1. Introduction and Main Results

The Heston Model

Heston (

1993) is a widely used stochastic volatility model to price financial options. It consists of two stochastic differential equations (SDEs) for an asset price process

S and its volatility

V:

with

,

,

,

and independent Brownian motions

,

, which are defined on a filtered probability space

, where the filtration satisfies the usual conditions. It is a simple and popular extension of the Black–Scholes model where the volatility of the asset was assumed to be constant. As a consequence, the Heston Model takes the asymmetry and excess kurtosis of financial asset returns into account which are typically observed in real market data. The volatility is given by the so-called Cox–Ingersoll–Ross process (CIR). Its Feller index

will be an important parameter for our results. Throughout this article, the initial values

,

are assumed to be deterministic.

To price options with maturity at time

T, one is interested in the value of

where

is the payoff function. Closed formulae for

are rarely known and often Monte Carlo methods are applied, for which in turn the simulation of

is required. Usually, the log-Heston model instead of the Heston model is considered in numerical practice. This yields the SDE

and the exponential is then incorporated in the payoff, i.e.,

g is replaced by

with

.

While exact simulation schemes and their refinements are known (see, e.g.,

Broadie and Kaya (

2006);

Glasserman and Kim (

2011);

Malham and Wiese (

2013);

Smith (

2007)), discretization schemes as, e.g.,

Altmayer and Neuenkirch (

2017);

Andersen (

2008);

Kahl and Jäckel (

2006);

Lord et al. (

2009), are very popular for the Heston model. The latter discretization schemes can be easily extended to the multi-dimensional case and avoid computational bottlenecks of the exact schemes. In particular, Euler-type methods, such as the fully truncated Euler scheme, seem to be very efficient (see, e.g.,

Coskun and Korn (

2018);

Lord et al. (

2009)), but no weak error analysis is available for them, up to the best of our knowledge.

A second order discretization scheme for the log-Heston model has been introduced in

Andersen (

2008) and analyzed in

Zheng (

2017). The so-called Broadie-Kaya trick and a removal of the drift, detailed in

Section 3.1, reduce the simulation of the log-Heston model to the joint simulation of

Moreover, since the transition density of the CIR process

follows a non-central chi-square distribution, it can be simulated exactly. Trapezoidal discretizations of the first component

lead to the trapezoidal scheme

where

,

and

. This discretization avoids in particular the cumbersome exact simulation of the integrated volatility.

Zheng (

2017) establishes weak order two for polynomial test functions by transferring the error analysis to that of a trapezoidal rule for multidimensional deterministic integrals. Our original intention was to extend this result to a larger class of test functions

f by using the Kolmogorov PDE approach. However, the required Itō-Taylor expansions turned out to be not feasible. So, instead, we analyzed the following two semi-exact discretization schemes: the Euler-type scheme

and the semi-trapezoidal scheme

In both schemes, the CIR process is simulated exactly. In our opinion, the analysis of these schemes gives valuable insights in the weak error analysis of discretization schemes for the log-Heston model and is also a good starting point for the analysis of full Euler-type discretization schemes.

Our error analysis relies on two regularity results for the Heston PDE (

Briani et al. (

2018);

Feehan and Pop (

2013)), the Kolmogorov PDE approach for the weak error analysis from

Talay and Tubaro (

1990), and Malliavin calculus. We also observe the usual trade off between the smoothness assumption on the payoff and the restriction on the Feller index. For payoffs of lower smoothness, a restriction on the Feller index

is required, which arises from the use of Malliavin calculus tools.

In the following, we use the notation

for the maximal step size and the usual notations for the spaces of differentiable functions. In particular, the subscript

c denotes compact support and

denotes polynomial growth. In addition, see

Section 3.1. The results of

Feehan and Pop (

2013) require compact support of the test functions

f, while the results of

Briani et al. (

2018) allow polynomial growth but require higher smoothness for

f.

Theorem 1. Let . (i) If and , then both schemes satisfy (ii) If , then both schemes satisfy Assuming more smoothness of f, we obtain more detailed results:

Theorem 2. Suppose that . (i) Then, the Euler scheme (4) satisfieswhereandfor.

In particular, for an equidistant discretization with,

, we haveHere, u denotes the solution of the associated Kolmogorov PDE; see Equation (7). (ii) For the semi-trapezoidal scheme (5), we havewhereandfor . In particular, for an equidistant discretization , , it holdsHere, u denotes again the solution of the associated Kolmogorov PDE; see Equation (7). Thus, the semi-trapezoidal rule eliminates the first two terms of the error expansion of the Euler scheme.

2. Numerical Results

In this section, we will test numerically whether the convergence rates for the Euler Scheme (

4) and the Semi-Trapezoidal Scheme (

5) are attained even under milder assumptions than those from Theorems 1 and 2. We use the following model parameters:

Model 1: ;

Model 2: ;

Model 3: .

The Feller index is in Model 1, in Model 2, and in Model 3. For each model, we use the following payoff functions:

- 1.

European Call: ;

- 2.

European Put: ;

- 3.

Indicator: .

Note that none of these payoffs satisfies the assumptions of our Theorems. Thus, the presented numerical experiments explore whether the Theorems are valid under milder assumptions. In order to measure the weak error rate, we simulated

independent copies

,

, of

to estimate

by

for each combination of model parameters, functional and number of steps

where

. The number of Monte Carlo samples is chosen in such a way that the Monte Carlo error is sufficiently small enough, i.e., does not dominate the theoretically expected convergence rates. The Monte Carlo mean of these samples was then compared to a reference solution

, i.e.,

and the error

is plotted in

Figure 1,

Figure 2,

Figure 3,

Figure 4,

Figure 5,

Figure 6,

Figure 7,

Figure 8,

Figure 9,

Figure 10,

Figure 11,

Figure 12,

Figure 13,

Figure 14,

Figure 15,

Figure 16,

Figure 17 and

Figure 18. We then measured the rate of convergence, i.e., the decay rate of

, by the slope of a least-squares fit in logarithmic coordinates. The reference solutions can be computed with sufficiently high accuracy from semi-explicit formulae via Fourier methods. In particular, the put price can be calculated from the call-price formula given in

Heston (

1993) via the put-call-parity. The price of the digital option can be computed from the probability

given in

Heston (

1993); it equals

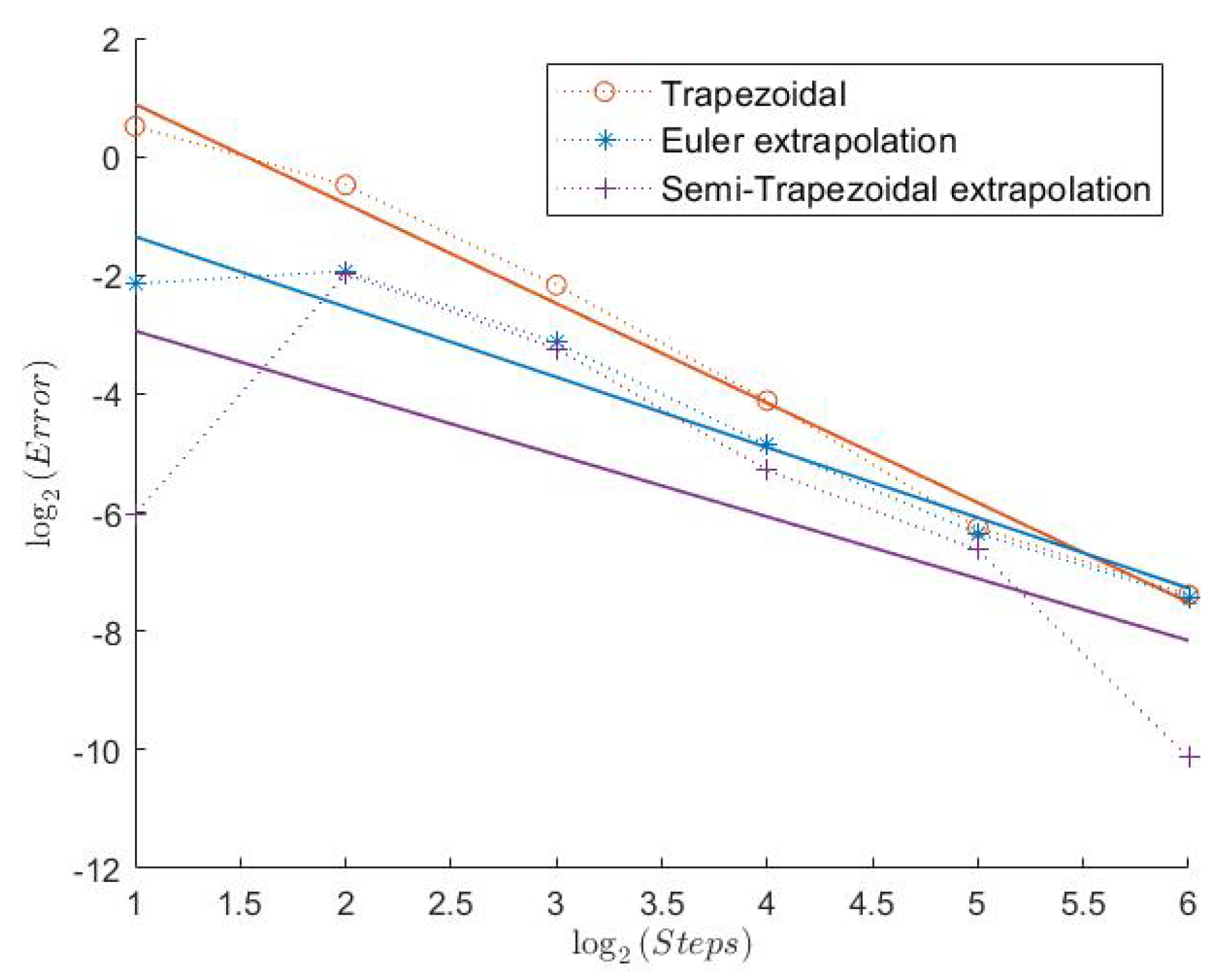

. Additionally to the Euler and Semi-Trapezoidal scheme, we simulated the Trapezoidal scheme as in

