1. Introduction

In today’s electric grids, power system security is managed in real time by the system operator, who coordinates electricity supply and demand in a manner that avoids fluctuations in frequency or disruption of supply (see, for example,

New Zealand Electricity Authority 2016). In addition, the system operator carries out planning work to ensure that supply can meet demand, including the procurement of non-energy or ancillary services such as operating reserve, the capacity to make near real-time adjustments to supply and demand. These services are provided principally by network solutions such as the control of large-scale generation, although from a technical perspective they can also be provided by smaller, distributed resources such as demand response or energy storage (

National Grid ESO 2019a;

Xu et al. 2016). Such resources have strongly differing operating characteristics: when compared to thermal generation, for example, energy storage is energy limited but can respond much more quickly. Storage also has important time linkages, since each discharge necessitates a corresponding recharge at a later time.

The coming decades are expected to bring a period of “energy transition” in which markets for ancillary services will evolve, among other highly significant changes to generation, consumption and network operation. The UK government, for example, has an ambition that

“new solutions such as storage or demand-side response can compete directly with more traditional network solutions” (

UK Office of Gas and Electricity Markets 2017, p. 29). In harmony, the UK System Operator National Grid has recently declared its intention to

“create a marketplace for balancing that encourages new and existing providers, and all new technology types” (

National Grid ESO 2019b). In anticipation of changes such as these, we will examine the participation of autonomous energy storage in a future marketplace for balancing.

Operating reserve is typically procured via a two-price mechanism, with a reservation payment plus an additional utilisation payment each time the reserve is called for (

Ghaffari and Venkatesh 2013;

Just and Weber 2008). Since the incentivisation and efficient use of operating reserve for system balancing is of increasing importance with growing penetration of variable renewable generation (

King et al. 2011), several system operators have recently introduced real-time energy imbalance markets (EIMs) in which operating reserve is pooled, including in Germany (

Ocker and Ehrhart 2017) and California (

Lenhart et al. 2016;

Western EIM 2019). Such markets typically involve the submission of bids and offers from several providers for reserves running across multiple time periods, which are then accepted, independently in each period, in price order until the real-time balancing requirement is met. As one provider can potentially be called upon over multiple consecutive periods, this reserve procurement mechanism is not well suited to energy-limited reserves such as energy storage. However, storage-oriented solutions are being pioneered in a number of countries including a recent tender by the National Grid in the UK (

National Grid ESO 2019a) and various trials by state system operators in the US (

Xu et al. 2016).

This paper considers operating reserve contracts for energy limited storage devices such as batteries. In contrast to previous work on the pricing and hedging of energy options where settlement is financial (see, for example,

Benth et al. (

2008) and references therein), we take account of the physical settlement required in system balancing, considering also the limited energy and time linkages of storage. The potential physical feedback effects of such contracts are investigated by studying the operational policy of the storage or battery operator. To address the limited nature of storage, the considered reserve contract is for a fixed quantity of energy. In this way, each contract written can be physically covered with the appropriate amount of stored energy. We consider a simple arrangement where the system operator sets the contract parameters, namely the premia (the reservation and utilisation payments) plus an EIM price level

at which the energy is delivered. That is, rather than being the outcome of a price formation process, these parameters are set administratively. Our analysis thus focuses exclusively on the timing of the battery operator’s actions. This dynamic modelling contrasts with previous economic studies of operating reserve in the literature, which have largely been static (

Just and Weber 2008).

To quantify the economic opportunity for the storage operator, we use real options analysis. Real Options analysis is the application of option pricing techniques to the valuation of non-financial or ‘real’ investments with flexibility (

Borison 2005;

Dixit and Pindyck 1994). Here, the energy storage unit is the real asset, and is coupled with the timing flexibility of the battery operator, who observes the EIM price in real time. The arrangement may be viewed as providing the battery operator with a real perpetual American put option on the reserve contract described above. This option is either of swing type (called the lifetime problem in this paper) or of single exercise type (the single problem). The feature that sets it apart from the existing literature on swing options is the random refraction time (cf.

Carmona and Touzi 2008).

