4.1. Determinants of Exchange Rate Volatility

As the Jarque-Bera test implies non-normal error distribution for ∆

et, we use EGARCH(1,1) models with the asymmetric Student’s t-distribution. Estimates of the baseline model are presented in

Table 3. Among determinants of the mean exchange rate, the interest rate differential is associated with depreciation for three out of four countries, being in line with the logic of Equation (3). However, the relationship for Romania is just the opposite. As for the lagged terms-of-trade, there is no evidence of a direct link between higher domestic prices and depreciation. For the Czech Republic, Poland, and Romania, there is an inverse relationship between both variables. Contrary to predictions of

Corsetti et al. (

2017), deflation abroad does not lead to depreciation of the exchange rate.

The ARCH term () indicates that impact of “surprises” from previous periods is the strongest in the Czech Republic and Poland (higher than one implies that shocks to exchange rate can destabilize its volatility), with a much weaker effect in Hungary and Romania. Based on the value of the EGARCH term (), persistence of exchange rate volatility is observed at the statistically significant level in the Czech Republic only. As indicated by the sum of α and β, the speed of convergence of the forecast of the conditional volatility to a steady state is very slow in the Czech Republic and Poland. The standardized shocks to are symmetrical in Poland, as the value of is not statistically different from zero. For the Czech Republic and Romania, the negative value of implies that negative news affects the exchange rate volatility more heavily than positive news. It is just the opposite in Hungary. No preconditions for leverage are met in any country.

Among the control variables, inflation contributes to exchange rate volatility in the Czech Republic and Romania, though with opposite signs. There is no difference between all four CEE countries in that crisis developments are associated with higher exchange rate volatility.

In the extended model (

Table 4), a statistically significant direct relationship between the lagged terms-of-trade and mean exchange rate emerges in Hungary. The ARCH effect somewhat decreases in Poland and Romania, with the opposite outcome observed in the Czech Republic and Hungary. As suggested by the value of

β, there are no changes to the assessment of persistence in exchange rate volatility in the Czech Republic. However, exchange rate variability becomes more persistent in Hungary. Considering the sum of ARCH and EGARCH coefficients, a control for institutional features implies a significantly slower speed of convergence of the forecast of the conditional volatility to a steady state in Hungary. For other countries, changes are rather marginal. Asymmetry of the standardized shocks to

is confirmed for Hungary and Romania, while the negative coefficient of

becomes insignificant for the Czech Republic. Among other changes, inflation becomes a factor behind lower exchange rate volatility in Hungary. Except the Czech Republic, the coefficient of

becomes significantly lower for other countries.

As suggested by the estimated coefficients on sub-indices of economic freedom, in a more liberal environment exchange rate volatility becomes lower. The only exception is Hungary, where monetary freedom brings about a higher exchange rate volatility. On the whole, the effects of economic freedom on exchange rate volatility are country specific. Property rights guarantees decrease exchange rate volatility in Romania. Fiscal health exerts the same effect on volatility in Hungary. Success in anticorruption activities contributes to a lower exchange rate volatility the Czech Republic and Poland. In the extended model, inflation becomes a volatility-decreasing factor in Poland, with a positive coefficient on changing sign. No changes in the effects of crisis developments are observed.