Zheng (

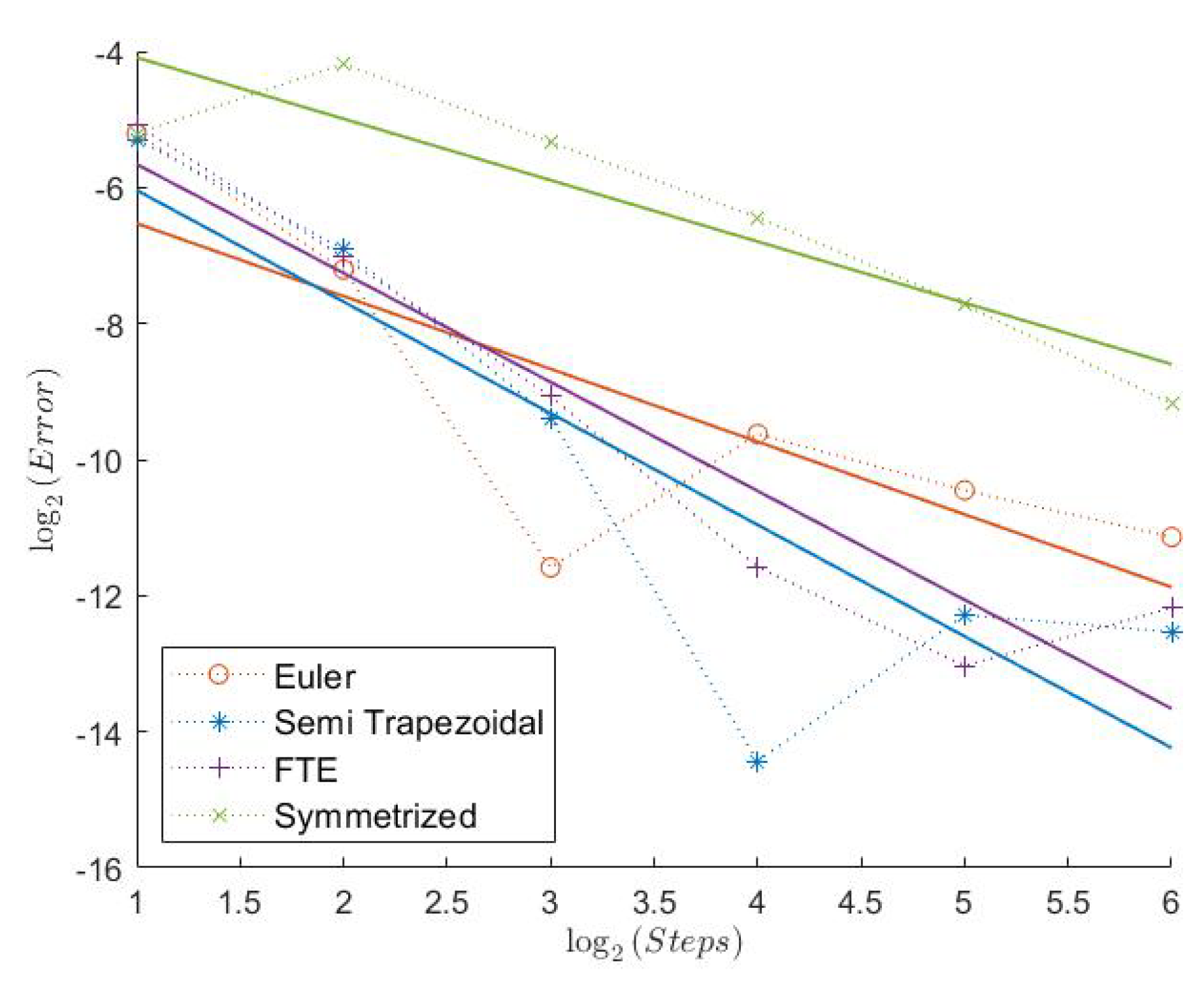

2017) and the two extrapolation schemes from Remark 2. Moreover, to present a broader picture we estimated the weak error order of two Euler-type discretizations of the full Heston Model, the Full Truncation Euler (FTE) as in