A key question in Real Options analyses is the specification of the driving randomness (

Borison 2005). In this paper, we model the EIM price to resemble the historical statistical dynamics of imbalance prices. In common with electricity spot prices and commodity prices more generally but unlike the prices of financial assets, imbalance prices typically exhibit significant mean reversion (

Ghaffari and Venkatesh 2013;

Pflug and Broussev 2009).

To avoid trivial cases, we impose the following, mild, sustainability conditions on the arrangement:

- S1.

The battery operator has a positive expected profit from the arrangement.

- S2.

The reserve contract cannot lead to a certain financial loss for the system operator.

Condition

S1 is also known as the individual rationality or participation condition (

Fudenberg et al. 1991). While the battery operator is assumed to be a profit maximiser, the system operator may engage in the arrangement for wider reasons than profit maximisation. To acknowledge the potential additional benefits provided by batteries, for example in providing response quickly and without direct emissions, condition

S2 is less strict than individual rationality.

By considering reserve contracts for incremental capacity (defined as an increase in generation or equivalently a decrease in load), we are able to provide complete solutions whose numerical evaluation is straightforward. Contracts for a decrease in generation, or an increase in load, lead to a fundamentally different set of optimisation problems which have been partially solved by

Szabó and Martyr (

2017).

This study extends earlier work (

Moriarty and Palczewski 2017) with two important differences. Firstly, the dynamics of the imbalance price is described there by an exponential Brownian motion. In the present paper, by employing a different methodological approach, we obtain explicit results for mean-reverting processes (and also other general diffusions) which better describe the statistical properties of imbalance prices (

Ghaffari and Venkatesh 2013;

Pflug and Broussev 2009). Secondly, the present paper takes into account deterioration of the store. Without this feature, it was found that the value of storage is either very small (corresponding roughly to writing a single reserve contract) or infinite.

Through a benchmark case study, we obtain the following economic recommendations. Firstly, investments in battery storage to provide reserve will be profitable on average for a wide range of the contract parameters. Secondly, the EIM price level at which energy is delivered is an important consideration. This is because, as increases, the EIM price reaches significantly less frequently and the reserve contract starts to provide cover for rare events, resulting in infrequent power delivery and low utilisation of the battery, which may make the business case unattractive. These observations suggest that the contractual arrangement studied in this paper is more suitable for the frequent balancing of less severe imbalance.

1.1. Objectives

Given the model parameters

,

and

, we wish to analyse the actions A1–A3 below (a graphical description of this sequence of actions is provided in

Figure 1):

- A1

The battery operator selects a time to purchase a unit of energy on the EIM and stores it.

- A2

With this physical cover in place, the battery operator then chooses a later time to sell the incremental reserve contract to the system operator in exchange for the initial premium .

- A3

The system operator requests delivery of power when the EIM price X first lies above the level and immediately receives the contracted unit of energy in return for the utilisation payment .

Thus, the system operator obtains incremental reserve from the arrangement in preference to using the EIM, when the EIM price is higher than the level specified by the system operator. When the sequence A1–A3 is carried out once, we refer to this as the single problem; when it is repeated indefinitely back-to-back, we refer to it as the lifetime problem.

In the lifetime problem, because storage is energy limited, action A3 must be completed before the sequence A1–A3 can begin again. Thus, if the arrangement is considered as a real swing put option, the time between A2 and A3 is a random refraction period during which no exercise is possible. Note that, after action A3, the battery operator will perform action A1 again when the EIM price has fallen sufficiently. Mathematically, therefore, we have the following objectives:

- M1

For the single and lifetime problems, find the highest EIM price at which the battery operator may buy energy when acting optimally.

- M2

For the single and lifetime problems, find the expected value of the total discounted cash flows (value function) for the battery operator corresponding to each initial EIM price .

We also aim to provide a straightforward numerical procedure to explicitly calculate and the value function (for ) in the lifetime problem.

1.2. Approach and Related Work

We take the EIM price to be a continuous time stochastic process . Since markets operate in discrete time, this is an approximation, made for analytical tractability. Nevertheless, it is consistent with the physical fact that the system operator’s system balancing challenge is both real-time and continuous.

