Climate Change-Related Disaster Risk Mitigation through Innovative Insurance Mechanism: A System Dynamics Model Application for a Case Study in Latvia

, ,

, ,

Abstract

1. Introduction

1.1. Climate Change and Natural Disasters

1.2. Role of Insurance Sector in Mitigating and Adapting to Climate Change-Related Risks

1.3. Aim of the Paper

2. Methodology

- Stocks and flows: stocks represent accumulations of resources or quantities within the system (e.g., inventory, population), while flows represent the rates at which these resources move between stocks.

- Feedback loops: feedback loops occur when the output of a system component influences its own behavior or that of other components in the system. There are two types of feedback loops: positive feedback loops, which amplify changes in the system, and negative feedback loops, which tend to stabilize the system.

- Delays: delays in system dynamics refer to the time it takes for an action or change in one part of the system to have an effect on other parts. Delays can lead to oscillations or non-intuitive behaviors in the system.

- Causal Loop Diagrams: causal loop diagrams are graphical representations used to visualize the relationships between the variables in a system and the direction of influence. They help identify feedback loops and understand the underlying dynamics.

- Simulation: SD models are typically implemented using computer simulation software. These models allow analysts to experiment with different scenarios and policies to help them understand how the system responds to changes over time.

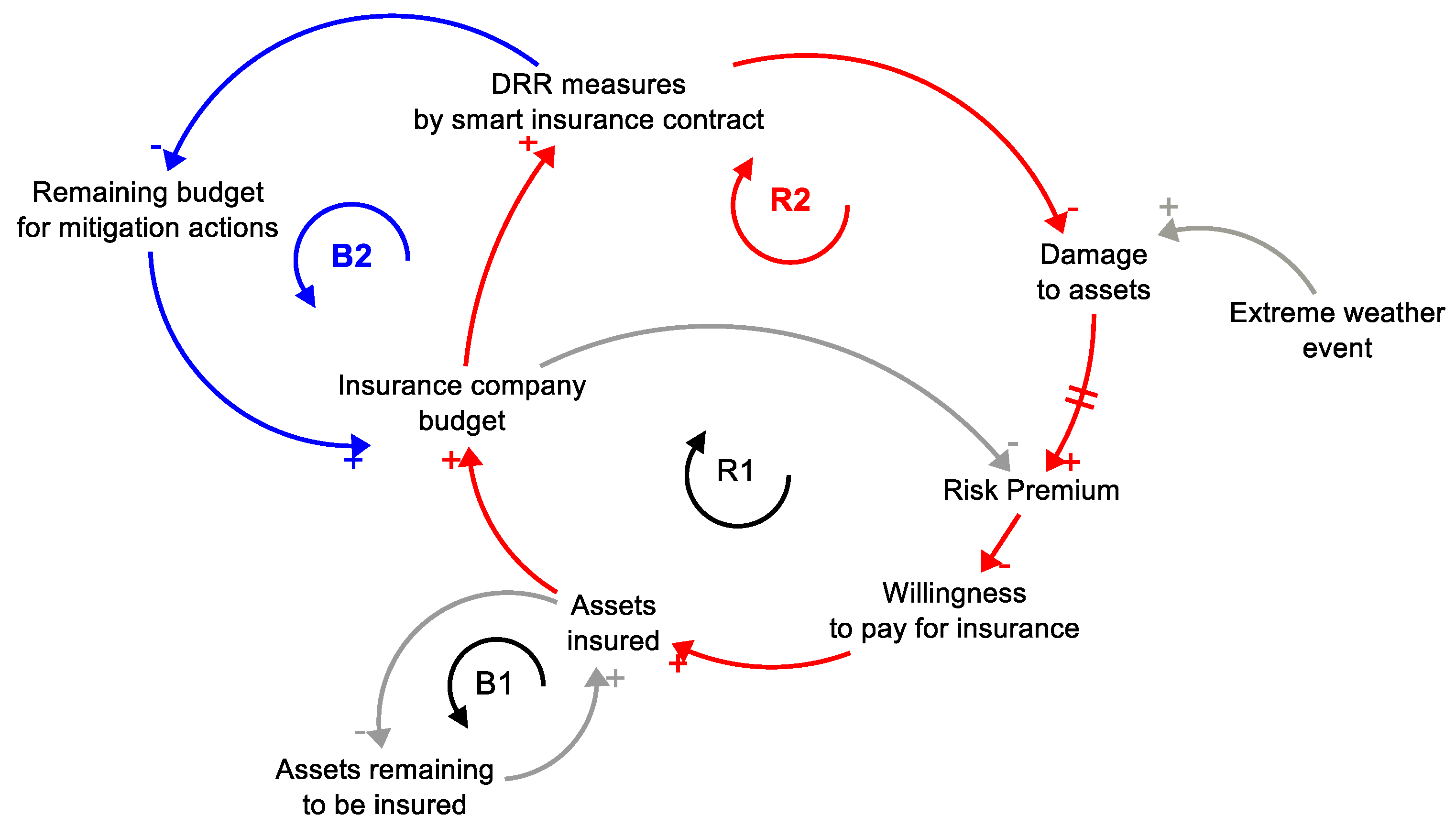

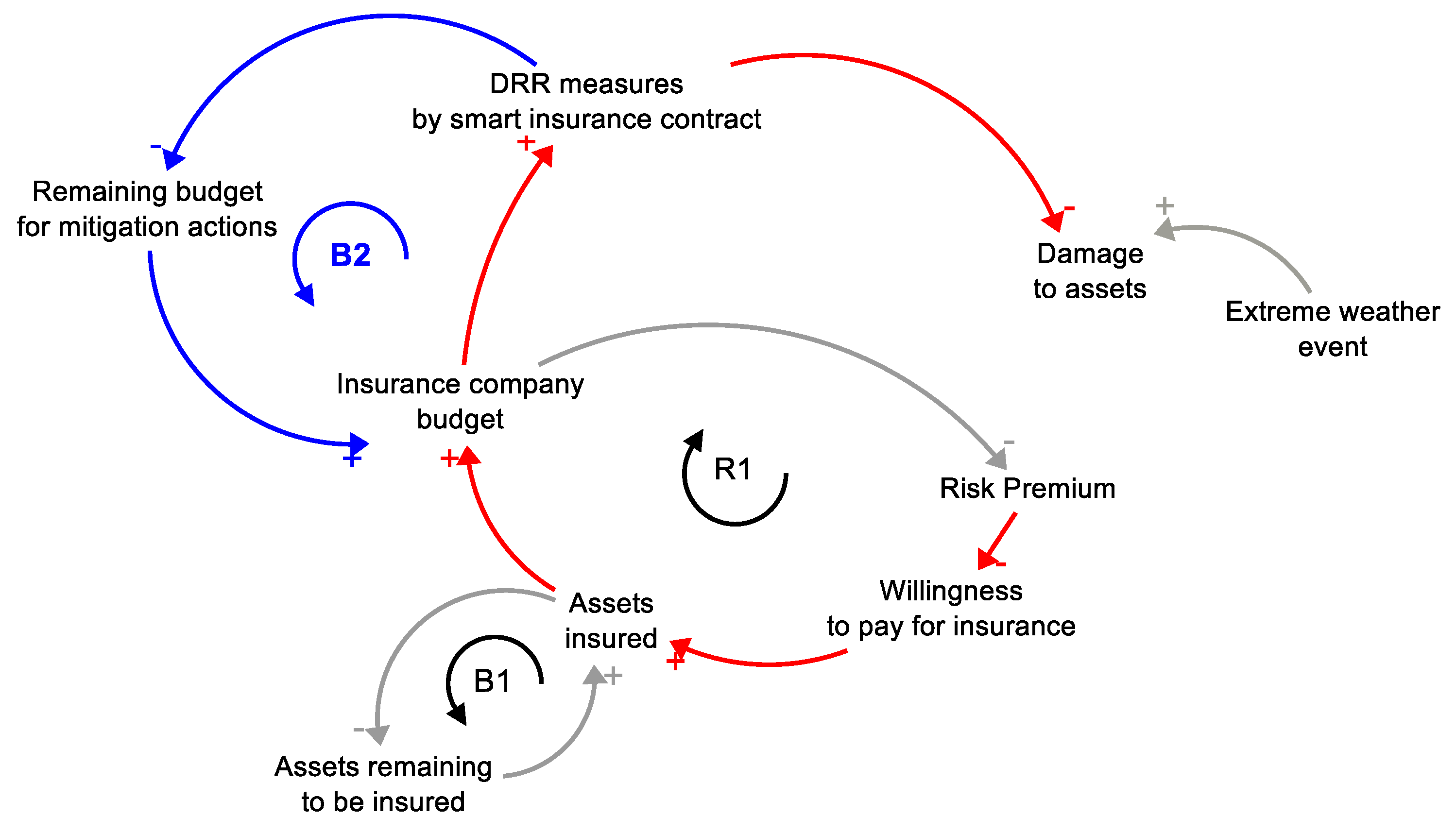

2.1. System Dynamics: Building Causal Loops Diagrams

- Reinforcing loops amplify changes within a system and may cause exponential growth or decline. They are marked with the letter R in CLD. Reinforcing loops embedded in the system are often the cause of the problematic behavior.

- Balancing loops have the opposite of the reinforcing loops. Balancing loops tend to restore equilibrium or maintain stability within a system due to their counter-interaction with the effect of the changes of the initial variable in the loop. Balancing loops are marked with the letter B in CLD.

2.2. Setting up System Dynamics Stock and Flow Model

- (i)

- stocks, which accumulate or deplete over time, and by

- (ii)

- flows, which represent the rate at which variables enter or exit a stock.

2.3. Defining a Case Study

- RP—Risk Premium,

- Laverage—loss associated with the average yearly loss per asset in the area subjected to disaster,

- σ—volatility of yearly loss per asset in the area subjected to disaster,P—premium charge in %.

- (1)

- Scenario 1—Business as usual (BAU)—conventional insurance mechanism;

- (2)

- Scenario 2—Investment in disaster risk reduction—the insurance with bond for DRR measures without fixed premium;

- (3)

- Scenario 3—Smart contract approach—the proposed smart contract insurance scheme with investment in disaster risk reduction (DRR) and fixed premium.

