Life Expectancy Heterogeneity and Pension Fairness: An Italian North-South Divide

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

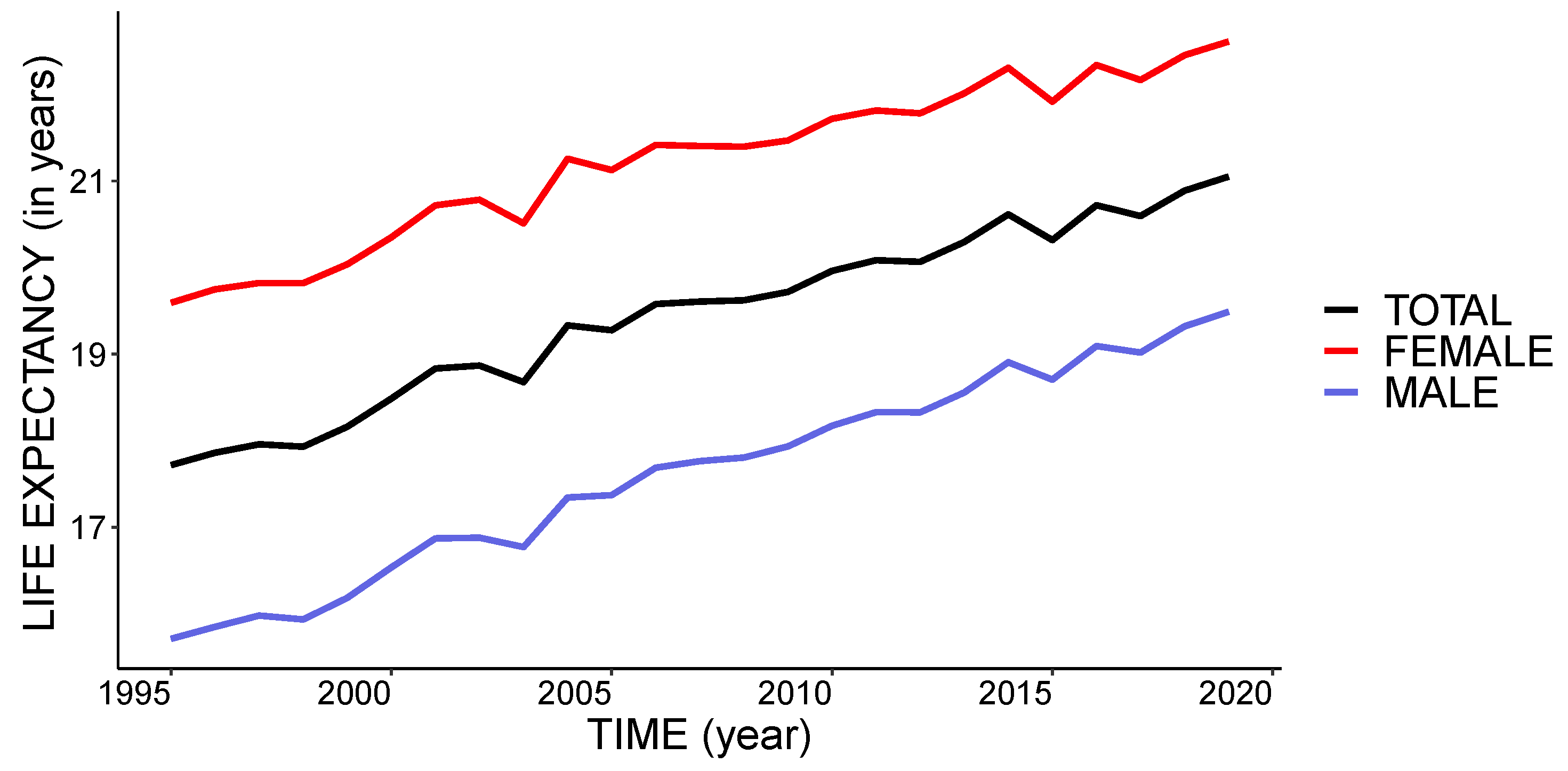

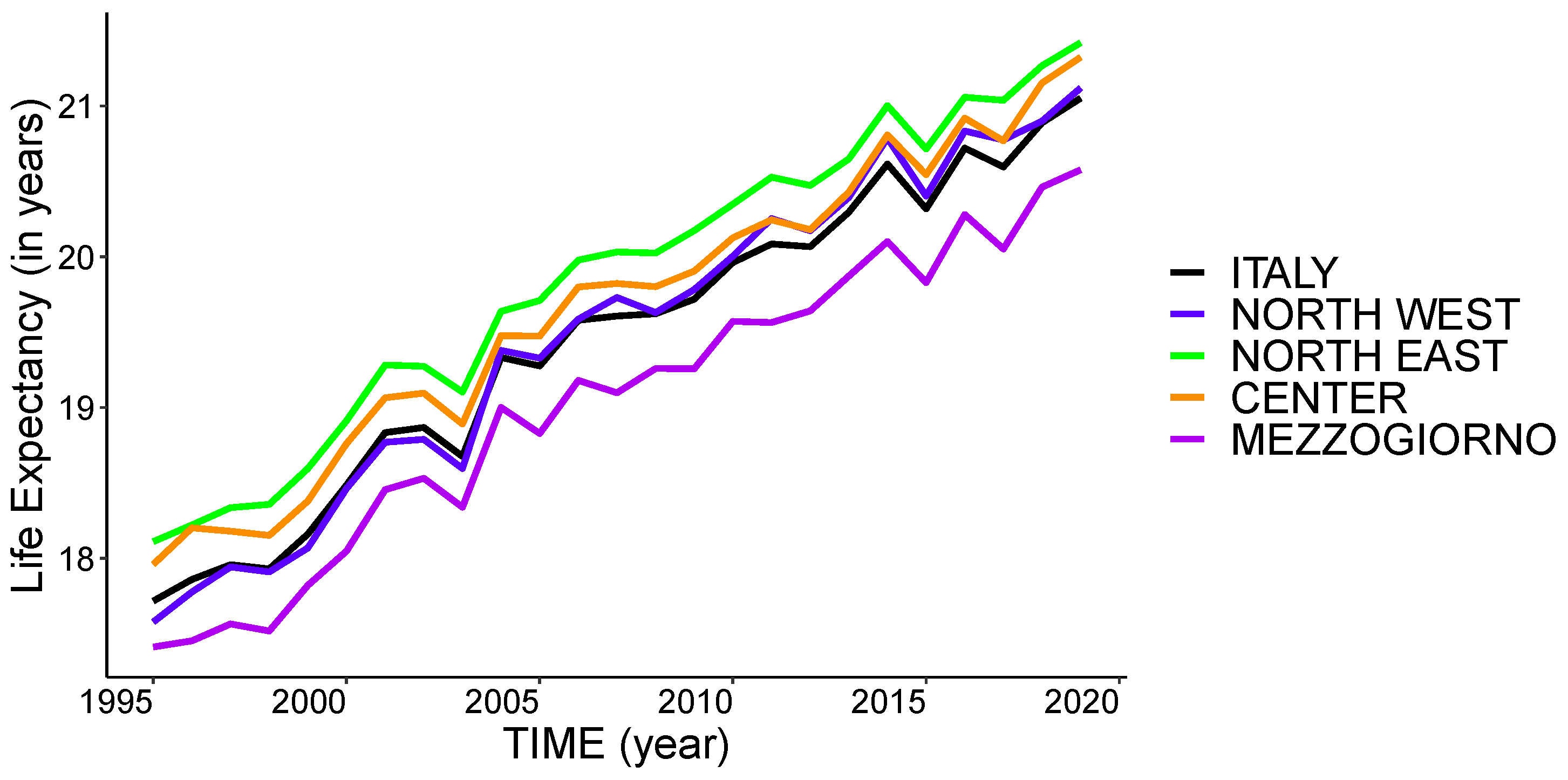