Mathematically, the problem is one of choosing two optimal stopping times corresponding to the two actions A1 and A2, based on the evolution of the stochastic process

X (The reader is refered to

Peskir and Shiryaev (

2006, chp. 1) for a thorough presentation of optimal stopping problems). We centre our solution techniques around ideas of

Beibel and Lerche (

2000), who characterise optimal stopping times using the Laplace transforms of first hitting times for the process

X (see, for example,

Borodin and Salminen (

2012, sec. 1.10)). Methods and results from the single problem are then combined with a fixed point argument for the lifetime analysis.

Our methodological results feed into a growing body of research on timing problems in trading. In a financial context,

Zervos et al. (

2013) optimise the performance of “buy low, sell high” strategies, using the same Laplace transforms to provide a candidate value function, which is later verified as a solution to certain quasi-variational inequalities. An analogous strategy in an electricity market using hydroelectric storage is studied in

Carmona and Ludkovski (

2010) where the authors use Regression Monte Carlo methods to approximately solve the dynamic programming equations for a related optimal switching problem. Our results differ from the above papers in two aspects. Our analysis is purely probabilistic, leading to arguments that do not refer to the theory of PDEs and quasi-variational inequalities. Secondly, our characterisation of the value function and the optimal policy is explicit up to a single, one-dimensional nonlinear optimisation, which, as we demonstrate in an empirical experiment, can be performed in milliseconds using standard scientific software. Related to our lifetime analysis,

Carmona and Dayanik (

2008) apply probabilistic techniques to study the optimal multiple-stopping problem for a general linear regular diffusion process and reward function. However, the latter work deals with a finite number of option exercises in contrast to our lifetime analysis which addresses an infinite sequence of exercises via a fixed point argument. Our work thus yields results with a significantly simpler and more convenient structure.

The contracts we consider have features in common with the reliability options used in Colombia, Ireland and the ISO New England market and currently being introduced in Italy (

Mastropietro et al. 2018). Reliability options pay an initial premium to a generator, usually require physical cover, and have a reference market price and a strike price that plays a similar role to

. Typically, the strike price is set at the variable cost of the technology used to satisfy demand peaks, and the generator is contracted to pay back the difference between the market price and the strike price in periods when energy is delivered and the market price is higher. However, instead of being designed for system balancing, the purpose of reliability options is to ensure sufficient investment in generation capacity.

The remainder of the paper is organised as follows. The mathematical formulation and main tools are developed in

Section 2. In the results of

Section 3, we show that, for a range of price processes

X incorporating mean reversion, solutions for all initial values

x can be obtained. Furthermore, an empirical illustration using data from the German Amprion system operator is provided and qualitative implications are drawn, while

Section 5 presents the conclusions. Auxiliary results are collected in the appendices.

3. Results

The general theory presented above provides optimal stopping times for initial EIM prices , where is the highest price at which the battery operator can buy energy optimally. In this section, for specific models of the EIM price, we derive optimal stopping times for all possible initial EIM prices when the sustainability conditions S1* and S2* hold. In the examples of this section, the stopping sets for the single and lifetime problems take the form although, in general, stopping sets may have much more complex structure. Interestingly, the stopping sets for the single and lifetime problem are either both half-lines or both compact intervals.

Note that condition S2* is ensured by the explicit choice of parameters. Verification of condition S1 is straightforward by checking, for example, if the left boundary a of the interval I satisfies , i.e., that . In particular, S1 always holds if .

Our approach is to combine the above general results with the geometric method drawn from

Section 5 of

Dayanik and Karatzas (

2003). Although Proposition 5.12 of the latter paper gives results for natural boundaries, we note that the same arguments apply to entrance-not-exit boundaries. In particular, we construct the least concave majorant

W of the obstacle

, where

(the latter equality was given in (

A5) in the appendices). Here, the function

is strictly increasing with

. Writing

for the set on which

W and

H coincide, under appropriate conditions, the smallest optimal stopping time is given by the first hitting time of the set

(

Dayanik and Karatzas 2003, Propositions 5.13 and 5.14).

The Ornstein-Uhlenbeck (OU) process is a continuous-time stochastic process with dynamics

where

and

. It has two natural boundaries,

and

. This process extends the scaled Brownian motion model by introducing a mean reverting drift term

. The mean reversion is commonly observed in commodity price time series and may have several causes (

Lutz 2009). In the present context, the mean reversion can also be interpreted as the impact on prices of the system operator’s corrective balancing actions.

