Bitcoin and Altcoins Price Dependency: Resilience and Portfolio Allocation in COVID-19 Outbreak

Abstract

1. Introduction

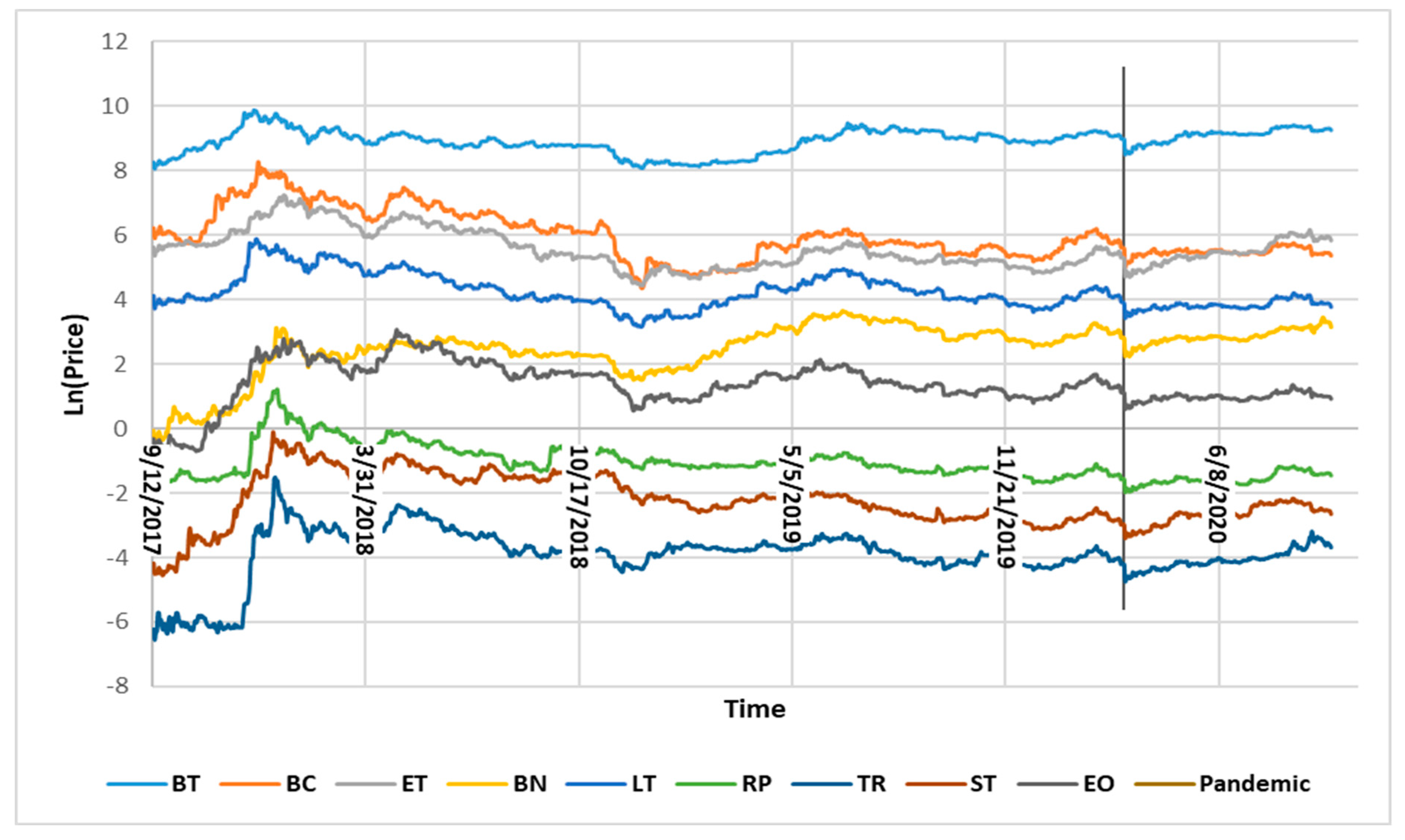

2. Data Collection and Methodology

2.1. Unit Root Tests

2.2. Johansen Cointegration Test

3. Empirical Results

3.1. Unit Root Test Results

