Does Working Capital Management Influence Operating and Market Risk of Firms?

Abstract

1. Introduction

2. Theoretical Background and Literature Review

2.1. Theoretical Underpinnings

2.2. Literature Review and Hypotheses Development

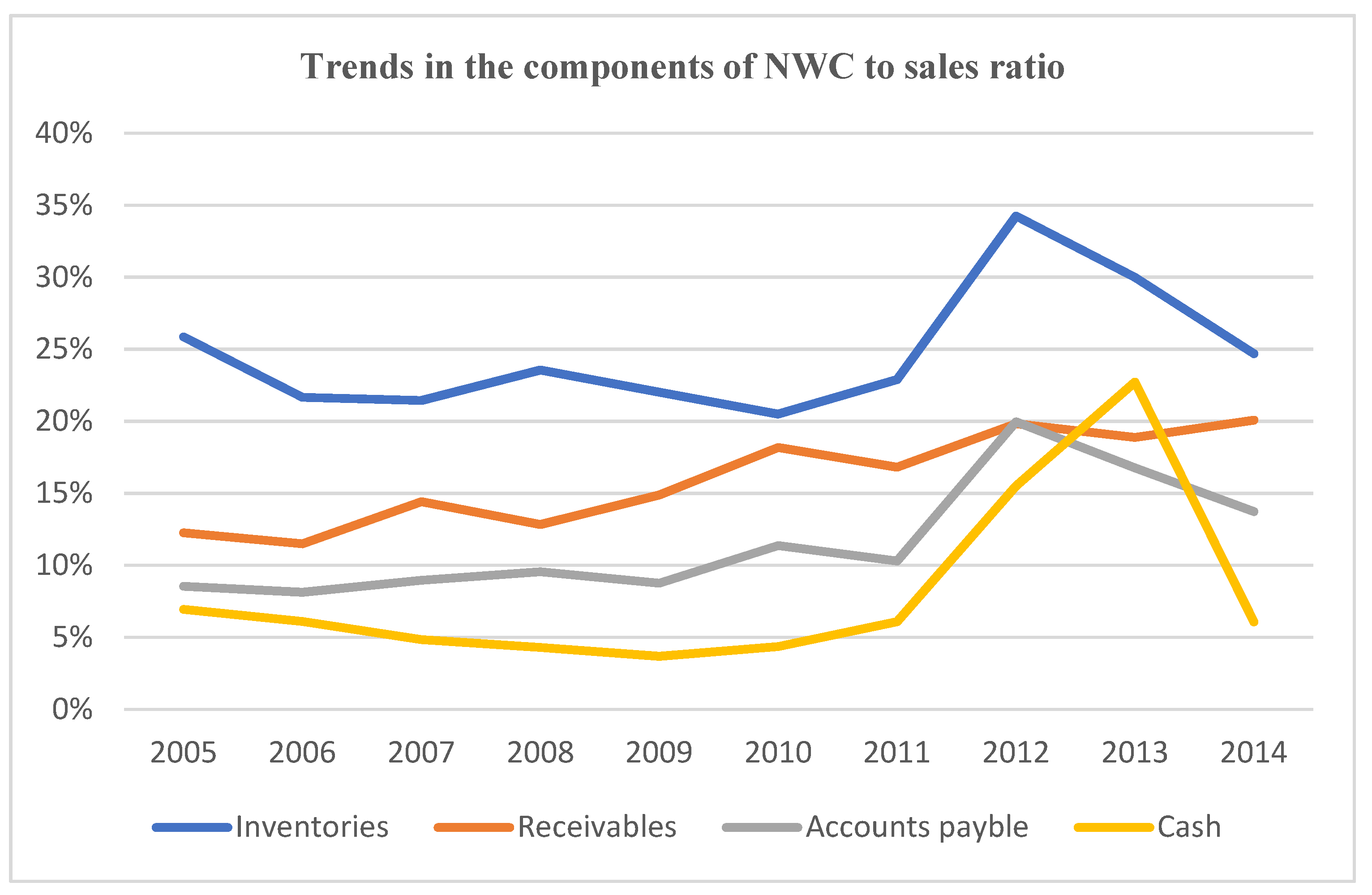

3. Data and Methodology

4. Empirical Strategy

5. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abuzayed, Bana. 2012. Working capital management and firms’ performance in emerging markets: The case of Jordan. International Journal of Managerial Finance 8: 155–79. [Google Scholar] [CrossRef]

