The Impact of Changes to the Unemployment Rate on Australian Disability Income Insurance Claim Incidence

Abstract

:1. Introduction

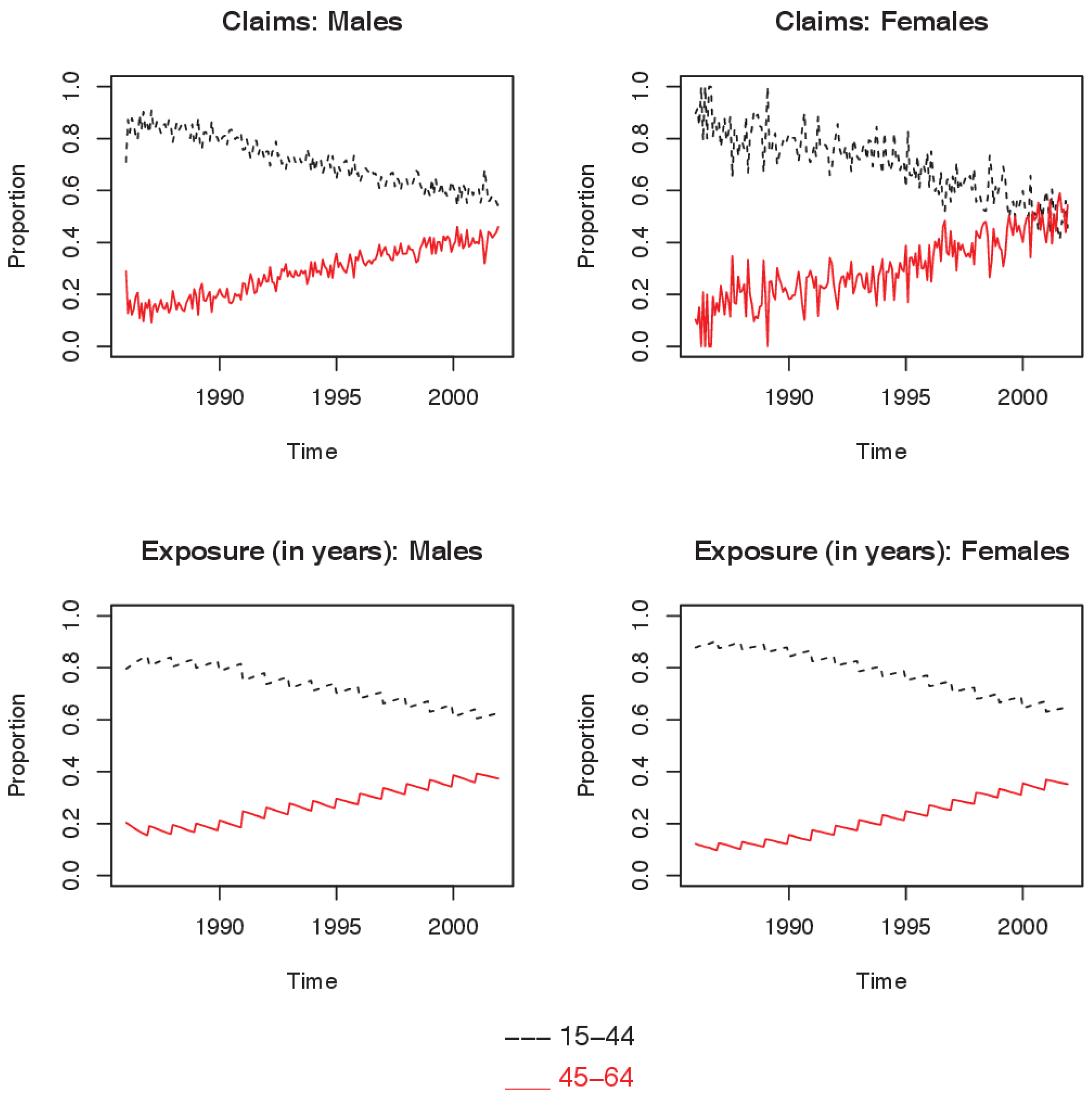

2. Data

3. Method

3.1. Modelling A/E for All DII Claims

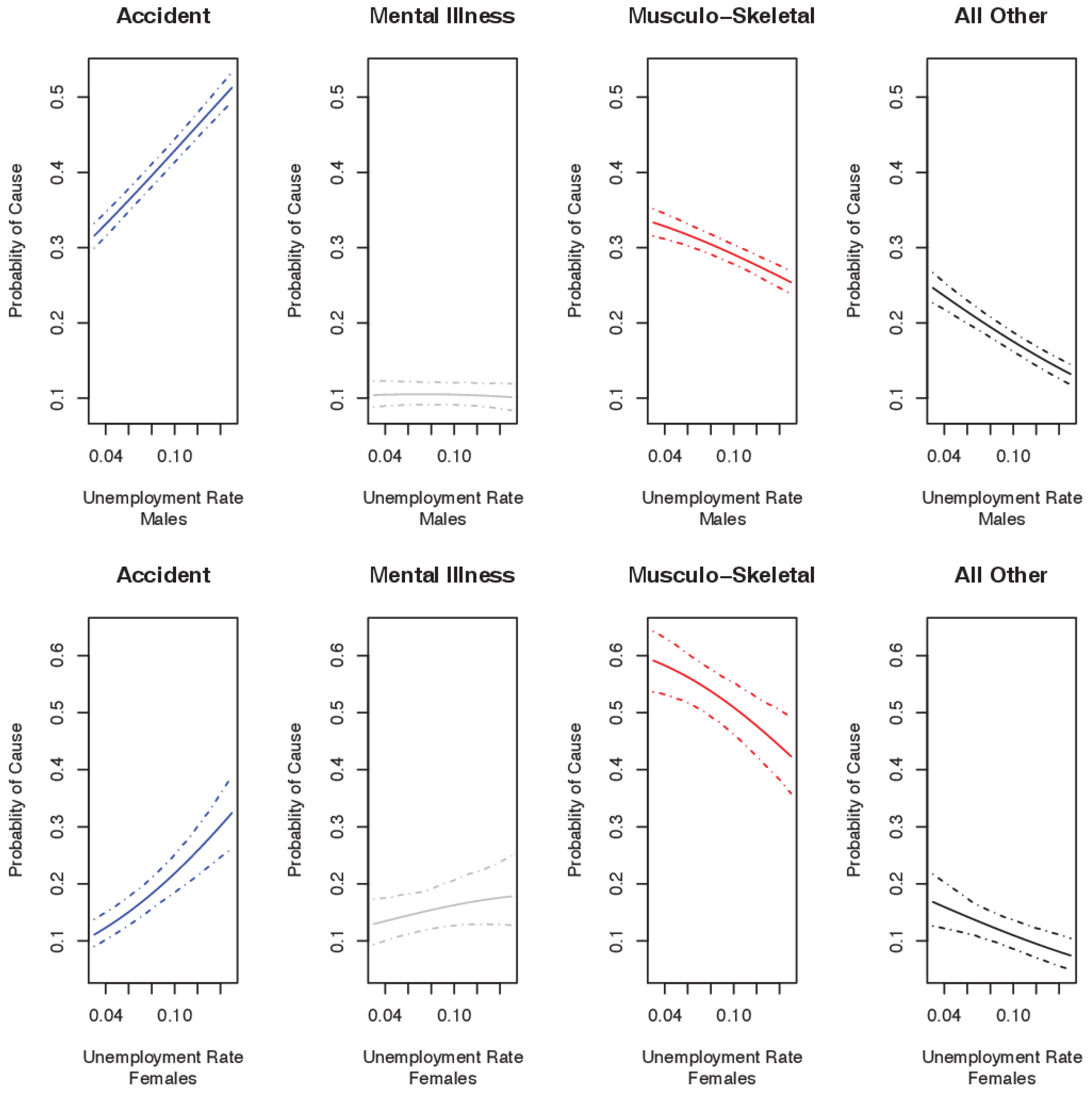

3.2. Modelling A/E by Cause of Claim

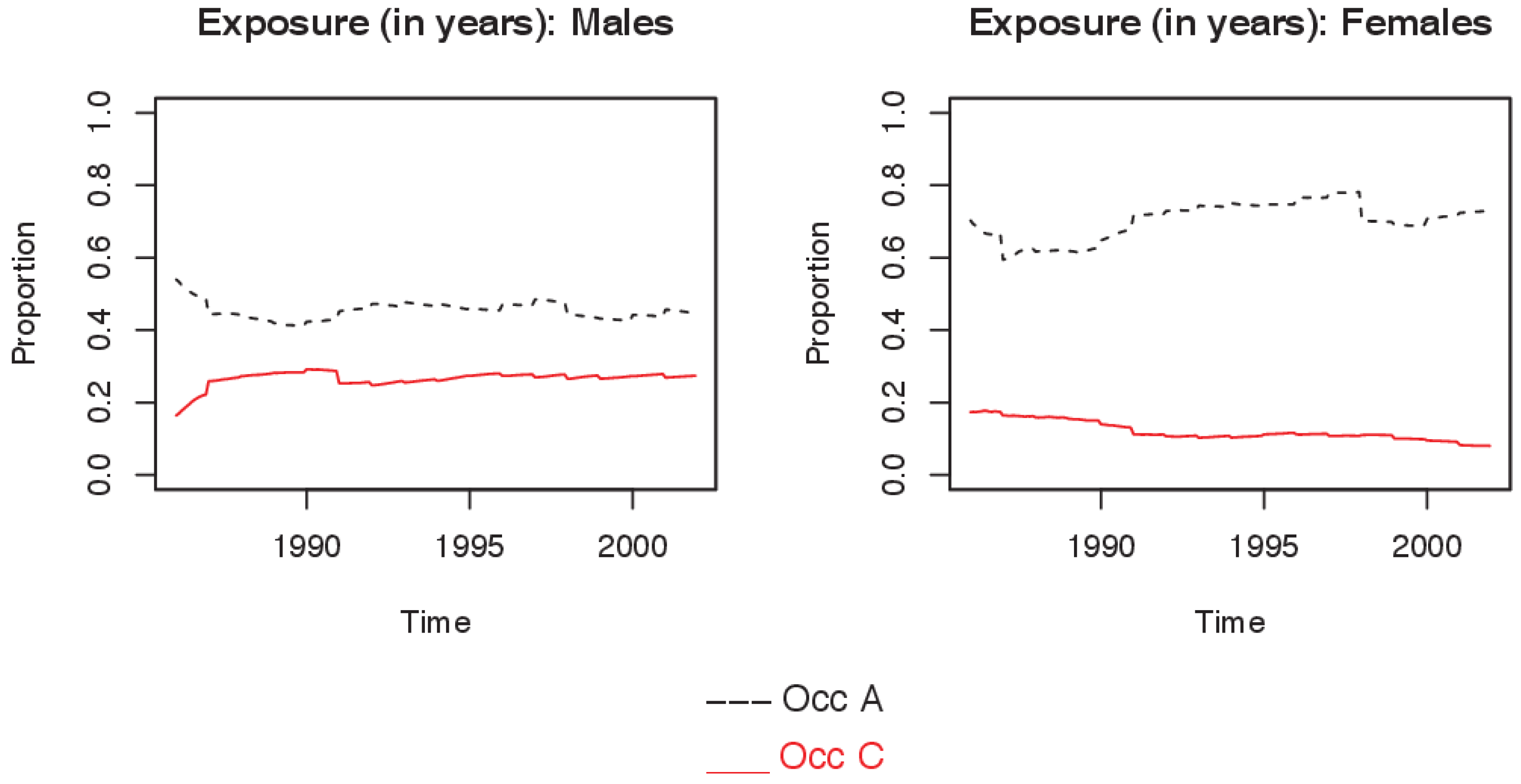

- Accidents;

- Mental Disorders;

- Musculoskeletal Diseases; and

- All Other.

