All articles published by MDPI are made immediately available worldwide under an open access license. No special

permission is required to reuse all or part of the article published by MDPI, including figures and tables. For

articles published under an open access Creative Common CC BY license, any part of the article may be reused without

permission provided that the original article is clearly cited. For more information, please refer to

https://www.mdpi.com/openaccess.

Feature papers represent the most advanced research with significant potential for high impact in the field. A Feature

Paper should be a substantial original Article that involves several techniques or approaches, provides an outlook for

future research directions and describes possible research applications.

Feature papers are submitted upon individual invitation or recommendation by the scientific editors and must receive

positive feedback from the reviewers.

Editor’s Choice articles are based on recommendations by the scientific editors of MDPI journals from around the world.

Editors select a small number of articles recently published in the journal that they believe will be particularly

interesting to readers, or important in the respective research area. The aim is to provide a snapshot of some of the

most exciting work published in the various research areas of the journal.

We study risk-minimization for a large class of insurance contracts. Given that the individual progress in time of visiting an insurance policy’s states follows an -doubly stochastic Markov chain, we describe different state-dependent types of insurance benefits. These cover single payments at maturity, annuity-type payments and payments at the time of a transition. Based on the intensity of the -doubly stochastic Markov chain, we provide the Galtchouk-Kunita-Watanabe decomposition for a general insurance contract and specify risk-minimizing strategies in a Brownian financial market setting. The results are further illustrated explicitly within an affine structure for the intensity.

The management of an insurance portfolio’s risk is one of the core challenges in actuarial science. While the classic form of risk mitigation is based on reinsurance contracts, in some cases it is also possible to hedge claim payments by appropriately trading in different assets. This particularly applies if the assets are correlated to the insurance contract’s benefits or their (conditional) probability of occurrence. Practical examples in this direction are unit-linked life insurance products, where benefits depend on the performance of the assets, or unemployment insurance products, where the occurrence of a claim payment may depend to some extend on economic and financial conditions of the markets. Moreover, there is an ongoing discussion about the introduction of so called longevity bonds which would establish the possibility for life insurance companies and pension funds to hedge parts of their longevity risk, see [1,2] or [3]. Due to their unsystematic risk part, most insurance claims are not hedgeable completely through a self-financing trading strategy which particularly means that a hybrid market, consisting among others of financial and insurance markets, is incomplete. A reasonable method for optimally choosing an investment strategy is then important to cover at least parts of the risk.

In the present paper we choose the risk-minimization approach and determine hedging strategies in the sense of this criterion for insurance contracts in a very general setting. This quadratic hedging approach bases on the results in [4] for European type payments and to [5] for payment processes. In most cases, the risk-minimizing strategies can be derived from the well known Galtchouk-Kunita-Watanabe (GKW-) decomposition, see [6] or [7].

Similar to the works of [5,8] or [9,10,11], we describe an insured person’s progress of sojourning different states of an insurance policy as a right continuous stochastic process with finite state space , 1 being a.s. the initial state. More specifically, we adopt the class of -doubly stochastic Markov chains as introduced in [12], see Appendix A and the comments therein. This family of processes has several properties which make them very suitable for applications in credit risk and insurance market modeling. Being a sub-class of -conditional Markov chains, they extend the classic notion of Markov chains by including a reference filtration which in our case represents additional market information. In this way we are able to take in consideration the influence of external risk factors and economic and financial conditions on transition probabilities of an insured person’s progress. In particular, -doubly stochastic Markov chains behave like time inhomogeneous Markov chains, if we know all the information concerning the underlying risk factors. This corresponds to the intuition that the transition probabilities would be completely specified, if we would dispose of full knowledge on the underlying economic and financial situation.

Another important feature is that, if we specify the information as given by the filtration , where is the natural filtration of the -doubly stochastic Markov chain X, then we have that predictable representation theorems and the so-called hypothesis (H) 1, or immersion property, hold. These properties play a fundamental role in order to compute the optimal strategy for insurance contracts according to the risk-minimization method.

Furthermore, -doubly stochastic Markov chains may admit matrix-valued stochastic intensity processes. This allows to investigate more flexible models compared to the results e.g., in Møller [5] where a (classical) Markov chain with deterministic intensity matrix function is considered. One further advantage is that -doubly stochastic Markov chains with intensity are fully characterized by some martingale properties, which can be used for the estimation of the underlying intensity processes, see Biagini et al. [13].

Well known examples of -doubly stochastic Markov chains are reduced form or intensity based models in the case that hypothesis (H) is satisfied. Here, the state space consists of two states with the second state being absorbing such that there can only occur one transition in time. There exist many works on quadratic hedging for these models particularly in the context of credit risk or life insurance theory, see e.g., [1,2,14,15,16,17,18,19] or [20]. In particular, the present paper extends these works to a multi-state framework where several subsequent transitions, driven by -adapted stochastic intensity processes, are considered. This general setting allows to investigate a larger class of insurance contracts, e.g., income protection insurance contracts with the states “healthy”, “sick” and “deceased”, and to include the influence of market conditions and external risk factors on the insured person’s progress.

Given an -doubly stochastic Markov chain, we propose a general insurance contract, defined by three different types of insurance benefits: state-dependent payments at maturity, state-dependent annuity-type payments, and (transition-dependent) payments at the time of a transition from one state to another. This definition covers a large set of currently adopted insurance policies. In particular, we illustrate the definitions for pure endowment, term insurance, general life annuity and payment protection insurance contracts. Similar to the results in [21], who applied -doubly stochastic Markov chains in the context of hedging rating-sensitive financial claims, we obtain the GKW-decomposition for the payment process of general insurance contracts with respect to a particular -martingale. In this context, we generalize and complement the proofs in [21] in order to adapt the results for the risk-minimization approach which is not investigated there.

Given that the reference information is generated by an N-dimensional Brownian motion , we then introduce a financial market model, driven by . In this setting we infer risk-minimizing hedging strategies for insurance contracts with deterministic payment structure with respect to the assets on the financial market. Similarly to the work in [2] we then assume a general affine structure for the intensity of the underlying -doubly stochastic Markov chain and obtain explicit formulas for the strategies and their residual risk processes. We apply these results in the specific example of an income protection insurance, where we assume that the intensities follow a (multi-dimensional) Ornstein-Uhlenbeck process. We discuss the resulting expected cumulative payment, which may be considered as a fair premium in the interpretation of [22,23], as a function of the time horizon, the payment amounts and the underlying interest rates.

The paper is organized as follows. In Section 2 we introduce the notion of general insurance contracts and discuss several examples. In Section 3 we prove our main results for the risk minimization of this kind of contracts in full generality. The risk minimizing strategies are then further illustrated within a general affine specification for the intensities and in a numerical example in an Ornstein-Uhlenbeck framework. We conclude the paper with Appendix A and Appendix B, where we summarize important results and concepts of risk-minimization and -doubly stochastic Markov chains for the reader’s convenience.

2. General Insurance Contracts

We now introduce the notion of general insurance contracts and provide some well known examples of actuarial practice.

In the same notation as in Appendix A, let be a filtered probability space with for some -doubly stochastic Markov chain X with state space . We assume . The following definition of general insurance contracts is based on the definitions for payment processes on rating sensitive claims as given e.g., in [21] or [20]. The definition also covers the concepts of insurance contracts as given in [5] or [9].

Definition1.

A general insurance contract is given by the quadruple , where is an -doubly stochastic Markov chain, is an -adapted, N-dimensional process of finite variation, is an -measurable, N-dimensional random vector, and with is an -adapted, -dimensional process with zeros on the diagonal.

