technology |

| QbD | Quality by design |

| RE | Renewable energy |

| WFI | Water for injection |

| WS | World-scale |

References

- IPCC. Climate Change 2022: Impacts, Adaptation, and Vulnerability: Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change 2022; IPCC: Geneva, Switzerland, 2022. [Google Scholar]

- Cook, J.; Oreskes, N.; Doran, P.T.; Anderegg, W.R.L.; Verheggen, B.; Maibach, E.W.; Carlton, J.S.; Lewandowsky, S.; Skuce, A.G.; Green, S.A.; et al. Consensus on consensus: A synthesis of consensus estimates on human-caused global warming. Environ. Res. Lett. 2016, 11, 48002. [Google Scholar] [CrossRef]

- SPD; Bündnis 90/Die Grünen; FDP. Mehr Fortschritt Wagen: Bündnis für Freiheit, Gerechtigkeit und Nachhaltigkeit 2021; Koalitionsvertrag Zwischen SPD, Bündnis 90/Die Grünen und FDP: Berlin, Germany, 2021. [Google Scholar]

- Böcking, D. Massiver Preisanstieg: So Lange Müssen Verbraucher in Deutschland für Einen Liter Benzin Arbeiten. DER SPIEGEL [Online]. 16 March 2022. Available online: https://www.spiegel.de/wirtschaft/service/benzinpreis-verbraucher-arbeiten-zwei-minuten-laenger-pro-liter-a-e23bfc1b-6258-4673-bc86-a8d932bfed5f (accessed on 17 March 2022).

- Deutscher Bundestag. Stenographischer Bericht 19. Sitzung 2022; Deutscher Bundesta: Berlin, Germany, 2022. [Google Scholar]

- Nguyen, C. Klimaschutz: Bundesregierung Will 200 Milliarden Euro in Klimaschutz Investieren. Die Zeit [Online]. 6 March 2022. Available online: https://www.zeit.de/politik/deutschland/2022-03/klimaschutz-bundesregierung-erneuerbare-energie-lindner-habeck?page=8&utm_referrer=https%3A%2F%2Fwww.google.com%2F (accessed on 18 March 2022).

- Webseite der Bundesregierung|Startseite. Klimaschutzgesetz: Klimaneutralität bis 2045|Bundesregierung. Available online: https://www.bundesregierung.de/breg-de/themen/klimaschutz/klimaschutzgesetz-2021-1913672 (accessed on 21 March 2022).

- Schmidt, A.; Köster, D.; Strube, J. Climate Neutrality Concepts for the German Chemical–Pharmaceutical Industry. Processes 2022, 10, 467. [Google Scholar] [CrossRef]

- Sinn, H. Das grüne Pardoxon; Weltbuch Verlag Gmbh: Dresden, Germany, 2020; ISBN 9783906212616. [Google Scholar]

- Saling, P. The BASF Eco-Efficiency Analysis: A 20-Year Success Story, 1st ed.; BASF SE Sustainability Strategy: Ludwigshafen, Germany, 2016; ISBN 9783000542732. [Google Scholar]

- Reiber, S. Verpatzte Chance; Spiegel: Hamburg, Germany, 2022; pp. 44–45. [Google Scholar]

- Ayompe, L.M.; Schaafsma, M.; Egoh, B.N. Towards sustainable palm oil production: The positive and negative impacts on ecosystem services and human wellbeing. J. Clean. Prod. 2021, 278, 123914. [Google Scholar] [CrossRef]

- Albert, C.; Hermes, J.; Neuendorf, F.; Von Haaren, C.; Rode, M. Assessing and Governing Ecosystem Services Trade-Offs in Agrarian Landscapes: The Case of Biogas. Land 2016, 5, 1. [Google Scholar] [CrossRef] [Green Version]

- Peters, D.; Ulber, R.; Wagemann, K. Bioraffinerien: Die deutsche Roadmap. Chem. Unserer Zeit 2014, 48, 46–59. [Google Scholar] [CrossRef]