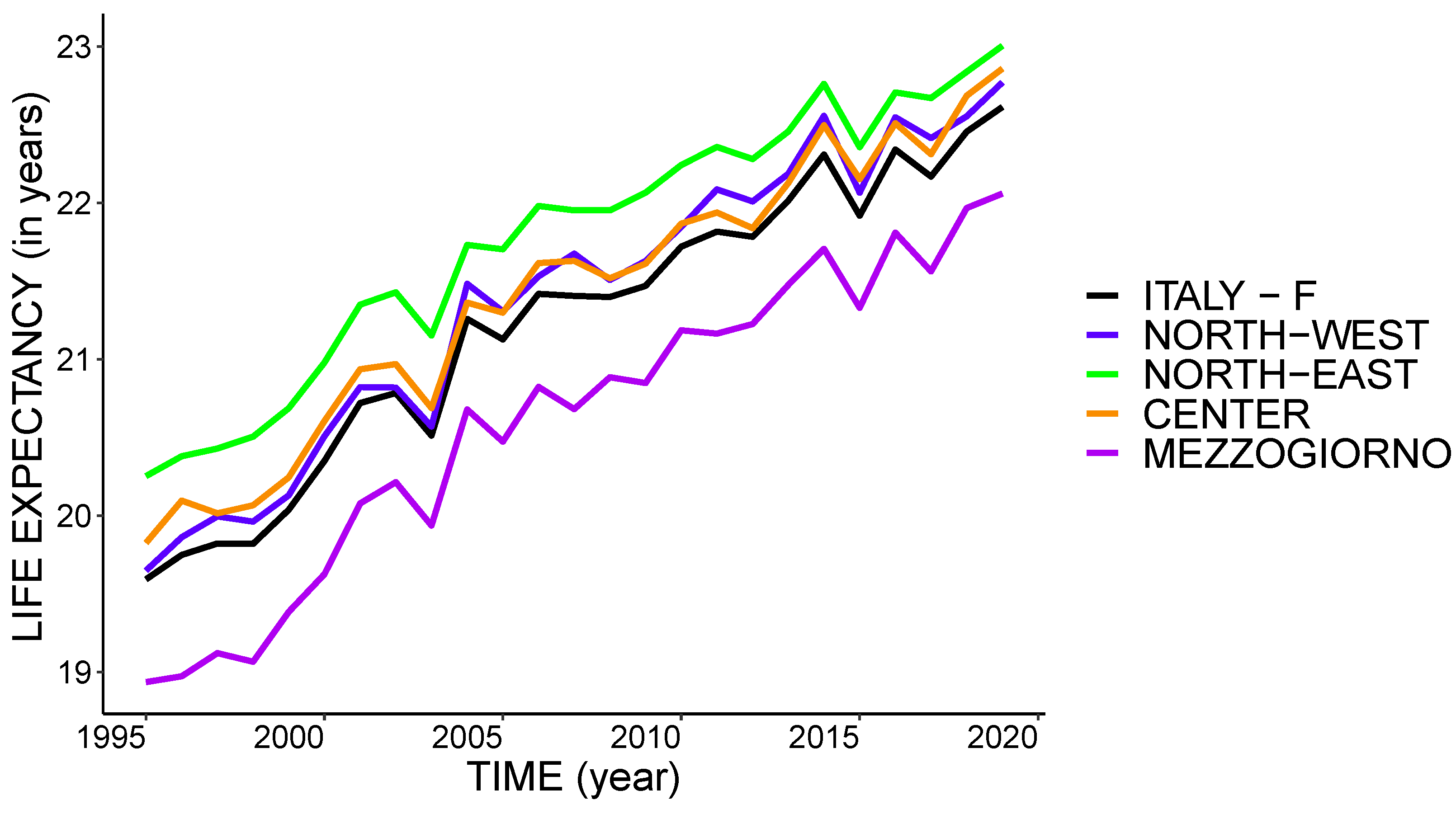

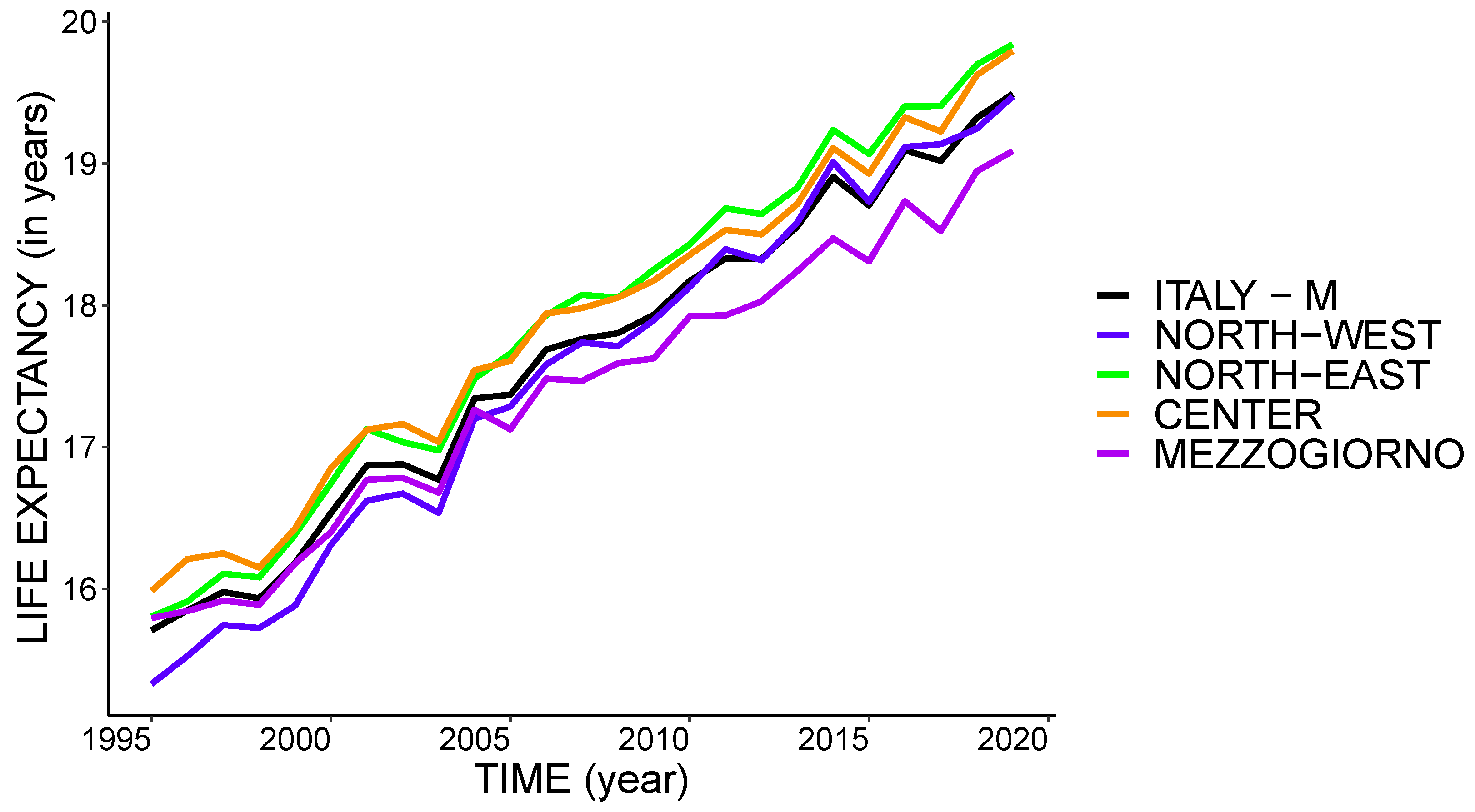

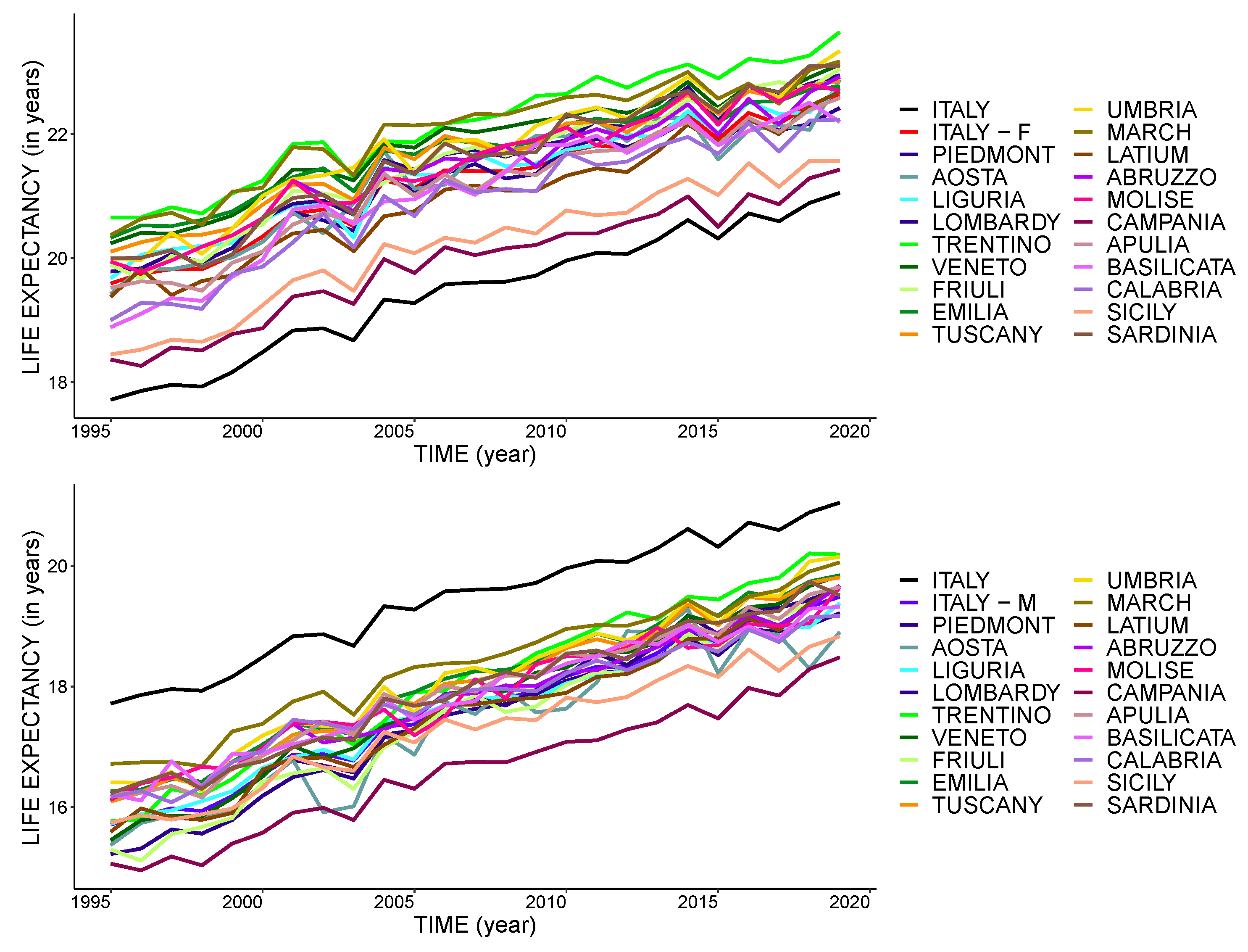

3.1. Data

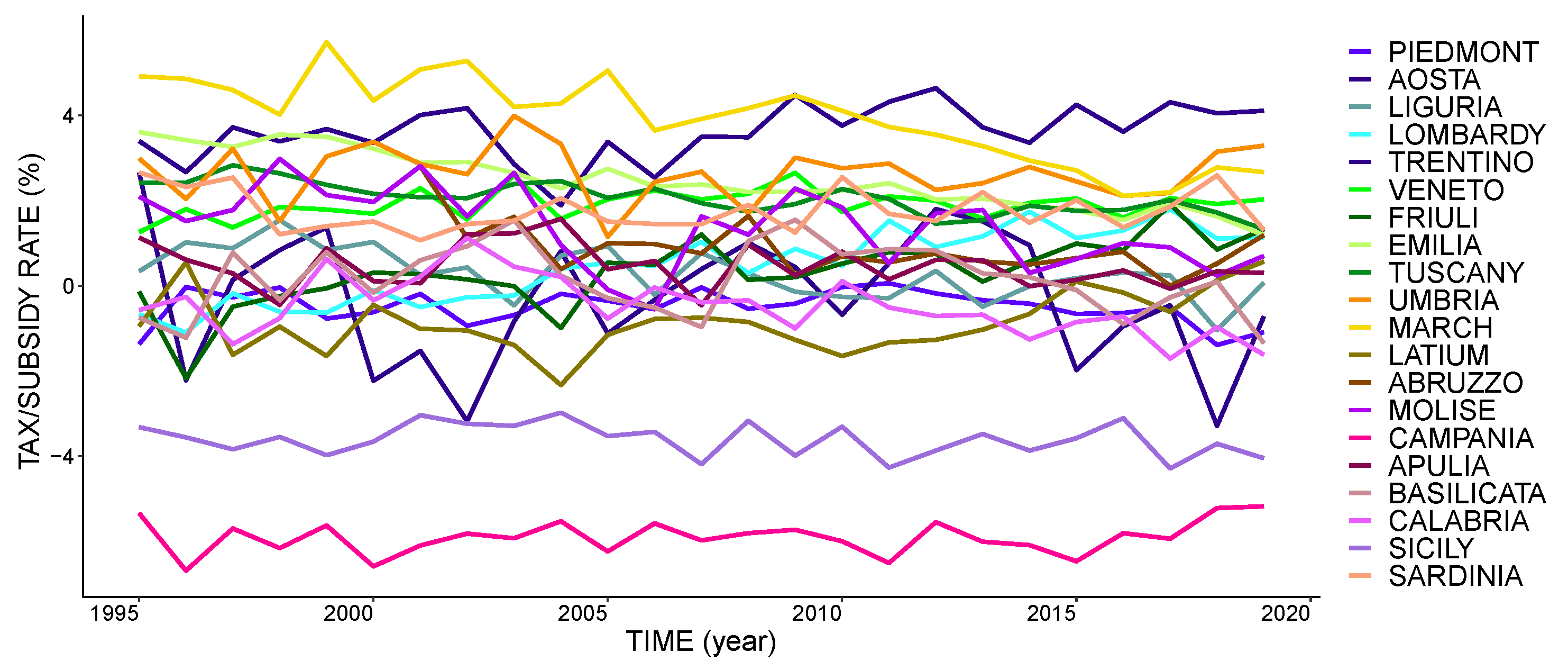