The different elements of a general insurance product’s quadruple are interpreted as follows. The process X is the insured person’s progress in time of sojourning in the states , considered by the insurance policy. The N-dimensional process characterizes the cumulative state-dependent payment streams which are continuously paid up to maturity. For example, one can take , with representing the cumulative state-dependent claim payments (e.g., annuities) and the cumulative state-dependent insurance premiums up to maturity. Both processes, and are then taken to be -adapted, càdlàg and increasing. The vector characterizes state-dependent “extra” claim payments at maturity T and the process the “immediate” claim payments at the transition times from one state to another.

For every general insurance contract the cumulative payment process is given by

with as defined in Equation (A7) and counting processes from Equation (A8). Note that D is of finite variation. We now provide some well known examples of insurance contracts.

Example1.

A pure endowment is an insurance contract which guarantees to the insured person some fixed payment if she is alive at maturity. For the sake of simplicity, we only consider the payment to be equal to 1.

We set with 1 being the state “alive” and 2 the absorbing state “deceased”. A pure endowment contract is then given as the quadruple or if premium payments are considered, respectively.

Example2.

A term insurance is an insurance contract which guarantees the heirs of an insured person some fixed payment at the time of decease. For the sake of simplicity, we only consider the payment to be equal to 1.

Again, we set with 1 being the state “alive” and 2 the absorbing state “deceased”. Then a term insurance contract is given as the quadruple or if premium payments are considered, respectively, with .

Example3.

A general annuity as defined in [2] is an insurance contract which guarantees the insured person an -progressively measurable, non-negative continuous rate payment as long as she is alive. The state space is again with 1 being the state “alive” and 2 the absorbing state “deceased”. Then a general annuity contract is given as the quadruple or if premium payments are considered, respectively.

Example4.

A payment protection insurance (PPI) is an insurance contract which is usually offered as an add-on product to some payment obligations, e.g., a loan. In the case of an insured event, the insurance company takes over the respective instalments of the payment obligation for the insured person or her heirs. Generally, the insured events are “disability”, “unemployment” and “decease”. Hence, the state space for PPI products is given as with “2” being the state “disabled”, “3” the state “unemployed”, “4” the absorbing state “deceased” and “1” the state where no insured event is present.

Then a PPI contract is given as the quadruple or if premium payments are considered, respectively.

As the underlying payment obligation usually stipulates fixed instalments at some given payment dates , the processes , , are generally given as .

Moreover, some payment obligations also contain a so-called balloon rate B at the end of the contract, which has to be paid on top of the usual instalment. If there exists a balloon rate and it is insured, then we set , if there exists no balloon rate or it is not insured, then we set .

Remark1.

(1)

The extra claim payment could also be included in the continuous claim payments. For the reader’s convenience, however, we explicitly separate continuous and extra claim payments.

(2)

The main concepts of premium payment are

-

a single premium P, where the complete price for the insurance contract is paid at its beginning. In this case, the vector would be given as .

-

periodically paid premiums. Here, the insurance price is paid according to periodically paid premiums at a priori specified dates . Moreover, some insurance policies consider premium freedoms which allow the insured person to intermit premium payments while sojourning (some) insured states. In this case, we have for each vector entry , , of

depending on whether state i is guarantees premium freedom or not.

3. Risk-Minimization for General Insurance Contracts

Aim of this paper is to provide the risk minimizing strategy for a general insurance contract by applying the approach presented in Appendix B. Risk minimization provides hedging strategies which perfectly replicate the claim. Since the market is incomplete, these strategies may not be self-financing and a readjustment (or cost) is needed to achieve perfect replication. According to this method we choose then the optimal strategy, i.e., the strategy with minimal cost.

For this sake, we first consider a general setting and then focus on a deterministic payment structure and an underlying market which is driven by some N-dimensional Brownian motion. These results are then further specified within a general affine setting for the different entries of the matrix-valued intensity.

3.1. Martingale Decomposition for Payment Processes of General Insurance Claims

We consider the payment process D in Equation (1). Let denote the market’s discounting factor, which will be further specified in Section 3.2. If , we get by Equation (B1) that the discounted cumulative payment stream is given as

We further assume the underlying -doubly stochastic Markov chain X to admit an intensity , as introduced in Definition A.5.

Note that Equations (3), (4), (6) and (7) ensure that the discounted payment stream generated by the general insurance contract is square integrable.

We remark that the following Lemma is given similarly in [21] (Theorem ) under the assumption the local martingale , defined in Equation (A9), is square integrable and the processes and are bounded. Here, we generalize their proof to the case where and satisfy the conditions of Assumption 2.

For notational convenience, we introduce the process with

Lemma3.

Let be a general insurance contract, satisfying Assumption 2, then

where the conditional transition probability process , is defined in Definition A.1.

Proof.

We proove the theorem by investigating the different conditional expectations separately.

First note that because is taken to be -measurable and to be -adapted, by Equation (A3) we get for every

where .

Next, by Equation (A10) of Theorem A.7, we get for , that

Note that because of Equations (A15) and (6), the integral-process with respect to is a square integrable -martingale. Hence, for every , , we have

by the conditional version of Fubini’s theorem, the definition of -doubly stochastic Markov chains and hypothesis (H).

Finally, for every and for fixed we define , . By Proposition A.9 we get

with

Since is -measurable, it follows by the hypothesis (H) that

Again by the conditional version of Fubini’s theorem, hypothesis (H) and with the Kolmogorov forward Equation (A6) it follows that

Hence, by integration by parts and since is continuous, we get

This completes the proof. ☐

Now we are ready to provide the Galtchouk-Kunita-Watanabe decomposition for payment processes of general insurance contracts.

Theorem4.

Let be a general insurance contract, satisfying Assumption 2, with discounted payment process , defined in Equation (2). Then the GKW-decomposition of the square-integrable discounted value process with is given as

where is given by Equation (A9), is a square-integrable -martingale, given by

and are -predictable -valued processes defined by

with , , defined by Equation (A7), , , defined in Equation (A11), , , defined by

and .

Proof.

The statement and the proof of this theorem can be found in [21] (Theorem 16.62). The authors there, however, prove Decomposition 10 only for . Because the integrals on the r.h.s. are not all continuous, it is a priori not clear if the decomposition also holds for . Here we refer to [24] (Theorem 4.2.3) for an extension of the proof of [21] to the case . ☐

3.2. Risk Minimization for General Insurance Contracts with Deterministic Payment Structure

In this section we focus on a more specific setting, where we specify the underlying financial market and derive risk-minimizing hedging strategies for insurance contracts with deterministic payment structures.

We start by specifying the underlying market. First of all, we assume the reference filtration to be the augmented filtration, generated by some N-dimensional Brownian motion . For computational reasons, particularly in the affine setting of the next section, we set the dimension N of the Brownian motion equal to the number of states under consideration.

Consider then a financial market consisting of traded assets , assumed to be -adapted, non-negative stochastic processes. Let denote the -valued stochastic process of the primary assets , discounted with the asset , i.e., , . Here is taken to be continuous with for all and shall generally represent the value of a self-financing portfolio on the primary assets. In the sequel, we assume to be a local -martingale, which particularly implies that the market model is arbitrage-free.

Remark2.

The requirement that is a local martingale may appear restrictive. However it is always satisfied if we choose to be the numéraire portfolio defined in [25], since we assume the underlying financial market to contain only continuous asset price processes.

We could also start with a general situation where the discounted asset price processes are given by semimartingales. In this case one has to assume some technical conditions to guarantee the existence of the optimal strategy, see [26,27].

Here we prefer to avoid technical complications since our aim is to compute explicitly the risk-minimizing strategy when it exists.

By the representation theorem with respect to Brownian motion it follows that there exists a measurable map , such that

Assumption5.

We assume that is a.s. left-invertible, i.e., that for almost every there exists an -adapted -valued matrix such that . This particularly implies .

From now on we focus on discount factors and insurance contracts with deterministic payment structure.

Assumption6.

(1)

is a deterministic vector in .

(2)

The payment is of the form for some bounded deterministic function .