- Geres, R.; Kohn, A.; Lenz, S.C.; Ausfelder, F.; Bazzanella, A.; Möller, A. Roadmap Chemie 2050: Auf dem Weg zu einer Treibhausgasneutralen Chemischen Industrie in Deutschland: Eine Studie von DECHEMA und FutureCamp für den VCI; DECHEMA Gesellschaft für Chemische Technik und Biotechnologie e.V: Frankfurt am Main, Germany, 2019; ISBN 978-3-89746-223-6. [Google Scholar]

- Zhang, C.; Xu, Y. Economic analysis of large-scale farm biogas power generation system considering environmental benefits based on LCA: A case study in China. J. Clean. Prod. 2020, 258, 120985. [Google Scholar] [CrossRef]

- Peters, M.S.; Timmerhaus, K.D.; West, R.E. Plant Design and Economics for Chemical Engineers, 5th ed.; McGraw-Hill: Boston, MA, USA, 2004; ISBN 978-0071240444. [Google Scholar]

- Woods, D.R. Rules of Thumb in Engineering Practice; John Wiley Distributor; Wiley-VCH: Chichester, UK; Weinheim, Germany, 2007; ISBN 978-3-527-31220-7. [Google Scholar]

- Green, D.W.; Southard, M.Z. Perry’s Chemical Engineers’ Handbook, 8th ed.; McGraw-Hill: New York, NY, USA, 2008; ISBN 0071422943. [Google Scholar]

- Lang, H.J. Simplified Approach to Preliminary Cost Estimates. Chem. Eng. 1948, 55, 112–113. [Google Scholar]

- Levi, P.G.; Cullen, J.M. Mapping Global Flows of Chemicals: From Fossil Fuel Feedstocks to Chemical Products. Environ. Sci. Technol. 2018, 52, 1725–1734. [Google Scholar] [CrossRef]

- Bazzanella, A.M.; Ausfelder, F. Low Carbon Energy and Feedstock for the European Chemical Industry: Technology Study; DECHEMA Gesellschaft für Chemische Technik und Biotechnologie e.V: Frankfurt am Main, Germany, 2017. [Google Scholar]

- Fleiter, T.; Rehfeldt, M. Langfristszenarien für die Transformation des Energiesystems in Deutschland 3: Treibhausgasneutrale Hauptszenarien; Modul Industrie: Karlsruhe, Germany, 2021. [Google Scholar]

- Agora Energiewende and Wuppertal Institute. Climate-Neutral Industry (Executive Summary): Key Technologies and Policy Options for Steel; Chemicals and Cement: Berlin, Germany, 2019. [Google Scholar]

- Dena. Leitstudie Integrierte Energiewende. 2018. Available online: https://www.dena.de/themen-projekte/projekte/energiesysteme/dena-leitstudie-integrierte-energiewende/ (accessed on 12 March 2022).

- Brandes, J.; Haun, M.; Wrede, D.; Jürgens, P.; Kost, C.; Henning, H.-M. Wege zu Einem Klimaneutralen Energiesystem: Die deutsche Energiewende im Kontext Gesellschaftlicher Verhaltensweisen. Update November 2021: Klimaneutralität 2045, Freiburg, Germany. 2021. Available online: https://www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/Fraunhofer-ISE-Studie-Wege-zu-einem-klimaneutralen-Energiesystem-Update-Klimaneutralitaet-2045.pdf (accessed on 1 March 2022).

- Robinius, M.; Markewitz, P.; Lopion, P. Kosteneffiziente und klimagerechte Transformationsstrategien für das deutsche Energiesystem bis zum Jahr 2050. Int. Nucl. Inf. Syst. 2020, 52, 161. [Google Scholar]

- Hehn, N.; Miosga, M. Die Zukunft der Windenergie in Bayern nach Einführung der 10 H-Regel. Inf. Zur Raumentwickl. 2015, 6, 97–109. [Google Scholar]

- Nieder, T. Auswertungstabellen zur Energiebilanz in Deutschland. 2021. Available online: https://ag-energiebilanzen.de/wp-content/uploads/2020/09/awt_2020_d.pdf (accessed on 1 March 2022).

- Chemie Technik. Linde Will Weltgrößte Wasserstoff-Elektrolyseanlage auf PEM-Basis in Leuna Bauen und Betreiben. Available online: https://www.chemietechnik.de/anlagenbau/linde-will-weltgroesste-wasserstoff-elektrolyseanlage-auf-pem-basis-in-leuna-bauen-und-betreiben-123.html (accessed on 30 December 2021).