4. Results

4.1. A/E for All DII Claims

4.2. A/E by Cause of Claim

5. Discussion

Supplementary Materials

Author Contributions

Conflicts of Interest

Abbreviations

| A/E | Actual-over-Expected |

| DII | Disability Income Insurance |

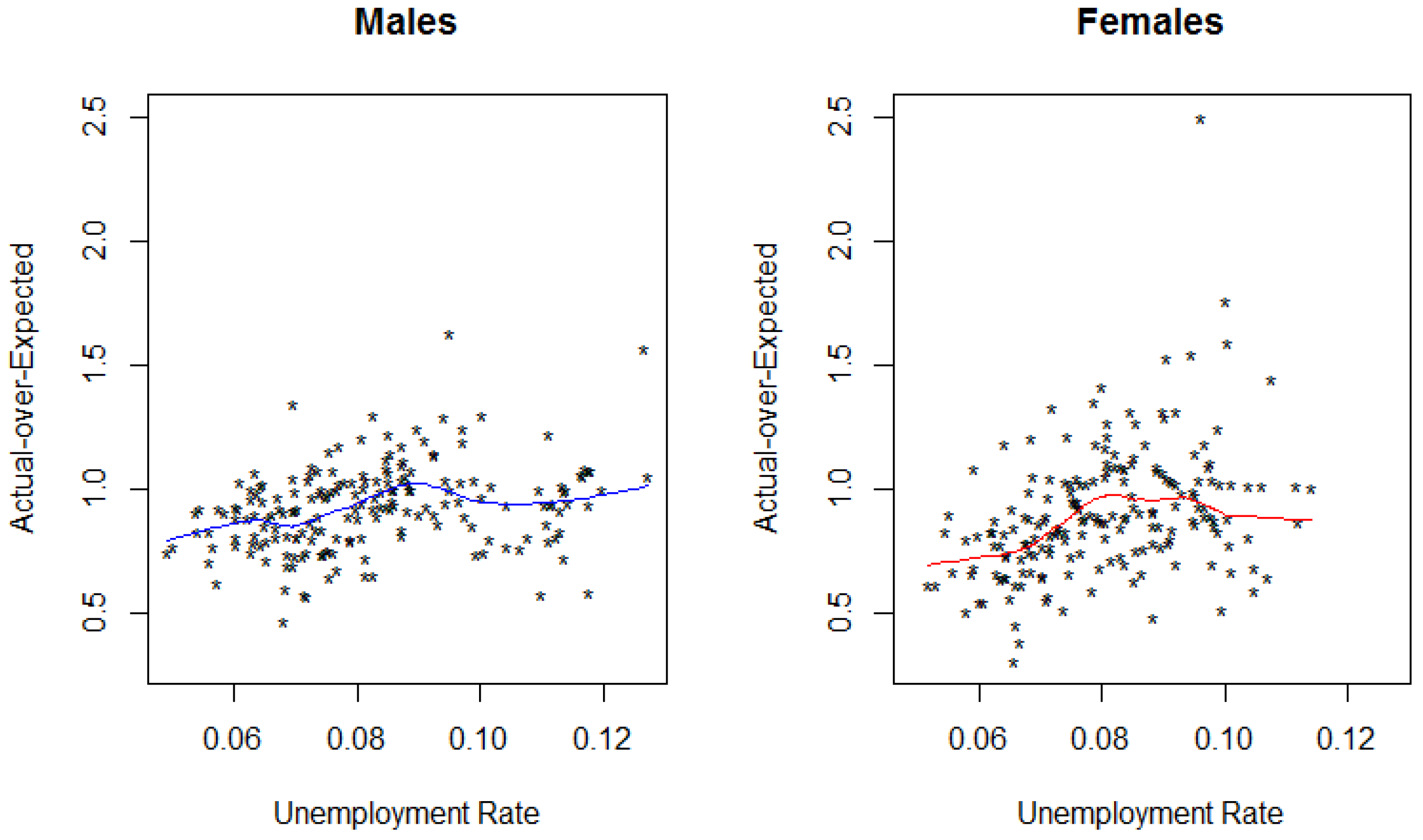

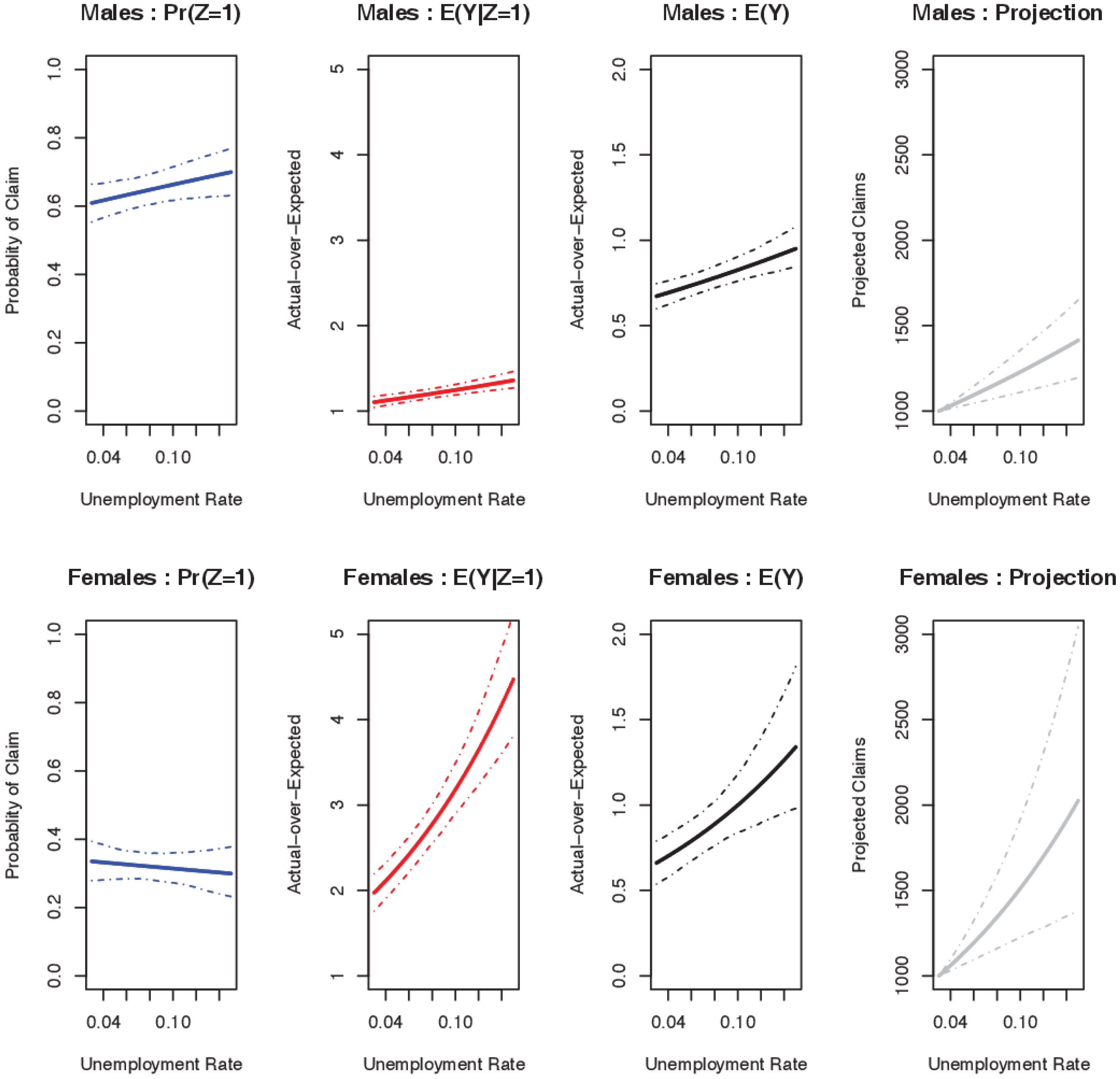

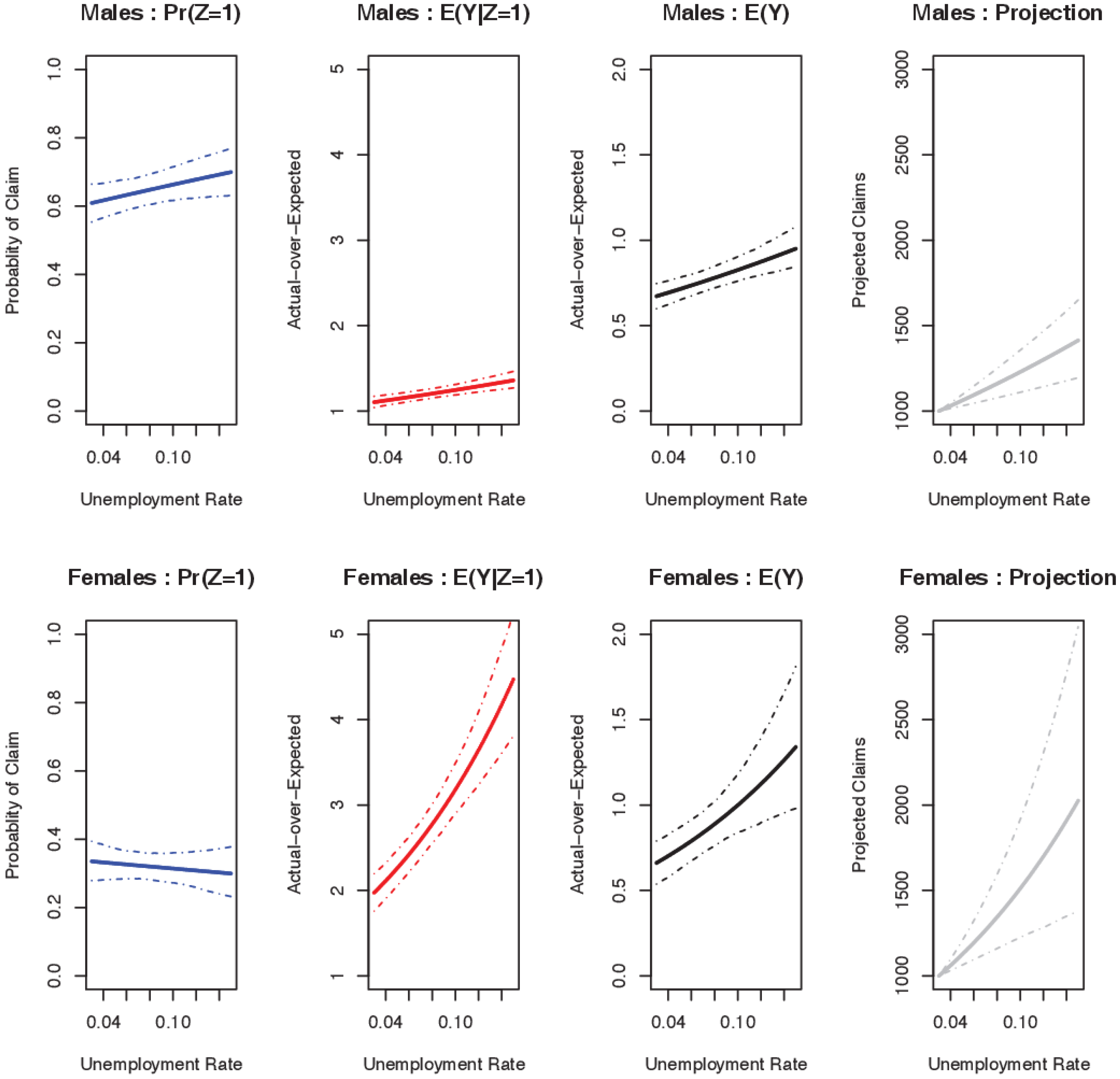

| IAAust | Australian Actuaries Institute |

| IAD | Incidence of Australian Disability |

| IBNyR | Incurred But Not yet Reported |

Appendix A

References

- D. Service, and K. Ferris. Disability Experience and Economic Correlations. Sydney, Australia: Institute of Actuaries of Australia Convention, 2001. [Google Scholar]

- M. Nordberg, and K. Røed. “Economic Incentives, Business Cycles, and Long-Term Sickness Absence.” Ind. Relat. J. Econ. Soc. 48 (2009): 203–230. [Google Scholar] [CrossRef]

- K. Schriek, and P. Lewis. “The Link between Disability Experience and Economic Conditions in South Africa.” International Congress of Actuaries 2010 Conference. Available online: http://www.ica2010.com/docs/02_final_paper_Schriek,_Lewis (accessed on 2 June 2012).

- I.C. Moore, and E. Tompa. “Understanding changes over time in workers’ compensation claim rates using time series analytical techniques.” Occup. Environ. Med. 68 (2011): 837–841. [Google Scholar] [CrossRef] [PubMed]

- D.A. Service. “Disability Income Insurance-The Australian Experience 1980–2001.” Ph.D. Thesis, Australian National University, Canberra, Australia, 2010. [Google Scholar]

- C. Donnelly, and M.V. Wüthrich. “Bayesian prediction of disability insurance frequencies using economic indicators.” Ann. Actuar. Sci. 6 (2012): 381–400. [Google Scholar] [CrossRef]

- D.J. Doudna. “Effect of the Economy on Group Long Term Disability Claims.” J. Risk Insur. 44 (1977): 223–235. [Google Scholar] [CrossRef]

- H. Smoluk, and B. Andrews. “Group Long-Term Disability Insurance Claims and the Business Cycle.” J. Insur. Issues 32 (2009): 154–172. [Google Scholar]

- S. Johnson. Unum Long Term Disability Insurance Study. Project Report; Worcester, MA, USA: Worcester Polytechnic Institute, 2011. [Google Scholar]

- B. König, F. Weber, and M.V. Wüthrich. “Prediction of disability frequencies in life insurance.” Zavarov. Horiz. 7 (2011): 5–23. [Google Scholar]

- B. Wolters. Reforming the Dutch Disability System-Just a Game. Stamford, CT, USA: Risk Insights®, Gen Re, 2008. [Google Scholar]

- A.S. Brooker, J.W. Frank, and V.S. Tarasuk. “Back pain claim rates and the business cycle.” Soc. Sci. Med. 45 (1997): 429–439. [Google Scholar] [CrossRef]

- Institute of Actuaries Australia. Graduation of the 1989–1993 Australian Disability Experience: IAD 89-93. Sydney, Australia: Graduation Subcommittee of the Disability Committe, 1996. [Google Scholar]

- Australian Bureau of Statistics. Labour Force Australia. Catalogue 6202.0; Canberra, Australia: Commonwealth of Australia, 2010.