- Akbar, Ahsan, Xinfeng Jiang, and Minhas Akbar. 2020a. Do working capital management practices influence investment and financing patterns of firms? Journal of Economic and Administrative Sciences 26: 1026–4116. [Google Scholar] [CrossRef]

- Akbar, Ahsan. 2014. Working capital management and corporate performance: Evidences from textile sector of China. European Academic Research 2: 11440–56. [Google Scholar]

- Akbar, Ahsan. 2021. Does frequent leadership changes influence firm performance? Insights from China. Insights from China 10: 291–98. [Google Scholar]

- Akbar, Minhas, Ahsan Akbar, and Muhammad Umar Draz. 2021. Global Financial Crisis, Working Capital Management, and Firm Performance: Evidence from an Islamic Market Index. Orignal Research 1: 21582440211015705. [Google Scholar] [CrossRef]

- Akbar, Minhas, Ahsan Akbar, Petra Maresova, Minghui Yang, and Hafiz Muhammad Arshad. 2020b. Unraveling the bankruptcy risk‒return paradox across the corporate life cycle. Sustainability 12: 3547. [Google Scholar] [CrossRef]

- Akbar, Minhas, and Ahsan Akbar. 2016. Working capital management and corporate performance in Shariah compliant firms. European Academic Research 4: 1946–65. [Google Scholar]

- Aktas, Nihat, Ettore Croci, and Dimitris Petmezas. 2015. Is working capital management value-enhancing? Evidence from firm performance and investments. Journal of Corporate Finance 30: 98–113. [Google Scholar] [CrossRef]

- Appuhami, BA Ranjith. 2008. The impact of firms’ capital expenditure on working capital management: An empirical study across industries in Thailand. International Management Review 4: 8. [Google Scholar]

- Arcuri, Maria Cristina, and Raoul Pisani. 2021. Is trade credit a sustainable resource for medium-sized italian green companies? Sustainability 13: 2872. [Google Scholar] [CrossRef]

- Armstrong, Christopher S, and Rahul Vashishtha. 2012. Executive stock options, differential risk-taking incentives, and firm value. Journal of Financial Economics 104: 70–88. [Google Scholar] [CrossRef]

- Baños-Caballero, Sonia, Pedro J. García-Teruel, and Pedro Martínez-Solano. 2014. Working capital management, corporate performance, and financial constraints. Journal of Business Research 67: 332–38. [Google Scholar] [CrossRef]

- Chalmers, David K. 2020. Working Capital Management (WCM) and Performance of SMEs: Evidence from India School of Strategy and Business UT Toronto—Canada Luca Sensini Department of Management and Innovation System University of Salerno—Italy Amit Shan BeLab, NIBS New Delhi. International Journal of Business and Social Science 11: 57–63. [Google Scholar] [CrossRef]

- Chen, Hanwen, Daoguang Yang, Joseph H. Zhang, and Haiyan Zhou. 2020. Internal controls, risk management, and cash holdings. Journal of Corporate Finance 64: 101695. [Google Scholar] [CrossRef]

- Ching, Hong Yuh, Ayrton Novazzi, and Fábio Gerab. 2011. Relationship between working capital management and profitability in Brazilian listed companies. Journal of Global Business and Economics 3: 74–86. [Google Scholar]

- Elbadry, Ahmed. 2018. The Determinants of Working Capital Management in the Egyptian SMEs. Accounting and Finance Research 7: 155. [Google Scholar] [CrossRef][Green Version]