Lord et al. (

2009), and the Symmetrized Euler as in

Bossy and Diop (

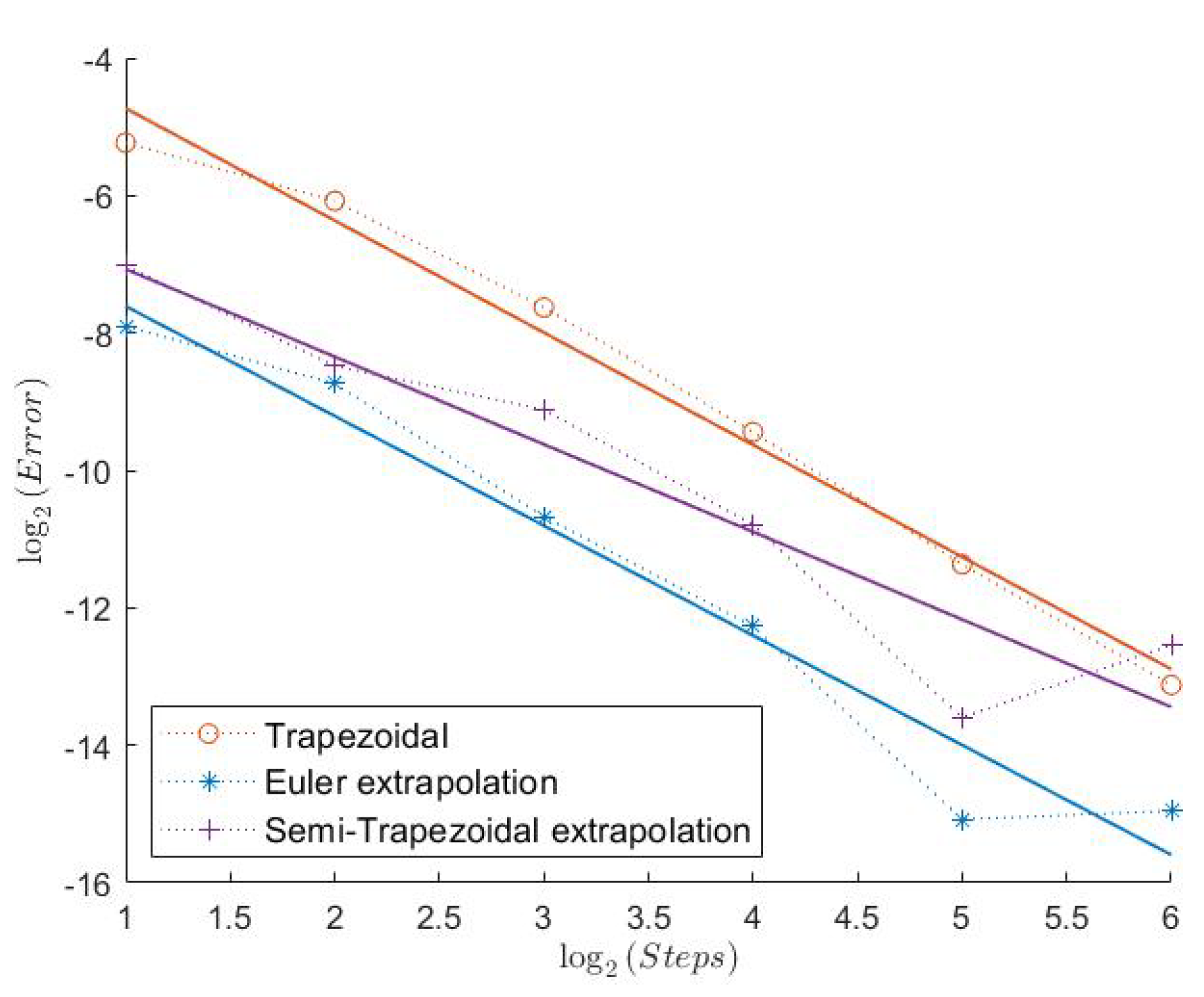

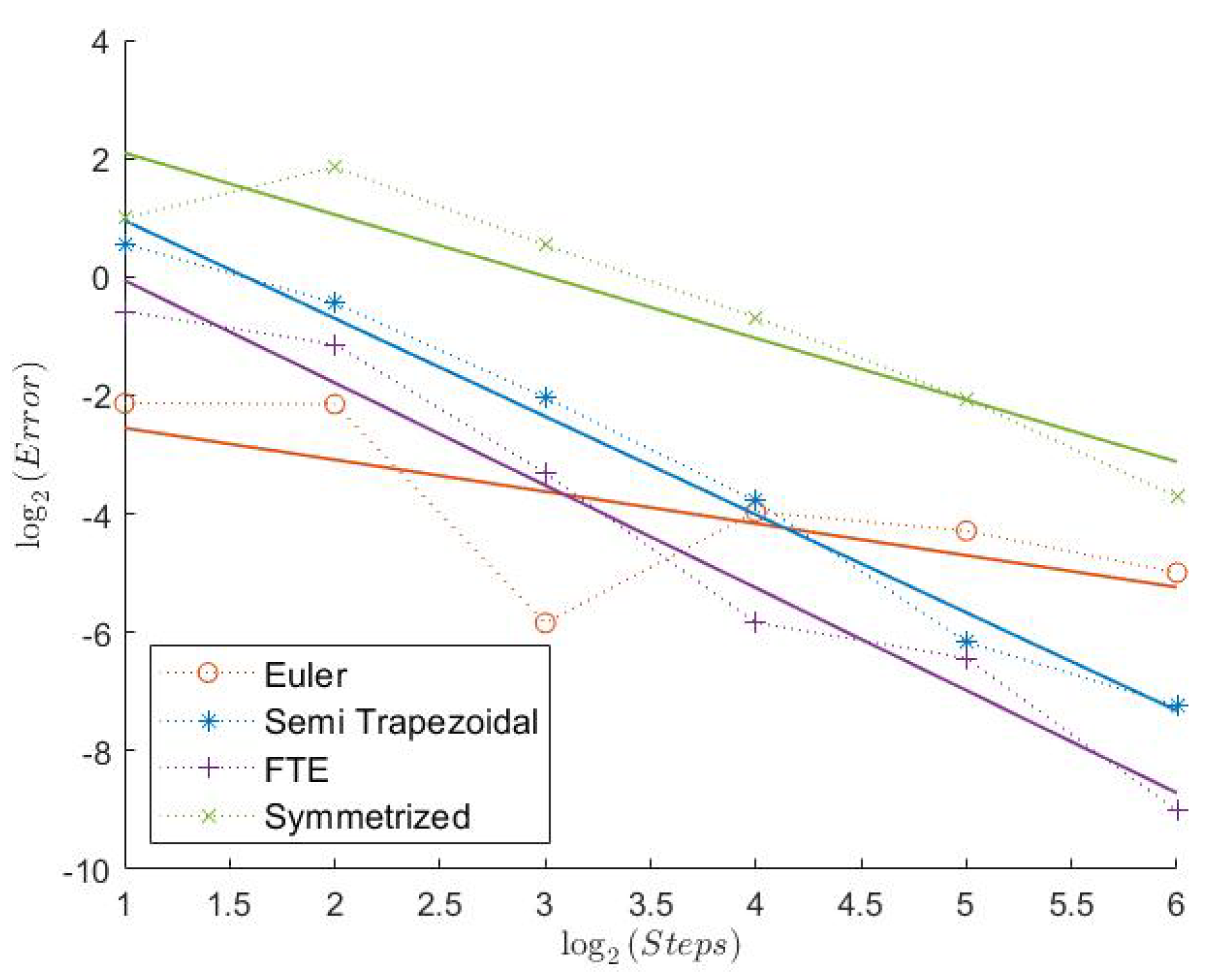

2015). To clarify things, we show two plots for each combination of model parameters and functional: one with the suspected order one schemes (Euler, Semi-Trapezoidal, FTE, and Symmetrized Euler) and one with the suspected order two schemes (Trapezoidal, Extrapolated Euler, and Extrapolated Semi-Trapezoidal).