Appendix F collects some useful facts about the Ornstein-Uhlenbeck process. In particular, when constructing

W, it is convenient to note that

has the same sign as

, where

is the infinitesimal generator of

X defined as in

Appendix F.

3.1. OU Price Process

Assume now that the EIM price follows the OU process (

25) so that

(see Equation (

A19) in

Appendix F) and, by Lemma 3, case A of Theorem 1 applies. We are able to deal with the single and lifetime problems simultaneously by setting

equal to 0 for the single problem and equal to (the positive function)

in the lifetime problem. The results of

Section 2.2 and

Section 2.3 yield that, in both problems, the right endpoint of the set

equals

for some

. Furthermore, since

is a solution to

and since

, for

, we have

Therefore, the function is negative on and positive on , where . This implies that H is strictly concave on and strictly convex on . Since the concave majorant W of H cannot coincide with H in any point of convexity, so necessarily and H is concave on . Hence, we conclude that W is equal to H on the latter interval and so .

3.2. General Mean-Reverting Processes

The above reasoning can be extended to mean-reverting processes with general volatility

for a measurable function

such that the above equation admits a unique solution, cf.

Section 2, and

(cf. (

24)). Recall that we assume that

has two non-exit boundaries

(natural or entrance-not-exit boundaries) satisfying

. Since

, Equations (

26)–(

28) still apply. In particular, we see that the diffusion coefficient

does not affect the sign of (28) and thus does not influence the concavity properties of

H on

. Proceeding as above, we argue that case A of Theorem 1 applies and the single and lifetime problems can be solved simultaneously. Particularly, the largest buy price is given by

(different for the single and lifetime problems). Note that the form of the stopping set is purely determined by

, the left boundary

a and the initial premium

. Obviously, the mean price level

satisfies

because

a is an unreachable boundary.

Lemma 5. If , then the stopping sets for the single and lifetime problems are of the form .

Proof. The same arguments as in the OU case are directly applicable to the present setting and, under the assumptions of the lemma, we have . Hence, for each problem, the stopping set has the form for some . ☐

In the particular case of the CIR model (

Cox et al. 1985)

we have

,

. Then:

Corollary 4. If X is the CIR process (

29)

with and , then the boundary is entrance-not-exit. Furthermore, if , then the stopping sets for the single and lifetime problems are of the form . Proof. It follows from (

Cox et al. 1985, p. 391) that the condition

is necessary and sufficient for the boundary 0 to be entrance-not-exit. By Lemma 3, we have

. An application of Lemma 5 concludes. ☐

Remark 1. More generally, suppose that the imbalance price process followsfor some . Then, the left boundary is entrance-not-exit for any choice of parameters since the scale function p given in (3) converges to negative infinity at 0. Therefore, the arguments in the above corollary apply and the stopping sets for the single and lifetime problems are also of the form . 3.3. Shifted Exponential Price Processes

In order to first recover and then generalise previously obtained results (

Moriarty and Palczewski 2017), take the following shifted exponential model for the price process:

where

Z is a regular one-dimensional diffusion with non-exit (natural or entrance-not-exit) boundaries

and

(we will use the superscripts

X and

Z where necessary to emphasise the dependence on the stochastic process). The idea is that

Z models the physical system imbalance process while

f represents a

price stack of bids and offers which is used to form the EIM price. In this case, the left boundary for

X is

and, by Lemma 3,

and case A of Theorem 1 applies. Rather than working with the implicitly defined process

X, however, we may work directly with the process

Z by setting:

and modifying the definitions for

and

accordingly. We then have

Theorem 4. Taking definitions (

30)

and (

32)–(

34)

, assume that conditions S1* and S2* hold. Then, In addition:

- (i)

(Single problem) There exists that maximises , the stopping time is optimal for , and - (ii)

(Lifetime problem) The lifetime value function is continuous and a fixed point of . There exists which maximises and is an optimal stopping time for with

Proof. The proof follows from the one-to-one correspondence between the process X and the process Z, and direct transfer from Theorems 1 and 3. ☐

In some cases, explicit necessary and/or sufficient conditions for S1 may be given in terms of the problem parameters. Assume that as in the examples studied below. If and , this is sufficient for the condition S1 to be satisfied as then for sufficiently small z. When and , it is sufficient to verify that as since then for . On the other hand, our assumption that S1 holds necessarily excludes parameter combinations with , since the reserve contract writer then cannot make any profit because for all z.