3.2. Johansen Cointegration Test Results

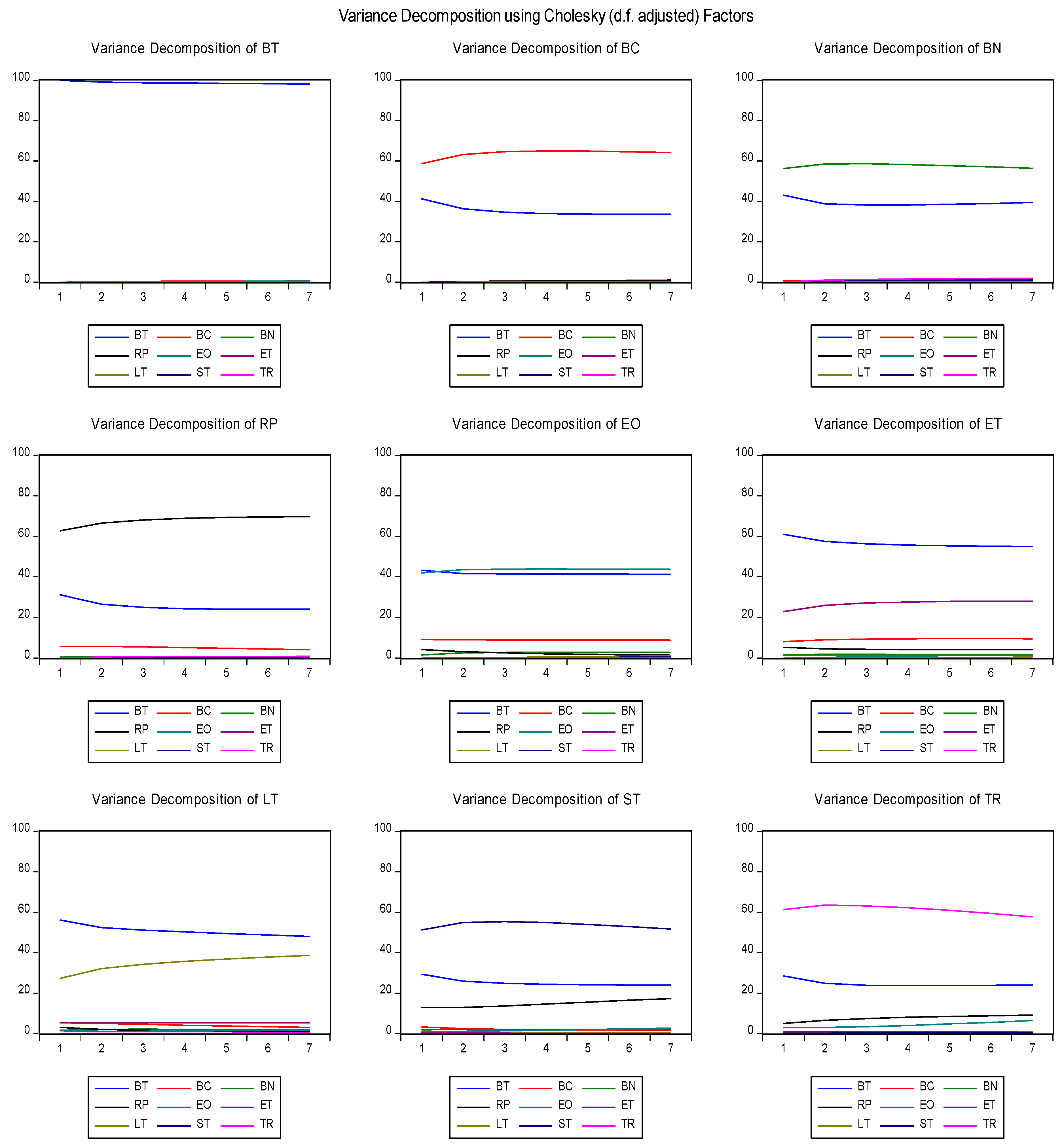

3.3. Vector Error Correction Model (VECM) Results

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Agosto, Arianna, and Alessia Cafferata. 2020. Financial Bubbles: A Study of Co-Explosivity in the Cryptocurrency Market. Risks 8: 34. [Google Scholar] [CrossRef]