(3)

is a bounded deterministic matrix-valued function.

(4)

is a deterministic continuous function.

(5)

For every , , .

Assumption 6 particularly implies that the integrability conditions of Assumption 2 hold. Note also that the insurance contracts, given in Examples 1, 2 and 4 all satisfy , and of Assumption 6. The assumption on being deterministic is applied very frequently in the literature, e.g if is assumed to be some risk-neutral probability measure and for some constant .

Remark3.

Here we assume constant interest rates for the sake of simplicity, since the focus of this paper is primarily to evaluate the role of a multi-state progression of the insured person on the risk-minimizing strategy. The following computations can be easily extended to the case of stochastic interest rates if is assumed to be independent of X. In more general models, the investigation of dependency structures will become inevitable. This goes beyond the scope of the paper and is left to further research.

Due to the representation theorem with respect to Brownian motion, for every and every , there exists some such that

Similarly, because of Assumption 6 , for every and every , , there exists some such that

Theorem7.

Given Assumptions 5 and 6, the unique risk-minimizing hedging strategy , characterized in Theorem B.5 for a general insurance claim , satisfying Assumption 6, is given as

where is the left-inverse of the volatility matrix and is the discounted value process of the cumulative payment process D.

Proof.

Because of Assumption 6, the i-th component of the martingale in Equation (11) is given as

By Assumption 6, Fubini’s theorem and the Itô isometry it then follows for every that

for some constant .

Due to Assumption 6 , we similarly have for every , that

for some constant .

Therefore, we can apply the stochastic version of Fubini’s theorem, see [28], and obtain

This finally implies

The result then follows immediately with Theorem A.7 and the results of Theorem B.5. ☐

3.3. Risk Minimization for General Insurance Contracts with Deterministic Payment Structure under an Affine Specification for the Intensities

In the same setting as in Section 3.2, we now specify the risk-minimizing hedging strategies, computed in Theorem 7 within a general affine setting for the intensities. In addition to Assumption 2 we also consider

Assumption8.

(1)

For every and every , , we assume the entries of the transition matrix are of the form

where are the respective entries of the intensity matrix Ψ.

(2)

For every and every , , is of the form

where , and an -valued affine process as specified e.g., in [29] (Section 3 and Appendix A) or [30]. Here, μ is a Markov process with respect to , given as the strong solution to the SDE

where for , and

with coefficient functions and , taking values in and , respectively.

(3)

The process μ is such that

This particularly implies that for every , , we have

With these assumptions and under some technical conditions, presented in [30], we obtain for every and every with that

Similarly, we obtain for every and every with ,

For every and every combination of , considered in Equations (25)–(28), the functions , solve the ODEs

with terminal conditions and , whereas the functions , solve the ODEs

with terminal conditions and .

The functions , , and , , corresponding to and or to and for as considered in Equations (25)–(28), then solve the ODEs

with terminal conditions , and

with terminal conditions , .

Note that with these specifications, we obtain by Equation (20) that for every and every ,

and

Moreover, as every martingale with respect to the Brownian filtration is continuous, we have for that

and

Hence, for arbitrary , we obtain

where for and every ,

Similarly we get for and every with , that

and

Note that by Jensen’s inequality and Assumption 8 , we get for every and every with that

Finally, with the same limit-arguments as above, we obtain for arbitrary and every with , that

where for , with ,

We can now apply these results to compute explicitly the risk minimizing strategy as given in Theorem 4 and more specifically by Theorem 7 in the Brownian setting in consideration. From Equations (37)–(40) it follows immediately that the processes and , , , of Equations (14) and (15) are given as

Moreover, with Equations (25)–(28) the i-th component , , of in Equation (13) is given as

and can hence be expressed explicitly in terms of μ.

3.4. Application: The Expected Cumulative Payment in an Ornstein-Uhlenbeck Framework

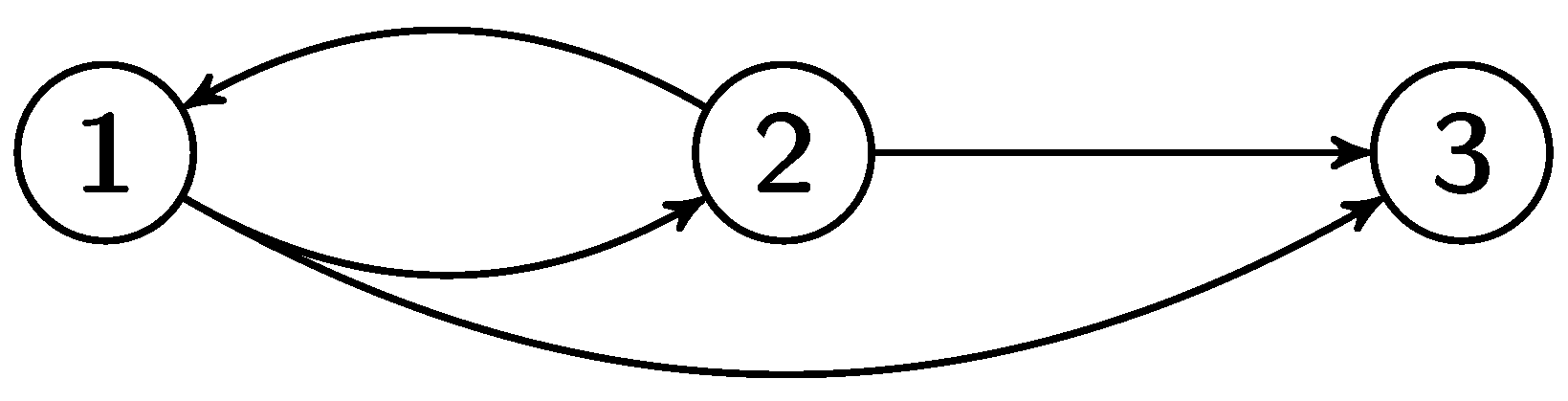

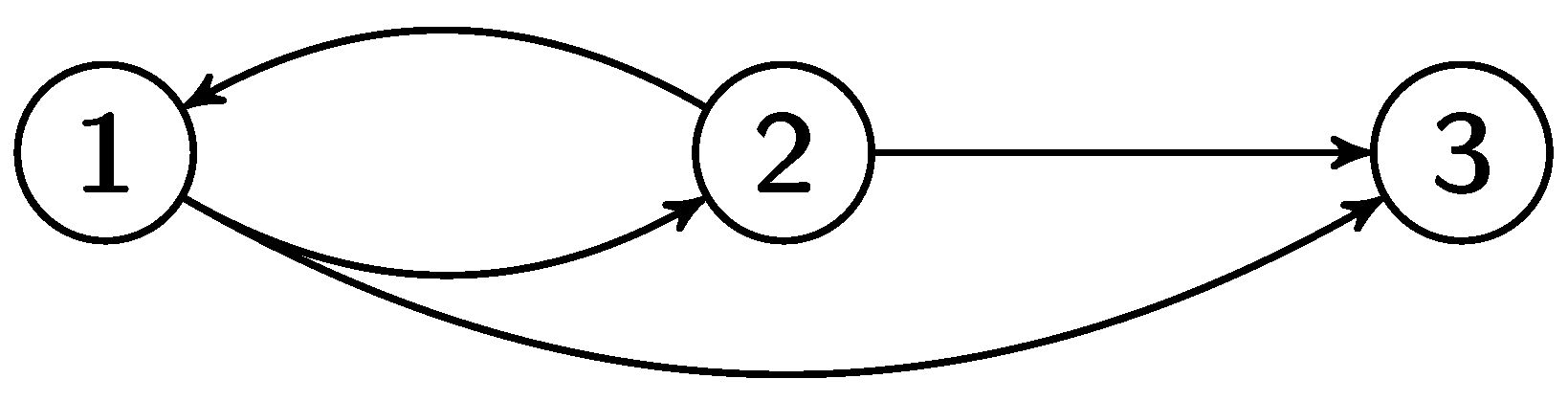

In this section, we illustrate in a specific example how the expected (discounted) cumulative payment from Lemma 3 can be calculated by using the explicit expression of the components from the previous section and the connection established through Equation (9). In the following, we regard a specific insurance product, namely an income protection insurance, and for simplicity we assume that the corresponding process X of the insured person can only take the three states , where state 3 is absorbing. The corresponding transitions are illustrated in Figure 1.