- W.S. Cleveland, and S.J. Devlin. “Locally Weighted Regression: An Approach to Regression Analysis by Local Fitting.” J. Am. Stat. Assoc. 83 (1988): 596–610. [Google Scholar] [CrossRef]

- J.P. Boucher, M. Denuit, and M. Guillén. “Risk Classification for Claim Counts.” N. Am. Actuar. J. 11 (2007): 110–131. [Google Scholar] [CrossRef]

- K. Antonio, E.W. Frees, and E.A. Valdez. “A Multilevel Analysis of Intercompany Claim Counts.” ASTIN Bull. 40 (2010): 151–177. [Google Scholar] [CrossRef]

- A. Welsh, R. Cunningham, C. Donnelly, and D. Lindenmayer. “Modelling the abundance of rare species: statistical models for counts with extra zeros.” Ecol. Model. 88 (1996): 297–308. [Google Scholar] [CrossRef]

- D. Fletcher, D. MacKenzie, and E. Villouta. “Modelling skewed data with many zeros: A simple approach combining ordinary and logistic regression.” Environ. Ecol. Stat. 12 (2005): 45–54. [Google Scholar] [CrossRef]

- A.C. Davison, and D.V. Hinkley. Bootstrap Methods and Their Application. Cambridge, UK: Cambridge University Press, 1997, Volume 1. [Google Scholar]

- 1.Schriek and Lewis [3] (p. 10), state that, “ ... more policyholders may enter disability claims for minor causes. While this may lead to increased claim notifications it should naturally also lead to an increase in declined claims”.

- 2.The other economic indicators used are the consumer sentiment index, the stock market index (S&P 500), corporate profitability and the consumption to wealth ratio. Service and Ferris [1] find a negative relationship between participation rate and disability incidence. One would expect a strong correlation between participation and employment rates during periods of economic downturn; high unemployment can discourage workers from remaining in the workforce, leading to a fall in participation rates. Although not modelled in this paper, we would expect similar results to those reported here if participation rates rather than unemployment rates were used in the model.

- 3.The country or company for which the data was analysed was not reported due to confidentiality reasons.

- 4.The claims incidence experience data makes a differentiation between the number of claims and the benefit paid, because there are various policies that only pay a partial amount of the claim. Partial claims arise when the insured claims partial loss of income arising out of disability. In order to illustrate the difference between actual number of claims and actual benefit per cent, consider four claimants: individuals A, B, C, and D. Individual A claims complete loss of income earning ability and hence is paid 100% of the sum insured per month. Individuals B and C claim to have lost 75% of their working capacity due to an accident and hence are awarded 75% of the sum insured per month, while individual D has been awarded 50% of their claim due to sickness. Since there are four claims, the actual number of claims is recorded as four, while the actual benefit per cent arising out of the four claims is 300% or the sum equivalent of three full claims paid. This gives rise to significant differences in the amounts of claims paid out by the insurer, and in order to avoid spurious bias, from here on claims imply actual benefit per cent.

- 5.Exposure refers to the total number of policy years for the group from which the Actual Benefit per cent and Expected data were obtained. In a way this refers to the underlying population size.

- 6.As far as we are aware this is the only such graduated table in publication over the period of the data used in this study, 1986–2001.

