1. Introduction

Deregulation of energy markets started in the early 1990s, with the main aim being making energy markets more efficient and reducing costs for the consumer (see

Al-Sunaidy and Green (

2006) for a detailed discussion on the history of deregulation). Today, energy is traded under free market conditions in many countries, and energy prices show characteristics that are rarely seen in other markets. These are, for example, seasonal effects, jumps with fast mean-reversion, and negative prices, and a large number of models have been produced in the recent years in order to capture those features and investigate their structure; see, among many others,

Borovkova and Schmeck (

2017);

Fanelli and Schmeck (

2019);

Genoese et al. (

2010);

Kaminski (

2013);

Kiesel et al. (

2009), as well as the recent review

Deschatre et al. (

2021).

Considerations involving the law of demand and supply can explain the presence in electricity prices of seasonal patters at different scales: Prices are typically higher during the morning and evening hours of the days, and—especially in countries where heating is performed via electricity—also in winter months. Since these seasonal patterns are predictable, they can be well described through deterministic time-dependent functions, such as a combination of different sinusoidal functions (

Escribano et al. 2011). Energy prices show very high volatility with jumps, which can be explained by the fact that energy cannot be stored on a large scale, at least in an economically feasible way. Furthermore, a large energy supply combined with a low demand leads electricity prices also to become negative, a feature allowed since 2008 by the European Energy Exchange. As a matter of fact, in periods of overproduction a shut down of the power plants would cost the energy producers more than paying for getting rid of energy.

From a mathematical point of view, there are clearly various modeling choices for electricity spot prices; see the reviews

Weron (

2014) and

Deschatre et al. (

2021) for an outlook on the state of the art and future perspectives. Following the seminal work by

Benth et al. (

2007), in this paper we choose to work with a (nowadays classical) multi-factor spot price model consisting of a non-stationary process and a sum of independent Ornstein-Uhlenbeck processes, driven by a suitable stochastic jump process. Namely, we take the spot price of electricity given by

for some index-set

J. Here,

is a deterministic seasonality function,

X is an arithmetic Brownian motion that reflects long term expectations, e.g., of political developments, and each

is a mean-reverting process, that converges back to the seasonal equilibrium level

. On the one hand, as we shall see also in this paper, this modeling choice is still simple enough to enable for explicit evaluations of electricity contracts (like futures and forward contracts). On the other hand, Equation (

1) allows to reproduce the well-known stylized fact for which electricity prices exhibit large price shocks (spikes), which mean revert very fast towards the original price level, as well as slower mean reverting components. As a matter of fact,

Meyer-Brandis and Tankov (

2008) find that the majority of European exchanges show an auto-correlating structure of the spot prices that can be well described by a models including a sum of mean reverting processes, where the mean reversion takes place with different rates. In particular,

Meyer-Brandis and Tankov (

2008) argue that two or three mean reverting factors are suitable to reproduce prices in the EEX.

However,

Ball and Torous (

1983) and

Knittel and Roberts (

2001), among others, also point out the difficulty of calibrating a multi-factor spot price model as in Equation (

1) to market data. Indeed, the question arises of how to filter from the observed time series the different, themselves not observable, components. It is therefore natural to investigate which is the error that one makes by neglecting some or all of the mean-reverting processes in the spot price model. In particular, if such an error is shown to be relatively small, then it might not be worth to provide the nontrivial calibration of a full jump model of electricity prices. In this paper we interpret such a question by comparing the price of vanilla options on swaps in two models for

S. In a first one all the

mean-reverting components are considered, and in a second one only

jump Ornstein-Uhlenbeck processes are considered. Our main result gives an analytical estimate of the pricing error by showing that the difference in the price of call options on swaps for the two models can be bounded from above and below by explicitly calculated quantities. These depend on the models’ parameters, such as the volatility parameters, the speeds of mean-reversion, and the delivery period in the swap pricing formula. We show that when the delivery period is sufficiently large, then the pricing error goes to zero. This is because the swap averages out the effects that spikes have on the call option price. We thus conclude that for sufficiently long delivery periods, considering a relatively less complex spot price model provides a good approximation to the more complex one. Our theoretical analysis is then illustrated by numerical examples. Here we show the effect of the mean-reverting components and of the volatility

of the non-stationary component on the price of call options. In particular, we confirm that for relatively large delivery periods of the swap contract the pricing error is negligible. Furthermore, we observe that the smaller

is, the larger becomes the pricing error.