In the following, we assume a specific form for the Markov process μ from Equation (19), namely a simple, 3-dimensional Ornstein-Uhlenbeck (OU) process with corresponding SDE

Note that for the OU process it is well-known that Condition (23) for the expectation is fulfilled. A major drawback, though, of choosing this process for the intensity is the undesirable feature that it can become negative with positive probability. However, [31] provide calibrated parameters for which the probability of negative values for μ turns out to be negligible. For this reason, we choose similar parameter values and set

Hence, Equations (21) and (22) simplify and yield to

with

As a consequence of these assumptions, the ODEs Equations (29)–(36) substantially simplify and can be explicitly solved, see e.g., [32]. For example, for every and every choice of , the ODEs Equations (29) and (30) now are given by

with terminal conditions and . For the k-th components of , i.e., , one obtains the explicit solutions

and

Similarly, the ODEs of the remaining Equations (31)–(36) can be derived.

Next, we need to specify all remaining parameters, i.e., for , the components of the quadruple and the discounting factor . For simplicity, we set with a constant interest rate r and choose

We have chosen the components of to be equal in order to emphasize the general dependence of the process in Equation (19) on and not on the specific linear combination.

Furthermore, similar to Example 2, we set

with and representing the cumulative state-dependent claim payments (e.g., annuities) and insurance premiums up to maturity, respectively, and z the “immediate” claim payment if the insured person dies. More precisely, we assume monthly equal insurance premiums and claim payments equal to 1, if the insured person is in the states 1 (healthy) or 2 (sick/unfit for work), respectively, and which are paid at the end of each month in a proportional way. Let the payment dates denote the final day of each month, i.e., , then we set

with and .

Clearly, with these specifications Assumption 6 is fulfilled. Finally, assuming that the insured persons process X starts in the state 1 (healthy) at , one obtains . Based on the explicit result for from Equation (41), now we are able to calculate the expected (discounted) cumulative payment from Lemma 3 in , depending on the claim payment amount z, which is payed when the insured person dies, and on the constant interest rate r. The corresponding integrals involved in Equation (41) are approximated using the integrate function in the statistical software program R ([33]).