- Nicaise, Nicolas, Hubert Anciaux, and Mikael Petitjean. 2019. Co-Movements in Market Quality of cryptocurrencies. Louvain: Louvain School of Management. [Google Scholar]

- Bação, Pedro, António Portugal Duarte, Helder Sebastião, and Srdjan Redzepagic. 2018. Information Transmission Between Cryptocurrencies: Does Bitcoin Rule the Cryptocurrency World? Scientific Annals of Economics and Busines 65: 97–117. [Google Scholar] [CrossRef]

- Batten, Jonathan A., Janusz Brzeszczynski, Cetin Ciner, Marco CK Lau, Brian Lucey, and Larisa Yarovaya. 2019. Price and volatility spillovers across the international steam coal market. Energy Economics 77: 119–38. [Google Scholar] [CrossRef]

- Brooks, Chris. 2014. Introductory Econometrics for Finance, 3rd ed. Cambridge: Cambridge University Press. [Google Scholar]

- Brzeszczyński, Janusz, and Boulis Maher Ibrahim. 2019. A stock market trading system based on foreign and domestic information. Expert Systems with Applications 118: 381–99. [Google Scholar] [CrossRef]

- Chuen, David LEE Kuo, Li Guo, and Yu Wang. 2017. Cryptocurrency: A new investment opportunity? The Journal of Alternative Investments 20: 16–40. [Google Scholar] [CrossRef]

- Ciaian, Pavel, and Miroslava Rajcaniova. 2018. Virtual relationships: Short- and long-run evidence from BitCoin and altcoin markets. Journal of International Financial Markets, Institutions, and Money 52: 173–95. [Google Scholar] [CrossRef]

- CoinMarketCap. 2019. Available online: https://coinmarketcap.com (accessed on September 23, 2020).

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Ethereum White Paper. 2019. Available online: https://ethereum.org (accessed on 3 November 2019).

- Giudici, Paolo, and Paolo Pagnottoni. 2019. High Frequency Price Change Spillovers in Bitcoin Markets. Risks 7: 111. [Google Scholar] [CrossRef]

- Joline, Göttfert. 2019. Cointegration among Cryptocurrencies: A Cointegration Analysis of Bitcoin, Bitcoin Cash, EOS, Ethereum, Litecoin, and Ripple. Master’s Thesis, MA in Economics, University in Umeå, Umeå, Sweden. [Google Scholar]

- Granger, Clive W. J., and Paul Newbold. 1974. Spurious regressions in econometrics. Journal of Econometrics 2: 111–20. [Google Scholar] [CrossRef]

- Harris, Richard, and Robert Sollis. 2003. Applied Time Series Modelling and Forecasting. New York: Wiley. [Google Scholar]

- Huang, Yingying, Kun Duan, and Tapas Mishra. 2021. Is Bitcoin really more than a diversifier? A pre- and post-COVID-19 analysis. Finance Research Letters 2021: 102016. [Google Scholar] [CrossRef]

- J McNeil, Alexander. 2021. Modelling Volatile Time Series with V-Transforms and Copulas. Risks 9: 14. [Google Scholar] [CrossRef]

- Johansen, Søren. 1995. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models. Oxford: Oxford University Press on Demand. [Google Scholar]

- Johansen, Soren, and Katarina Juselius. 1990. Maximum likelihood estimation and inference on cointegration—With applications to the demand for money. Oxford Bulletin of Economics and Statistics 52: 169–210. [Google Scholar] [CrossRef]