Our study is related to the one performed in

Benth and Schmeck (

2014) and

Schmeck (

2016) (see also

Nomikos and Soldatos (

2010) for a study of the importance of mean reversion and spikes in the stochastic behavior of the underlying asset when pricing options on power). The main difference between

Benth and Schmeck (

2014) and

Schmeck (

2016) and our paper lie in the structure of the dynamics of the spot price process. These are geometric in

Schmeck (

2016), while arithmetic in this work. The choice of considering an arithmetic model has essentially two main reasons. First of all, arithmetic dynamics allow to encompass the observed negativity of spot prices of electricity. The importance of taking into account such a stylized fact of electricity prices in the modeling is also confirmed by the increasing interest that arithmetic models are recently obtaining in the literature (see, e.g.,

Benth et al. 2019;

Edoli et al. 2017;

Fanone et al. 2013;

Hinderks and Wagner 2020;

Latini et al. 2019;

Piccirilli et al. 2021). Second of all, using arithmetic models one can obtain explicit closed form formulas for the price of the swap price, given by the time-average of the spot price over the delivery period. This is not possible for geometric models, such that

Benth and Schmeck (

2014) and

Schmeck (

2016) approximate the delivery period by its midpoint.

The rest of this paper is organized as follows. In

Section 2 we provide the spot price dynamics and derive the dynamics of the swap price. In

Section 3 we then determine the price of the call option on the swap, which is then employed in

Section 4 in order to estimate the pricing error obtained by neglecting jump mean-reverting components in the spot price evolution. Finally,

Section 5 illustrates the theoretical analysis by numerical examples.

3. Pricing a Call Option on the Swap

In this section, we are going to calculate the fair price of a call option that is written on a swap. Notice that such a pricing can be performed under the measure

used for pricing the swaps. Indeed, from the very definition Equation (

6), as well as from the fact that the compensated jump process

in Equation (

8) is a

-martingale, we can see that the swap price is a

-martingale.

Because in

Section 4 we shall study the effect of mean-reversion components on a call option price that is written on a swap

F, it is useful from now on to stress that the spot and swap prices depend on these mean-reverting components. This is done in the following way: For any index set

, with cardinality

, we parametrize the swap price and spot price by

L by assuming that only

of the mean-reverting components

in Equation (

2) affect the dynamics of the spot price, and we write

Then, we define accordingly

and the fair price at time

of a call option with maturity

, underlying

, and strike price

, is

Here

is a given and fixed interest rate. Clearly,

as in Equation (

6) and

as in Equation (

2).

By using the dynamics of the swap Equation (

8) and Itô’s lemma, we can simply rewrite

as

with

From Equation (

12)

can be decomposed as

where the continuous part

is defined as

while the jump component is

It is clear that

. On the other hand, by Itô’s isometry and the independence of the Brownian motions one obtains

where we have set

These distributional properties of will be used in the next theorem, which provides a formula for the fair price of the considered call option. Throughout the rest of this paper, denotes the cumulative standard normal distribution function.

Theorem 3. Let and . Let the spot price be given as in Equation (9) and the swap be defined by Equation (10). Then, the fair price of the call option as in Equation (11) is given by Proof. By combining Equations (

11) and (

12), we find

with

given as in Equation (

20) and

defined through Equation (

13). Because the stochastic integrals are independent of

we obtain from the latter

Define now

and, recalling Equation (

14)

Then, by the tower property and the assumed independence of the Brownian motions with respect to the Poisson processes, we can write from Equation (

22)

In order to complete the proof it thus remains only to evaluate

of Equation (

24). Denoting by

Z a random variable with standard Normal distribution, and recalling that

(Equations (

14) and (

16)) we find

Then, standard calculations lead for any

to

where we have set

By feeding Equation (

26) back into Equation (

25) and rearranging terms, one easily derives Equation (

18). □

Considerations on the Effect of the Jump Components’ Volatilities

Notice that the expression of the call price in Equation (

18) is consistent with the classical fair pricing formula in the Bachelier model, as expected (see

Musiela and Rutkowski (

1997) for a review of the Bachelier model). The main difference lies in the fact that the coefficient

in Equation (

18) depends on the jump-components of the spot price dynamics. However, from Equation (

18) it is not clear how those jump factors affect the pricing formula. In order to get a feeling for that, we now perform a Taylor expansion of the term

around the point

That is, we are assuming that the term

is sufficiently small. Then

where the remainder is given by

Such an approximation gives

Here, we have used the martingale property of

to have

. Furthermore, defining

and employing Equation (

20) we have calculated

By inserting Equation (

30) into Equation (

18), we find

By a rough consideration that does not take into account the remainder, the last formula shows that a larger volatility of the jump components of the spot price (i.e., a larger

) implies a larger call price. From Equation (

32) we also observe that the more jump-components are considered (i.e., the larger

is), the larger is

, and therefore the larger is the call option’s price. This argument will be made precise in the next section, where we investigate how the call option’s price is affected by the number of mean-reverting jump processes in the spot and the swap price.