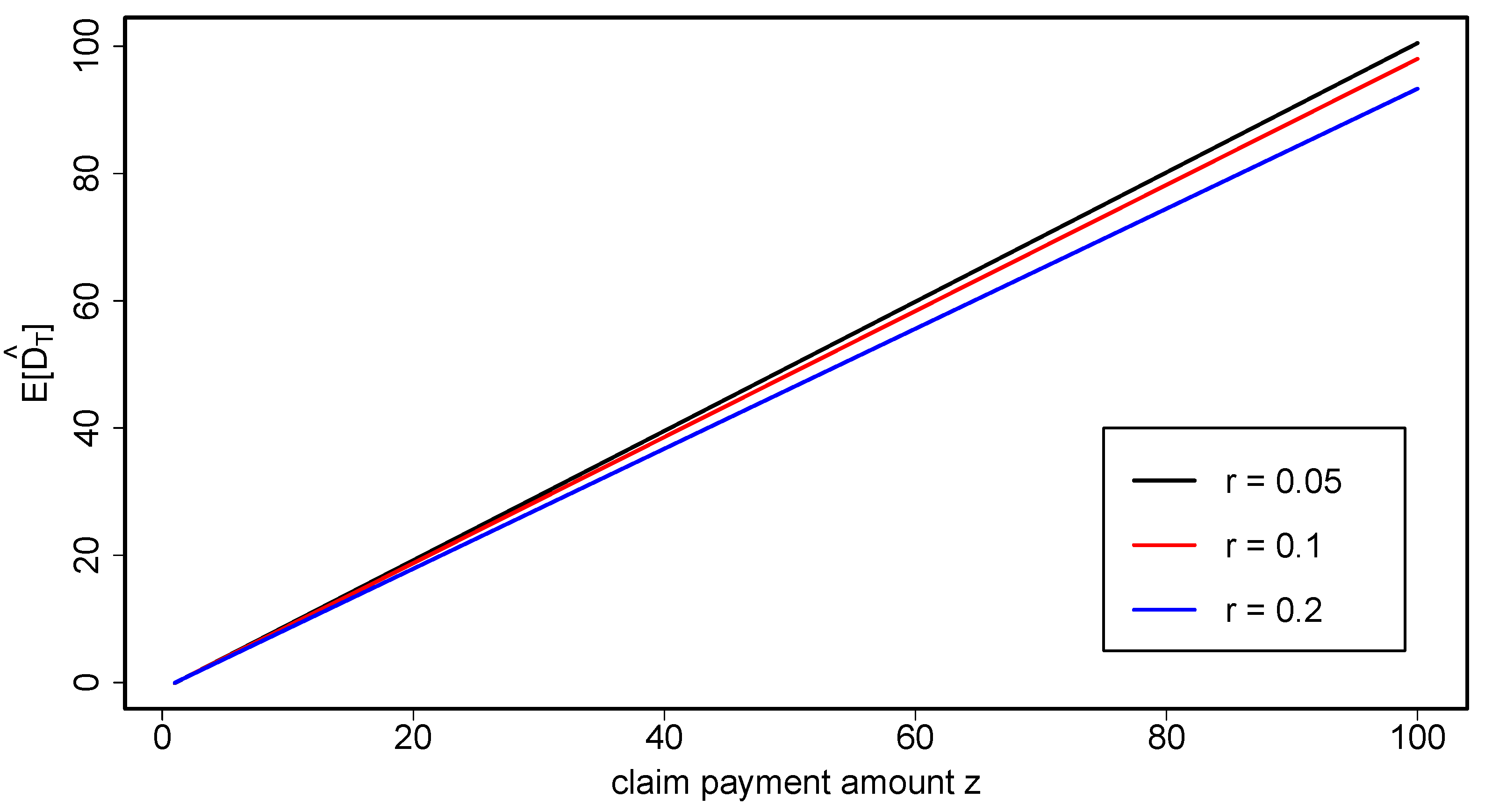

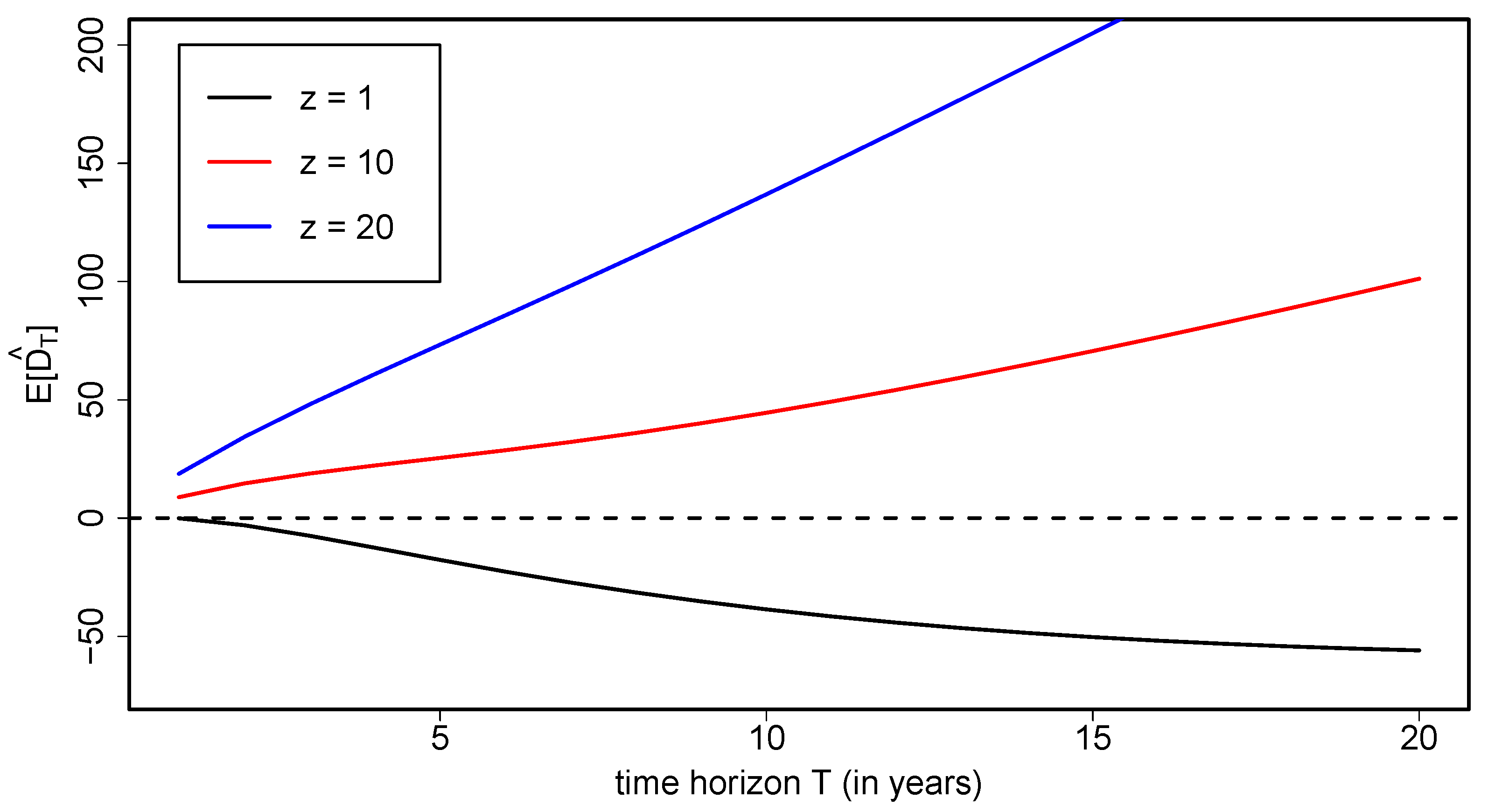

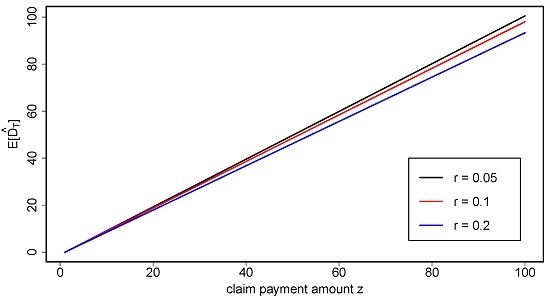

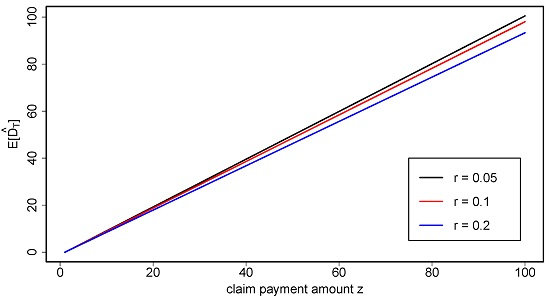

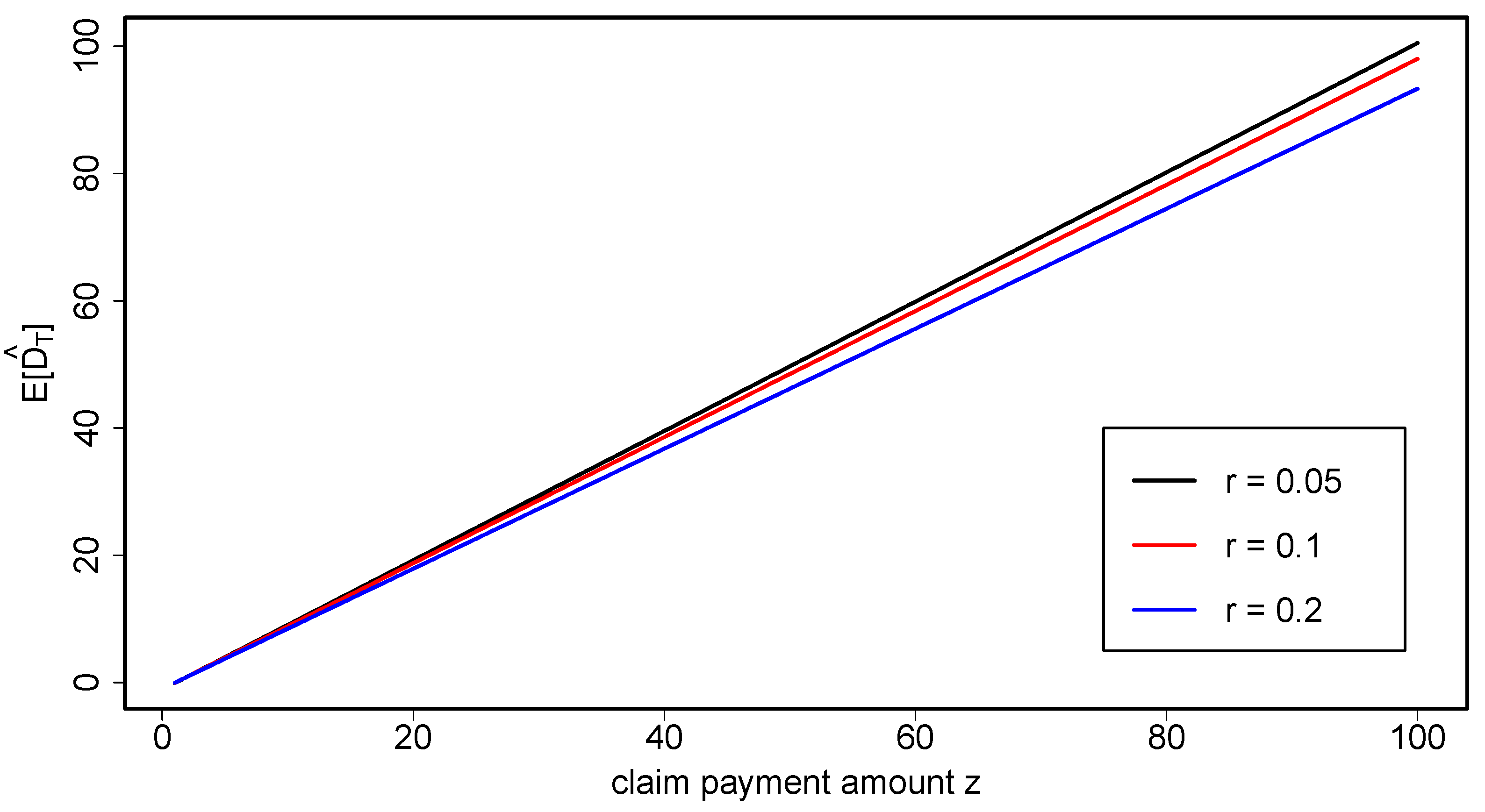

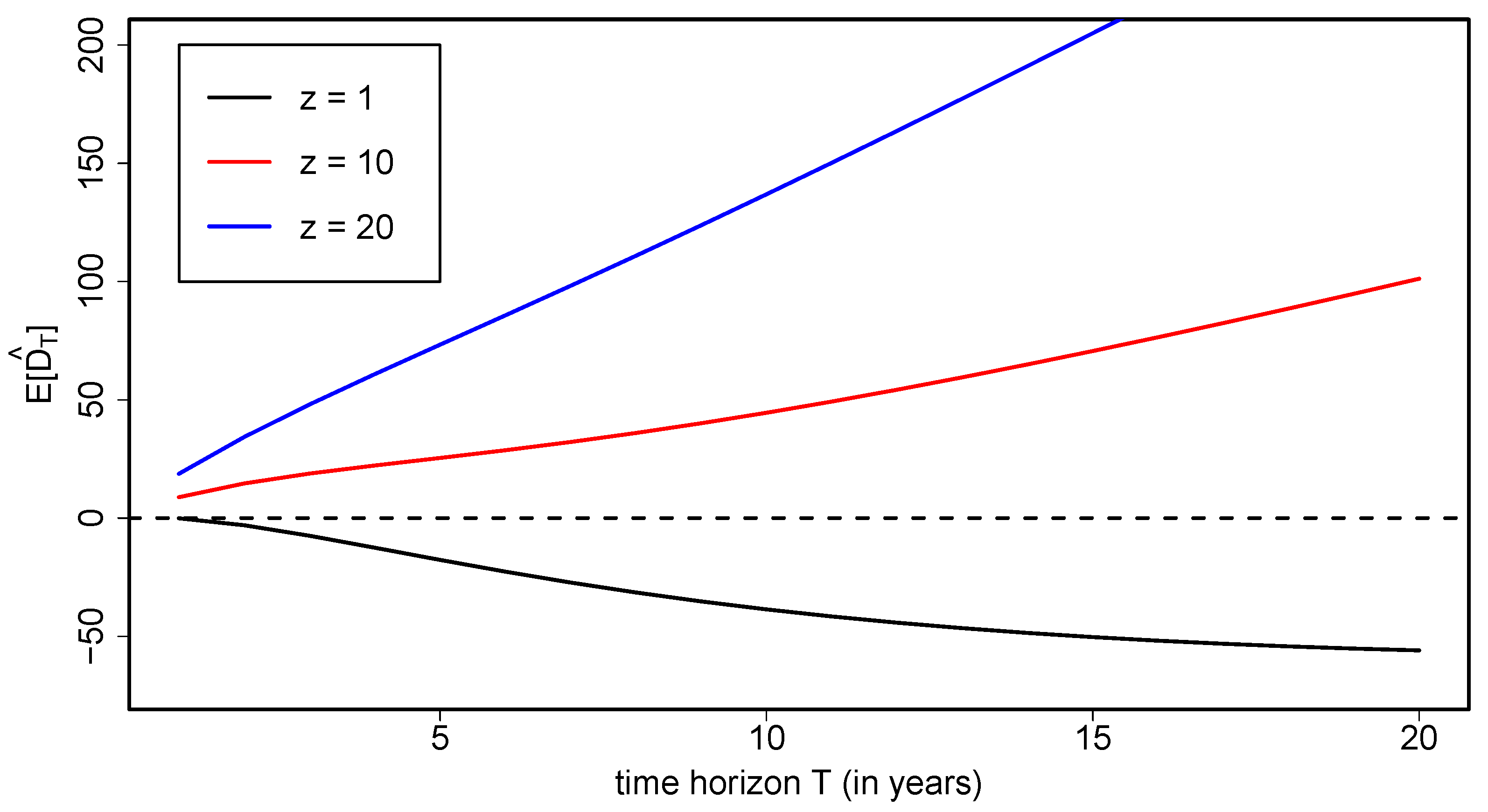

Figure 2 illustrates the expected cumulative payment as a function of the claim payment amount z, a time horizon of one year () and three different values of the constant interest rate r. In Figure 3, the expected cumulative payment are displayed against the time horizon T, for three different values of the claim payment amount z and for a constant interest rate .

4. Conclusions

In this paper, we consider pricing and hedging of general insurance contracts by means of risk minimization. We model the individual progress in time of visiting an insurance policy’s states by using -doubly stochastic Markov chains. In this way we are able to consider a multi-state setting to describe different types of insurance benefits and to include the influence of market conditions and external risk factors on the evolution of the insured person among the policy’s states as well as on the insurance benefits, when they are linked to some financial performance. We explicitly provide the risk-minimizing strategy for an insurance contract in a Brownian financial market setting and specify it within an affine structure for the intensity. The results are illustrated by a numerical example, which shows how this technical setting can actually be easily implemented.

Acknowledgments

The research leading to these results has received funding from the European Research Council under the European Community’s Seventh Framework Programme (FP7/2007-2013)/ERC grant agreement No [228087].

Author Contributions

All authors have contributed equally to all aspects of this paper.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. -Doubly Stochastic Markov Chains

In this section we introduce briefly to some basic properties of -doubly stochastic Markov chains, which we are going to use in the sequel. Main references are [12,21].

On a probability space , let be a right-continuous stochastic process with state space . We denote by the filtration generated by X, i.e., for all , and consider the filtration to be the enlargement of through some reference filtration , i.e., we assume for all . Further, we set , and assume that all filtrations satisfy the usual conditions of completeness and right-continuity, see [28].

DefinitionA.1.

A process is called an -doubly stochastic Markov chain with state space , if there exists a family of stochastic matrices

such that

(1)

the matrix is -measurable, and is progressively measurable,

(2)

for every we have