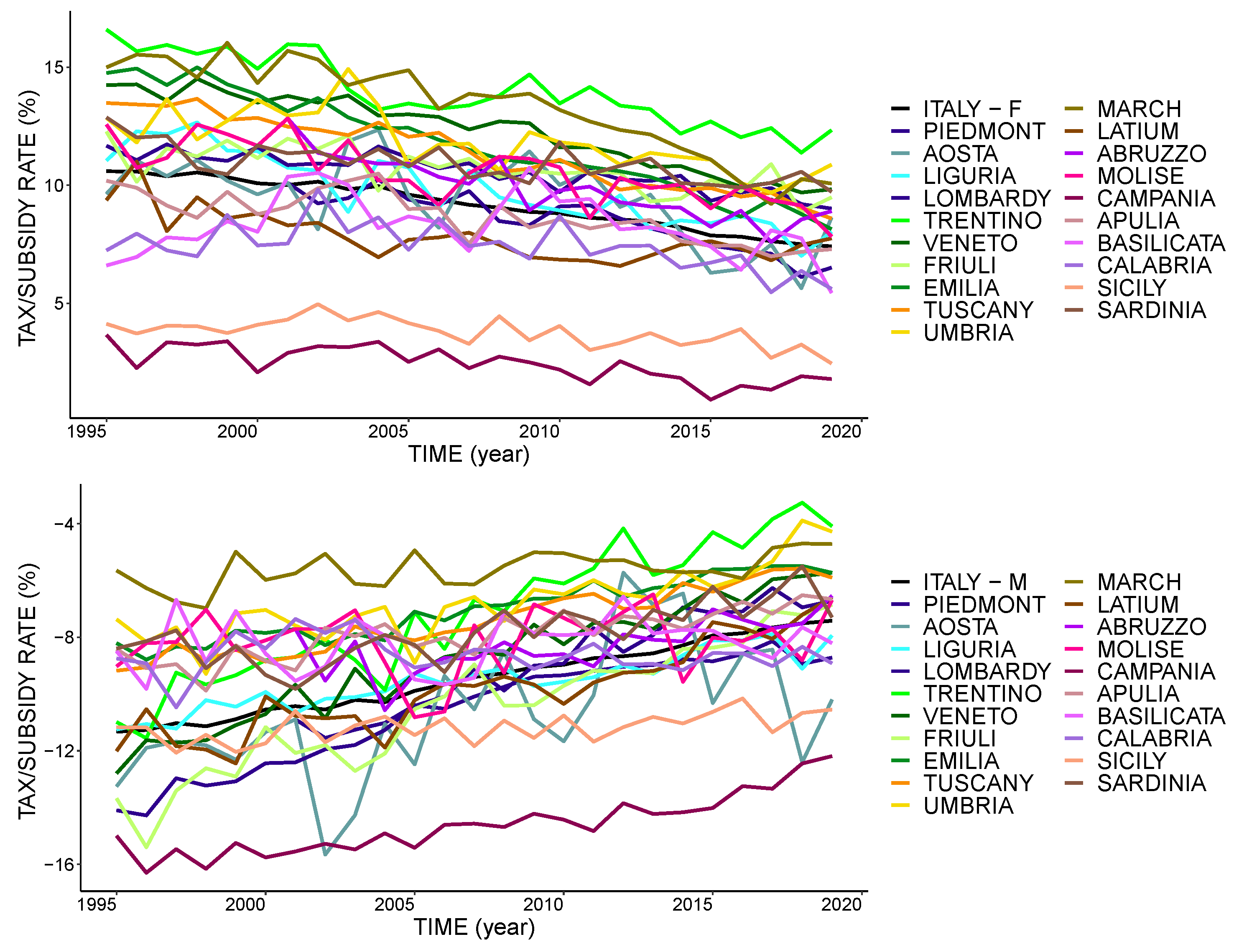

3.2. The Tax/Subsidy Mechanism

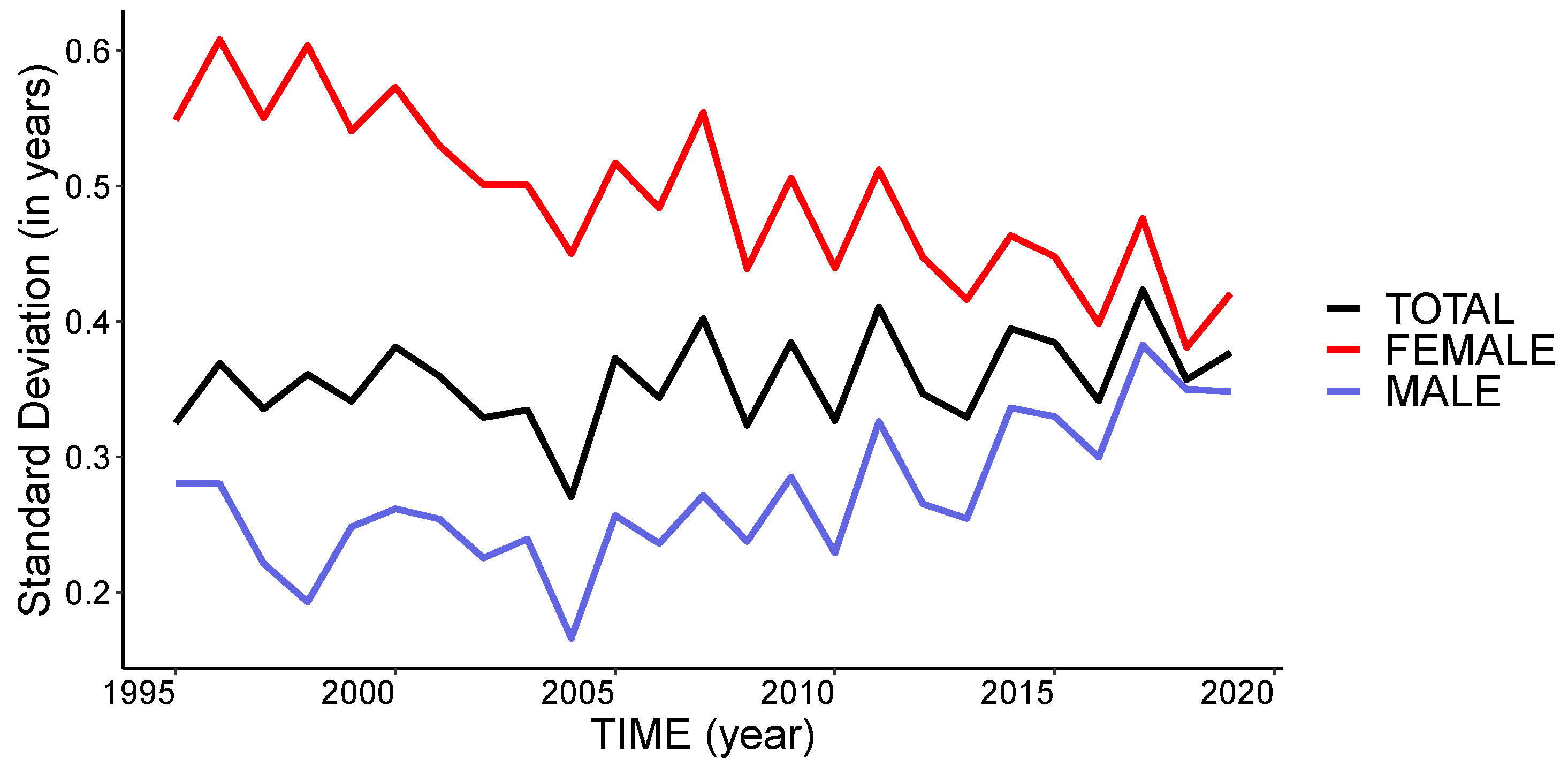

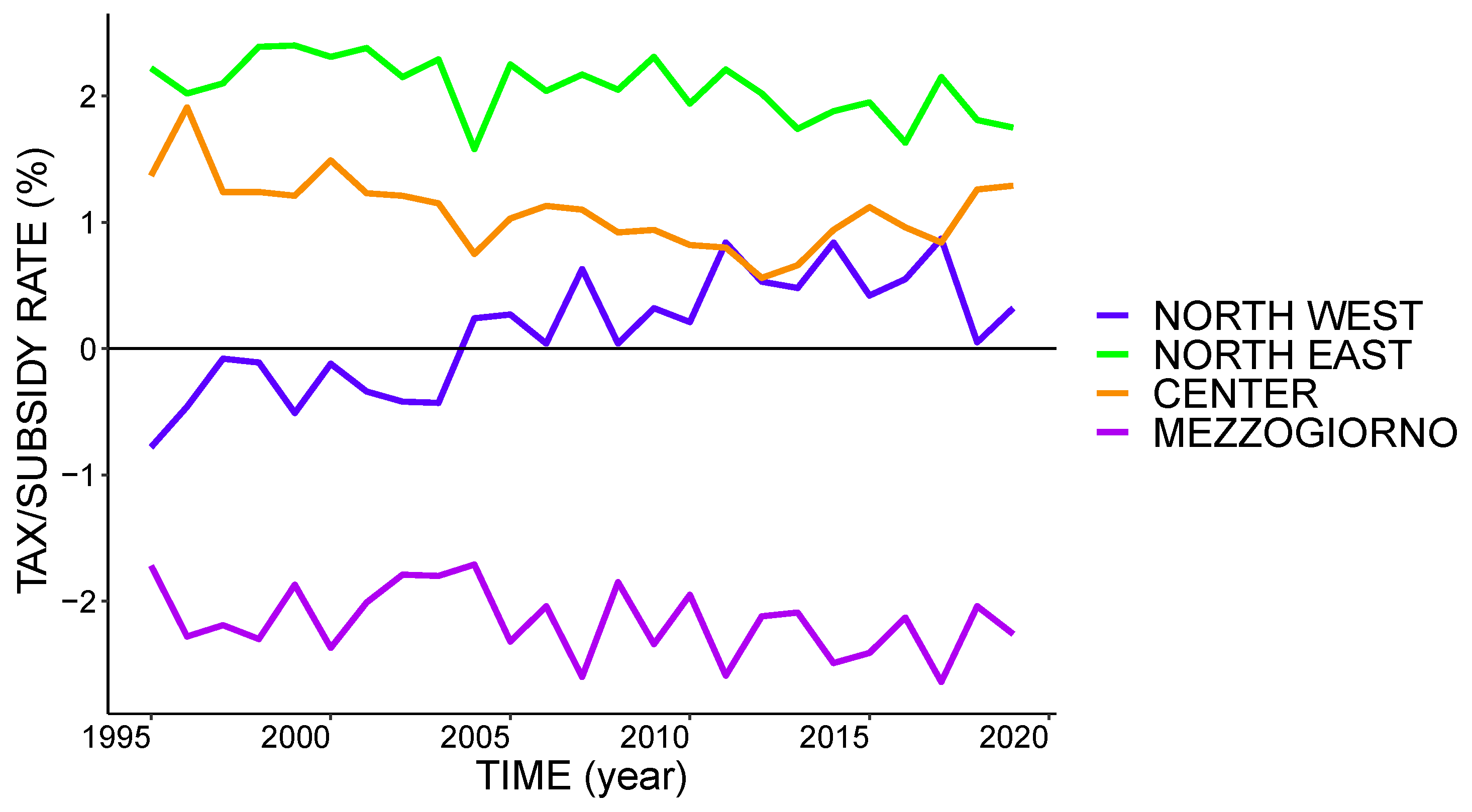

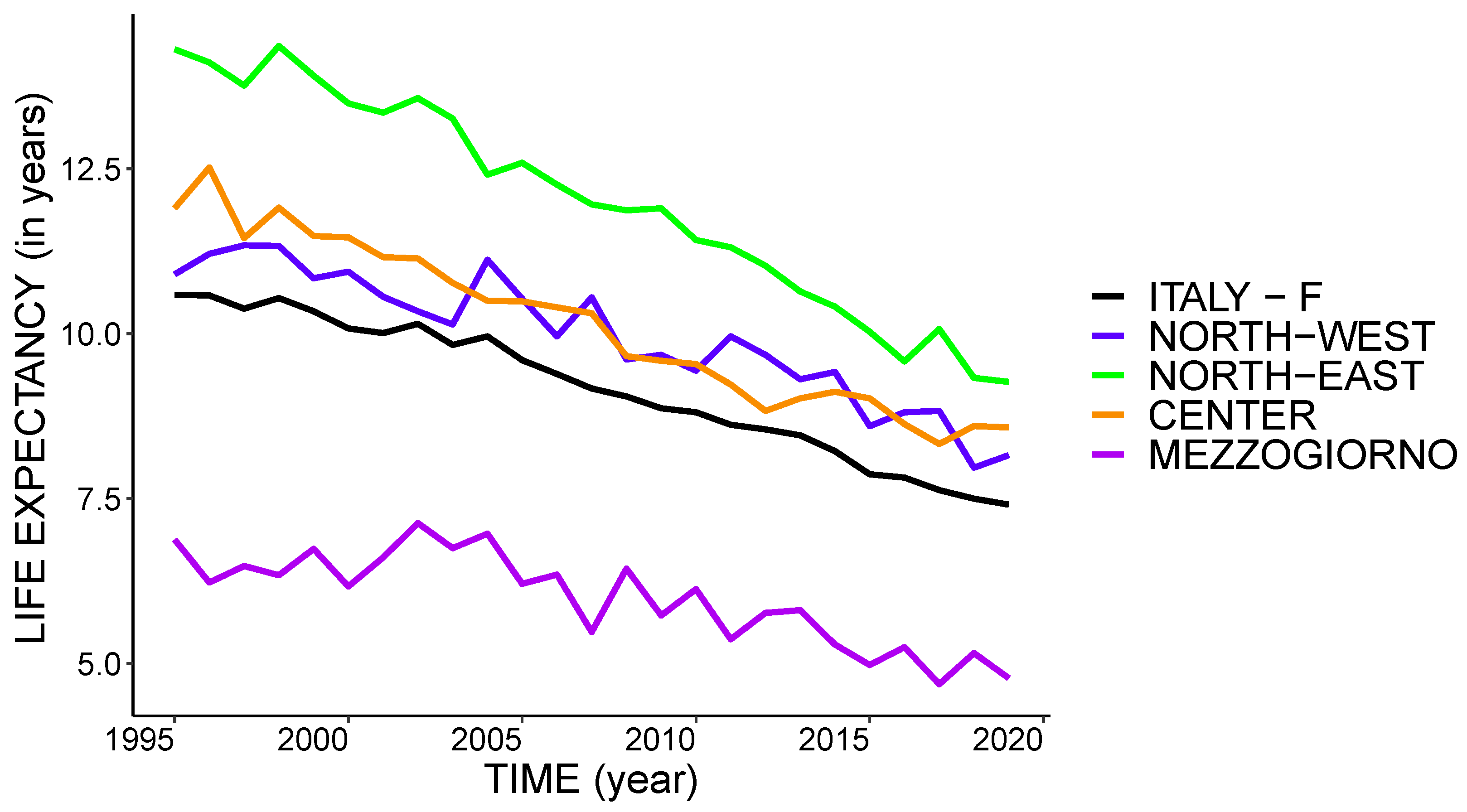