4. The Effect of Mean-Reverting Jump Processes on the Call Option Price

In this section, we push forward the discussion made at the end of the previous section and we study in detail the role that the mean-reverting components of the spot price play on the price of the call option. We start from the implicit assumption that the call option price

(defined as in Equation (

11) with

J instead of

L) provides the most precise representation of the actual price of the contingent claim. By considering in Equation (

2) only

of the mean-reverting processes, our model becomes less accurate but at the same time easier to handle (e.g., for parameter estimation). To quantify the resulting pricing error, we are going to estimate from above and below the difference

.

Before doing that we need the following simple lemma, whose proof is immediate.

Lemma 1. Recall Equations (16) and (17). Then for any subset we have that Furthermore, for , Hence, for delivery periods that are sufficiently large (i.e.,

), the previous lemma provides simple bounds on the volatility arising in the continuous part of the swap price. The following result provides an upper and a lower bound for the pricing error

, and for its proof Equation (

35) will be used. We shall also assume that at the initial time

t the swap price is observed, and it is equal for both models with

or

mean-reverting components; that is,

. Moreover, following

Schmeck (

2016), we require that

is constant, meaning that

has to be chosen accordingly in a delivery-period-dependent form. This condition enforces that call options with different delivery periods are comparable.

Theorem 4. Let and assume that . Furthermore, let and suppose also that is constant for all delivery periods. Recall , , and as defined in Equations (17), (31) and (34) respectively, and define Note that we aim at determining a lower and upper error depending on the delivery period . Therefore, for fixed time t and exercise time of the option the expressions can indeed be interpretated as constants .

Proof. The proof is organized in several steps. Throughout this proof, we let , , and and be given and fixed times satisfying and . Furthermore, when needed, denotes an index set such that .

Step 1. For

, and

let

and define

Then, for

with

as in Equation (

20), we have

and

Step 2. We now want to evaluate the derivatives of

with respect to its arguments. By explicit computations using that

and

one obtains

Recalling also that

, one finally finds

Similar computations employing that

and

also yield

Since

is clearly a continuously differentiable function for all

and

, we can apply the mean value theorem and find an

such that

where

has components

Note that per definition

(see Equation (

16)).

Step 3. With regards to Equation (

41), we here determine bounds for

.

Notice that, given the independence of

and

, by the “freezing lemma” of conditional expectations, we can write

However,

is an increasing function and it is well known that two comonotonic random variables have nonnegative covariance. Hence, we obtain from Equation (

42)

In order to determine an upper bound for

we perform a Taylor expansion. To this end, recall

, so that

for some rest

.

From Equation (

35) we know that

for

. Now, because

,

and

are independent, and

, we obtain that

Then, plugging Equation (

46) into Equation (

44), yields

Hence, to conclude with the estimate of the left-hand side of the latter, we need to control for the expectation involving the remainder term

. In order to accomplish that, observe that

Then, since

, the definition of

and the fact that

, yield

where we have used that

in the last step.

By combining Equations (

47) and (

48), it follows that

Step 4. With regards to Equation (

41), we here determine bounds for

. By employing Equation (

40) we have

By using Equation (

35) we then find

On the other hand, Equation (

35), Jensen’s inequality, the independence of

and

, and the fact that

, give

Hence, from the previous estimates we obtain

where we recall that

Step 5. By Equations (

43), (

49) and (

53), the claimed result follows from Equation (

41), upon using

and

as in Equations (

16) and (

32), respectively, and defining analogously

and

. □

The previous theorem shows that for sufficiently large delivery periods the pricing error becomes smaller. As a matter of fact,

This means that for long delivery periods, considering a simpler model with only a few of the mean-reverting jump components leads to a negligible error. Clearly, such a result is consistent with the fact that the swap price averages out the effect of the jump processes affecting the spot price. Since on the European Energy Exchange (

Options Trading at EEX 2018), delivery periods are usually at least one month long—i.e.,

in our framework—Theorem 4 provides a quantitative estimate that might be useful also for practical purposes.

It is also interesting to notice that large values of reduce the pricing error. This can be explained by noticing that a large makes the jump spikes relatively not influential, as the Brownian process B plays then the role of the leading factor for the evolution of the spot and swap prices.