- Kwiatkowski, Denis, Peter CB Phillips, Peter Schmidt, and Yongcheol Shin. 1992a. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Kwiatkowski, Denis, Peter CB Phillips, Peter Schmidt, and Yongcheol Shin. 1992b. Testing the null hypothesis of stationarity against the alternative of a unit root. Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Leung, Tim, and Hung Nguyen. 2019. Constructing cointegrated cryptocurrency portfolios for statistical arbitrage. Studies in Economics and Finance 36: 581–59. [Google Scholar] [CrossRef]

- Mariana, Christy Dwita, Irwan Adi Ekaputra, and Zaäfri Ananto Husodo. 2021. Are Bitcoin and Ethereum safe-havens for stocks during the COVID-19 pandemic? Finance Research Letters 38: 101798. [Google Scholar] [CrossRef]

- Phillips, Peter CB, and Pierre Perron. 1988. Testing for a unit root in time series regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Resta, Marina, Paolo Pagnottoni, and Maria Elena De Giuli. 2020. Technical Analysis on the Bitcoin Market: Trading Opportunities or Investors’ Pitfall? Risks 8: 44. [Google Scholar] [CrossRef]

- Ripple White Paper. 2019. Available online: https://ripple.com (accessed on 3 November 2019).

- Shams, Amin. 2019. What Drives the Covariation of Cryptocurrencies Returns? Paper presented at the Association of Financial Economists & American Economic Association Beyond Bitcoin Paper Session Conference, Atlanta, GA, USA, January 4–6. [Google Scholar]

- Sovbetov, Yhlas. 2018. Factors Influencing Cryptocurrency Prices: Evidence from Bitcoin, Ethereum, Dash, Litcoin, and Monero. Journal of Economics and Financial Analysis 2: 1–27. [Google Scholar]

- Tron White Paper. 2019. Available online: https://tron.network (accessed on 3 November 2019).

- Umar, Muhammad, Chi-Wei Su, Syed Kumail Abbas Rizvi, and Xue-Feng Shao. 2021. Bitcoin: A safe haven asset and a winner amid political and economic uncertainties in the US? Technological Forecasting and Social Change 167: 120680. [Google Scholar] [CrossRef]

- Zhang, Hongwei, and Peijin Wang. 2021. Does Bitcoin or gold react to financial stress alike? Evidence from the US and China. International Review of Economics & Finance 71: 629–48. [Google Scholar]

{kind=link}

{kind=link}

| Abbreviation | Full Description |

|---|---|

| BT | |

| BC | |

| ET | |

| BN | |

| LT | |

| RP | |

| TR | |

| ST | |

| EO | |

| DP |

| Crypto Currencies | BC | BN | BT | EO | ET | LT | RP | ST | TR |

|---|---|---|---|---|---|---|---|---|---|

| Mean | 5.979050 | 2.489788 | 8.923931 | 1.382447 | 5.569162 | 4.234047 | −1.064664 | −2.219531 | −3.900057 |

| Median | 5.773277 | 2.678965 | 8.982603 | 1.327075 | 5.434246 | 4.090002 | −1.186821 | −2.303816 | −3.809241 |

| Maximum | 8.274630 | 3.658936 | 9.878036 | 3.069912 | 7.241667 | 5.881482 | 1.217876 | −0.109562 | −1.511608 |

| Minimum | 4.348599 | −0.387452 | 8.056728 | −0.706790 | 4.434500 | 3.155297 | −1.968723 | −4.546901 | −6.552181 |

| Std. Dev. | 0.753795 | 0.780537 | 0.362569 | 0.678709 | 0.590756 | 0.529539 | 0.536189 | 0.789454 | 0.800641 |

| Skewness | 0.658173 | −1.597372 | −0.442579 | −0.488491 | 0.660800 | 0.767978 | 1.285009 | −0.065045 | −1.126748 |

| Kurtosis | 2.842304 | 5.553269 | 2.826004 | 4.129425 | 2.729676 | 3.119208 | 4.904194 | 3.053315 | 5.354942 |

| Jarque-Bera | 80.92433 | 770.0731 | 37.46773 | 102.6773 | 83.78199 | 109.2739 | 471.0498 | 0.910054 | 489.1463 |