2.4. Model Testing and Validation

2.4.1. Content Validation Procedure

2.4.2. Extreme Value Test

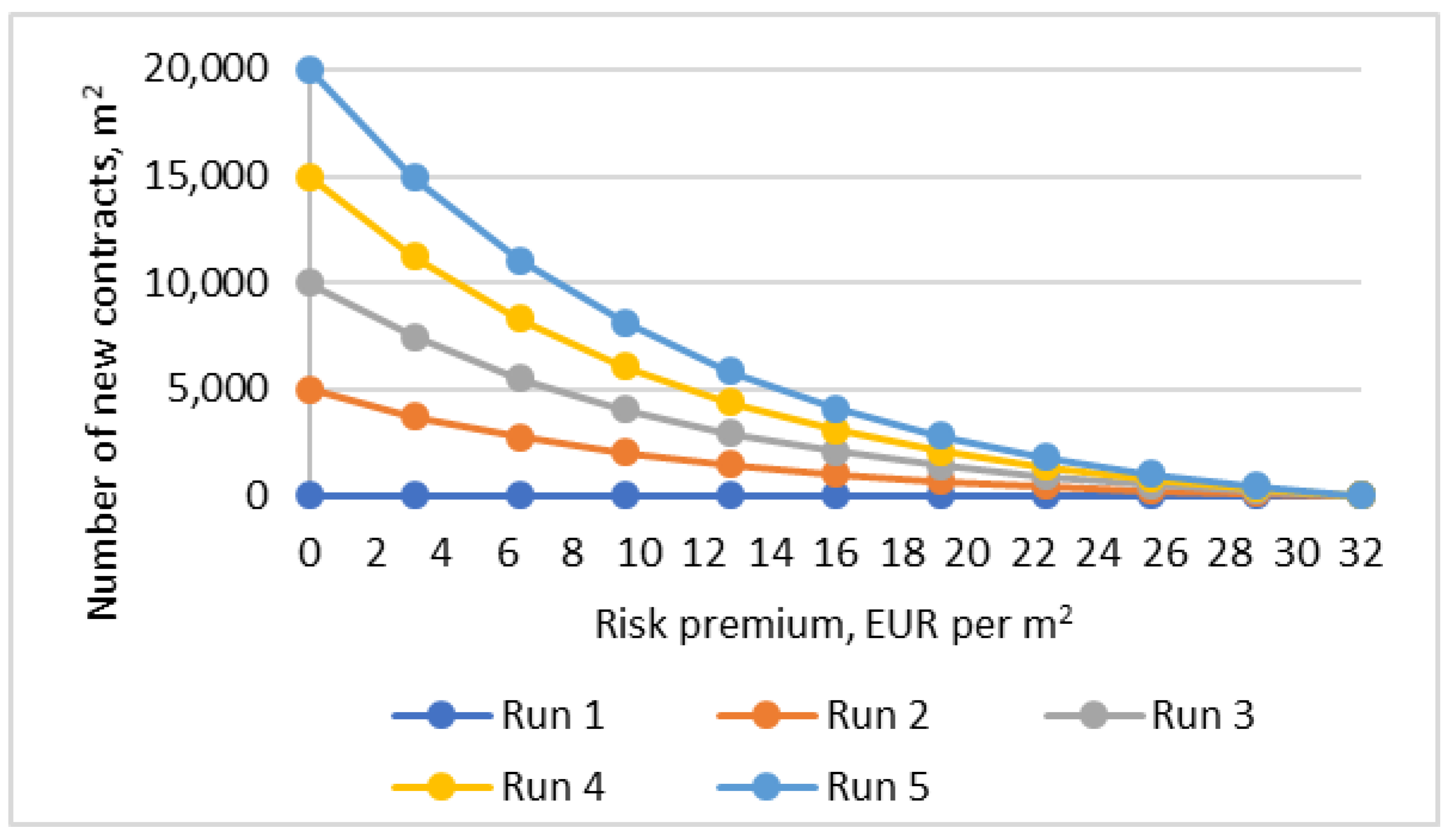

2.4.3. Sensitivity Analysis

3. Results and Discussion

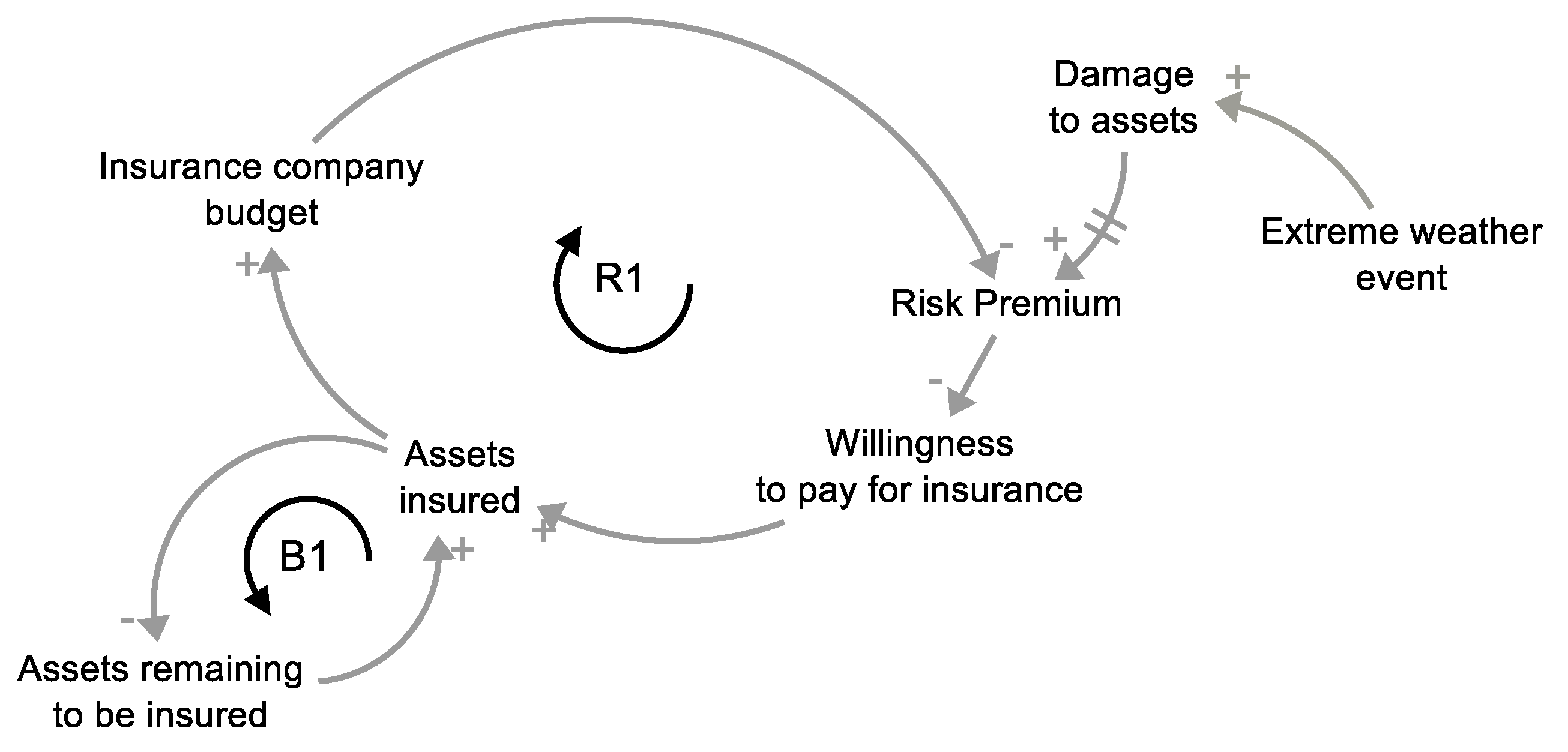

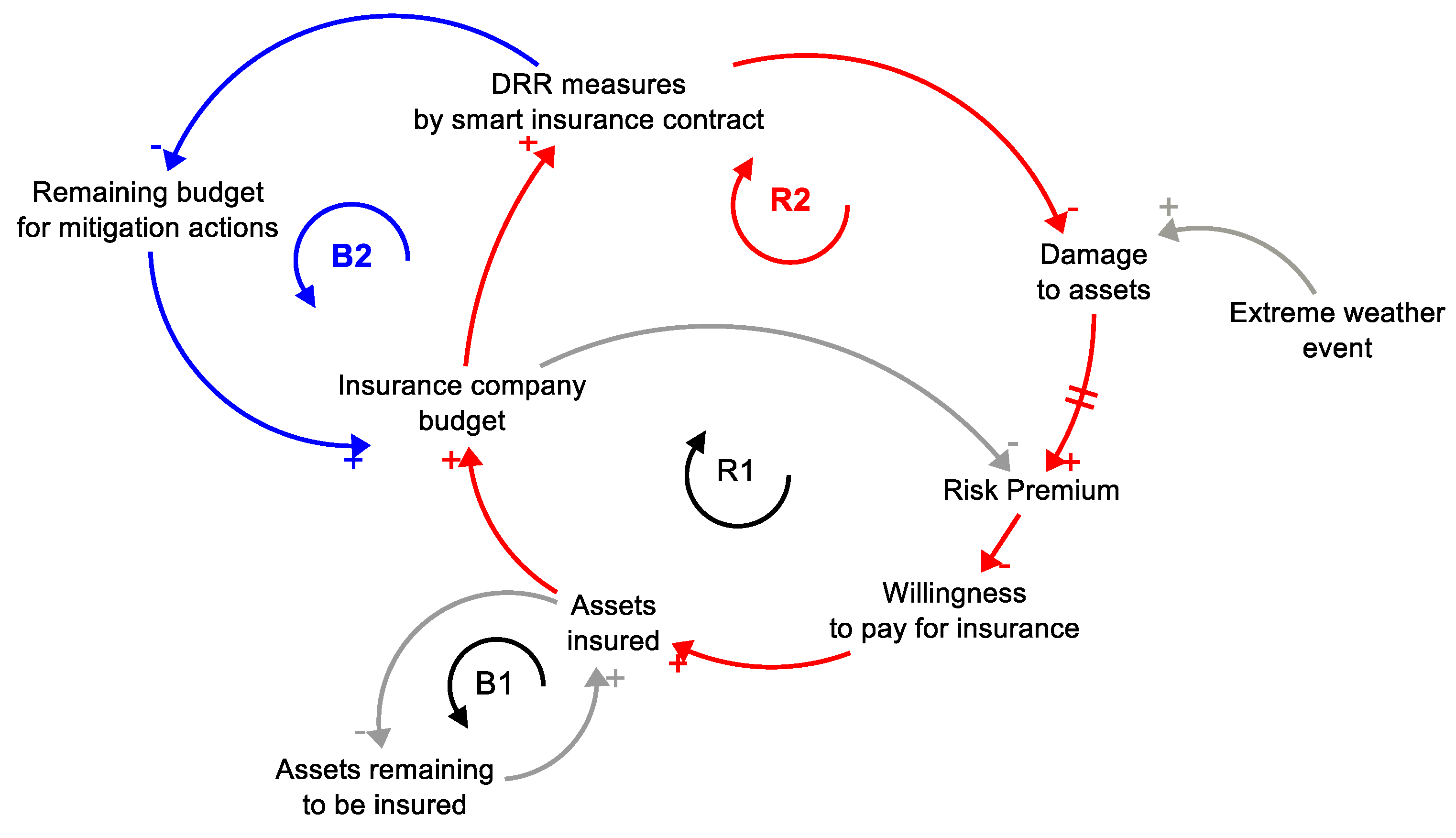

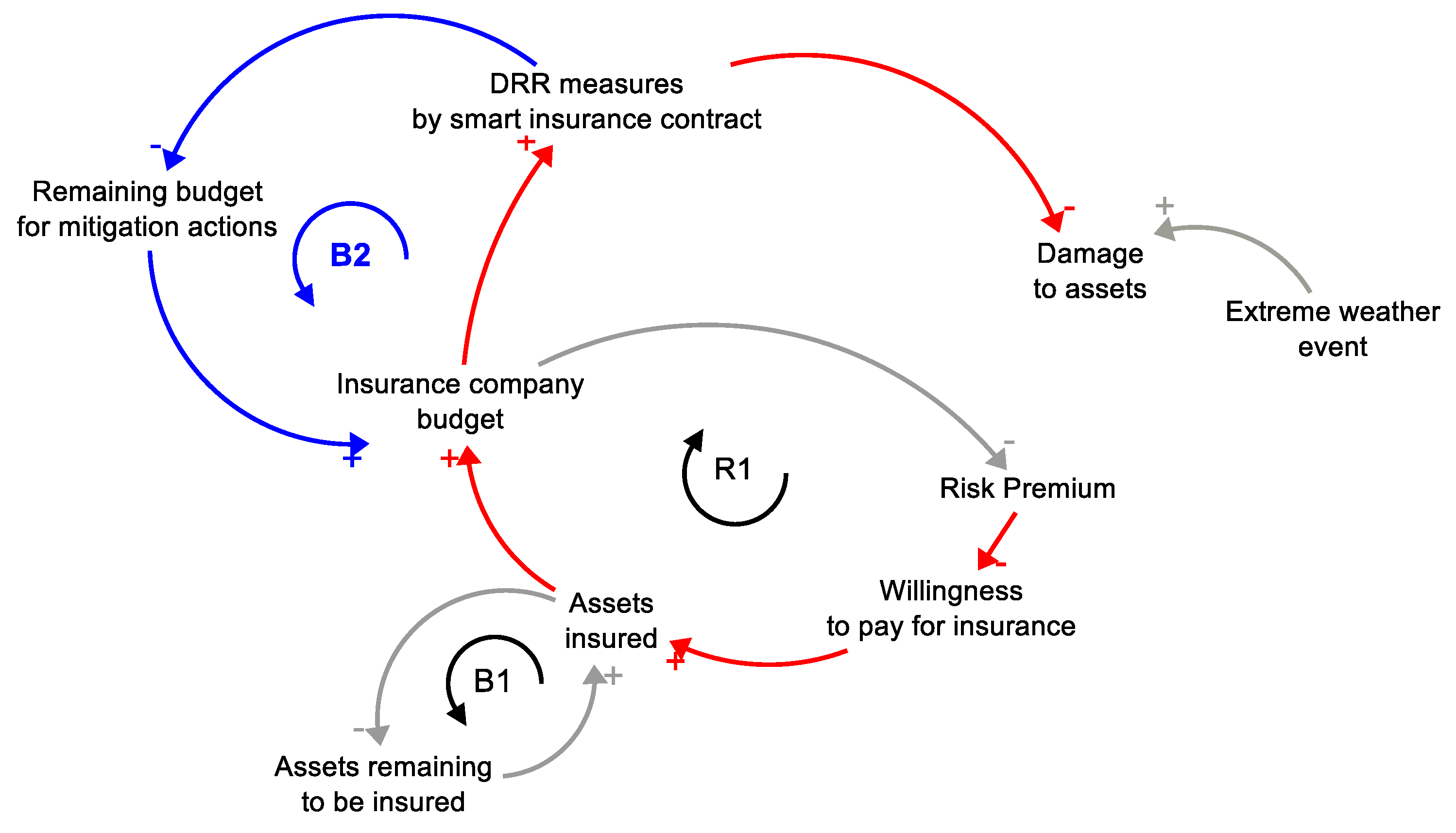

3.1. Causal Loop Diagrams of the Developed Model

3.2. Empirical Model Testing and Validation

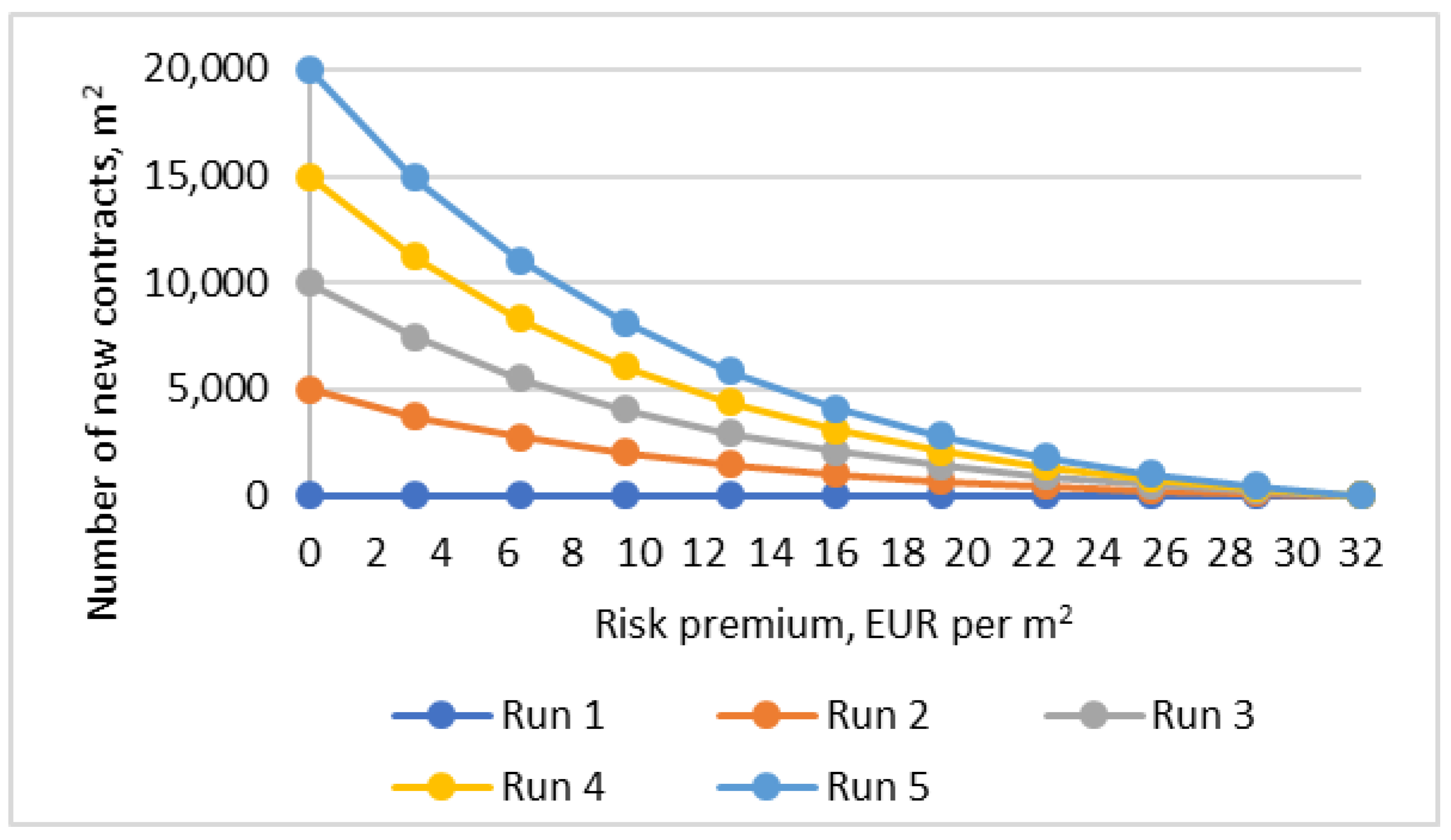

3.2.1. Results of Extreme Value Test

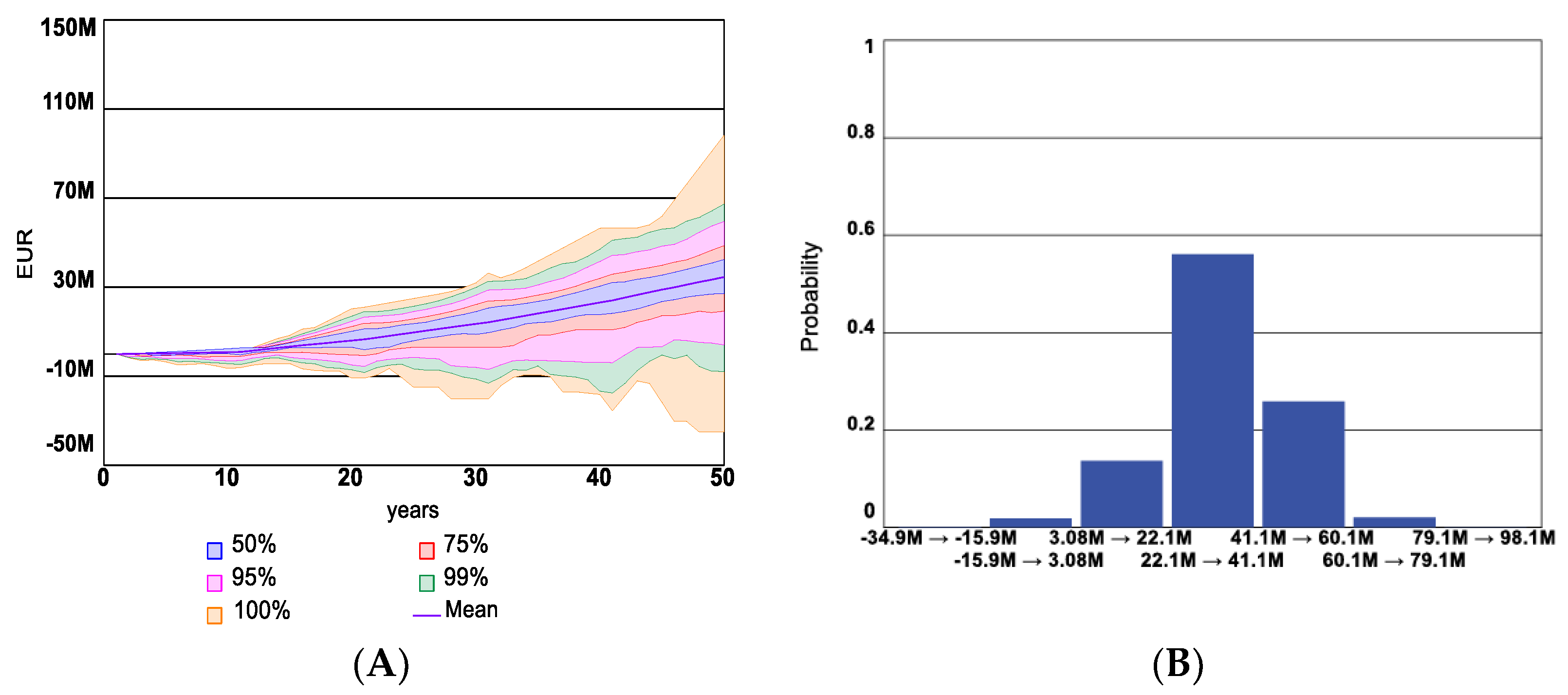

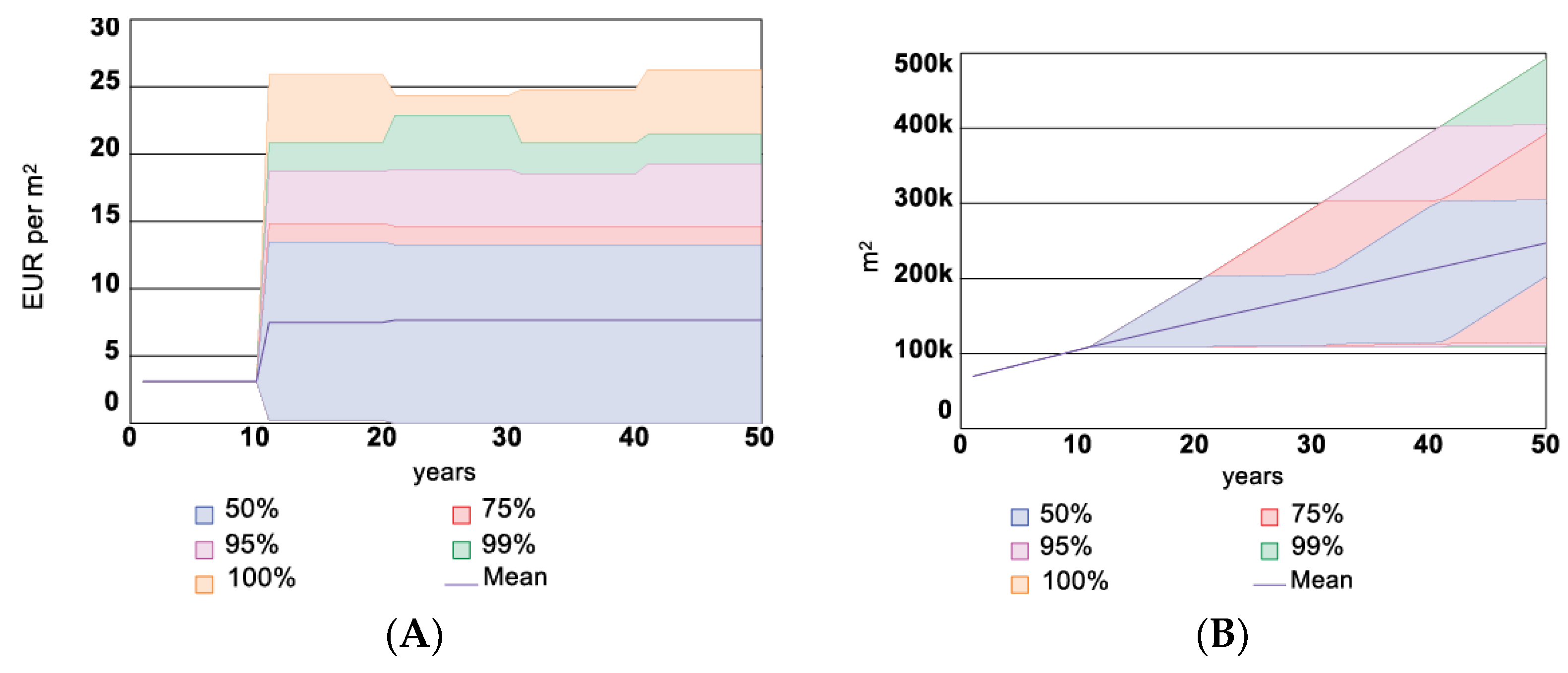

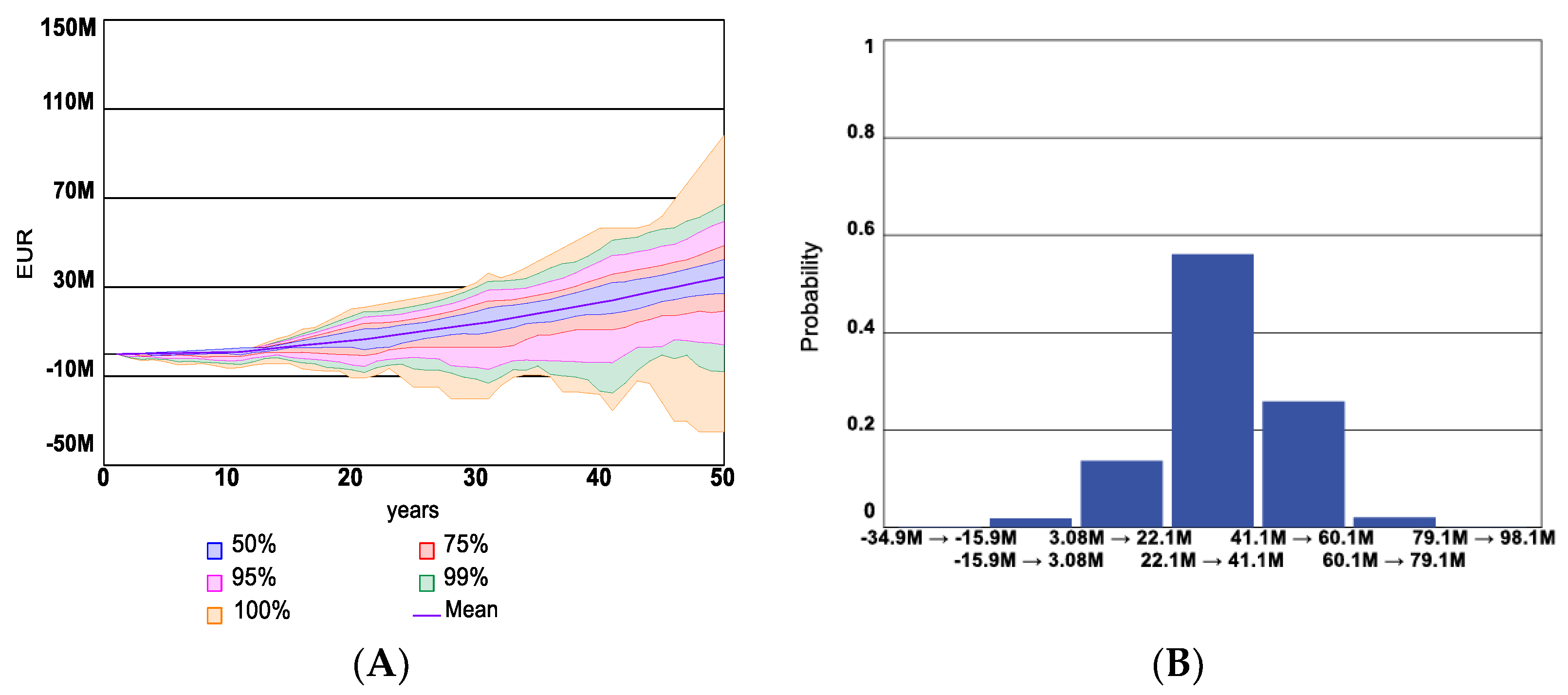

3.2.2. Sensitivity Analysis Output

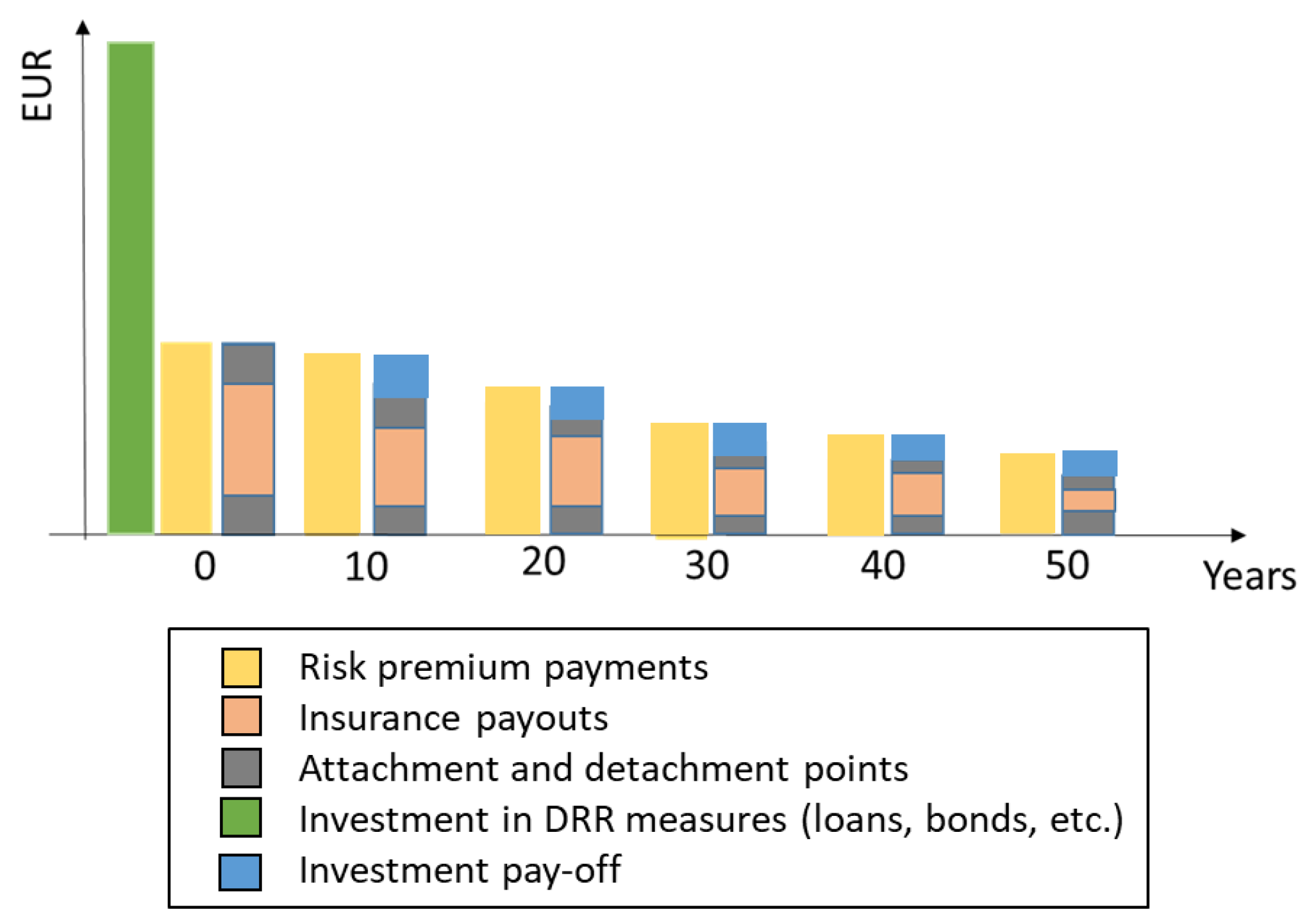

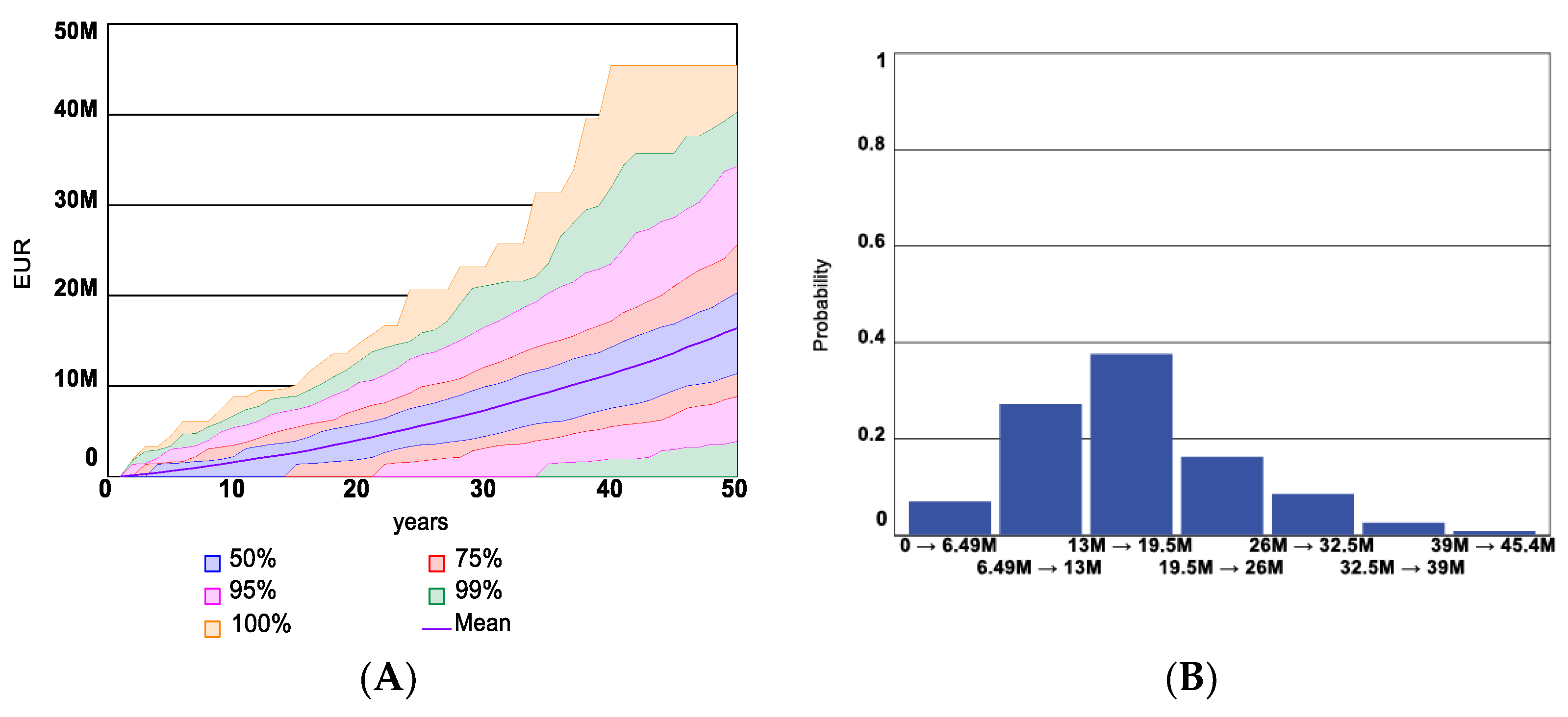

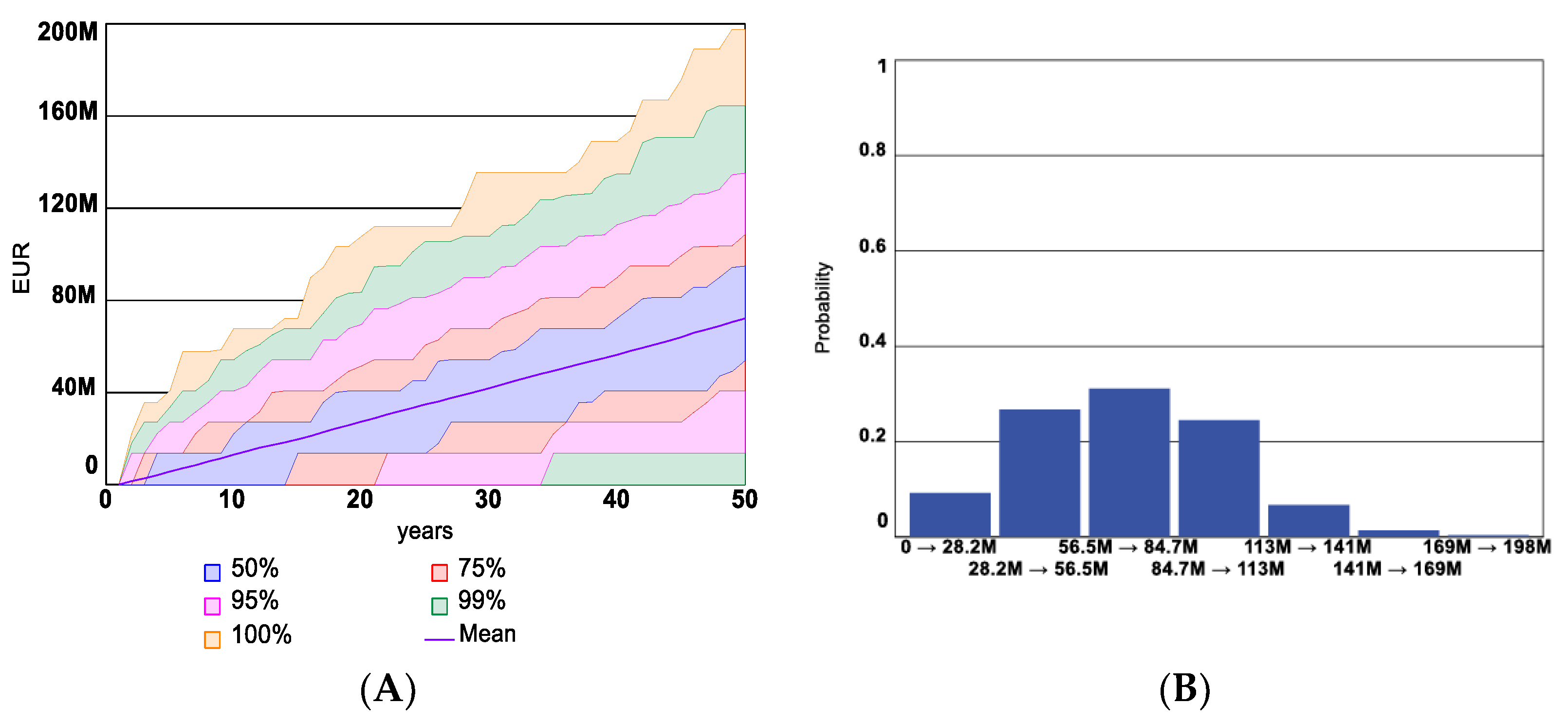

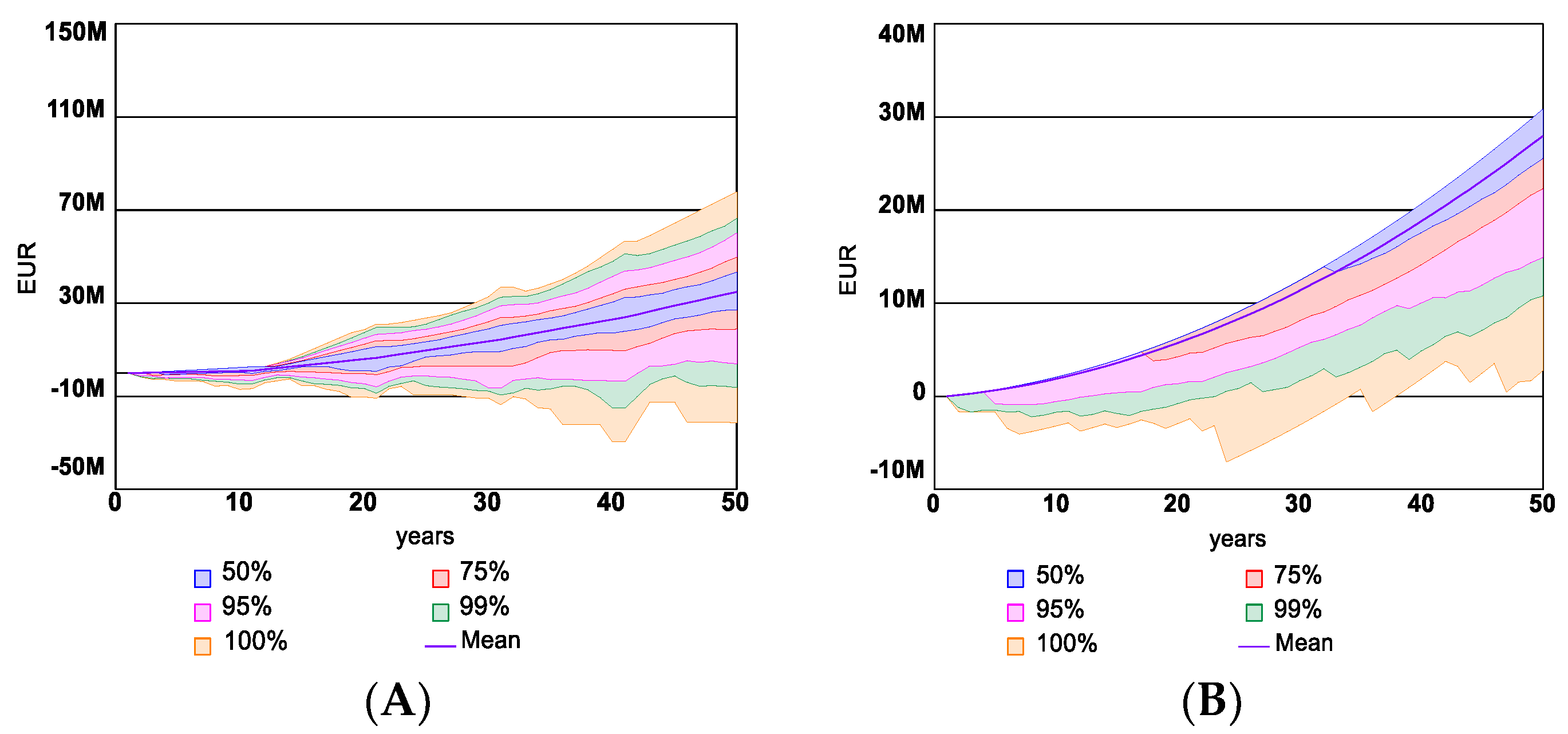

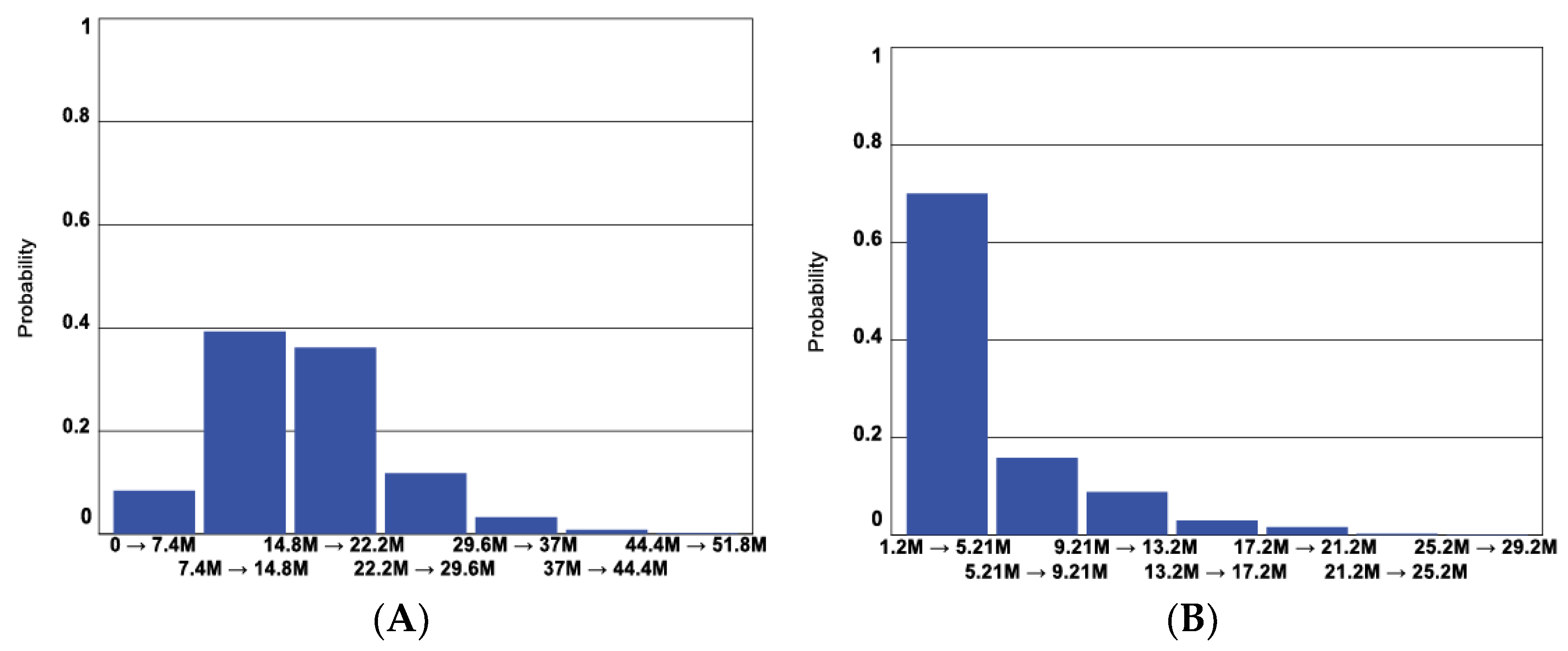

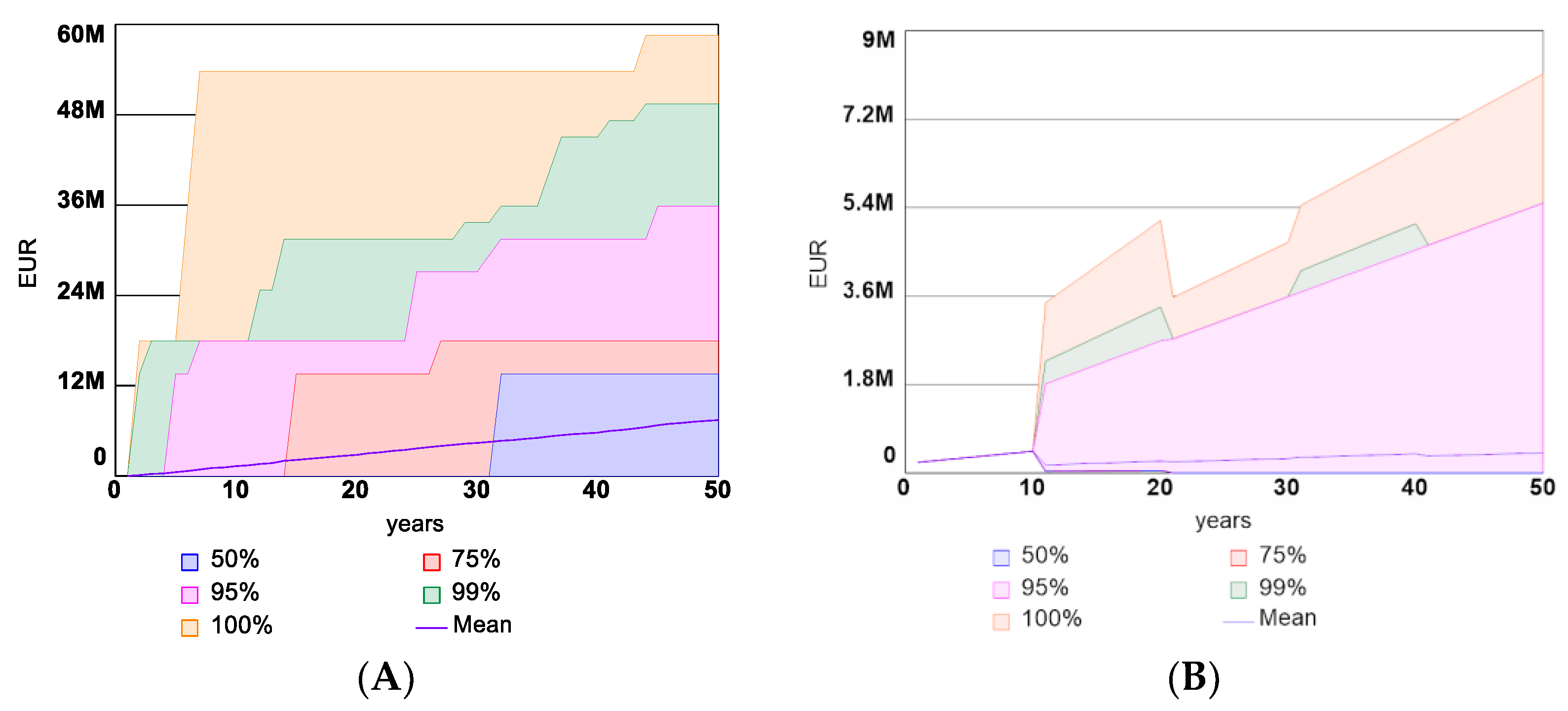

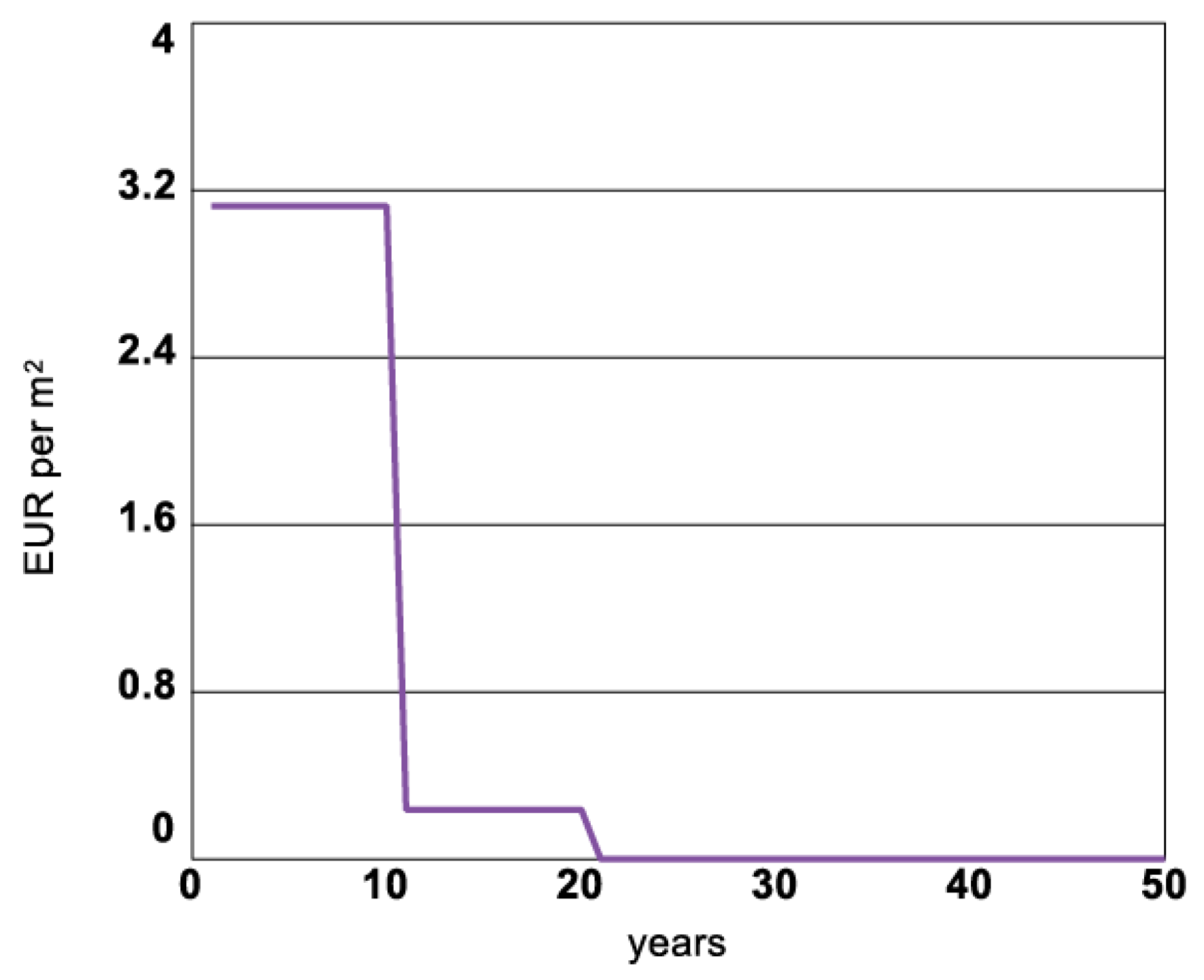

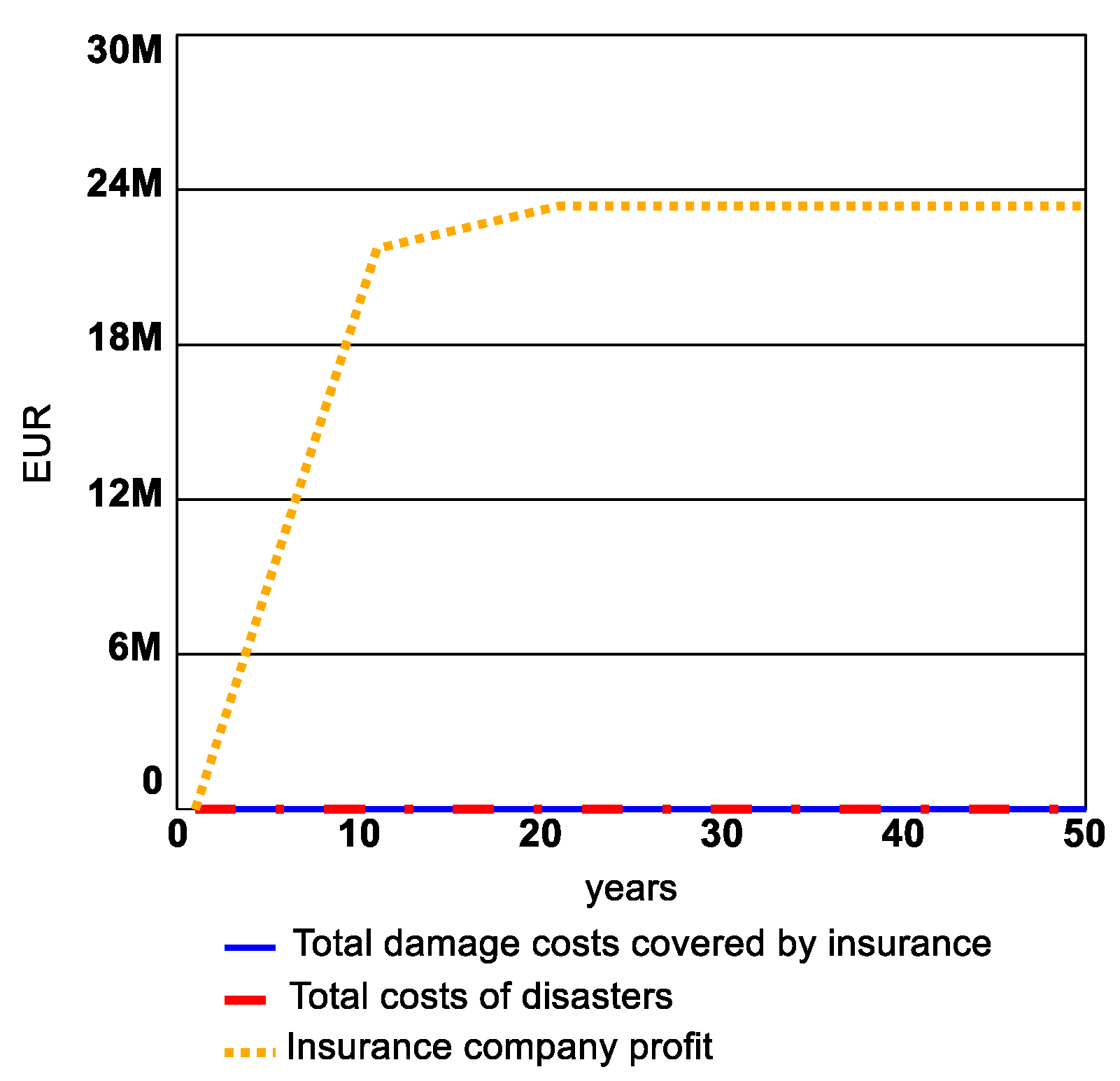

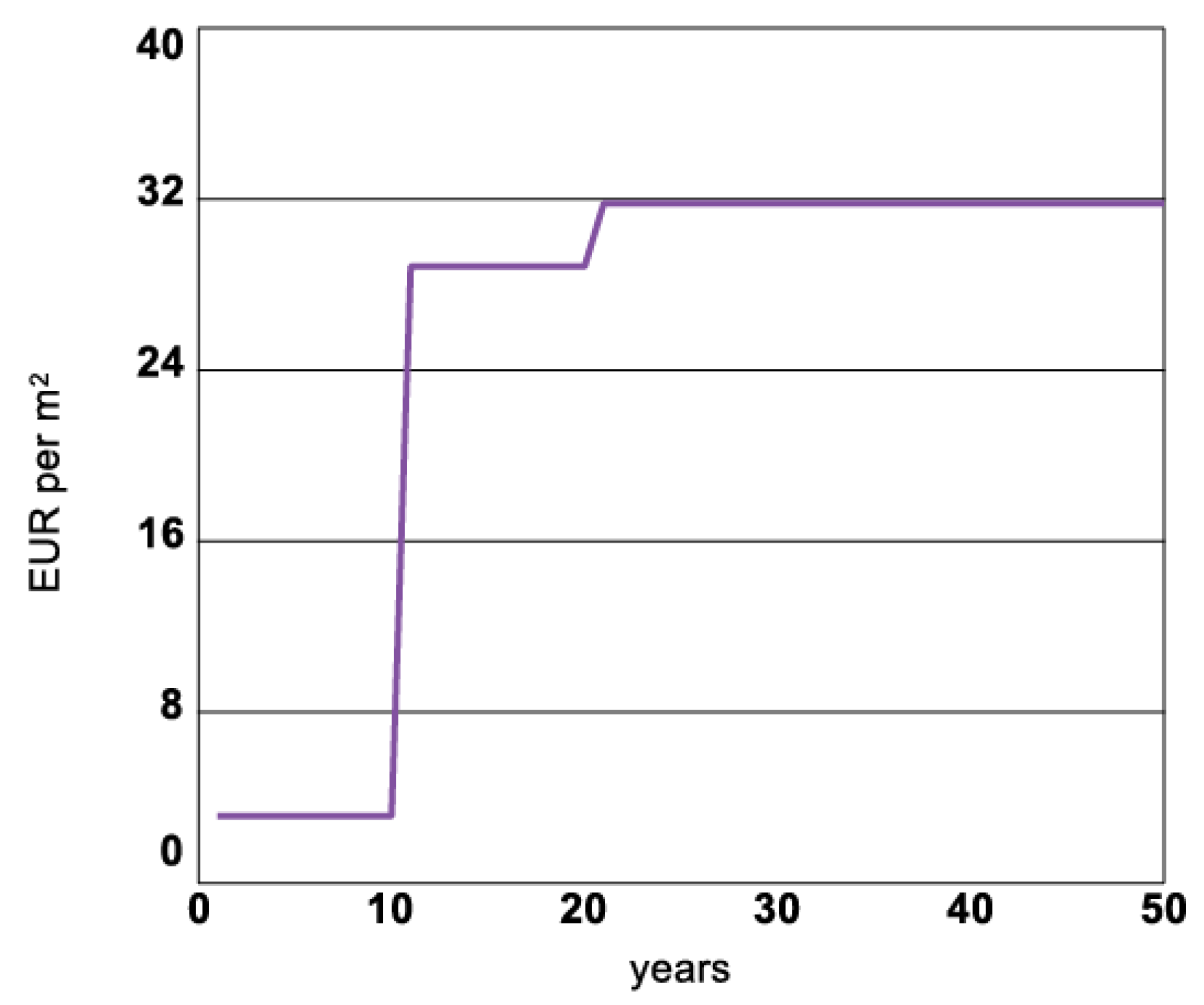

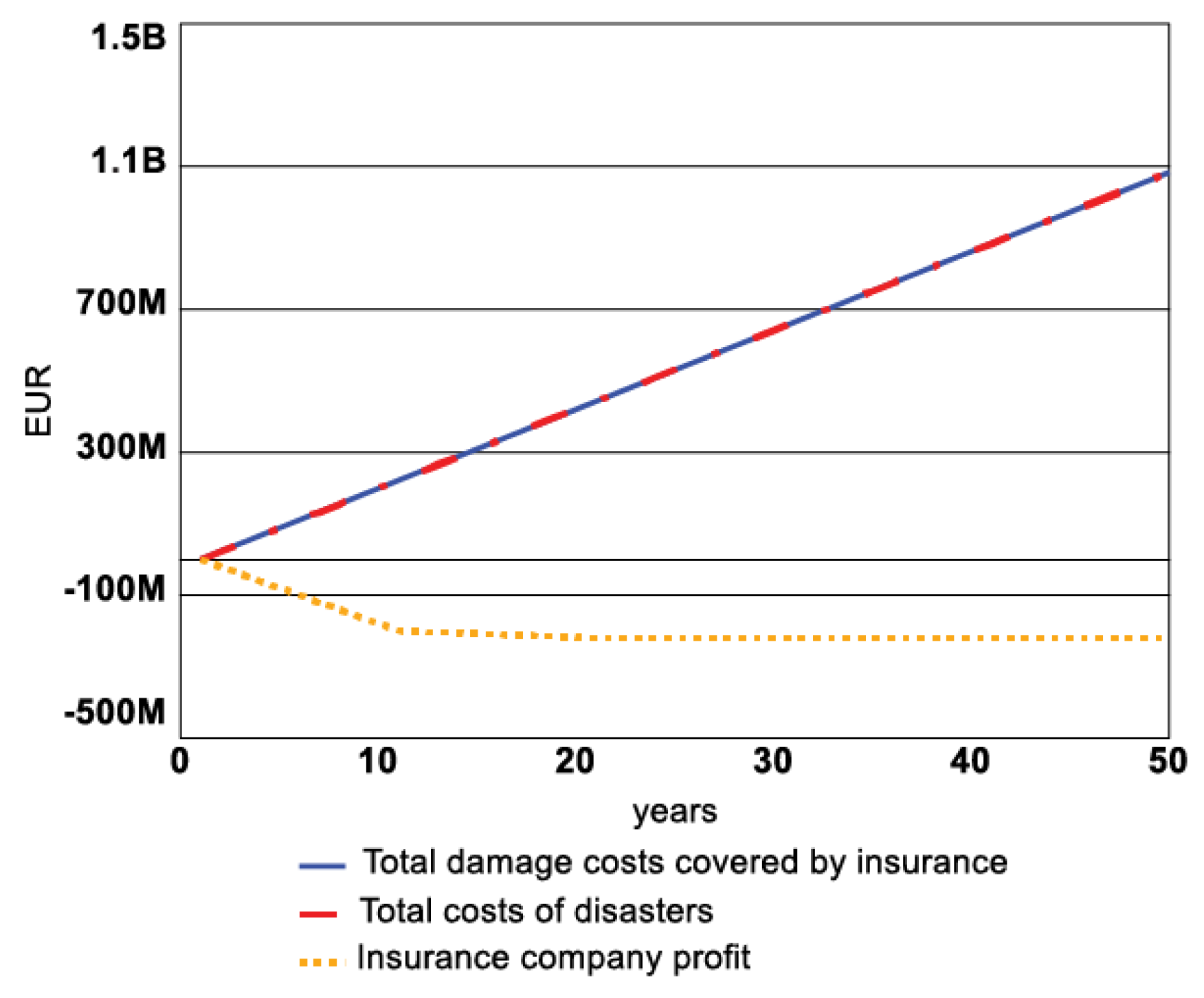

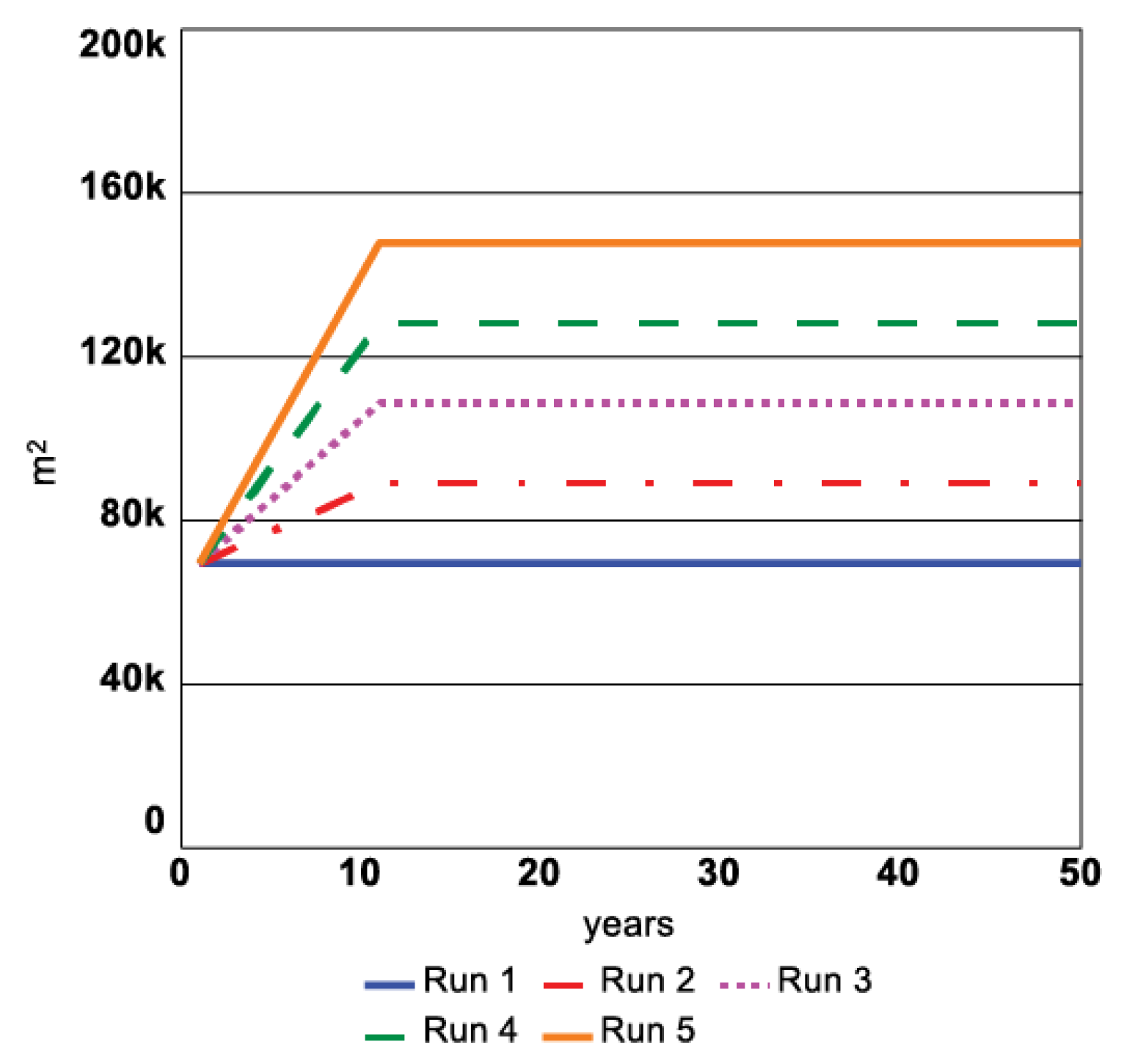

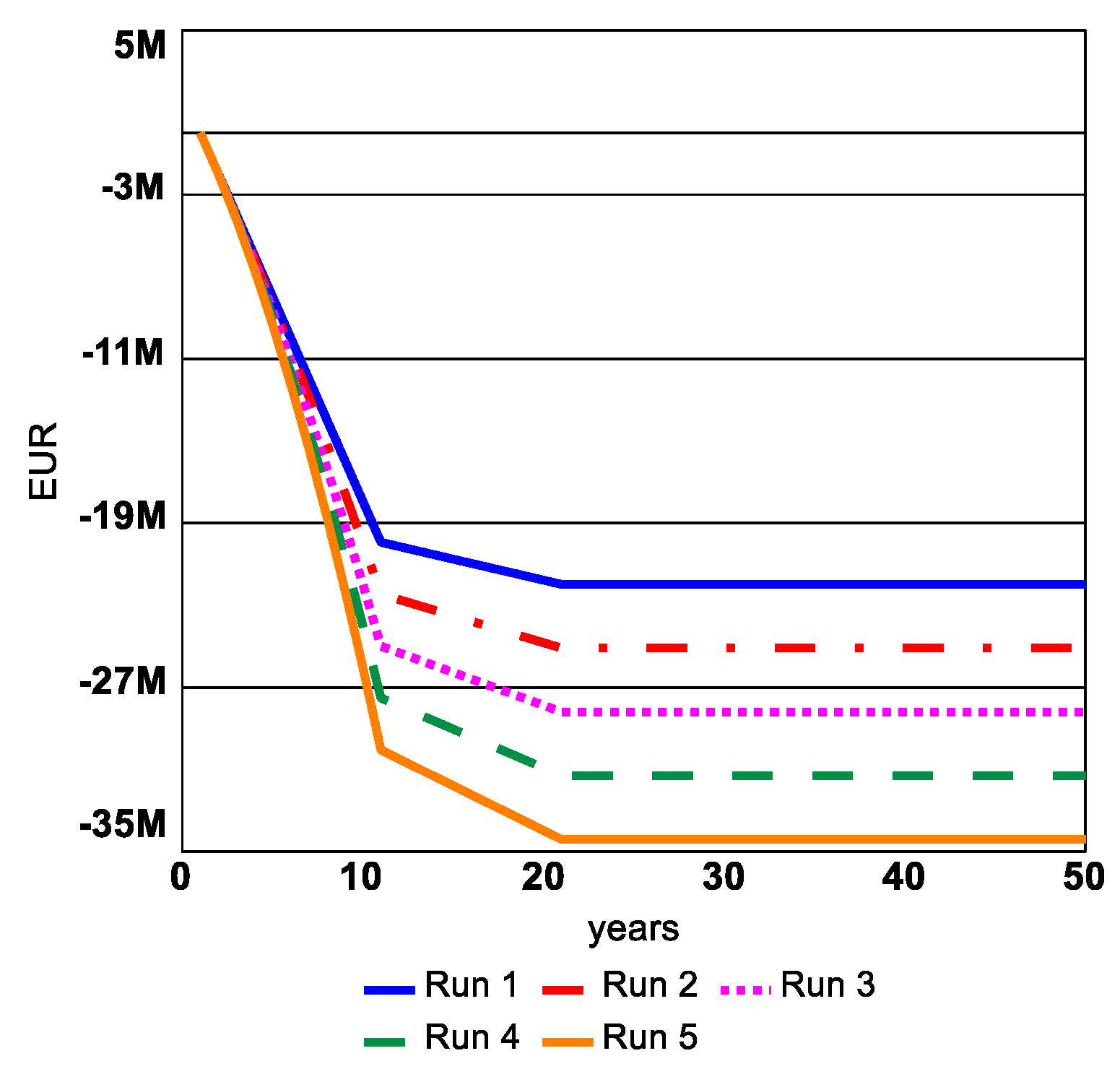

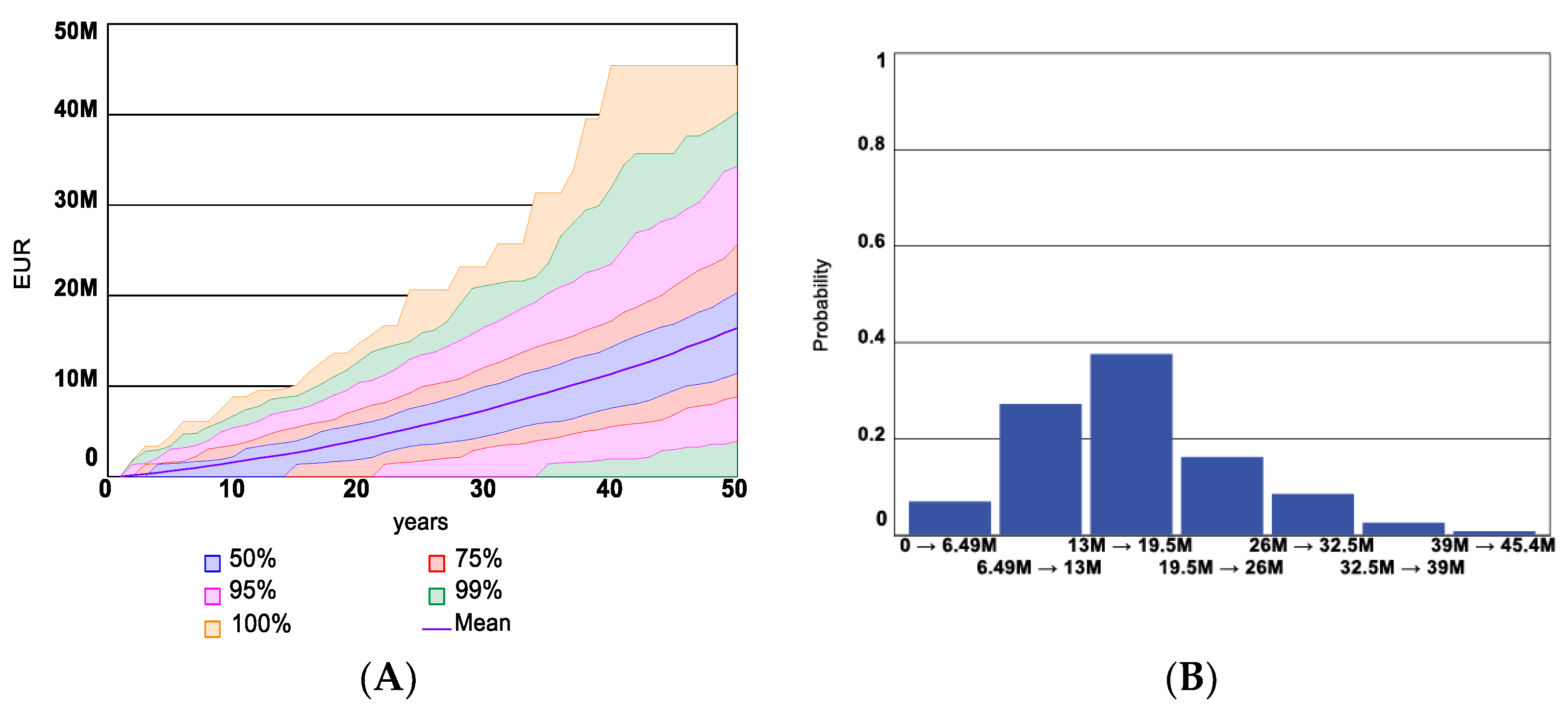

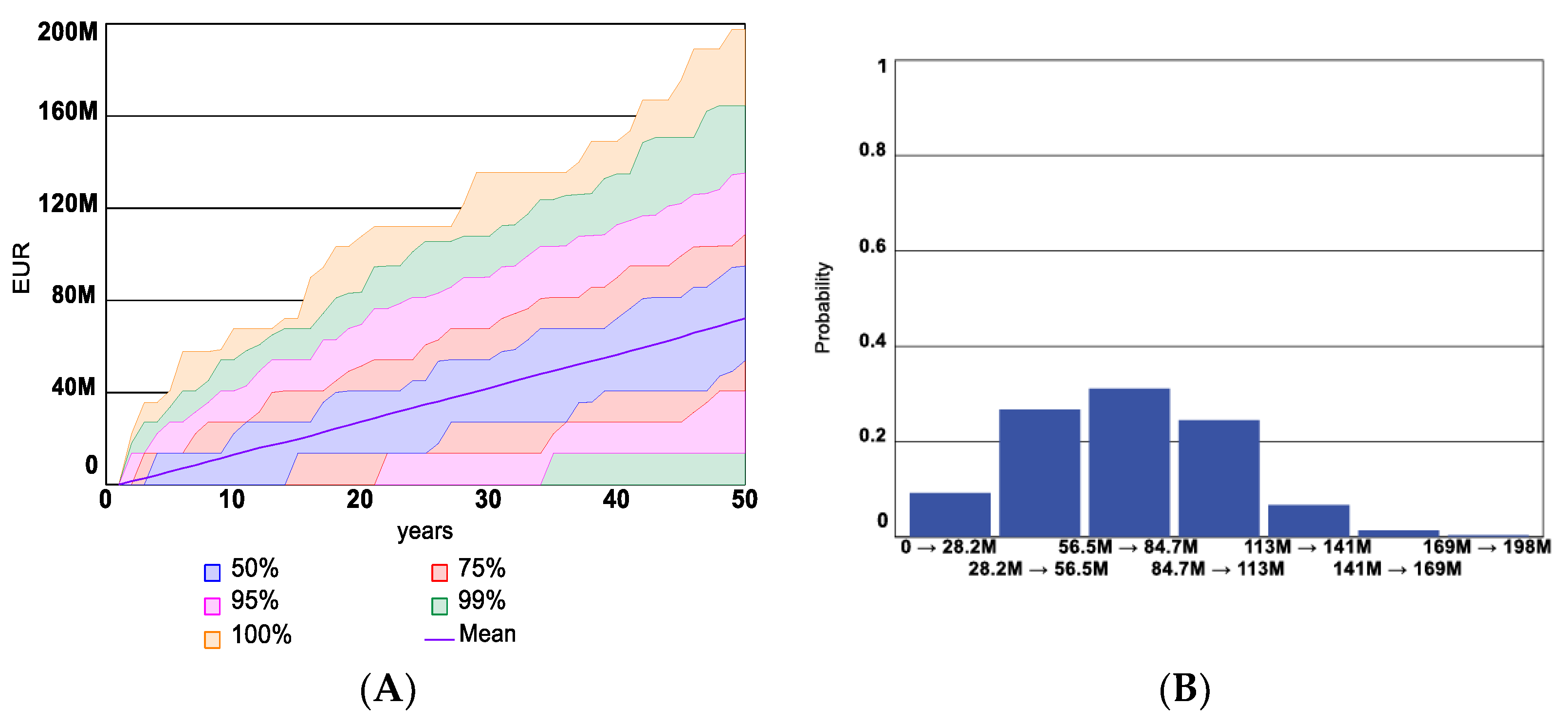

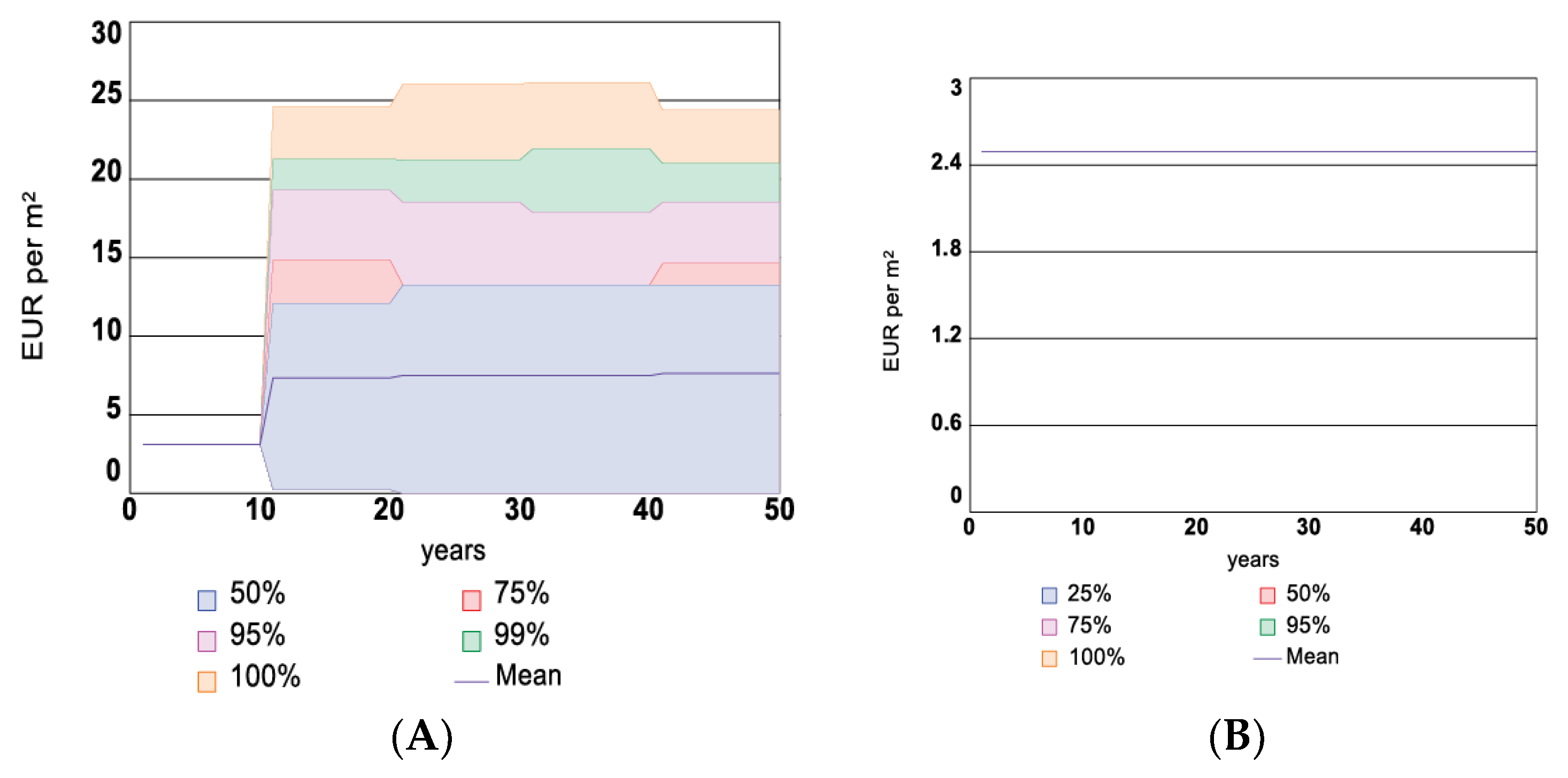

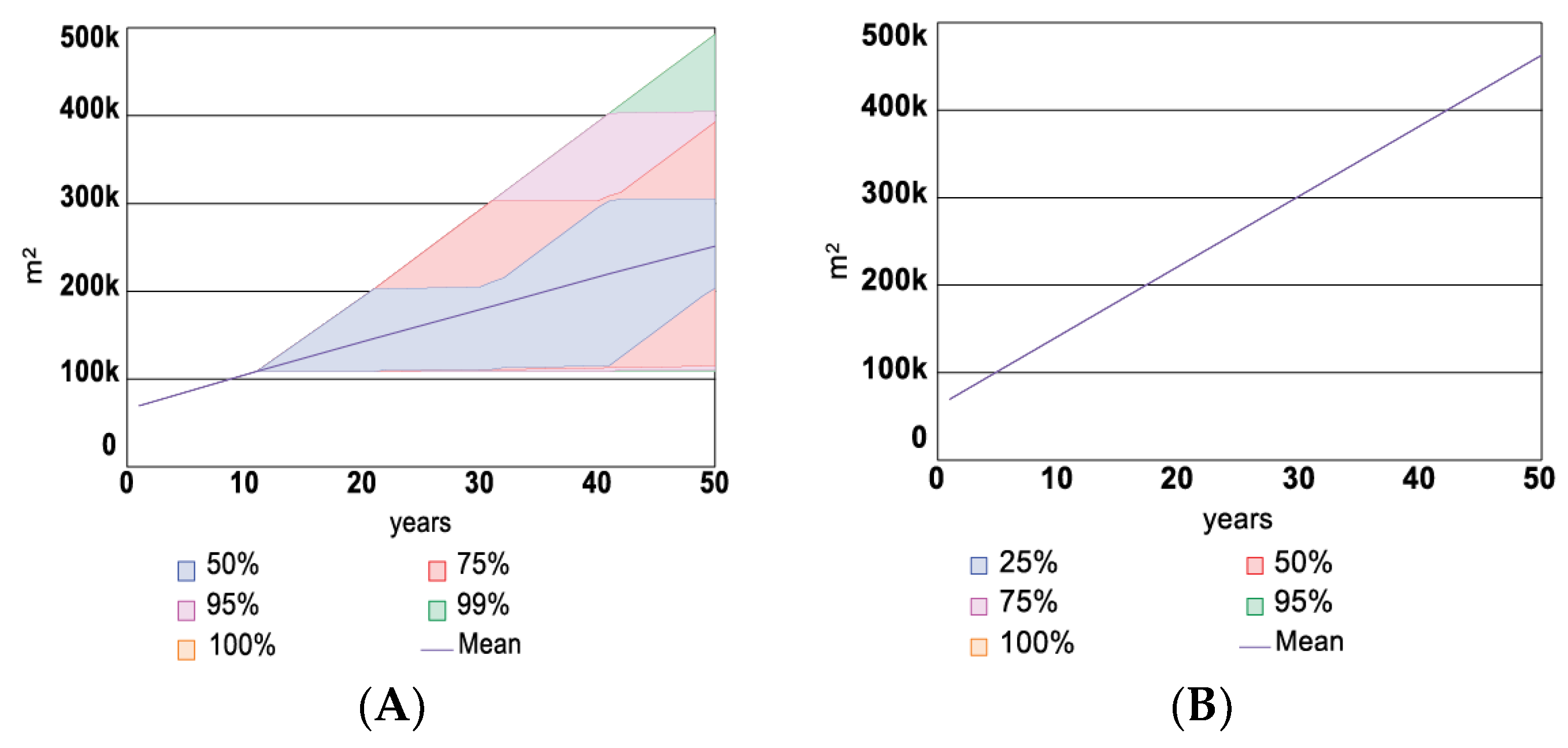

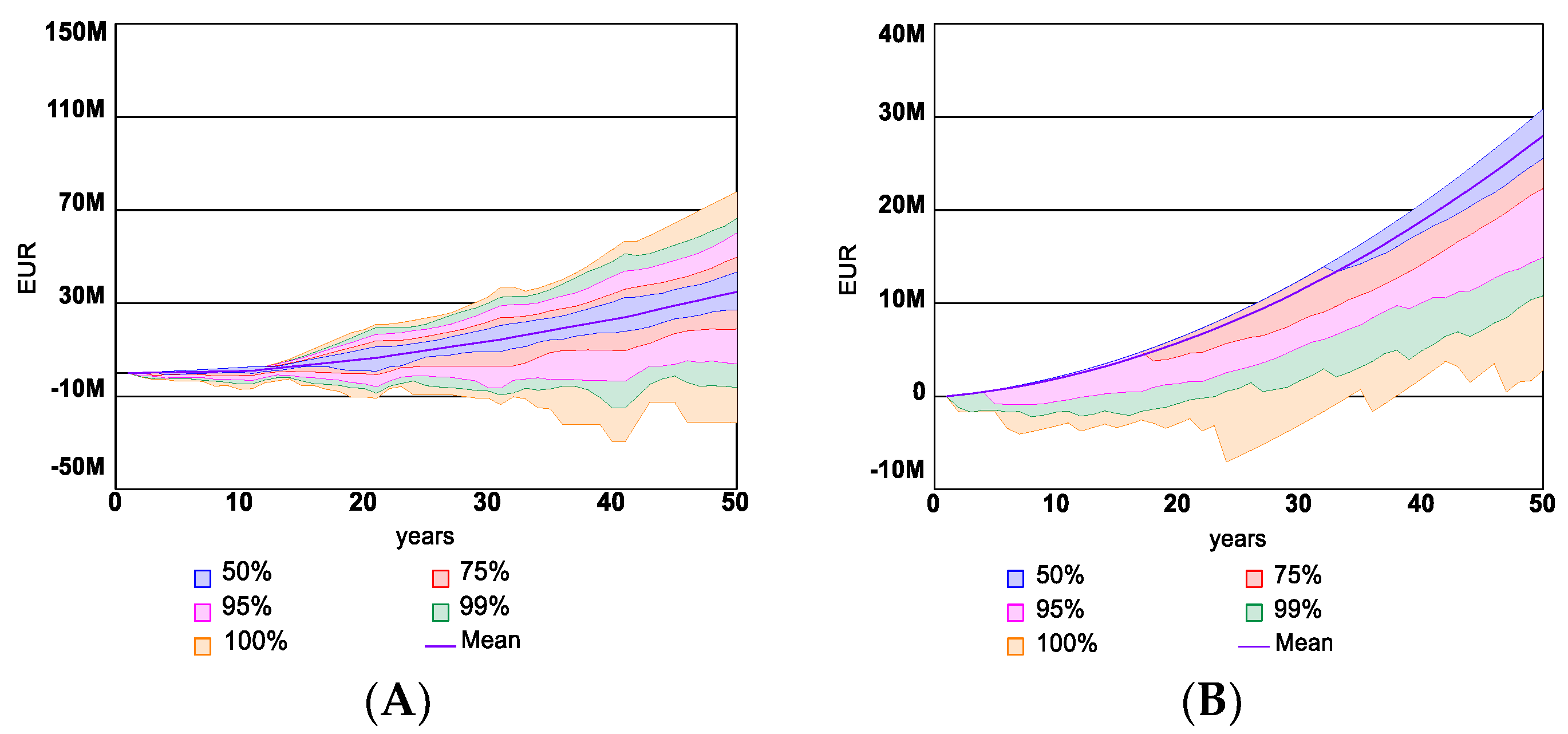

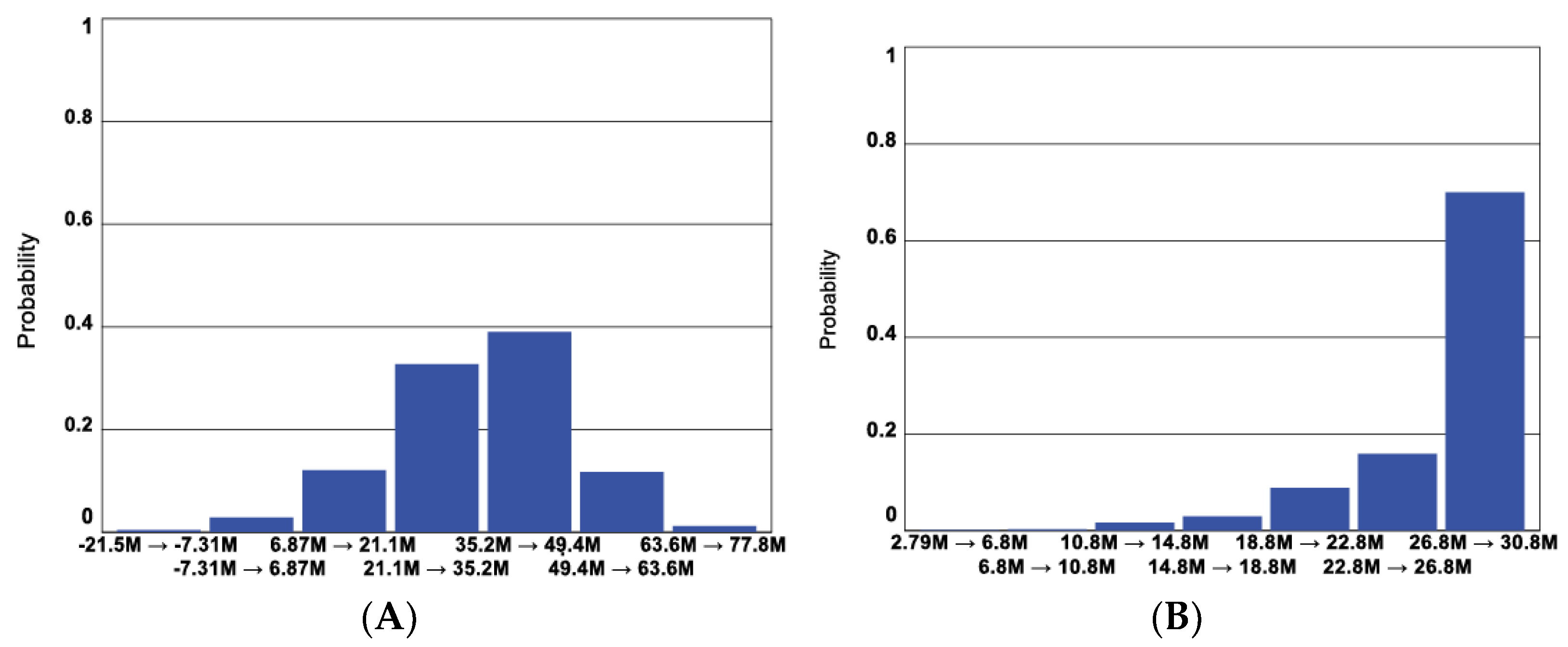

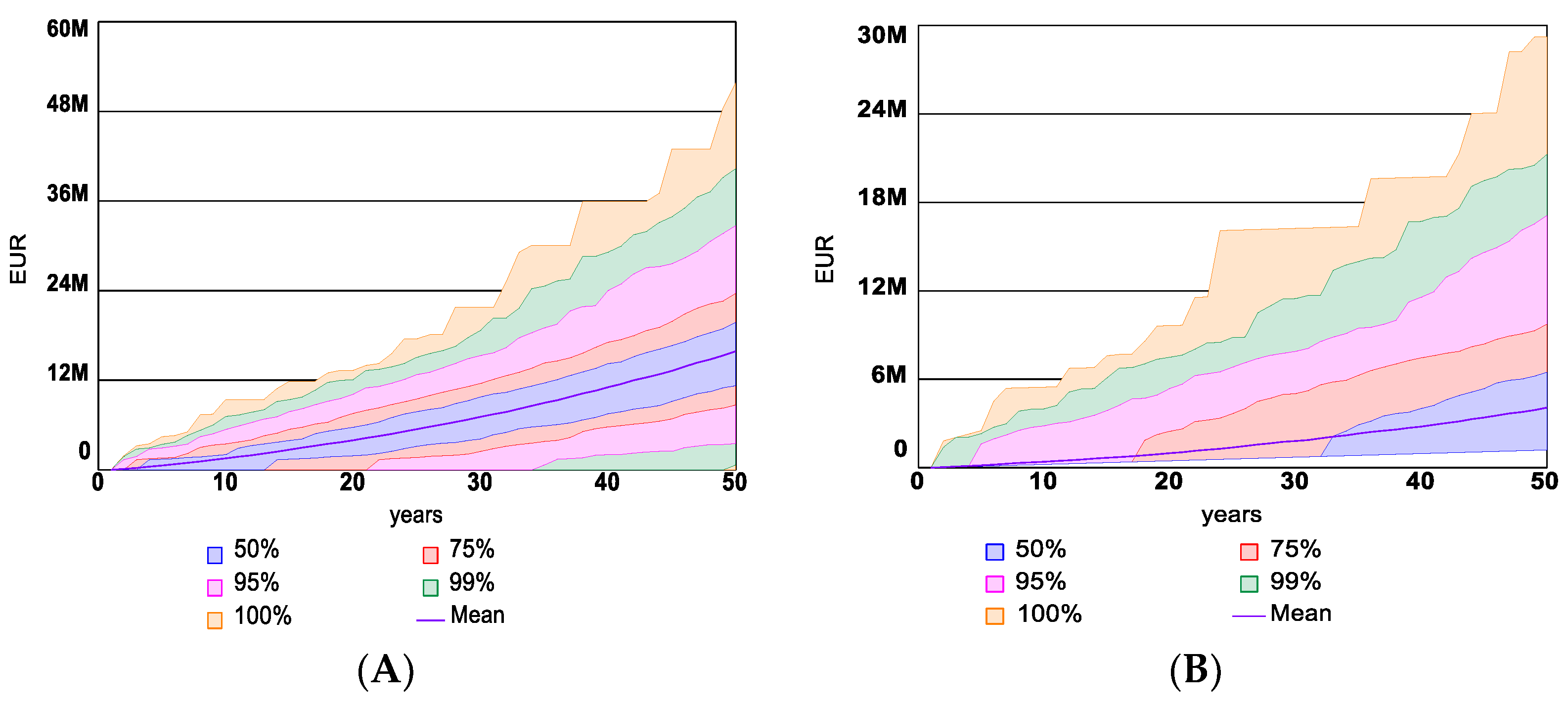

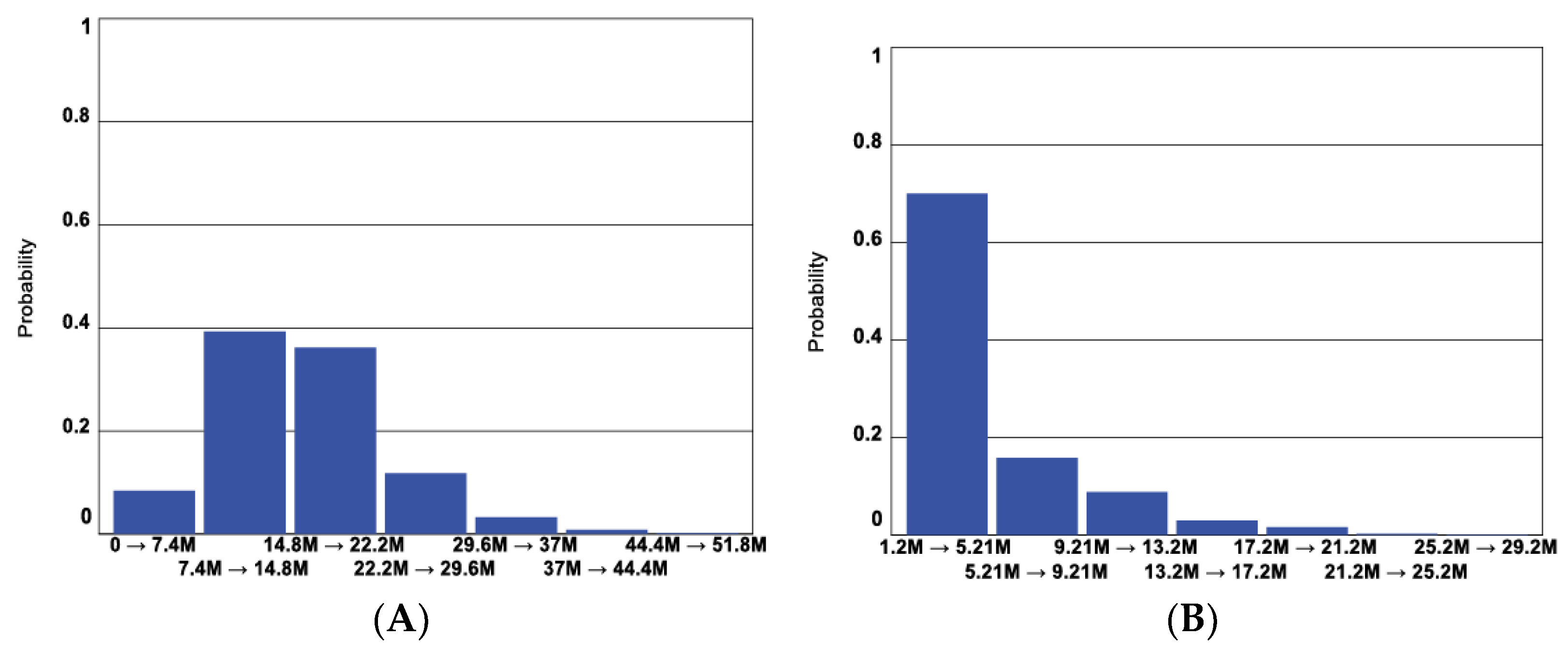

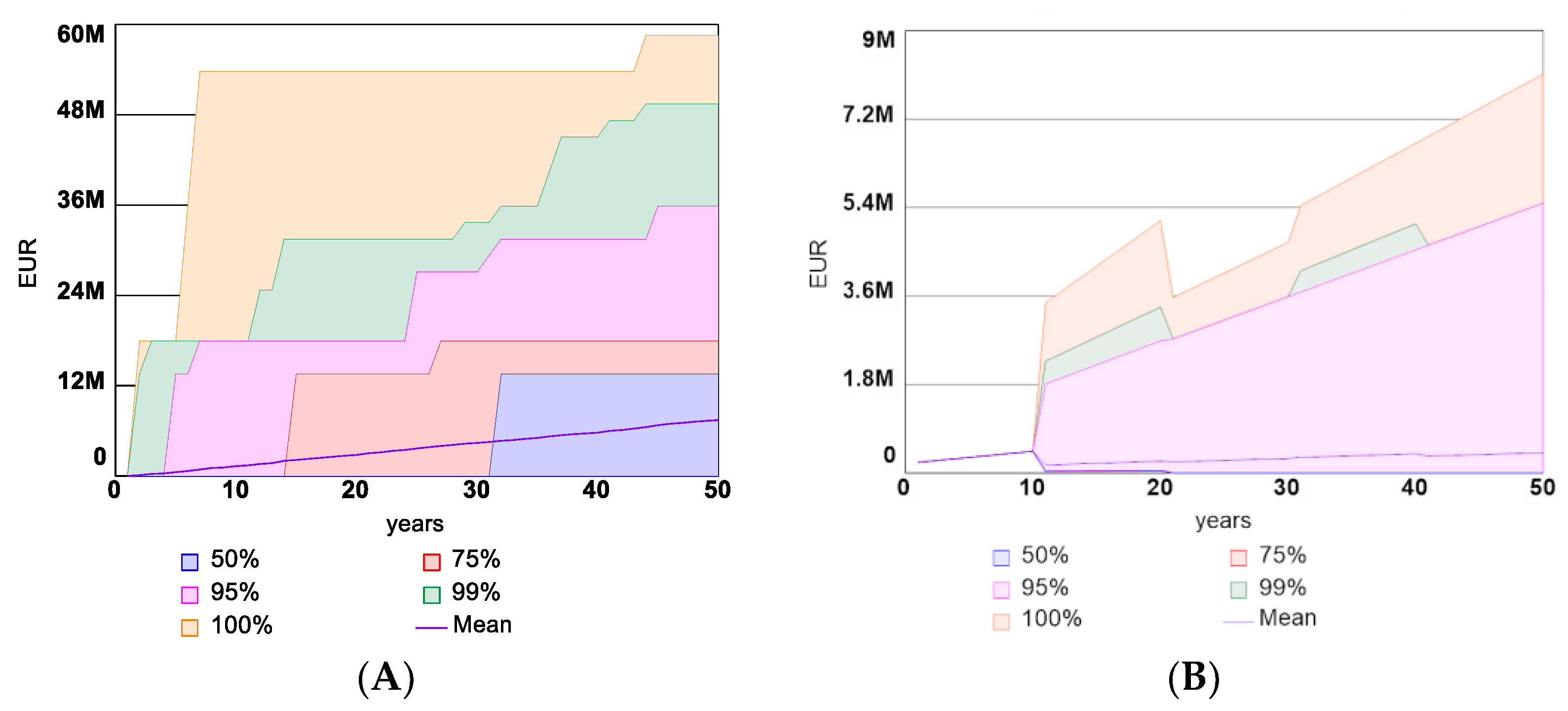

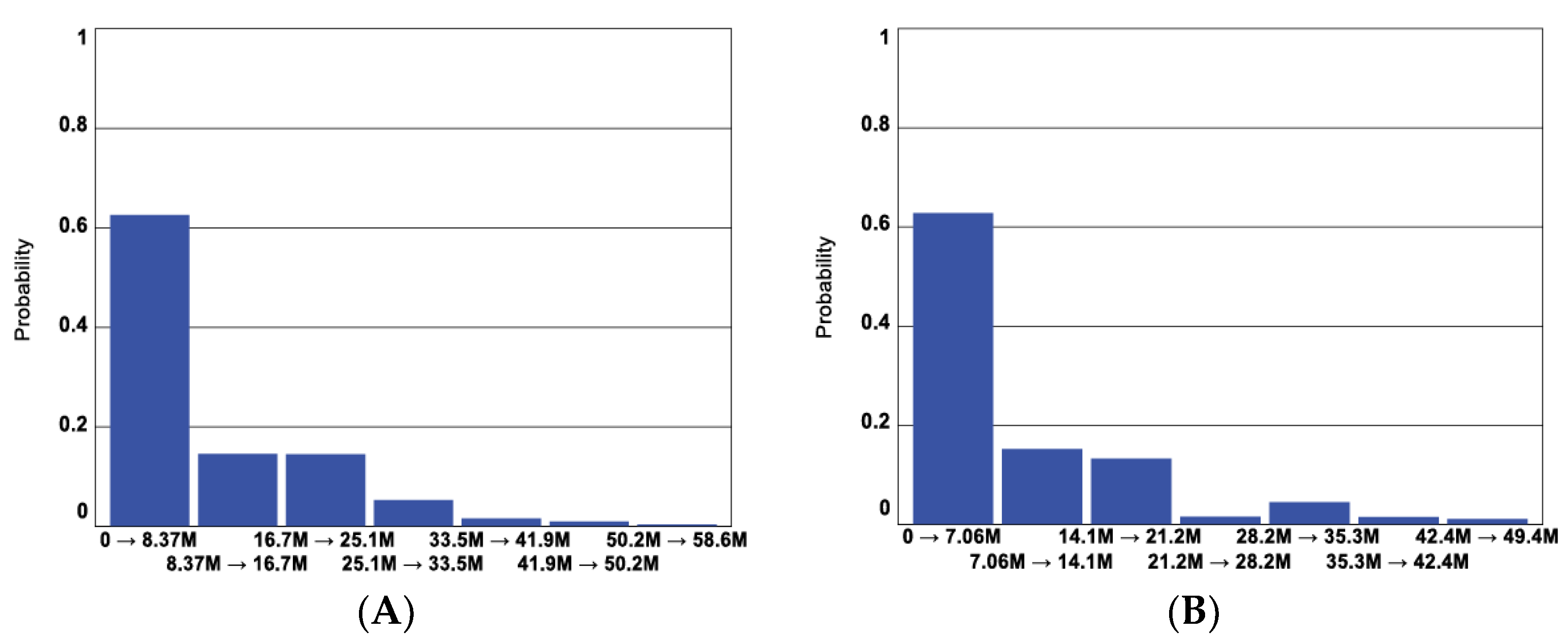

3.3. Results of Case Study and Policy Scenarios