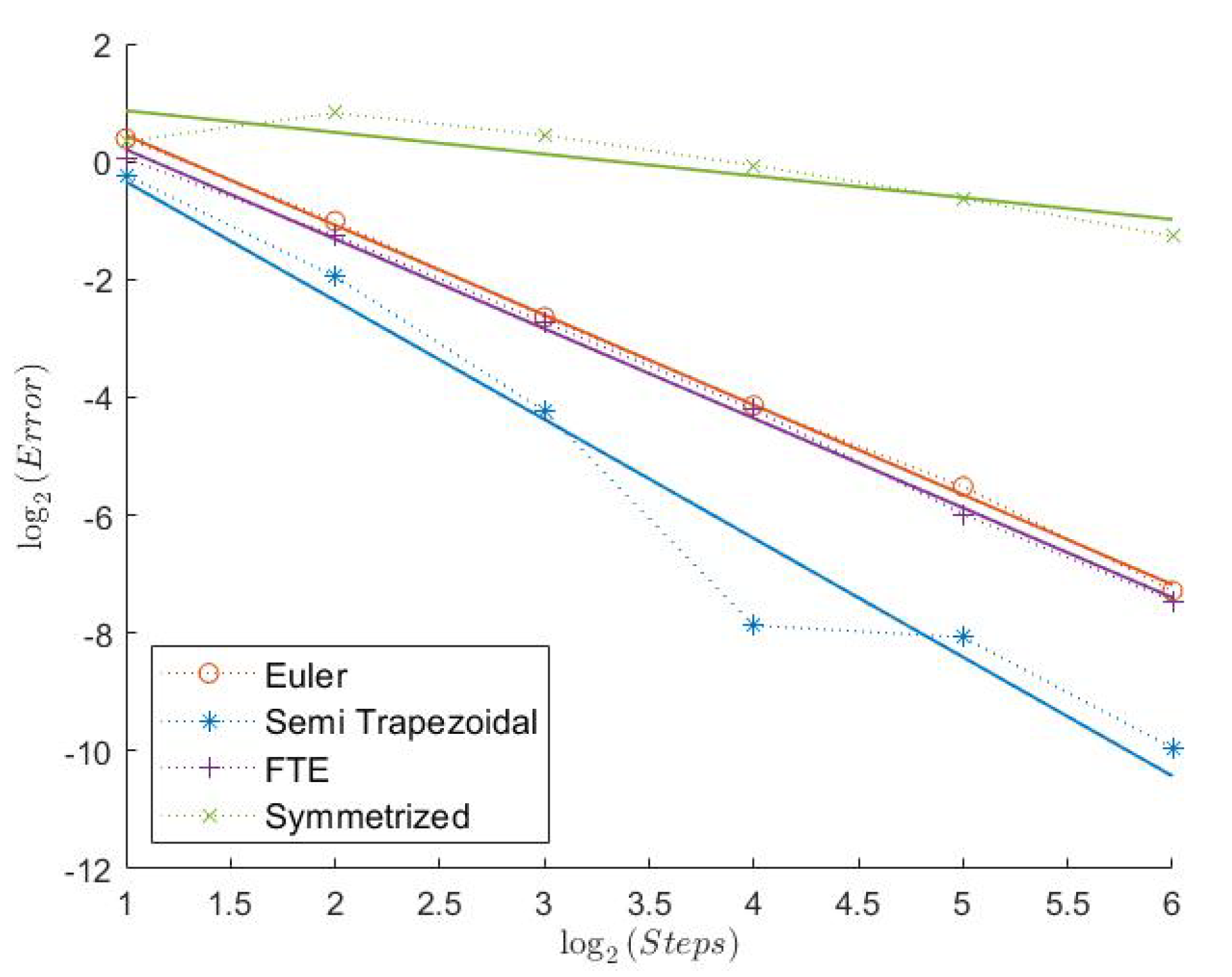

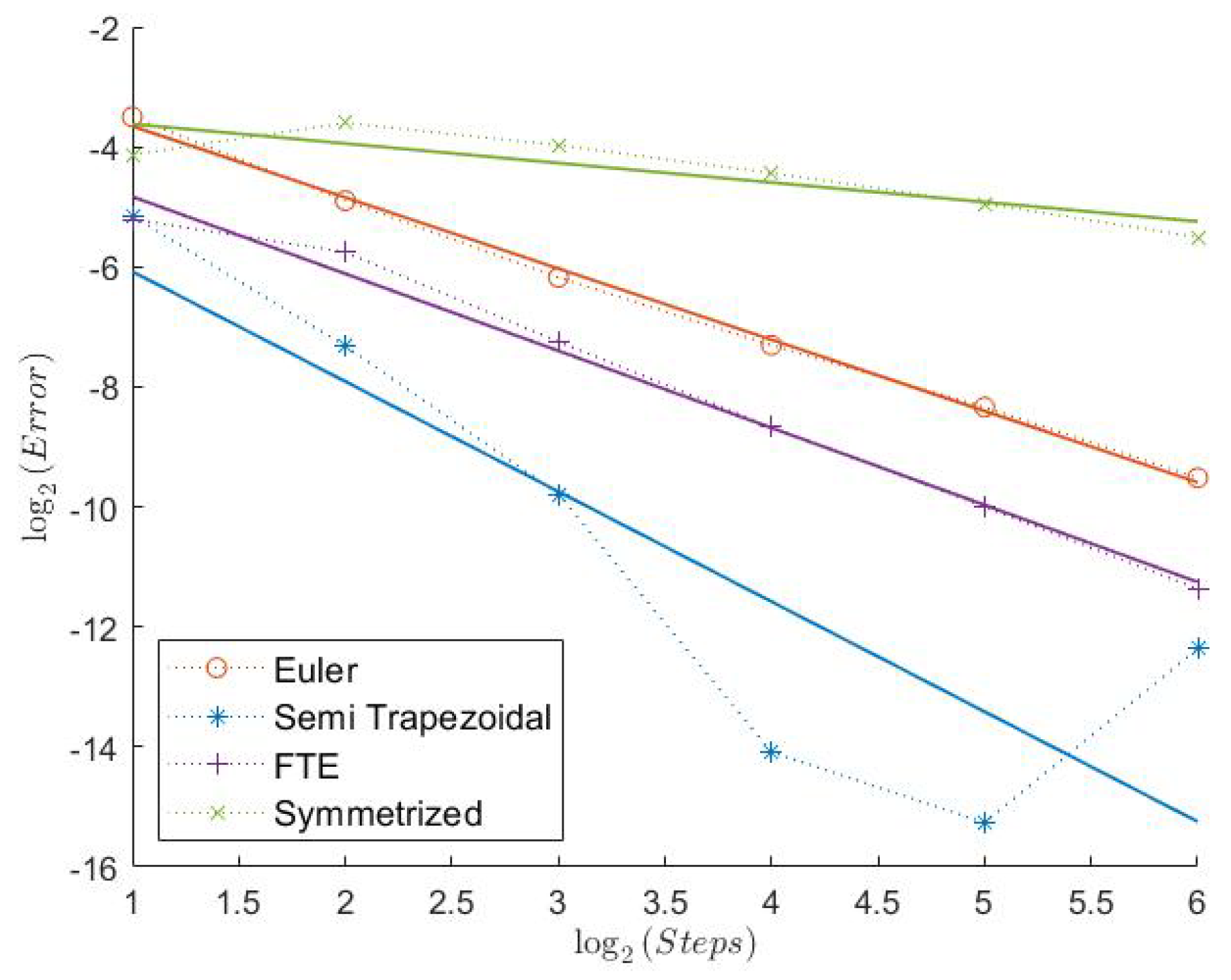

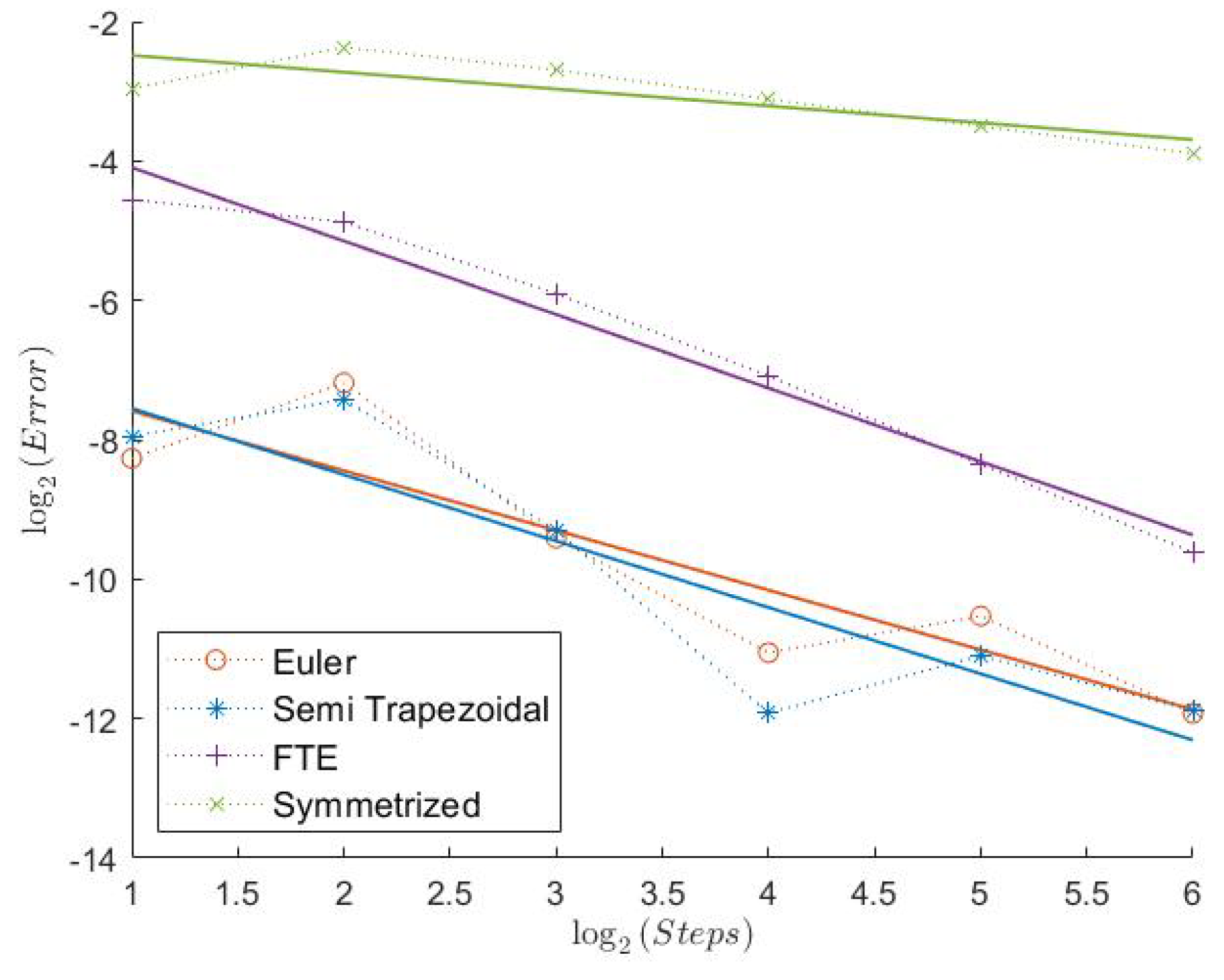

2.1. Model 1

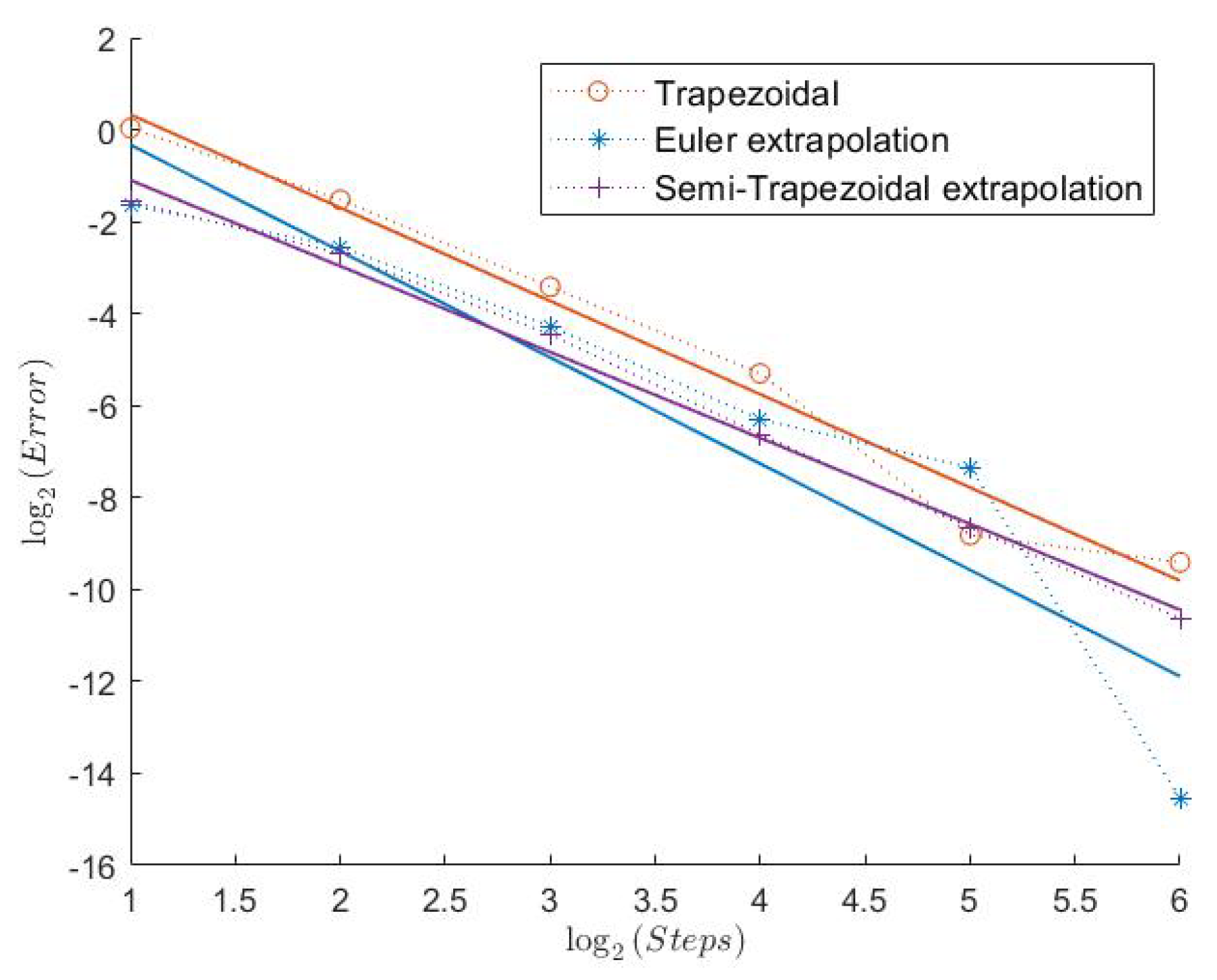

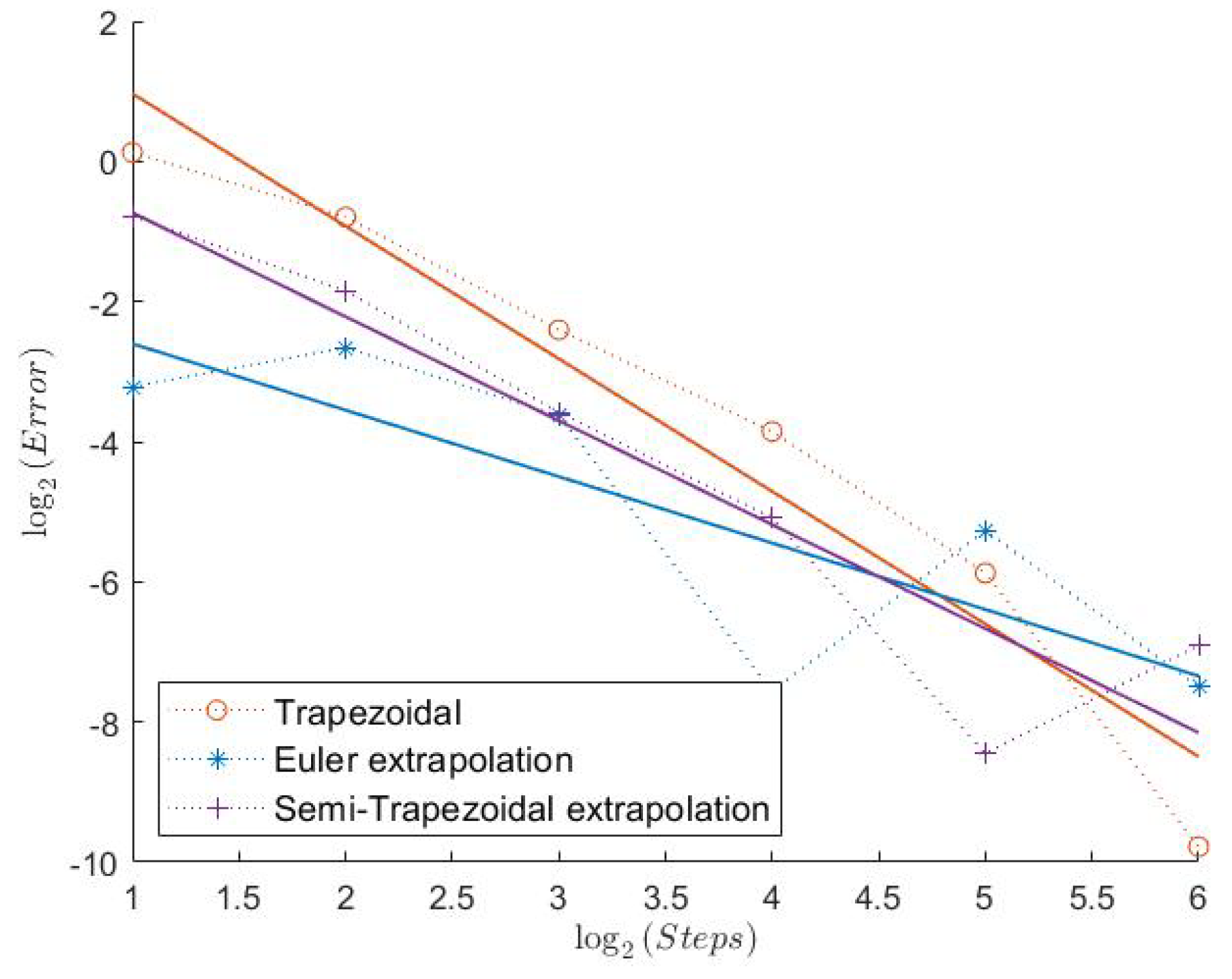

All “Order 1” schemes seem to have a very regular convergence behavior except for the Semi-Trapezoidal scheme for the Indicator, which could be explained by the low absolute error. Especially for the Call and the Indicator, both schemes from Theorem 1 seem to have very high weak convergence rates. Because of the Feller index of 0.63 in this model, this indicates that the assertion of Theorems 1 and 2 could hold under weaker assumptions. The extremely low estimated convergence rate for the Semi-Trapezoidal scheme in combination with the Put could be due to the low error. The estimated weak error order of the FTE scheme is noticeably higher than 1, whereas the Symmetrized Euler has low convergence rates. The convergence behavior of the “Order 2” schemes is a bit less regular. The Extrapolated Euler scheme seems to converge with order 2 for all payoff functions, whereas the Extrapolated Semi-Trapezoidal scheme seem to have only order 1 for the Indicator. But, again, we notice that the error for just 2 discretization steps already starts at around 2−10, which is extremely low.

2.2. Model 2

Here, we have an even lower Feller index of

. We can see that the estimated convergence rates for all “Order 1” schemes are lower than before, see

Table 2. However, the Semi-Trapezoidal scheme and the FTE scheme seem to converge with order 1. The convergence behavior is still quite regular as we can see in

Figure 7,

Figure 9, and

Figure 11. In absolute terms, the errors of the schemes from Theorem 1 are the lowest, especially for Put and Indicator. Looking at the “Order 2” schemes, the Trapezoidal discretization still shows an estimated weak convergence rate of around 2, whereas the two extrapolation schemes show a weaker performance. But, especially for the Indicator, all three schemes seem to have a very low error and a quite regular convergence behavior.