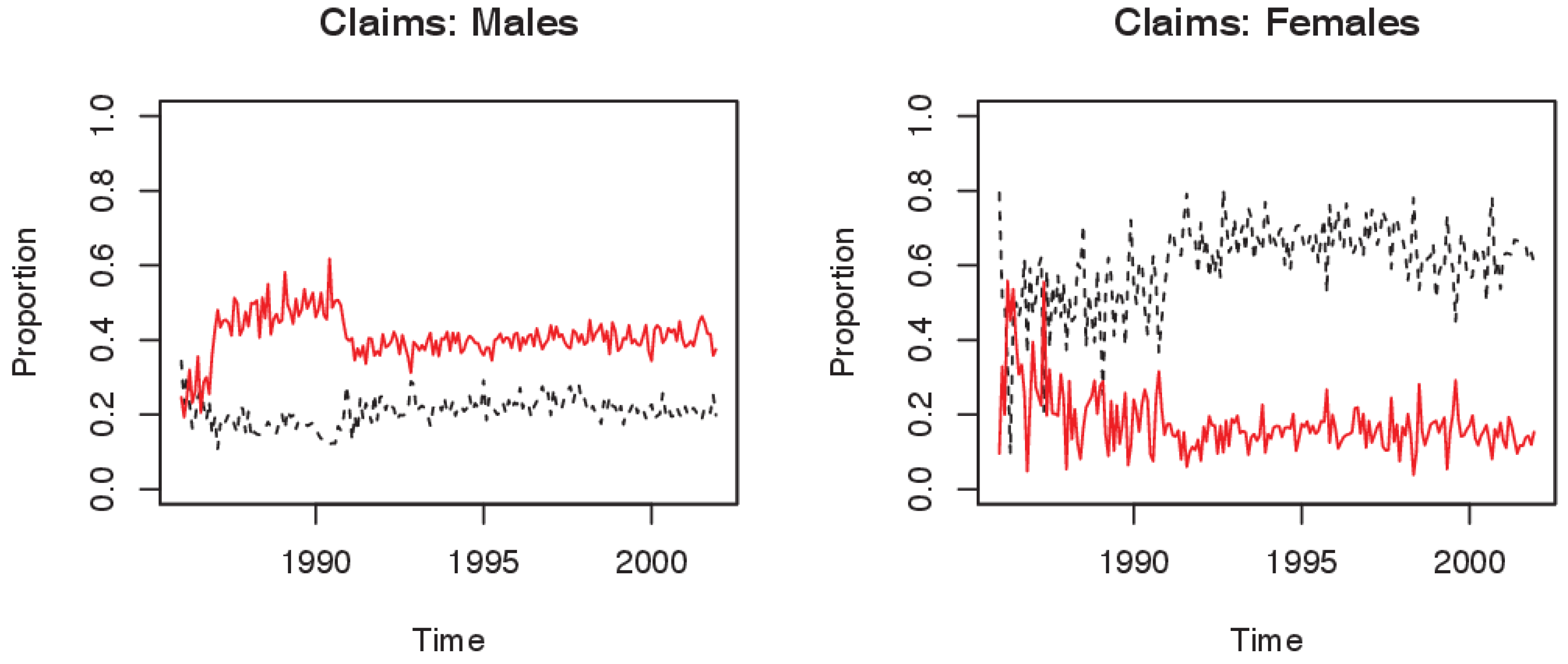

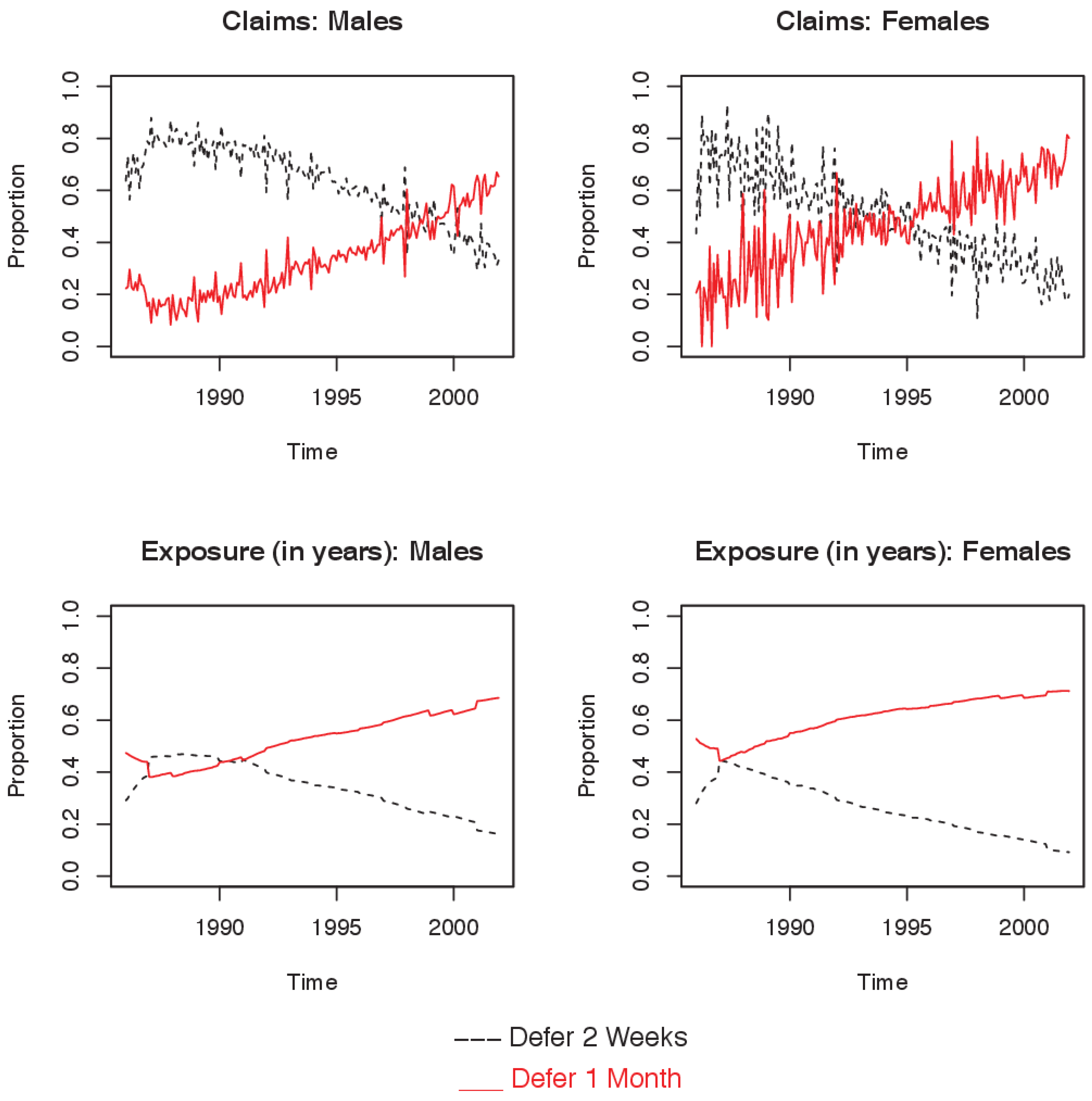

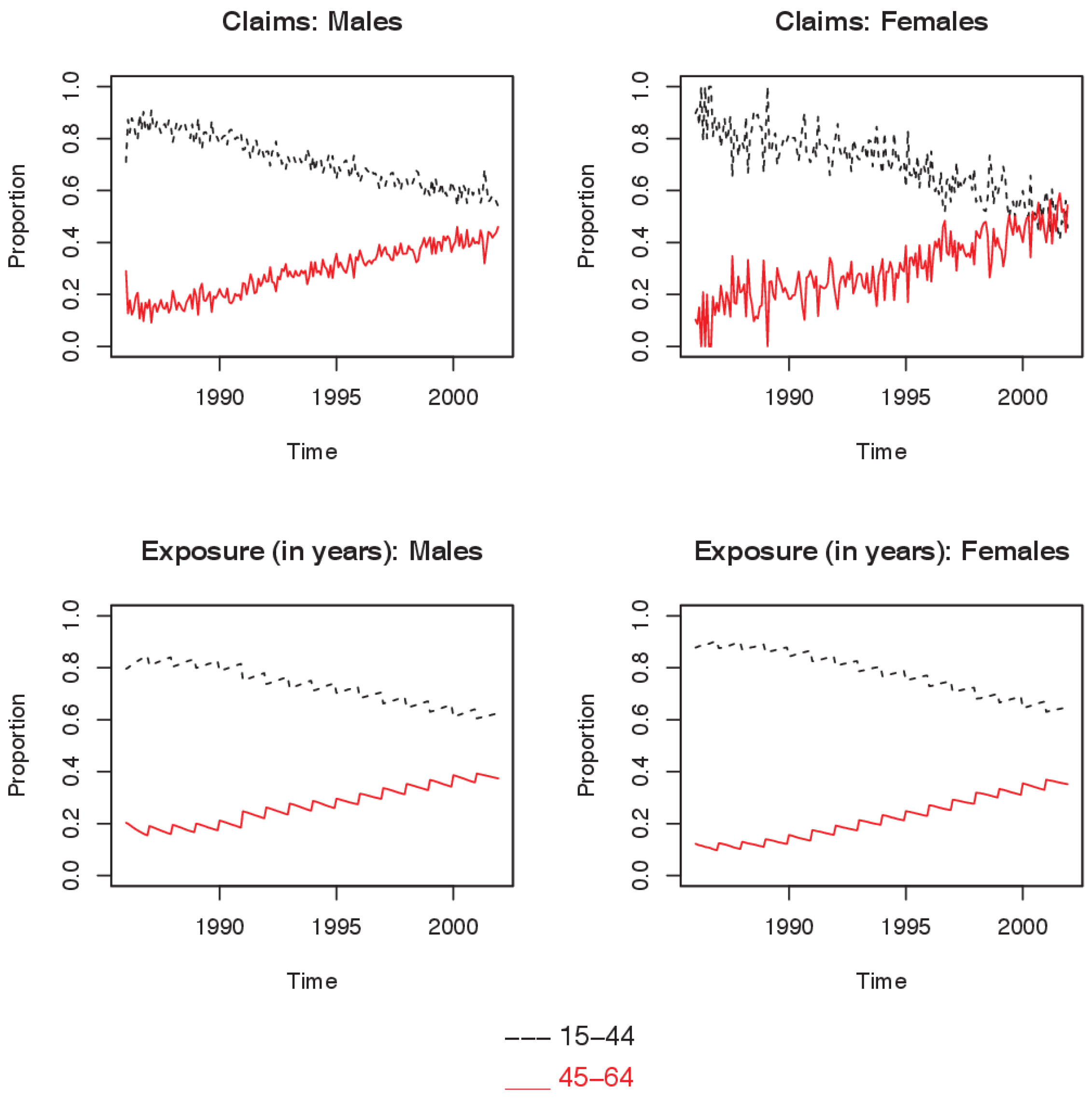

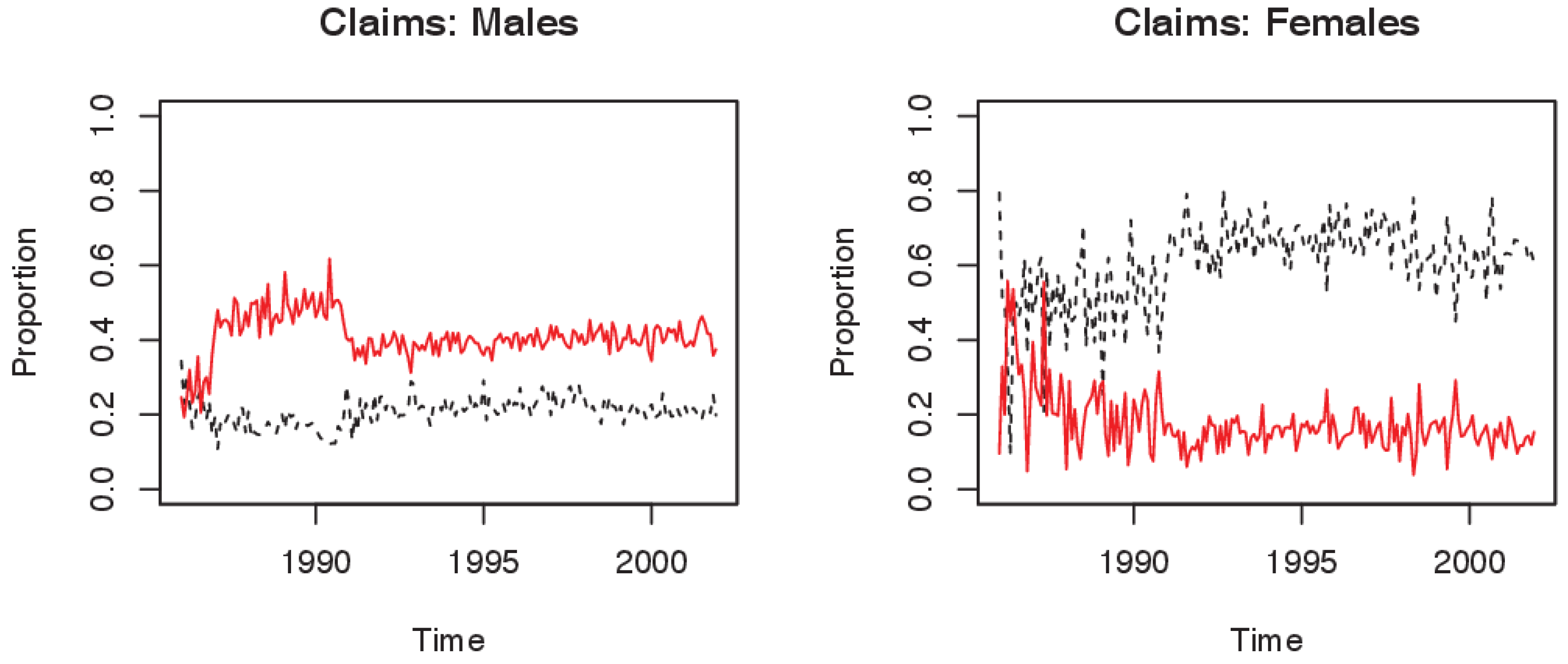

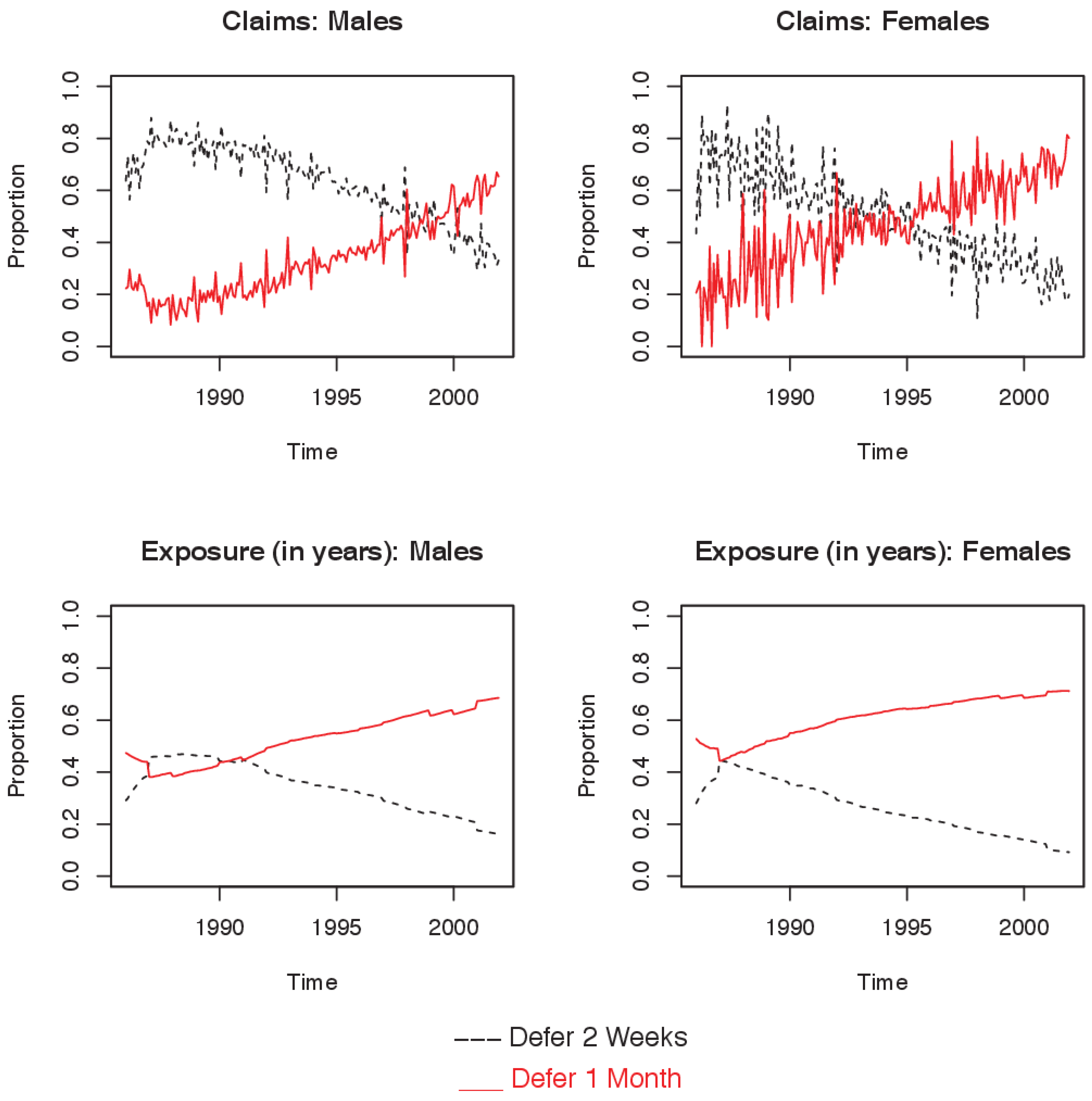

- 7.The data groups occupation into four broad classes. The classes are labeled as A, B, C and D. Briefly, the classes are as follows: A: Professional white-collar and sedentary, B: Other sedentary, C: Light manual worker, and D: Moderate and heavy manual workers. See Service [5] for more complete definitions. The original data included eight deferment periods: 7 and 14 days, 1, 2, 3, and 6 months, 1 and 2 years. As the data was sparse for deferment periods over 1 month, the corresponding categories were combined as > 1 month for the purpose of this study. In order to ensure that incidence of claims is recorded consistently, in the grouping of the deferment period data, claims are assigned to the date of incidence rather than commencement of benefits. For example, if a claim commences on June 2000 for a policy with a 1-year deferred period, then the claim is assigned to June 1999.

- 8.We say ‘approximately’, because the graduated table is based only on data from 1989–1993.