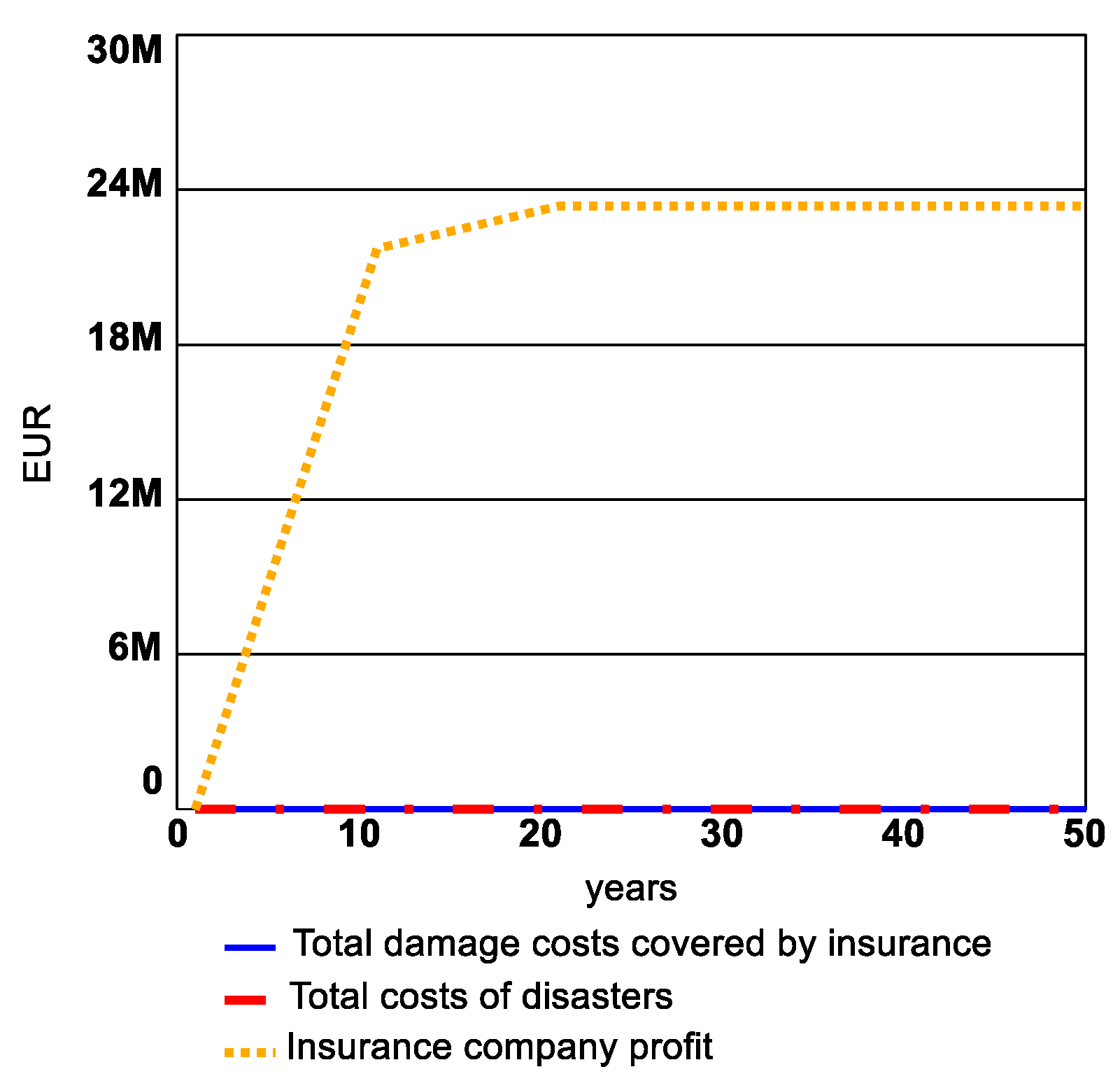

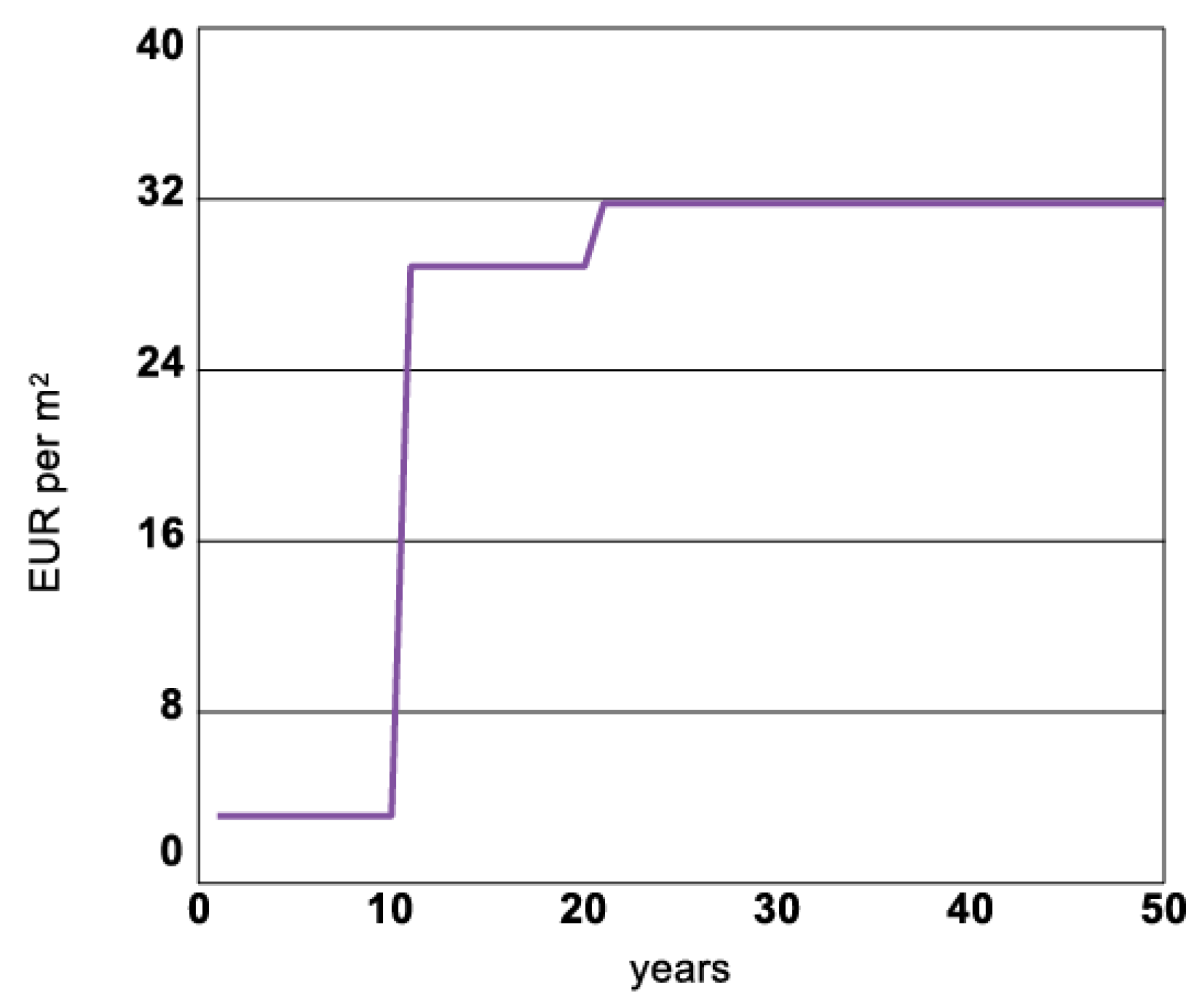

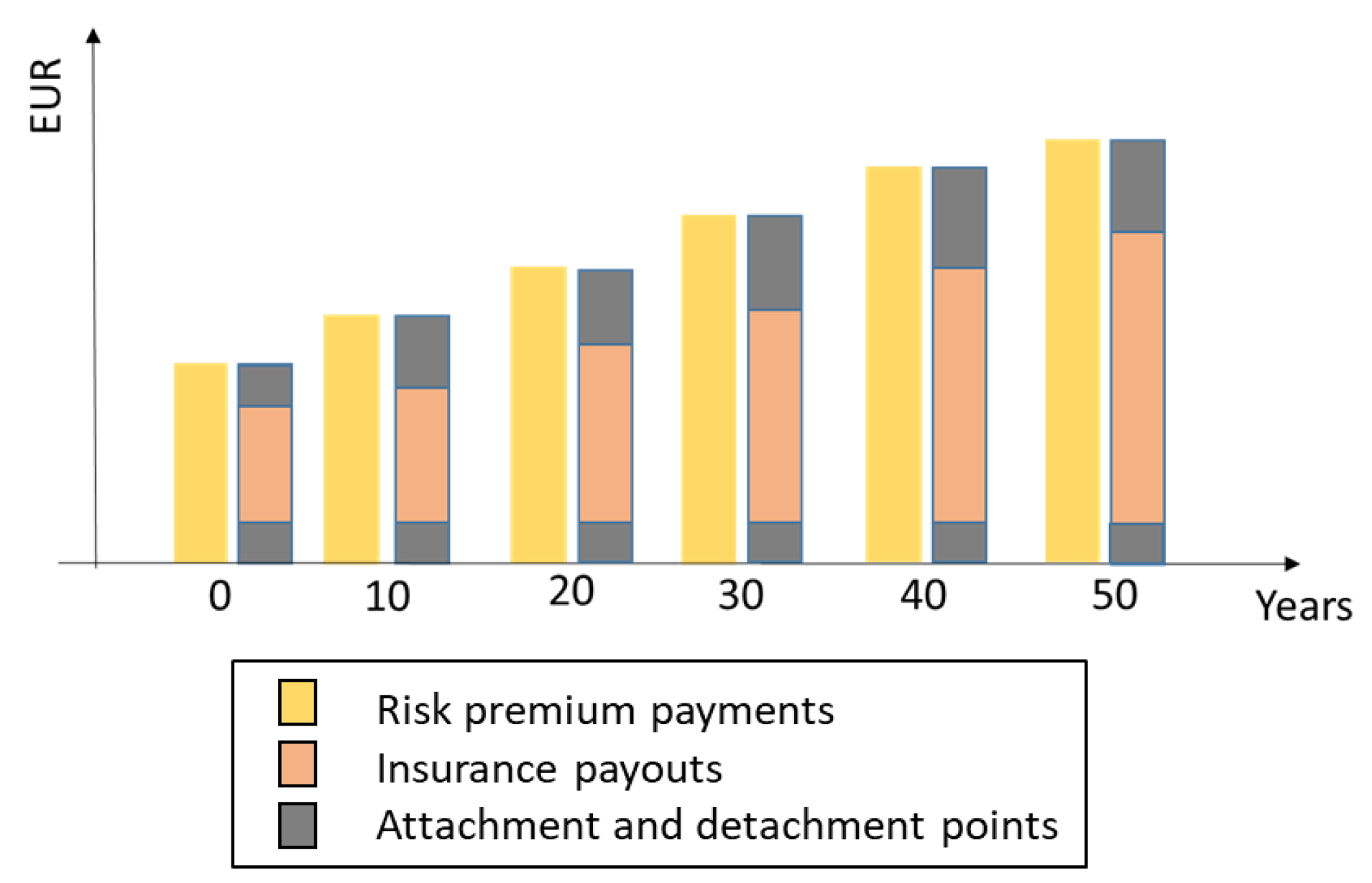

3.3.1. Business as Usual Scenario

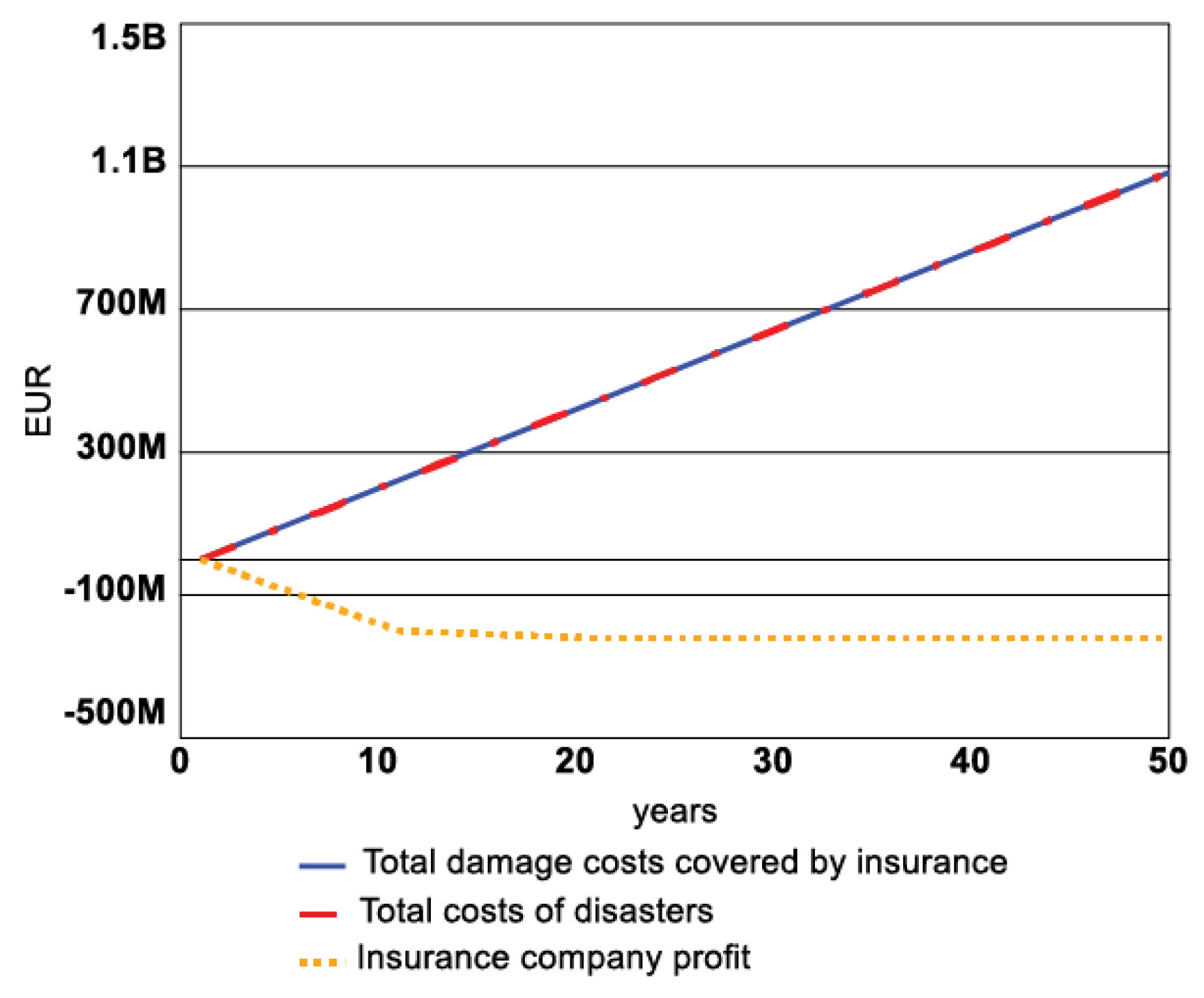

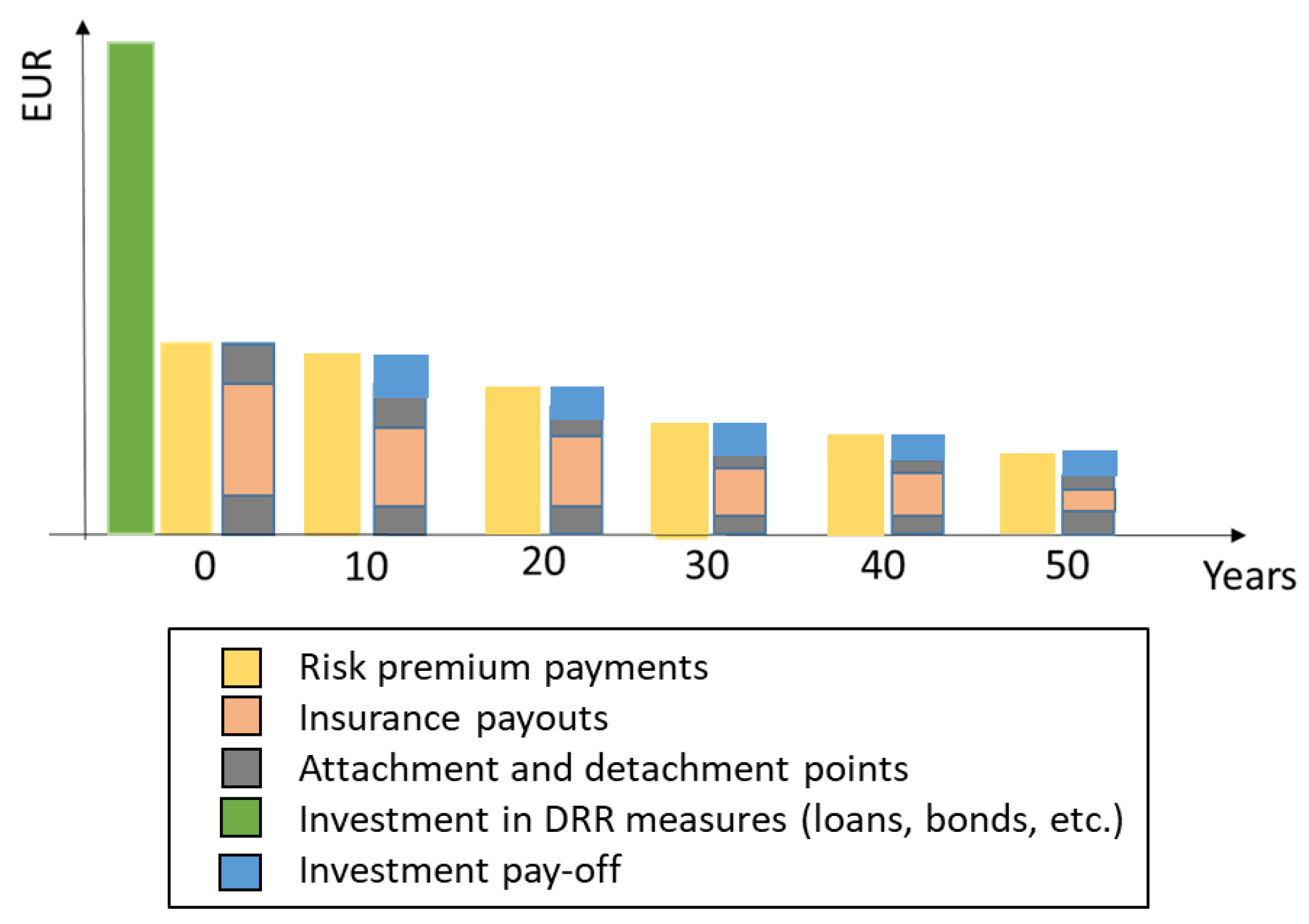

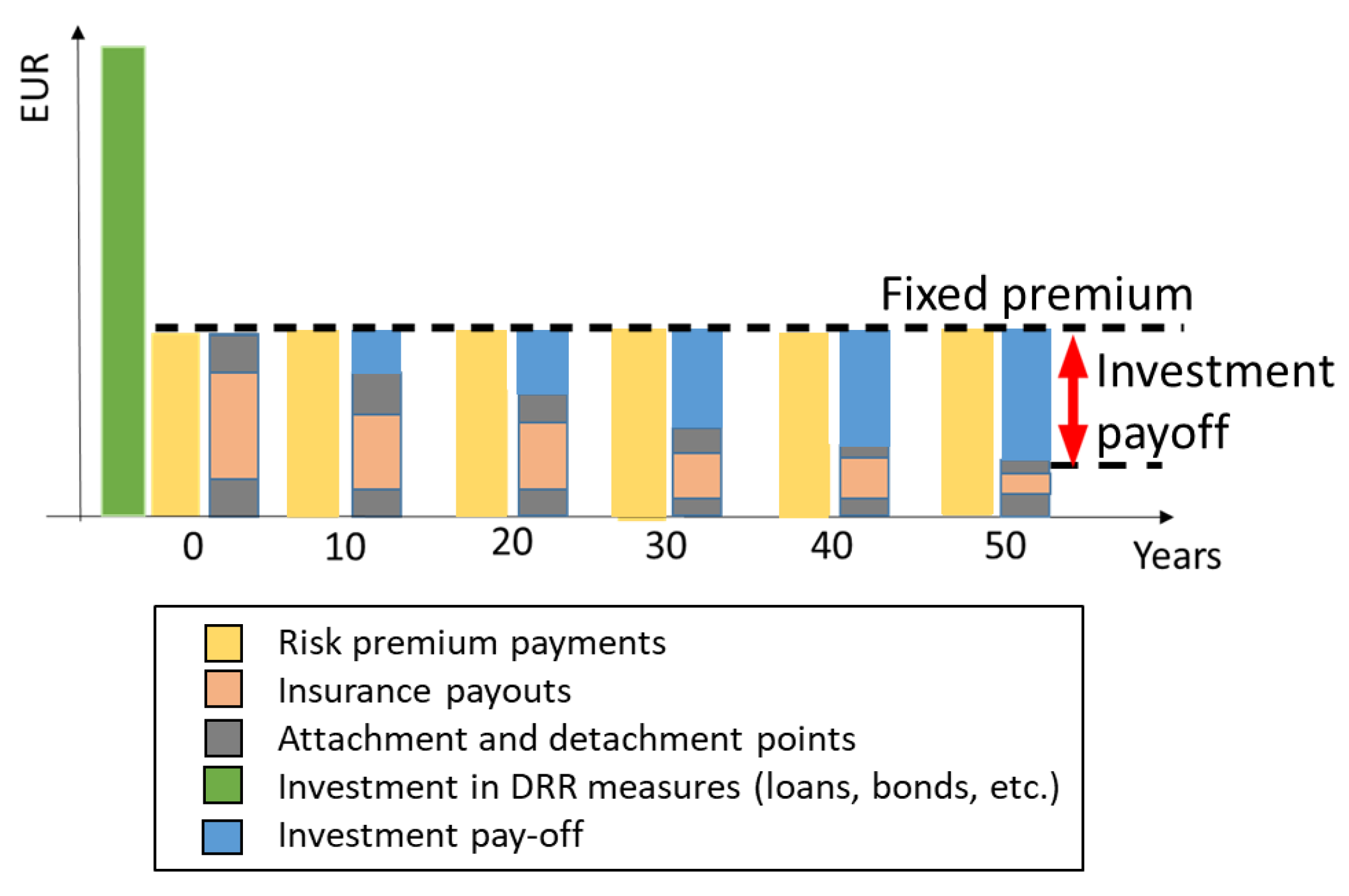

3.3.2. Scenarios with Investment in Disaster Risk Reduction

3.4. Discussion on Findings and Limitations of the Case Study Results

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abdi, Mukhtar Jibril, Nurfarhana Raffar, Zed Zulkafli, Khairudin Nurulhuda, Balqis Mohamed Rehan, Farrah Melissa Muharam, Nor Ain Khosim, and Fredolin Tangang. 2022. Index-based insurance and hydroclimatic risk management in agriculture: A systematic review of index. International Journal of Disaster Risk Reduction 67: 102653. [Google Scholar] [CrossRef]

- Berghuijs, Wouter R., Scott T. Allen, Shaun Harrigan, and James W. Kirchner. 2019. Growing Spatial Scales of Synchronous River Flooding in Europe. Geophysical Research Letters 46: 1423–28. [Google Scholar] [CrossRef]

- Bevere, Lucia, Michael Gloor, and Adam Sobel. 2020. Natural Catastrophes in Times of Economic Accumulation and Climate Change. Zurich: Swiss Re Sigma. [Google Scholar]

- Blumberga, Andra, Blumberga Dagnija, Bažbauers Gatis, Davidsen Paul, Moxnes Erling, Dzene Ilze, Barisa Barisa, Žogla Gatis, Dāce Elīna, and Ozarska Alise. 2011. System Dynamics for Environmental Engineering Students, 1st ed. Riga: Riga Technical University. [Google Scholar]

- Cabinet of Ministers. 2019. Latvian Adaptation Plan to Climate Change for Time Period to 2030. Available online: https://likumi.lv/ta/en/en/id/308330 (accessed on 30 June 2023).