The process is called the conditional transition probability process of X.

By Definition A.1. we can see that the class of -doubly stochastic Markov chains contains Markov chains, compound Poisson processes with integer-valued jumps, Cox processes as in [34] and processes of rating migration as in [35]. The adjective “double” refers to the fact that there are two sources of uncertainty in their definition. We remark that an -doubly stochastic Markov chain is a different object than a doubly stochastic Markov chain which is a Markov chain with a doubly stochastic transition matrix. Furthermore, in [12] it is shown that -doubly stochastic Markov chains are a subclass of -conditional Markov chains. In particular, -doubly stochastic Markov chains behave like time inhomogeneous Markov chains conditioned on , i.e., if we know all the information concerning the underlying risk factors.

DefinitionA.2.

We say that a state is an absorbing state, if for all and all with .

PropositionA.3.

Let X be an -doubly stochastic Markov chain with transition matrices , then for every we have

PropositionA.4.

If X is an -doubly stochastic Markov chain, then for every bounded, -measurable random variable Y and for each , we have

Property Equation (A3) is well-known in the context of survival analysis and credit risk as hypothesis (H) or immersion property. According to Proposition A.4, -martingales remain martingales with respect to the enlarged filtration . If we think of a martingale as a process describing a fair game, this property means that the additional information contained in does not change the valuation of processes which are considered fair by taking in account only the information .

Another property, which makes the class of -doubly stochastic Markov chains interesting for applications is that they may admit matrix-valued stochastic intensity processes in the following sense.

DefinitionA.5.

An -doubly stochastic Markov chain X with state space is said to have an intensity, if there exists an -adapted matrix-valued stochastic process with such that

(1)

Ψ is integrable, i.e.,

(2)

Ψ satisfies the following conditions:

A processΨ, satisfying the above conditions, is called an intensity of the -doubly stochastic Markov chain X.

TheoremA6.

Let be an -adapted matrix-valued stochastic process, satisfying the Conditions (A4) and (A5) of Definition A.5. Then there exists an -doubly stochastic Markov chain X with intensity .

For , let

be the indicator function for X, being in state j at time t and denote by the corresponding N-variate vector. Moreover, for , , let with

define the counting processes of the jumps of X from state j to k up to time t, .