- 9.Labour statistics by age group, sex and states were obtained from the Australian Bureau of Statistics [14]. The unemployment rate was calculated by taking the ratio of the total unemployed to the total labour force for a given group (grouped by age and sex).

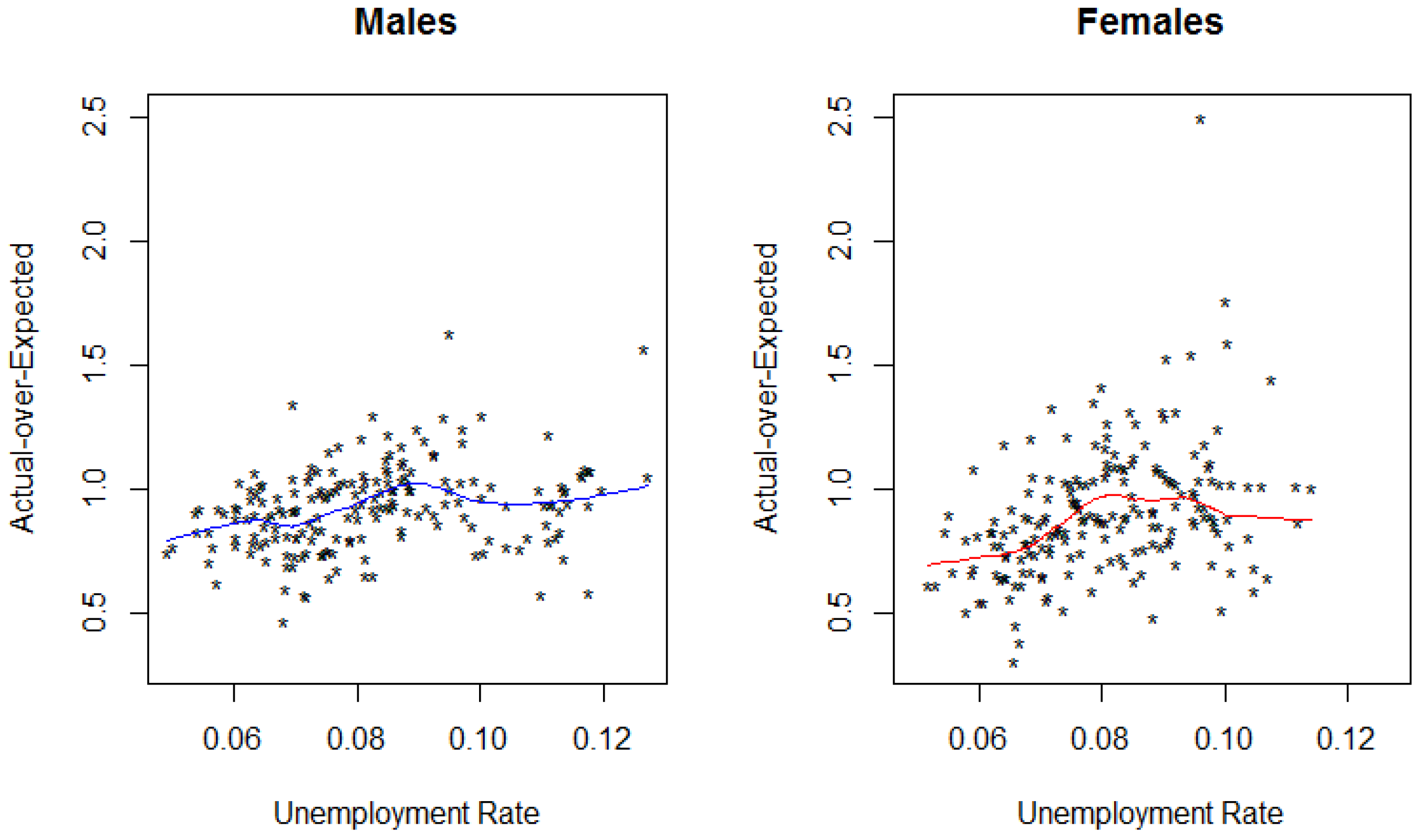

- 10.Lowess curves are locally weighted scatterplot smoothing curves. See Cleveland and Devlin [15].

- 12.The characteristics, as mentioned in Section 2, are those that are not included in the calculation of the Expected.

- 13.Unemployment rate with lags of 0, 1 and 2 months were analysed. However, concurrent unemployment rate (lag 0) had the highest significance in all the models analysed. Hence, only those are presented in this study.

- 14.See Section 2 for a list of these characteristics. The characteristics included in the logistic model are selected using a procedure similar to analysis of variance and only those characteristics that had a significant explanatory power were included. However, all the characteristics were included in the log-linear model (Model B).

- 15.In order to calculate the weights of each observation, we take the ratio of the exposure for the particular observation and the sum of all exposures in the data set. The resulting value is then multiplied by the total number of observations. These weights are applied to both the logistic and the log-linear model.

- 16.In the model-based bootstrap resampling method (parametric),using the model fitted on the initial dataset, we generate 1000 new vectors of the response variable and then fit the model again to the same predictor set to generate new estimates of π, μ and . From the resulting 1000 estimated vectors of π, μ and , the 2.5th and the 97.5th percentiles were taken, which formed the 95% confidence interval.

- 17.We also fitted a set of models with a modified , where we included available characteristics of age, deferment period and occupation class (along with the other characteristics). These three characteristics were included in the expected in the hurdle model, but were not accounted for here. The results of these set of models were very similar to the ones reported in this paper. We do not report these models to maintain consistency between the Multinomial Logistic and the Hurdle model.