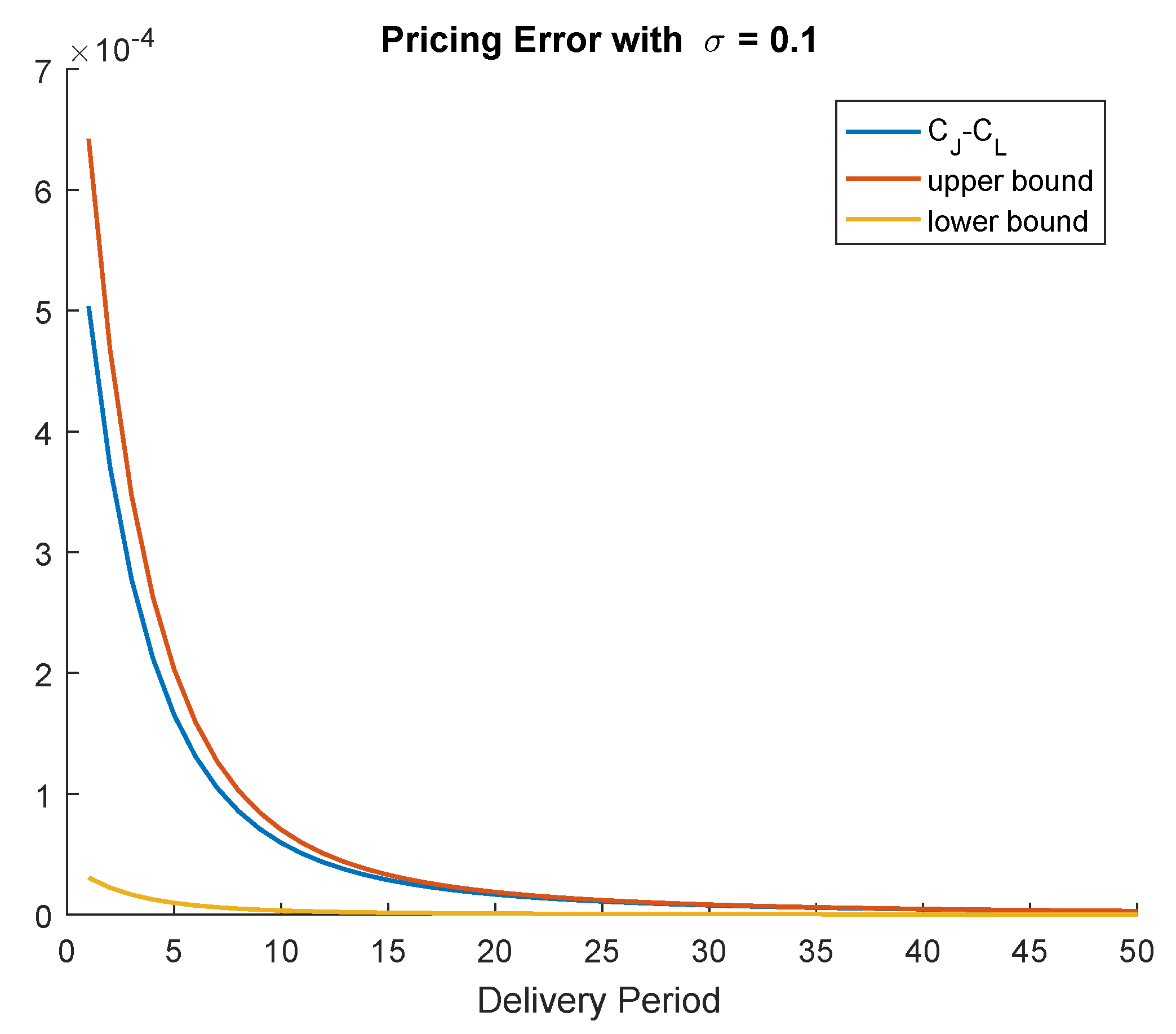

5. Numerical Illustration

In this section, we provide an illustration of the theoretical findings collected in Theorem 4. We consider the simplest example possible, by taking and , we plot the error bounds obtained in Theorem 4 as functions of the delivery period, and we show the convergence of to zero when the delivery period becomes sufficiently large.

Bearing in mind the spot price model from

Section 2, we now compare two specifications of this model. In the first model, we set

, meaning that the spot price is described by

with the drifted Brownian Motion

and two Brownian Ornstein-Uhlenbeck processes

Furthermore, for the second model, set ; that is, we consider the first Ornstein-Uhlenbeck process only.

The parameters

are all constant, and given by

,

,

for all

. The values of

and

are chosen as in

Schmeck (

2016); that is,

is the fast mean-reversion rate, while

is the slower one. We consider options at the money, that is

. Finally, we set

, for simplicity, the maturity of the option is

, and the delivery period starts four days later (see

Options Trading at EEX 2018).