- Carter, Jeremy G. 2011. Climate change adaptation in European cities. Current Opinion in Environmental Sustainability 3: 193–98. [Google Scholar] [CrossRef]

- Centre for Research on the Epidemiology of Disasters (CRED), and United Nations Office for Disaster Risk Reduction (UNDRR). 2020. Human Cost of Disasters, an Overview of the Last 20 Years (2000–2019). Geneva: United Nations Office for Disaster Risk Reduction (UNDRR). [Google Scholar] [CrossRef]

- Chen, Mei-Su, Chih-Tung Hsiao, Gene C. Lai, and Pao-Long Chang. 2009. A System Dynamics Model of Development and Business Strategy in Taiwan Life Insurance Industry. The Journal of Risk Management and Insurance 13: 1. [Google Scholar]

- Clarvis, Margot Hill, Erin Bohensky, and Masaru Yarime. 2015. Can resilience thinking inform resilience investments? Learning from resilience principles for disaster risk reduction. Sustainability 7: 9048–66. [Google Scholar] [CrossRef]

- Coffee, Joyce. 2020. Financing Resilient Infrastructure. In Optimizing Community Infrastructure: Resilience in the Face of Shocks and Stresses. Amsterdam: Elsevier, pp. 101–21. [Google Scholar] [CrossRef]

- Colker, Ryan M. 2019. Optimizing Community Infrastructure: Resilience in the Face of Shocks and Stresses. In Optimizing Community Infrastructure: Resilience in the Face of Shocks and Stresses. Amsterdam: Elsevier. [Google Scholar] [CrossRef]

- EM-DAT. 2022. The OFDA/CRED International Disaster Database. Brussels: UCLouvain. Available online: https://www.emdat.be/ (accessed on 30 June 2023).