- Smolinka, T.; Wiebke, N.; Sterchele, P.; Lehner, F.; Jansen, M. Studie: IndWEDe Industrialisierung der Wasser elektrolyse in Deutschland: Chancen und Herausforderungen für nachhaltigen Wasserstoff für Verkehr, Strom und Wärme; NOW GmbH: Berlin, Germany, 2018. [Google Scholar]

- Department of Forestry, Fisheries and the Environment. Minister Molewa Together with SASOL and Air Liquide. Inaugurate World’s First Largest Oxygen Production Plant in Secunda. Available online: https://www.dffe.gov.za/events/department_activities/molewa_sasolairliquide_oxygenplant_secunda#:~%7B%7D:text=Introduction%20and%20background%20Air%20Liquide%20recently%20started%20the,to%205%2C800%20tonnes%20per%20day%20at%20sea%20level%29 (accessed on 11 March 2022).

- Thyssenkrupp Industrial Solutions AG. Thyssenkrupp uhde Advanced Ammonia Processes dual Pressure. Available online: https://de.slideshare.net/tswittrig/thyssenkrupp-uhde-advanced-ammonia-processes-dual-pressure?from_action=save%20:Thyssenkrupp%20Uhde%20slides (accessed on 22 December 2021).

- de Klerk, A. Greener Fischer-Tropsch Processes for Fuels and Feedstocks; Klerk, A.D., Maitlis, P.M., Eds.; Wiley-VCH: Weinheim, Germany, 2013; ISBN 9783527329458. [Google Scholar]

- Riedewald, F.; Patel, Y.; Wilson, E.; Santos, S.; Sousa-Gallagher, M. Economic assessment of a 40,000 t/y mixed plastic waste pyrolysis plant using direct heat treatment with molten metal: A case study of a plant located in Belgium. Waste Manag. 2021, 120, 698–707. [Google Scholar] [CrossRef] [PubMed]

- Karpf, R.H.; Bergins, C. CO2 Abscheidung als Wertstoff-Rueckgewinnung: Eine Symbiose fuer die Umwelt? Müll Und Abfall 2016, 5, 05. [Google Scholar]

- Bellmann, E.; Zimmermann, P. Klimaschutz in der Beton- und Zementindustrie: Hintergrund und Hanglungsoptionen 2019; WWF: Berlin, Germany, 2019. [Google Scholar]

- Vereinigung der Fernleitungsnetzbetreiber Gas, e.V. Wasserstoffnetz 2050: Für ein klimaneutrales Deutschland. Available online: https://fnb-gas.de/wasserstoffnetz/h2-netz-2050/ (accessed on 7 January 2022).

- Statista. Chemisch-pharmazeutische Industrie: Energieverbrauch bis 2019|Statista. Available online: https://de.statista.com/statistik/daten/studie/203419/umfrage/energieverbrauch-in-der-chemisch-pharmazeutischen-industrie-in-deutschland/#:~:text=Die%20Statistik%20zeigt%20den%20Energieverbrauch%20in%20der%20chemisch-pharmazeutischen,Chemieindustrie%20Energie%20in%20H%C3%B6he%20von%20rund%20666.300%20Terajoule (accessed on 8 January 2022).

- Cesaro, Z.; Ives, M.; Nayak-Luke, R.; Mason, M.; Bañares-Alcántara, R. Ammonia to power: Forecasting the levelized cost of electricity from green ammonia in large-scale power plants. Appl. Energy 2021, 282, 116009. [Google Scholar] [CrossRef]

- Fahnestock, J.; Søgaard, K.; Lawson, E.; Kilemo, H. NoGAPS: Nordic Green Ammonia Powered Ships; Global Maritime Forum: New York, NY, USA, 2021. [Google Scholar]

- NuStar. Pipeline Transportation of Ammonia: Helping to Bridge the Gap to a Carbon Free Future. Available online: https://www.ammoniaenergy.org/wp-content/uploads/2021/11/AEA-Ammonia-Pipeline-Transportation-MEA-11-4-2021.pdf (accessed on 14 March 2022).