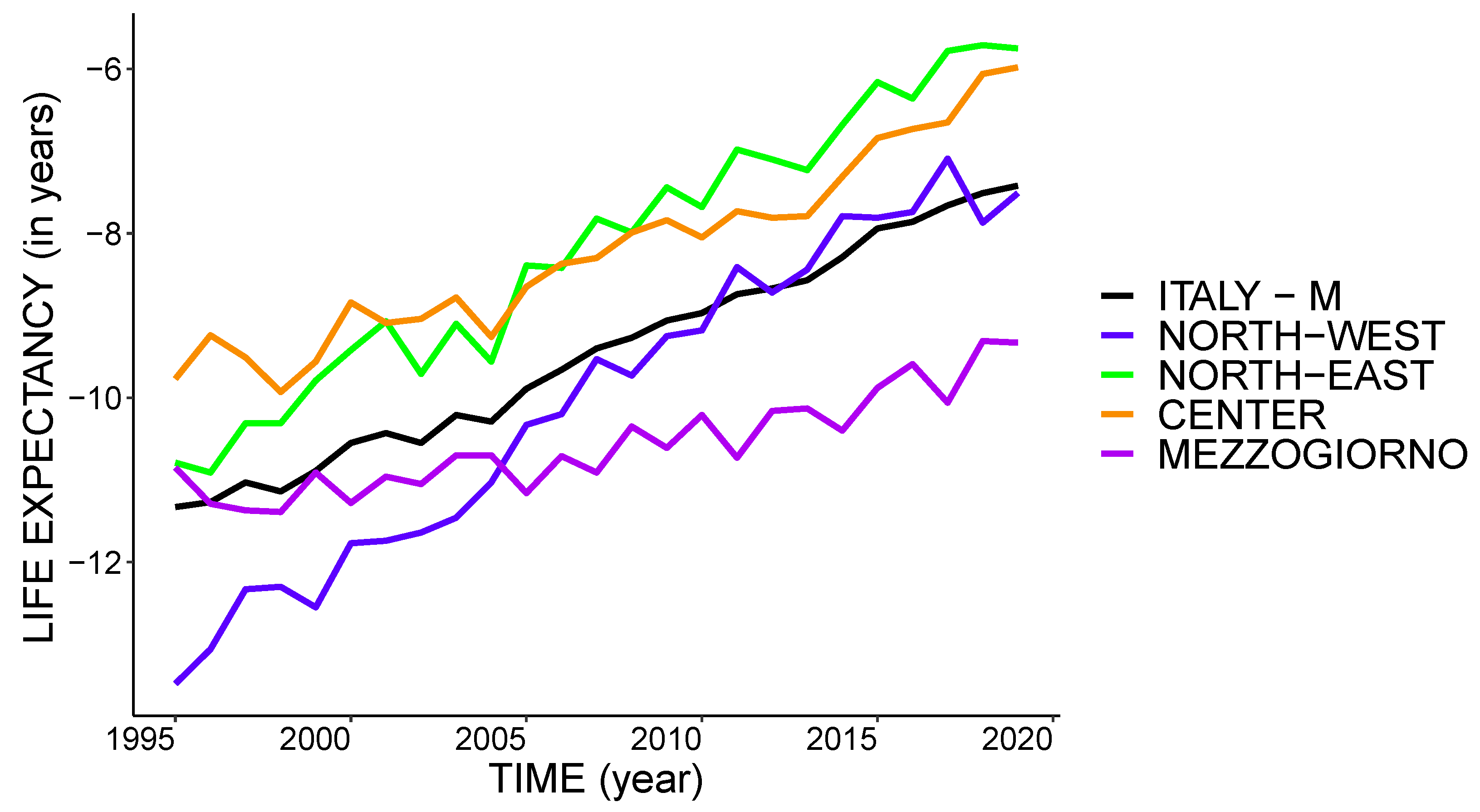

4. Results

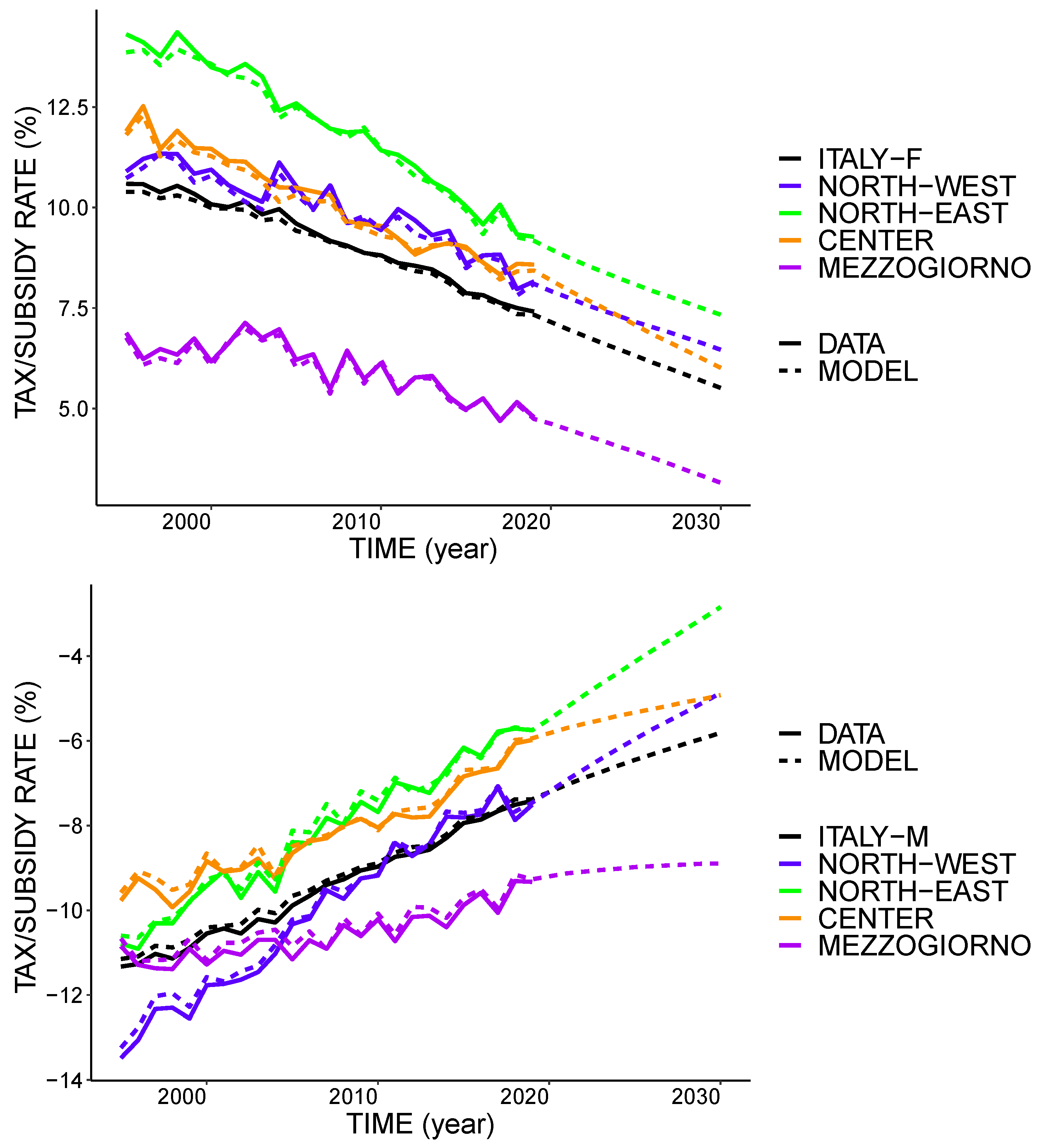

4.1. Tax/Subsidy Profiles

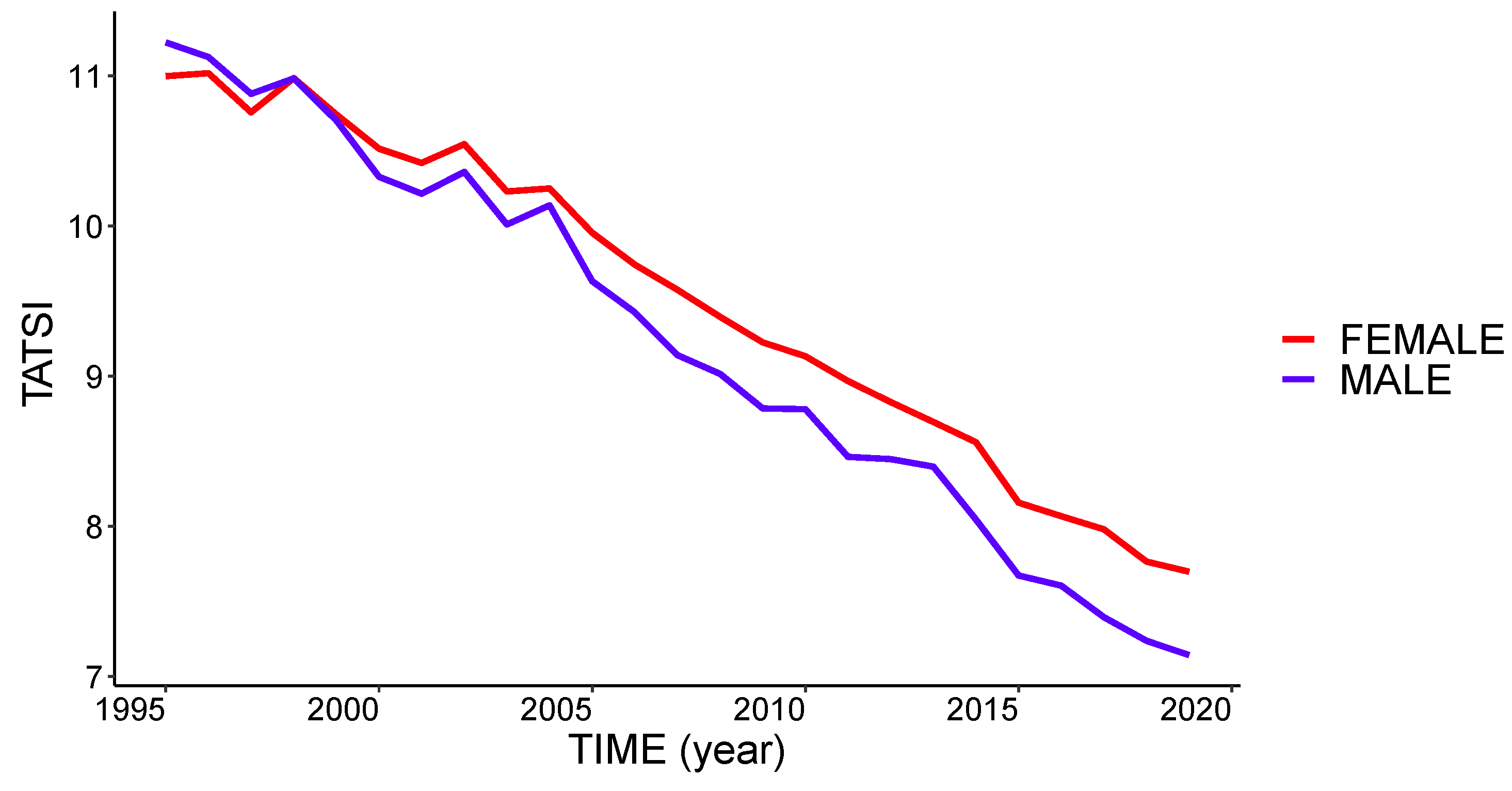

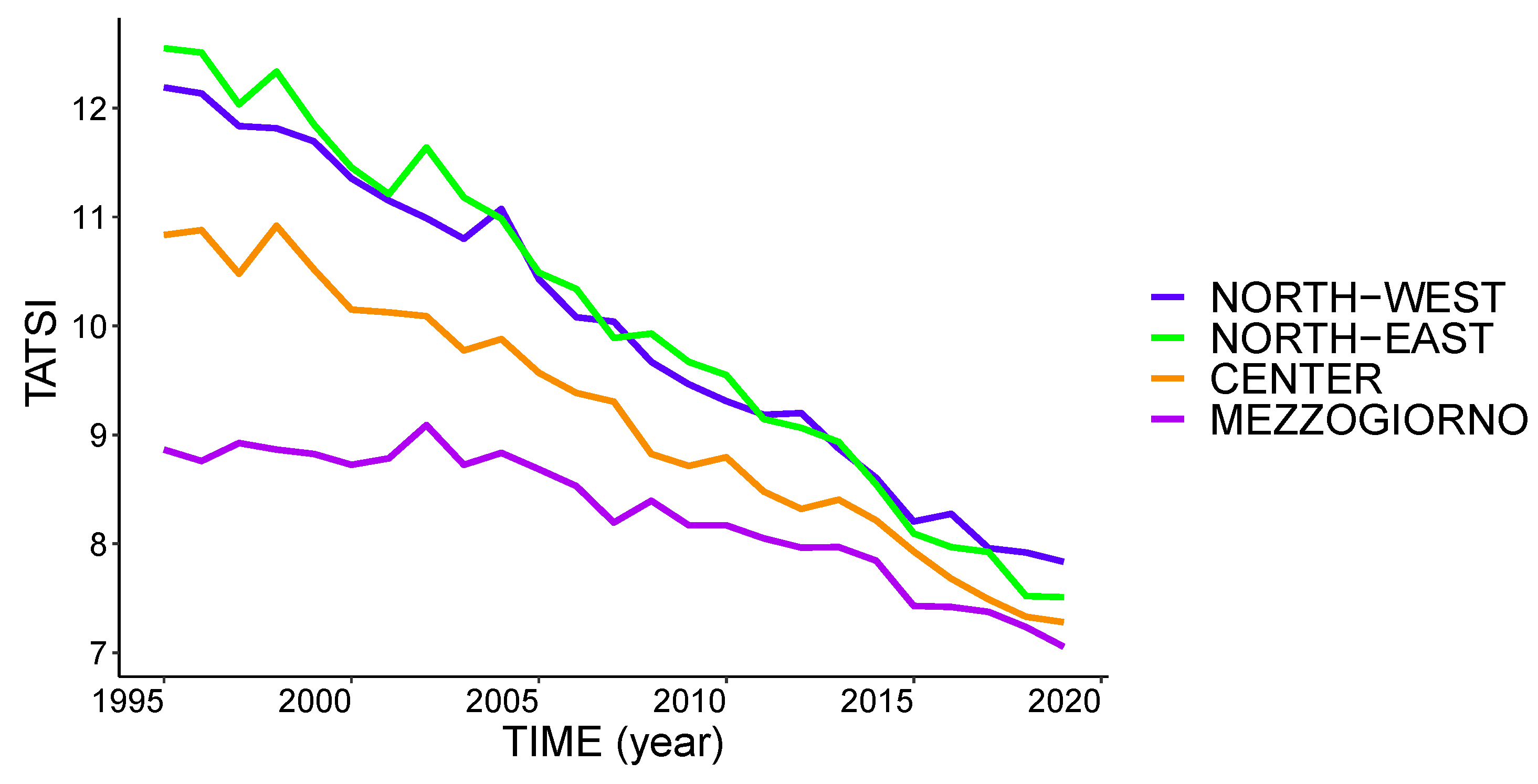