- Emery, Gary W. 1984. A pure financial explanation for trade credit. Journal of Financial and Quantitative Analysis 19: 271–85. [Google Scholar] [CrossRef]

- GAPENSKI, LOUIS C. 1999. Debt-maturity structures should match risk preferences. Healthcare Financial Management 53: 56. [Google Scholar]

- Gill, Amarjit, Nahum Biger, and Neil Mathur. 2010. The relationship between working capital management and profitability: Evidence from the United States. Business and Economics Journal 10: 1–9. [Google Scholar]

- Gounopoulos, Dimitrios, Antonios Kallias, Konstantinos Kallias, and Panayiotis G. Tzeremes. 2017. Political money contributions of U.S. IPOs. Journal of Corporate Finance 43: 19–38. [Google Scholar] [CrossRef]

- Gupta, Ranjan Das, and Rajesh Pathak. 2018. Firm’s risk-return association facets and prospect theory findings-an emerging versus developed country context. Risks 6: 143. [Google Scholar] [CrossRef]

- Haj-Salem, Issal, and Khaled Hussainey. 2021. Risk Disclosure and Corporate Cash Holdings. Journal of Risk and Financial Management 14: 328. [Google Scholar] [CrossRef]

- Hussain, Sarfraz, Quang Minh Nguyen, Huu Tinh Nguyen, and Thu Thuy Nguyen. 2021. Macroeconomic factors, working capital management, and firm performance—A static and dynamic panel analysis. Humanities and Social Sciences Communications 8: 1–14. [Google Scholar] [CrossRef]

- Javeed, Sohail Ahmad, Rashid Latief, and Lin Lefen. 2020. An analysis of relationship between environmental regulations and firm performance with moderating effects of product market competition: Empirical evidence from Pakistan. Journal of Cleaner Production 254: 120197. [Google Scholar] [CrossRef]

- Kamath, Ravindra. 1989. How useful are common liquidity measures. Journal of Cash Management 9: 24–28. [Google Scholar]

- Kasozi, Jason. 2017. The effect of working capital management on profitability: A case of listed manufacturing firms in South Africa. Investment Management and Financial Innovations 14: 336–46. [Google Scholar] [CrossRef]

- Kassi, Diby François, Dilesha Nawadali Rathnayake, Pierre Axel Louembe, and Ning Ding. 2019. Market risk and financial performance of non-financial companies listed on the Moroccan stock exchange. Risks 7: 20. [Google Scholar] [CrossRef]

- Kaushik, Nikhil, and Swati Chauhan. 2019. The Role of Financial Constraints in the Relationship Between Working Capital Management and Firm Performance. Journal of Asset Management 25: 60. [Google Scholar]

- Kayani, Umar Nawaz, Tracy-Anne De Silva, and Christopher Gan. 2020. Working capital management and firm performance relationship: An empirical investigation of Australasian firms. Review of Pacific Basin Financial Markets and Policies 23: 1–23. [Google Scholar] [CrossRef]

- Khan, Nawab, Minhas Akbar, and Ahsan Akbar. 2016. Does an optimal working capital exist? The role of financial constraints. Research Journal of Finance and Accounting 7: 131–36. [Google Scholar]

- Kieschnick, Robert, Mark Laplante, and Rabih Moussawi. 2013. Working capital management and shareholders’ wealth. Review of Finance 17: 1827–52. [Google Scholar] [CrossRef]

- Le, Ben. 2019. Working capital management and firm’s valuation, profitability and risk: Evidence from a developing market. International Journal of Managerial Finance 15: 191–204. [Google Scholar] [CrossRef]

- Lukason, Oliver, and María-del-Mar Camacho-Miñano. 2019. Bankruptcy risk, its financial determinants and reporting delays: Do managers have anything to hide? Risks 7: 77. [Google Scholar] [CrossRef]

- Lyngstadaas, Hakim, and Terje Berg. 2016. Working capital management: Evidence from Norway. International Journal of Managerial Finance 12: 295–313. [Google Scholar] [CrossRef]