- Nigbur, F.E. Ammoniak-Cracker zur Brenngasversorgung von Brennstoffzellen. Ph.D. Dissertation, Universität Duisburg-Essen, Duisburg, Germany, 21 September 2021. [Google Scholar]

- Engbaek, J. Ammonia cracker for Hydrogen Generation for PEM Application, 2008. In Proceedings of the Annual NH3 Fuel Conference, Pittsburgh, PA, USA, 31 October 2018. [Google Scholar]

- Giddey, S.; Badwal, S.P.S.; Munnings, C.; Dolan, M. Ammonia as a Renewable Energy Transportation Media. ACS Sustain. Chem. Eng. 2017, 5, 10231–10239. [Google Scholar] [CrossRef]

- Myers, D.B.; Ariff, G.D.; James, B.D.; Lettow, J.S. Cost and Performance Comparison of Stationary Hydrogen Fueling Appliances. In Proceedings of the 2002 U.S. DOE Hydrogen Program Review, Golden, CO, USA, 6–10 May 2002. [Google Scholar]

- Asgari, M.; Snisi, H.; Mohammadi, H.; Sadighi, S. Designing a commercial scale pressure swing adsorber for hydrogen purification. Pet. Coal 2014, 56, 552–561. [Google Scholar]

- Kordesch, K.; Hacker, V.; Frankhauser, R.; Falschini, G. Ammonia Cracker for Production of Hydrogen. PCT/US01/41387, 25 July 2001. [Google Scholar]

- Rais, A. Is CCUS the Future of Decarbonizing the Industry? Process Worldwide [Online]. 7 March 2022. Available online: https://www.process-worldwide.com/is-ccus-the-future-of-decarbonizing-the-industry-a-1100698/ (accessed on 14 March 2022).

- Axens. Bio Olefins|Axens. Available online: https://www.axens.net/markets/renewable-fuels-bio-based-chemicals/bio-olefins#:~:text=Ethylene%20is%20one%20of%20the%20most%20important%20building,green%20route%20via%20catalytic%20dehydration%20of%20renewable%20ethanol (accessed on 5 January 2022).

- Koutinas, A.A.; Vlysidis, A.; Pleissner, D.; Kopsahelis, N.; Lopez Garcia, I.; Kookos, I.K.; Papanikolaou, S.; Kwan, T.H.; Lin, C.S.K. Valorization of industrial waste and by-product streams via fermentation for the production of chemicals and biopolymers. Chem. Soc. Rev. 2014, 43, 2587–2627. [Google Scholar] [CrossRef]

- Brosowski, A.; Adler, P.; Erdmann, G.; Stinner, W.; Thrän, D.; Mantau, U. Biomassepotenziale von Rest- und Abfallstoffen: Status Quo in Deutschland; Fachagentur Nachwachsende Rohstoffe e.V. (FNR): Gülzow-Prüzen, Germany, 2015; ISBN 978-3-942147-29-3. [Google Scholar]

- Kintscher, L.; Lawrenz, S.; Poschmann, H. A Life Cycle Oriented Data-Driven Architecture for an Advanced Circular Economy. Procedia CIRP 2021, 98, 318–323. [Google Scholar] [CrossRef]

- Kardung, M.; Cingiz, K.; Costenoble, O.; Delahaye, R.; Heijman, W.; Lovrić, M.; van Leeuwen, M.; M’Barek, R.; van Meijl, H.; Piotrowski, S.; et al. Development of the Circular Bioeconomy: Drivers and Indicators. Sustainability 2021, 13, 413. [Google Scholar] [CrossRef]

- Römer, F.; Goldmann, D. Reprocessing of a mining waste deposit in the Harz mountains—How contaminated sites might become raw material deposits in the future. Chemkon 2019, 26, 66–71. [Google Scholar] [CrossRef]

- Jensch, C.; Schmidt, A.; Strube, J. Versatile Green Processing for Recovery of Phenolic Compounds from Natural Product Extracts towards Bioeconomy and Cascade Utilization for Waste Valorization on the Example of Cocoa Bean Shell (CBS). Sustainability 2022, 14, 3126. [Google Scholar] [CrossRef]