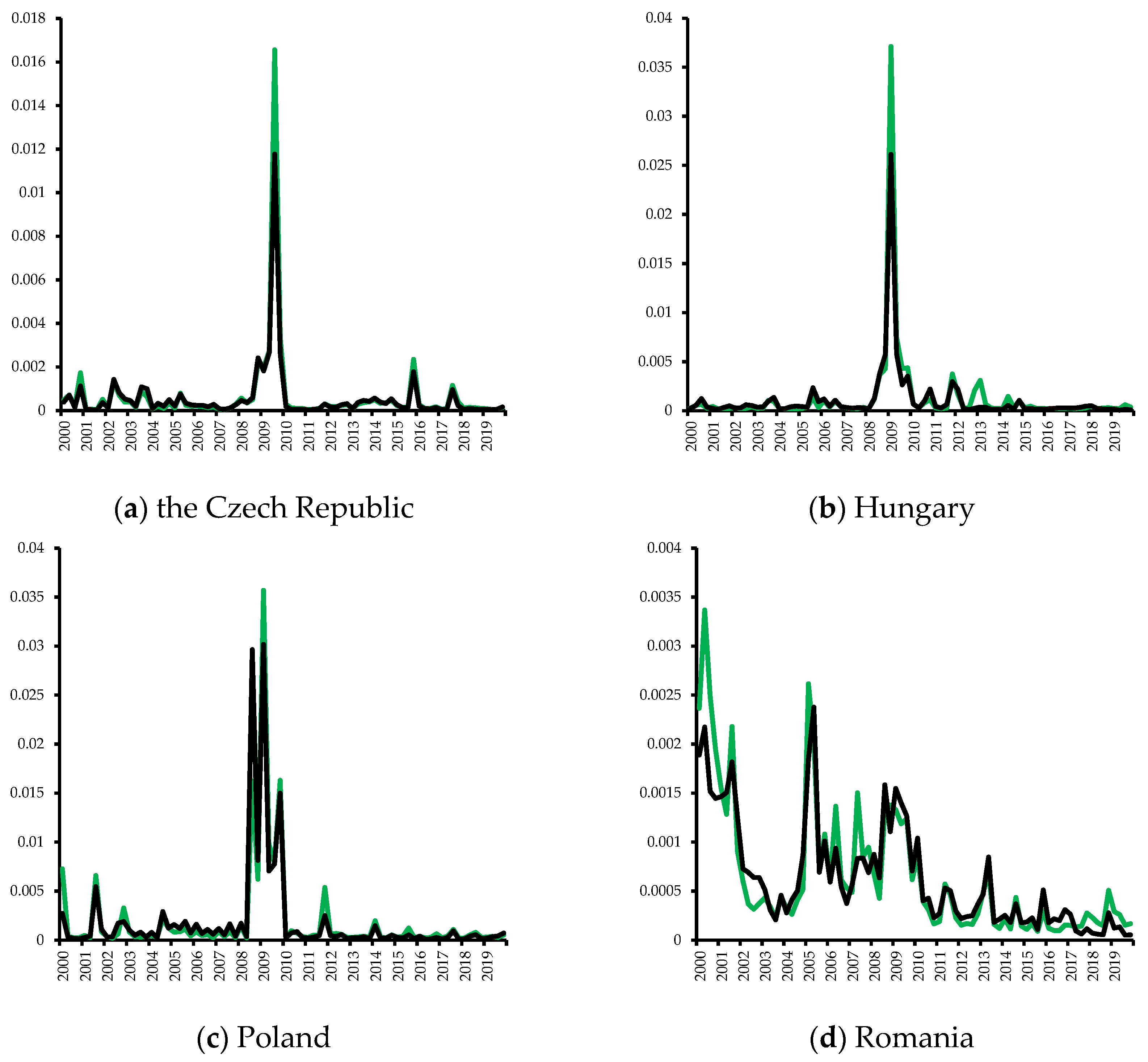

Figure 2 plots the evolution of quarterly exchange rate volatility by country, with the conditional variation obtained by fitting the baseline and extended EGARCH(1,1) models in green and black colors, respectively. For all countries, periods of low volatility are followed by periods of high volatility which could be associated with periods of global financial crisis of 2008–2009 and/or domestic financial turmoil (the Czech Republic in 2001–2002, Hungary in 2012–2013, Romania in 2004–2005). Differences between two measures of exchange rate volatility seem to be quite small in the Czech Republic and Hungary, while being more pronounced in Poland and Romania. After controlling for the institutional features, volatility becomes somewhat smaller. Except Romania, the exchange rate volatility rose from the beginning of 2007, with a peak during the world financial crisis of 2008–2009. Volatility then subsided in the majority of CEE countries, except Hungary in 2012–2013. For Romania, there is an increase in volatility around 2005 that is followed by a smaller jump in 2008–2009.

To summarize, volatility patterns of the CEE countries seem to be similar in respect to both ARCH and EGARCH effects, especially after controlling for the institutional features. However, there are differences in asymmetry of volatility shocks and effects of control variables. In that respect, our results do not reject that volatility in the CEE economies has country-specific features (

Kočenda and Valachy 2006).

4.2. Determinants of the Business Cycle

We estimate Equation (3) with the general method of moments (GMM) estimator. Comparing with OLS or IV estimators, the GMM method is preferred for better dealing with problems of simultaneity bias, reverse causality, and omitted variable bias, as well as for obtaining estimates of dummy coefficients (

Caporale et al. 2011).

Table 5 presents the results for the baseline model of cyclical components of real output.