- European Environment Agency. 2010. Mapping the Impacts of Natural HAZARDS and Technological Accidents in Europe. Technical Report No. 13. Copenhagen: European Environment Agency. [Google Scholar]

- Feofilovs, Maksims. 2020. Dynamics of Urban Resilience to Natural Hazards. Ph.D. Thesis, RTU, Riga, Latvia; 179p. [Google Scholar]

- Feofilovs, Maksims, and Francesco Romagnoli. 2021. Dynamic assessment of urban resilience to natural hazards. International Journal of Disaster Risk Reduction 62: 102328. [Google Scholar] [CrossRef]

- Forrester, Jay Wright. 2009. Some Basic Concepts in System Dynamics. Sloan School of Management. pp. 1–17, [Online]. Available online: http://www.systemsmodelbook.org/uploadedfile/238_63f73156-02df-4d87-b0c6-c286a7beec26_SomeBasicConcepts.pdf (accessed on 30 June 2023).

- Forzieri, Giovanni, Luc Feyen, Simone Russo, Michalis Vousdoukas, Lorenzo Alfieri, Stephen Outten, Mirco Migliavacca, Alessandra Bianchi, Rodrigo Rojas, and Alba Cid. 2016. Multi-hazard assessment in Europe under climate change. Climate Change 137: 105–19. [Google Scholar] [CrossRef]

- Frisari, Giovanni Leo, Anaitée Mills, Mariana Silva, Marcel Ham, Elisa Donadi, Christine Shepherd, and Irene Pohl. 2020. Climate Resilient Public Private Partnerships: A Toolkit for Decision Makers. Washington, DC: IDB. [Google Scholar] [CrossRef]

- Gall, Melanie, and Caro J. Friedland. 2020. If Mitigation Saves $6 Per Every $1 Spent, Then Why Are We Not Investing More? A Louisiana Perspective on a National Issue. Natural Hazards Review 21: 04019013. [Google Scholar] [CrossRef]