- Jensch, C.; Strube, J. Proposal of a New Green Process for Waste Valorization and Cascade Utilization of Essential Oil Plants. Sustainability 2022, 14, 3227. [Google Scholar] [CrossRef]

- Schmidt, A.; Uhlenbrock, L.; Strube, J. Technical Potential for Energy and GWP Reduction in Chemical–Pharmaceutical Industry in Germany and EU—Focused on Biologics and Botanicals Manufacturing. Processes 2020, 8, 818. [Google Scholar] [CrossRef]

- Brauers, H.; Braunger, I.; Jewell, J. Liquefied natural gas expansion plans in Germany: The risk of gas lock-in under energy transitions. Energy Res. Soc. Sci. 2021, 76, 102059. [Google Scholar] [CrossRef]

- Kurmayer, N.J. Germany Signs Initial Contract to Build First LNG Terminal. EURACTIV [Online]. 7 March 2022. Available online: https://www.euractiv.com/section/energy/news/germany-signs-first-stage-contract-to-build-first-lng-terminal (accessed on 22 March 2022).

- Weiss, R. Germany Opens Door to Qatar Natural Gas in Pivot From Russia. Bloomberg [Online]. 20 March 2022. Available online: https://www.bloomberg.com/news/articles/2022-03-20/germany-reaches-deal-to-buy-qatari-gas-in-pivot-from-russia (accessed on 22 March 2022).

- Al-Breiki, M.; Bicer, Y. Comparative cost assessment of sustainable energy carriers produced from natural gas accounting for boil-off gas and social cost of carbon. Energy Rep. 2020, 6, 1897–1909. [Google Scholar] [CrossRef]

- Wang, Y. Energy Efficiency and Emissions Analysis of Ammonia, Hydrogen, and Hydrocarbon Fuels. J. Energy Nat. Resour. 2018, 7, 47. [Google Scholar] [CrossRef]

- Li, J.; Lai, S.; Chen, D.; Wu, R.; Kobayashi, N.; Deng, L.; Huang, H. A Review on Combustion Characteristics of Ammonia as a Carbon-Free Fuel. Front. Energy Res. 2021, 9, 822. [Google Scholar] [CrossRef]

- Kurata, O.; Iki, N.; Fan, Y.; Matsunuma, T. Pure Ammonia Combustion Micro Gas Turbine. In Proceedings of the 2019 AIChE Annual Meeting, Orlando, FL, USA, 10–15 November 2019. [Google Scholar]

- German National Academy of Sciences Leopoldina; Union of the German Academies of Sciences and Humanities e. V. Centralized and Decentralized Components in the Energy System: The Right Mix for Ensuring A Stable and Sustainable Supply; Laser Line GmbH: Berlin, Germany, 2020; ISBN 978-3-8047-4061-7. [Google Scholar]

- Uniper Plans to Make Wilhelmshaven a Hub for Climate friendly Hydrogen. Uniper [Online]. 14 April 2021. Available online: https://www.uniper.energy/news/uniper-plans-to-make-wilhelmshaven-a-hub-for-climate-friendly-hydrogen (accessed on 27 April 2022).

- GETEC unterzeichnet Abkommen für die Nutzung von Sauberem Wasserstoff aus den VAE|CHEManager. Available online: https://www.chemanager-online.com/news/getec-unterzeichnet-abkommen-fuer-die-nutzung-von-sauberem-wasserstoff-aus-den-vae (accessed on 27 April 2022).

- Göbelbecker, J. Getec Unterzeichnet Kooperationsabkommen für Grünen Wasserstoff. CHEMIE TECHNIK [Online]. 22 March 2022. Available online: https://www.chemietechnik.de/energie-utilities/getec-unterzeichnet-kooperationsabkommen-fuer-gruenen-wasserstoff-161.html (accessed on 22 March 2022).

- Mitsubishi Power. Mitsubishi Power|Mitsubishi Power Commences Development of World’s First Ammonia-fired 40 MW Class Gas Turbine System—Targets to Expand Lineup of Carbon-free Power Generation Options, with Commercialization around 2025. Available online: https://power.mhi.com/news/20210301.html (accessed on 18 March 2022).