Figure 2 shows the pricing error that is made by using the above parameters. As our theoretical analysis proved, the error vanishes for long delivery periods. Here, we can see that the upper bound better fits the actual pricing error. However, the lower bound is quite far away from the actual error.

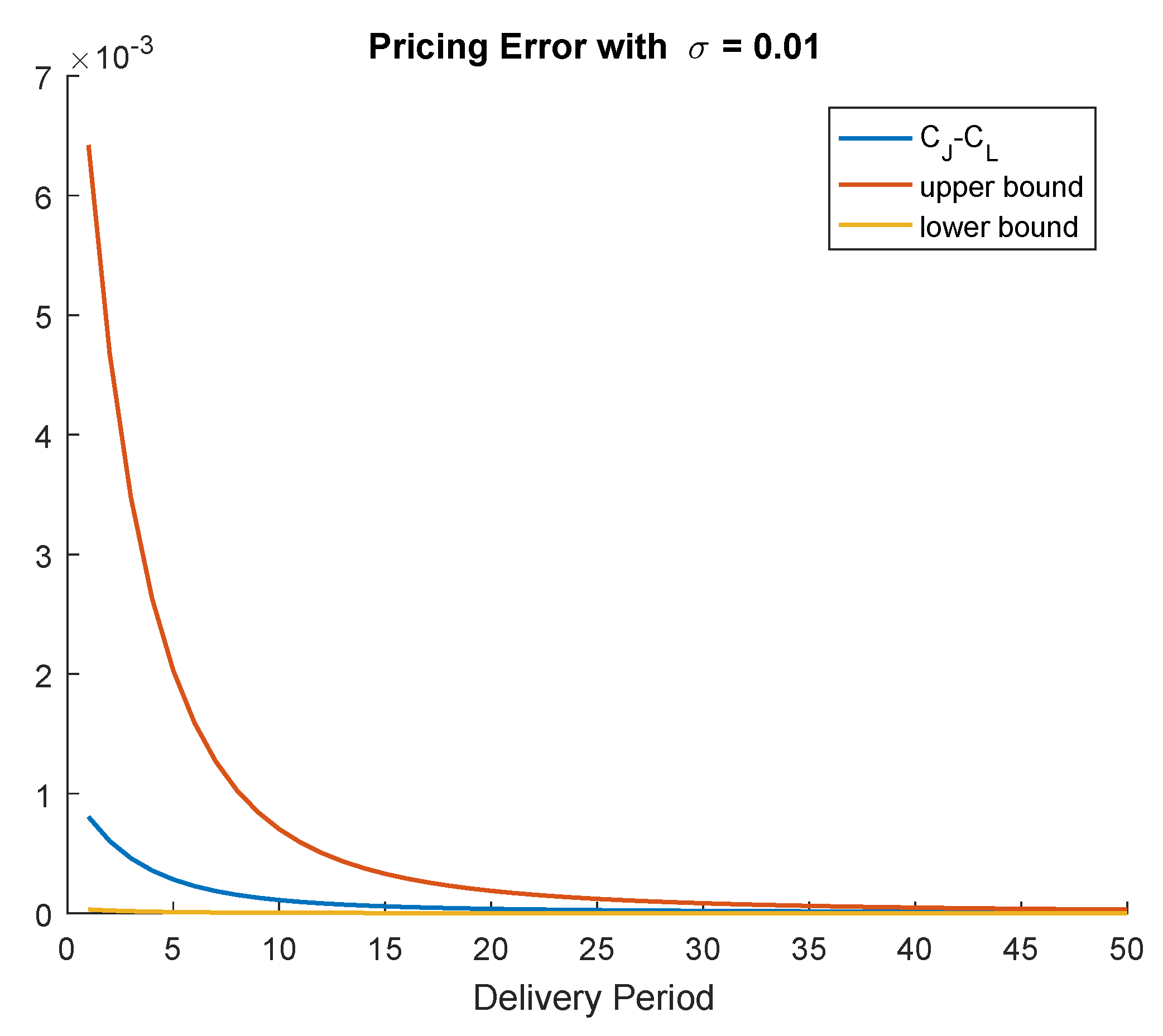

On the other hand, if we reduce

to the value

, we observe from

Figure 3 that the situation reverse; i.e., the lower bound on the pricing error becomes closer to the actual difference

than the upper bound. Overall, these numerical exercises illustrate that, depending on the model’s parameters, either the upper or the lower bound deliver better information about the real difference between the call options’ prices.

{kind=link}

{kind=link}

{kind=link}