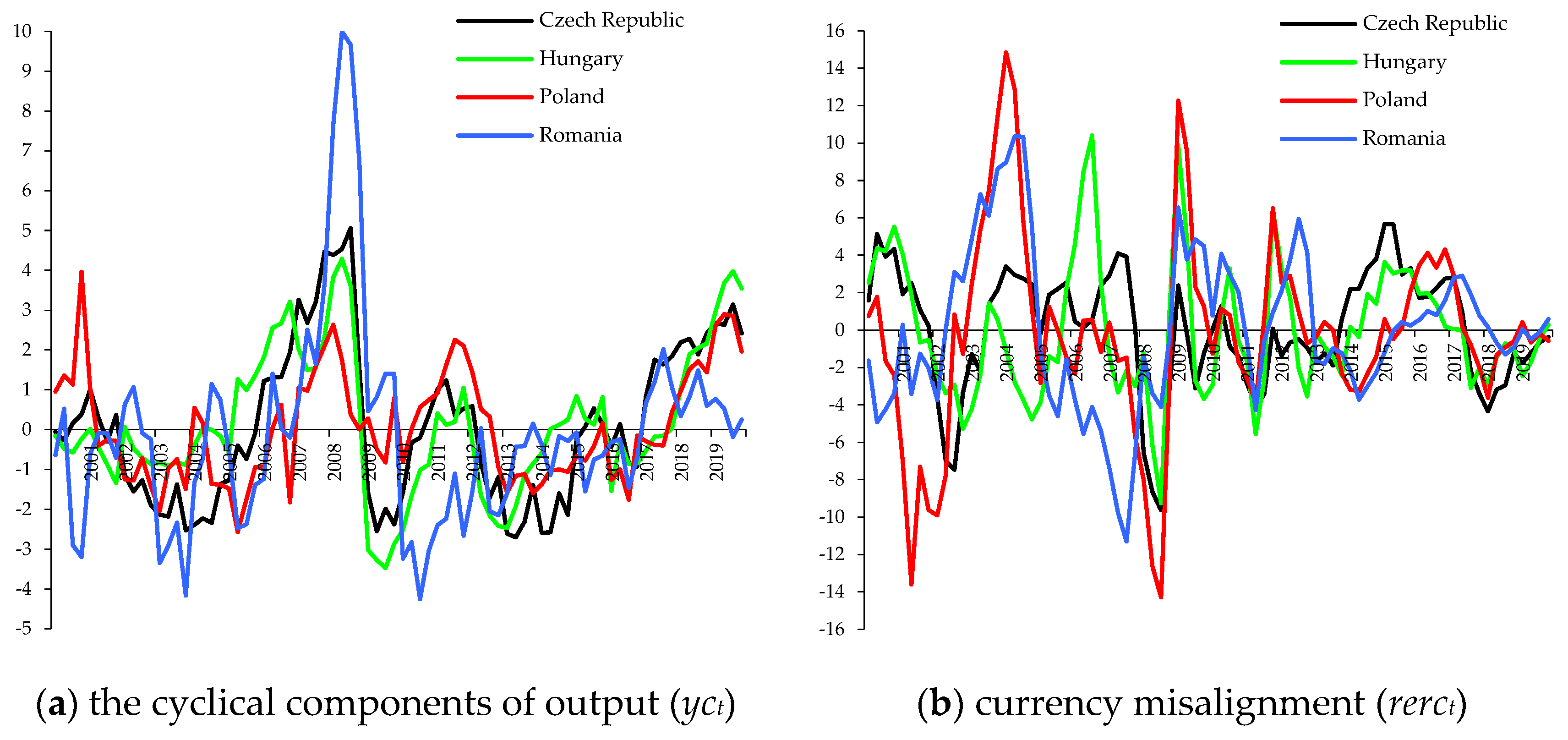

For all countries, coefficients on the lagged dependent variable are significant at the 1% level. Inertia of cyclical developments in output is stronger in Hungary and Romania. These two countries are characterized by the lowest correlation with the business cycle of the Eurozone as well. Correlation between national and European business cycles is the strongest in the Czech Republic.

According to the estimates of the baseline model, exchange rate volatility is associated with the risk of recession only in Hungary. An opposite effect is obtained for the Czech Republic. Exchange rate volatility is neutral in respect to the cyclical output developments in Poland and Romania. Such findings can be considered as evidence in favor of the exchange rate disconnect. However, neutrality of output fluctuations in respect to exchange rate volatility does not mean the same lack of reaction to currency misalignment. Exchange rate undervaluation has favorable growth effects in Poland. Assuming that there is exchange rate depreciation in response to such real shock as an increase in the foreign interest rate (

Table 3 and

Table 4), it helps to stabilize the economy. Under such architecture of the exchange rate effects, a switch to free or managed floating looks like a reasonable exchange rate policy. In a wider context, our results imply that the Czech Republic and especially Poland both benefit from exchange rate flexibility and thus may not be interested in joining the Eurozone. However, such benefits are visible for Hungary, as the exchange rate volatility seems to be destabilizing. Among numerous explanations of the inverse relationship between exchange rate volatility and output, several ones are worth attention in the case of Hungary, such as higher risk premium, greater uncertainty about export revenues, higher risk for domestic and foreign direct investment, and adverse effect of credit constraints on domestic investments. Additionally, it is not ruled out that in a country with relatively low levels of financial development (real) exchange rate uncertainty exacerbates the negative investment effects of domestic credit market constraints (

Aghion et al. 2009) or reflect disincentives for firms in creating jobs (

Belke and Setzer 2003).