In

Section 3.3.1, we take

Z to be the standard Brownian motion and recover results from the single problem of

Moriarty and Palczewski (

2017) (the lifetime problem is formulated differently in the latter reference, where degradation of the store is not modelled). In

Section 3.3.2, we generalise to the case when

Z is an OU process.

3.3.1. Brownian Motion Imbalance Process

When the imbalance process

, the Brownian motion, we have

We have several cases depending on the sign of and .

Assume first that :

- (i)

We may exclude the subcase , since then is strictly convex on for any and cannot intersect this interval, contradicting Theorem 4 and, consequently, violating S1 or S2.

- (ii)

If

,

H is concave on

and convex on

, where

By Theorem 4 and the positivity of H on we have and for the single and lifetime problems, respectively, with .

Suppose that .

- (i)

When , the function H is concave on . Hence, the stopping sets for single and lifetime problems have the same form as in case 1(ii) above.

- (ii)

If

, the function

H is convex on

and concave on

. The set

must then be an interval, respectively

and

. For explicit expressions for the left and right endpoints for the single problem, as well as sufficient conditions for

S1, the reader is refered to

Moriarty and Palczewski (

2017).

In the boundary case , the convexity of H is determined by the sign of the difference . As above, the possibility is excluded since then H is strictly convex. Otherwise, H is concave and the stopping sets have the same form as in case 1(ii) above.

3.3.2. OU Imbalance Process

When

Z is the Ornstein-Uhlenbeck process, by adjusting

d and

b in the price stack function

f (see (

30)), we can restrict our analysis to the OU process with zero mean and unit volatility, that is:

Then, for

Differentiating

, we obtain

which has a unique root at

. The function

decreases from

at

until

at

and then increases to positive infinity.

4. Benchmark Case Study and Economic Implications

In this section, we use a case study to draw qualitative implications from the above results. An OU model is assumed, which captures both the mean reversion and random variability present in EIM prices, and is fitted to relevant data. The interest rate is taken to be per annum, and the degradation factor for the store to be .

Our data is the ‘balancing group price’ from the German Amprion system operator, which is available for every 15 min period (

AMPRION 2016). Summary statistics for the period from 1 June 2012 to 31 May 2016 are presented in

Table 1. To address the issue of its extreme range, which impacts the fitting of both volatility and mean reversion in the OU model, the data was truncated at the values −150 and 150. The parameters obtained by maximum likelihood fitting were then

(the rate of mean reversion),

(the volatility),

(the mean-reversion level). The effect of the truncation step was to approximately halve the fitted volatility.