- Institute for Sustainable Process Technology. Power to Ammonia: Feasibility Study for the Value Chains and Business Cases to Produce Co2-Free Ammonia Suitable for Various Market Applications. 2017. Available online: https://www.topsectorenergie.nl/sites/default/files/uploads/Energie%20en%20Industrie/Power%20to%20Ammonia%202017.pdf (accessed on 18 March 2022).

- Ammonia Cracker. Available online: https://samgasprojects.com/detail/ammonia-cracker.html (accessed on 18 March 2022).

- Luedicke, R. Ammonia Cracker, Hydrogen Generator. Available online: https://www.crystec.com/kllhyame.htm (accessed on 18 March 2022).

- Projekt NH3toH2. Available online: https://www.uni-due.de/energietechnik/de/pro_nh3toh2 (accessed on 18 March 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Plant (Product) | Capacity (kt/a) | Power Usage (MWh/t) | CAPEX (€/t) | |||

|---|---|---|---|---|---|---|

| Electrolysis (H2) | 3.9 | [30] | 51.6 | [15] | 2461.5 | [31] |

| Air Separation (N2) | 3240 | [32] | 0.185 | [15] | 61.7 | [32] |

| Haber-Bosch (NH3) | 1645 | [33] | 1.72 | [15] | 588 | [15] |

| Fischer-Tropsch (Naphtha) | 850 | [34] | 0.83 | [15] | 2398.8 | [34] |

| Pyrolysis (Naphtha) | 40 | [35] | 3.11 | [15] | 500 | [35] |

| Electric Cracker (HVC) | 4.86 | [15] | 250 | [15] | ||

| Urea (Urea) | 0.97 | [15] | 100 | [15] | ||

| Electrolysis (Cl2) | 2.39 | [15] | ||||

| Fischer-Tropsch (MeOH) | 1.50 | [15] | 1607 | [15] |

| CAPEX (bn. €) | Scenario A | Scenario B | Scenario C |

|---|---|---|---|

| German Plants | |||

| Electrolysis | 26.2 | 24.9 | |

| Air Separation | 0.2 | ||

| Haber Bosch | 1.9 | ||

| Ammonia Cracker | 3.9 | ||

| CCU | 6.5 | 6.5 | 6.5 |

| Others | 39.69 | 39.69 | 39.69 |

| Total | 74.49 | 71.09 | 50.09 |

| MENA Plants | |||

| Electrolysis | 60.8 | 29 | |

| Air Separation | 7.4 | 3.4 | |

| Haber Bosch | 84.1 | 39.7 | |

| Total | 152.3 | 72.1 | |

| Pipelines and Transportation | |||

| Hydrogen | 18 | 18 | 18 |

| Carbon Dioxide | 2.5 | 2.5 | 2.5 |

| Ammonia | 7.4 | 7.4 | |

| Ammonia Ships | 9.4 | 4.4 | |

| Total | 20.5 | 37.3 | 32.3 |

| Total | 94.99 | 260.69 | 155.49 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Uhl, A.; Schmidt, A.; Jensch, C.; Köster, D.; Strube, J. Development of Concepts for a Climate-Neutral Chemical–Pharmaceutical Industry in 2045. Processes 2022, 10, 1289. https://doi.org/10.3390/pr10071289

Uhl A, Schmidt A, Jensch C, Köster D, Strube J. Development of Concepts for a Climate-Neutral Chemical–Pharmaceutical Industry in 2045. Processes. 2022; 10(7):1289. https://doi.org/10.3390/pr10071289

Chicago/Turabian StyleUhl, Alexander, Axel Schmidt, Christoph Jensch, Dirk Köster, and Jochen Strube. 2022. "Development of Concepts for a Climate-Neutral Chemical–Pharmaceutical Industry in 2045" Processes 10, no. 7: 1289. https://doi.org/10.3390/pr10071289

APA StyleUhl, A., Schmidt, A., Jensch, C., Köster, D., & Strube, J. (2022). Development of Concepts for a Climate-Neutral Chemical–Pharmaceutical Industry in 2045. Processes, 10(7), 1289. https://doi.org/10.3390/pr10071289