| Probability | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.634431 | 0.000000 |

| Sum | 6606.850 | 2751.216 | 9860.944 | 1527.604 | 6153.924 | 4678.622 | −1176.453 | −2452.582 | −4309.563 |

| Sum Sq. Dev. | 627.3011 | 672.5984 | 145.1281 | 508.5530 | 385.2874 | 309.5742 | 317.3989 | 688.0547 | 707.6924 |

| Observations | 1105 | 1105 | 1105 | 1105 | 1105 | 1105 | 1105 | 1105 | 1105 |

| Test | Crypto Currency | At Level | First Difference | Conclusion | ||

|---|---|---|---|---|---|---|

| Constant | Trend | Constant | Trend | |||

| Augmented Dicky–Fuller (ADF) Test | BC | −1.455527 | −2.164669 | −32.89931 *** | −32.89108 *** | I(1) |

| BN | −3.214448 ** | −2.890817 | −32.64170 *** | −32.72287 *** | I(1) | |

| BT | −2.291515 | −2.256309 | −35.08992 *** | −35.08628 *** | I(1) | |

| EO | −2.550569 | −2.983509 | −33.92567 *** | −34.01012 *** | I(1) | |

| ET | −1.449358 | −1.496356 | −35.65421 *** | −35.63660 *** | I(1) | |

| LT | −1.688528 | −2.258656 | −35.25764 *** | −35.26472 *** | I(1) | |

| RP | −2.221522 | −3.394790 * | −20.85174 *** | −20.86436 *** | I(1) | |

| ST | −2.466247 | −3.454159 ** | −32.85974 *** | −32.96970 *** | I(1) | |

| TR | −3.263085 ** | −3.254660 * | −16.49659 *** | −16.53361 *** | I(1) | |

| Philips Perron (PP) Test | BC | −1.581304 | −2.343344 | −32.96597 *** | −32.95737 *** | I(1) |

| BN | −3.214448 ** | −2.898840 | −32.64170 *** | −32.72998 *** | I(1) | |

| BT | −2.359067 | −2.328691 | −35.02309 *** | −35.01879 *** | I(1) | |

| EO | −2.600346 * | −3.002913 | −33.95103 *** | −34.01285 *** | I(1) | |

| ET | −1.566195 | −1.651572 | −35.61452 *** | −35.59931 *** | I(1) | |

| LT | −1.810645 | −2.383506 | −35.16615 *** | −35.16919 *** | I(1) | |

| RP | −2.319534 | −3.376422 * | −33.32651 *** | −33.32241 *** | I(1) | |

| ST | −2.502271 | −3.445074 ** | −32.91205 *** | −32.98776 *** | I(1) | |

| TR | −3.134089 ** | −3.106928 | −33.28017 *** | −33.29494 *** | I(1) | |

| Kwiatkowski-Phillips-Schmidt-Shin (KPSS) Test | BC | 2.216446 *** | 0.395057 *** | 0.067451 | 0.068722 | I(1) |

| BN | 1.971803 *** | 0.327697 *** | 0.302892 | 0.101509 | I(1) | |

| BT | 0.553574 *** | 0.386815 *** | 0.093659 | 0.093311 | I(1) | |

| EO | 0.557306 *** | 0.247062 *** | 0.322137 | 0.124309 * | I(1) | |

| ET | 1.681350 *** | 0.536573 *** | 1.681350 | 0.101914 | I(1) | |

| LT | 1.307524 *** | 0.200836 *** | 0.080388 | 0.067071 | I(1) | |

| RP | 1.930178 *** | 0.137626 *** | 0.093588 | 0.058407 | I(1) | |

| ST | 1.206848 *** | 0.310630 *** | 0.417179 | 0.200480 | I(1) | |

| TR | 0.267004 | 0.276951 *** | 0.191082 | 0.094042 | I(1) | |

| Null Hypothesis | Null Hypothesis | Without DP as Exogenous | With DP as Exogenous | ||