- Michaelas, Nicos, Francis Chittenden, and Panikkos Poutziouris. 1998. A model of capital structure decision making in small firms. Journal of Small Business and Enterprise Development 5: 246–60. [Google Scholar] [CrossRef]

- Mohamad, Nor Edi Azhar Binti, and Noriza Binti Mohd Saad. 2010. Working Capital Management: The Effect of Market Valuation and Profitability in Malaysia. International Journal of Business and Management 5: 140. [Google Scholar] [CrossRef]

- Opler, Tim, Lee Pinkowitz, René Stulz, and Rohan Williamson. 1999. The determinants and implications of corporate cash holdings. Journal of Financial Economics 52: 3–46. Available online: https://econpapers.repec.org/RePEc:eee:jfinec:v:52:y:1999:i:1:p:3-46 (accessed on 25 August 2021). [CrossRef]

- Nazir, Mian Sajid, and Talat Afza. 2009. Impact of Aggressive Working Capital Management Policy on Firms’ Profitability. IUP Journal of Applied Finance 15: 19–30. [Google Scholar]

- Osisioma, B. C. 1997. Sources and management of working capital. Journal of Management Sciences 2: 21–26. [Google Scholar]

- Petersen, Mitchell A., and Raghuram G. Rajan. 1997. Trade Credit: Theories and Evidence. Review of Financial Studies 10: 661–91. Available online: https://econpapers.repec.org/RePEc:oup:rfinst:v:10:y:1997:i:3:p:661-91 (accessed on 15 June 2021). [CrossRef]

- Prasad, Punam, Sivasankaran Narayanasamy, Samit Paul, Subir Chattopadhyay, and Palanisamy Saravanan. 2019. Review of Literature on Working Capital Management and Future Research Agenda. Journal of Economic Surveys 33: 827–61. [Google Scholar] [CrossRef]

- ur Rahman, Shams, Khurshed Iqbal, and Aamir Nadeem. 2019. Effect of Working Capital Management on Firm Performance: The Role of Ownership Structure. Global Social Sciences Review 4: 75–83. [Google Scholar] [CrossRef]

- Razi, Nazila, Elizabeth More, and Gensheng Shen. 2021. Risk Implications for the Role of Budgets in Implementing Post-Acquisition Systems Integration Strategies. Journal of Risk and Financial Management 14: 323. [Google Scholar] [CrossRef]

- Rubino, Michele. 2018. Comparison of the Main ERM Frameworks: How Limitations and Weaknesses can be Overcome Implementing IT Governance. International Journal of Business and Management 13: 139. [Google Scholar] [CrossRef]

- Ruiz-Canela López, José. 2021. How Can Enterprise Risk Management Help in Evaluating the Operational Risks for a Telecommunications Company? Journal of Risk and Financial Management 14: 139. [Google Scholar] [CrossRef]

- Sagan, John. 1955. Toward a theory of working capital management. The Journal of finance 10: 121–29. [Google Scholar] [CrossRef]

- Sohail, Sundas, Farhat Rasul, and Ummara Fatima. 2016. Effect of Aggressive & Conservative Working Capital Management Policy on Performance of Scheduled Commercial Banks of Pakistan. European Journal of Business and Management 8: 40–48. Available online: www.iiste.org (accessed on 17 July 2021).

- Soukhakian, Iman, and Mehdi Khodakarami. 2019. Working capital management, firm performance and macroeconomic factors: Evidence from Iran. Cogent Business & Management 6: 1–24. [Google Scholar] [CrossRef]

- Tauringana, Venancio, and Godfred Adjapong Afrifa. 2013. The relative importance of working capital management and its components to SMEs’ profitability. Journal of Small Business and Enterprise Development 20: 453–69. [Google Scholar] [CrossRef]

- Tzeremes, Panayiotis. 2020. Productivity, efficiency and firm’s market value: Microeconomic evidence from multinational corporations. Bulletin of Applied Economics 10: 95–105. [Google Scholar]