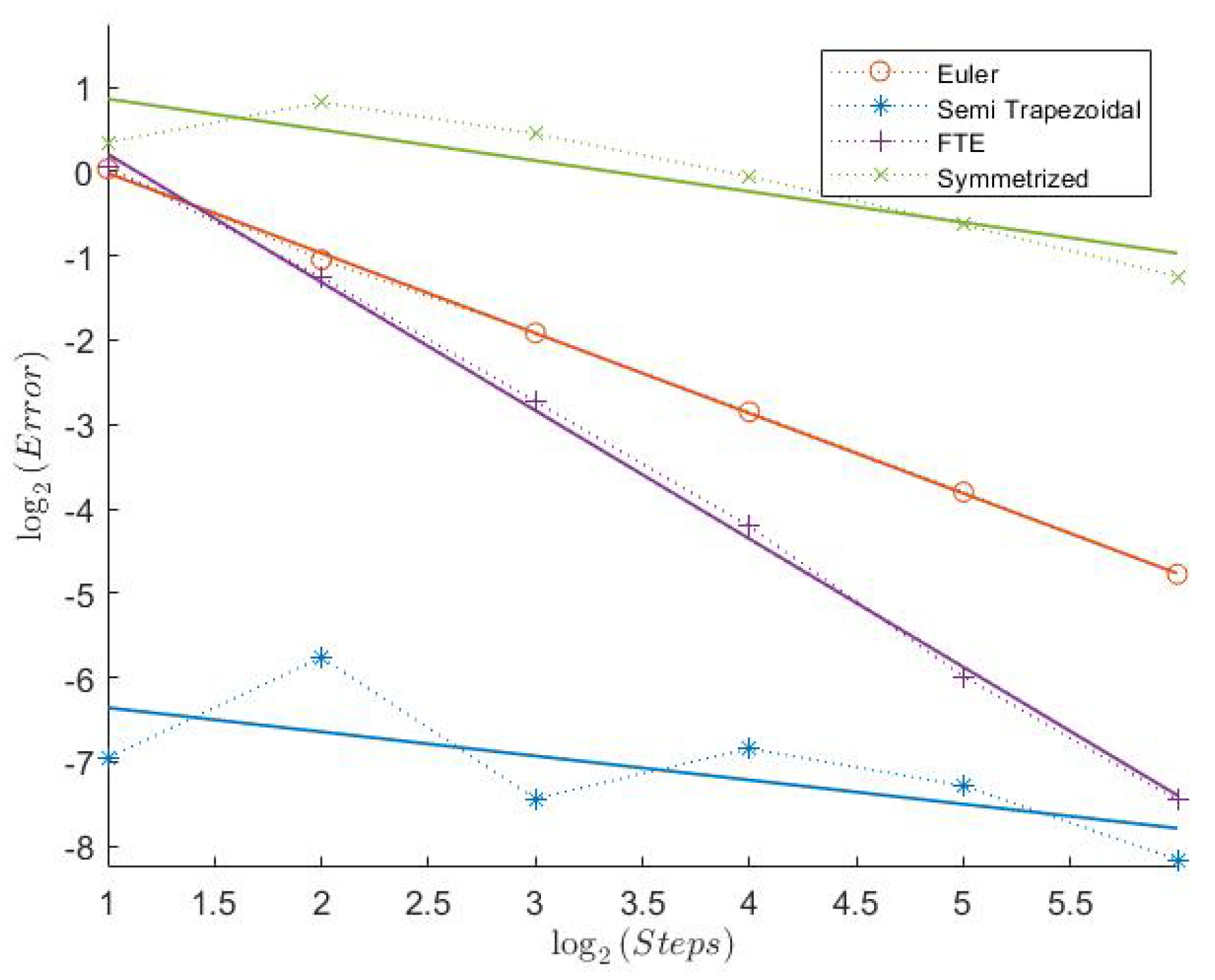

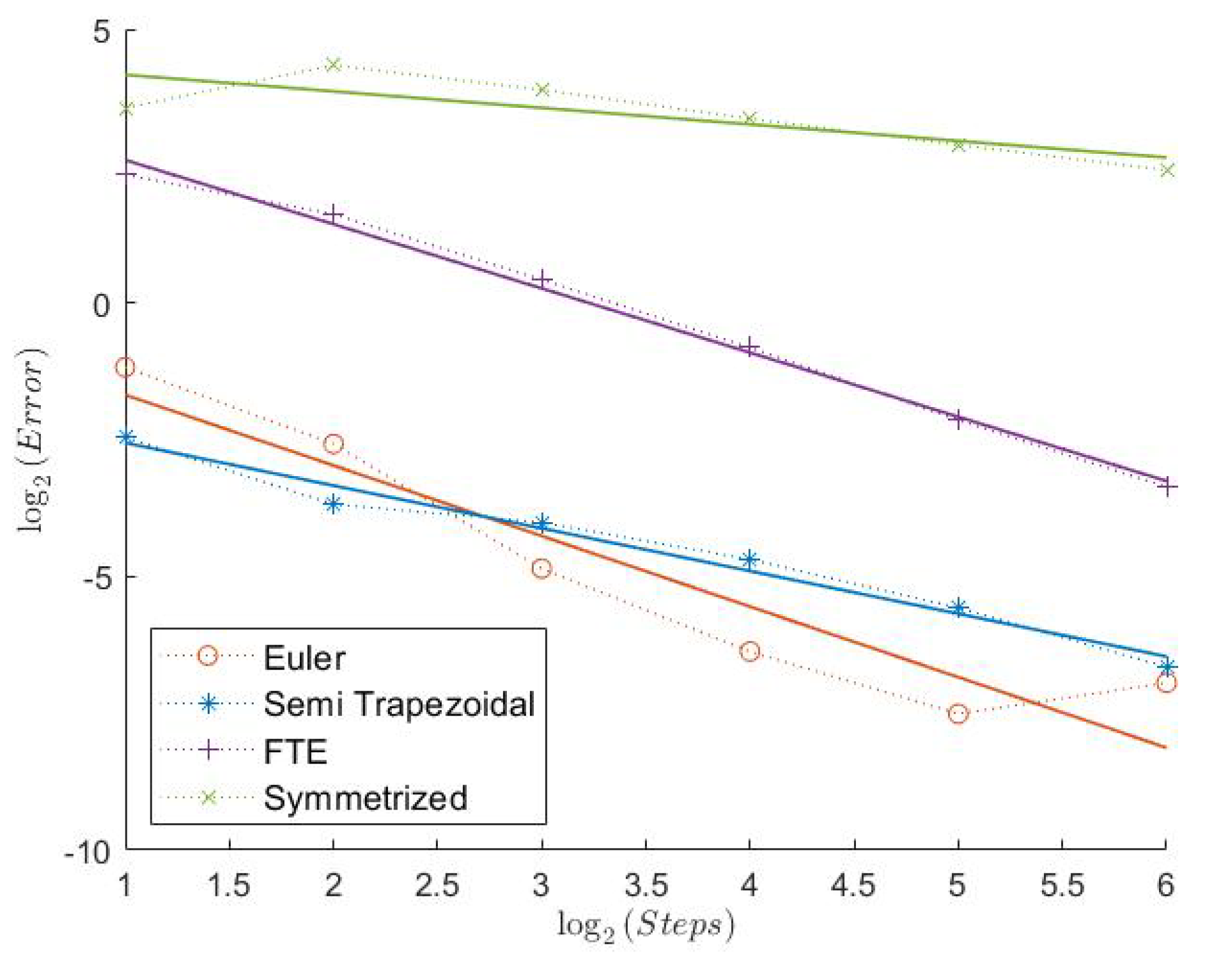

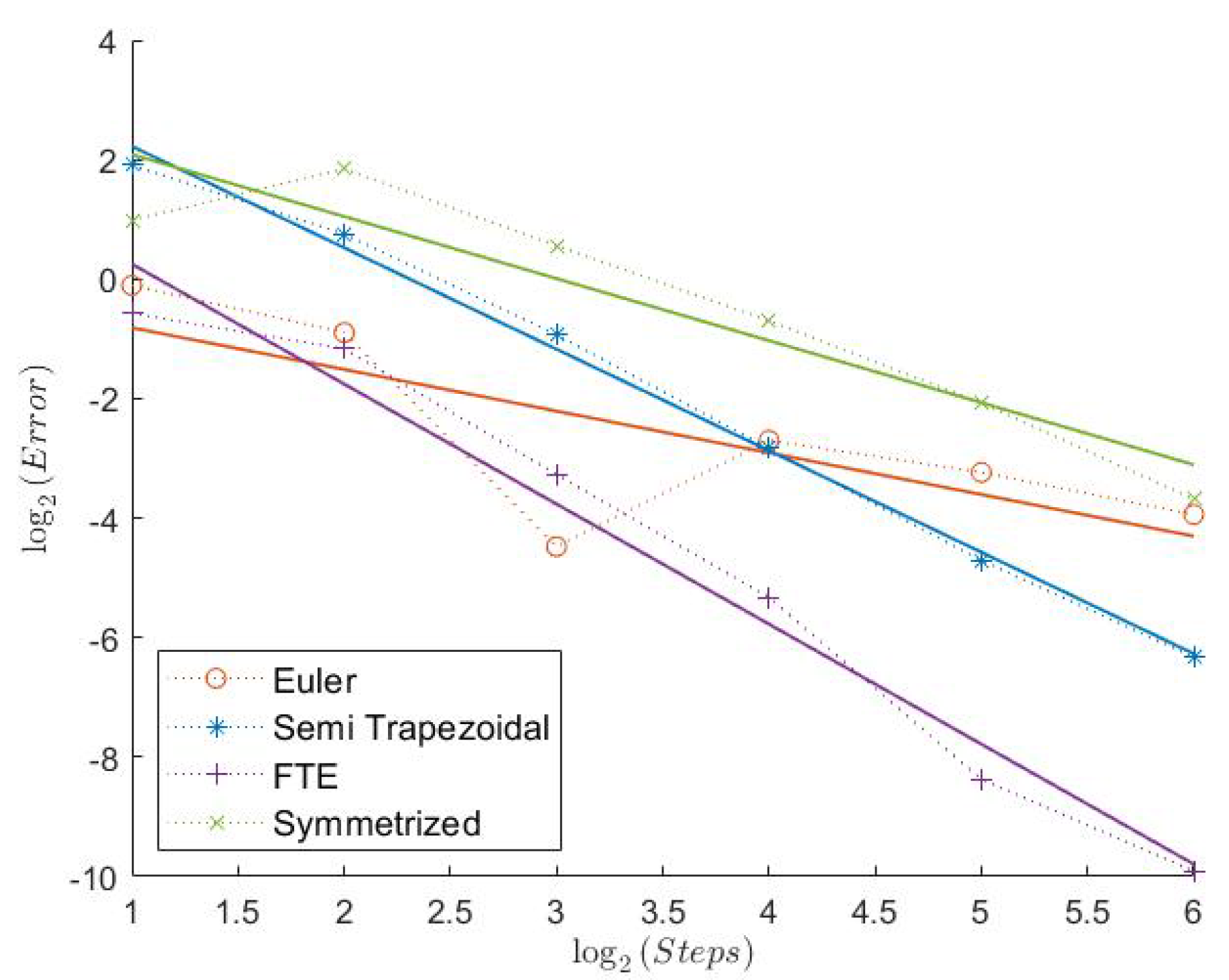

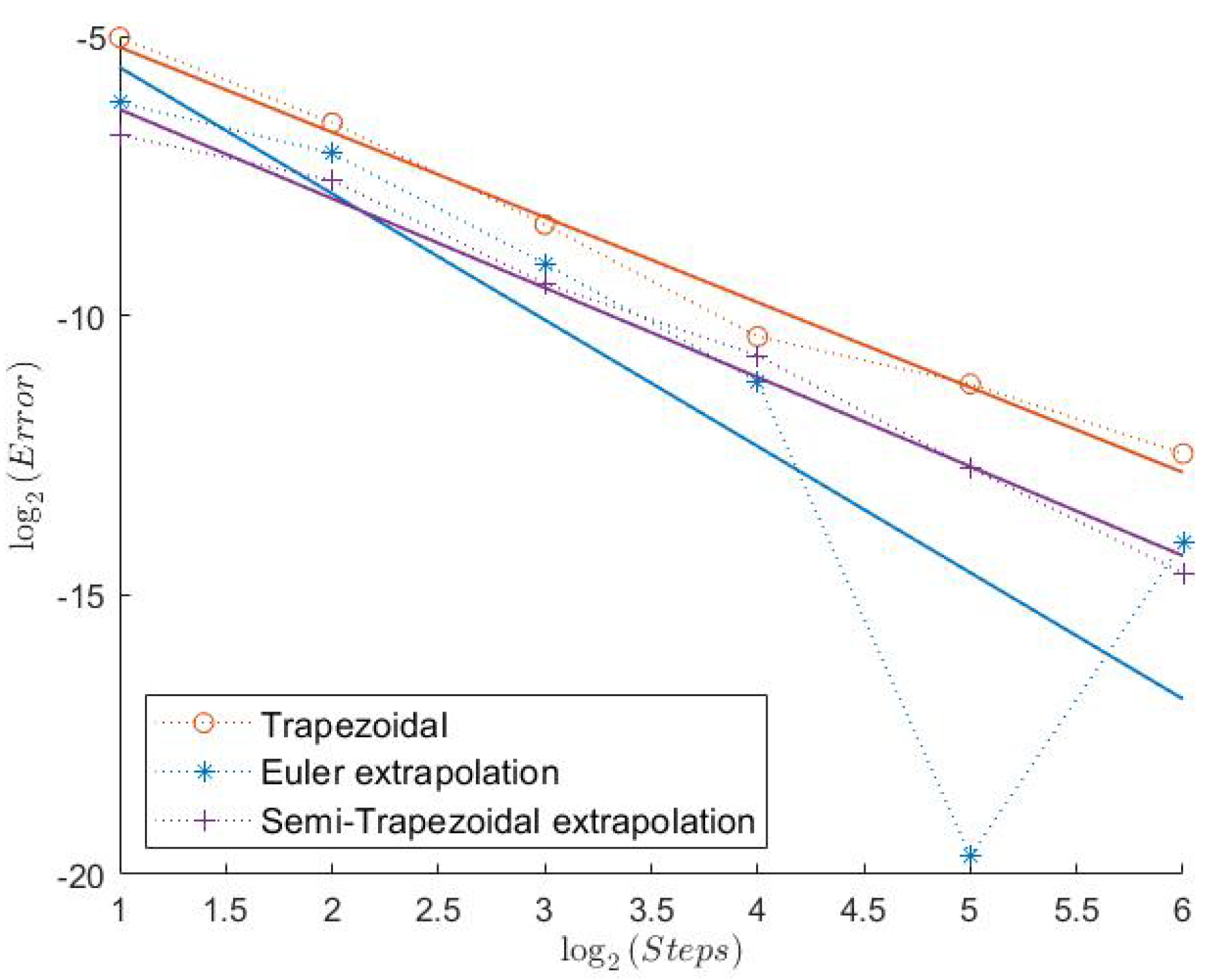

2.3. Model 3

Here, we have the highest Feller Index with

. It is, therefore, a bit surprising that the Euler scheme seems to have a convergence rate of less than 1 in this case. In general, the errors for the “Order 1” schemes show a more irregular behavior, as can be seen from