The following theorem provides a martingale characterization of -doubly stochastic Markov chains and is the core connection of the theory of -doubly stochastic Markov chains and the counting process theory, underlying for example several estimation schemes for intensity processes, see [13].

TheoremA.7.

Let be a stochastic process with state space and be a matrix-valued process, satisfying Equations (A4) and (A5) of Definition A.5. The following conditions are equivalent:

(i)

X is an -doubly stochastic Markov chain.

(ii)

The process with

is a -local martingale.

(iii)

For , , the processes with

are -local martingales.

(iv)

The process with

is a -local martingale. Here is a unique solution to the random integral equation

Note that then

RemarkA.1

(1)

For every , the matrix is the unique inverse matrix of . More generally, for , we denote by the unique inverse matrix of . The existence and further properties of the family is given in [12].

It follows immediately from Equation (A2) that for every , we have

(2)

As the processes , and , , , are -adapted, they are also -local martingales.

CorollaryA.8.

For every , , and for every we have

Moreover, with , , we have

Proof.

Equalities (A14) and (A15) follow directly by the definition of in Equation (A10).

Moreover, we observe that is a continuous finite variation process. It follows that

as counts the jumps of X into and out of the state j up to time t. As is the compensator of it follows that

where the last equality follows from Equation (A5). This ends the proof. ☐

PropositionA.9.

Let X be an -doubly stochastic Markov chain with intensity and jump times and

Then every jump time , , avoids -stopping times, i.e., for every -stopping time ϱ, provided that a.s..

The following proposition is the crucial result in order to compute the risk-minimizing strategies for general insurance claims which we provide in Section 3.

PropositionA.10.

Let X be an -doubly stochastic Markov chain. Then the local martingale , given in Equation (A9), is orthogonal to every -local martingale N, in the sense that for each , the product is a -local martingale.

Proof.

First note that is a finite variation local martingale. Its sequence of jump times with and

is a subsequence of the jump times of X, as given by Equation (A17). As the jump times of the càdlàg local martingale N are -stopping times, the processes and N have almost surely no common jumps due to Proposition A.9.

This implies that for all we have

and ends the proof. ☐

RemarkA.2.

It is easily seen that hazard-rate models, as applied frequently in the context of credit risk or life insurance, are particular examples of -doubly stochastic Markov chains, provided they satisfy hypothesis (H). A thorough description of this relation is given in [24].

Appendix B. Risk-Minimization for Payment Processes

The following survey of risk-minimization for payment processes is borrowed to some extend from [1], as well as [22]. As in the foregoing sections, we provide the results with respect to a general numéraire process such that one could also consider e.g., the -numéraire portfolio as discount factor, see [25]. The results base on the proofs, given in [4] for the case of European type contingent claims and in [5,36,37] (Chapter 4) for the case of payment processes.

In the market model, defined in Section 3.2, we would like to find a hedging strategy for a -adapted, square integrable payment process representing the cumulative discounted payments up to time .

Note that if an undiscounted cumulative payment stream is a stochastic process of finite variation and we have with denoting the absolute variation process of D, then is given as

DefinitionB.1.

If , then the value process of a payment process D is defined as

Since the market is not necessarily complete, it is in general not possible to find a self-financing hedging strategy that perfectly replicates the discounted cumulative payment process . In this context, the idea of risk-minimization is to relax the self-financing assumption, allowing for a wider class of admissible strategies, and to find an optimal hedging strategy with “minimal risk” within this class of strategies that perfectly replicate .

For the local martingale , we denote

It is well known that for every , the process is a square integrable martingale.

In the following we now explain how to find the risk-minimizing strategy and explain in what sense this strategy is optimal. We begin with some definitions.

DefinitionB.2.

An-strategy is a pair such that and is a real-valued -adapted process, such that the discounted portfolio value process

is right-continuous and square integrable.

For an -strategy the discounted (cumulative) cost process is defined as

describing the accumulated costs of the trading strategy during , including the payments . Note that should therefore be interpreted as the discounted value of the portfolio held at time t after the payments have been made. In particular, is the discounted value of the portfolio upon settlement of all liabilities, and a natural condition is then to restrict to 0-admissible strategies, satisfying

The risk process of is given by the conditional expected value of the squared future costs

and is taken as a measure of the hedger’s remaining risk. We would like to find a trading strategy that minimizes the risk in the following sense.

DefinitionB.3.

An -strategy is called risk-minimizing for the discounted payment process , if for any -strategy such that -a.s., we have

i.e., minimizes pointwise the risk process introduced in Equation (B4).

The key to finding the strategy with minimal risk in our setting is the so-called Galtchouk-Kunita-Watana decomposition.

DefinitionB.4.

Given a square integrable martingale and the local martingale , the Galtchouk-Kunita-Watanabe decomposition for with respect to is given as

where and is a square integrable martingale null at 0 which is strongly orthogonal to the space of all integral processes with .

It is well known that the set is a closed stable subset of , the set of all square integrable martingales, zero at 0.

Due to Jensen’s inequality and the fact that is square-integrable, the discounted value process is a square-integrable martingale and may be decomposed according to Equation (B5).

TheoremB.5.

For every (discounted) square integrable payment stream , there exists a unique 0-admissible risk-minimizing -strategy , given by

with discounted portfolio value process

discounted optimal cost process

and minimal risk process

where and are given by Equation (B5) for the square integrable martingale .

Proof.

See [26] for the single payoff case or [5,36] for the extension to the case of payment streams. ☐

Note that the approach, described above, relies heavily on the fact that the discounted asset prices are local martingales under the measure . In a more general setting, when the vector of discounted asset is a semimartingale under , one has to apply the local risk-minimization technique, see [36] or [37] (Chapter 4). For more information on (local) risk-minimization and other quadratic hedging approaches we refer to the survey paper of [26].

1.For the definition and further comments on hypothesis (H), see Proposition A.4 and the text below.

References

F. Biagini, and I. Schreiber. “Risk minimization for life insurance liabilities.” SIAM J. Financ. Math. 4 (2013): 243–264. [Google Scholar] [CrossRef]

F. Biagini, T. Rheinländer, and J. Widenmann. “Hedging mortality claims with longevity bonds.” ASTIN Bull. 43 (2013): 123–157. [Google Scholar] [CrossRef]

D. Blake, A.J.G. Cairns, and K. Dowd. “The birth of the life market.” Asia-Pac. J. Risk Insur. 3 (2008): 6–36. [Google Scholar] [CrossRef]

H. Föllmer, and D. Sondermann. “Hedging of non-redundant contingent claims.” In Contributions to Mathematical Economics. Edited by A. Mas-Colell and W. Hildenbrand. Haarlem, The Netherlands: North Holland, 1986, pp. 205–223. [Google Scholar]

T. Møller. “Risk-Minimizing Hedging Strategies for Insurance Payment Processes.” Finance Stoch. 5 (2001): 419–446. [Google Scholar] [CrossRef]

J.P. Ansel, and C. Stricker. “Décomposition de Kunita-Watanabe.” In Séminaire de Probabilités XXVII. Lecture Notes in Mathematics Volume 1557; Berlin, Germany: Springer, 1993. [Google Scholar]

H. Kunita, and S. Watanabe. “On square integrable martingales.” Nagoya Math. J. 30 (1967): 209–245. [Google Scholar]

J. Hoem. “Markov Chain Models in Life Insurance.” In Blätter der Deutschen Gesellschaft für Versicherungs- und Finanzmathematik. Berlin, Germany: Springer, 1969, Volume 9, pp. 91–107. [Google Scholar]

R. Norberg. “Hattendorff’s theorem and Thiele’s differential equation generalized.” Scand. Actuar. J. 1 (1992): 2–14. [Google Scholar] [CrossRef]