- Van Horne, James C. 1969. A risk-return analysis of a firm’s working-capital position. The Engineering Economist 14: 71–89. [Google Scholar] [CrossRef]

- Van Horne, James C. 1980. An application of the capital asset pricing model to divisional required returns. Financial Management 9: 14–19. [Google Scholar] [CrossRef]

- Wang, Zanxin, Minhas Akbar, and Ahsan Akbar. 2020. The interplay between working capital management and a firm’s financial performance across the corporate life cycle. Sustainability 12: 1661. [Google Scholar] [CrossRef]

- Wanyoike, Hellen W., Samuel O. Onyuma, and James N. Kung’u. 2021. Working capital management practices and operational performance of selected supermarkets with national network. International Journal of Research in Business and Social Science 10: 72–85. [Google Scholar] [CrossRef]

- Wintoki, M Babajide, James S Linck, and Jeffry M Netter. 2012. Endogeneity and the dynamics of internal corporate governance. Journal of Financial Economics 105: 581–606. [Google Scholar] [CrossRef]

- Xing, Haipeng, and Yang Yu. 2018. Firm’s credit risk in the presence of market structural breaks. Risks 6: 136. [Google Scholar] [CrossRef]

{kind=link}

| Industry | (1) 2005 | (2) 2014 | (3) | (4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Median | S.D. | N | Median | S.D. | N | Slope Median | p-Value | Slope S.D. | p-Value | |

| Chemical and Pharmaceutical | 16.1% | 20% | 35 | 22.4% | 25.5% | 41 | 0.4403 | 0.0807 | −0.4665 | 0.3822 |

| Coke and Petroleum | 5.4% | 7.5% | 9 | 7.7% | 13.9 | 9 | 0.1927 | 0.3039 | 0.9080 | 0.0112 |

| Electric and Apparatus | 26.4% | 30.2% | 7 | 74.7% | 145.5% | 7 | 5.6009 | 0.0000 | 9.8053 | 0.0053 |

| Food Sector | 14.0% | 26.5% | 43 | 14.0% | 22.8% | 44 | 0.2279 | 0.5537 | 0.4882 | 0.5060 |

| Fuel and Energy | 14.5% | 32.5% | 14 | 32.5% | 91.9% | 17 | 2.3302 | 0.0210 | −5.1648 | 0.4020 |

| Information and Transport | 10.5% | 12.2% | 10 | 2.7% | 12.0% | 13 | −0.2739 | 0.3356 | 0.1244 | 0.8454 |

| Motor Vehicle | 18.2% | 73.9% | 21 | 22.4% | 36.1% | 21 | 0.8470 | 0.0322 | 4.9628 | 0.2130 |

| Other Manufacturing | 22.8% | 24.4% | 26 | 24.2% | 109.3% | 28 | 0.5006 | 0.0409 | 9.9805 | 0.0153 |

| Other Services activities | 8.2% | 10.9 | 6 | 15.5% | 89.6 | 8 | 0.3817 | 0.3315 | 12.1277 | 0.0368 |

| Textile Sector | 32.3% | 25.8% | 134 | 18.6% | 44.3% | 124 | −1.1753 | 0.0076 | 3.2656 | 0.0003 |

| Non-Metallic | 3.0% | 92.3% | 22 | 8.7% | 13.8% | 27 | 0.5846 | 0.0028 | −6.2022 | 0.0133 |

| Paper and Board | 22.5% | 9.6% | 7 | 25% | 113.8% | 7 | 0.7552 | 0.4138 | 14.9749 | 0.0024 |

| Variable | Description | Calculation | Expected Sign |

|---|---|---|---|

| Dependent variables: MR | Market Risk | The standard deviation of the mean of annualized stock returns. | Both excessively high as well as excessively low levels of working capital can increase the perceived risk of a firm’s stocks. |

| VONOI | Variability of Net Operating Income | The standard deviation of net operating profit for each firm during the sampled period. | Lower working capital levels can trigger variations in the profitability of a firm; hence, a negative relation is expected between the level of working capital and volatility in operating profits. |