|---|---|---|---|---|---|

| Trace Test Stat | Prob. | Trace Test Stat | Prob. | ||

| 374.8589 *** | 0.0000 | 399.4607 *** | 0.0000 | ||

| 250.9382 *** | 0.0000 | 276.2578 *** | 0.0000 | ||

| 153.8667 *** | 0.0003 | 176.7178 *** | 0.0000 | ||

| 87.91191 | 0.1533 | 97.23498 ** | 0.0394 | ||

| ------ | ------ | 59.35614 | 0.2557 | ||

| Cointegrating Vectors | Without DPas Exogenous | With DPas Exogenous | |||||

|---|---|---|---|---|---|---|---|

| CV 1 | CV 2 | CV 3 | CV 1 | CV 2 | CV 3 | CV 4 | |

| BT(-1) | 1 | ----- | ----- | 1 | ----- | ----- | ----- |

| BC(-1) | ----- | 1 | ----- | ----- | 1 | ----- | ----- |

| BN(-1) | ----- | ----- | 1 | ----- | ----- | 1 | ----- |

| RP(-1) | 2.737076 *** (0.27536) | ----- | 3.592859 *** (0.33853) | ----- | ----- | ----- | 1 |

| EO(-1) | 0.842660 *** (0.07967) | ----- | ----- | ----- | −1.068516 *** (0.07490) | ----- | 0.492085 *** (0.07511) |

| ET(-1) | ----- | −0.621420 *** (0.16820) | 0.794492 *** (0.19873) | ----- | −0.822628 *** (0.05139) | 1.226244 *** (0.09771) | ----- |

| LT(-1) | −1.689590 *** (0.17877) | ----- | −2.600232 *** (0.22541) | −1.015065 *** (0.15196) | ----- | −1.851291 *** (0.20849) | −0.393801 *** (0.04954) |

| ST(-1) | −1.549811 *** (0.15847) | −0.589472 *** (0.12607) | −1.231458 *** (0.22233) | ----- | ----- | ----- | −0.599264 *** (0.04632) |

| TR(-1) | ----- | ----- | ----- | 0.624704 *** (0.03728) | 0.857581 *** (0.05841) | ----- | −0.214680 *** (0.04742) |

| C | −3.460887 | −3.825852 | 5.186469 | −2.190680 | 3.423958 | -1.480889 | −0.115496 |

| D(BT) | D(BC) | D(BN) | D(RP) | D(EO) | D(ET) | D(LT) | D(ST) | D(TR) |

|---|---|---|---|---|---|---|---|---|

| 0.005165 | 0.006750 | 0.022341 *** | 0.012153 * | 0.006938 | 0.015194 *** | 0.007722 | 0.025631 *** | 0.027721 *** |

| (0.00446) | (0.00731) | (0.00648) | (0.00621) | (0.00720) | (0.00552) | (0.00585) | (0.00713) | (0.00911) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aysan, A.F.; Khan, A.U.I.; Topuz, H. Bitcoin and Altcoins Price Dependency: Resilience and Portfolio Allocation in COVID-19 Outbreak. Risks 2021, 9, 74. https://doi.org/10.3390/risks9040074

Aysan AF, Khan AUI, Topuz H. Bitcoin and Altcoins Price Dependency: Resilience and Portfolio Allocation in COVID-19 Outbreak. Risks. 2021; 9(4):74. https://doi.org/10.3390/risks9040074

Chicago/Turabian StyleAysan, Ahmet Faruk, Asad Ul Islam Khan, and Humeyra Topuz. 2021. "Bitcoin and Altcoins Price Dependency: Resilience and Portfolio Allocation in COVID-19 Outbreak" Risks 9, no. 4: 74. https://doi.org/10.3390/risks9040074

APA StyleAysan, A. F., Khan, A. U. I., & Topuz, H. (2021). Bitcoin and Altcoins Price Dependency: Resilience and Portfolio Allocation in COVID-19 Outbreak. Risks, 9(4), 74. https://doi.org/10.3390/risks9040074