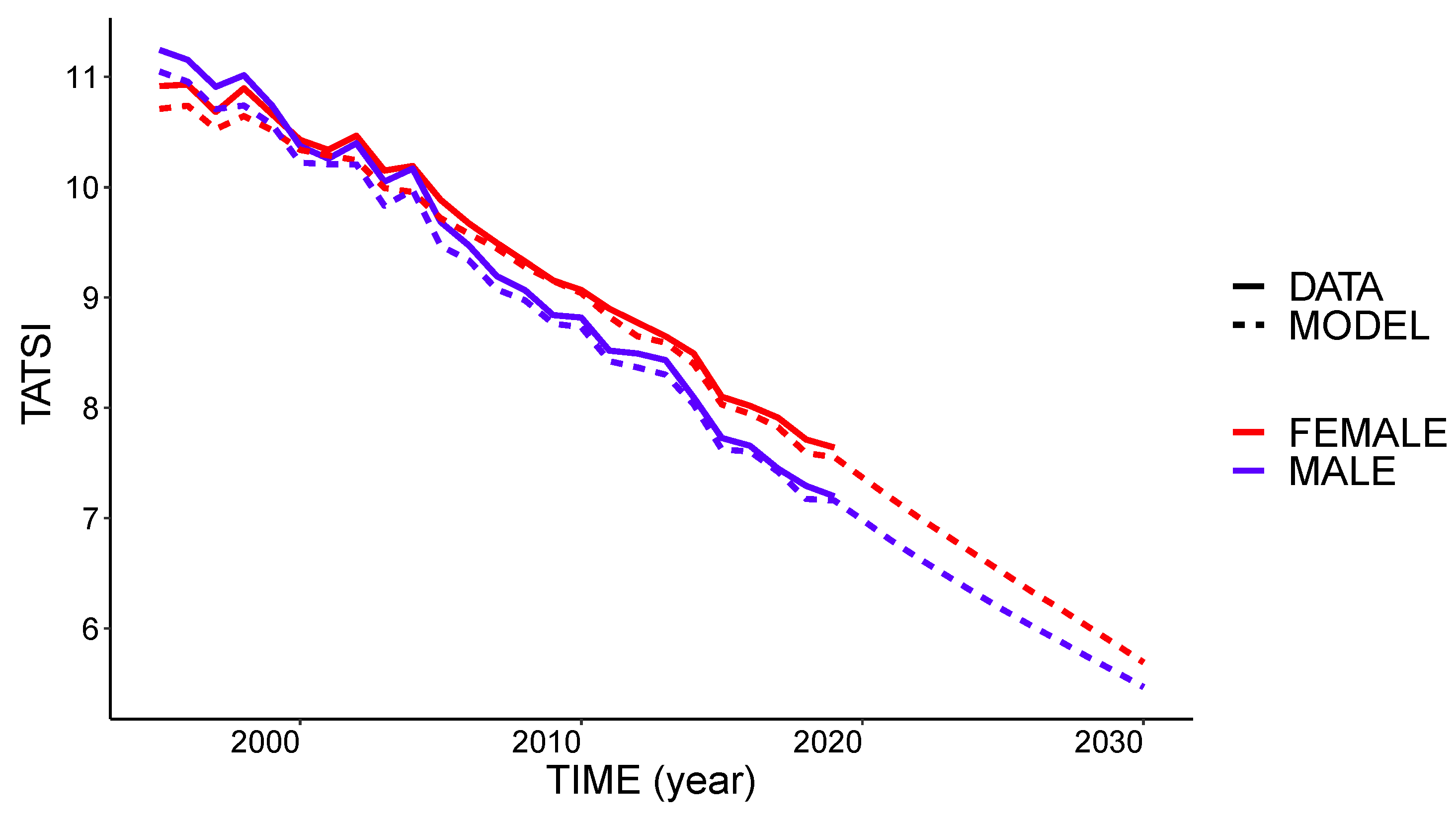

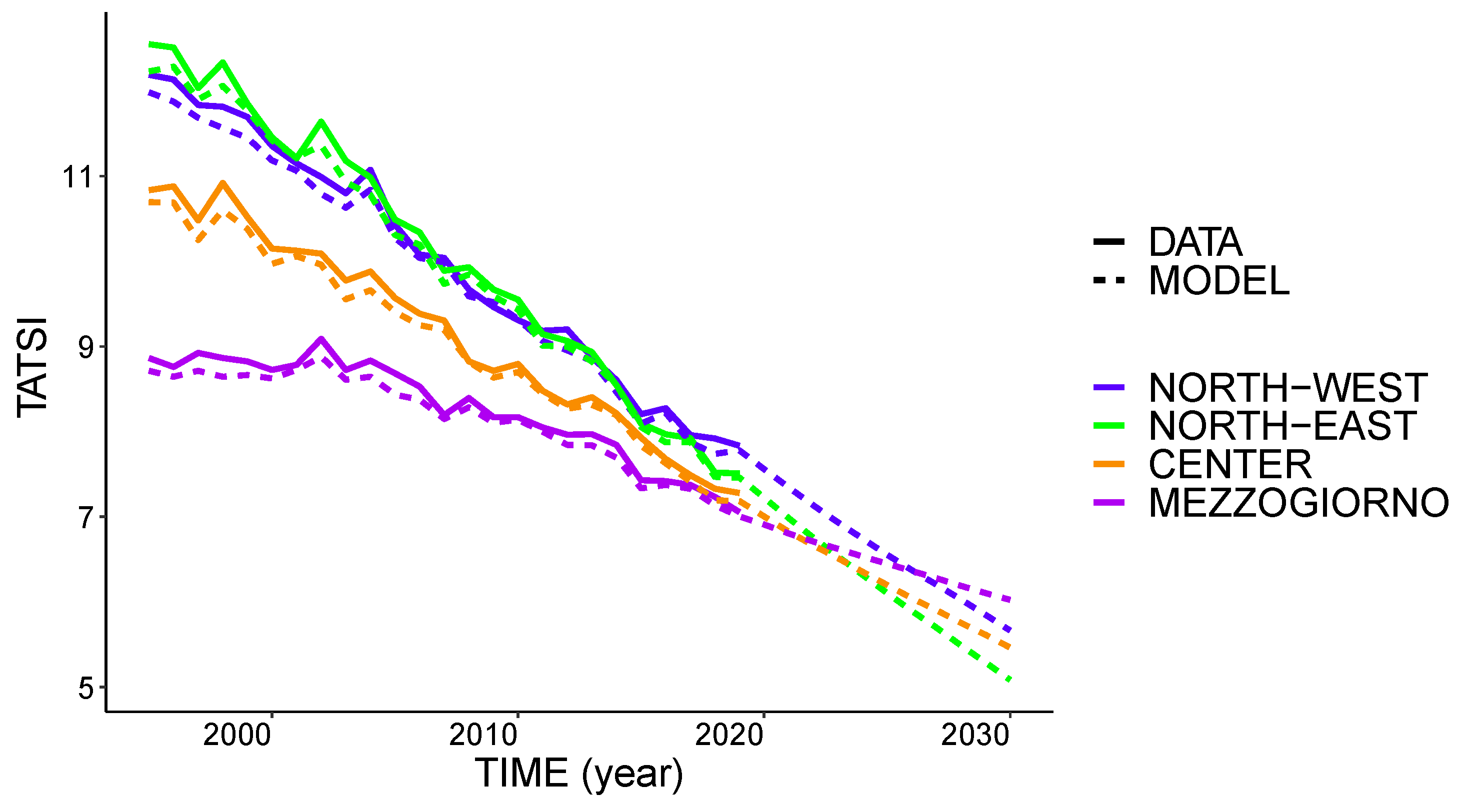

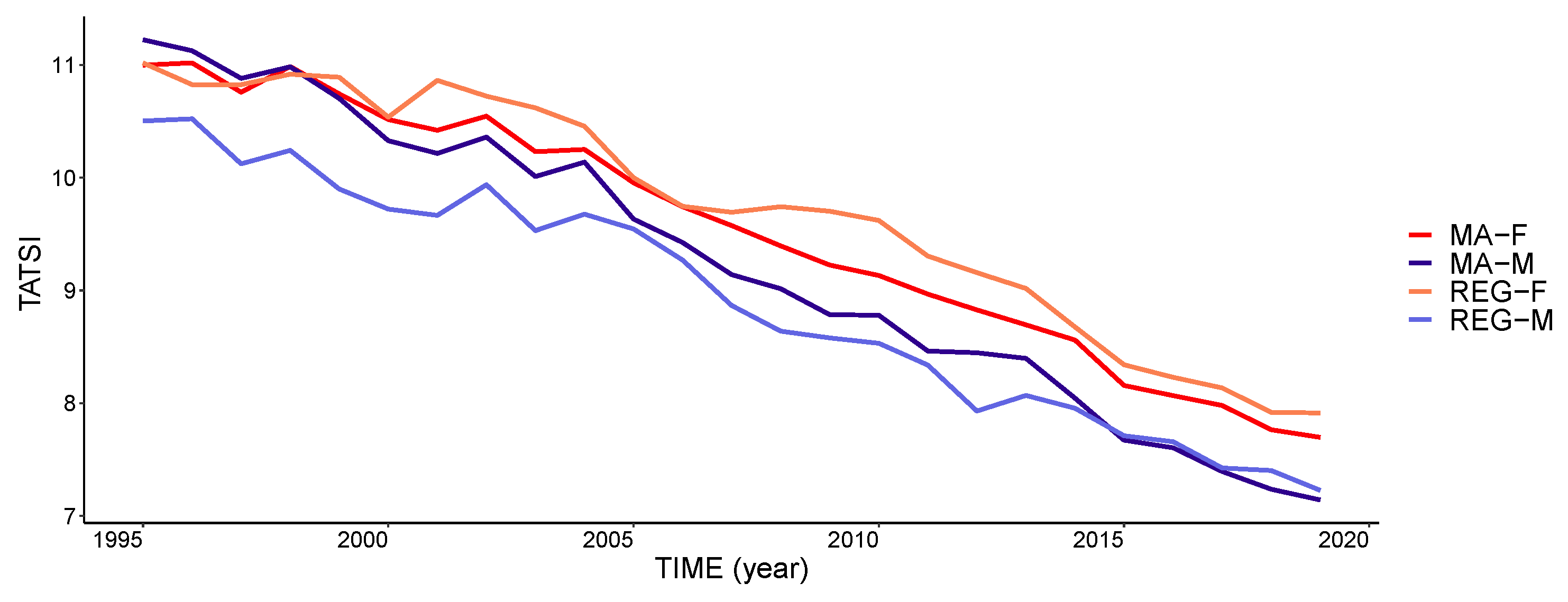

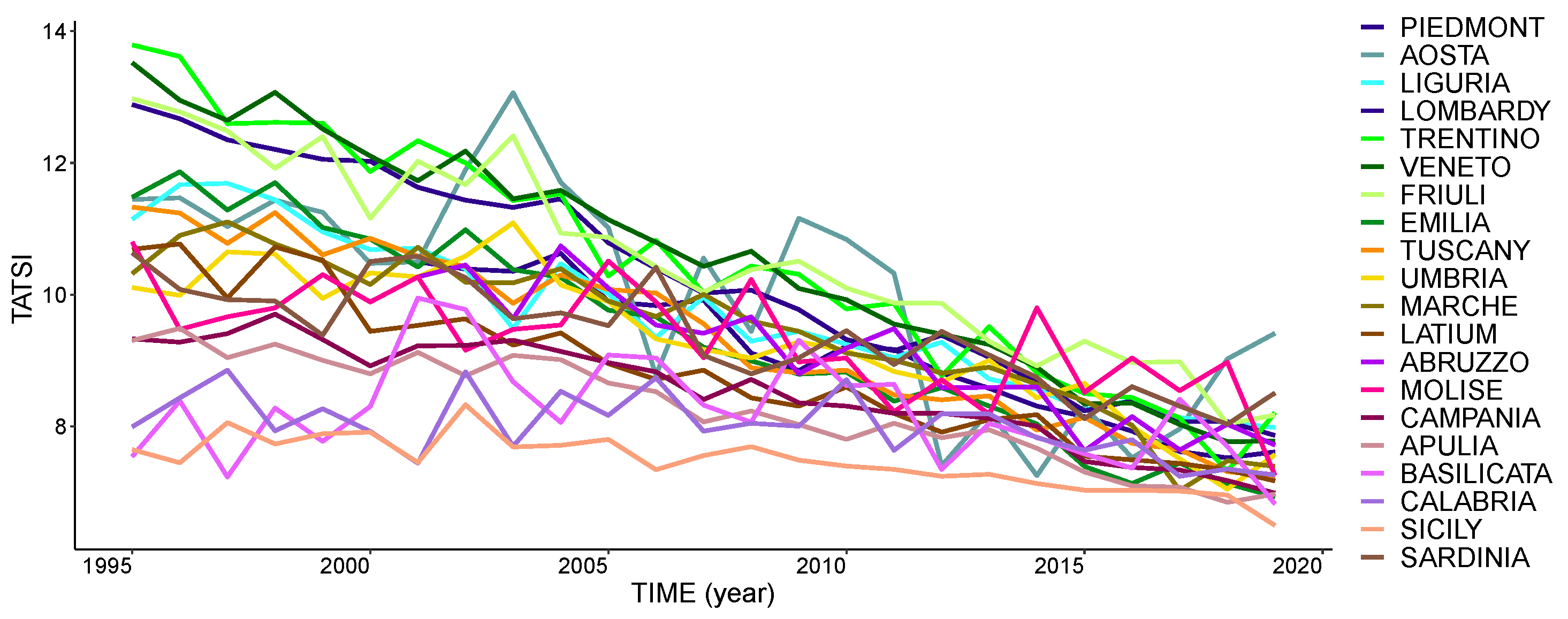

4.2. TATSI Analysis