| Independent variables: ENWC | Excess Net Working Capital to sales ratio | Firm net working capital to sales—industry mean networking capital to sales ratio | Higher ENWC is expected to mitigate the perceived risk of going bankrupt in the short-term. |

| NTC | Net Trade Cycle | Days account receivable + Days inventory—Days account payables | A larger NTC ensures that the firm has a sufficient number of liquid resources to fulfill short-term obligations, thus minimizing firm risk. |

| DAR | Days Account Receivables | (Account receivables/sales) × 365 | Larger DAR can increase the possibility of doubtful debts, leading to an increase in operating and market risk. |

| DI | Days Inventory | (Inventory/Sales) × 365 | Days inventories are expected to be positively linked to firm risk. |

| DAP | Days Account Payables | (Account payables/sales) × 365 | The larger DAP will provide liquidity to the firm for a longer time, thus resulting in a lower perceived risk of a short-term liquidity crunch. |

| CR | Current Ratio | Current assets/Current liabilities | A higher value of current assets will indicate that enough current assets are available to satisfy short-term obligations, consequently minimizing risk exposure. |

| QR | Quick Ratio | (Cash + receivables + Short-term investments)/Current liabilities | Holding a reasonable amount of liquid assets can ensure the smooth functioning of operations, resulting in lower risk. |

| CATS | Current Assets to Sales Ratio | Current assets/sales | The more current assets employed to generate sales, the lower the firm’s operating and market risk. |

| CTCA | Cash to Current Assets Ratio | Cash/Current Assets | Larger cash deflated by current assets shows financial stability and can instantly help firms meet unexpected liquidity requirements. |

| CTS | Cash to Sales Ratio | Cash/Sales | Larger cash to sales shows the availability of idle funds, therefore a negative sign is expected with firm risk. |

| Control variables: | |||

| Size | Size of the Company | Natural log of total assets | A negative relationship is likely between the size of a firm and its operating and market risk. |

| Lev | Leverage | Total debt/total assets | Higher debt levels increase the risk perception of a firm’s stock in the market. |

| Age | Age of the Firm | Number of years since the inception of the company | MR and VONOI have a negative relation with the age of the firm. |

| TQ | Tobin’s Q | The market value of equity/book value of total assets | A positive sign is anticipated from TQ with MR and VONOI. |

| Growth | Sales Growth of the Firm | Current year sales and previous year sales/Current year sales | Higher sales growth minimizes the risk of the firm. |

| GDP | Gross Domestic Product of Pakistan Economy | Current year’s GDP minus previous year’s GDP divided by previous year’s GDP. | Better economic conditions decrease the riskiness for the firm. |

| ICR | Interest Coverage Ratio | EBIT/Interest | The higher the ratio, the lower the risk. |

| Variable | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| MR | 3123 | 0.607 | 0.388 | 0.152 | 1.685 |