- 18.The estimated probabilities sum to 1. That is, the results of the multinomial logistic model do not give the overall probability of a claim arising from a specific cause, but rather the conditional probability of a claim arising from a specific cause given that a claim has occurred.

- 19.Since the Expected does not take economic conditions into consideration, any systematic change in the A/E in the hurdle model can be attributed to the change in actual claims (the numerator).

- 20.In order to calculate the predictions, the value of the response for a given level of unemployment rate was calculated for every combination of the different characteristics for which the Expected was not available. There were 120 such possible combinations in all (the value of month was set at its modal value). The final prediction was obtained by averaging the results of the 120 combinations. This process was repeated for all the plots shown in the results section, and the corresponding plots in the appendix.

- 21.An A/E value of unity indicates that the actual claim experience is exactly equal to the Expected, whereas indicates that actual claim experience is better than Expected and vice versa. The results of the conditional model indicate that A/E does not equal unity for most of the range of the unemployment rate. In the case of males, is always less than unity, indicating that while unemployment is associated with an increase in claims, the resultant claim experience is always better than the Expected claim experience. In the case of females, however, the starts below unity and ends above unity, indicating that increasing unemployment leads to a worsening of the claim experience beyond the theoretical Expected. Hence, if a DII insurer were to base its capital reserves on the basis of the Expected, the reserves, in the case of female claimants, would be insufficient at higher levels of unemployment.

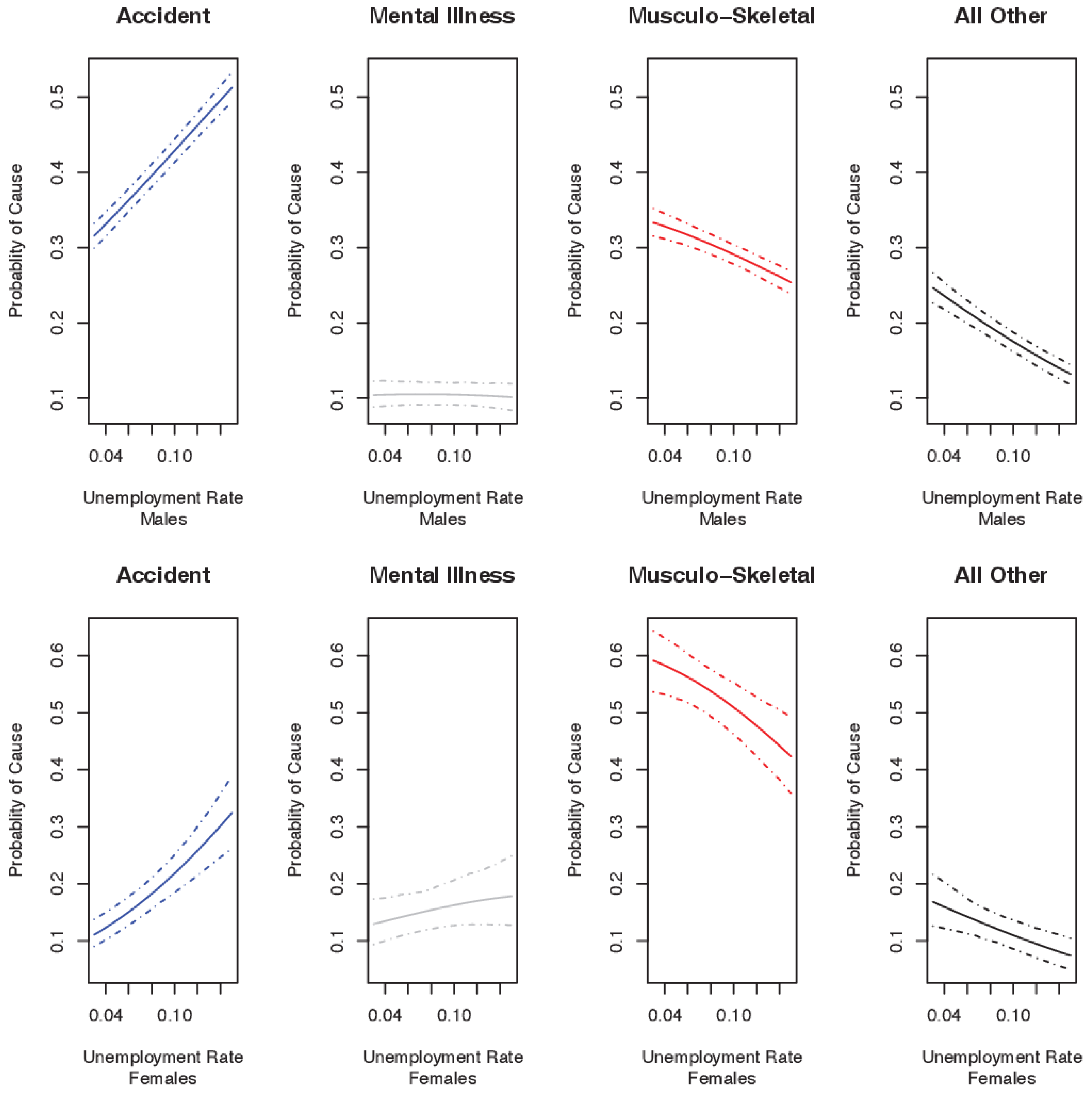

- 23.Note, by definition the probabilities have to sum up to unity. Hence, an increase in one of the four probabilities would indicate a decrease in one or more of the remaining causes. Also, the reader should interpret the conclusions regarding the magnitude and patterns of claim by cause of claim with caution due to the relative age of the data used in the analysis. Recent evidence of increases in mental disorder claims in Australia suggest a need for re-examination of this research question with more contemporary data once it becomes available.

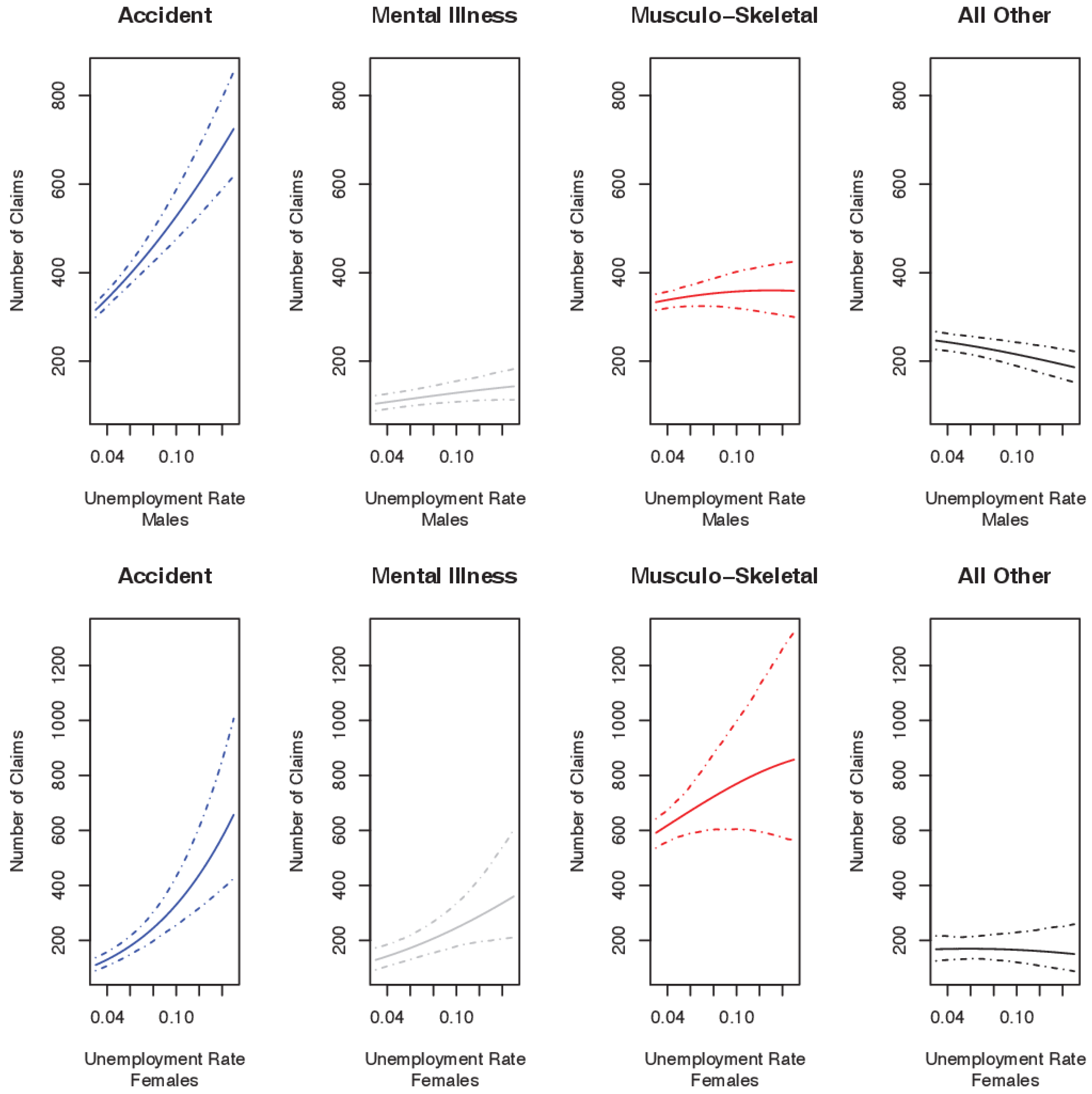

- 24.For all calculations, the base number of claims at the 3% unemployment rate is taken to be 1,000; claims are then projected from a 3% to 15% unemployment rate. Thereafter, the average change in claims for 1% change in unemployment rate are calculated and reported.