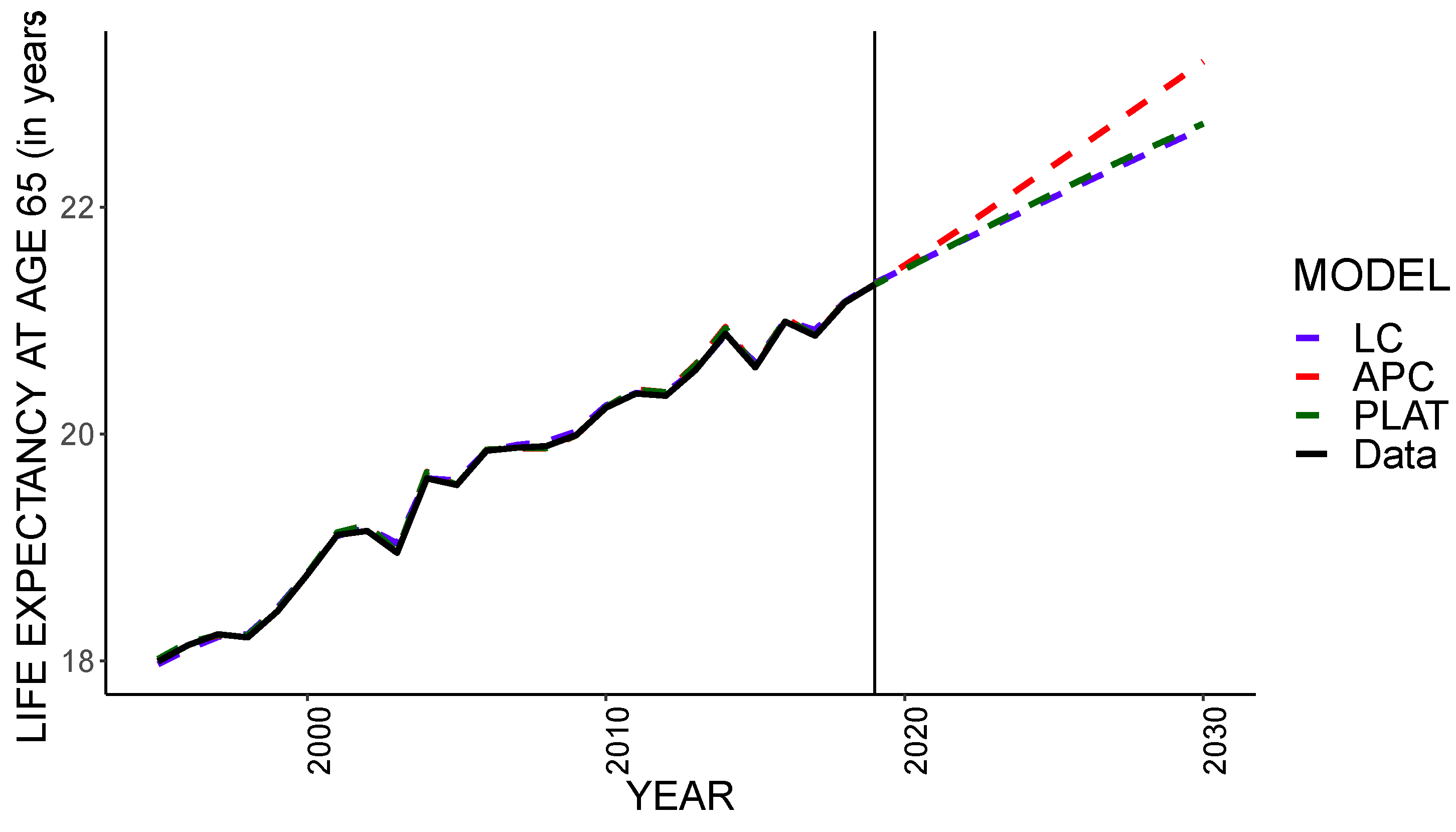

4.3. Projecting TATSI

5. Discussion and Conclusions

Supplementary Materials

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Tax/Subsidy Mechanism at Regional Level