| VONOI | 3123 | 0.339 | 0.307 | 0.067 | 1.297 |

| NWC to sales ratio | 3123 | 0.248 | 0.206 | 0.007 | 0.781 |

| NTC | 3123 | 0.905 | 0.75 | 0.026 | 2.85 |

| DI | 3123 | 0.734 | 0.585 | 0.042 | 2.291 |

| DAR | 3123 | 0.414 | 0.446 | 0.006 | 1.693 |

| DAP | 3123 | 0.28 | 0.302 | 0.018 | 1.125 |

| CR | 3123 | 1.301 | 0.892 | 0.26 | 3.86 |

| QR | 3123 | 0.493 | 0.55 | 0.01 | 2.11 |

| CTCA | 3122 | 0.071 | 0.092 | 0.002 | 0.338 |

| CTS | 3122 | 0.034 | 0.048 | 0.001 | 0.186 |

| Size | 3123 | 14.477 | 1.381 | 12.015 | 17.062 |

| Leverage | 3123 | 0.622 | 0.262 | 0.18 | 1.26 |

| Age | 3123 | 32.329 | 14.368 | 12 | 60 |

| TQ | 3123 | 1.088 | 0.97 | 0.106 | 4.033 |

| Growth | 3123 | 0.136 | 0.292 | −0.441 | 0.803 |

| ATR | 3123 | 1.116 | 0.682 | 0.14 | 2.68 |

| GDP | 3123 | 4.355 | 1.649 | 1.596 | 7.667 |

| ROA | 3123 | 4.752 | 10.841 | −14.35 | 29.33 |

| COEF | 3122 | 0.055 | 0.038 | 0.001 | 0.128 |

| ICR | 3123 | 7.853 | 21.346 | −12.639 | 84.865 |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| LMR | 0.141 *** | 0.142 *** | 0.135 *** | 0.138 *** | 0.144 *** |

| (15.64) | (15.77) | (23.96) | (18.95) | (19.59) | |

| ENWC | −0.056 * | ||||

| (−1.74) | |||||

| NTC | −0.042 *** | ||||

| (−4.80) | |||||

| DI | −0.081 *** | ||||

| (−12.18) | |||||

| DAR | 0.069 *** | ||||

| (7.79) | |||||

| DAP | −0.079 *** | ||||

| (−6.90) | |||||

| CR | −0.116 *** | ||||

| (−15.80) | |||||

| QR | 0.130 *** | ||||

| (13.51) | |||||

| CTCA | 0.743 *** | ||||

| (13.23) | |||||

| CATS | −0.949 *** | ||||

| (−9.62) | |||||

| Size | 0.049 * | 0.049 * | 0.090 *** | 0.094 *** | 0.159 *** |

| (1.93) | (1.91) | (7.02) | (4.51) | (8.40) | |

| Lev | 0.024 | 0.048 | 0.005 | −0.144 *** | 0.046 |

| (0.61) | (1.15) | (0.18) | (−3.90) | (1.49) | |

| Age | 0.010 ** | 0.011 ** | 0.011 *** | 0.004 | 0.006 |

| (2.05) | (2.20) | (3.38) | (1.35) | (1.64) | |

| TQ | 0.111 *** | 0.102 *** | 0.104 *** | 0.107 *** | 0.110 *** |

| (20.17) | (19.98) | (26.04) | (22.38) | (23.42) | |

| Growth | −0.007 | −0.016 ** | −0.015 *** | 0.002 | 0.002 |

| (−1.04) | (−2.55) | (−3.57) | (0.32) | (0.29) | |

| GDP | −0.045 | −0.061 * | −0.076 *** | −0.034 | −0.081 *** |

| (−1.24) | (−1.65) | (−3.66) | (−1.31) | (−3.07) | |

| ICR | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** | 0.001 *** |

| (3.15) | (3.38) | (7.26) | (5.36) | (3.86) | |

| N | 2465 | 2465 | 2465 | 2465 | 2463 |

| ar2 | −0.883 | −0.862 | −0.936 | −0.951 | −0.802 |

| ar2p | 0.377 | 0.388 | 0.349 | 0.341 | 0.422 |

| Hansen | 258.211 | 257.578 | 297.091 | 276.964 | 279.318 |

| hansen_df | 231.000 | 231.000 | 287.000 | 259.000 | 259.000 |

| Hansenp | 0.106 | 0.111 | 0.328 | 0.212 | 0.184 |

| (1) | |

|---|---|

| L.Marketrisk | 0.125 *** |

| (41.88) | |

| NTC | −0.011 ** |

| (−2.52) | |

| current | −0.083 *** |

| (−16.44) | |

| acid | 0.092 *** |

| (14.92) | |

| ctca | 0.425 *** |

| (8.04) | |

| cts | −0.820 *** |

| (−6.78) | |

| size1 | 0.080 *** |

| (8.54) | |

| lev | −0.071 *** |

| (−3.78) | |

| Age | 0.003 |

| (1.51) | |

| tobin | 0.099 *** |

| (37.10) | |

| salesgrowth | −0.012 *** |

| (−3.98) | |

| GDPgrowth | −0.055 *** |

| (−3.05) | |

| N | 2463 |

| ar2 | −1.154 |

| ar2p | 0.248 |

| hansen | 315.810 |

| hansen_df | 373.000 |

| hansenp | 0.986 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| ENWC | 0.019 *** | ||||