- 25.Further, more detailed data would ideally enable inclusion of claim duration and claim severity in the modelling, thereby allowing more complete quantification of the financial implications of increasing unemployment rates.

- 26.The authors made all possible efforts to obtain data for later periods, but were unable to do so. The authors would welcome contact from readers who may have be aware of the existence of more recent publicly available data sources.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Actual Benefit per Cent | Expected Claims | Actual-over-Expected | Exposure (000s of Years) | |||||

|---|---|---|---|---|---|---|---|---|

| Year | M | F | M | F | M | F | M | F |

| 1986 | 1230 | 140 | 1395 | 128 | 0.88 | 1.1 | 19,591 | 2004 |

| 1987 | 2575 | 306 | 2582 | 279 | 1 | 1.09 | 33,311 | 4035 |

| 1988 | 2536 | 342 | 2941 | 343 | 0.86 | 1 | 37,616 | 5083 |

| 1989 | 2849 | 377 | 3228 | 409 | 0.88 | 0.92 | 41,147 | 6218 |

| 1990 | 3164 | 419 | 3782 | 527 | 0.84 | 0.8 | 49,125 | 8240 |

| 1991 | 4596 | 578 | 5405 | 738 | 0.85 | 0.78 | 68,306 | 11,761 |

| 1992 | 4966 | 730 | 5545 | 826 | 0.9 | 0.88 | 74,795 | 13,672 |

| 1993 | 5799 | 869 | 5876 | 880 | 0.99 | 0.99 | 81,365 | 14,793 |

| 1994 | 6332 | 880 | 6522 | 981 | 0.97 | 0.9 | 92,019 | 16,657 |

| 1995 | 6615 | 968 | 6245 | 967 | 1.06 | 1 | 87,582 | 16,485 |

| 1996 | 6826 | 1043 | 6449 | 1030 | 1.06 | 1.01 | 91,771 | 17,524 |

| 1997 | 6794 | 1090 | 6589 | 1090 | 1.03 | 1 | 96,921 | 18,756 |

| 1998 | 6130 | 918 | 6734 | 1140 | 0.91 | 0.81 | 98,995 | 19,424 |

| 1999 | 6165 | 912 | 6690 | 1142 | 0.92 | 0.8 | 97,240 | 19,297 |

| 2000 | 6332 | 919 | 7220 | 1282 | 0.88 | 0.72 | 107,555 | 21,608 |

| 2001 | 5524 | 803 | 7433 | 1379 | 0.74 | 0.58 | 120,539 | 24,570 |

| Males | Females | |||

|---|---|---|---|---|

| Claims | Exposure | Claims | Exposure | |

| Age Group | ||||

| 15–44 | 0.69 | 0.71 | 0.66 | 0.74 |

| 45–64 | 0.31 | 0.3 | 0.34 | 0.26 |

| Occupation Group | ||||

| A | 0.21 | 0.45 | 0.64 | 0.72 |

| B | 0.09 | 0.11 | 0.16 | 0.14 |

| C | 0.41 | 0.27 | 0.16 | 0.11 |

| D | 0.29 | 0.16 | 0.05 | 0.03 |

| Deferment Period | ||||

| One Week | 0.01 | 0.01 | 0.01 | 0 |

| Two Weeks | 0.6 | 0.31 | 0.44 | 0.21 |

| One Month | 0.37 | 0.56 | 0.52 | 0.65 |

| > One Month | 0.02 | 0.12 | 0.03 | 0.14 |

| Age | 15–44 | 45–64 | All |

|---|---|---|---|

| Males | |||

| Minimum | 5.32 | 3.87 | 4.92 |

| Maximum | 14.29 | 9.62 | 12.71 |

| Median | 9.06 | 5.84 | 8.04 |

| Mean | 9.25 | 6.2 | 8.27 |

| Standard deviation | 1.92 | 1.49 | 1.76 |

| Females | |||

| Minimum | 6.2 | 2.92 | 5.19 |

| Maximum | 12.82 | 7.02 | 11.4 |

| Median | 9.05 | 4.48 | 8.03 |

| Mean | 9.16 | 4.75 | 8.06 |

| Standard deviation | 1.48 | 0.91 | 1.36 |

| Males | Females | |||

|---|---|---|---|---|

| Log-Linear | Logistic | Log-Linear | Logistic | |

| Entire Population | 5.894 * | 1.731 ** | −2.309 | 6.815 ** |

| (2.373) | (0.356) | (1.881) | (0.801) | |

| Age Groups | ||||

| 15–44 | 2.314 | 1.388 ** | 4.531 ** | 5.465 ** |

| (1.827) | (0.366) | (1.645) | (0.891) | |

| 45–64 | −0.472 | 3.108 ** | −23.800 ** | 14.138 ** |

| (1.728) | (0.580) | (2.343) | (1.739) | |

| Occupation Classes | ||||

| A | 6.093 ** | 1.397 * | 2.807 | 7.307 ** |

| (1.503) | (0.545) | (1.811) | (0.954) | |

| C | −8.805 ** | 3.653 ** | −6.734 ** | 12.995 ** |

| (2.175) | (0.492) | (1.796) | (1.647) | |

| D | 11.160 ** | 6.140 ** | NA | |

| (2.107) | (0.607) | |||

| Deferment Periods | ||||

| Two Weeks | 10.250 ** | 2.702 ** | 12.802 ** | 3.997 ** |

| (2.066) | (0.405) | (1.597) | (1.101) | |

| One Month | −4.119 * | 0.64 | −14.181 ** | 8.020 ** |

| (1.643) | (0.496) | (1.717) | (1.061) | |

| All Claims | Accident | Mental Illness | Muscolo-Skeletal | All Other | ||

|---|---|---|---|---|---|---|

| Entire Population | Males | 34.5 * | 34.1 * | 3.3 | 2.1 | −5 |

| Females | 85.5 * | 45.5 * | 19.2 * | 22.2 | −1.5 | |

| Age Groups | ||||||

| 15–44 | Males | 21.8 * | 25.7 * | 1.8 | 0.2 | −5.8 * |

| Females | 120.7 * | 36.8 * | 21.3 * | 65.4 * | −2.8 | |

| 45–64 | Males | 35.6 * | 30.0 * | 5 | 4.3 | −3.8 |

| Females | −14.3 | 31.4 * | 3.3 | −44.7 * | −4.3 | |

| Occupation Classes | ||||||

| A | Males | 41.8 * | 46.7 * | 10.8 * | −17.6 * | 1.9 |

| Females | 150.7 * | 50.4 * | 32.4 * | 60.6 * | 7.3 | |

| C | Males | 13.7 | 35.2 * | 1.8 | −18.6 * | −4.7 |

| Females | 146.4 * | 45.9 * | 16.6 | 77.8 | 6.3 | |

| D | Males | 175.3 * | 160.1 * | 1.4 | 9 | 4.9 |

| Deferment Periods | ||||||

| Two Weeks | Males | 71.4 * | 72.4 * | 2 | −1.8 | −1.2 |

| Females | 207.0 * | 74.6 * | 27.6 * | 96.7 * | 8.1 | |

| One Month | Males | −5.2 | 30.6 * | 0.2 | −30.1 * | −5.9 * |

| Females | 9.4 | 14 | 6.5 | −8.3 | −2.9 | |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Khemka, G.; Roberts, S.; Higgins, T. The Impact of Changes to the Unemployment Rate on Australian Disability Income Insurance Claim Incidence. Risks 2017, 5, 17. https://doi.org/10.3390/risks5010017

Khemka G, Roberts S, Higgins T. The Impact of Changes to the Unemployment Rate on Australian Disability Income Insurance Claim Incidence. Risks. 2017; 5(1):17. https://doi.org/10.3390/risks5010017

Chicago/Turabian StyleKhemka, Gaurav, Steven Roberts, and Timothy Higgins. 2017. "The Impact of Changes to the Unemployment Rate on Australian Disability Income Insurance Claim Incidence" Risks 5, no. 1: 17. https://doi.org/10.3390/risks5010017

APA StyleKhemka, G., Roberts, S., & Higgins, T. (2017). The Impact of Changes to the Unemployment Rate on Australian Disability Income Insurance Claim Incidence. Risks, 5(1), 17. https://doi.org/10.3390/risks5010017