- Hennighausen, Hannah, Yanjun Liao, Christoph Nolte, and Adam Pollack. 2023. Flood insurance reforms, housing market dynamics, and adaptation to climate risks. Journal of Housing Economics 62: 101953. [Google Scholar] [CrossRef]

- Hofer, Lorenzo, Paolo Gardoni, and Mariano Angelo Zanini. 2021. Risk-based CAT bond pricing considering parameter uncertainties. Sustainable and Resilient Infrastructure 6: 315–29. [Google Scholar] [CrossRef]

- Hudson, Paul, W. J. Wouter Botzen, and Jeroen C. J. H. Aerts. 2019. Flood insurance arrangements in the European Union for future flood risk under climate and socioeconomic change. Global Environmental Change 58: 101966. [Google Scholar] [CrossRef]

- Kunreuther, Howard, Michel-Kerjan Erwann, and Tonn Gina. 2016. Insurance, Economic Incentives and other Policy Tools for Strengthening Critical Infrastructure Resilience: 20 Proposals for Action. Philadelphia: The Wharton School, University of Pennsylvania. [Google Scholar]

- Kurnianingtyas, Diva, Budi Santosa, and Nurhadi Siswanto. 2020. A System Dynamics for Financial Strategy Model Assessment in National Health Insurance System. Paper presented at the MSIE 2020, Osaka, Japan, 7–9 April. [Google Scholar]

- Latvian Environment, Geology and Meteorology Centre. 2019. Preliminary Flood Risk Assessment for 2019–2024; Riga: Latvian Environment, Geology and Meteorology Centre.

- Li, Qiang, and Wei Liu. 2023. Impact of government risk communication on residents’ decisions to adopt earthquake insurance: Evidence from a field survey in China. International Journal of Disaster Risk Reduction 91: 103695. [Google Scholar] [CrossRef]