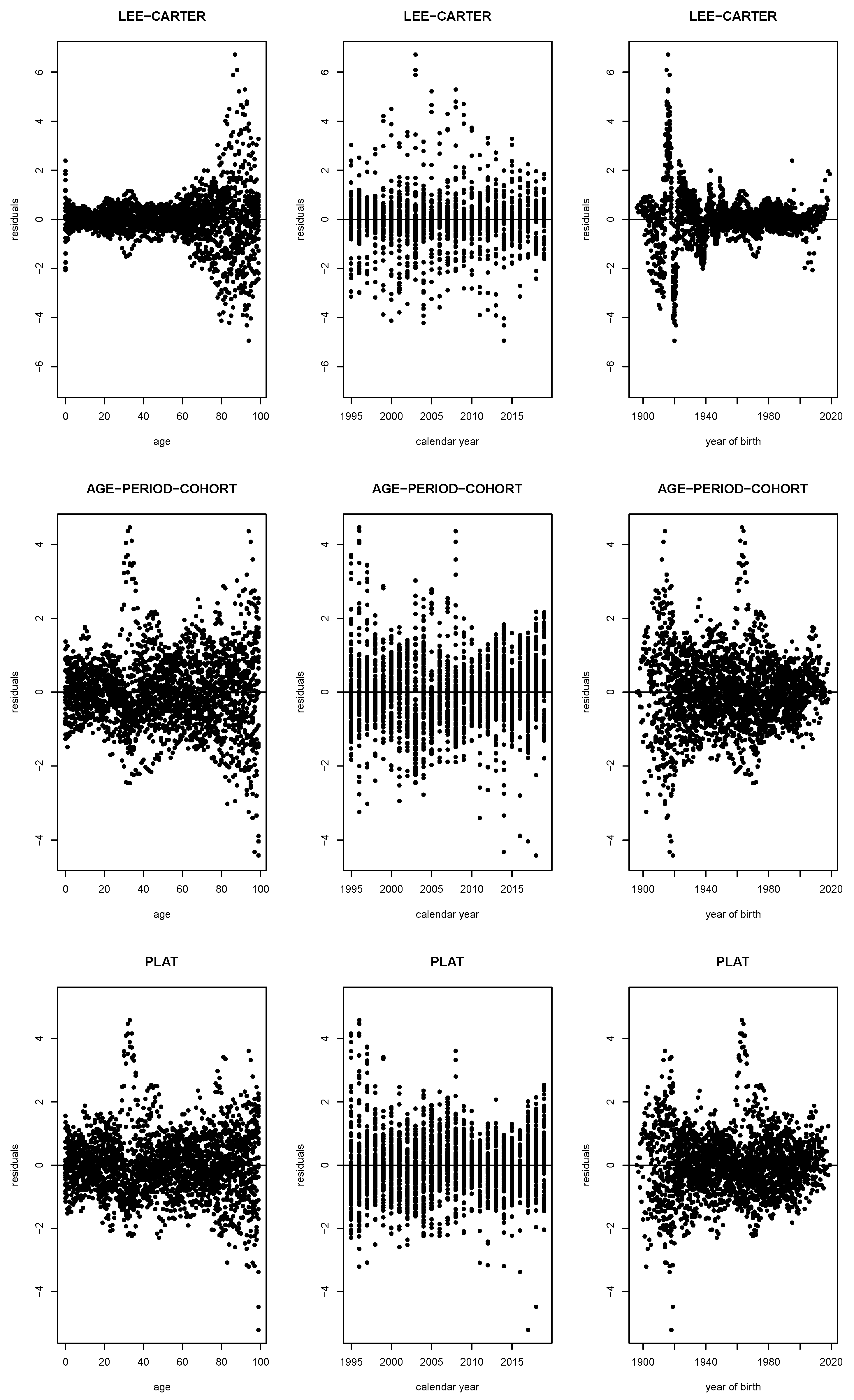

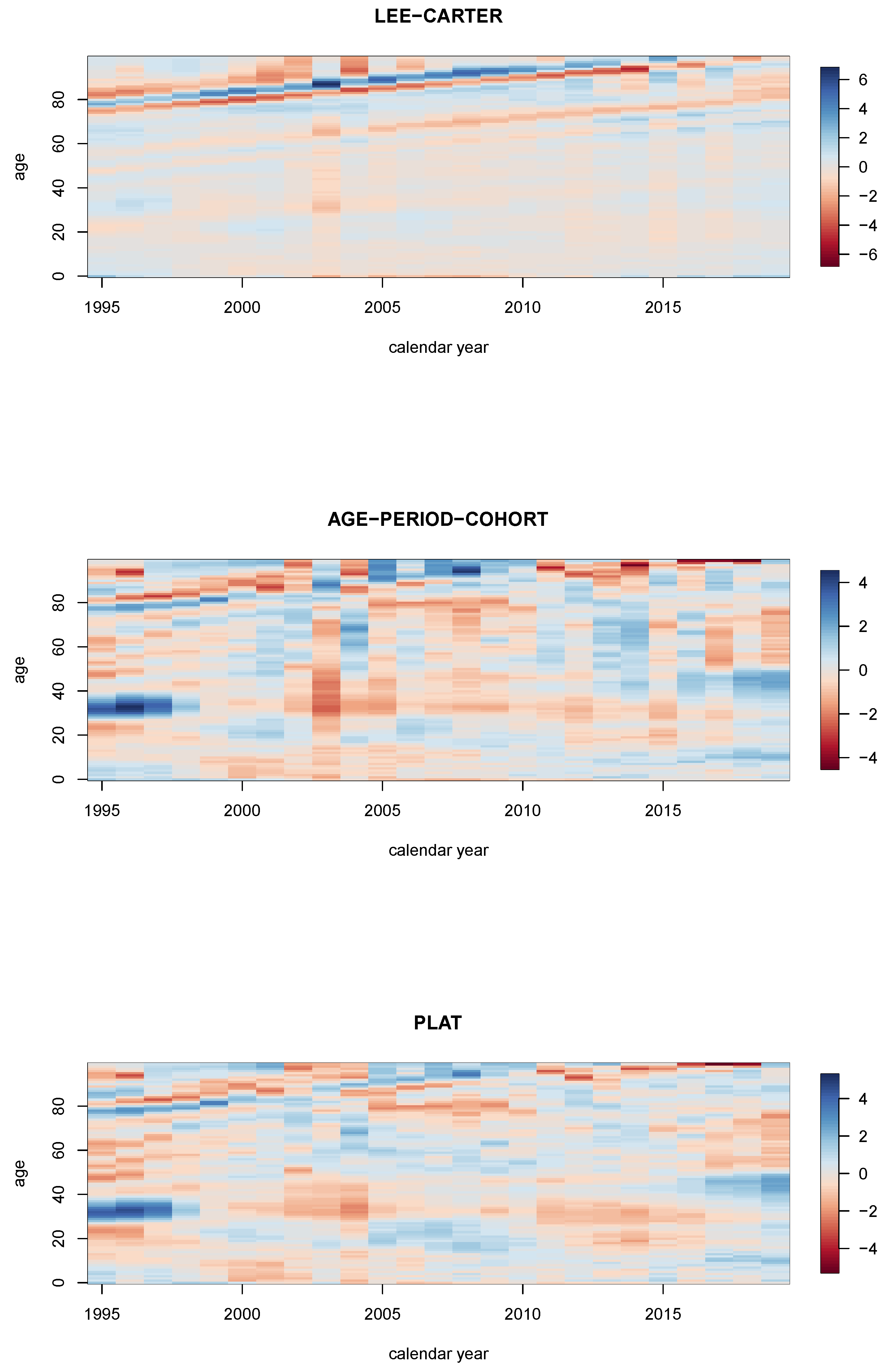

Appendix B. Stochastic Mortality Models

- Lee-Carter (Brouhns et al. 2002, LC):where captures the general shape of mortality by age, is a time index and is its effect across ages. It is assumed that follows a random walk with drift, i.e. where . To ensure model identifiability, the following restrictions are imposed:

- Age-Period-Cohort (Hunt and Blake 2015, APC):where captures the cohort effect and indexes cohorts. It is assumed that follows an ARIMA(1,1,0) with drift. As in (Cairns et al. 2009), the following is imposed to ensure identifiability:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| MODEL | AIC | BIC |

|---|---|---|

| Lee-Carter | 22,129.5 | 23,428.2 |

| Age-Period Cohort | 19,465.4 | 20,898.1 |

| Platen | 19,342.2 | 20,908.8 |

References

- Antonovsky, Aaron. 1967. Social class, life expectancy and overall mortality. The Milbank Memorial Fund Quarterly 45: 31–73. [Google Scholar] [CrossRef]

- Auerbach, Alan, Kermin Charles, Courtney Coile, William Gale, Dana Goldman, Ronald Lee, and Donald Weil. 2017. How the growing gap in life expectancy may affect retirement benefits and reforms. The Geneva Papers on Risk and Insurance-Issues and Practice 42: 475–99. [Google Scholar] [CrossRef]

- Ayuso, Mercedes, Jorge Miguel Bravo, and Robert Holzmann. 2017a. On the Heterogeneity in Longevity among Socioeconomic Groups. Global Journal of Human Social Science Research 17: 33–58. [Google Scholar]

- Ayuso, Mercedes, Jorge Miguel Bravo, and Robert Holzmann. 2017b. Addressing Longevity Heterogeneity in Pension Scheme Design. Journal of Finance and Economics 6: 1–21. [Google Scholar] [CrossRef]

- Ayuso, Mercedes, Jorge Miguel Bravo, and Robert Holzmann. 2020. Getting life expectancy estimates right for pension policy: Period versus cohort approach. Journal of Pension Economics and Finance 1: 1–20. [Google Scholar]

- Belloni, Michele, and Carlo Maccheroni. 2013. Actuarial fairness when longevity increases: An evaluation of the Italian pension system. The Geneva Papers on Risk and Insurance-Issues and Practice 38: 638–74. [Google Scholar] [CrossRef]

- Belloni, Michele, Rob Alessie, Adrian Kalwij, and Chiara Marinacci. 2013. Lifetime income and old age mortality risk in Italy over two decades. Demographic Research 29: 1261–98. [Google Scholar] [CrossRef]

- Bravo, Jorge Miguel, and Jose Herce. 2020. Career breaks, Broken pensions? Long-run effects of early and late-career unemployment spells on pension entitlements. Journal of Pension Economics and Finance 1: 1–27. [Google Scholar] [CrossRef]

- Boskin, Michael, Laurence Kotlikoff, Douglas Puffert, and John Shoven. 1987. Social Security: A Financial Appraisal Across and Within Generations. National Tax Journal 40: 1–19. [Google Scholar] [CrossRef]

- Brouhns, Natasha, Michel Denuit, and Jeroen Vermunt. 2002. A Poisson log-bilinear regression approach to the construction of projected lifetables. Insurance: Mathematics and Economics 31: 373–93. [Google Scholar] [CrossRef]