Figure 13,

Figure 15, and

Figure 17. The Semi-Trapezoidal and the FTE scheme work especially well in this scenario as we can see in

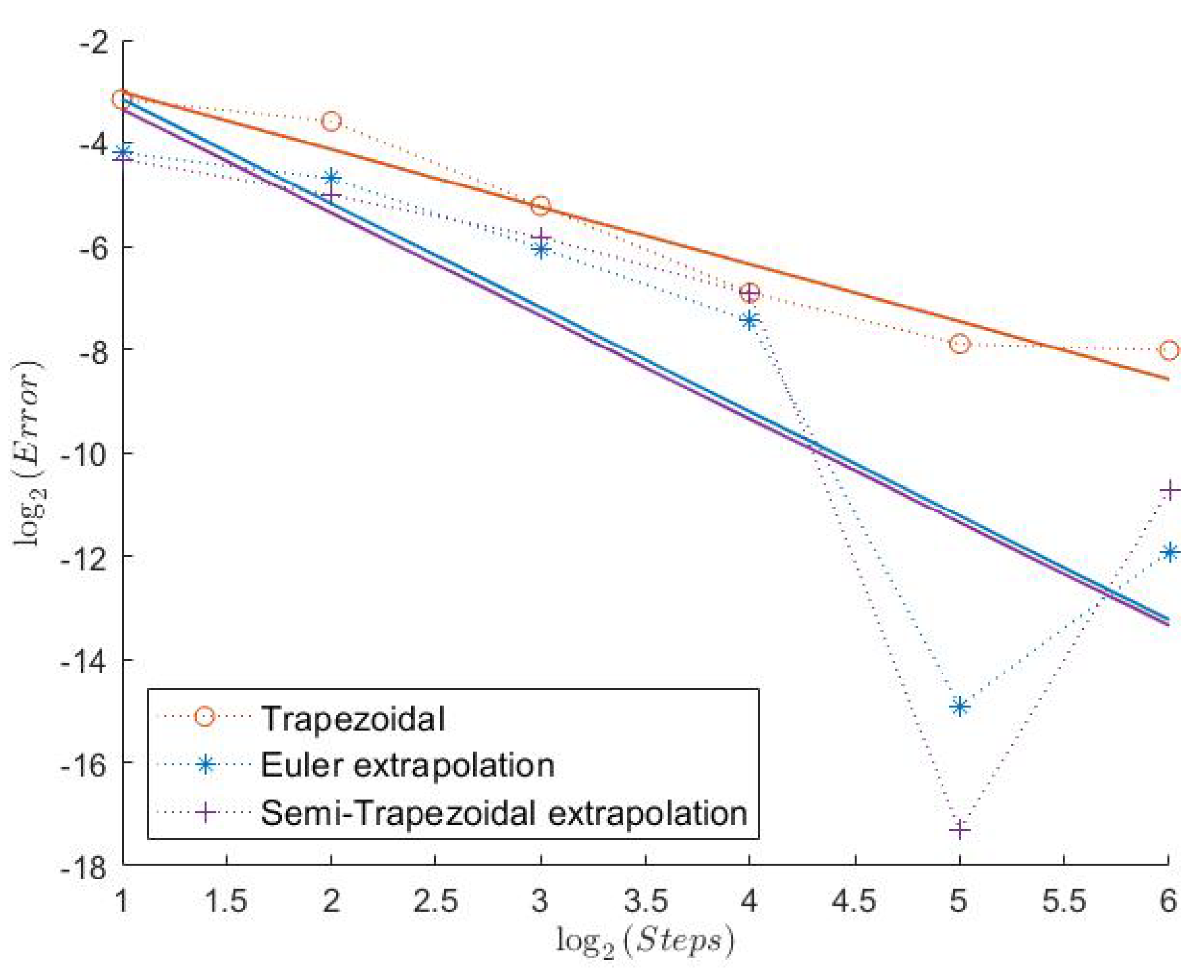

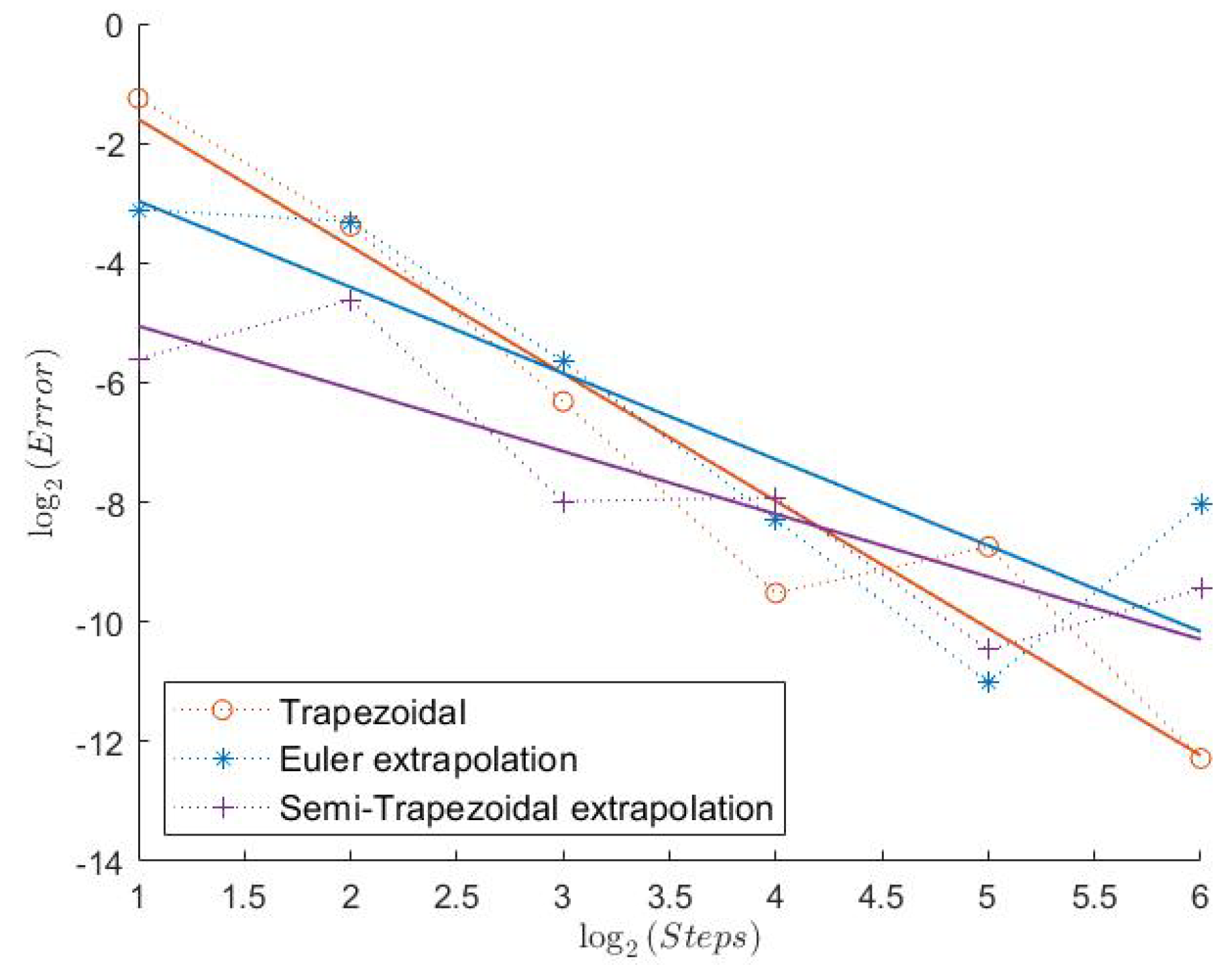

Table 3. This is also the only case where the Symmetrized Euler shows an estimated convergence order of around 1. The extrapolation definitely improves the convergence rate of the Euler scheme with order 2 for the Indicator, but this is not the case for the Semi-Trapezoidal scheme.

2.4. Computational Times

The computational times show the expected behavior, i.e., the simulation times for the semi-exact schemes increase as the Feller index decreases. See

Table 4 and

Table 5. This is a well known feature of the MATLAB-generator

ncx2rnd for the non-central chi-square distribution, which we used. (All simulations were carried out in MATLAB.)

2.5. Conclusions

Except for the Euler scheme for the Call in Model 3, the simulation studies support the conjecture that the convergence rates of Theorems 1 and 2 hold under weaker assumptions. For the mentioned behavior of the Euler scheme, we do not have an explanation, except the possibly pre-asymptotic step sizes. For the extrapolated schemes, which might have order two, the situation is less clear. Since the behavior of the trapezoidal scheme is regular, a too large Monte Carlo error seems an unlikely explanation. Explanations could be again the pre-asymptotic step sizes or, in fact, the non-smoothness of the considered payoffs.