There is no evidence of any favorable stabilization effects of economic freedom. A negative effect is the strongest for the Czech Republic, followed by Poland and Hungary. For Romania, a negative coefficient of heritt is insignificant. It is likely that our findings reflect an excessive level of economic liberalization attained during the period of negotiations with the European Union on the terms of EU accession. While the level of economic freedom is negatively correlated with cyclical fluctuations in output, changes in the level of economic freedom are neutral in respect to yct.

Trade deficit is still an important factor behind economic growth in Hungary, Romania, and Poland (to lesser extent). Our results mean that economic recovery depends more on imports, not exports. In this context, traditional supply-side trade channels, as capital accumulation, modernization of industrial structure, and technological and institutional progress, seem to be relevant. As can be seen in the example of the Czech Republic and Poland, statistical significance of the coefficient on tradet−1 depends on the choice of the exchange rate variability.

The stimulating effect of the EU accession is the strongest in the Czech Republic, followed by Hungary. For Poland, the coefficient of EUt is much smaller and statistically significant at the 10% level only in specification with . No evidence of any EU accession effects is found for Romania.

After controlling for fiscal and monetary policies (

Table 6 and

Table 7), there are no changes in the assessment of exchange rate effects for Poland and Romania. For the Czech Republic, effects of exchange rate volatility on

yct are confirmed but the same favorable effect of the RER undervaluation emerges in the specification with the money supply. Similar stimulating effect of the RER undervaluation is found for Hungary, although only in specification with

. It is confirmed that exchange rate volatility contributes to a recession in Hungary.

A negative link between economic freedom (in levels) and business cycle is very robust for the Czech Republic, while the estimates for other countries are specification dependent. For Hungary, economic freedom becomes neutral in respect to cyclical developments in output in 3 out of 4 specifications. It is just the opposite for Romania, where a statistically significant negative link between heritt and yct emerges in specifications with both moneyct and rcbt. Additionally, Romania emerges as the only CEE country with a statistically significant positive effect of an increase in economic freedom (in first differences) on output. For Poland, a negative relationship between heritt and yct disappears in specification with moneyct, while being strengthened in the specification with rcbt.

An excessive money supply,

moneyct, helps to stabilize output in the Czech Republic and Poland. Assuming a link between the money supply and exchange rate volatility (

Devereux and Engel 2002), it only strengthens the assumption of shock-absorbing properties of the floating exchange rate regimes for the Czech

koruna and Polish

zloty.

An increase in the central bank reference rate acts in the expected countercyclical manner in Hungary, while counterintuitive proportional link between

rcbt and

yct is observed in Poland. It is possible to hypothesize that such an outcome results from efforts by the central bank to avoid appreciation of the exchange rate. As a higher central bank rate can tap capital inflows, sterilization policies substitute a stronger currency with a higher excessive money supply that ultimately becomes responsible for an increase in output. For Romania, it is likely that the lack of sensitivity to the central bank policy rate is explained by the balance sheet effect, as argued by

Georgiadis and Zhu (

2019).

For the Czech Republic and Romania, there is evidence of stabilization properties of the fiscal tightening. The so-called non-Keynesian effects of fiscal policy mean that in the case of recession it is necessary to improve the budget balance, not engage in rounds of fiscal stimuli, as has been the case in many industrial countries since the world financial crisis of 2008–2009.

When the extended dataset is used (using both fiscal and monetary variables), there are several changes to the assessment of trade and EU accession output effects. A negative link between tradet−1 and yct is confirmed for Hungary and it becomes more stable for the Czech Republic. As for Poland and Romania, a negative impact of the trade balance is observed in specifications with moneyct, but the effect is lost in specifications with rcbt. A strong procyclical effect of entering the EU is confirmed for the Czech Republic and Hungary. For Poland, a stimulating effect of similar amplitude emerges in the specification with rcbt, although it is not observed in the specification with moneyct.

{kind=link}

{kind=link}