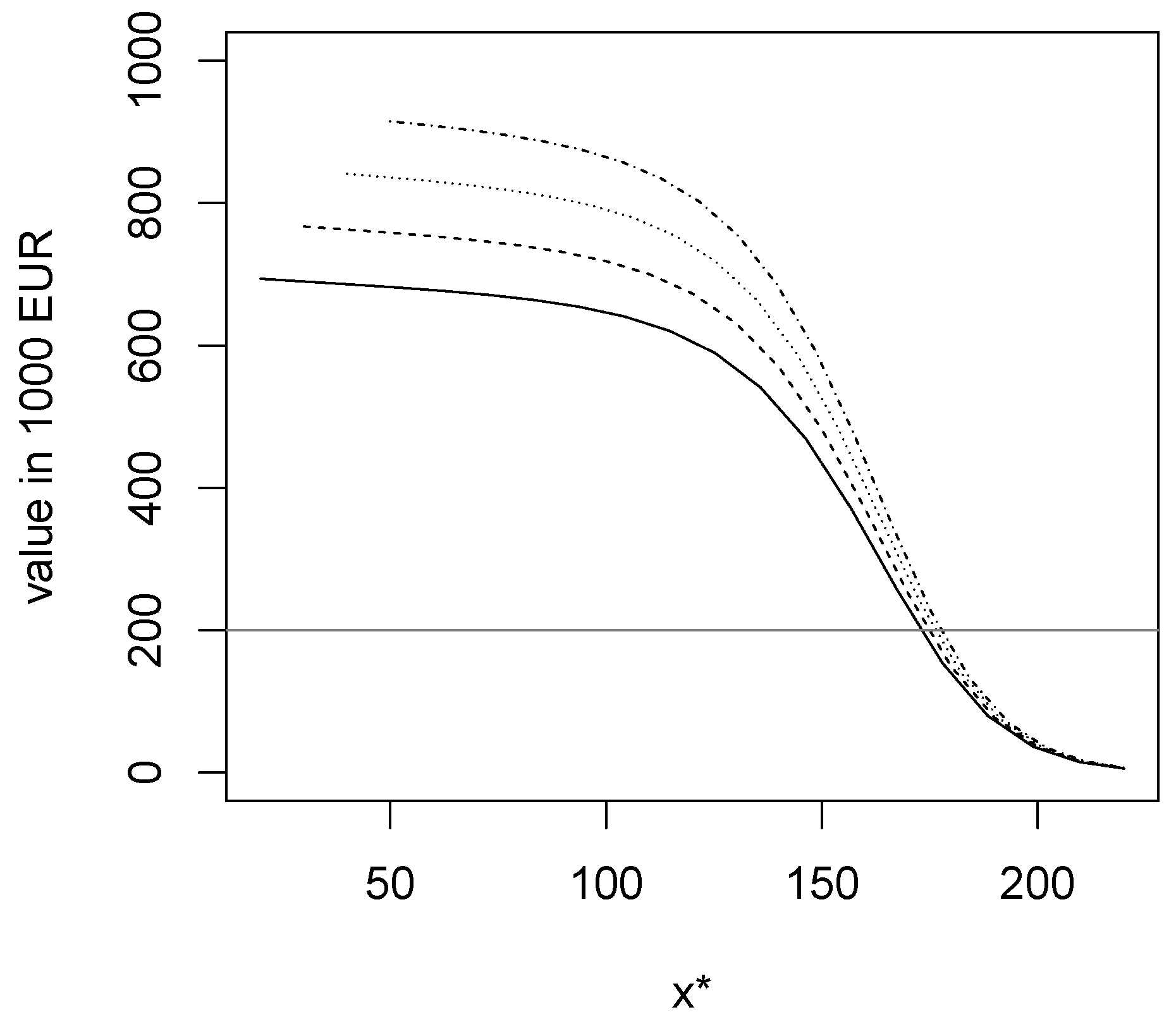

The left panel of

Figure 3 and

Figure 4 show the lifetime value

, while the right panel of

Figure 3 plots the stopping boundary

, which is the maximum price at which the battery operator can buy energy optimally. These values of

are significantly below the long-term mean price

D, indeed the former value is negative while the latter is positive. Thus, in this example, the battery operator purchases energy when it is in excess supply, further contributing to balancing. To place the negative values on the stopping boundary in

Figure 3 in the statistical context, recall from

Table 1 that the first quartile of the price distribution is approximately zero. Indeed, negative energy prices usually occur several times per day in the German EIM. In the present dataset of 1461 days, there are only 11 days without negative prices and the longest observed time between negative prices is

h.

We make the following empirical observations. Firstly, defining the total premium as the sum

, altering its distribution between the initial premium

(which is received at

) and the utilisation payment

(which is received at

) results in insignificant changes to the graphs, with relative differences on the vertical axes of the order

(data not shown). It is for this reason that the figures are indexed by the total premium

rather than by individual premia. Secondly, it is seen from the right-hand panel of

Figure 3 that the (negative valued) stopping boundary increases with the total premium, making exercise more frequent. Thus, as the total premium increases, both the frequency and size of the cashflows increase, yielding a superlinear relationship in the left-hand panel of

Figure 3. This superlinearity is not very pronounced since the stopping boundary is relatively insensitive to the total premium in the range presented in the graphs (see the right hand panel), so that the lifetime value is driven principally by the size of the cashflows. Thirdly, the grey horizontal line of

Figure 4 is placed at a level indicative of recent costs for lithium-ion batteries per MWh (megawatt hour). Thus, the investment case for battery storage providing reserve is significantly positive for a wide range of the contract parameters. Finally, the contours in

Figure 4 have an S-shape, the marginal influence of

being smaller in the range

and larger for greater values of

(with the marginal influence eventually decreasing again in the limit of large

).