3. Auxiliary Results

In this section, we will collect and establish, respectively, several auxiliary results for the weak error analysis.

3.1. Kolmogorov PDE

Recall that the stochastic integral equations for the log-Heston model for

read as

Now, we apply the so-called Broadie-Kaya trick from

Broadie and Kaya (

2006). We can rearrange the second equation:

Then, we plug this equation into the first one:

Without loss of generality, we can neglect the non-integral part in

, since we have

with

given below. To get the Kolmogorov backward PDE, we look at the following integral equations:

We set

and obtain for

bounded and continuous the Kolmogorov backward PDE by an application of the Feynman-Kac Theorem (see, e.g., Theorem 5.7.6 in

Karatzas and Shreve (

1991)):

In our error analysis, we will follow the now classical approach of

Talay and Tubaro (

1990), which exploits the regularity of the Kolmogorov backward PDE. For the latter we will rely on the works of

Feehan and Pop (

2013) and

Briani et al. (

2018). To state these regularity results, we will need the following notation:

For a multi-index

, we define

and for

, we define

. Moreover, we denote by

the standard Euclidean norm in

. Let

be a domain and

. The set

is the set of all real-valued functions on

which are

q-times continuously differentiable. For

, we denote by

the set of all functions from

in which partial derivatives of order

q are Hölder-continuous of order

, and

is the set of all functions from

, who have compact support. Moreover,

is the set of functions

such that there exist

for which

Finally, we denote by

the set of functions

such that there exist

for which

The work of Feehan and Pop deals with general degenerated parabolic equations and establishes a-priori regularity estimates for them. In the context of Equation (7), the main result of

Feehan and Pop (

2013), i.e., Theorem 1.1, reads as follows:

Theorem 3. Let and . Then, there exists a constant , depending only on and σ such that the solution u of PDE (7) satisfies So, under the above assumptions on f, the solution u and the first order derivatives are bounded. Moreover, the second order derivatives are also bounded, if they are damped by v for .

Assuming more smoothness on

f, we can achieve more regularity for

u using the above result, at least for the partial derivatives with respect to

x. Set

This is well defined: by continuity and boundedness of

and dominated convergence we have

with

An analogous calculation for

shows that

. Thus,

is also bounded, if

. Moreover,

fulfills the Kolmogorov backward PDE

while

fulfills the same PDE with terminal condition

Applying Theorem 3 now to and , we obtain the following additional bounds (case (ii)) for the derivatives of u:

Corollary 1. (i) Let and . Then, there exists a constant , depending only on and σ such that the solution u of PDE (7) satisfies (ii) Let and . Then, there exists a constant , depending only on and σ such that the solution u of PDE (7) satisfies The recent work of Briani et al. is a specialized approach for the log-Bates model, of which the log-Heston model is a particular case. In our setting, they obtain in Proposition 5.3 and Remark 5.4 of

Briani et al. (

2018) the following:

Theorem 4. Let , and suppose that . Then, the solution u of PDE (7) satisfies .

In contrast to the results of Feehan and Pop, the result of Briani et al. requires more smoothness of f but allows polynomial growth instead of compact support.

3.2. Properties of the CIR Process

We recall here the following estimates for the CIR process, which are well known or can be found in

Hurd and Kuznetsov (

2008).

Lemma 1. (1) We havefor all and(2) For all , there exist constants , depending only on and , such that We will need the following bound on the growth of the -norm of a specific stochastic integral of the CIR process:

Lemma 2. For all , it holds that Proof. With the Burkholder-Davis-Gundy inequality and the Hölder inequality, we have

for all

. The assertion now follows from Lemma 1 (1). □

3.3. Malliavin Calculus

When working with low smoothness assumptions on

f, we will use a Malliavin integration by parts procedure to establish weak convergence order one. As in

Altmayer and Neuenkirch (

2017), this paragraph gives a short introduction into Malliavin calculus; for more details, we refer to

Nualart (

1995).

Malliavin calculus adds a derivative operator to stochastic analysis. Basically, if

Y is a random variable and

a two-dimensional Brownian motion, then the Malliavin derivative measures the dependence of

Y on

. The Malliavin derivative is defined by a standard extension procedure: Let

be the set of smooth random variables of the form

with

bounded with bounded derivatives,

,

, and the stochastic integrals

The derivative operator

D of such a smooth random variable is defined as

This operator is closable from

into

with

and the Sobolev space

denotes the closure of

with respect to the norm

In particular, if

denotes the first component of the Malliavin derivative, i.e., the derivative with respect to

W, we have

and vice versa for the derivative with respect to

B, i.e.,

This, in particular, implies that, if

is independent of

B, then

.

For the CIR process, we will, therefore, have that for all .

The derivative operator follows rules similar to ordinary calculus.

Proposition 1. Let be a random variable with components in . If

- (i)

is in ,

- (ii)

,

- (iii)

,

then the chain rule holds: and For example, for a random variable

and

with bounded derivative, the chain rule reads as

Another simple example for the application of this chain rule is

The divergence operator

is the adjoint of the derivative operator. If a random variable

belongs to

, the domain of the divergence operator, then

is defined by the duality—also called integration by parts—relationship

If

u is adapted to the canonical filtration generated by

and satisfies

, then

and

coincides with the Itō integral

. For the Malliavin regularity of the CIR process, the following is well known. See, e.g., Proposition 4.5 and Theorem 4.6 in

Altmayer (

2015) or Proposition 4.1 in

Alos and Ewald (

2008).

Lemma 3. Let and . Then, we have and with In

Altmayer and Neuenkirch (

2015), this and the integration by parts formula was used to establish

under the assumption

with

differentiable and

bounded, see Proposition 4.1 in

Altmayer and Neuenkirch (

2015). Indeed, using

and

,

and the chain rule, i.e.,

we have

where the first equality is due to the integration by parts formula.

In Lemmas 5 and 9, we will establish discrete counterparts for this integration by parts result, i.e., on the level of the approximation schemes. In this context, we will also need the Malliavin differentiability of

. Since

we obtain

by exchanging the Riemann integral and the Malliavin derivative (via a standard approximation argument for the Riemann integral, Lemma 3 and Lemma 1.2.3 in

Nualart (

1995)) and the independence of

and

B. Thus, we can conclude that

3.4. Properties of the Euler Discretization

Recall that the Euler discretization of the price process is given by

with

. We extend this discretization in every interval

as the following Itō process:

Here, we have set , and .

We have the following result on the Malliavin regularity of the Euler discretization:

Lemma 4. Let and . Then, , and we have Proof. Following the steps of the proof of Lemma 3.5 from Altmayer and Neuenkirch

Altmayer and Neuenkirch (

2017), we then have

exploiting that

and

under the assumption

. The chain rule from Proposition 1 yields

and

□

Note that we write, in the following, instead of to unify the notation. With the above result, we can express without the second order derivative of u, which will be needed later on.

Lemma 5. Let . Under the assumptions of Theorem 3 and , we have Proof. To avoid stronger restrictions on the Feller index we will use a localization procedure. So, for , let be a function such that

- 1.

is continuously differentiable with bounded derivative,

- 2.

on ,

- 3.

on ,

- 4.

on .

Since

and

B are independent, the chain rule from Proposition 1 implies

with

. Recall the integration by parts formula from Equation (8), i.e.,

where we now choose

Before we can apply the integration by parts rule, we need to check whether

for

. We deduced these terms by using again the chain rule for

. Note that the properties of the localizing function and Theorem 3 imply that

are all uniformly bounded in

. So, Equation (10) holds, then, due to Lemma 1, Lemma 3, Equation (9), and Lemma 4.

Since

is also well-defined by Lemma 1 due to

, we obtain now

Due to Corollary 1 (i), not only but also is bounded. Since almost surely for and for all , the assertion follows now by dominated convergence using the Itô-isometry and again Lemma 1. □

We also need the following -convergence result:

Lemma 6. Let . There exists a constant , depending only on and , such that Proof. Assume without loss of generality that

. Jensen’s inequality and the Burkholder-Davis-Gundy inequality now imply that there exists a constant

, depending only on

p,

T, the parameters of the CIR process, and

, such that

Since

for

, the assertion follows from Lemma 1. □

Straightforward calculations also yield the following -smoothness result for the Euler-type scheme:

Lemma 7. Let . There exists a constant , depending only on , and , such thatfor all . 3.5. Properties of the Semi-Trapezoidal Rule

Recall that our semi-trapezoidal rule reads as

Again, we write the scheme as a time-continuous process:

Expanding the last term with Itō’s lemma, we obtain

with

Here, we have set again , , , and we also write again , instead of , to unify the notation.

We need the following result on the Malliavin regularity of the semi-trapezoidal scheme:

Lemma 8. Let and . Then, we have and Proof. We already know that

and

. We can write

as

with

Following the steps of the proof of Lemma 3.5 from

Altmayer and Neuenkirch (

2017), we then also have

. The chain rule from Proposition 1 yields

and

□

Note that the partial Malliavin derivative with respect to B for the Euler and the semi-trapezoidal scheme coincide. So, by analogous calculations as for the Euler scheme, we obtain the following integration by parts result:

Lemma 9. Let . Under the assumptions of Theorem 3 and , we have By similar calculations as for the Euler scheme, we also have:

Lemma 10. Let . There exists a constant , depending only on , and , such that Lemma 11. Let . There exists a constant , depending only on , and , such thatfor all .

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}