R. Norberg. “A Theory of Bonus in Life Insurance.” Finance Stoch. 3 (1999): 373–390. [Google Scholar] [CrossRef]

R. Norberg. “Optimal hedging of demographic risk in life insurance.” Finance Stoch. 17 (2013): 197–222. [Google Scholar] [CrossRef]

J. Jakubowski, and M. Niewęgłowski. “A class of F-doubly stochastic Markov chains.” Electron. J. Probab. 15 (2010): 1743–1771. [Google Scholar] [CrossRef]

F. Biagini, A. Groll, and J. Widenmann. “Intensity-based premium evaluation for unemployment insurance products.” Insur.: Math. Econ. 53 (2013): 302–316. [Google Scholar] [CrossRef]

J. Barbarin. “Heath-Jarrow-Morton modelling of longevity bonds and the risk minimization of life insurance portfolios.” Insur.: Math. Econ. 43 (2008): 41–55. [Google Scholar] [CrossRef]

F. Biagini, and A. Cretarola. “Quadratic Hedging Methods for Defaultable Claims.” Appl. Math. Optim. 56 (2007): 425–443. [Google Scholar] [CrossRef]

F. Biagini, and A. Cretarola. “Local Risk-Minimization for Defaultable Markets.” Math. Financ. 19 (2009): 669–689. [Google Scholar] [CrossRef]

F. Biagini, and A. Cretarola. “Local Risk-Minimization for defaultable claims with recovery process.” Appl. Math. Optim. 65 (2012): 293–314. [Google Scholar] [CrossRef]

F. Biagini, T. Rheinländer, and I. Schreiber. “Risk-minimization for life insurance liabilities with basis risk.” Math. Financ. Econ. 10 (2016): 151–178. [Google Scholar] [CrossRef]

F. Biagini, C. Botero, and I. Schreiber. “Risk-minimization for life insurance liabilities with dependent mortality risk.” Math. Finance, 2015. [Google Scholar] [CrossRef]

T.R. Bielecki, M. Jeanblanc, and M. Rutkowski. “Pricing and trading credit default swaps in a hazard process model.” Ann. Appl. Probab. 18 (2008): 2495–2529. [Google Scholar] [CrossRef]

J. Jakubowski, and M. Niewęgłowski. “Pricing and Hedging of Rating-Sensitive Claims Modeled by -doubly stochastic Markov chains.” In Advanced Mathematical Methods for Finance. Edited by G. DiNunno and B.O. Ksendal. Berlin, Germany: Springer, 2011, pp. 417–454. [Google Scholar]

F. Biagini, A. Cretarola, and E. Platen. “Local risk-minimization under the benchmark approach.” Math. Financ. Econ. 8 (2014): 109–134. [Google Scholar] [CrossRef]

F. Biagini. “Evaluating hybrid products: The interplay between financial and insurance markets.” In Seminar on Stochastic Analysis, Random Fields and Applications VII, Centro Stefano Franscini, Ascona, May 2011. Edited by R. Dalang, M. Dozzi and F. Russo. Basel, Switzerland: Springer & Birkhäuser, 2013, pp. 285–304. [Google Scholar]

J. Widenmann. “Pricing and Hedging Insurance Contracts in Hybrid Markets.” Ph.D. Thesis, Ludwig Maximilians University Munich, Munich, Germany, 2013. [Google Scholar]

E. Platen, and D. Heath. A Benchmark Approach to Quantitative Finance. Berlin, Germany: Springer, 2007. [Google Scholar]

M. Schweizer. “A guided tour through quadratic hedging approaches.” In Option Pricing, Interest Rates and Risk Management. Edited by E. Jouini, J. Cvitanic and M. Musiela. Cambridge, UK: Cambridge University Press, 2001, pp. 538–574. [Google Scholar]

L.F.B. Henriksen, and T. Møller. “Local risk-minimization with survivor bonds.” Appl. Stoch. Models Bus. Ind. 31 (2015): 241–263. [Google Scholar] [CrossRef]

P.E. Protter. Stochastic Integration and Differential Equations, 2nd ed. New York, NY, USA: Springer, 2005. [Google Scholar]

E. Biffis. “Affine processes for dynamic mortality and actuarial valuation.” Insur.: Math. Econ. 37 (2005): 443–468. [Google Scholar] [CrossRef]

D. Duffie, J. Pan, and K. Singleton. “Transform analysis and asset pricing for affine jump-diffusions.” Econometrica 68 (2000): 1343–1376. [Google Scholar] [CrossRef]

E. Luciano, and E. Vigna. “Mortality Risk via affine stochastic intensities: Calibration and empirical relevance.” Belg. Actuar. Bull. 8 (2008): 5–16. [Google Scholar]

D. Filipović. Term-Structure Models. Berlin, Germany: Springer, 2009. [Google Scholar]

R.C. Team. R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing, 2015. [Google Scholar]

D. Lando. “On Cox processes and credit risk securities.” Rev. Deriv. Res. 2 (1998): 99–120. [Google Scholar] [CrossRef]

T. Bielecki, and M. Rutkowski. Credit Risk: Modelling, Valuation and Hedging, 2nd ed. Berlin, Germany: Springer-Finance, Springer, 2004. [Google Scholar]

M. Schweizer. “Local Risk-Minimization for Multidimensional Assets and Payment Streams.” Warszawa, Poland: Banach Center Publications, 2008, Volume 83, pp. 213–229. [Google Scholar]

J. Barbarin. “Valuation, Hedging and the Risk Management of Insurance Contracts.” Ph.D. Thesis, Université Catholique de Louvain, Louvain, Belgium, 2008. [Google Scholar]

Figure 1.

Possible transitions for an insured person’s process in an income protection insurance with the three states with absorbing state 3.

Figure 1.

Possible transitions for an insured person’s process in an income protection insurance with the three states with absorbing state 3.

Figure 2.

Expected (discounted) cumulative payments as a function of the claim payment amount z and for three different constant interest rate values r for a time horizon of one year, i.e., .

Figure 2.

Expected (discounted) cumulative payments as a function of the claim payment amount z and for three different constant interest rate values r for a time horizon of one year, i.e., .

Figure 3.

Expected (discounted) cumulative payments as a function of the time horizon T (in years) and three different claim payment amounts z and for a constant interest rate .

Figure 3.

Expected (discounted) cumulative payments as a function of the time horizon T (in years) and three different claim payment amounts z and for a constant interest rate .

Biagini, F.; Groll, A.; Widenmann, J.

Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks2016, 4, 23.

https://doi.org/10.3390/risks4030023

AMA Style

Biagini F, Groll A, Widenmann J.

Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks. 2016; 4(3):23.

https://doi.org/10.3390/risks4030023

Chicago/Turabian Style

Biagini, Francesca, Andreas Groll, and Jan Widenmann.

2016. "Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains" Risks 4, no. 3: 23.

https://doi.org/10.3390/risks4030023

APA Style

Biagini, F., Groll, A., & Widenmann, J.

(2016). Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks, 4(3), 23.

https://doi.org/10.3390/risks4030023

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.

Article Metrics

No

No

Article Access Statistics

For more information on the journal statistics, click here.

Multiple requests from the same IP address are counted as one view.

Biagini, F.; Groll, A.; Widenmann, J.

Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks2016, 4, 23.

https://doi.org/10.3390/risks4030023

AMA Style

Biagini F, Groll A, Widenmann J.

Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks. 2016; 4(3):23.

https://doi.org/10.3390/risks4030023

Chicago/Turabian Style

Biagini, Francesca, Andreas Groll, and Jan Widenmann.

2016. "Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains" Risks 4, no. 3: 23.

https://doi.org/10.3390/risks4030023

APA Style

Biagini, F., Groll, A., & Widenmann, J.

(2016). Risk Minimization for Insurance Products via F-Doubly Stochastic Markov Chains. Risks, 4(3), 23.

https://doi.org/10.3390/risks4030023

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}