These phenomena are explained by the presence of mean reversion in the OU price model. The timings of the cashflows to the battery operator are entirely determined by the successive

passage times of the price process between the levels

and

. These passage times are relatively short on average for the fitted OU model. This means that the premia are received at almost the same time under each reserve contract, and it is the total premium which drives the real option value. Furthermore, the passage times between

and

may be decomposed into passage times between

and

D, and between

D and

. Since the OU process is statistically symmetric about

D, let us compare the distances

and

. From

Figure 3, we have

so that

. Therefore, for

, we have

and the passage time between

D and

, which varies little, dominates that between

and

D. Correspondingly, we observe in

Figure 4 that the value function changes relatively little as

varies below 110. Conversely, as

increases beyond 110, it is the distance between

and

D which dominates, and the value function begins to decrease relatively rapidly.

These results provide insights into the suitability of the considered arrangement for correcting differing levels of imbalance. As the distance between and the mean level D grows, the energy price reaches significantly less frequently and the reserve contract starts to provide insurance against rare events, resulting in infrequent power delivery and low utilisation of the battery. These observations suggest that the contractual arrangement studied in this paper is more suitable for the frequent balancing of less severe imbalance. In contrast, the more rapid reduction in the lifetime value for large values of suggests that such arrangements based on real-time markets are not suitable for balancing relatively rare events such as large system disturbances due to unplanned outages of large generators. The system operator may prefer to use alternative arrangements, based, for example, on fixed availability payments, to provide security against such events.

5. Conclusions

In this paper, we investigate the procurement of operating reserve from energy-limited storage using a sequence of physically covered incremental reserve contracts. This leads to the pricing of a real perpetual American swing put option with a random refraction time. We model the underlying energy imbalance market price as a general linear regular diffusion, which, in particular, is capable of modelling the mean reversion present in imbalance prices. Both the optimal operational policy and the real option value of the store are characterised explicitly. Although the solutions are generally not available in an analytical form, we have provided a straightforward procedure for their numerical evaluation together with empirical examples from the German energy imbalance market.

The results of the lifetime analysis in particular have both managerial implications for the battery operator and policy implications for the system operator. From the operational viewpoint, under the setup described in

Section 1.1, we have established that the battery operator should purchase energy as soon as the EIM price falls to the level

, which may be calculated as described in

Section 2.4. Furthermore, the battery operator should then sell the reserve contract immediately. Our real options valuation may be taken into account when deciding whether to invest in an energy store, and whether to sell such reserve contracts in preference to trading in other markets (for example, performing price arbitrage in the spot energy market).

Turning to the perspective of the system operator, we have demonstrated that the proposed arrangement can be mutually beneficial to the system operator and battery operator. More precisely, the system operator can be protected against guaranteed financial losses from the incremental capacity contract purchase while the battery operator has a quantifiable profit. The analysis also provides information on feedback due to battery charging by determining the highest price at which the battery operator buys energy, hence identifying conditions under which the battery operator’s operational strategy is aligned with system stability.

We address incremental reserve contracts, which are particularly valuable to the system operator when the margin of electricity generation capacity over peak demand is low. Decremental reserve may also be studied in the above framework, although the second stopping time (action A2) is non-trivial, which leads to a nested stopping problem beyond the scope of the present paper. Furthermore, we assume that the energy storage unit is dedicated to providing incremental reserve contracts, so that the opportunity costs of not operating in other markets or providing other services are not modelled. The extension to a finite expiry time, the lifetime analysis with decremental reserve contracts, and also the opportunity cost of not operating in other markets would be interesting areas for further work.

The methodological advances of this paper reach beyond energy markets. In particular, they are relevant to real options’ analyses of storable commodities where the timing problem over the lifetime of the store is of primary interest. The lifetime analysis via optimal stopping techniques, developed in

Section 2.3, provides an example of how timing problems can be addressed for rather general dynamics of the underlying stochastic process. In this context, we provide an alternative method to quasi-variational inequalities, which are often dynamics-specific and technically more involved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}