| (5.15) | |||||

| ENWCD | 0.041 *** | ||||

| (13.08) | |||||

| ENWCD1 | −0.014 ** | ||||

| (−2.09) | |||||

| DI | −0.019 *** | ||||

| (−12.65) | |||||

| DAR | 0.002 *** | ||||

| (2.75) | |||||

| DAP | 0.002 | ||||

| (1.04) | |||||

| CR | −0.008 *** | ||||

| (−4.96) | |||||

| QR | 0.099 *** | ||||

| (76.84) | |||||

| CTCA | −0.238 *** | ||||

| (−14.08) | |||||

| CTS | 0.431 *** | ||||

| (13.58) | |||||

| Size | −0.387 *** | −0.377 *** | −0.361 *** | −0.408 *** | −0.359 *** |

| (−60.41) | (−75.41) | (−89.37) | (−70.40) | (−75.65) | |

| Age | 0.007 *** | 0.006 *** | 0.009 *** | 0.005 *** | 0.009 *** |

| (5.60) | (6.37) | (12.29) | (5.21) | (7.31) | |

| TQ | 0.012 *** | 0.012 *** | 0.011 *** | 0.007 *** | 0.013 *** |

| (8.93) | (11.60) | (12.49) | (4.36) | (11.88) | |

| Growth | 0.008 *** | 0.011 *** | 0.006 *** | 0.006 *** | 0.018 *** |

| (8.12) | (14.19) | (8.24) | (5.63) | (21.40) | |

| GDP | 0.021 ** | 0.027 *** | 0.003 | 0.043 *** | 0.011 |

| (1.99) | (3.66) | (0.52) | (4.60) | (1.32) | |

| COEF | 0.147 *** | 0.181 *** | 0.115 *** | 0.217 *** | 0.153 *** |

| (4.49) | (7.41) | (6.84) | (9.88) | (7.33) | |

| N | 2793 | 2793 | 2793 | 2793 | 2791 |

| ar1 | 0.691 | 0.674 | 0.545 | 0.281 | 0.422 |

| ar1p | 0.490 | 0.500 | 0.586 | 0.779 | 0.673 |

| ar2 | 1.181 | 1.161 | 1.146 | 1.398 | 1.146 |

| ar2p | 0.237 | 0.246 | 0.252 | 0.162 | 0.252 |

| hansen | 211.174 | 234.408 | 263.122 | 226.536 | 231.766 |

| hansen_df | 190.000 | 219.000 | 248.000 | 219.000 | 219.000 |

| hansenp | 0.140 | 0.226 | 0.243 | 0.349 | 0.264 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Akbar, A.; Akbar, M.; Nazir, M.; Poulova, P.; Ray, S. Does Working Capital Management Influence Operating and Market Risk of Firms? Risks 2021, 9, 201. https://doi.org/10.3390/risks9110201

Akbar A, Akbar M, Nazir M, Poulova P, Ray S. Does Working Capital Management Influence Operating and Market Risk of Firms? Risks. 2021; 9(11):201. https://doi.org/10.3390/risks9110201

Chicago/Turabian StyleAkbar, Ahsan, Minhas Akbar, Marina Nazir, Petra Poulova, and Samrat Ray. 2021. "Does Working Capital Management Influence Operating and Market Risk of Firms?" Risks 9, no. 11: 201. https://doi.org/10.3390/risks9110201

APA StyleAkbar, A., Akbar, M., Nazir, M., Poulova, P., & Ray, S. (2021). Does Working Capital Management Influence Operating and Market Risk of Firms? Risks, 9(11), 201. https://doi.org/10.3390/risks9110201