- Robinson, Peter John, W. J. Wouter Botzen, Sem Duijndam, and Aimée Molenaar. 2021. Risk communication nudges and flood insurance demand. Climate Risk Management 34: 100366. [Google Scholar] [CrossRef]

- Roder, Giulia, Paul Hudson, and Paolo Tarolli. 2019. Flood risk perceptions and the willingness to pay for flood insurance in the Veneto region of Italy. International Journal of Disaster Risk Reduction 37: 101172. [Google Scholar] [CrossRef]

- Schanz, Kai-Uwe. 2021. Future Urban Risk Landscapes: An Insurance Perspective. Zürich: The Geneva Association. [Google Scholar]

- Sterman, John D. 1994. Learning in and about complex systems. System Dynamics Review 10: 291–330. [Google Scholar] [CrossRef]

- Vaijhala, Shalini, and James Rhodes. 2015. Leveraging Catastrophe Bonds As a Mechanism for Resilient Infrastructure Project Finance. Available online: www.refocuspartners.com (accessed on 30 June 2023).

- Vaijhala, Shalini, and James Rhodes. 2018. Resilience Bonds: A Business-Model for Resilient infrastructure. Field Actions Science Reports [Online], Special Issue 18|2018. Available online: http://journals.openedition.org/factsreports/4910 (accessed on 30 June 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Flooding Probability in 100 Years, % | Flooded Buildings Area, m2 | Restoration Costs per m2 |

|---|---|---|

| 10% | 103,773 | 19.5 |

| 1% | 547,400 | 25.8 |

| 0.5% | 695,111 | 31.8 |

| Scenario | Title | Risk Premium | DRR Measure | Flood Risk Reduction Measure Efficiency, % | Flood Risk Reduction Measure Cost, EUR |

|---|---|---|---|---|---|