- Cairns, Andrew, David Blake, Kevin Dowd, Guy Coughlan, David Epstein, Alen Ong, and Igor Balevich. 2009. A quantitative comparison of stochastic mortality models using data from England and Wales and the United States. North American Actuarial Journal 13: 1–35. [Google Scholar] [CrossRef]

- Caselli, Graziella. 1983. Il contributo dell’analisi per generazioni allo studio della geografia della mortalita’. Genus 39: 37–60. [Google Scholar] [PubMed]

- Caselli, Graziella, and Alessandra Reale. 1999. Does cohort analysis contribute to the study of the geography of mortality? Genus 55: 27–59. [Google Scholar]

- Caselli, Graziella, and Rosa Maria Lipsi. 2006. Survival differences among the oldest old in Sardinia: Who, what, where, and why? Demographic Research 14: 267–94. [Google Scholar] [CrossRef]

- Caselli, Graziella, Franco Peracchi, Elisabetta Barbi, and Rosa Maria Lipsi. 2003a. Differential mortality and the design of the Italian system of public pensions. Labour 17: 45–78. [Google Scholar] [CrossRef]

- Caselli, Graziella, Loredana Cerbara, Frank Heinsg, and Rosa Maria Lipsi. 2003b. What impact do contextual variables have on the changing geography of mortality in Italy? European Journal of Population 19: 339–73. [Google Scholar] [CrossRef]

- Case, Anne, and Angus Deaton. 2015. Rising morbidity and mortality in midlife among white non-Hispanic Americans in the 21st century. Proceedings of the National Academy of Sciences of the United States of America 112: 15078–83. [Google Scholar] [CrossRef] [PubMed]

- Chetty, Raj, Michael Stepner, Sarah Abraham, Shelby Lin, Benjamin Scuderi, Nicholas Turner, and David Cutler. 2016. The association between income and life expectancy in the United States, 2001–2014. JAMA 315: 1750–66. [Google Scholar] [CrossRef]

- Conti, Stefano, Gino Farchi, Maria Masocco, Giada Minelli, Virgilia Toccaceli, and Maurizio Vichi. 2003. Gender differentials in life expectancy in Italy. European Journal of Epidemiology 18: 107–12. [Google Scholar] [CrossRef]

- Currie, Janet, and Hannes Schwandt. 2016. Mortality inequality: The good news from a county-level approach. Journal of Economic Perspectives 30: 29–52. [Google Scholar] [CrossRef]

- De Vogli, Roberto, Ritesh Mistry, Roberto Gnesotto, and Giovanni Andrea Cornia. 2005. Has the relation between income inequality and life expectancy disappeared? Evidence from Italy and top industrialised countries. Journal of Epidemiology and Community Health 59: 158–62. [Google Scholar] [CrossRef]

- Garrett, Daniel. 1995. The effects of differential mortality rates on the progressivity of social security. Economic Inquiry 33: 457–75. [Google Scholar] [CrossRef]

- Holzmann, Robert, and Edward Palmer. 2006. Pension Reform: Issues and Prospects for Non-Financial Defined Contribution (NDC) Schemes. Washington, DC: The World Bank. [Google Scholar]

- Holzmann, Robert. 2017. The ABCs of nonfinancial defined contribution (NDC) schemes. International Social Security Review 70: 53–77. [Google Scholar] [CrossRef]

- Holzmann, Robert, Jennifer Alonso-García, Heloise Labit-Hardy, and Andres Villegas. 2019. NDC Schemes and Heterogeneity in Longevity: Proposals for Redesign. Social Protection and Jobs Discussion Paper (No. 1913). Washington, DC: World Bank. [Google Scholar]

- Hunt, Andrew, and David Blake. 2015. Modelling longevity bonds: Analysing the swiss re kortis bond. Insurance: Mathematics and Economics 63: 12–29. [Google Scholar] [CrossRef]

- Lallo, Carlo, and Michele Raitano. 2018. Life expectancy inequalities in the elderly by socioeconomic status: Evidence from Italy. Population Health Metrics 16: 1–21. [Google Scholar] [CrossRef] [PubMed]

- Liu, Yan, Asuna Arai, Koji Kanda, Romeo Lee, Jay Glasser, and Hiko Tamashiro. 2013. Gender gaps in life expectancy: Generalized trends and negative associations with development indices in OECD countries. The European Journal of Public Health 23: 563–68. [Google Scholar] [CrossRef]

- Luy, Marc, Paola Di Giulio, and Graziella Caselli. 2011. Differences in life expectancy by education and occupation in Italy, 1980–1994: Indirect estimates from maternal and paternal orphanhood. Population Studies 65: 137–55. [Google Scholar] [CrossRef] [PubMed]

- Maccheroni, Carlo. 2006. La mortalità differenziale: Un fattore demografico di cui la riforma del sistema previdenziale non tiene conto adeguatamente. Quaderni Europei sul Nuovo Welfare 1: 76–84. [Google Scholar]

- Maccheroni, Carlo. 2009. Una stima della speranza di vita per grado di istruzione in Italia all’inizio degli anni 2000. Polis 23: 127–44. [Google Scholar]

- Maccheroni, Carlo, and Samuel Nocito. 2017. Backtesting the lee–carter and the cairns–blake–dowd stochastic mortality models on italian death rates. Risks 5: 1–23. [Google Scholar] [CrossRef]

- Mackenbach, Johan, Ivana Kulhánová, Barbara Artnik, Matthias Bopp, Carme Borrell, and Tom Clemens. 2016. Changes in mortality inequalities over two decades: Regsister based study of European countries. BMJ 353: i1732. [Google Scholar] [CrossRef]

- Materia, Enrico, Laura Cacciani, Giulio Bugarini, Giulia Cesaroni, Marina Davoli, Maria Paola Mirale, and Carlo Perucci. 2005. Income inequality and mortality in Italy. The European Journal of Public Health 15: 411–17. [Google Scholar] [CrossRef]

- Mazzaferro, Carlo, Marcello Morciano, and Marco Savegnago. 2012. Differential mortality and redistribution in the Italian notional defined contribution system. Journal of Pension Economics and Finance 11: 500–30. [Google Scholar] [CrossRef][Green Version]

- Millossovich, Pietro, Andres Villegas, and Vladimir Kaishev. 2018. Stmomo: An r package for stochastic mortality modelling. Journal of Statistical Software 84: 1–39. [Google Scholar]

- Murtin, Fabrice, Johan Mackenbach, Domandas Jasilionis, and Marco Mira d’Ercole. 2017. Inequalities in Longevity by Education in OECD Countries: Insights from New OECD Estimates. OECD Statistics Working Papers. Paris: OECD. [Google Scholar]

- Natale, Marcelo, and Amedeo Bernassola. 1973. La Mortalità per causa Nelle Regioni Italiane: Tavole per Contemporanei 1965–1966 e per Generazioni 1790–1964. Roma: Facoltà di Scienze Statistiche Demografiche ed Attuariali, Università di Roma. [Google Scholar]

- Oeppen, Jim, and James Vaupel. 2002. Enhanced: Broken limits to life expectancy. Science 296: 1029–31. [Google Scholar] [CrossRef] [PubMed]

- Plat, Richard. 2009. On stochastic mortality modeling (2009). Insurance: Mathematics and Economics 45: 393–404. [Google Scholar]

- Robine, Jean Marie, Graziella Caselli, Domenica Rasulo, and Amandine Cournil. 2006. Differentials in the femininity ratio among centenarians: Variations between northern and southern Italy from 1870. Population Studies 60: 99–113. [Google Scholar] [CrossRef]

- Trovato, Frank, and Manoj Lalu. 1996. Narrowing sex differentials in life expectancy in the industrialized world: Early 1970’s to early 1990’s. Social Biology 43: 20–37. [Google Scholar] [CrossRef] [PubMed]

- Whitehouse, E. 2007. Life-Expectancy Risk and Pensions: Who Bears the Burden? OECD Social, Employment, and Migration Working Papers OECD 60. Paris: OECD. [Google Scholar]

- Whitehouse, Edward, and Asghar Zaidi. 2008. Socio-Economic Differences in Mortality: Implications for Pensions Policy. OECD Social, Employment, and Migration Working Papers OECD 71. Paris: OECD. [Google Scholar]

| Reference | Socioeconomic Dimension | Dataset | Time Period |

|---|---|---|---|

| Natale and Bernassola (1973) | Gender | 1790–1964 | |

| Caselli (1983) | Cohort | Regional Mortality Tables | 1882–1953 |

| Caselli (1999) | Gender, Geography | Regional Mortality Tables | 1952–1992 |

| Caselli and Reale (2003a) | Cohort, Gender, Geography | ISTAT | 1887–1997 |

| Caselli et al. (2003b) | Causes of Death, Cohort, Gender, Geography | Provincial Mortality Tables | 1971–73, 1981–83, 1991–93 |

| Conti et al. (2003) | Cause of Death, Gender | ISTAT + ISS | 1970, 1980, 1990, 1997 |

| Materia et al. (2005) | Gender, Income (Inequality) | ISTAT + MEF | 1994 |

| DeVogli et al. (2005) | Income (Inequality) | ISTAT + SHIW + UN | 1995, 1998, 2000, 2001, 2003 |

| Caselli and Lipsi (2006) | Age (80–100), Gender, Sardinia | Provincial Mortality Tables | 1975–1977, 1996–1997, 1998–2000 |

| Robine et al. (2006) | Age (60+), Gender | ISTAT + Census | 1871–2001 |

| Maccheroni (2006) | Education, Gender, Geography | ISTAT | 1960, 1970, 1980, 1990, 2000 |

| Maccheroni (2009) | Education, Gender | ISTAT + Census | 2001 |

| Luy et al. (2011) | Education, Men, Occupation | ISTAT + Census | 1980–1994 |

| Mazzaferro et al. (2012) | Education, Income | ISTAT | 1975–2000 |

| Belloni et al. (2013) | Income (Quintiles) | INPS | 1979–1990, 1991–2001 |

| Belloni and Maccheroni (2013) | Cohort, Gender, Occupation | INPS + SHIW | 1985–1997 |

| Mackenbach et al. (2016) | Education, Occupation | Turin Mortality Table | 1990–2010 |

| Maccheroni and Nocito (2017) | Gender | ISTAT | 1975–2014 |

| Lallo and Raitano (2018) | Occupation | EU-SILC + INPS | 2005–2009 |

| Macroarea | Regions |

|---|---|

| North-West | Piedmont, Aosta Valley, Liguria, Lombardy. |

| North-East | Provinces of Bolzano and Trento, Veneto, Friuli-Venezia-Giulia, Emilia-Romagna. |

| Center | Tuscany, Umbria, Marche, Latium. |

| Mezzogiorno | Abruzzo, Molise, Campania, Apulia, Basilicata, Calabria, Sicily, Sardinia. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Culotta, F. Life Expectancy Heterogeneity and Pension Fairness: An Italian North-South Divide. Risks 2021, 9, 57. https://doi.org/10.3390/risks9030057

Culotta F. Life Expectancy Heterogeneity and Pension Fairness: An Italian North-South Divide. Risks. 2021; 9(3):57. https://doi.org/10.3390/risks9030057

Chicago/Turabian StyleCulotta, Fabrizio. 2021. "Life Expectancy Heterogeneity and Pension Fairness: An Italian North-South Divide" Risks 9, no. 3: 57. https://doi.org/10.3390/risks9030057

APA StyleCulotta, F. (2021). Life Expectancy Heterogeneity and Pension Fairness: An Italian North-South Divide. Risks, 9(3), 57. https://doi.org/10.3390/risks9030057