| 1. | Business as usual | Assessed every 10 years | No | - | - |

| 2. | Investment in disaster risk reduction | Assessed every 10 years | Riverbed cleaning, coastal erosion prevention, and flow-through restoration | 20.5 | 1,200,000 |

| 3. | Smart contract approach | Fixed | Riverbed cleaning, coastal erosion prevention, and flow-through restoration | 20.5 | 1,200,000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Feofilovs, M.; Pagano, A.J.; Vannucci, E.; Spiotta, M.; Romagnoli, F. Climate Change-Related Disaster Risk Mitigation through Innovative Insurance Mechanism: A System Dynamics Model Application for a Case Study in Latvia. Risks 2024, 12, 43. https://doi.org/10.3390/risks12030043

Feofilovs M, Pagano AJ, Vannucci E, Spiotta M, Romagnoli F. Climate Change-Related Disaster Risk Mitigation through Innovative Insurance Mechanism: A System Dynamics Model Application for a Case Study in Latvia. Risks. 2024; 12(3):43. https://doi.org/10.3390/risks12030043

Chicago/Turabian StyleFeofilovs, Maksims, Andrea Jonathan Pagano, Emanuele Vannucci, Marina Spiotta, and Francesco Romagnoli. 2024. "Climate Change-Related Disaster Risk Mitigation through Innovative Insurance Mechanism: A System Dynamics Model Application for a Case Study in Latvia" Risks 12, no. 3: 43. https://doi.org/10.3390/risks12030043

APA StyleFeofilovs, M., Pagano, A. J., Vannucci, E., Spiotta, M., & Romagnoli, F. (2024). Climate Change-Related Disaster Risk Mitigation through Innovative Insurance Mechanism: A System Dynamics Model Application for a Case Study in Latvia. Risks, 12(3), 43. https://doi.org/10.3390/risks12030043